Accounting and Finance Assignment: Journal Entries and Impairment

VerifiedAdded on 2022/08/30

|14

|1110

|25

Homework Assignment

AI Summary

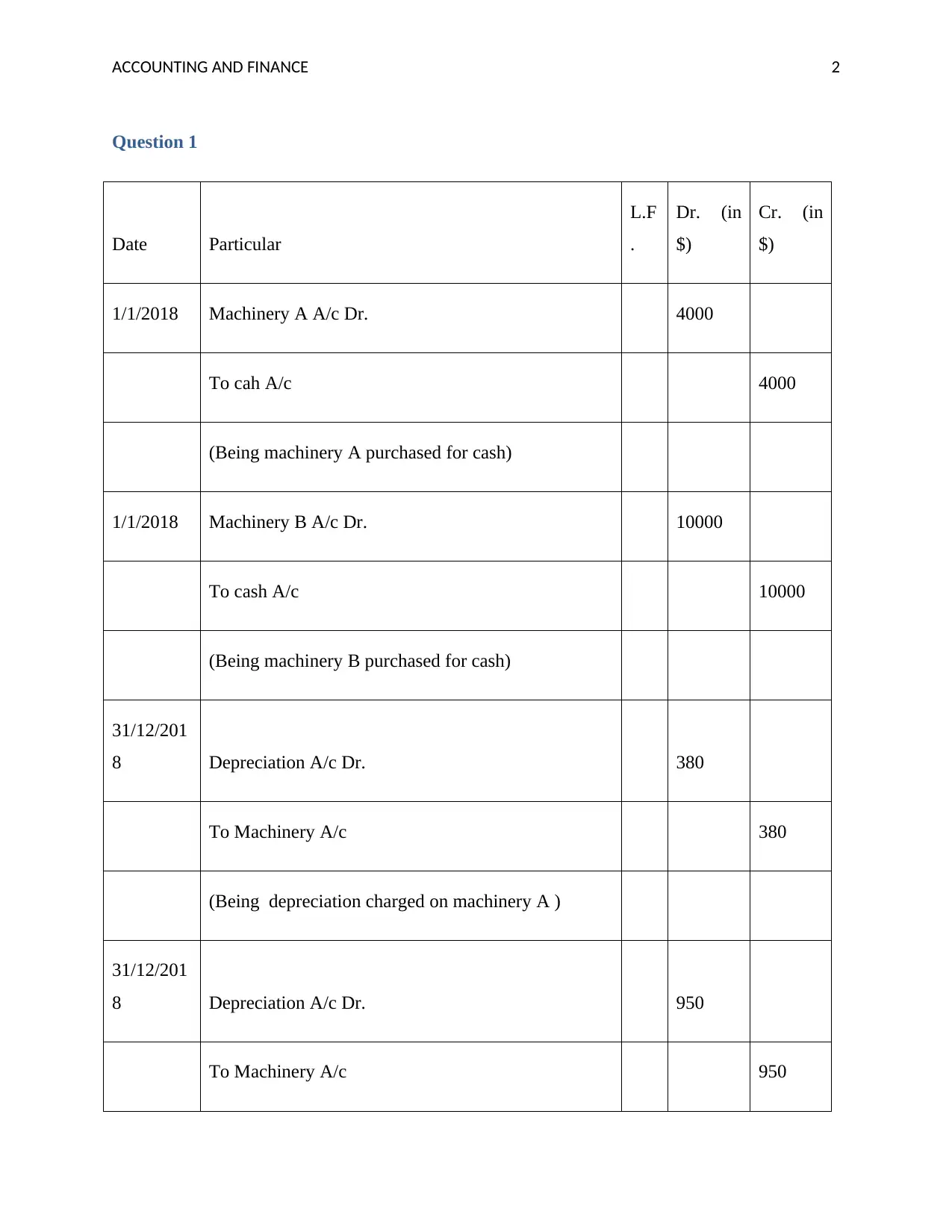

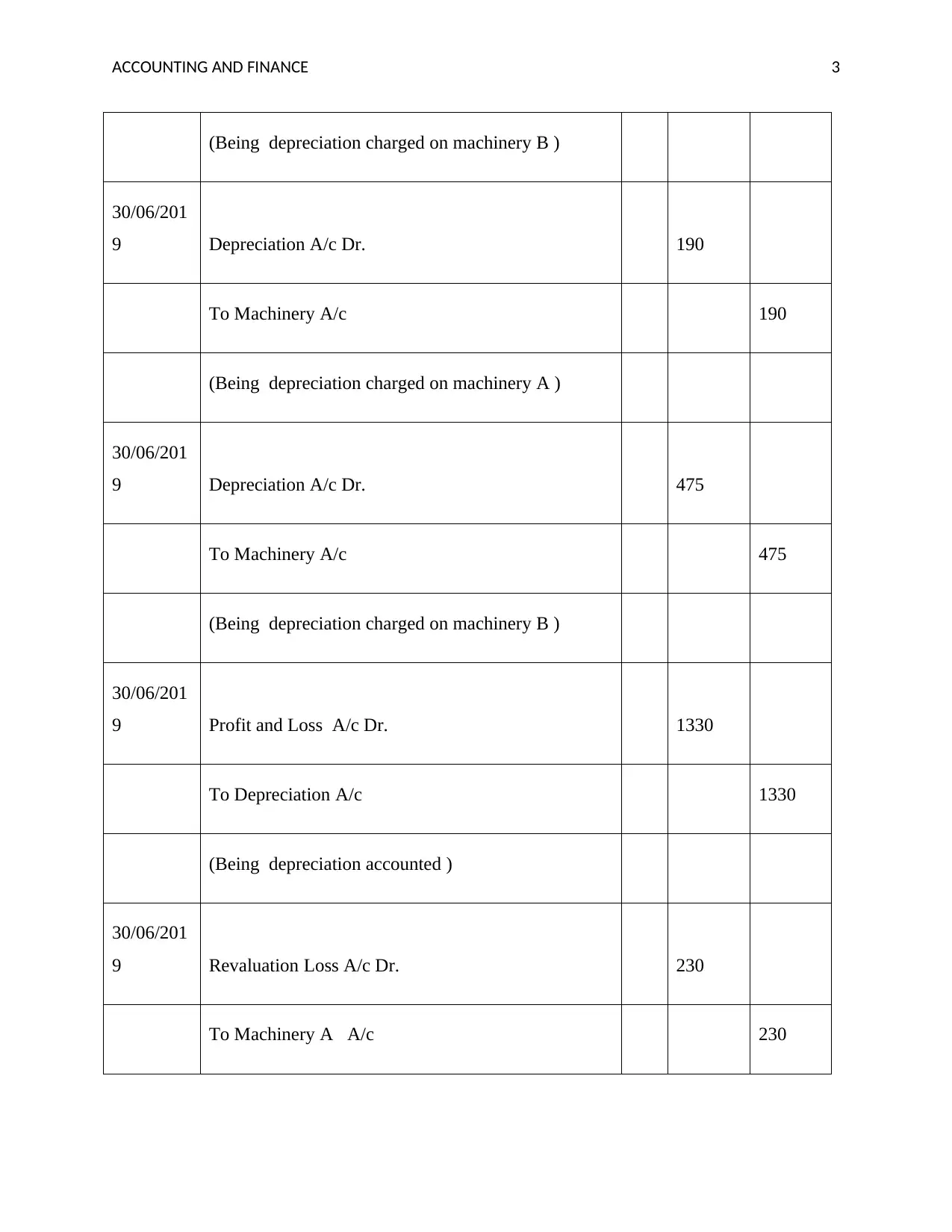

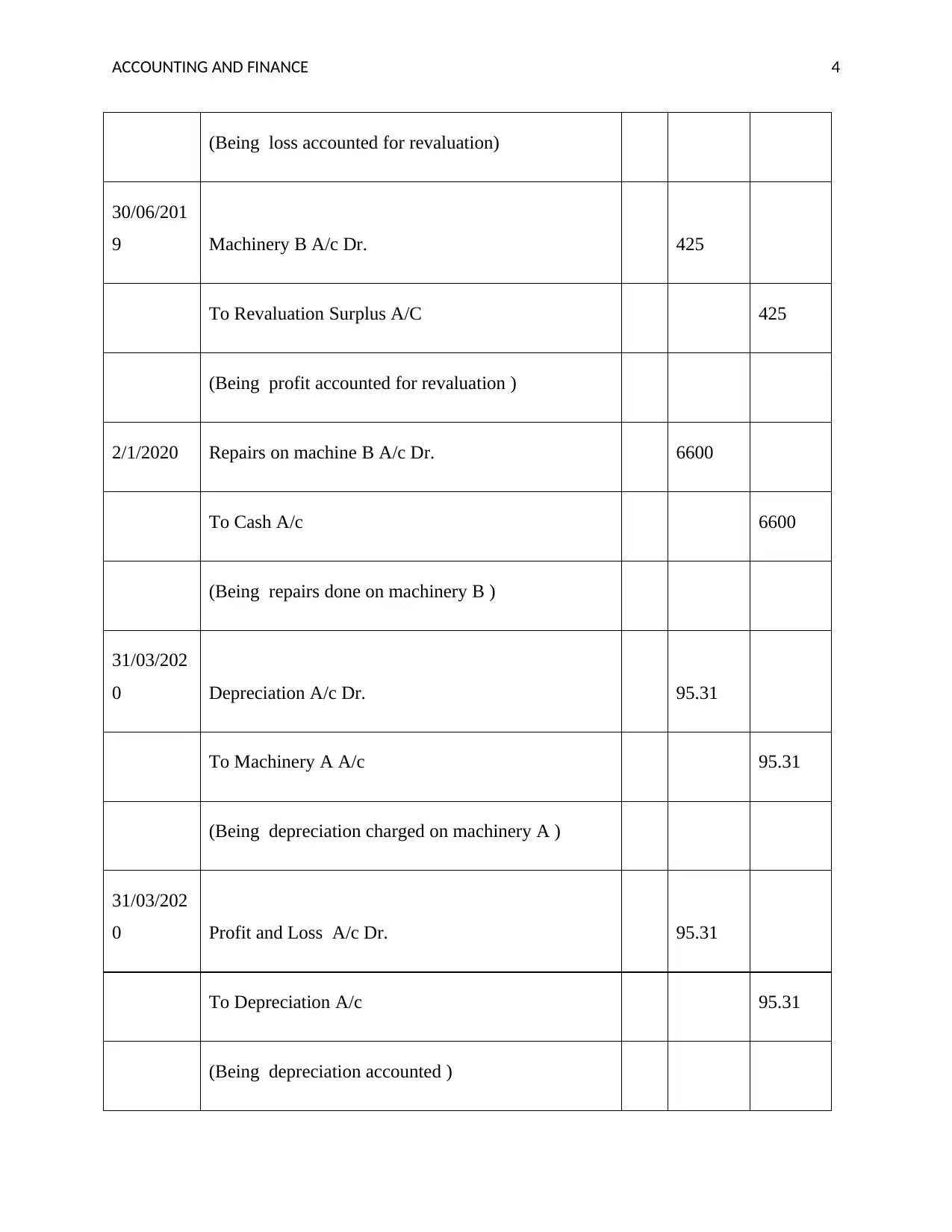

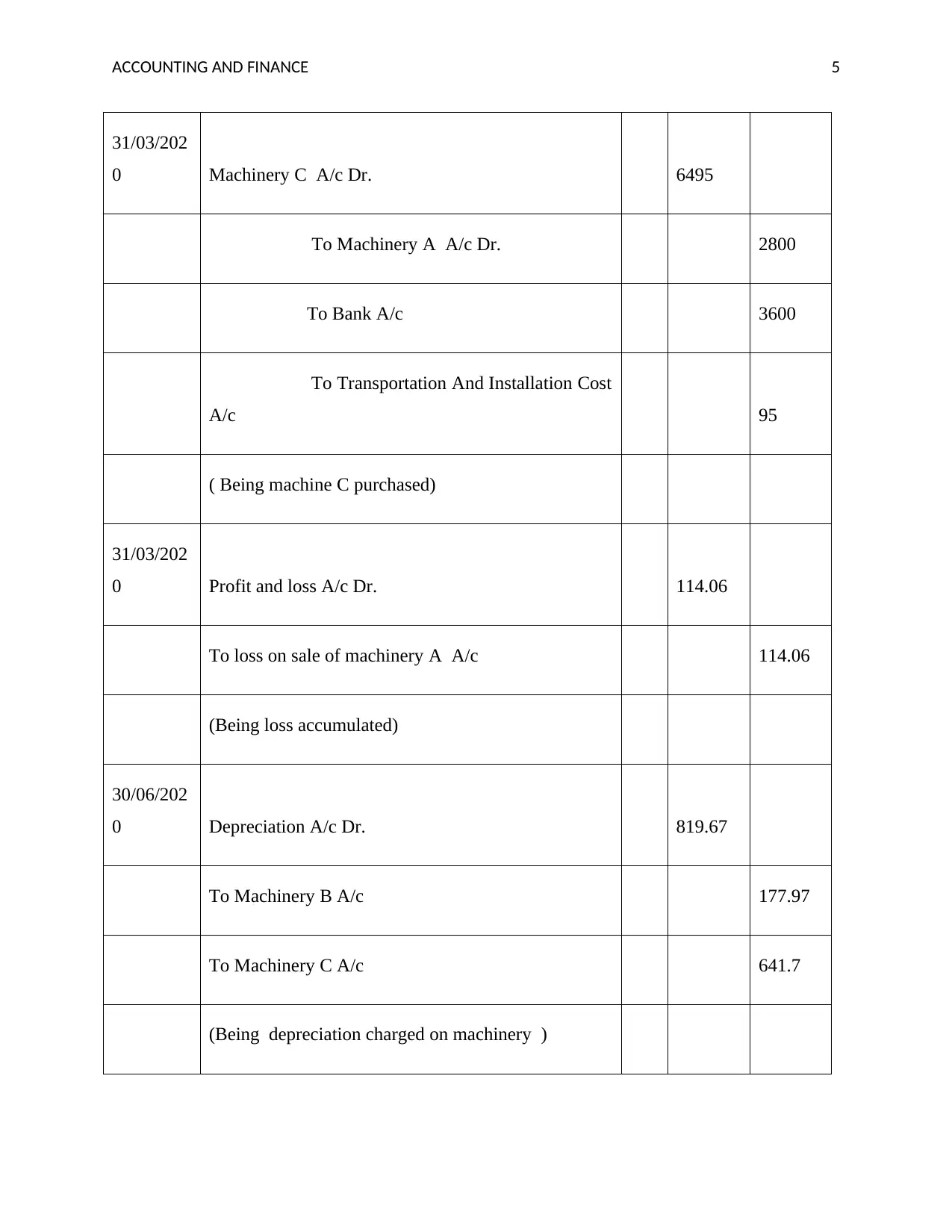

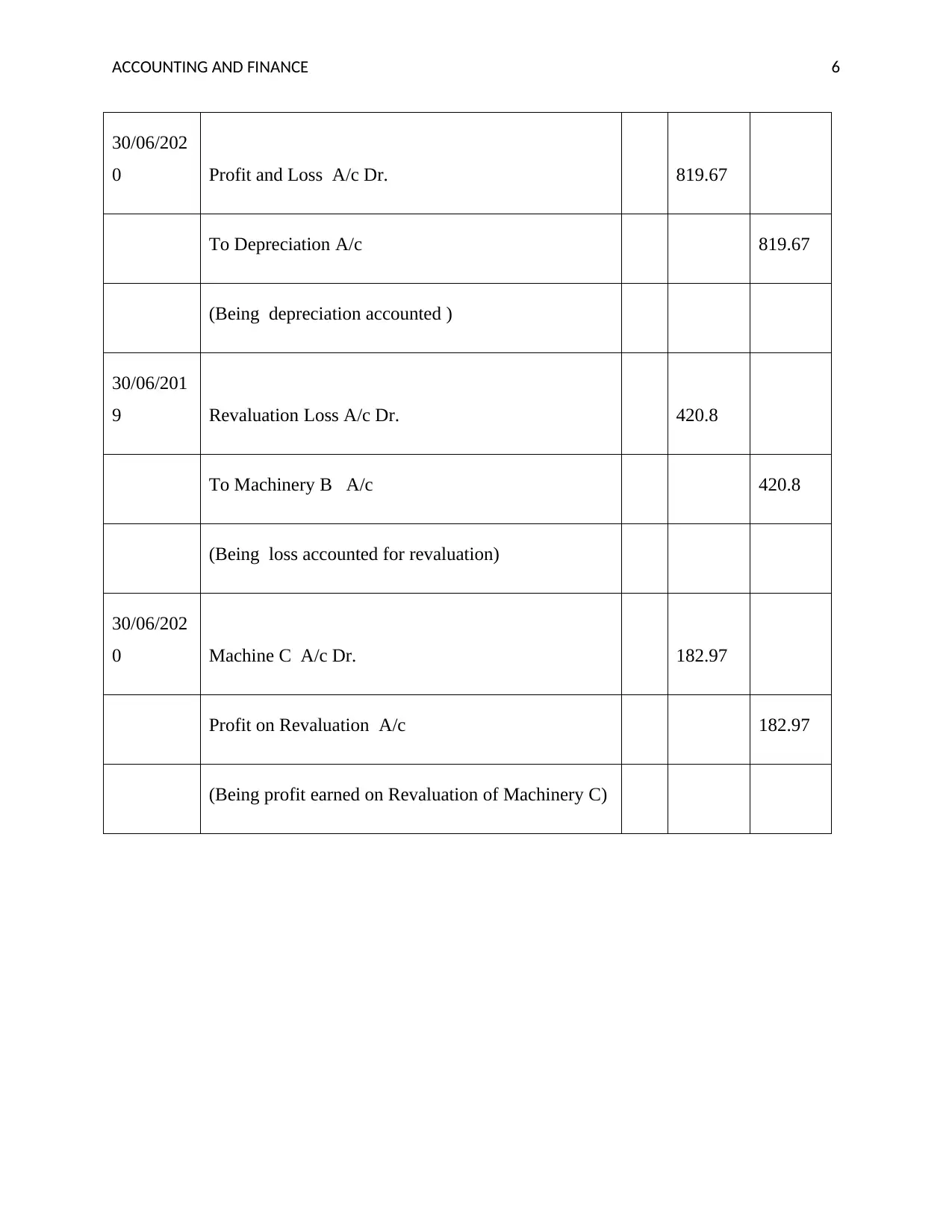

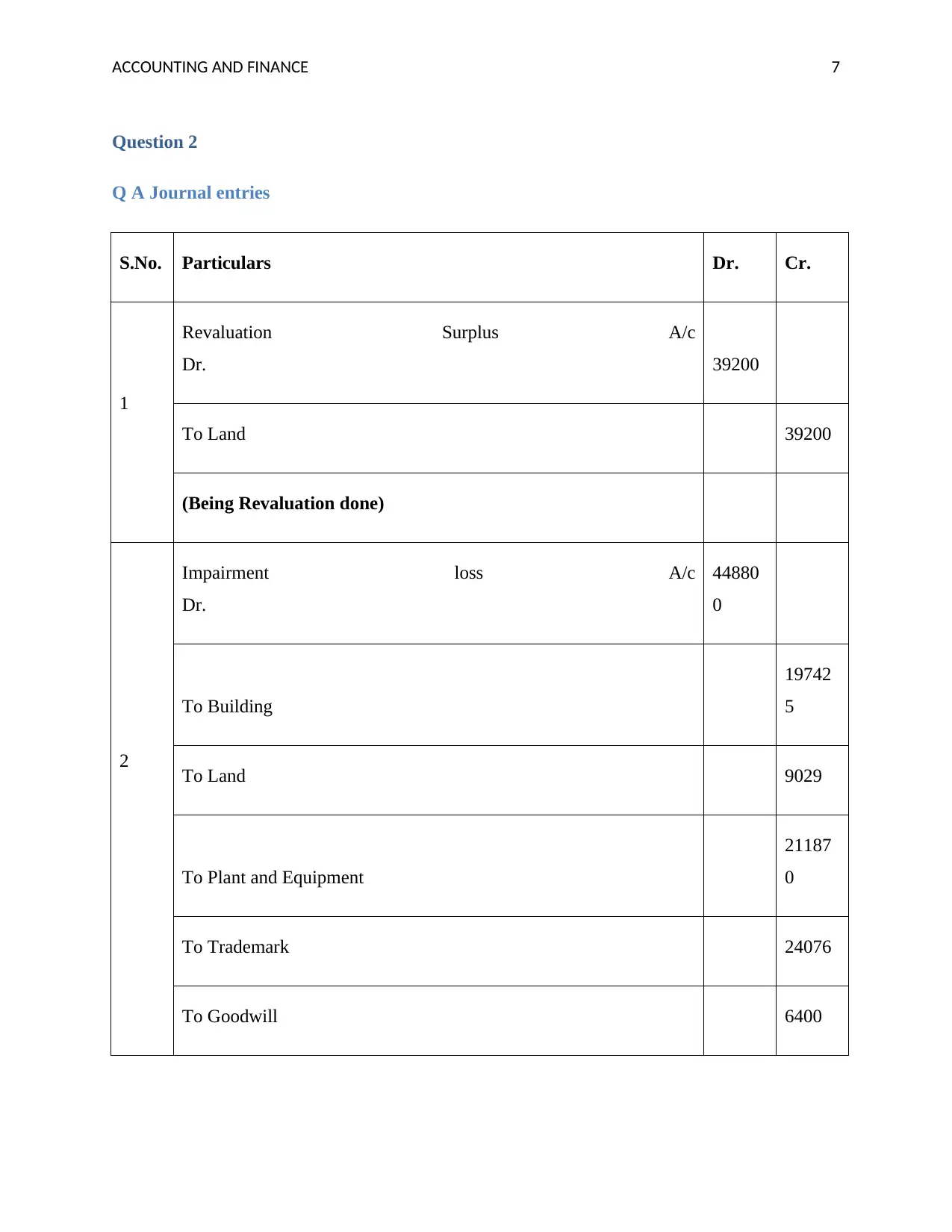

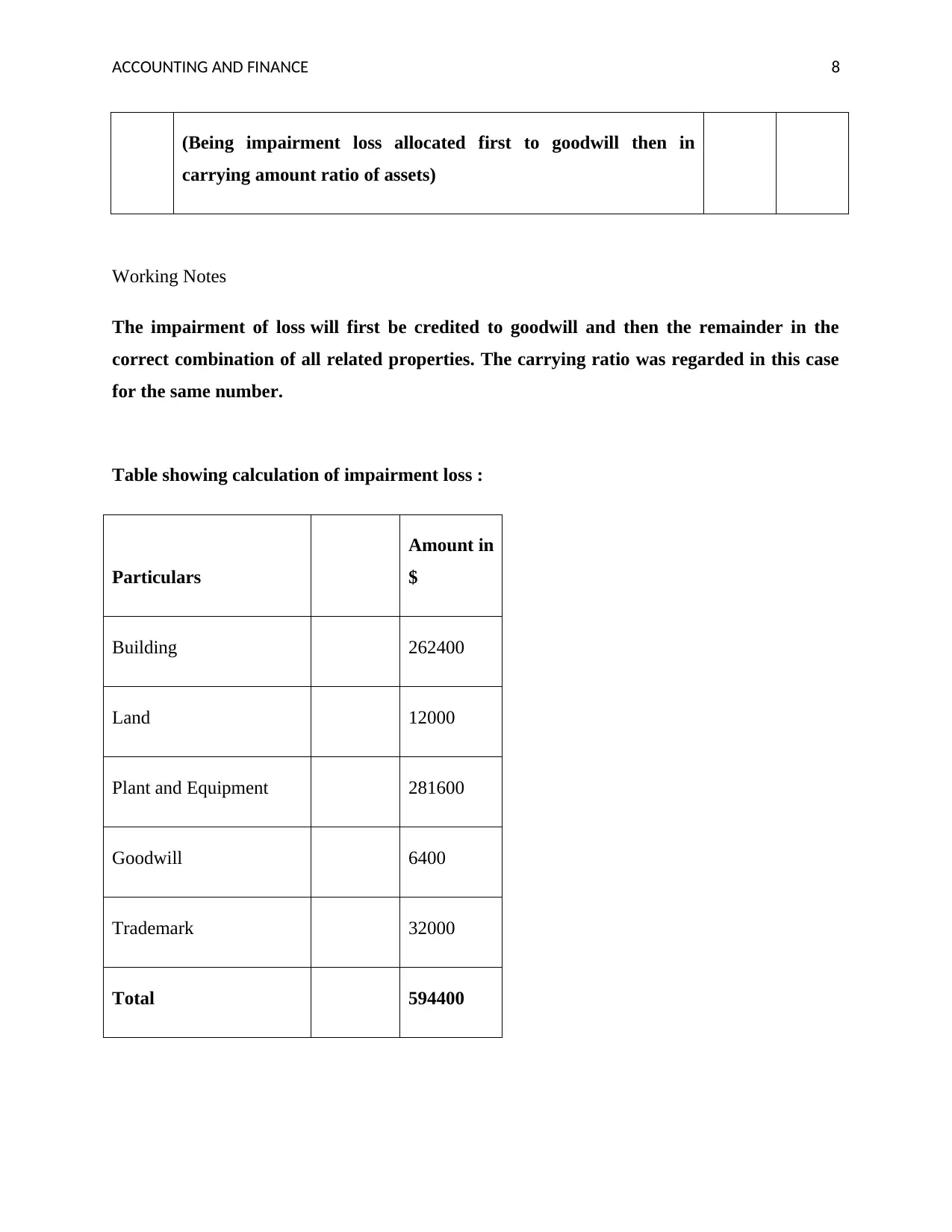

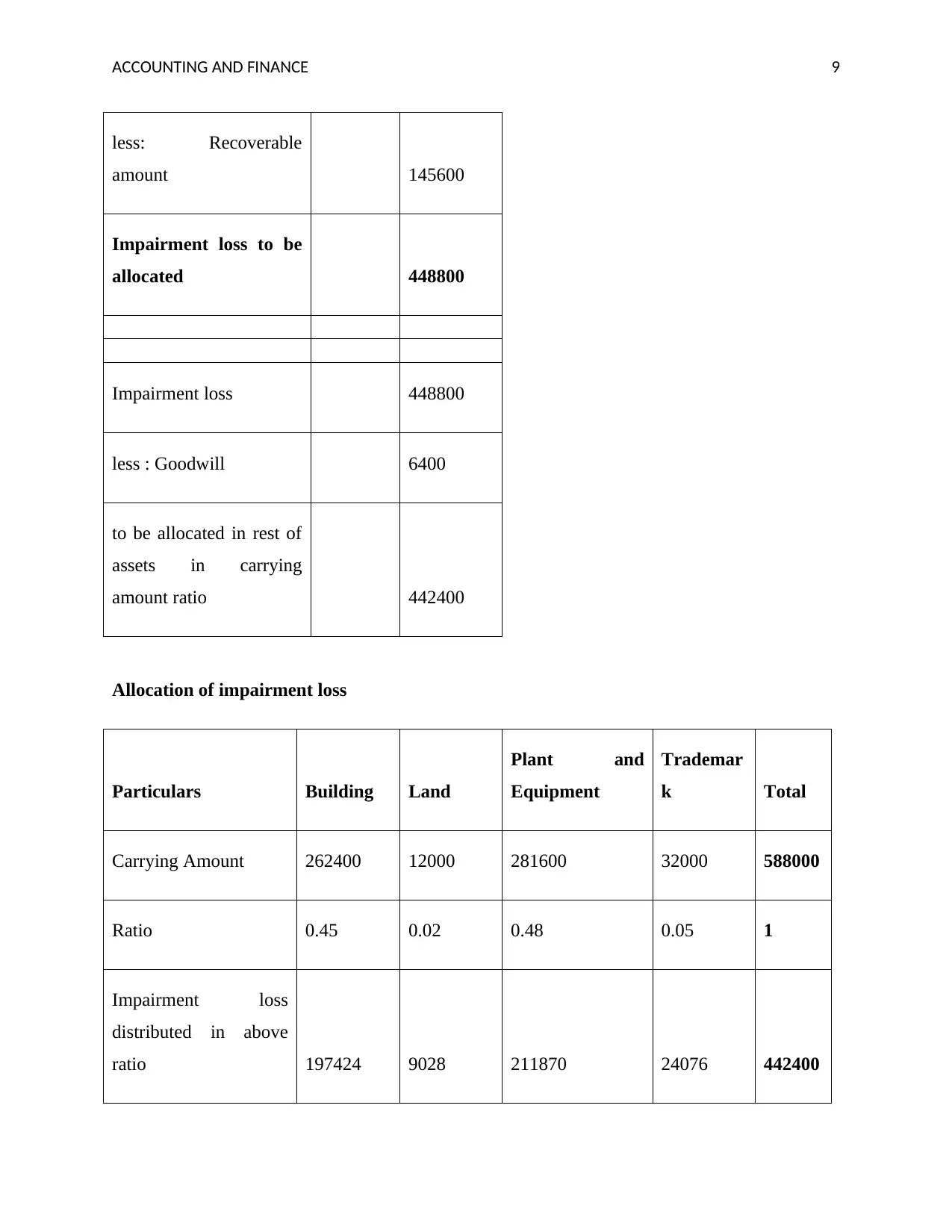

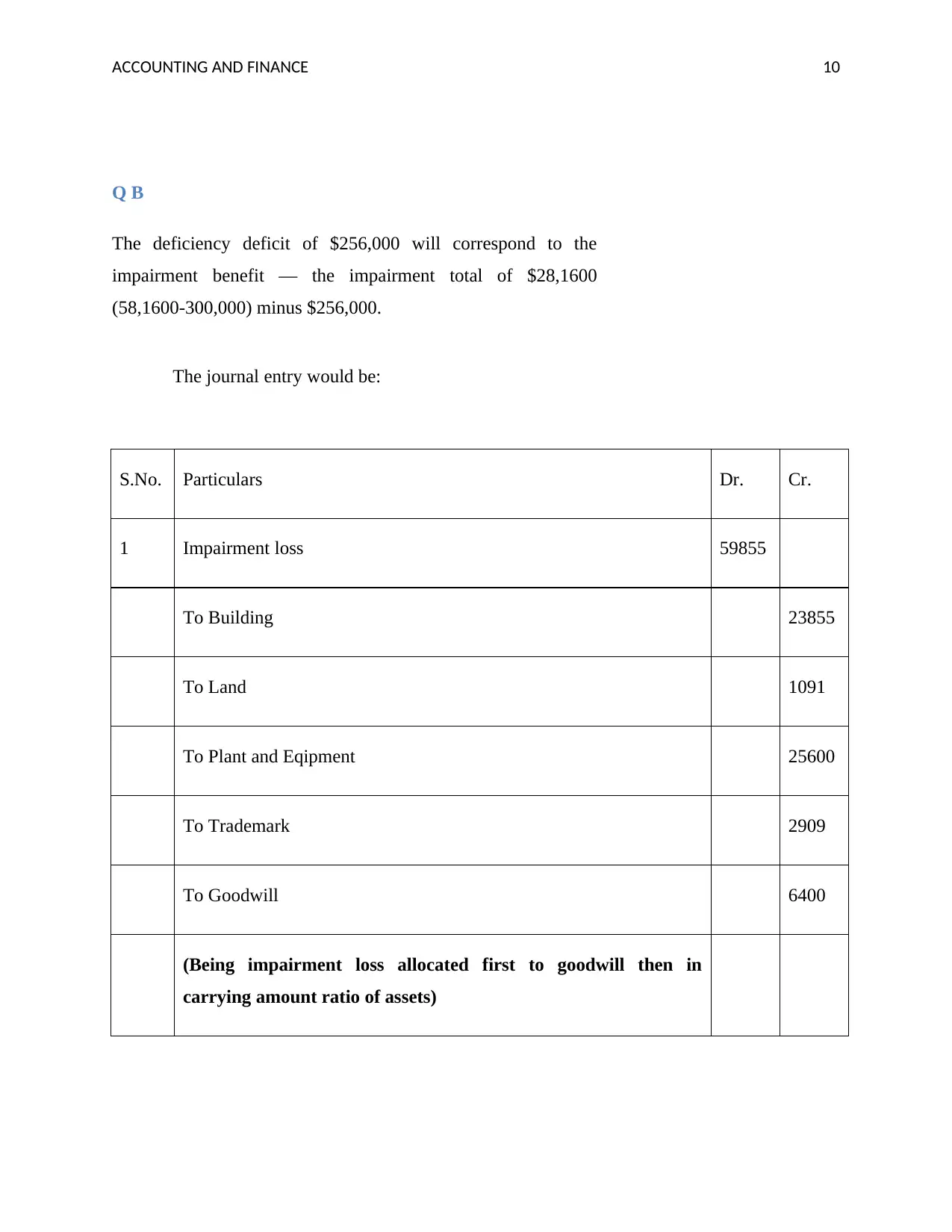

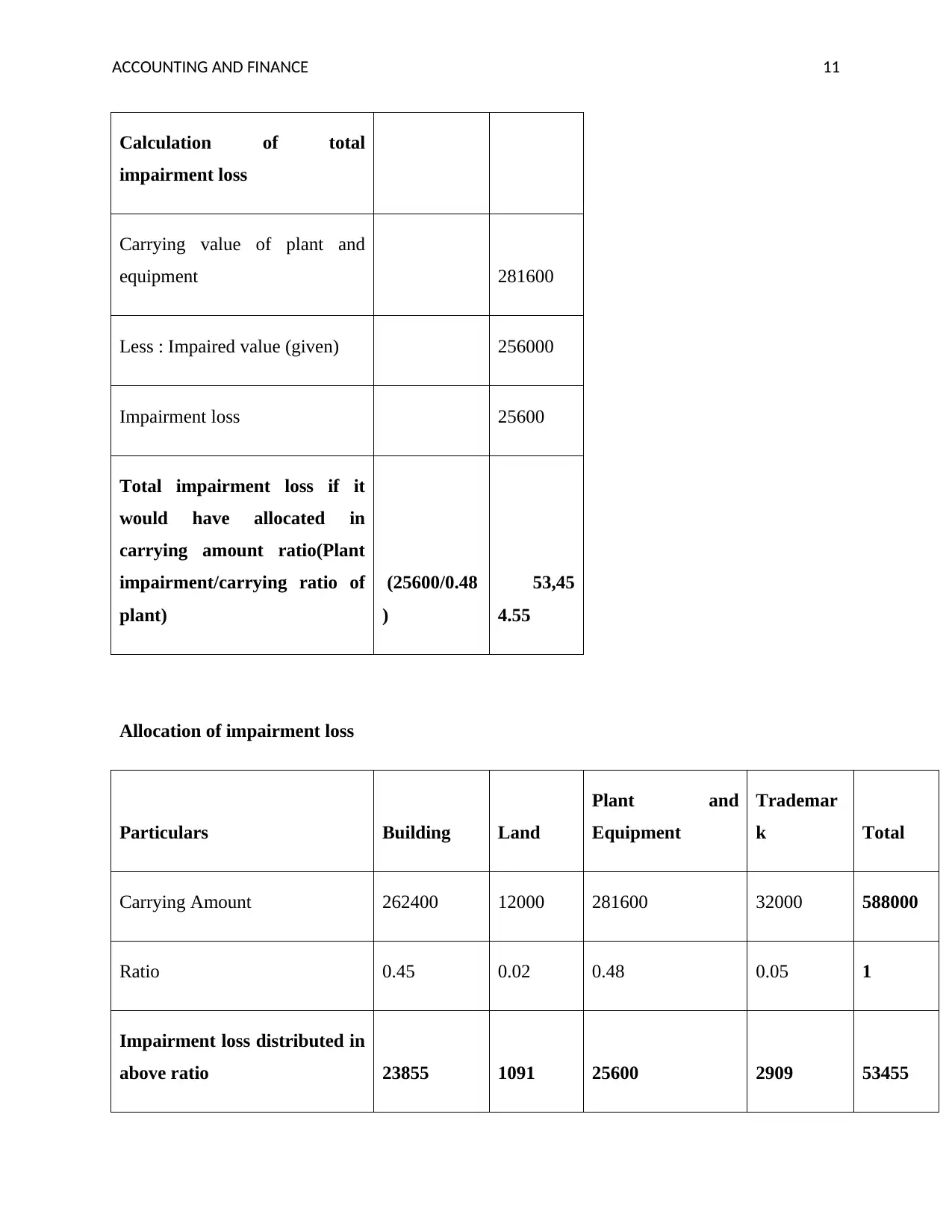

This assignment solution addresses accounting and finance concepts, specifically focusing on journal entries, depreciation, revaluation, and impairment losses. Question 1 presents detailed journal entries for machinery purchases, depreciation, revaluation, and disposal, providing a comprehensive understanding of asset accounting. Question 2 delves into impairment losses, including journal entries for revaluation surplus and impairment loss allocation across various assets like land, buildings, plant, equipment, goodwill, and trademarks. The solution includes working notes and calculations for impairment loss allocation, demonstrating the application of accounting standards. Furthermore, the assignment includes a discussion on asset assessment and impairment, explaining how recoverable amounts are determined, and providing a bibliography for further reading.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.