Finance Assignment: Shareholder Wealth, Risk, and Returns Analysis

VerifiedAdded on 2020/02/24

|15

|1193

|123

Homework Assignment

AI Summary

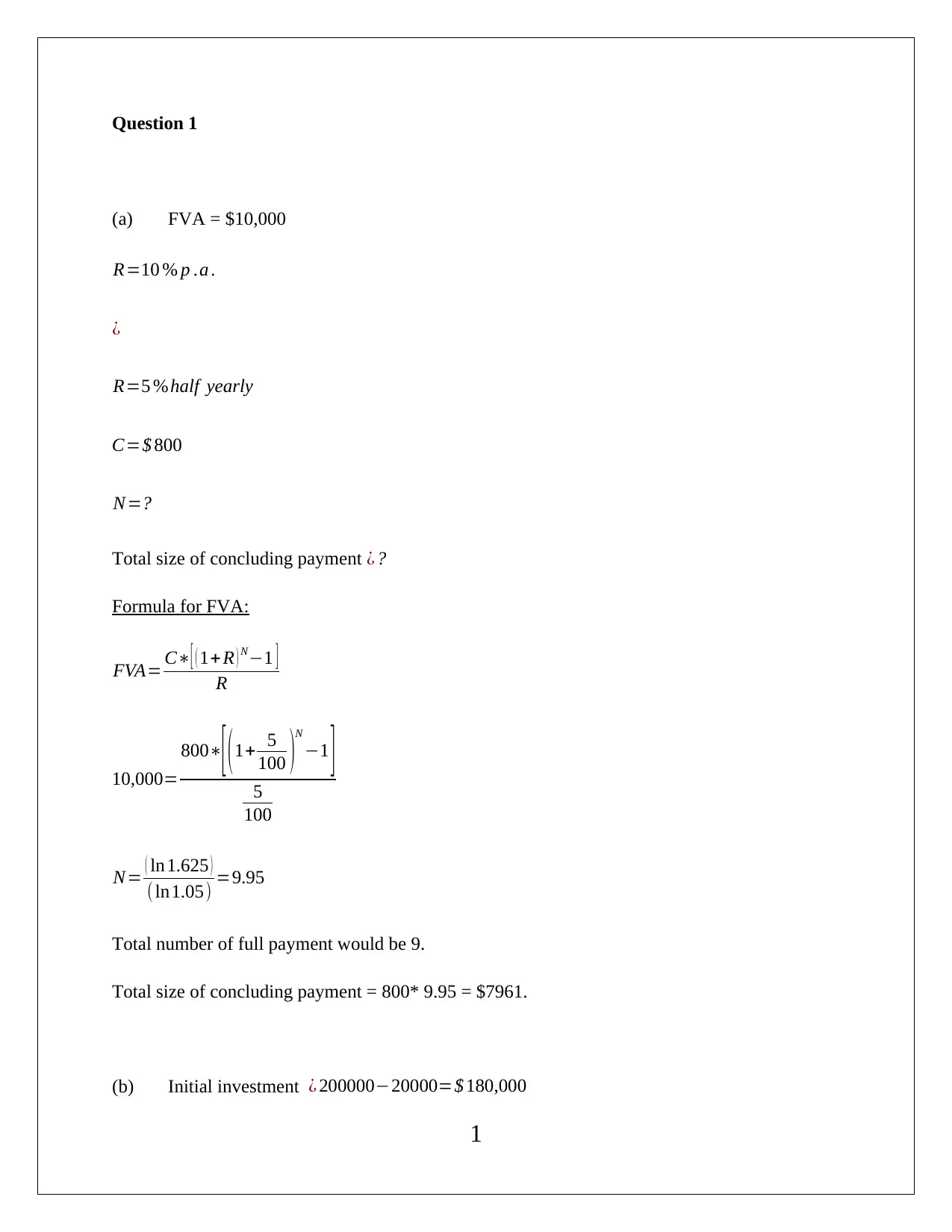

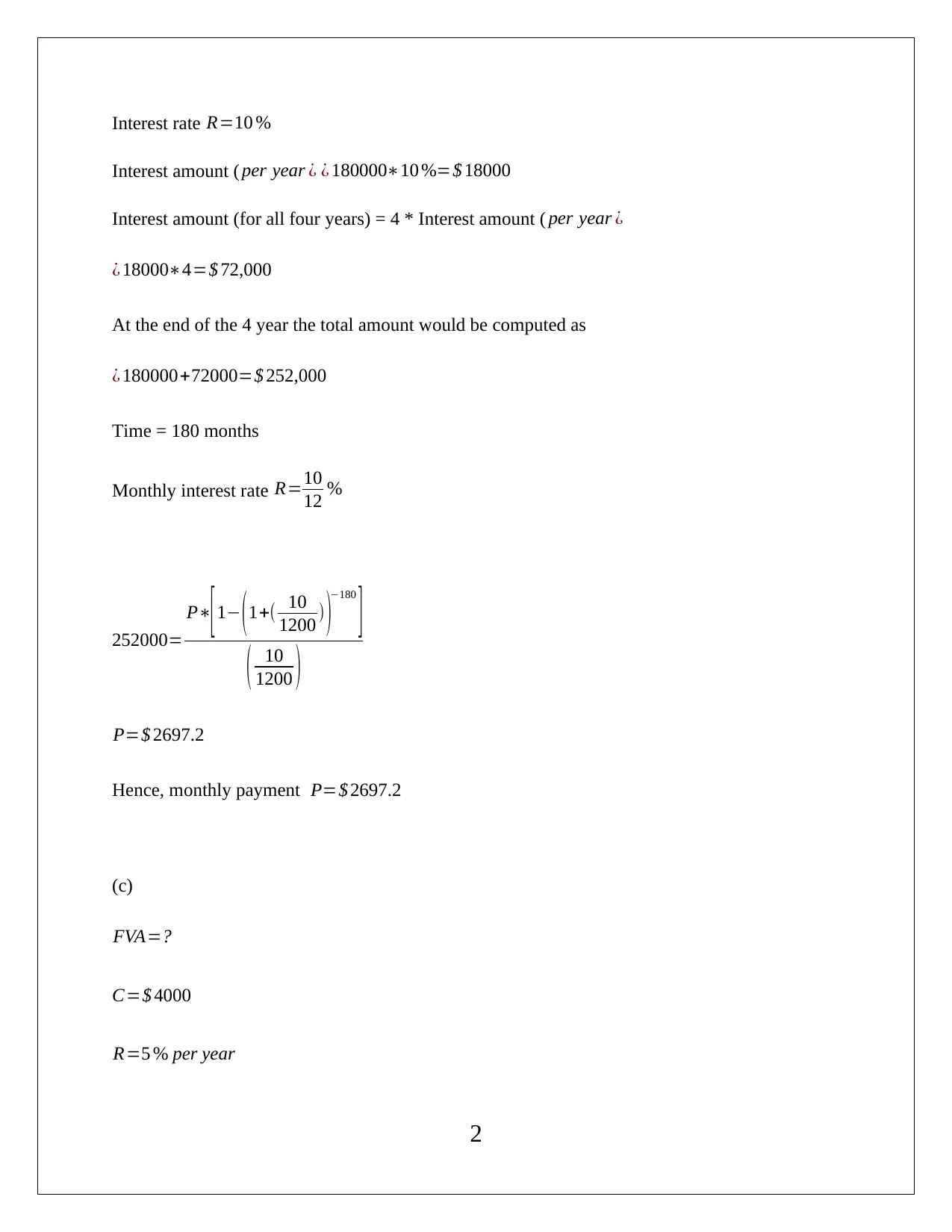

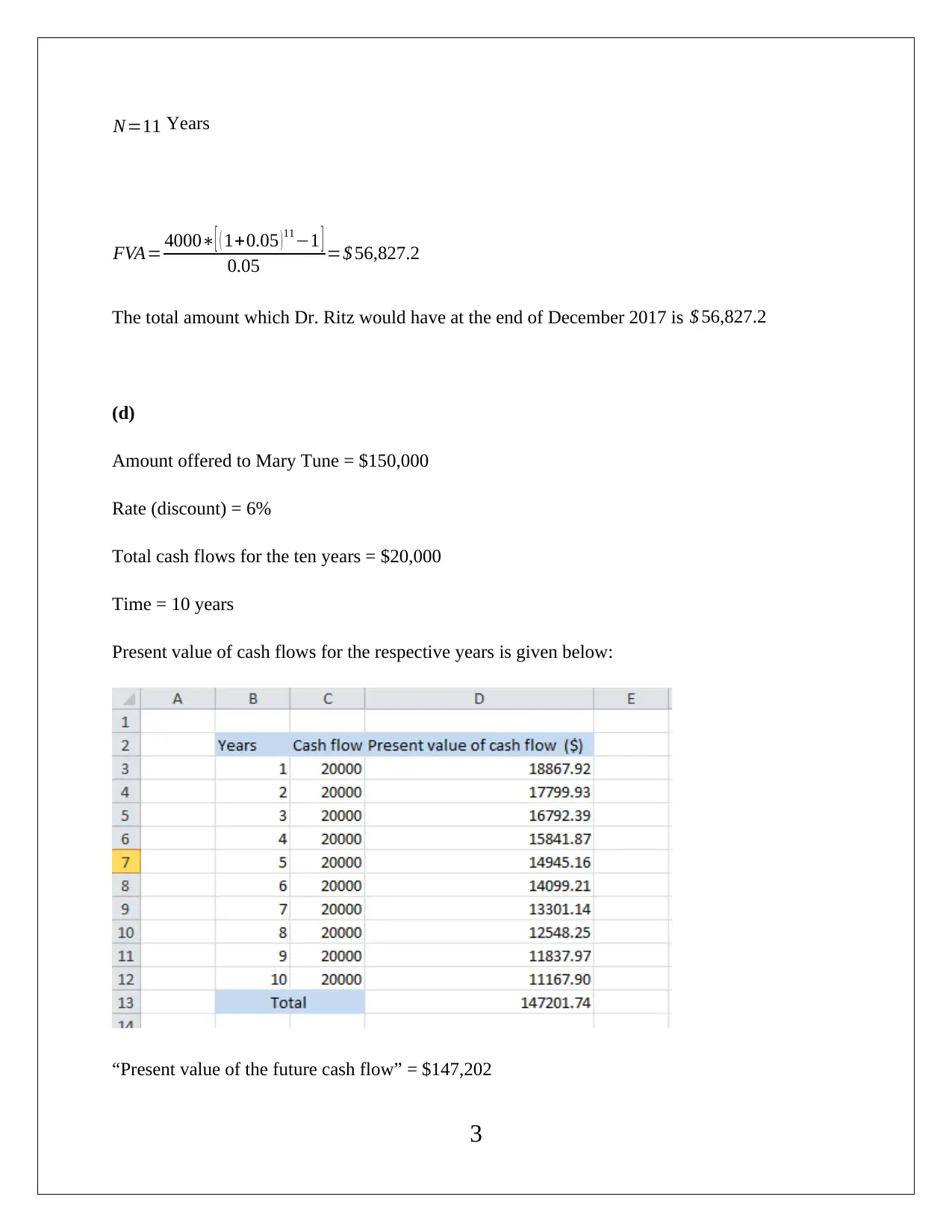

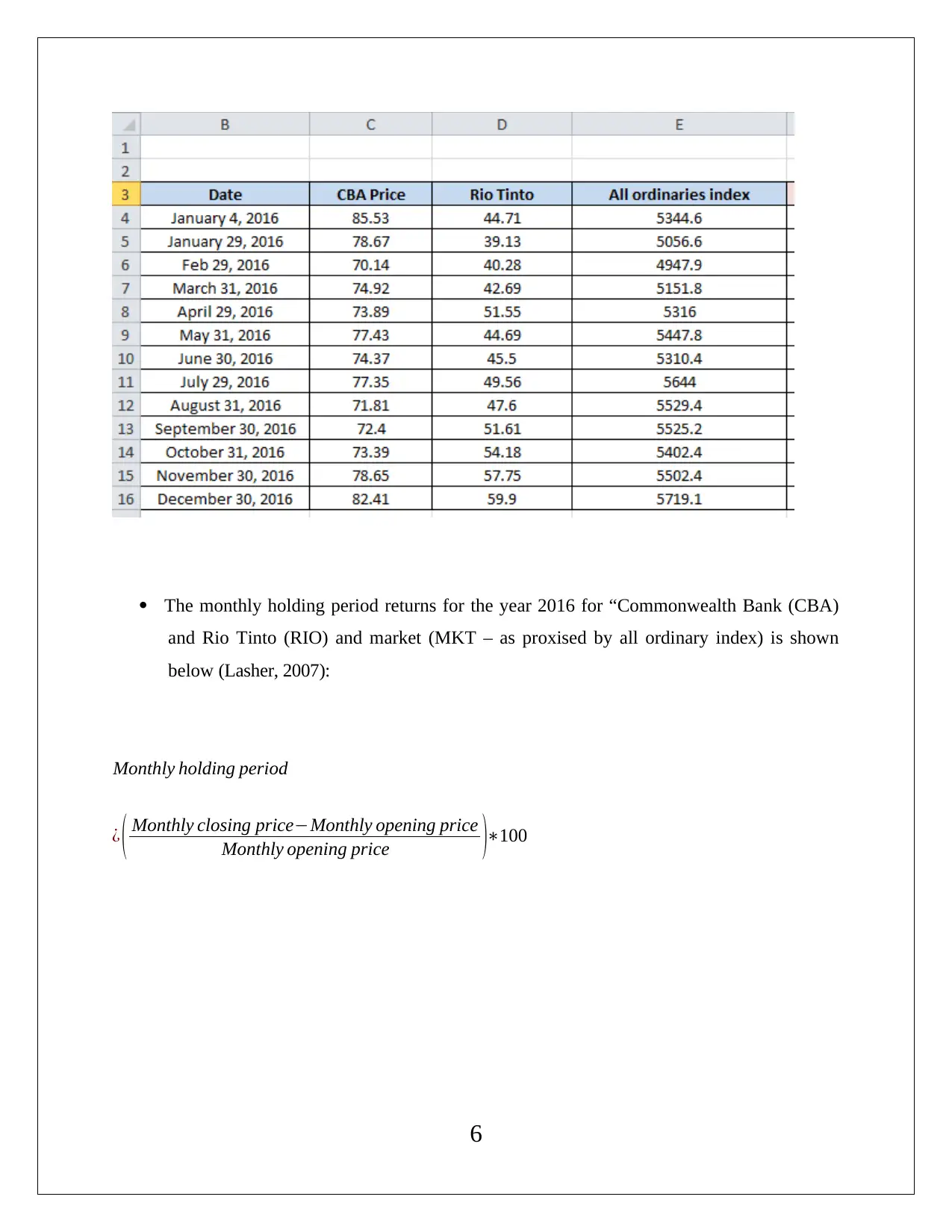

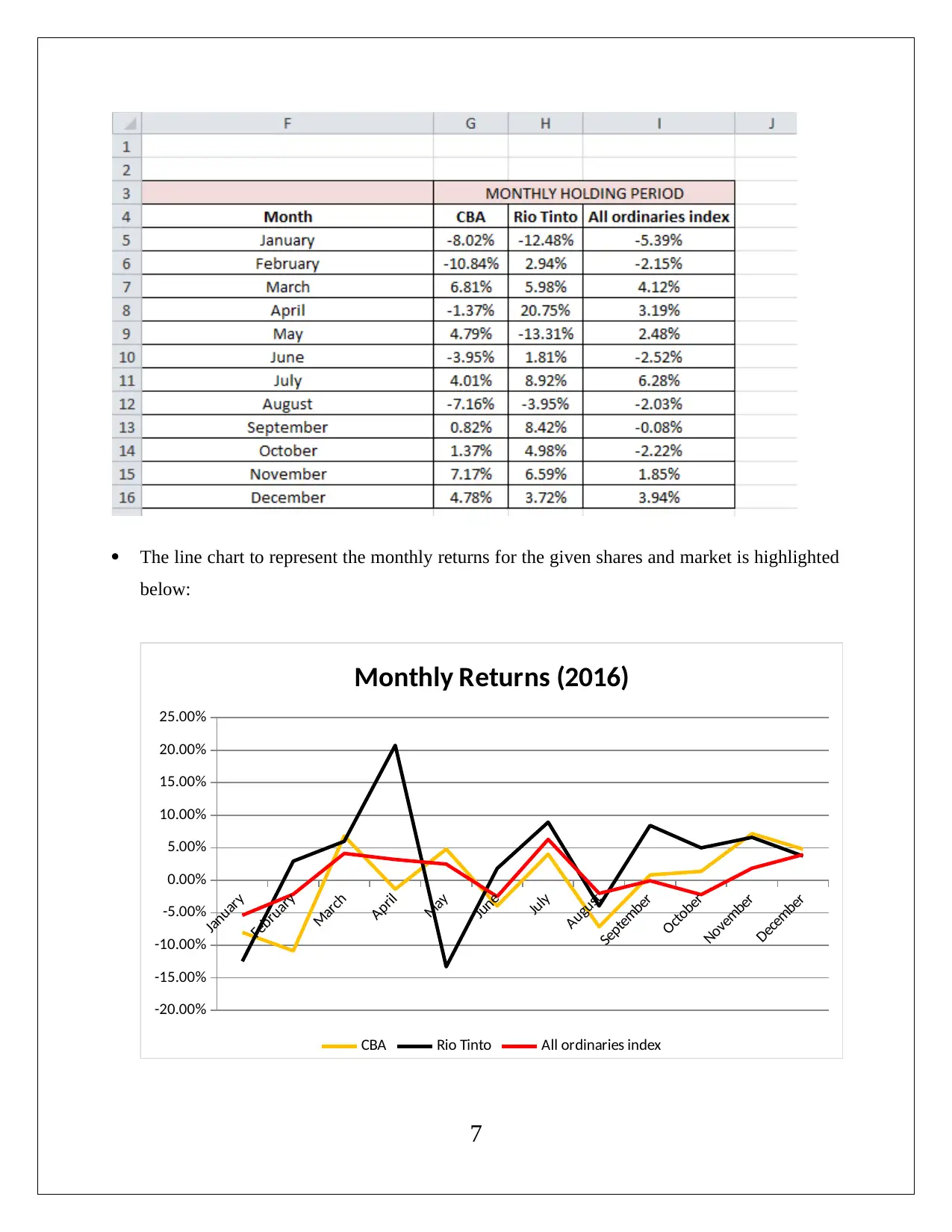

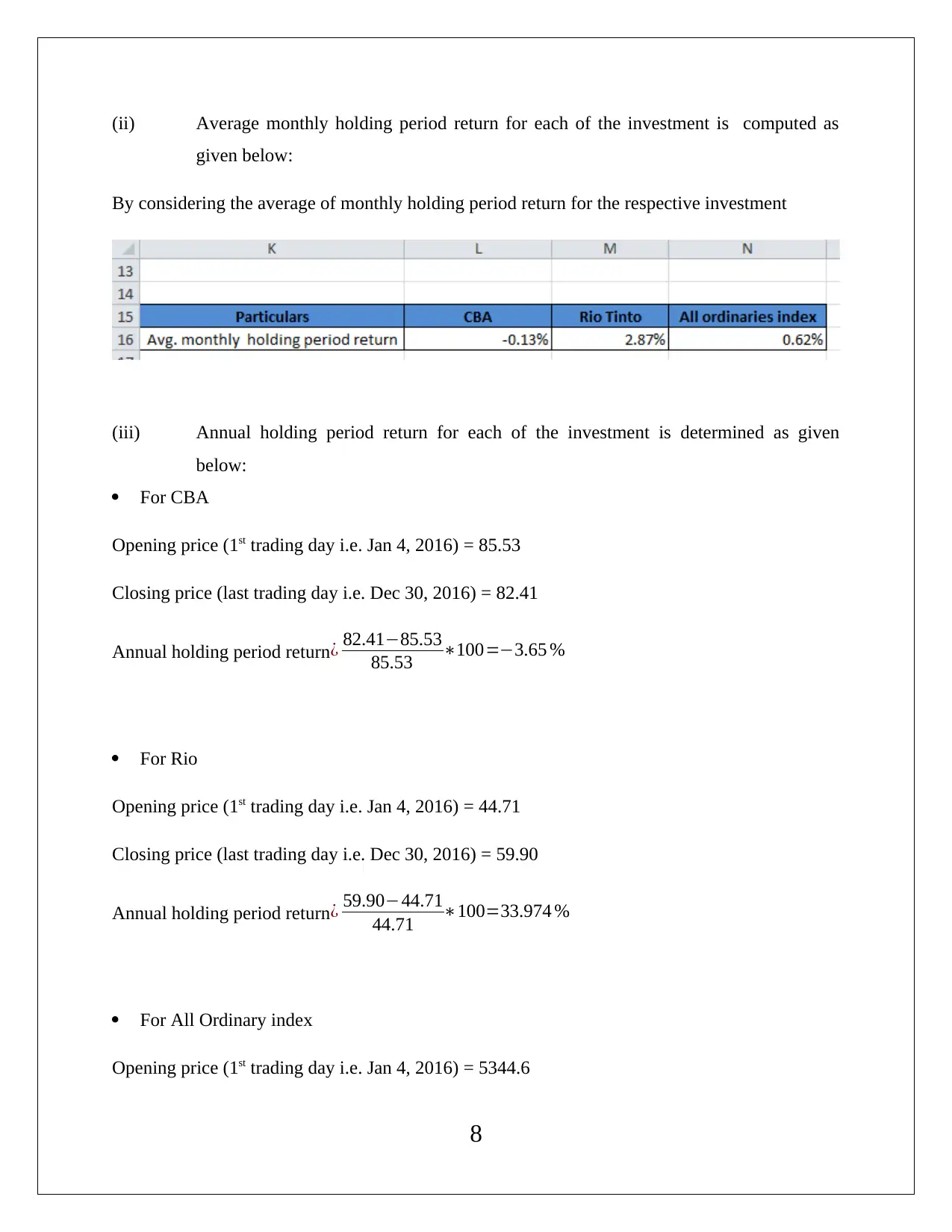

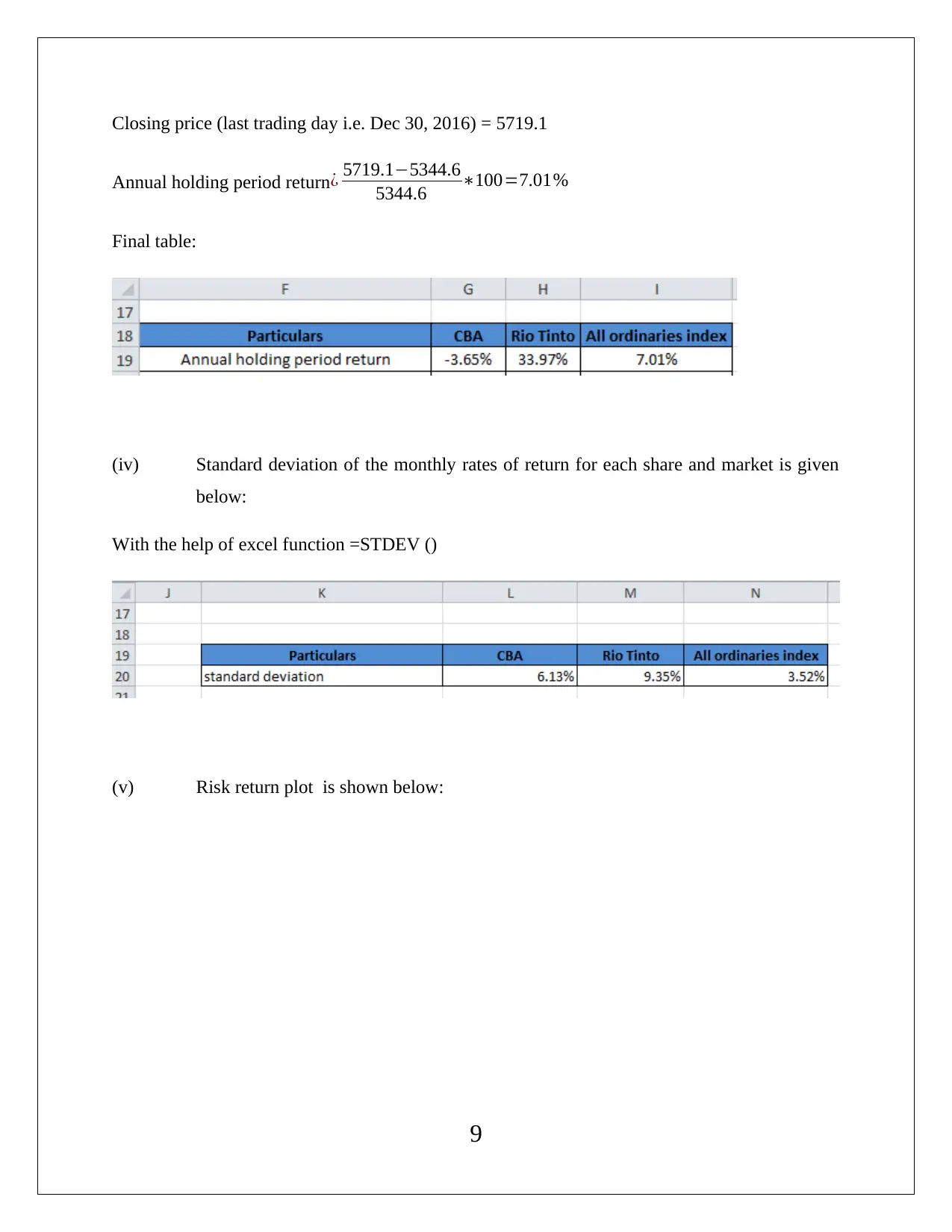

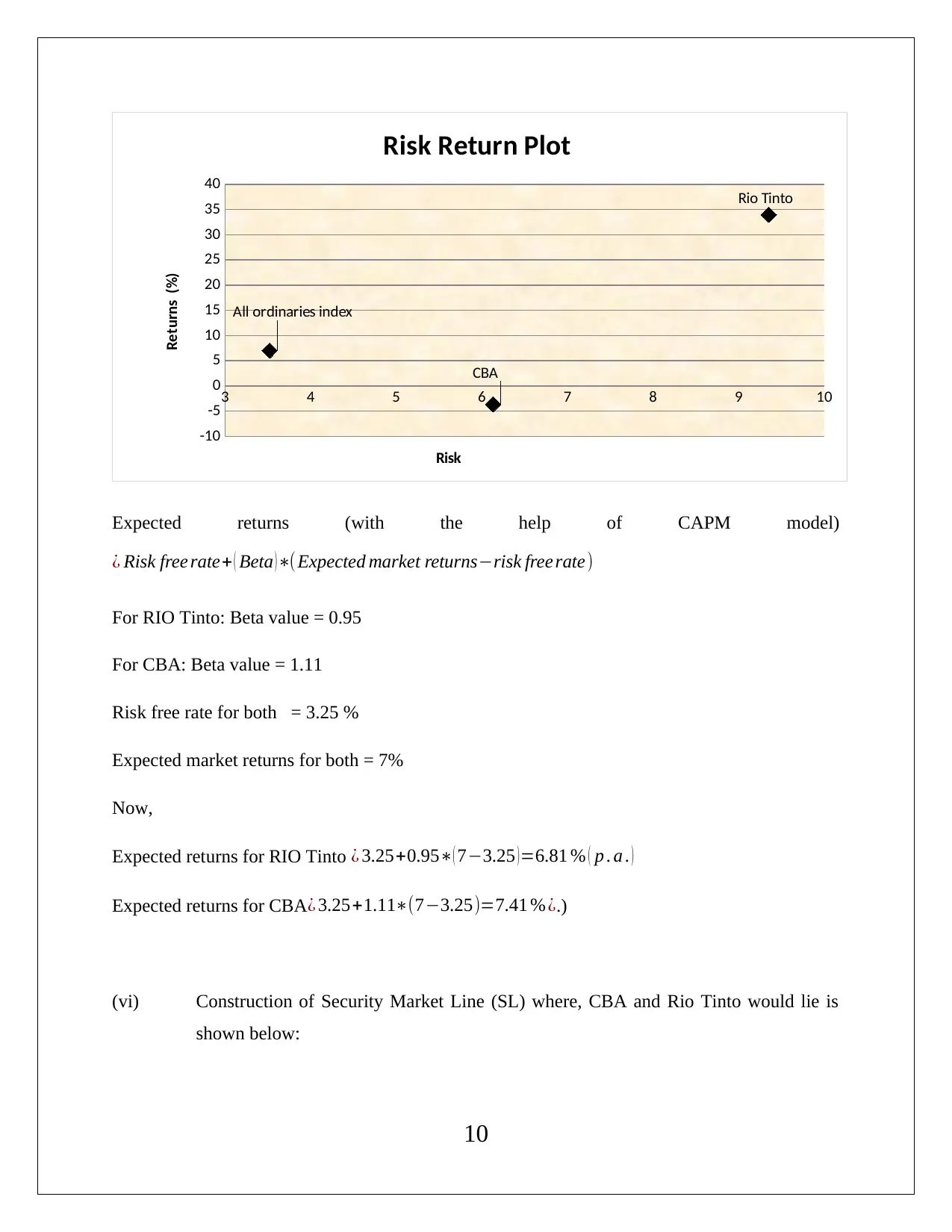

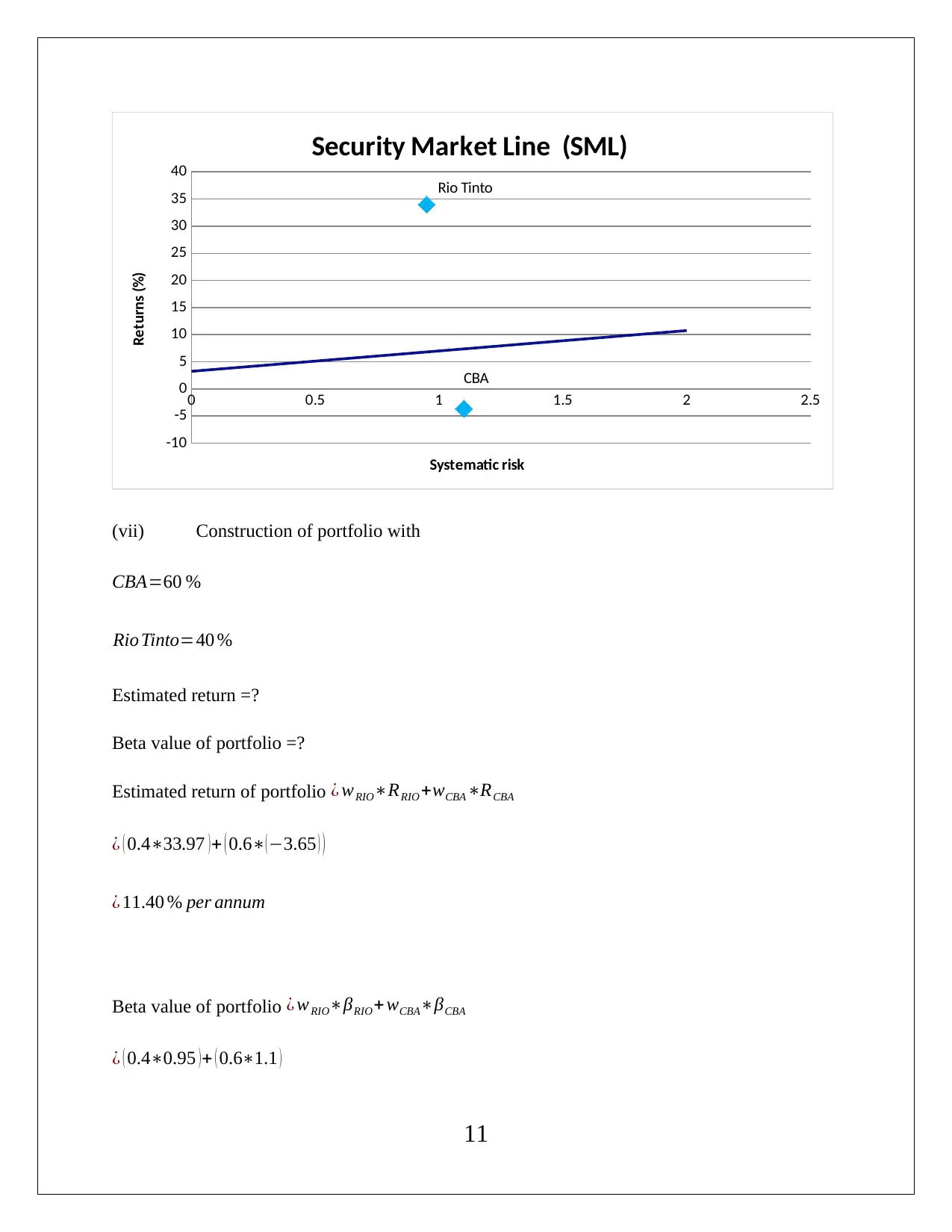

This finance assignment solution addresses key concepts in financial management, including shareholder wealth maximization, risk and return analysis, and investment strategies. The solution begins with calculations related to future value of annuity and present value of cash flows. It then explores the differences between profit maximization and shareholder wealth maximization, emphasizing the long-term perspective and the importance of considering risk. The solution also includes an analysis of market data for Commonwealth Bank (CBA) and Rio Tinto (RIO), utilizing the CAPM model and Security Market Line (SML) to evaluate their performance and make investment recommendations. The analysis involves calculating holding period returns, standard deviations, and expected returns, providing a comprehensive assessment of the investment opportunities. The document concludes with a comparison of CBA and Rio Tinto, suggesting an investment in Rio Tinto based on the analysis.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.