Financial Analysis: Dexter Plc, Philly Ltd, and Sankrust Ltd

VerifiedAdded on 2020/10/22

|18

|5159

|497

Homework Assignment

AI Summary

This assignment delves into core accounting and finance principles through the analysis of three companies: Dexter Plc, Philly Ltd, and Sankrust Ltd. Part A focuses on Dexter Plc, constructing an income statement and balance sheet for the year 2018, along with detailed working notes for key calculations. Part B analyzes Philly Ltd, calculating break-even points, profit margins, and the impact of sales price changes. Part C examines Sankrust Ltd, calculating net present value, payback period, and accounting rate of return, alongside a discussion of investment appraisal techniques and the role of budgeting in strategic planning. The assignment provides comprehensive insights into financial statement analysis, cost-volume-profit analysis, and investment decision-making.

INTRODUCTION TO

ACCOUNTING AND

FINANCE

ACCOUNTING AND

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

PART A- Dexter Plc..............................................................................................................................3

PART B: Philly Ltd..............................................................................................................................7

a...................................................................................................................................................7

b...................................................................................................................................................8

c...................................................................................................................................................9

d...................................................................................................................................................9

e. Assumption of breakeven model...........................................................................................10

PART C: Sankrust Ltd........................................................................................................................11

a. Calculation of net present value, payback period and accounting rate of return..................11

b. Merits and limitation of investment appraisal techniques ....................................................12

c. Budget as a tool for strategic planning .................................................................................13

CONCLUSION .................................................................................................................................16

REFERENCES...................................................................................................................................17

INTRODUCTION................................................................................................................................3

PART A- Dexter Plc..............................................................................................................................3

PART B: Philly Ltd..............................................................................................................................7

a...................................................................................................................................................7

b...................................................................................................................................................8

c...................................................................................................................................................9

d...................................................................................................................................................9

e. Assumption of breakeven model...........................................................................................10

PART C: Sankrust Ltd........................................................................................................................11

a. Calculation of net present value, payback period and accounting rate of return..................11

b. Merits and limitation of investment appraisal techniques ....................................................12

c. Budget as a tool for strategic planning .................................................................................13

CONCLUSION .................................................................................................................................16

REFERENCES...................................................................................................................................17

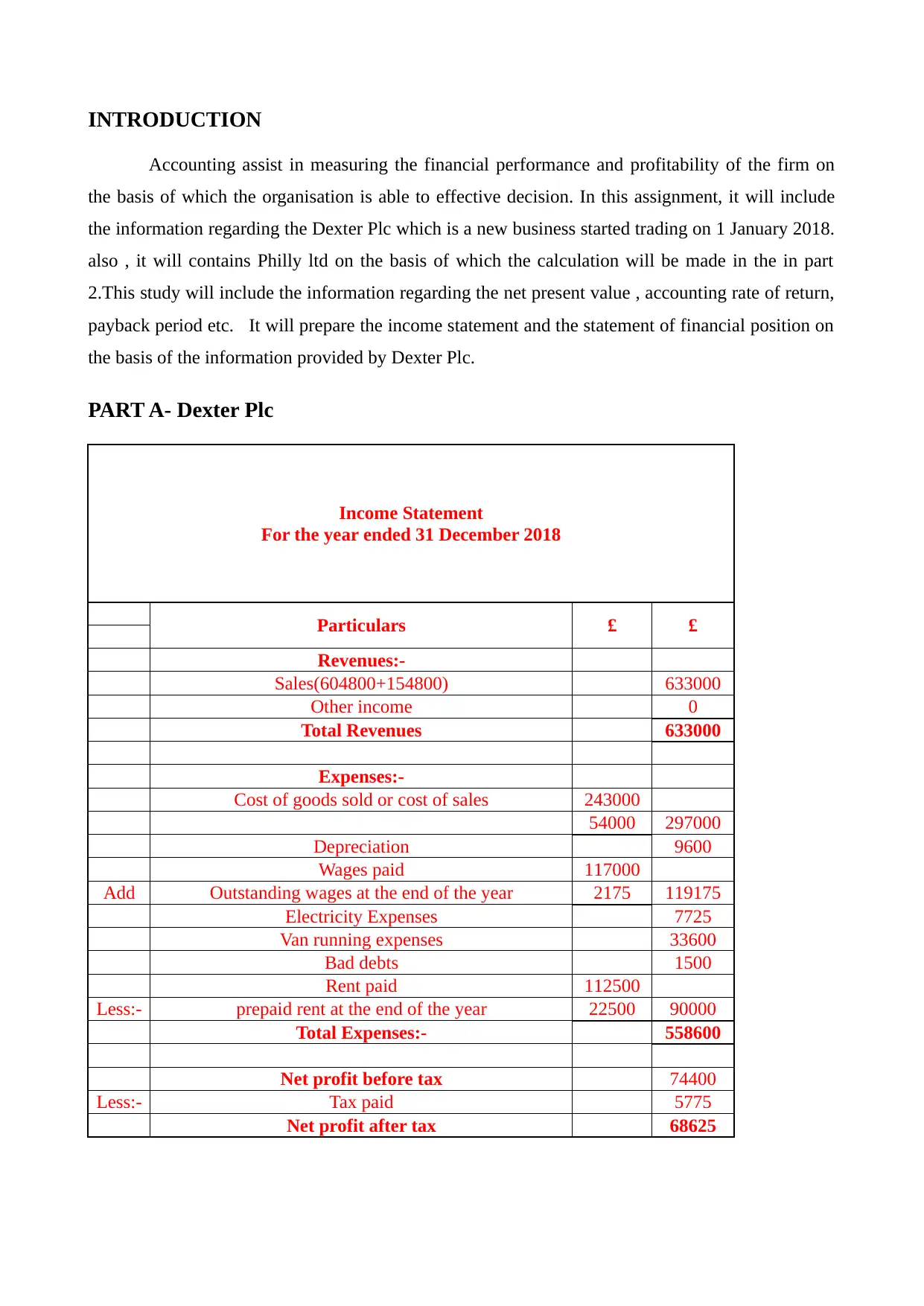

INTRODUCTION

Accounting assist in measuring the financial performance and profitability of the firm on

the basis of which the organisation is able to effective decision. In this assignment, it will include

the information regarding the Dexter Plc which is a new business started trading on 1 January 2018.

also , it will contains Philly ltd on the basis of which the calculation will be made in the in part

2.This study will include the information regarding the net present value , accounting rate of return,

payback period etc. It will prepare the income statement and the statement of financial position on

the basis of the information provided by Dexter Plc.

PART A- Dexter Plc

Income Statement

For the year ended 31 December 2018

Particulars £ £

Revenues:-

Sales(604800+154800) 633000

Other income 0

Total Revenues 633000

Expenses:-

Cost of goods sold or cost of sales 243000

54000 297000

Depreciation 9600

Wages paid 117000

Add Outstanding wages at the end of the year 2175 119175

Electricity Expenses 7725

Van running expenses 33600

Bad debts 1500

Rent paid 112500

Less:- prepaid rent at the end of the year 22500 90000

Total Expenses:- 558600

Net profit before tax 74400

Less:- Tax paid 5775

Net profit after tax 68625

Accounting assist in measuring the financial performance and profitability of the firm on

the basis of which the organisation is able to effective decision. In this assignment, it will include

the information regarding the Dexter Plc which is a new business started trading on 1 January 2018.

also , it will contains Philly ltd on the basis of which the calculation will be made in the in part

2.This study will include the information regarding the net present value , accounting rate of return,

payback period etc. It will prepare the income statement and the statement of financial position on

the basis of the information provided by Dexter Plc.

PART A- Dexter Plc

Income Statement

For the year ended 31 December 2018

Particulars £ £

Revenues:-

Sales(604800+154800) 633000

Other income 0

Total Revenues 633000

Expenses:-

Cost of goods sold or cost of sales 243000

54000 297000

Depreciation 9600

Wages paid 117000

Add Outstanding wages at the end of the year 2175 119175

Electricity Expenses 7725

Van running expenses 33600

Bad debts 1500

Rent paid 112500

Less:- prepaid rent at the end of the year 22500 90000

Total Expenses:- 558600

Net profit before tax 74400

Less:- Tax paid 5775

Net profit after tax 68625

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

From the above statement of income which has provided information about the income and

expenses which are being incurred by the organisation in that period which help in identifying the

profits earned by the firm during that period. The net profit earned by the firm in that period is

181905 which means the business is profitable and is growing to increase their market share in the

industry.

Balance Sheet

For the year ended 31 December 2018

£ £

Assets

Fixed Assets

Delivery Van 50400

Current Assets

Prepaid Rent 22500

Closing Inventory 228000

Trade Recievables 64500

Prepaid Tax 1125

Cash 90000

Total Assets 456525

LIABILITIES

Shareholder's Equity

Equity share capital 180000

Reserves and surplus 68625

Long Term Liabilities

Current Liabilities

Outstanding Wages 2175

Outstanding Electricity Expenses 2025

Trade Payables 93000

Bank Overdraft 110700

expenses which are being incurred by the organisation in that period which help in identifying the

profits earned by the firm during that period. The net profit earned by the firm in that period is

181905 which means the business is profitable and is growing to increase their market share in the

industry.

Balance Sheet

For the year ended 31 December 2018

£ £

Assets

Fixed Assets

Delivery Van 50400

Current Assets

Prepaid Rent 22500

Closing Inventory 228000

Trade Recievables 64500

Prepaid Tax 1125

Cash 90000

Total Assets 456525

LIABILITIES

Shareholder's Equity

Equity share capital 180000

Reserves and surplus 68625

Long Term Liabilities

Current Liabilities

Outstanding Wages 2175

Outstanding Electricity Expenses 2025

Trade Payables 93000

Bank Overdraft 110700

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

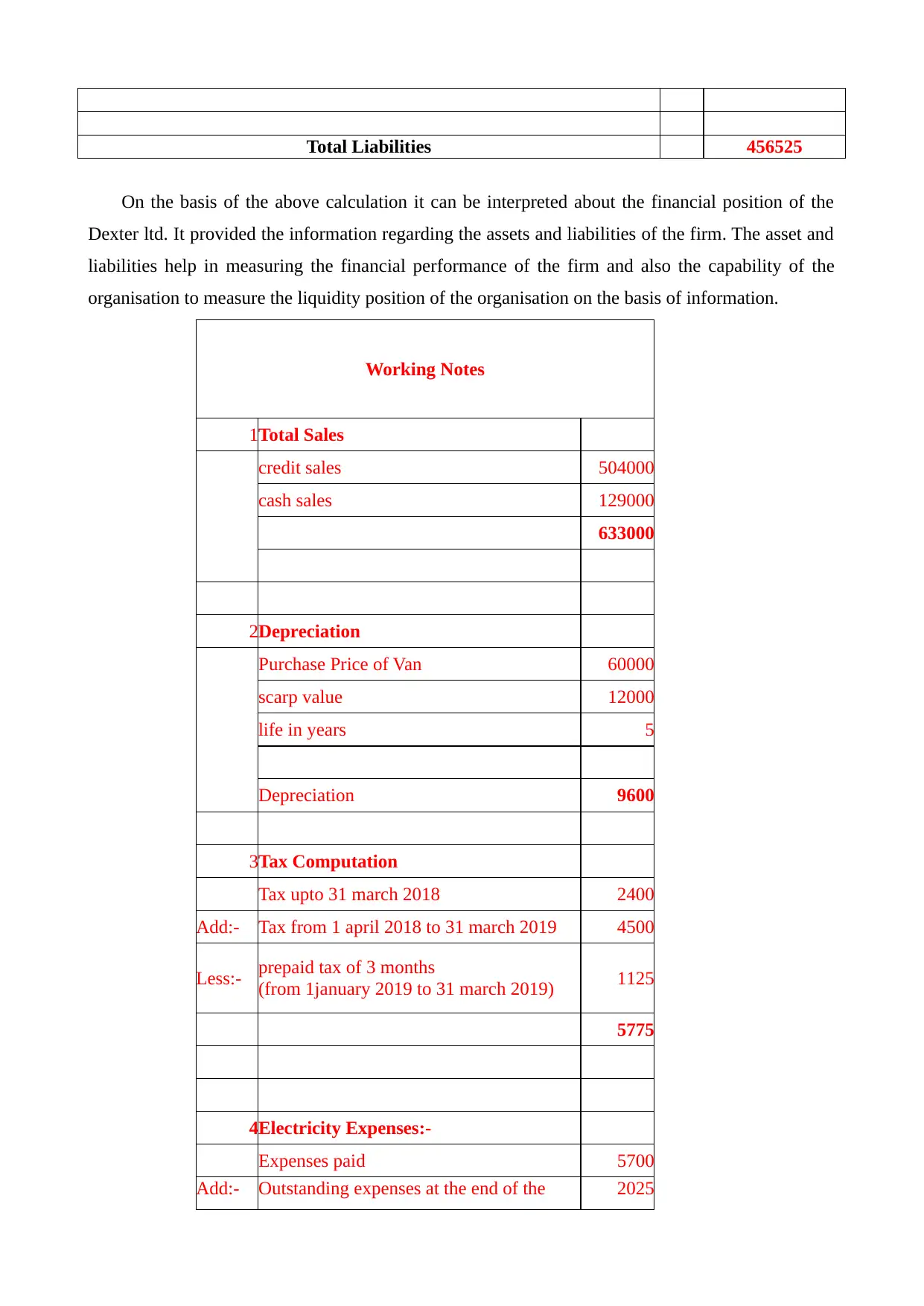

Total Liabilities 456525

On the basis of the above calculation it can be interpreted about the financial position of the

Dexter ltd. It provided the information regarding the assets and liabilities of the firm. The asset and

liabilities help in measuring the financial performance of the firm and also the capability of the

organisation to measure the liquidity position of the organisation on the basis of information.

Working Notes

1Total Sales

credit sales 504000

cash sales 129000

633000

2Depreciation

Purchase Price of Van 60000

scarp value 12000

life in years 5

Depreciation 9600

3Tax Computation

Tax upto 31 march 2018 2400

Add:- Tax from 1 april 2018 to 31 march 2019 4500

Less:- prepaid tax of 3 months

(from 1january 2019 to 31 march 2019) 1125

5775

4Electricity Expenses:-

Expenses paid 5700

Add:- Outstanding expenses at the end of the 2025

On the basis of the above calculation it can be interpreted about the financial position of the

Dexter ltd. It provided the information regarding the assets and liabilities of the firm. The asset and

liabilities help in measuring the financial performance of the firm and also the capability of the

organisation to measure the liquidity position of the organisation on the basis of information.

Working Notes

1Total Sales

credit sales 504000

cash sales 129000

633000

2Depreciation

Purchase Price of Van 60000

scarp value 12000

life in years 5

Depreciation 9600

3Tax Computation

Tax upto 31 march 2018 2400

Add:- Tax from 1 april 2018 to 31 march 2019 4500

Less:- prepaid tax of 3 months

(from 1january 2019 to 31 march 2019) 1125

5775

4Electricity Expenses:-

Expenses paid 5700

Add:- Outstanding expenses at the end of the 2025

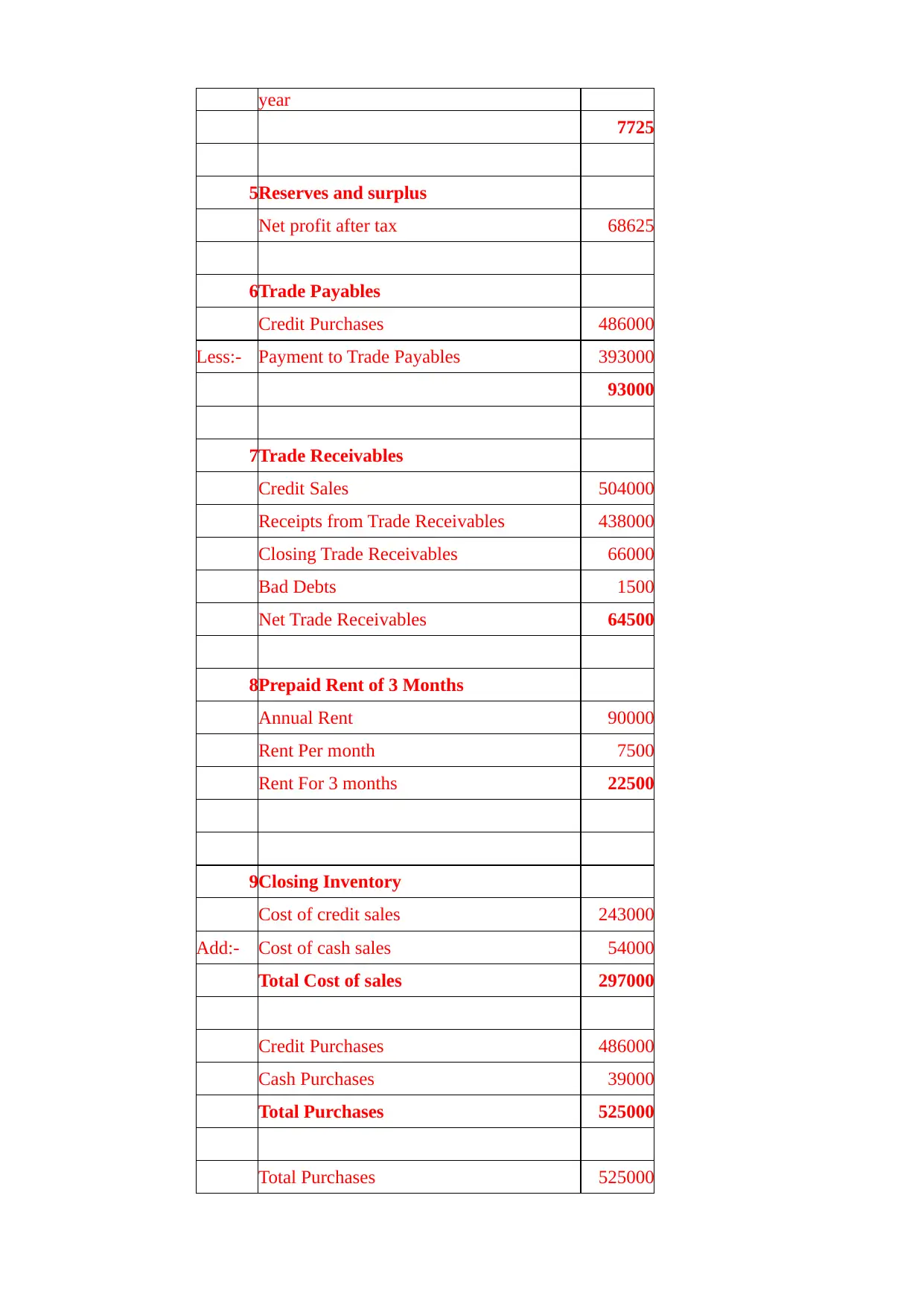

year

7725

5Reserves and surplus

Net profit after tax 68625

6Trade Payables

Credit Purchases 486000

Less:- Payment to Trade Payables 393000

93000

7Trade Receivables

Credit Sales 504000

Receipts from Trade Receivables 438000

Closing Trade Receivables 66000

Bad Debts 1500

Net Trade Receivables 64500

8Prepaid Rent of 3 Months

Annual Rent 90000

Rent Per month 7500

Rent For 3 months 22500

9Closing Inventory

Cost of credit sales 243000

Add:- Cost of cash sales 54000

Total Cost of sales 297000

Credit Purchases 486000

Cash Purchases 39000

Total Purchases 525000

Total Purchases 525000

7725

5Reserves and surplus

Net profit after tax 68625

6Trade Payables

Credit Purchases 486000

Less:- Payment to Trade Payables 393000

93000

7Trade Receivables

Credit Sales 504000

Receipts from Trade Receivables 438000

Closing Trade Receivables 66000

Bad Debts 1500

Net Trade Receivables 64500

8Prepaid Rent of 3 Months

Annual Rent 90000

Rent Per month 7500

Rent For 3 months 22500

9Closing Inventory

Cost of credit sales 243000

Add:- Cost of cash sales 54000

Total Cost of sales 297000

Credit Purchases 486000

Cash Purchases 39000

Total Purchases 525000

Total Purchases 525000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

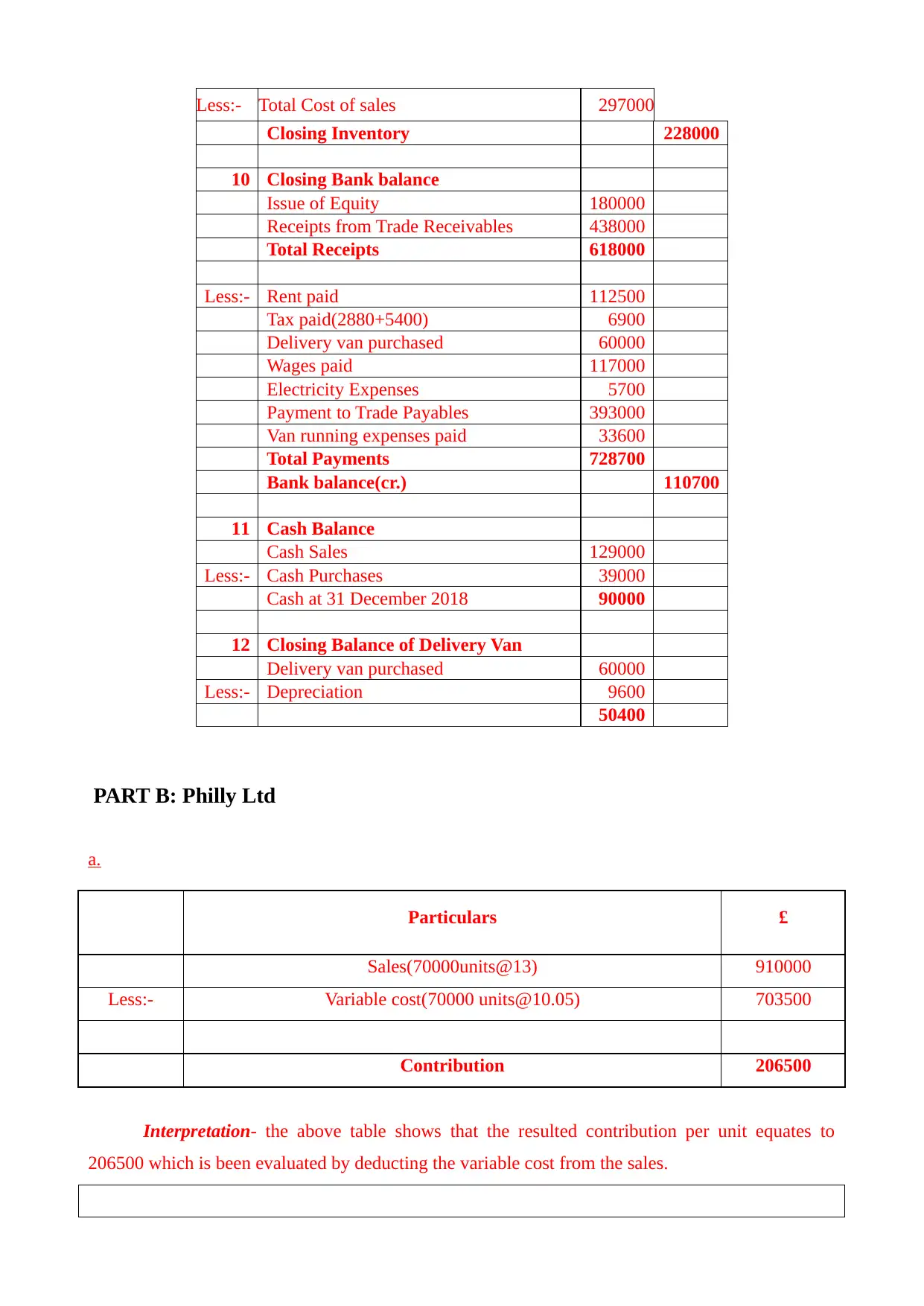

Less:- Total Cost of sales 297000

Closing Inventory 228000

10 Closing Bank balance

Issue of Equity 180000

Receipts from Trade Receivables 438000

Total Receipts 618000

Less:- Rent paid 112500

Tax paid(2880+5400) 6900

Delivery van purchased 60000

Wages paid 117000

Electricity Expenses 5700

Payment to Trade Payables 393000

Van running expenses paid 33600

Total Payments 728700

Bank balance(cr.) 110700

11 Cash Balance

Cash Sales 129000

Less:- Cash Purchases 39000

Cash at 31 December 2018 90000

12 Closing Balance of Delivery Van

Delivery van purchased 60000

Less:- Depreciation 9600

50400

PART B: Philly Ltd

a.

Particulars £

Sales(70000units@13) 910000

Less:- Variable cost(70000 units@10.05) 703500

Contribution 206500

Interpretation- the above table shows that the resulted contribution per unit equates to

206500 which is been evaluated by deducting the variable cost from the sales.

Closing Inventory 228000

10 Closing Bank balance

Issue of Equity 180000

Receipts from Trade Receivables 438000

Total Receipts 618000

Less:- Rent paid 112500

Tax paid(2880+5400) 6900

Delivery van purchased 60000

Wages paid 117000

Electricity Expenses 5700

Payment to Trade Payables 393000

Van running expenses paid 33600

Total Payments 728700

Bank balance(cr.) 110700

11 Cash Balance

Cash Sales 129000

Less:- Cash Purchases 39000

Cash at 31 December 2018 90000

12 Closing Balance of Delivery Van

Delivery van purchased 60000

Less:- Depreciation 9600

50400

PART B: Philly Ltd

a.

Particulars £

Sales(70000units@13) 910000

Less:- Variable cost(70000 units@10.05) 703500

Contribution 206500

Interpretation- the above table shows that the resulted contribution per unit equates to

206500 which is been evaluated by deducting the variable cost from the sales.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

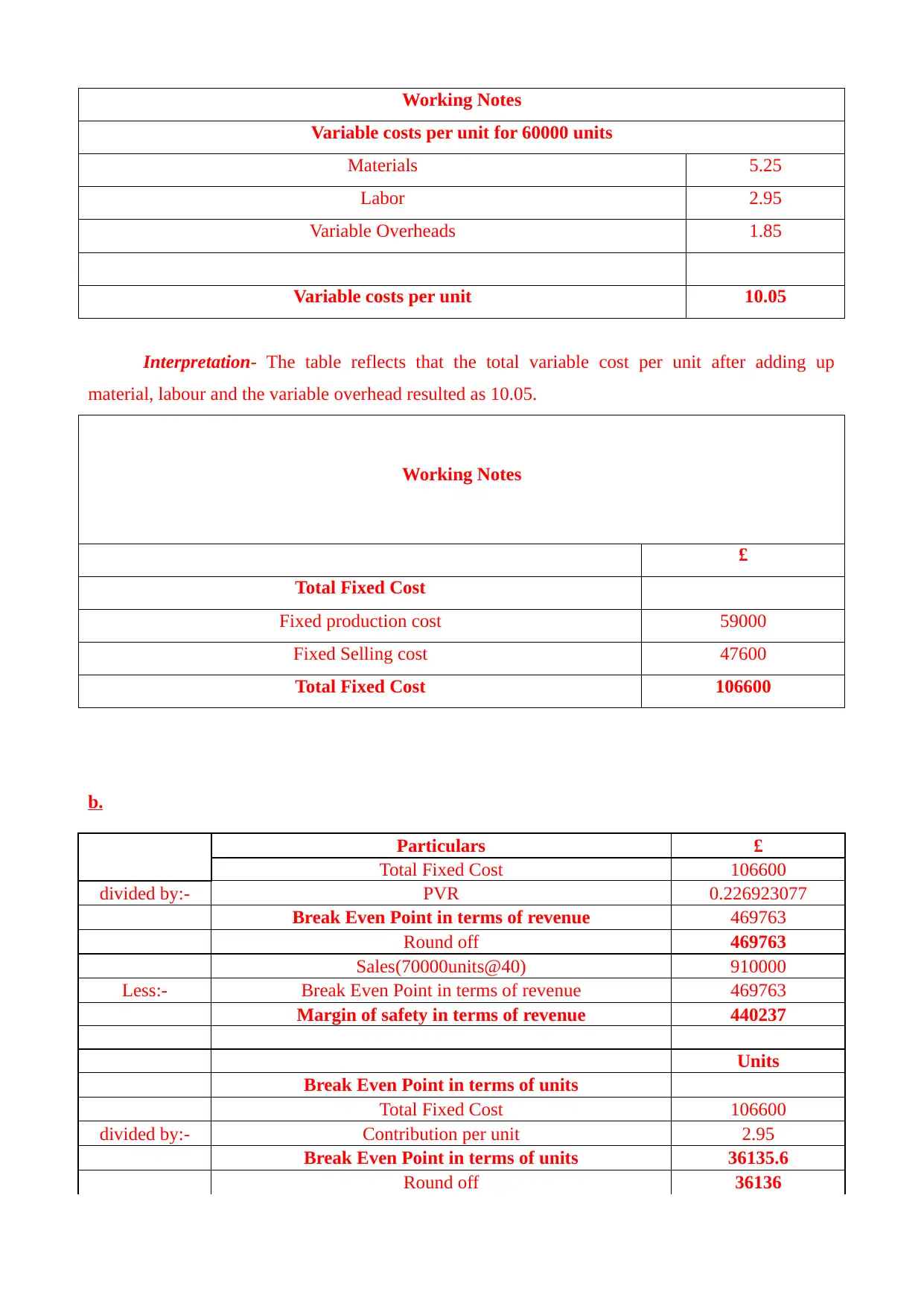

Working Notes

Variable costs per unit for 60000 units

Materials 5.25

Labor 2.95

Variable Overheads 1.85

Variable costs per unit 10.05

Interpretation- The table reflects that the total variable cost per unit after adding up

material, labour and the variable overhead resulted as 10.05.

Working Notes

£

Total Fixed Cost

Fixed production cost 59000

Fixed Selling cost 47600

Total Fixed Cost 106600

b.

Particulars £

Total Fixed Cost 106600

divided by:- PVR 0.226923077

Break Even Point in terms of revenue 469763

Round off 469763

Sales(70000units@40) 910000

Less:- Break Even Point in terms of revenue 469763

Margin of safety in terms of revenue 440237

Units

Break Even Point in terms of units

Total Fixed Cost 106600

divided by:- Contribution per unit 2.95

Break Even Point in terms of units 36135.6

Round off 36136

Variable costs per unit for 60000 units

Materials 5.25

Labor 2.95

Variable Overheads 1.85

Variable costs per unit 10.05

Interpretation- The table reflects that the total variable cost per unit after adding up

material, labour and the variable overhead resulted as 10.05.

Working Notes

£

Total Fixed Cost

Fixed production cost 59000

Fixed Selling cost 47600

Total Fixed Cost 106600

b.

Particulars £

Total Fixed Cost 106600

divided by:- PVR 0.226923077

Break Even Point in terms of revenue 469763

Round off 469763

Sales(70000units@40) 910000

Less:- Break Even Point in terms of revenue 469763

Margin of safety in terms of revenue 440237

Units

Break Even Point in terms of units

Total Fixed Cost 106600

divided by:- Contribution per unit 2.95

Break Even Point in terms of units 36135.6

Round off 36136

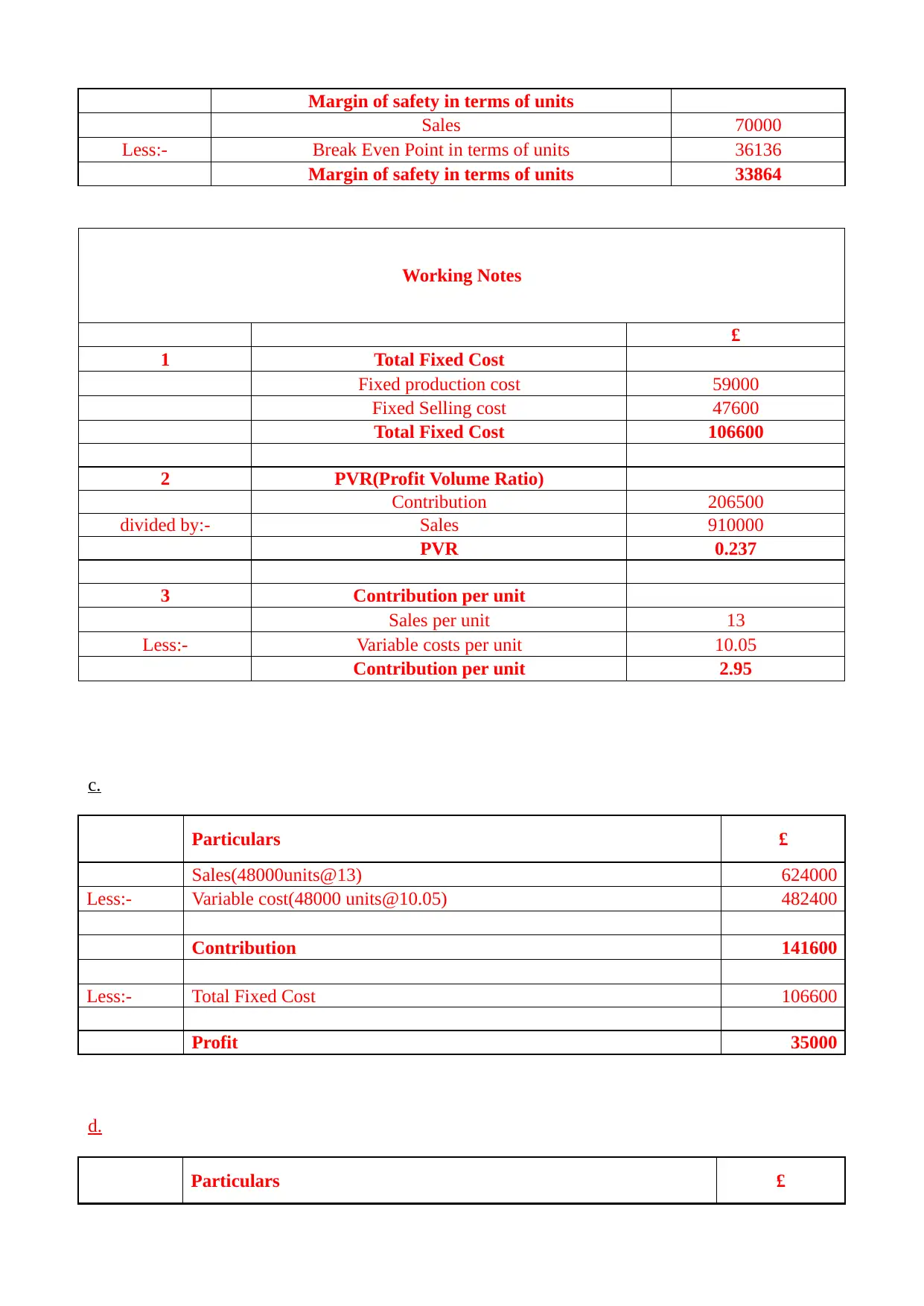

Margin of safety in terms of units

Sales 70000

Less:- Break Even Point in terms of units 36136

Margin of safety in terms of units 33864

Working Notes

£

1 Total Fixed Cost

Fixed production cost 59000

Fixed Selling cost 47600

Total Fixed Cost 106600

2 PVR(Profit Volume Ratio)

Contribution 206500

divided by:- Sales 910000

PVR 0.237

3 Contribution per unit

Sales per unit 13

Less:- Variable costs per unit 10.05

Contribution per unit 2.95

c.

Particulars £

Sales(48000units@13) 624000

Less:- Variable cost(48000 units@10.05) 482400

Contribution 141600

Less:- Total Fixed Cost 106600

Profit 35000

d.

Particulars £

Sales 70000

Less:- Break Even Point in terms of units 36136

Margin of safety in terms of units 33864

Working Notes

£

1 Total Fixed Cost

Fixed production cost 59000

Fixed Selling cost 47600

Total Fixed Cost 106600

2 PVR(Profit Volume Ratio)

Contribution 206500

divided by:- Sales 910000

PVR 0.237

3 Contribution per unit

Sales per unit 13

Less:- Variable costs per unit 10.05

Contribution per unit 2.95

c.

Particulars £

Sales(48000units@13) 624000

Less:- Variable cost(48000 units@10.05) 482400

Contribution 141600

Less:- Total Fixed Cost 106600

Profit 35000

d.

Particulars £

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

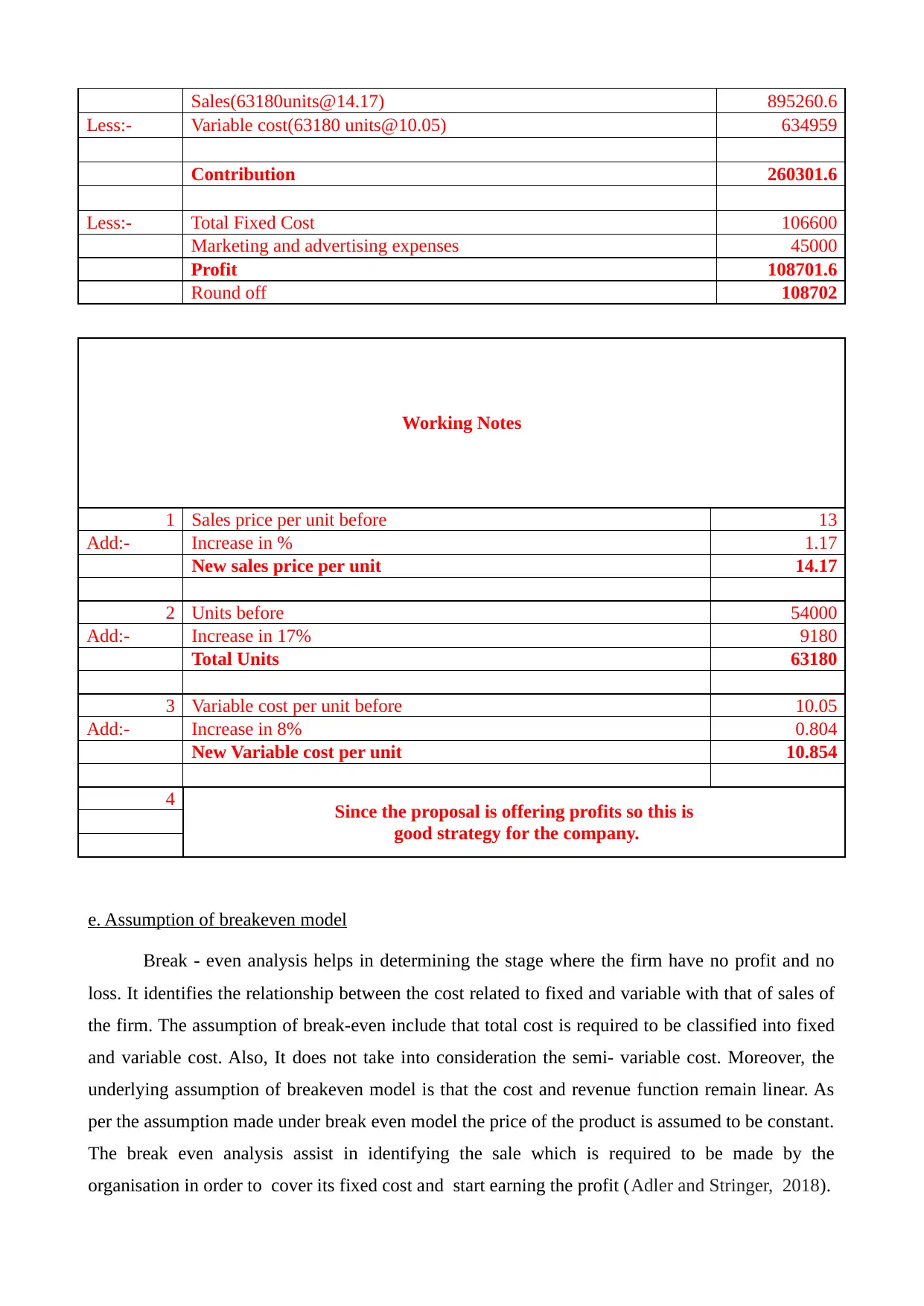

Sales(63180units@14.17) 895260.6

Less:- Variable cost(63180 units@10.05) 634959

Contribution 260301.6

Less:- Total Fixed Cost 106600

Marketing and advertising expenses 45000

Profit 108701.6

Round off 108702

Working Notes

1 Sales price per unit before 13

Add:- Increase in % 1.17

New sales price per unit 14.17

2 Units before 54000

Add:- Increase in 17% 9180

Total Units 63180

3 Variable cost per unit before 10.05

Add:- Increase in 8% 0.804

New Variable cost per unit 10.854

4 Since the proposal is offering profits so this is

good strategy for the company.

e. Assumption of breakeven model

Break - even analysis helps in determining the stage where the firm have no profit and no

loss. It identifies the relationship between the cost related to fixed and variable with that of sales of

the firm. The assumption of break-even include that total cost is required to be classified into fixed

and variable cost. Also, It does not take into consideration the semi- variable cost. Moreover, the

underlying assumption of breakeven model is that the cost and revenue function remain linear. As

per the assumption made under break even model the price of the product is assumed to be constant.

The break even analysis assist in identifying the sale which is required to be made by the

organisation in order to cover its fixed cost and start earning the profit (Adler and Stringer, 2018).

Less:- Variable cost(63180 units@10.05) 634959

Contribution 260301.6

Less:- Total Fixed Cost 106600

Marketing and advertising expenses 45000

Profit 108701.6

Round off 108702

Working Notes

1 Sales price per unit before 13

Add:- Increase in % 1.17

New sales price per unit 14.17

2 Units before 54000

Add:- Increase in 17% 9180

Total Units 63180

3 Variable cost per unit before 10.05

Add:- Increase in 8% 0.804

New Variable cost per unit 10.854

4 Since the proposal is offering profits so this is

good strategy for the company.

e. Assumption of breakeven model

Break - even analysis helps in determining the stage where the firm have no profit and no

loss. It identifies the relationship between the cost related to fixed and variable with that of sales of

the firm. The assumption of break-even include that total cost is required to be classified into fixed

and variable cost. Also, It does not take into consideration the semi- variable cost. Moreover, the

underlying assumption of breakeven model is that the cost and revenue function remain linear. As

per the assumption made under break even model the price of the product is assumed to be constant.

The break even analysis assist in identifying the sale which is required to be made by the

organisation in order to cover its fixed cost and start earning the profit (Adler and Stringer, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

With the help of its revenue can cost the organisation is able to measure its break even

because when the firm revenue and cost are equal than it is said that the firm is in the position of

break-even where there is no profit and loss. This analysis assist in identifying the cost- volume -

profit relationships. Moreover the assumption of break - even analysis state that unit of selling price

remain constant. break- even analysis is used by various organisation because there are various

benefit of using this analysis as it helps the firm in understanding their level of sales which will

assist in recovering their cost. Moreover, the organisation by using this analysis is able to estimate

the level of profit which is required by the firm for the growth and success of the organisation.

Moreover, it is useful for the firm because it assist in determining the operating risk associated with

the firm. The finance manager with the help of the break - even analysis is able to make planning

for the capital structure of the firm. The assumption of break - even analysis include that the

productivity of per worker is assumed to be unchanged. Company uses the break - even analysis as

it help the firm in determining the level of sales which will be required for covering the cost

(Cortese and Walton, 2018). Moreover, it helps in determining the level of profit which is required

for covering the cost. Break -even analysis is used by different businesses because it provide

assistance to the firm in identifying the level of sales and profit.

PART C: Sankrust Ltd

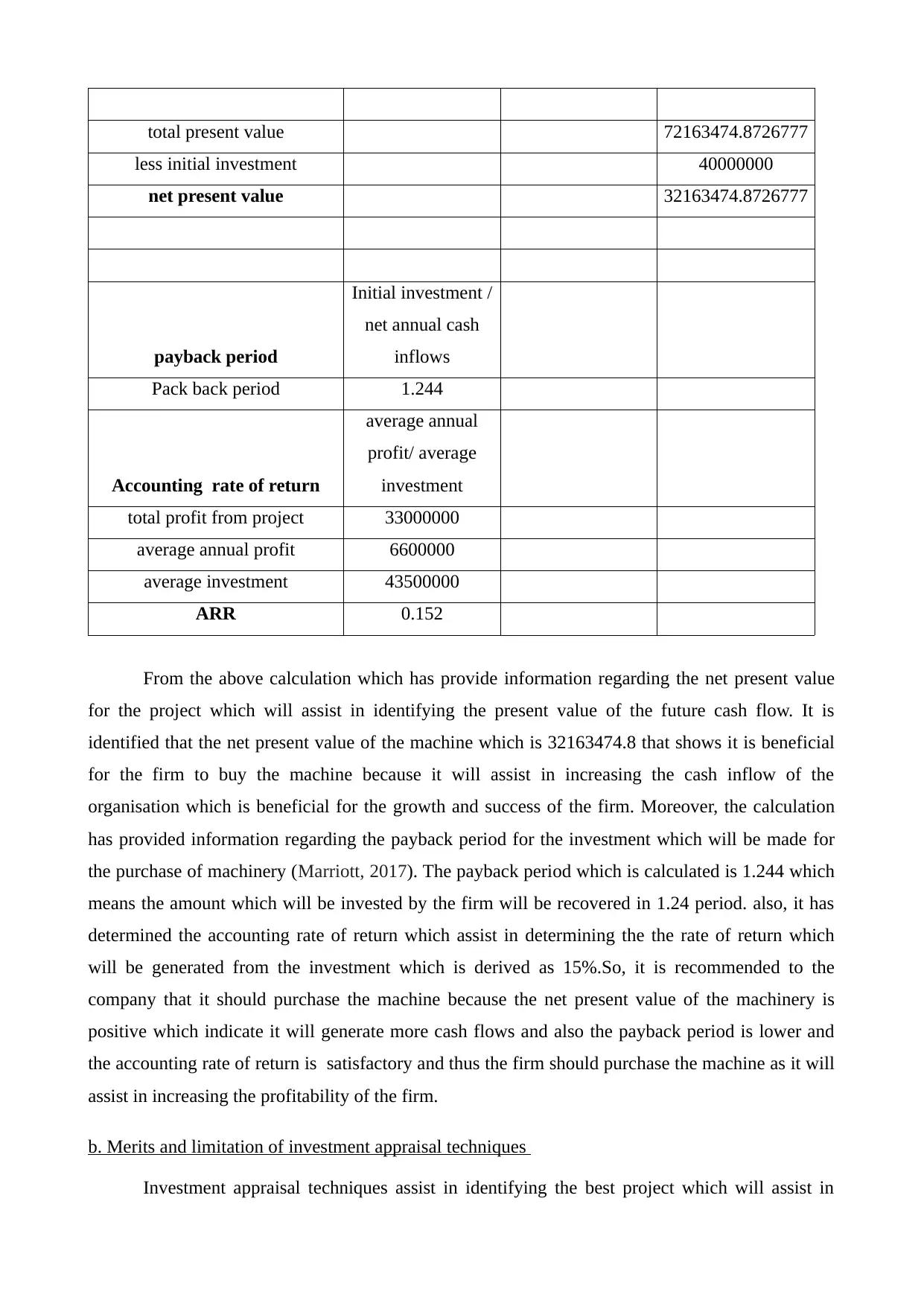

a. Calculation of net present value, payback period and accounting rate of return

Depreciation

cost of machine 40000000

selling amount 5000000

expected life 5

depreciation amount 7000000

years net cash flow

discounting

factor@7% present value

0 40000000

1 17600000 0.935 16448598.1308411

2 17600000 0.873 15372521.6176085

3 17600000 0.816 14366842.633279

4 17600000 0.763 13426955.7320364

5 17600000 0.713 12548556.7589126

because when the firm revenue and cost are equal than it is said that the firm is in the position of

break-even where there is no profit and loss. This analysis assist in identifying the cost- volume -

profit relationships. Moreover the assumption of break - even analysis state that unit of selling price

remain constant. break- even analysis is used by various organisation because there are various

benefit of using this analysis as it helps the firm in understanding their level of sales which will

assist in recovering their cost. Moreover, the organisation by using this analysis is able to estimate

the level of profit which is required by the firm for the growth and success of the organisation.

Moreover, it is useful for the firm because it assist in determining the operating risk associated with

the firm. The finance manager with the help of the break - even analysis is able to make planning

for the capital structure of the firm. The assumption of break - even analysis include that the

productivity of per worker is assumed to be unchanged. Company uses the break - even analysis as

it help the firm in determining the level of sales which will be required for covering the cost

(Cortese and Walton, 2018). Moreover, it helps in determining the level of profit which is required

for covering the cost. Break -even analysis is used by different businesses because it provide

assistance to the firm in identifying the level of sales and profit.

PART C: Sankrust Ltd

a. Calculation of net present value, payback period and accounting rate of return

Depreciation

cost of machine 40000000

selling amount 5000000

expected life 5

depreciation amount 7000000

years net cash flow

discounting

factor@7% present value

0 40000000

1 17600000 0.935 16448598.1308411

2 17600000 0.873 15372521.6176085

3 17600000 0.816 14366842.633279

4 17600000 0.763 13426955.7320364

5 17600000 0.713 12548556.7589126

total present value 72163474.8726777

less initial investment 40000000

net present value 32163474.8726777

payback period

Initial investment /

net annual cash

inflows

Pack back period 1.244

Accounting rate of return

average annual

profit/ average

investment

total profit from project 33000000

average annual profit 6600000

average investment 43500000

ARR 0.152

From the above calculation which has provide information regarding the net present value

for the project which will assist in identifying the present value of the future cash flow. It is

identified that the net present value of the machine which is 32163474.8 that shows it is beneficial

for the firm to buy the machine because it will assist in increasing the cash inflow of the

organisation which is beneficial for the growth and success of the firm. Moreover, the calculation

has provided information regarding the payback period for the investment which will be made for

the purchase of machinery (Marriott, 2017). The payback period which is calculated is 1.244 which

means the amount which will be invested by the firm will be recovered in 1.24 period. also, it has

determined the accounting rate of return which assist in determining the the rate of return which

will be generated from the investment which is derived as 15%.So, it is recommended to the

company that it should purchase the machine because the net present value of the machinery is

positive which indicate it will generate more cash flows and also the payback period is lower and

the accounting rate of return is satisfactory and thus the firm should purchase the machine as it will

assist in increasing the profitability of the firm.

b. Merits and limitation of investment appraisal techniques

Investment appraisal techniques assist in identifying the best project which will assist in

less initial investment 40000000

net present value 32163474.8726777

payback period

Initial investment /

net annual cash

inflows

Pack back period 1.244

Accounting rate of return

average annual

profit/ average

investment

total profit from project 33000000

average annual profit 6600000

average investment 43500000

ARR 0.152

From the above calculation which has provide information regarding the net present value

for the project which will assist in identifying the present value of the future cash flow. It is

identified that the net present value of the machine which is 32163474.8 that shows it is beneficial

for the firm to buy the machine because it will assist in increasing the cash inflow of the

organisation which is beneficial for the growth and success of the firm. Moreover, the calculation

has provided information regarding the payback period for the investment which will be made for

the purchase of machinery (Marriott, 2017). The payback period which is calculated is 1.244 which

means the amount which will be invested by the firm will be recovered in 1.24 period. also, it has

determined the accounting rate of return which assist in determining the the rate of return which

will be generated from the investment which is derived as 15%.So, it is recommended to the

company that it should purchase the machine because the net present value of the machinery is

positive which indicate it will generate more cash flows and also the payback period is lower and

the accounting rate of return is satisfactory and thus the firm should purchase the machine as it will

assist in increasing the profitability of the firm.

b. Merits and limitation of investment appraisal techniques

Investment appraisal techniques assist in identifying the best project which will assist in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.