Accounting & Finance Assignment Solution - University Name, Semester 1

VerifiedAdded on 2020/03/02

|9

|1563

|93

Homework Assignment

AI Summary

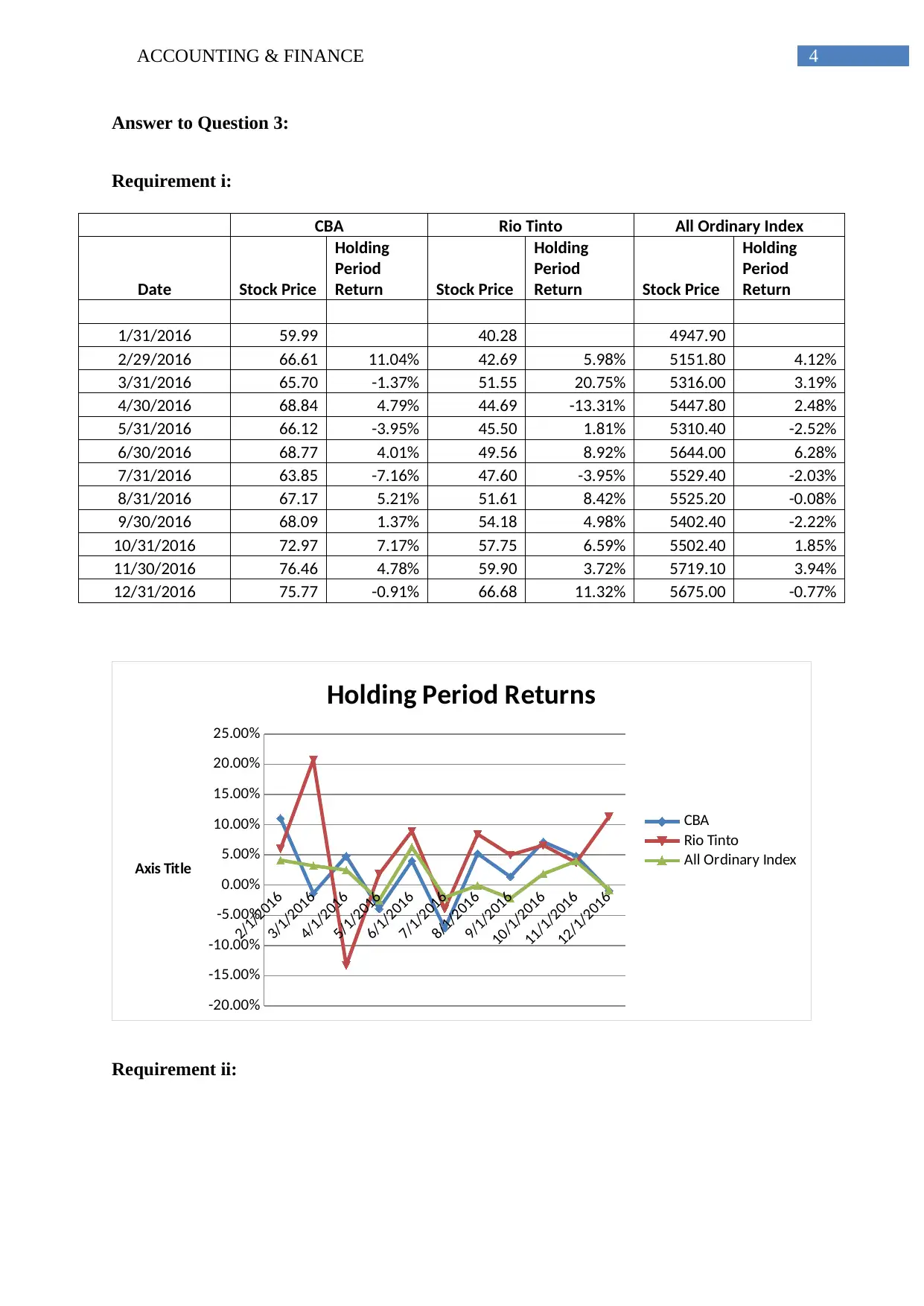

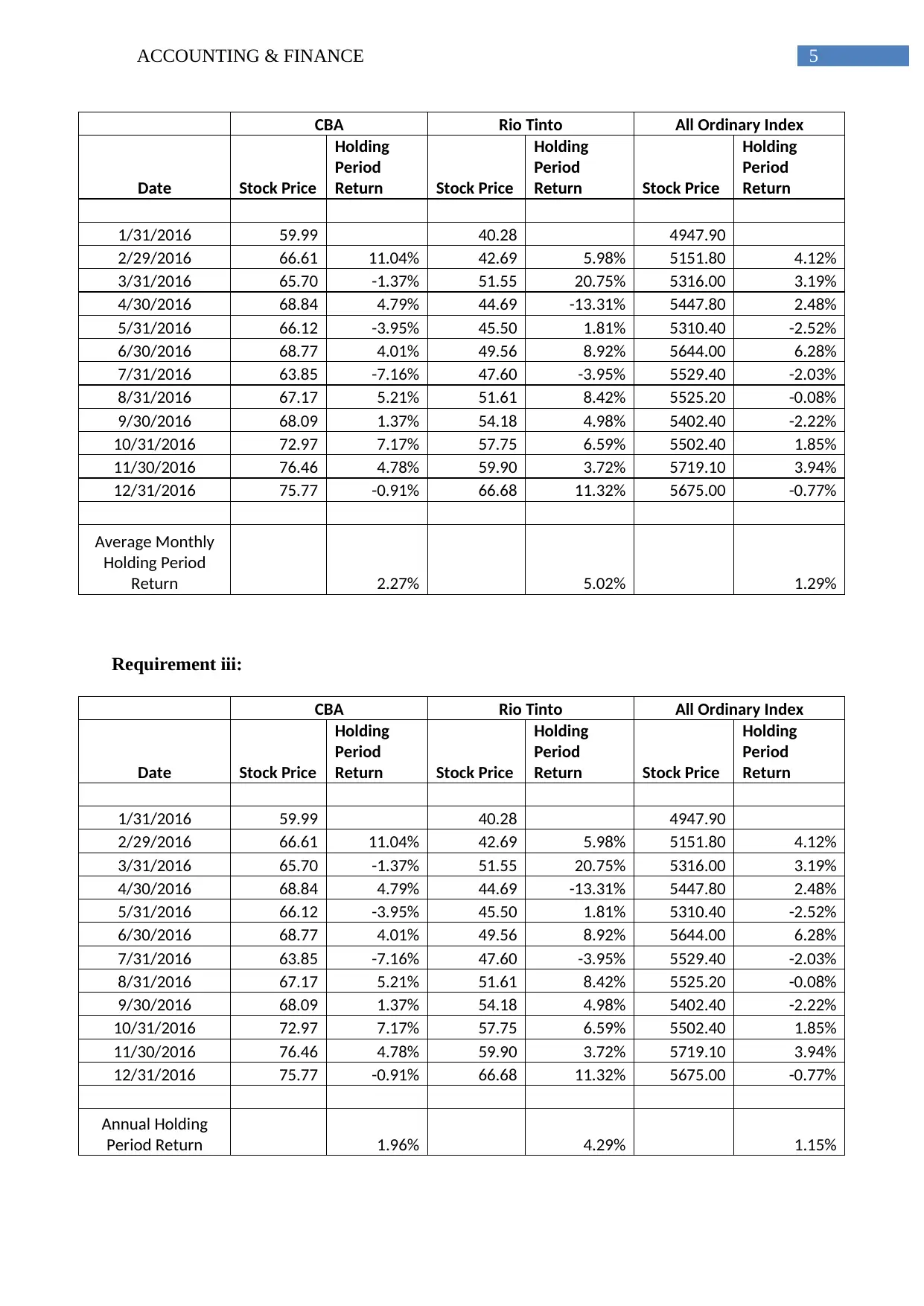

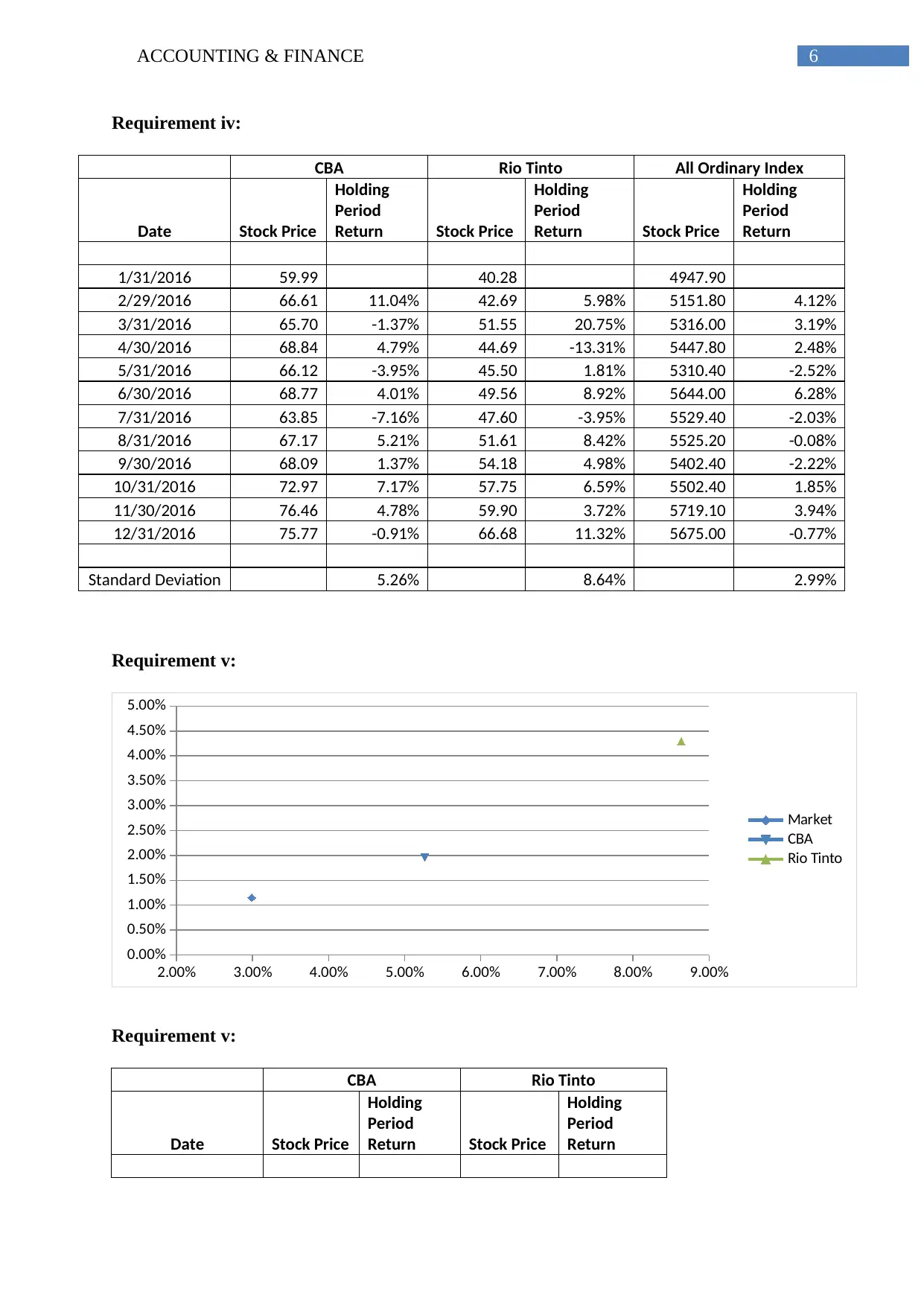

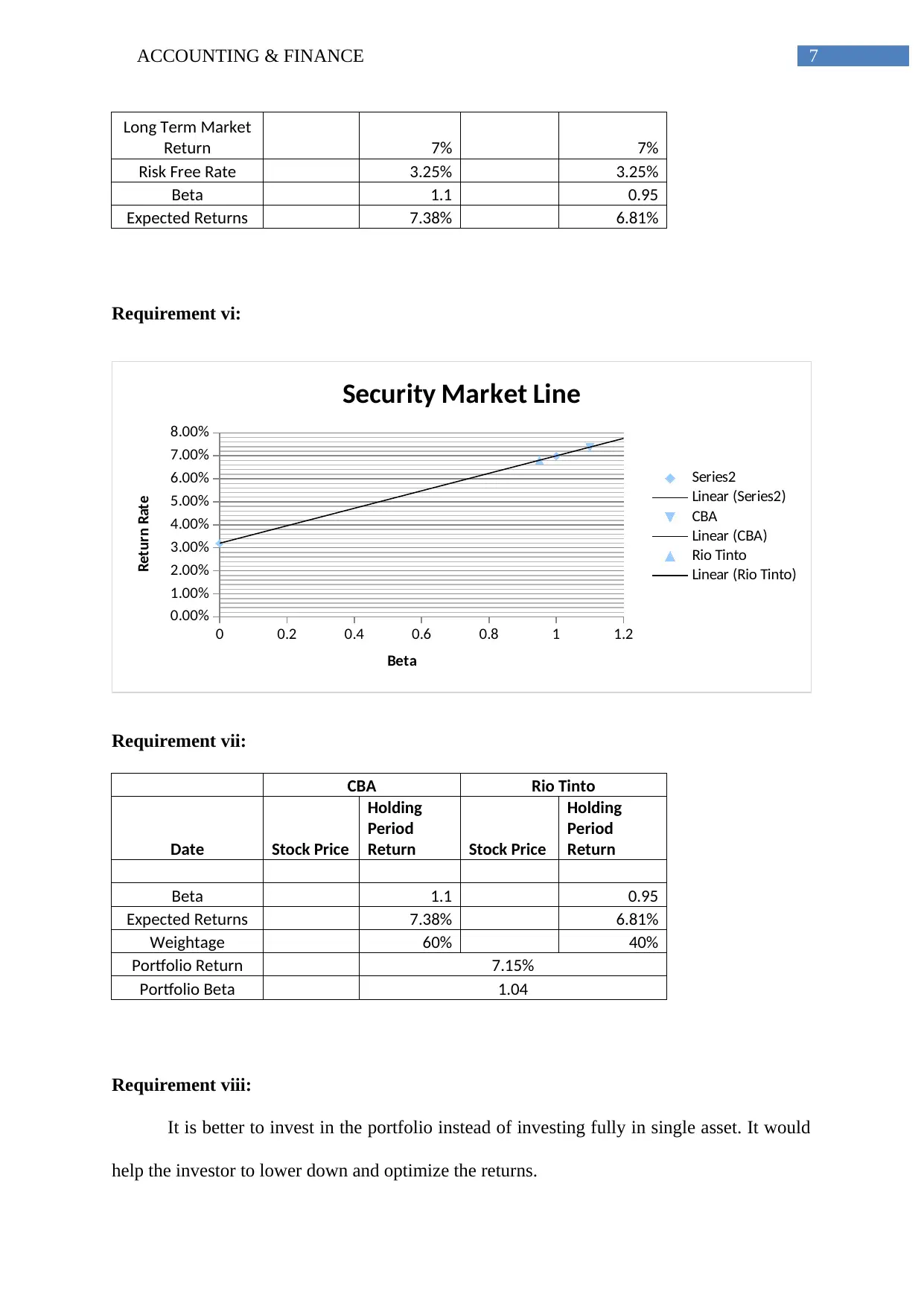

This assignment solution for an Accounting & Finance course delves into key financial concepts. It begins by contrasting the objectives of profit maximization and shareholder wealth maximization, emphasizing the long-term value creation inherent in the latter. The solution then explores the behavior of risk-averse investors and their investment choices, highlighting the trade-offs between risk and return. The core of the assignment involves a detailed analysis of stock performance data for CBA, Rio Tinto, and an All Ordinary Index. The solution includes calculations of holding period returns, average monthly and annual returns, and standard deviations. Furthermore, it applies the Capital Asset Pricing Model (CAPM) to estimate expected returns, and culminates in a portfolio analysis, determining portfolio returns and beta. The assignment concludes with a recommendation to diversify investments through a portfolio approach.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.