Accounting Finance for Executive: Financial Statement Analysis Report

VerifiedAdded on 2020/04/13

|18

|2077

|43

Report

AI Summary

This report delves into the core concepts of accounting and finance, beginning with a comparison of cash and accrual basis accounting, highlighting their differences in transaction timing and recognition. It then proceeds to analyze financial statements, using the 2016 annual report of Air New Zealand as a case study. The analysis examines the auditor's role, the audit opinion, and the distinction between net profit and cash from operations. The report also explores contingent liabilities and working capital management. The report also includes practical calculations for working capital and references relevant literature. The analysis covers key aspects of financial reporting and provides insights into the financial health of a company.

Running head: ACCOUNTING FINANCE FOR EXECUTIVE

Accounting Finance for Executive

Name of the Student:

Student’s ID:

Lecturer’s Name:

Author’s Note

Accounting Finance for Executive

Name of the Student:

Student’s ID:

Lecturer’s Name:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING FINANCE FOR EXECUTIVE

Table of Contents

Answer to Question 1......................................................................................................................2

Cash Versus Accrual Basis of Accounting..................................................................................2

Question 2........................................................................................................................................4

Financial Statement Analysis......................................................................................................4

Question 2........................................................................................................................................6

Requirement a:.............................................................................................................................6

Requirement b:.............................................................................................................................7

Requirement c:.............................................................................................................................9

Workings..........................................................................................................................................9

Reference.......................................................................................................................................17

ACCOUNTING FINANCE FOR EXECUTIVE

Table of Contents

Answer to Question 1......................................................................................................................2

Cash Versus Accrual Basis of Accounting..................................................................................2

Question 2........................................................................................................................................4

Financial Statement Analysis......................................................................................................4

Question 2........................................................................................................................................6

Requirement a:.............................................................................................................................6

Requirement b:.............................................................................................................................7

Requirement c:.............................................................................................................................9

Workings..........................................................................................................................................9

Reference.......................................................................................................................................17

2

ACCOUNTING FINANCE FOR EXECUTIVE

Answer to Question 1

Cash Versus Accrual Basis of Accounting

The process of accounting is a dynamic process wherein the recording and recognition of

transactions are done on the basis of two method which are generally used. These methods are

Cash basis of Accounting and Accrual basis of Accounting. These methods are used widely used

in every accounting business.

In cash basis accounting system, all the transactions are recorded and presented on the

basis of cash as and when such cash are received. In accrual system of accounting the revenue is

recorded when it is actually earned and expenses are recorded when such expenses are actually

incurred. Accrual basis of accounting does not depend on whether cash is received or paid. The

core difference between cash basis of accounting and accrual basis of accounting is that the

timing of the transactions is different in each case. The difference which arises between cash

basis of accounting and accrual basis of accounting is mainly due to the difference in timing of

recognition of elements of the financial statements (Tiron Tudor and Mutiu 2012). In business,

normally accrual basis for recording of transactions are preferred as transactions are recognized

as and when such transactions take place. However, certain businesses are there which do not

have a high revenue or turnover and has simple transactions to record follow cash basis of

accounting. Accrual basis Accounting of transactions are used by firms which have a high

turnover and also there is the cash that in order to get the financial accounts audited the company

needs to prepare the financial accounts on the basis of accrual system of recording transactions

(Bergmann 2012).

The benefits of using cash method of recording transactions is that it is a simple method

and easy to implement and follow. Moreover, it allows the business to keep a track of the cash

inflows and outflows in a business (Irwin 2012). The method of cash basis also has its impact on

the amount of tax which is to be paid by the business considering the amount of cash which is

banked. In the case of accrual method, the basic advantage is that the matching of income and

expenses as and when they occur. Accrual method allows the business to estimate clearly the

future profits which can be earned by the business (VanZante 2013).

Alpha ltd is engaged in the business of providing online services to airlines which is

situated in New Zealand. The company recognizes transactions on accrual basis and the

difference which arises in the value of cash basis and accrual basis is due to the treatment of

ACCOUNTING FINANCE FOR EXECUTIVE

Answer to Question 1

Cash Versus Accrual Basis of Accounting

The process of accounting is a dynamic process wherein the recording and recognition of

transactions are done on the basis of two method which are generally used. These methods are

Cash basis of Accounting and Accrual basis of Accounting. These methods are used widely used

in every accounting business.

In cash basis accounting system, all the transactions are recorded and presented on the

basis of cash as and when such cash are received. In accrual system of accounting the revenue is

recorded when it is actually earned and expenses are recorded when such expenses are actually

incurred. Accrual basis of accounting does not depend on whether cash is received or paid. The

core difference between cash basis of accounting and accrual basis of accounting is that the

timing of the transactions is different in each case. The difference which arises between cash

basis of accounting and accrual basis of accounting is mainly due to the difference in timing of

recognition of elements of the financial statements (Tiron Tudor and Mutiu 2012). In business,

normally accrual basis for recording of transactions are preferred as transactions are recognized

as and when such transactions take place. However, certain businesses are there which do not

have a high revenue or turnover and has simple transactions to record follow cash basis of

accounting. Accrual basis Accounting of transactions are used by firms which have a high

turnover and also there is the cash that in order to get the financial accounts audited the company

needs to prepare the financial accounts on the basis of accrual system of recording transactions

(Bergmann 2012).

The benefits of using cash method of recording transactions is that it is a simple method

and easy to implement and follow. Moreover, it allows the business to keep a track of the cash

inflows and outflows in a business (Irwin 2012). The method of cash basis also has its impact on

the amount of tax which is to be paid by the business considering the amount of cash which is

banked. In the case of accrual method, the basic advantage is that the matching of income and

expenses as and when they occur. Accrual method allows the business to estimate clearly the

future profits which can be earned by the business (VanZante 2013).

Alpha ltd is engaged in the business of providing online services to airlines which is

situated in New Zealand. The company recognizes transactions on accrual basis and the

difference which arises in the value of cash basis and accrual basis is due to the treatment of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING FINANCE FOR EXECUTIVE

depreciation which is $ 96,000 and also due to the unallocated revenue which is of amount

43,000. The management of the company follows accrual basis which is very useful for matching

the revenues and expenses of the company. The net profit which is generated by the company is

estimated following the accrual basis of accounting and the cash generated from operations is

calculated following cash basis of accounting. Both the figures are necessary as they are used for

matching the revenues and also clearly pointing out the transaction which have caused the

difference in revenues on the basis of cash and accrual accounting.

The responsibility of the external auditor is to ensure that the financial statement is

showing true and fair view. The role of the external auditor is to investigate the annual reports of

the company and form an opinion whether annual reports of company are fairly represented or

not. The main responsibility of the auditor is to analyze the financial reports of the company and

also form an opinion on the financial statement of the company (Davidson, Desai and Gerard

2013). In many cases the management of the company is of the view that the auditor is

responsible for detecting fraud and error which is not the case and therefore the auditor is an

independent person who is responsible for the analysis of the financial statements of the

company in order to form an opinion on the financial statement of the company.

Therefore, from the above discussion it is clear that an auditor is responsible to ensure

that the financial statements are fairly represented and the shareholders are protected from any

manipulations. The audited balance sheet of the company is the basis on which the potential

investors of the company decide whether or not to invest in the shares of the company. The

auditor is responsible to act in the best interest of the shareholders of the company and determine

whether the financial reports of the company is showing true and fair view or not. The auditors

of the company are to also ensure that the there is no omission or manipulation in the financial

statement of the company.

Question 2

Financial Statement Analysis

As per the case study provided in the assignment, the annual reports of Air New Zealand

is given for the year 2016. The analysis of the financial statement is to be done, on the basis

which the questions given in the assignment is to be solved.

ACCOUNTING FINANCE FOR EXECUTIVE

depreciation which is $ 96,000 and also due to the unallocated revenue which is of amount

43,000. The management of the company follows accrual basis which is very useful for matching

the revenues and expenses of the company. The net profit which is generated by the company is

estimated following the accrual basis of accounting and the cash generated from operations is

calculated following cash basis of accounting. Both the figures are necessary as they are used for

matching the revenues and also clearly pointing out the transaction which have caused the

difference in revenues on the basis of cash and accrual accounting.

The responsibility of the external auditor is to ensure that the financial statement is

showing true and fair view. The role of the external auditor is to investigate the annual reports of

the company and form an opinion whether annual reports of company are fairly represented or

not. The main responsibility of the auditor is to analyze the financial reports of the company and

also form an opinion on the financial statement of the company (Davidson, Desai and Gerard

2013). In many cases the management of the company is of the view that the auditor is

responsible for detecting fraud and error which is not the case and therefore the auditor is an

independent person who is responsible for the analysis of the financial statements of the

company in order to form an opinion on the financial statement of the company.

Therefore, from the above discussion it is clear that an auditor is responsible to ensure

that the financial statements are fairly represented and the shareholders are protected from any

manipulations. The audited balance sheet of the company is the basis on which the potential

investors of the company decide whether or not to invest in the shares of the company. The

auditor is responsible to act in the best interest of the shareholders of the company and determine

whether the financial reports of the company is showing true and fair view or not. The auditors

of the company are to also ensure that the there is no omission or manipulation in the financial

statement of the company.

Question 2

Financial Statement Analysis

As per the case study provided in the assignment, the annual reports of Air New Zealand

is given for the year 2016. The analysis of the financial statement is to be done, on the basis

which the questions given in the assignment is to be solved.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING FINANCE FOR EXECUTIVE

As shown in the financial report of the company, the annual report of the company is

audited by Deloitte which is an auditing firm engaged in the auditing and other non-auditing

services which it can provide to other companies. As per the Deloitte, all the matters which are

presented in the financial statement of Air New Zealand for the year 2016 are shown and

presented fairly as per the requirements of New Zealand Equivalents to the Financial reporting

standard and International financial reporting standards. All components of the financial

statements are fairly represented as per the opinion of the auditor (William Jr, Glover and Prawitt

2016). Deloitte has issued an unqualified report for the company and believes that the financial

statements are fairly represented following all relevant New Zealand standards on accounting.

The auditor do not take any responsibility about the securities and control over the group

financial statement.

A qualified Audit opinion refers to the opinion which is issued by an auditor when there

is some material misstatement in the financial reports of the company. Such type of report might

also be given if the there is some restriction on the access of information by the management of

the company (Blandón and Bosch 2013).

The net profit as shown in the annual reports of the company for 2016 is $ 463 million

and the figure of cash from operation is shown at $ 1074 million. The cash from operation which

is shown in the cash flow statements is greater than the net profit figure which is shown in the

profit and loss statement of the company. The major reason for the difference in the figure which

is stated as net profit and cash flow from operations can be attributed to certain transaction which

are treated differently in case of both the statements (Wu and Shen 2013). There are certain items

which are to be deducted in order to arrive at total revenue and certain non-cash items which are

needed to be added back in order get the cash revenue of the company. Such Items includes

Depreciation expenses, impairment losses and similar other expenses of such nature.

As provided in the annual reports, the directors of the company which are members of the

audit committee are Tony Crater, Jan Dawson and Jonathan Mason. The audit committee main

function is to supervise financial reporting framework and review various disclosures and

treatments. The audit committee of any company is the major committee which have a

significant role in the management of the company (Aldamen et al. 2012). The primary

responsibility of the committee is to look after the audit process, framework for reporting,

various legal regulations which are followed by the company

ACCOUNTING FINANCE FOR EXECUTIVE

As shown in the financial report of the company, the annual report of the company is

audited by Deloitte which is an auditing firm engaged in the auditing and other non-auditing

services which it can provide to other companies. As per the Deloitte, all the matters which are

presented in the financial statement of Air New Zealand for the year 2016 are shown and

presented fairly as per the requirements of New Zealand Equivalents to the Financial reporting

standard and International financial reporting standards. All components of the financial

statements are fairly represented as per the opinion of the auditor (William Jr, Glover and Prawitt

2016). Deloitte has issued an unqualified report for the company and believes that the financial

statements are fairly represented following all relevant New Zealand standards on accounting.

The auditor do not take any responsibility about the securities and control over the group

financial statement.

A qualified Audit opinion refers to the opinion which is issued by an auditor when there

is some material misstatement in the financial reports of the company. Such type of report might

also be given if the there is some restriction on the access of information by the management of

the company (Blandón and Bosch 2013).

The net profit as shown in the annual reports of the company for 2016 is $ 463 million

and the figure of cash from operation is shown at $ 1074 million. The cash from operation which

is shown in the cash flow statements is greater than the net profit figure which is shown in the

profit and loss statement of the company. The major reason for the difference in the figure which

is stated as net profit and cash flow from operations can be attributed to certain transaction which

are treated differently in case of both the statements (Wu and Shen 2013). There are certain items

which are to be deducted in order to arrive at total revenue and certain non-cash items which are

needed to be added back in order get the cash revenue of the company. Such Items includes

Depreciation expenses, impairment losses and similar other expenses of such nature.

As provided in the annual reports, the directors of the company which are members of the

audit committee are Tony Crater, Jan Dawson and Jonathan Mason. The audit committee main

function is to supervise financial reporting framework and review various disclosures and

treatments. The audit committee of any company is the major committee which have a

significant role in the management of the company (Aldamen et al. 2012). The primary

responsibility of the committee is to look after the audit process, framework for reporting,

various legal regulations which are followed by the company

5

ACCOUNTING FINANCE FOR EXECUTIVE

The directors have identified letter of credit and performance of bonds which is of the

amount of $ 33 million as contingent liability of the business. This is disclosed in the notes to

accounts of the company. Contingent Liability can be defined as certain transactions which are

uncertain in nature that might occur in the near future and which cannot be measured reliably in

current circumstances (Bova 2016).

ACCOUNTING FINANCE FOR EXECUTIVE

The directors have identified letter of credit and performance of bonds which is of the

amount of $ 33 million as contingent liability of the business. This is disclosed in the notes to

accounts of the company. Contingent Liability can be defined as certain transactions which are

uncertain in nature that might occur in the near future and which cannot be measured reliably in

current circumstances (Bova 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING FINANCE FOR EXECUTIVE

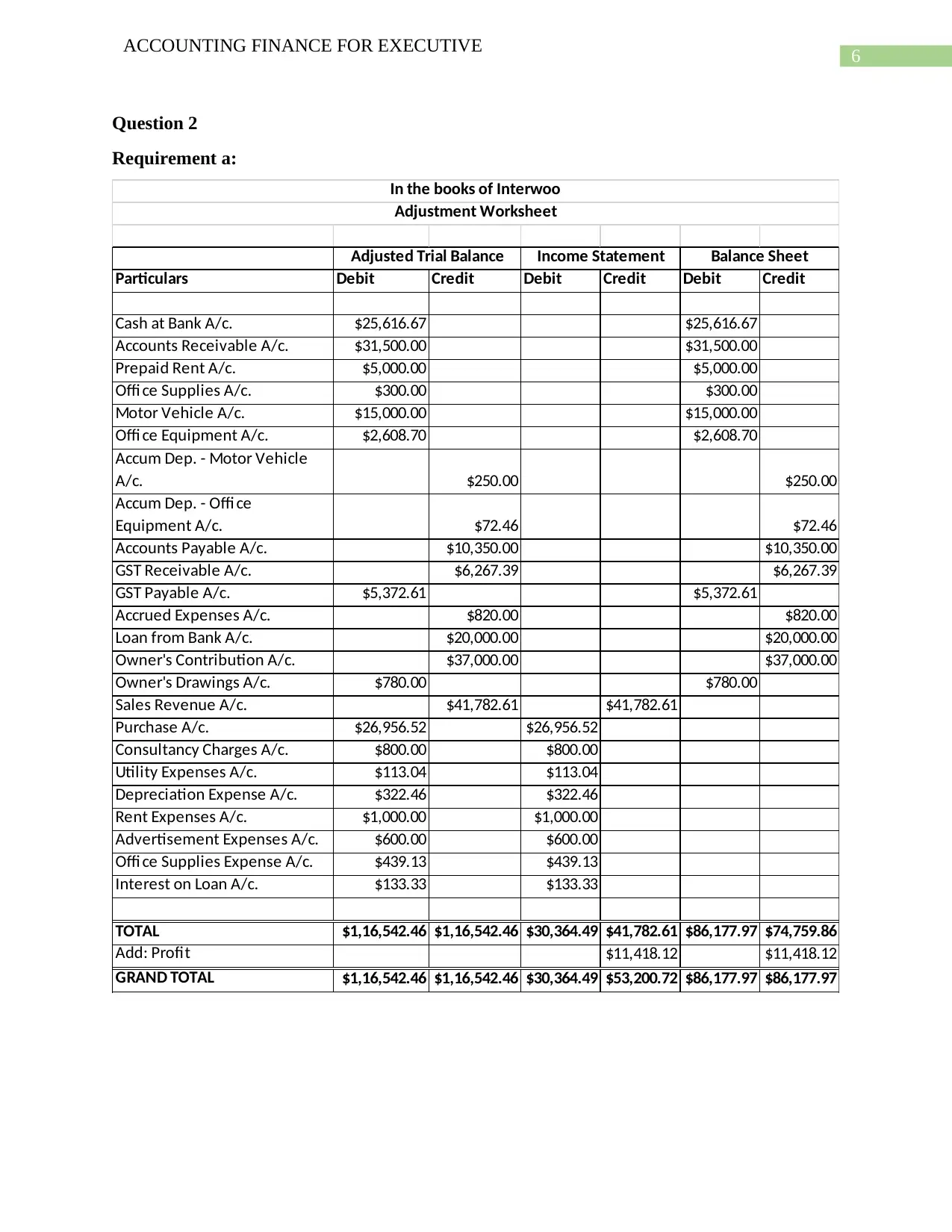

Question 2

Requirement a:

Particulars Debit Credit Debit Credit Debit Credit

Cash at Bank A/c. $25,616.67 $25,616.67

Accounts Receivable A/c. $31,500.00 $31,500.00

Prepaid Rent A/c. $5,000.00 $5,000.00

Offi ce Supplies A/c. $300.00 $300.00

Motor Vehicle A/c. $15,000.00 $15,000.00

Offi ce Equipment A/c. $2,608.70 $2,608.70

Accum Dep. - Motor Vehicle

A/c. $250.00 $250.00

Accum Dep. - Offi ce

Equipment A/c. $72.46 $72.46

Accounts Payable A/c. $10,350.00 $10,350.00

GST Receivable A/c. $6,267.39 $6,267.39

GST Payable A/c. $5,372.61 $5,372.61

Accrued Expenses A/c. $820.00 $820.00

Loan from Bank A/c. $20,000.00 $20,000.00

Owner's Contribution A/c. $37,000.00 $37,000.00

Owner's Drawings A/c. $780.00 $780.00

Sales Revenue A/c. $41,782.61 $41,782.61

Purchase A/c. $26,956.52 $26,956.52

Consultancy Charges A/c. $800.00 $800.00

Utility Expenses A/c. $113.04 $113.04

Depreciation Expense A/c. $322.46 $322.46

Rent Expenses A/c. $1,000.00 $1,000.00

Advertisement Expenses A/c. $600.00 $600.00

Offi ce Supplies Expense A/c. $439.13 $439.13

Interest on Loan A/c. $133.33 $133.33

TOTAL $1,16,542.46 $1,16,542.46 $30,364.49 $41,782.61 $86,177.97 $74,759.86

Add: Profit $11,418.12 $11,418.12

GRAND TOTAL $1,16,542.46 $1,16,542.46 $30,364.49 $53,200.72 $86,177.97 $86,177.97

Adjusted Trial Balance Income Statement Balance Sheet

In the books of Interwoo

Adjustment Worksheet

ACCOUNTING FINANCE FOR EXECUTIVE

Question 2

Requirement a:

Particulars Debit Credit Debit Credit Debit Credit

Cash at Bank A/c. $25,616.67 $25,616.67

Accounts Receivable A/c. $31,500.00 $31,500.00

Prepaid Rent A/c. $5,000.00 $5,000.00

Offi ce Supplies A/c. $300.00 $300.00

Motor Vehicle A/c. $15,000.00 $15,000.00

Offi ce Equipment A/c. $2,608.70 $2,608.70

Accum Dep. - Motor Vehicle

A/c. $250.00 $250.00

Accum Dep. - Offi ce

Equipment A/c. $72.46 $72.46

Accounts Payable A/c. $10,350.00 $10,350.00

GST Receivable A/c. $6,267.39 $6,267.39

GST Payable A/c. $5,372.61 $5,372.61

Accrued Expenses A/c. $820.00 $820.00

Loan from Bank A/c. $20,000.00 $20,000.00

Owner's Contribution A/c. $37,000.00 $37,000.00

Owner's Drawings A/c. $780.00 $780.00

Sales Revenue A/c. $41,782.61 $41,782.61

Purchase A/c. $26,956.52 $26,956.52

Consultancy Charges A/c. $800.00 $800.00

Utility Expenses A/c. $113.04 $113.04

Depreciation Expense A/c. $322.46 $322.46

Rent Expenses A/c. $1,000.00 $1,000.00

Advertisement Expenses A/c. $600.00 $600.00

Offi ce Supplies Expense A/c. $439.13 $439.13

Interest on Loan A/c. $133.33 $133.33

TOTAL $1,16,542.46 $1,16,542.46 $30,364.49 $41,782.61 $86,177.97 $74,759.86

Add: Profit $11,418.12 $11,418.12

GRAND TOTAL $1,16,542.46 $1,16,542.46 $30,364.49 $53,200.72 $86,177.97 $86,177.97

Adjusted Trial Balance Income Statement Balance Sheet

In the books of Interwoo

Adjustment Worksheet

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING FINANCE FOR EXECUTIVE

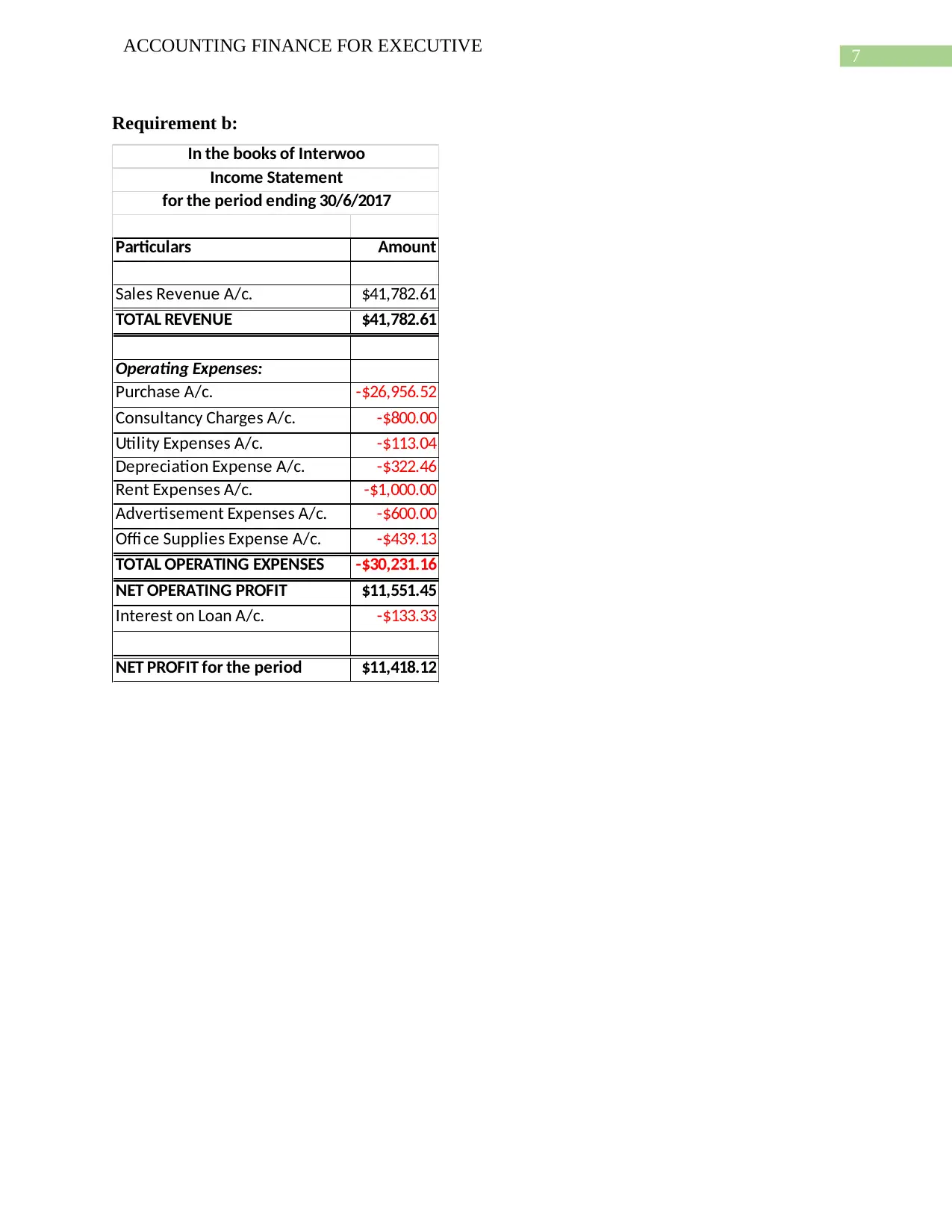

Requirement b:

Particulars Amount

Sales Revenue A/c. $41,782.61

TOTAL REVENUE $41,782.61

Operating Expenses:

Purchase A/c. -$26,956.52

Consultancy Charges A/c. -$800.00

Utility Expenses A/c. -$113.04

Depreciation Expense A/c. -$322.46

Rent Expenses A/c. -$1,000.00

Advertisement Expenses A/c. -$600.00

Offi ce Supplies Expense A/c. -$439.13

TOTAL OPERATING EXPENSES -$30,231.16

NET OPERATING PROFIT $11,551.45

Interest on Loan A/c. -$133.33

NET PROFIT for the period $11,418.12

In the books of Interwoo

Income Statement

for the period ending 30/6/2017

ACCOUNTING FINANCE FOR EXECUTIVE

Requirement b:

Particulars Amount

Sales Revenue A/c. $41,782.61

TOTAL REVENUE $41,782.61

Operating Expenses:

Purchase A/c. -$26,956.52

Consultancy Charges A/c. -$800.00

Utility Expenses A/c. -$113.04

Depreciation Expense A/c. -$322.46

Rent Expenses A/c. -$1,000.00

Advertisement Expenses A/c. -$600.00

Offi ce Supplies Expense A/c. -$439.13

TOTAL OPERATING EXPENSES -$30,231.16

NET OPERATING PROFIT $11,551.45

Interest on Loan A/c. -$133.33

NET PROFIT for the period $11,418.12

In the books of Interwoo

Income Statement

for the period ending 30/6/2017

8

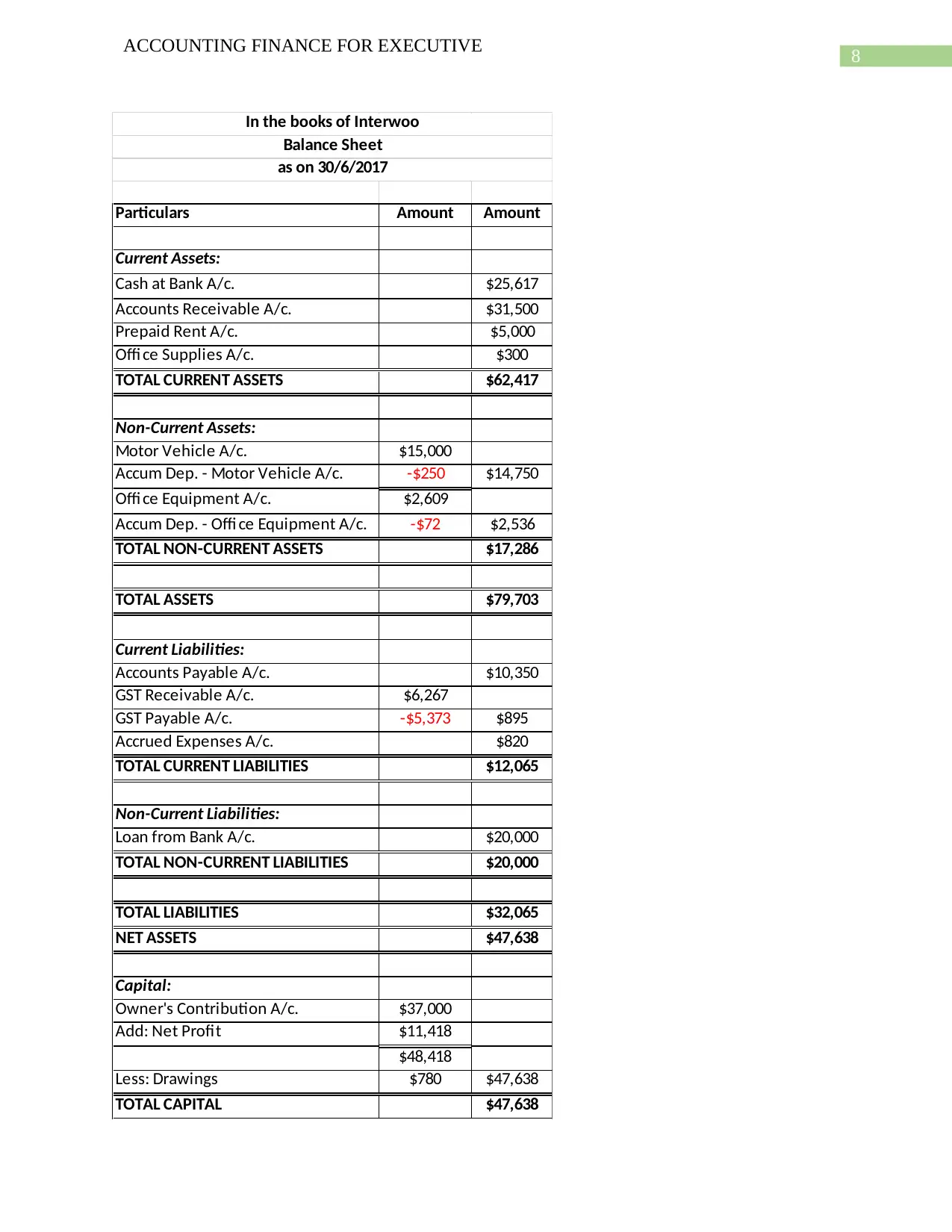

ACCOUNTING FINANCE FOR EXECUTIVE

Particulars Amount Amount

Current Assets:

Cash at Bank A/c. $25,617

Accounts Receivable A/c. $31,500

Prepaid Rent A/c. $5,000

Offi ce Supplies A/c. $300

TOTAL CURRENT ASSETS $62,417

Non-Current Assets:

Motor Vehicle A/c. $15,000

Accum Dep. - Motor Vehicle A/c. -$250 $14,750

Offi ce Equipment A/c. $2,609

Accum Dep. - Offi ce Equipment A/c. -$72 $2,536

TOTAL NON-CURRENT ASSETS $17,286

TOTAL ASSETS $79,703

Current Liabilities:

Accounts Payable A/c. $10,350

GST Receivable A/c. $6,267

GST Payable A/c. -$5,373 $895

Accrued Expenses A/c. $820

TOTAL CURRENT LIABILITIES $12,065

Non-Current Liabilities:

Loan from Bank A/c. $20,000

TOTAL NON-CURRENT LIABILITIES $20,000

TOTAL LIABILITIES $32,065

NET ASSETS $47,638

Capital:

Owner's Contribution A/c. $37,000

Add: Net Profit $11,418

$48,418

Less: Drawings $780 $47,638

TOTAL CAPITAL $47,638

In the books of Interwoo

Balance Sheet

as on 30/6/2017

ACCOUNTING FINANCE FOR EXECUTIVE

Particulars Amount Amount

Current Assets:

Cash at Bank A/c. $25,617

Accounts Receivable A/c. $31,500

Prepaid Rent A/c. $5,000

Offi ce Supplies A/c. $300

TOTAL CURRENT ASSETS $62,417

Non-Current Assets:

Motor Vehicle A/c. $15,000

Accum Dep. - Motor Vehicle A/c. -$250 $14,750

Offi ce Equipment A/c. $2,609

Accum Dep. - Offi ce Equipment A/c. -$72 $2,536

TOTAL NON-CURRENT ASSETS $17,286

TOTAL ASSETS $79,703

Current Liabilities:

Accounts Payable A/c. $10,350

GST Receivable A/c. $6,267

GST Payable A/c. -$5,373 $895

Accrued Expenses A/c. $820

TOTAL CURRENT LIABILITIES $12,065

Non-Current Liabilities:

Loan from Bank A/c. $20,000

TOTAL NON-CURRENT LIABILITIES $20,000

TOTAL LIABILITIES $32,065

NET ASSETS $47,638

Capital:

Owner's Contribution A/c. $37,000

Add: Net Profit $11,418

$48,418

Less: Drawings $780 $47,638

TOTAL CAPITAL $47,638

In the books of Interwoo

Balance Sheet

as on 30/6/2017

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING FINANCE FOR EXECUTIVE

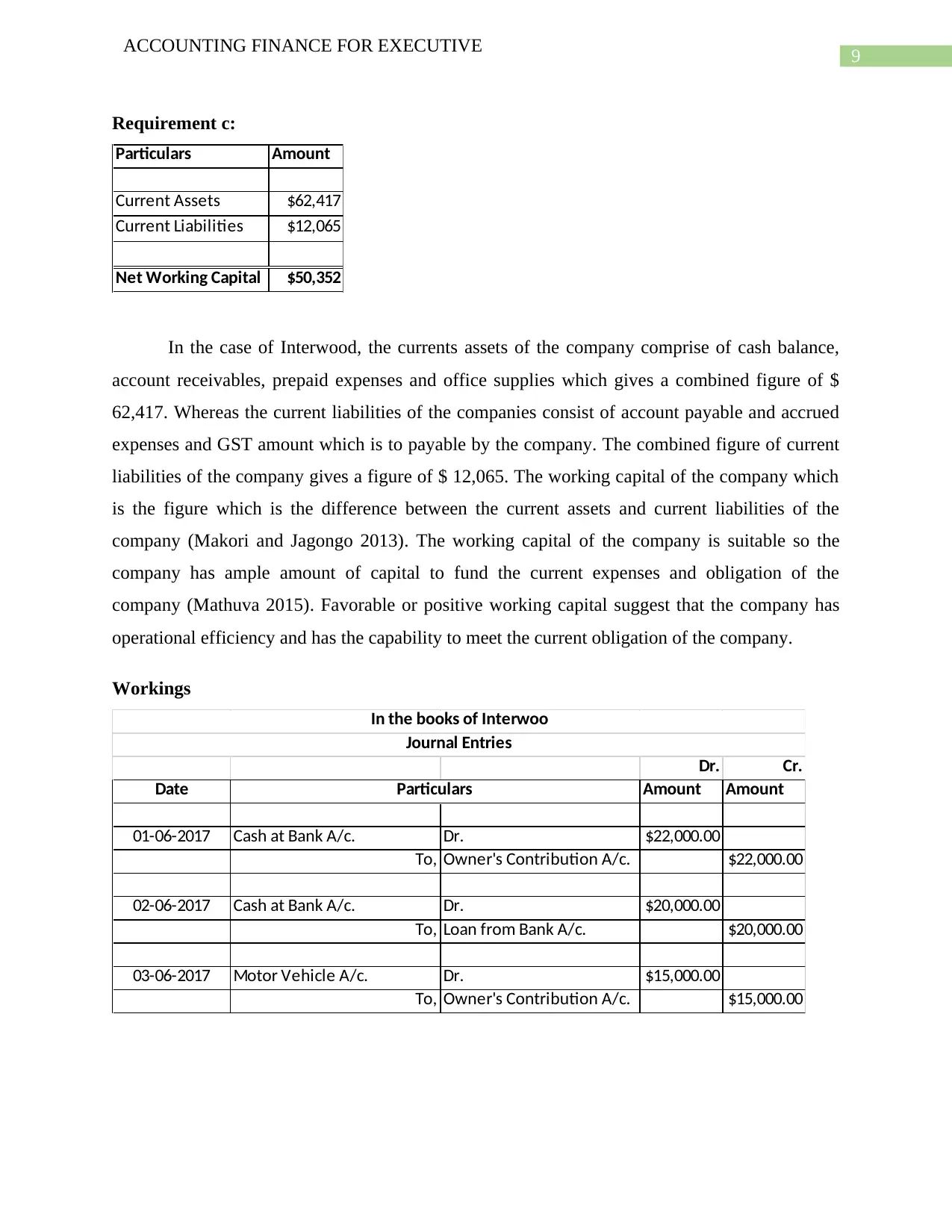

Requirement c:

Particulars Amount

Current Assets $62,417

Current Liabilities $12,065

Net Working Capital $50,352

In the case of Interwood, the currents assets of the company comprise of cash balance,

account receivables, prepaid expenses and office supplies which gives a combined figure of $

62,417. Whereas the current liabilities of the companies consist of account payable and accrued

expenses and GST amount which is to payable by the company. The combined figure of current

liabilities of the company gives a figure of $ 12,065. The working capital of the company which

is the figure which is the difference between the current assets and current liabilities of the

company (Makori and Jagongo 2013). The working capital of the company is suitable so the

company has ample amount of capital to fund the current expenses and obligation of the

company (Mathuva 2015). Favorable or positive working capital suggest that the company has

operational efficiency and has the capability to meet the current obligation of the company.

Workings

Dr. Cr.

Date Amount Amount

01-06-2017 Cash at Bank A/c. Dr. $22,000.00

To, Owner's Contribution A/c. $22,000.00

02-06-2017 Cash at Bank A/c. Dr. $20,000.00

To, Loan from Bank A/c. $20,000.00

03-06-2017 Motor Vehicle A/c. Dr. $15,000.00

To, Owner's Contribution A/c. $15,000.00

Particulars

In the books of Interwoo

Journal Entries

ACCOUNTING FINANCE FOR EXECUTIVE

Requirement c:

Particulars Amount

Current Assets $62,417

Current Liabilities $12,065

Net Working Capital $50,352

In the case of Interwood, the currents assets of the company comprise of cash balance,

account receivables, prepaid expenses and office supplies which gives a combined figure of $

62,417. Whereas the current liabilities of the companies consist of account payable and accrued

expenses and GST amount which is to payable by the company. The combined figure of current

liabilities of the company gives a figure of $ 12,065. The working capital of the company which

is the figure which is the difference between the current assets and current liabilities of the

company (Makori and Jagongo 2013). The working capital of the company is suitable so the

company has ample amount of capital to fund the current expenses and obligation of the

company (Mathuva 2015). Favorable or positive working capital suggest that the company has

operational efficiency and has the capability to meet the current obligation of the company.

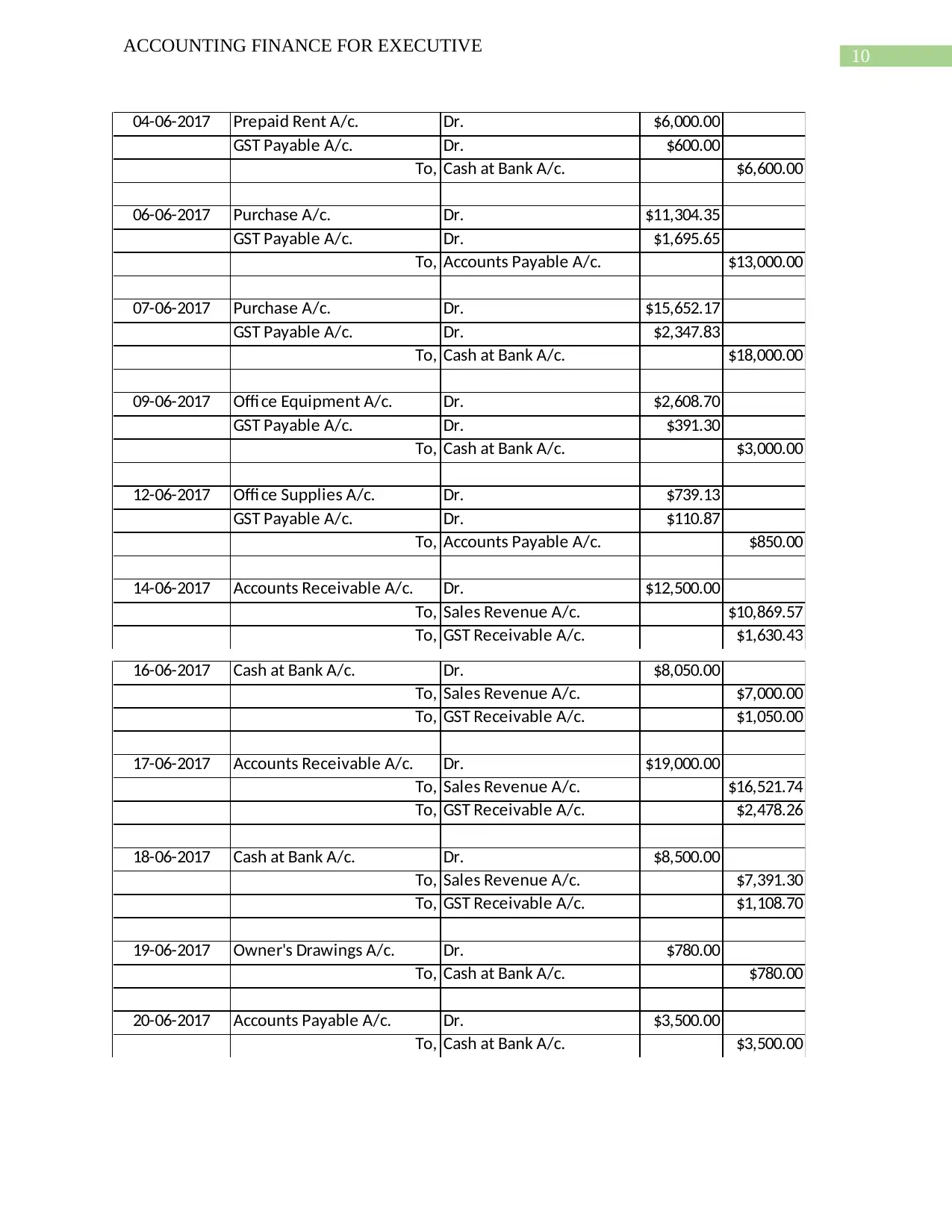

Workings

Dr. Cr.

Date Amount Amount

01-06-2017 Cash at Bank A/c. Dr. $22,000.00

To, Owner's Contribution A/c. $22,000.00

02-06-2017 Cash at Bank A/c. Dr. $20,000.00

To, Loan from Bank A/c. $20,000.00

03-06-2017 Motor Vehicle A/c. Dr. $15,000.00

To, Owner's Contribution A/c. $15,000.00

Particulars

In the books of Interwoo

Journal Entries

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING FINANCE FOR EXECUTIVE

04-06-2017 Prepaid Rent A/c. Dr. $6,000.00

GST Payable A/c. Dr. $600.00

To, Cash at Bank A/c. $6,600.00

06-06-2017 Purchase A/c. Dr. $11,304.35

GST Payable A/c. Dr. $1,695.65

To, Accounts Payable A/c. $13,000.00

07-06-2017 Purchase A/c. Dr. $15,652.17

GST Payable A/c. Dr. $2,347.83

To, Cash at Bank A/c. $18,000.00

09-06-2017 Offi ce Equipment A/c. Dr. $2,608.70

GST Payable A/c. Dr. $391.30

To, Cash at Bank A/c. $3,000.00

12-06-2017 Offi ce Supplies A/c. Dr. $739.13

GST Payable A/c. Dr. $110.87

To, Accounts Payable A/c. $850.00

14-06-2017 Accounts Receivable A/c. Dr. $12,500.00

To, Sales Revenue A/c. $10,869.57

To, GST Receivable A/c. $1,630.43

16-06-2017 Cash at Bank A/c. Dr. $8,050.00

To, Sales Revenue A/c. $7,000.00

To, GST Receivable A/c. $1,050.00

17-06-2017 Accounts Receivable A/c. Dr. $19,000.00

To, Sales Revenue A/c. $16,521.74

To, GST Receivable A/c. $2,478.26

18-06-2017 Cash at Bank A/c. Dr. $8,500.00

To, Sales Revenue A/c. $7,391.30

To, GST Receivable A/c. $1,108.70

19-06-2017 Owner's Drawings A/c. Dr. $780.00

To, Cash at Bank A/c. $780.00

20-06-2017 Accounts Payable A/c. Dr. $3,500.00

To, Cash at Bank A/c. $3,500.00

ACCOUNTING FINANCE FOR EXECUTIVE

04-06-2017 Prepaid Rent A/c. Dr. $6,000.00

GST Payable A/c. Dr. $600.00

To, Cash at Bank A/c. $6,600.00

06-06-2017 Purchase A/c. Dr. $11,304.35

GST Payable A/c. Dr. $1,695.65

To, Accounts Payable A/c. $13,000.00

07-06-2017 Purchase A/c. Dr. $15,652.17

GST Payable A/c. Dr. $2,347.83

To, Cash at Bank A/c. $18,000.00

09-06-2017 Offi ce Equipment A/c. Dr. $2,608.70

GST Payable A/c. Dr. $391.30

To, Cash at Bank A/c. $3,000.00

12-06-2017 Offi ce Supplies A/c. Dr. $739.13

GST Payable A/c. Dr. $110.87

To, Accounts Payable A/c. $850.00

14-06-2017 Accounts Receivable A/c. Dr. $12,500.00

To, Sales Revenue A/c. $10,869.57

To, GST Receivable A/c. $1,630.43

16-06-2017 Cash at Bank A/c. Dr. $8,050.00

To, Sales Revenue A/c. $7,000.00

To, GST Receivable A/c. $1,050.00

17-06-2017 Accounts Receivable A/c. Dr. $19,000.00

To, Sales Revenue A/c. $16,521.74

To, GST Receivable A/c. $2,478.26

18-06-2017 Cash at Bank A/c. Dr. $8,500.00

To, Sales Revenue A/c. $7,391.30

To, GST Receivable A/c. $1,108.70

19-06-2017 Owner's Drawings A/c. Dr. $780.00

To, Cash at Bank A/c. $780.00

20-06-2017 Accounts Payable A/c. Dr. $3,500.00

To, Cash at Bank A/c. $3,500.00

11

ACCOUNTING FINANCE FOR EXECUTIVE

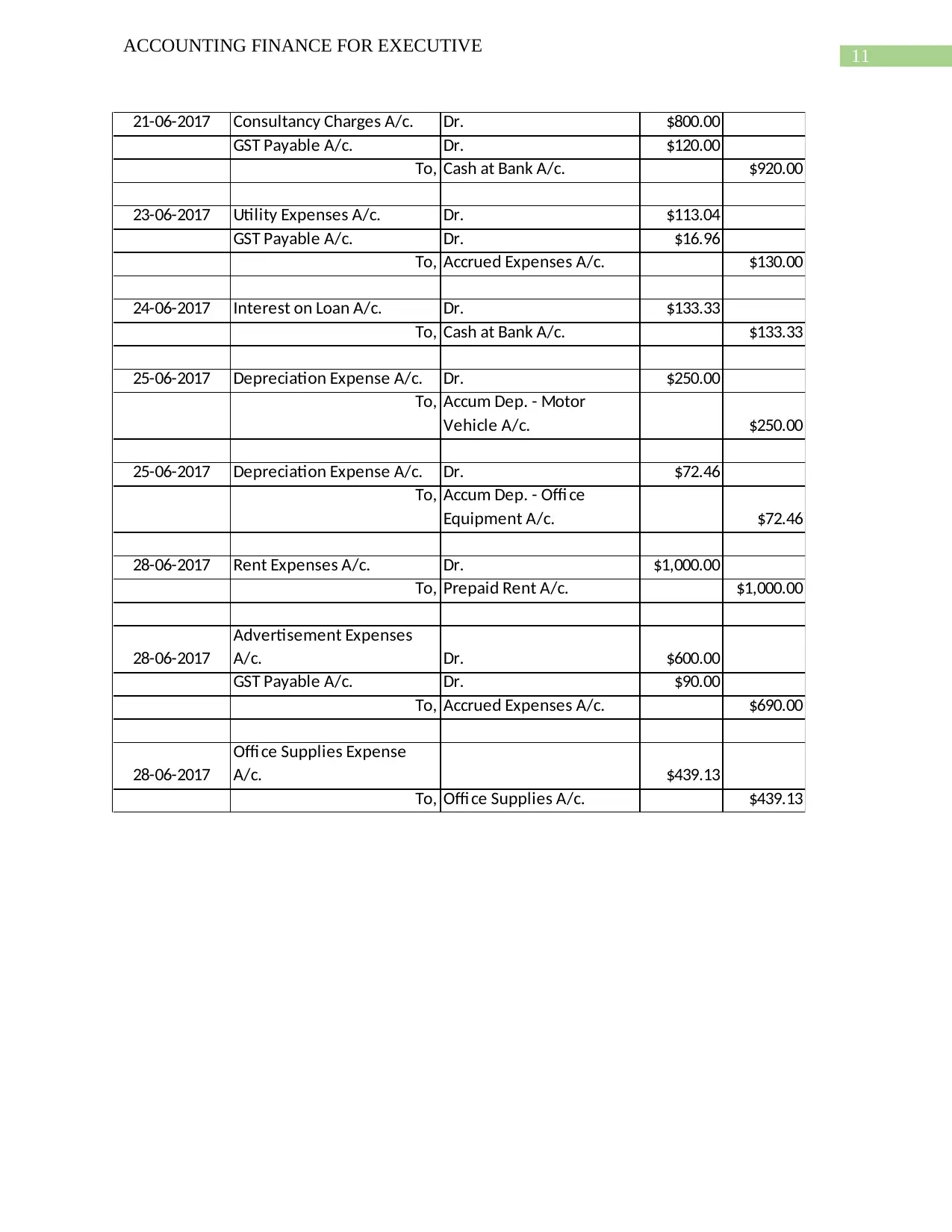

21-06-2017 Consultancy Charges A/c. Dr. $800.00

GST Payable A/c. Dr. $120.00

To, Cash at Bank A/c. $920.00

23-06-2017 Utility Expenses A/c. Dr. $113.04

GST Payable A/c. Dr. $16.96

To, Accrued Expenses A/c. $130.00

24-06-2017 Interest on Loan A/c. Dr. $133.33

To, Cash at Bank A/c. $133.33

25-06-2017 Depreciation Expense A/c. Dr. $250.00

To, Accum Dep. - Motor

Vehicle A/c. $250.00

25-06-2017 Depreciation Expense A/c. Dr. $72.46

To, Accum Dep. - Offi ce

Equipment A/c. $72.46

28-06-2017 Rent Expenses A/c. Dr. $1,000.00

To, Prepaid Rent A/c. $1,000.00

28-06-2017

Advertisement Expenses

A/c. Dr. $600.00

GST Payable A/c. Dr. $90.00

To, Accrued Expenses A/c. $690.00

28-06-2017

Offi ce Supplies Expense

A/c. $439.13

To, Offi ce Supplies A/c. $439.13

ACCOUNTING FINANCE FOR EXECUTIVE

21-06-2017 Consultancy Charges A/c. Dr. $800.00

GST Payable A/c. Dr. $120.00

To, Cash at Bank A/c. $920.00

23-06-2017 Utility Expenses A/c. Dr. $113.04

GST Payable A/c. Dr. $16.96

To, Accrued Expenses A/c. $130.00

24-06-2017 Interest on Loan A/c. Dr. $133.33

To, Cash at Bank A/c. $133.33

25-06-2017 Depreciation Expense A/c. Dr. $250.00

To, Accum Dep. - Motor

Vehicle A/c. $250.00

25-06-2017 Depreciation Expense A/c. Dr. $72.46

To, Accum Dep. - Offi ce

Equipment A/c. $72.46

28-06-2017 Rent Expenses A/c. Dr. $1,000.00

To, Prepaid Rent A/c. $1,000.00

28-06-2017

Advertisement Expenses

A/c. Dr. $600.00

GST Payable A/c. Dr. $90.00

To, Accrued Expenses A/c. $690.00

28-06-2017

Offi ce Supplies Expense

A/c. $439.13

To, Offi ce Supplies A/c. $439.13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.