UGB163 Accounting and Finance: Financial Performance Analysis Report

VerifiedAdded on 2023/02/13

|25

|4329

|78

Homework Assignment

AI Summary

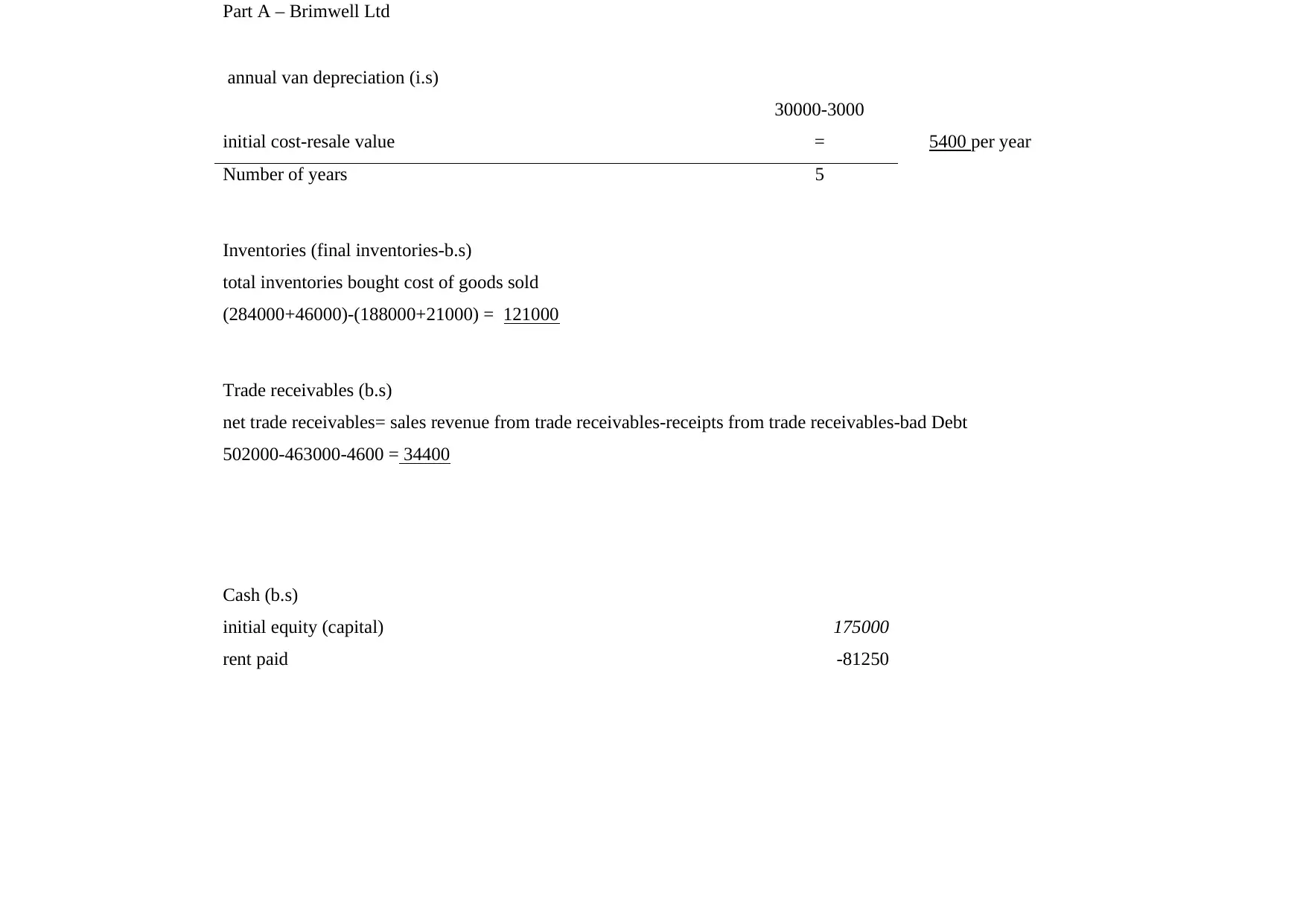

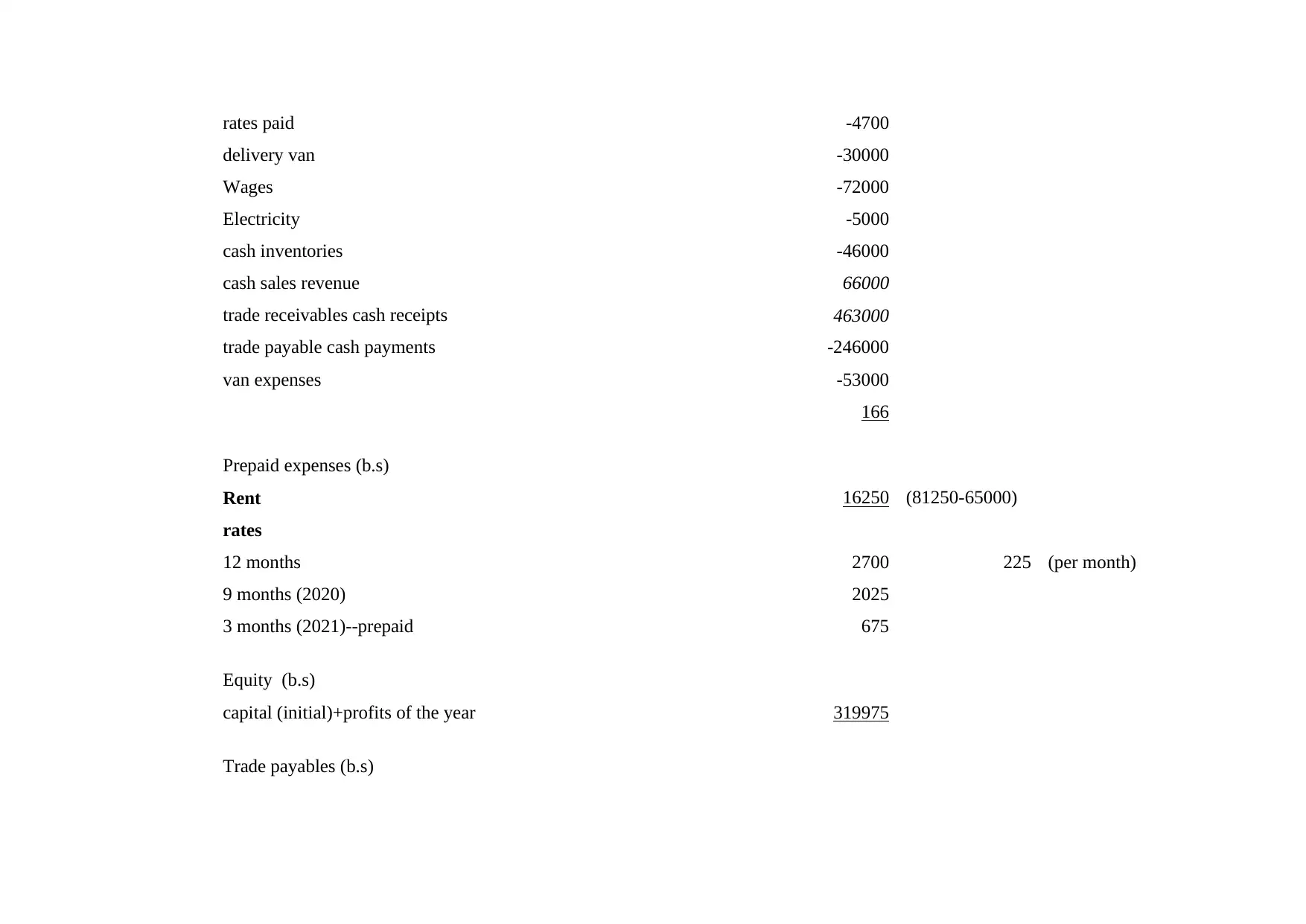

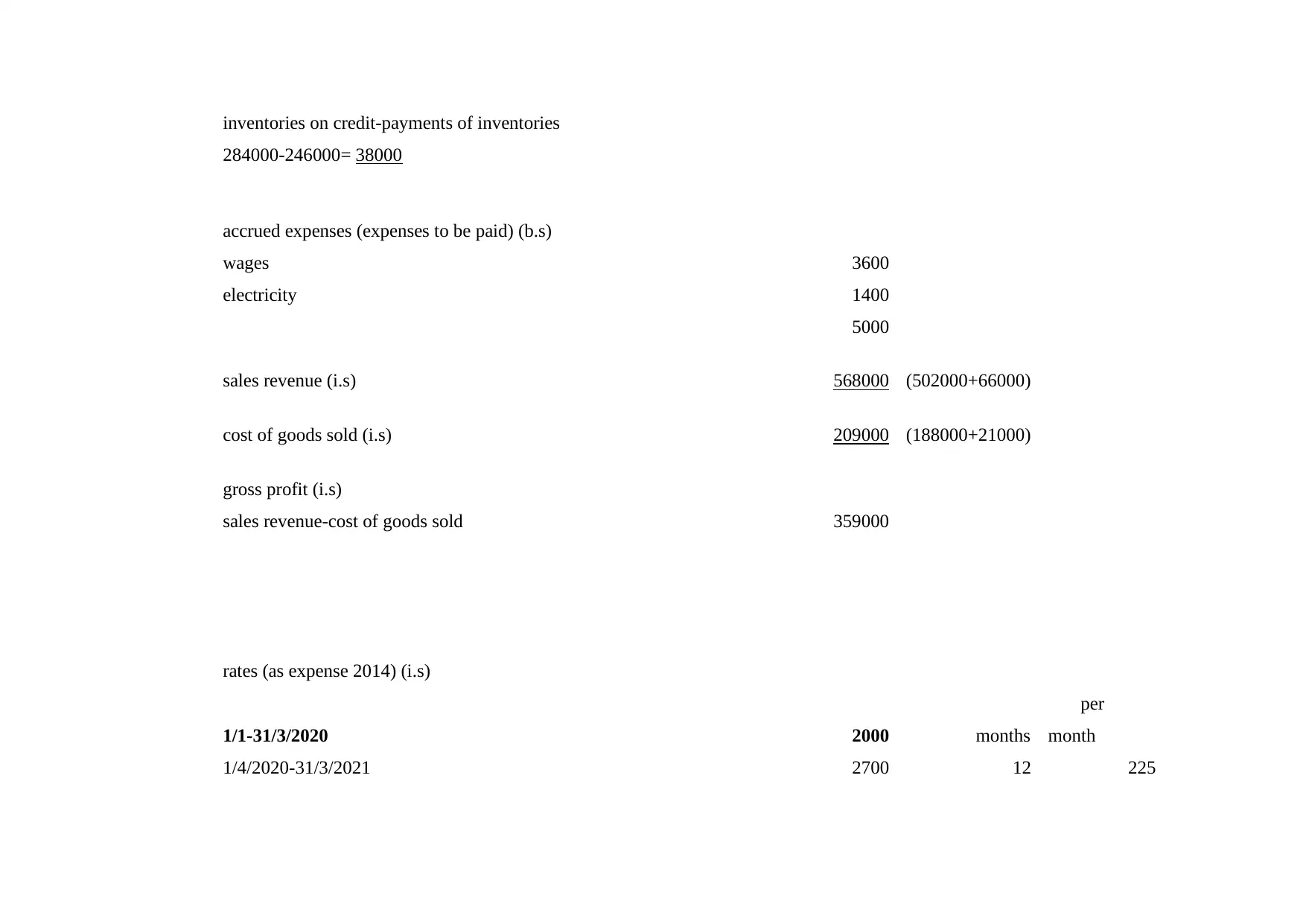

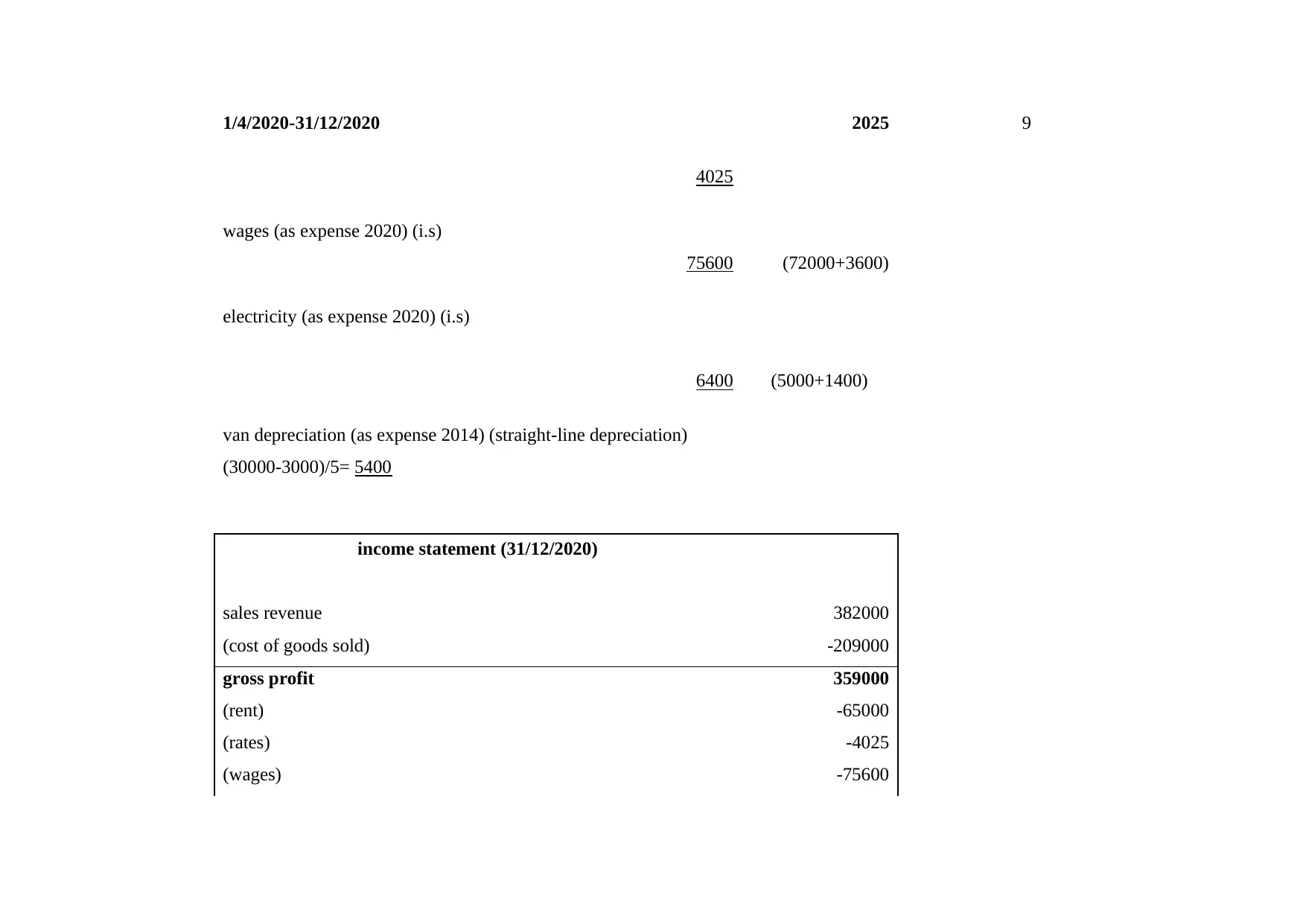

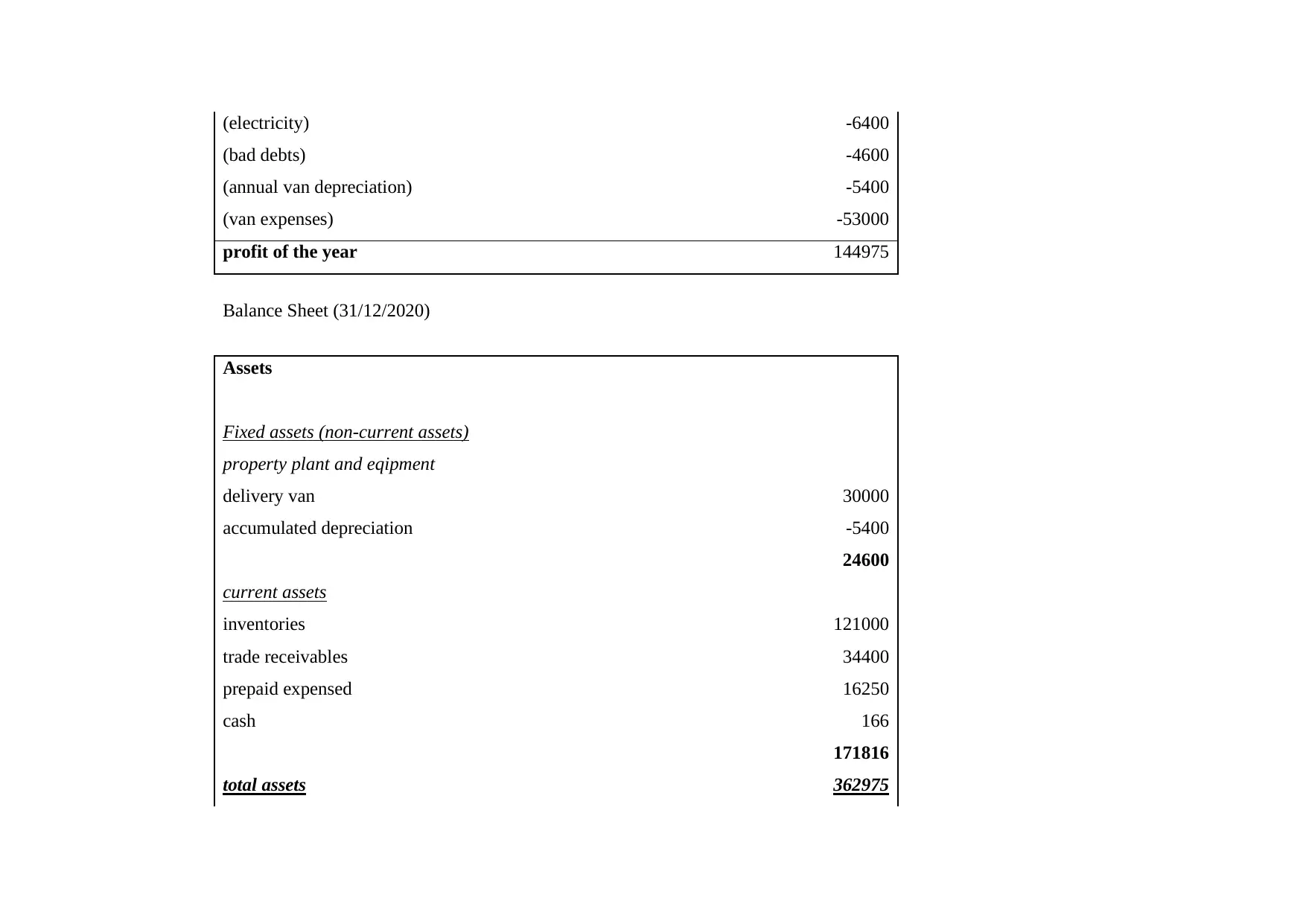

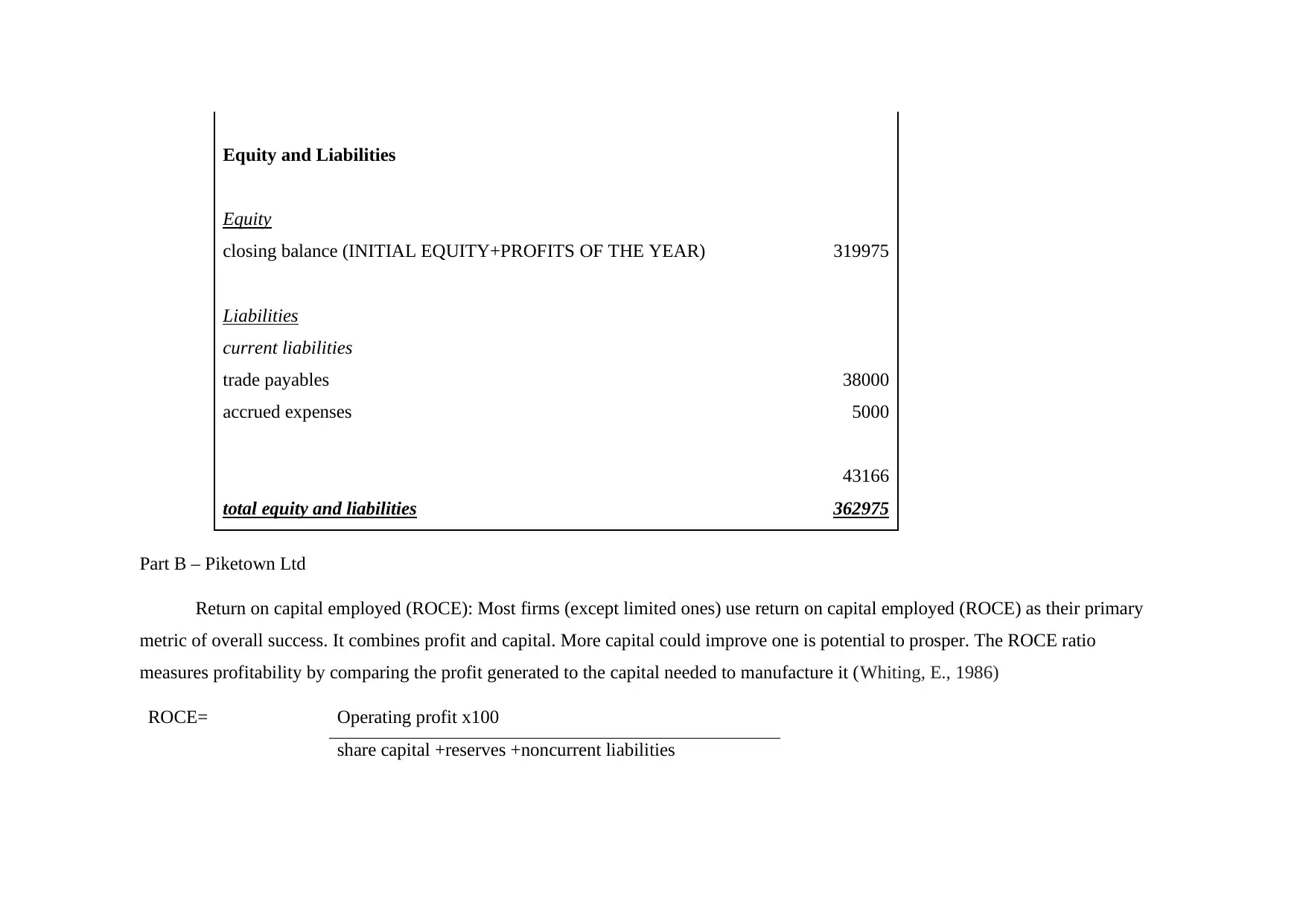

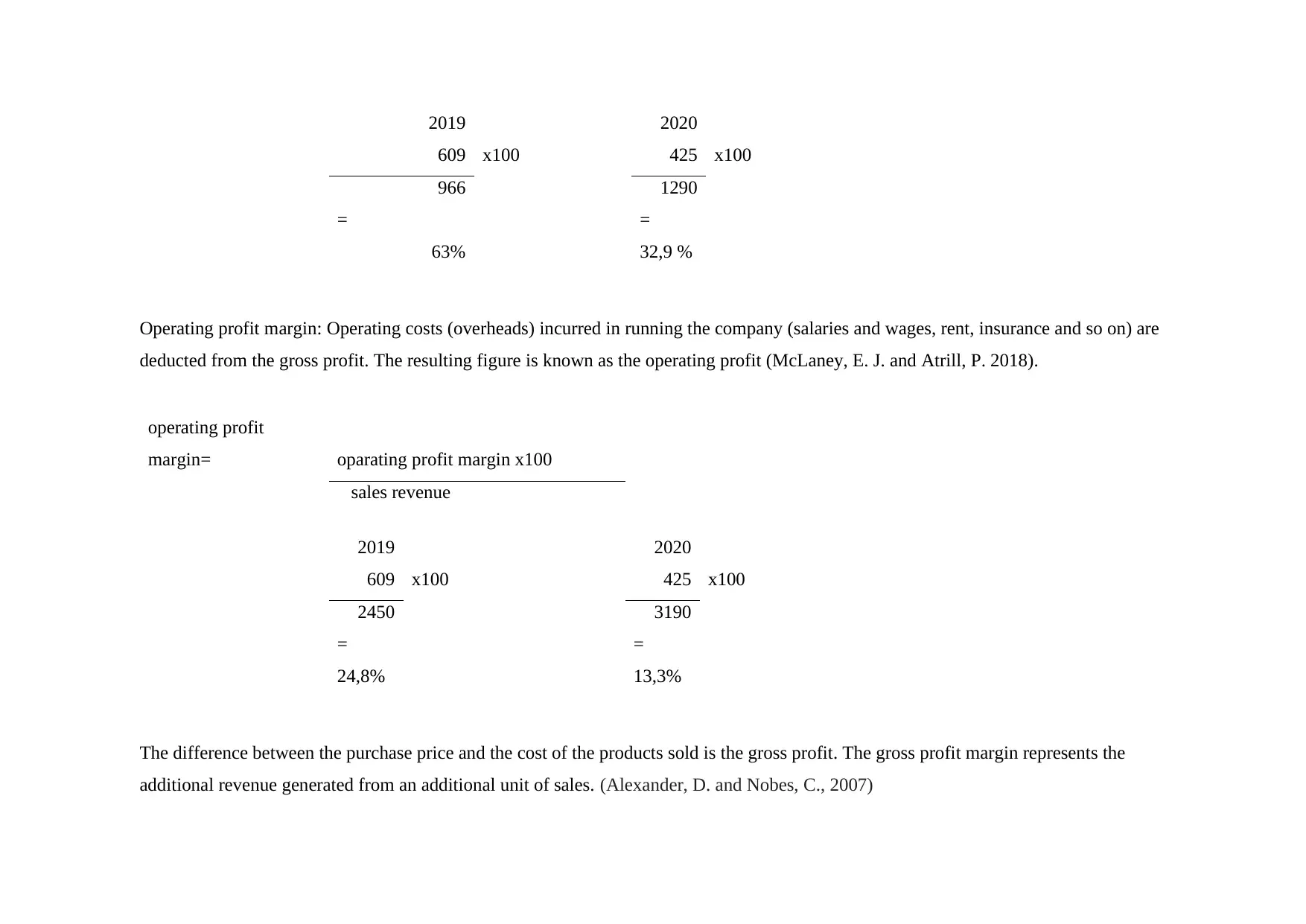

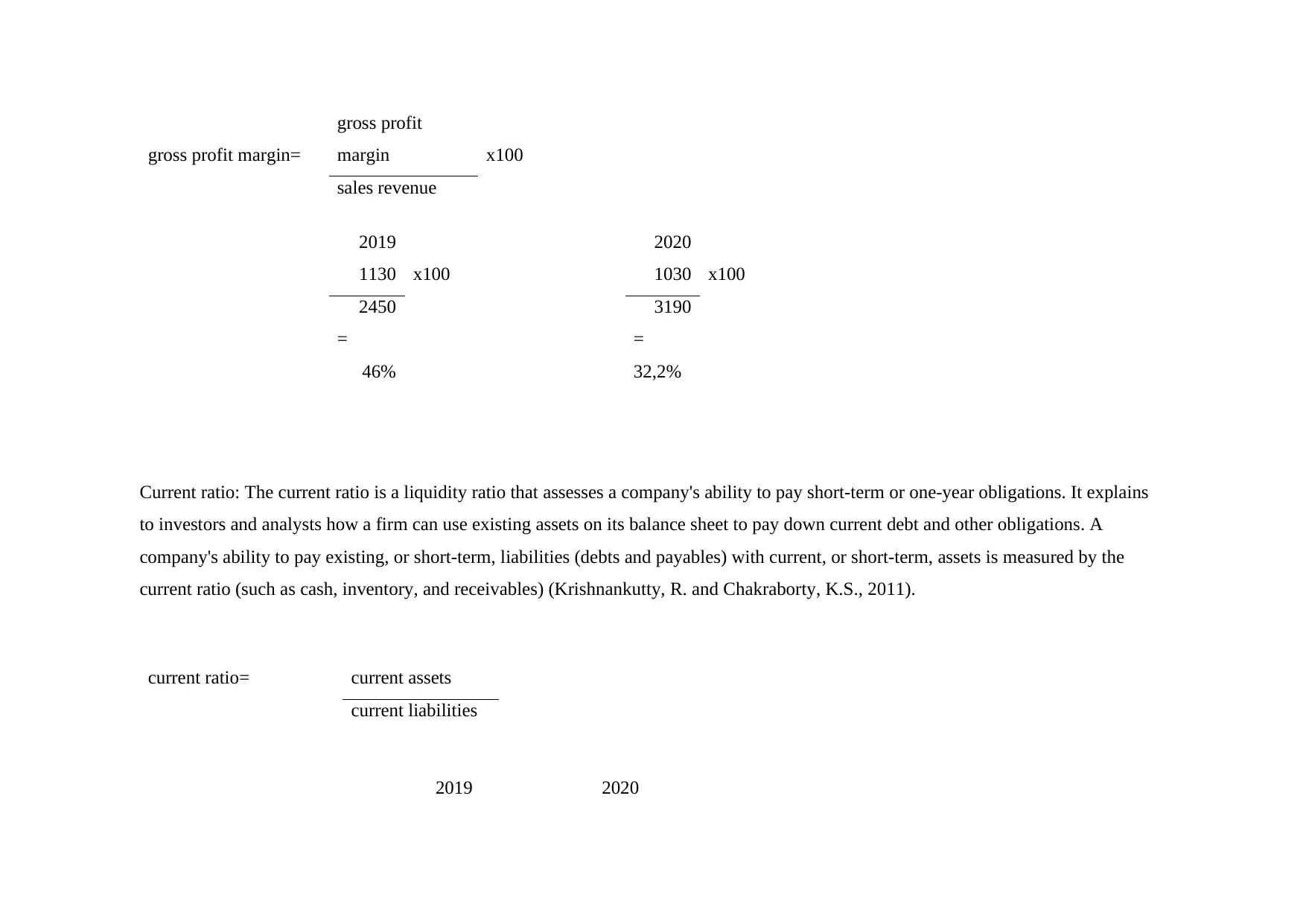

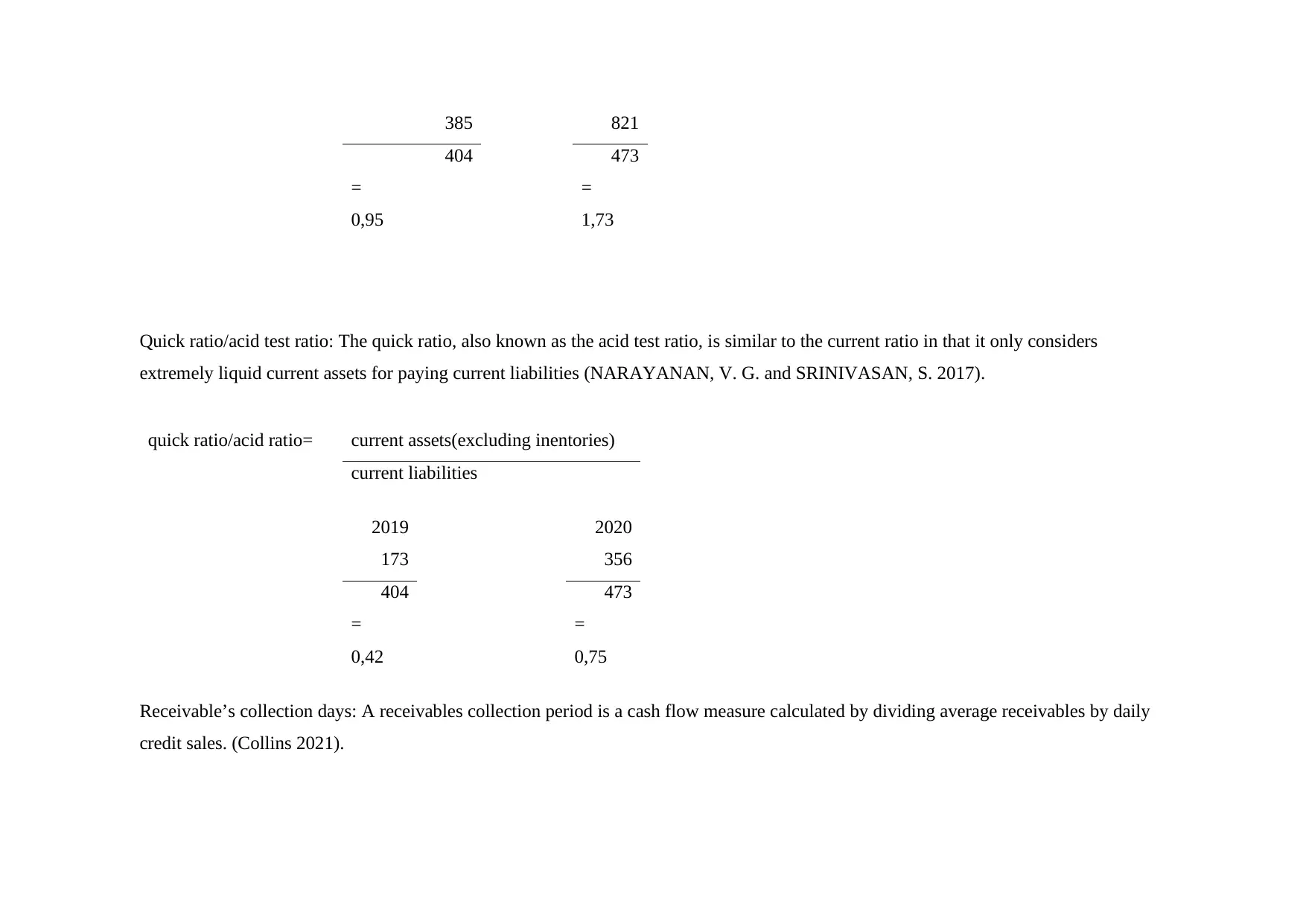

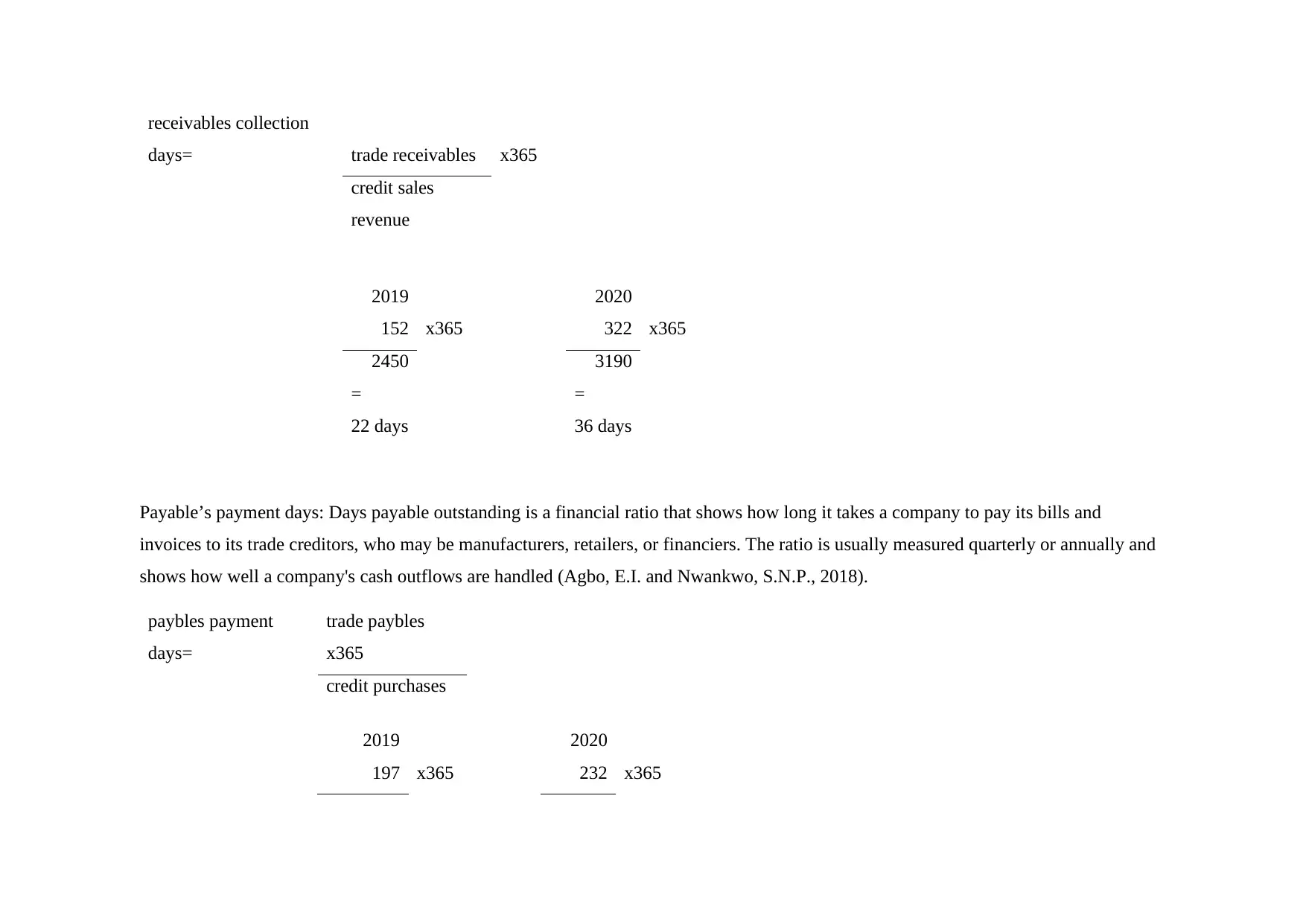

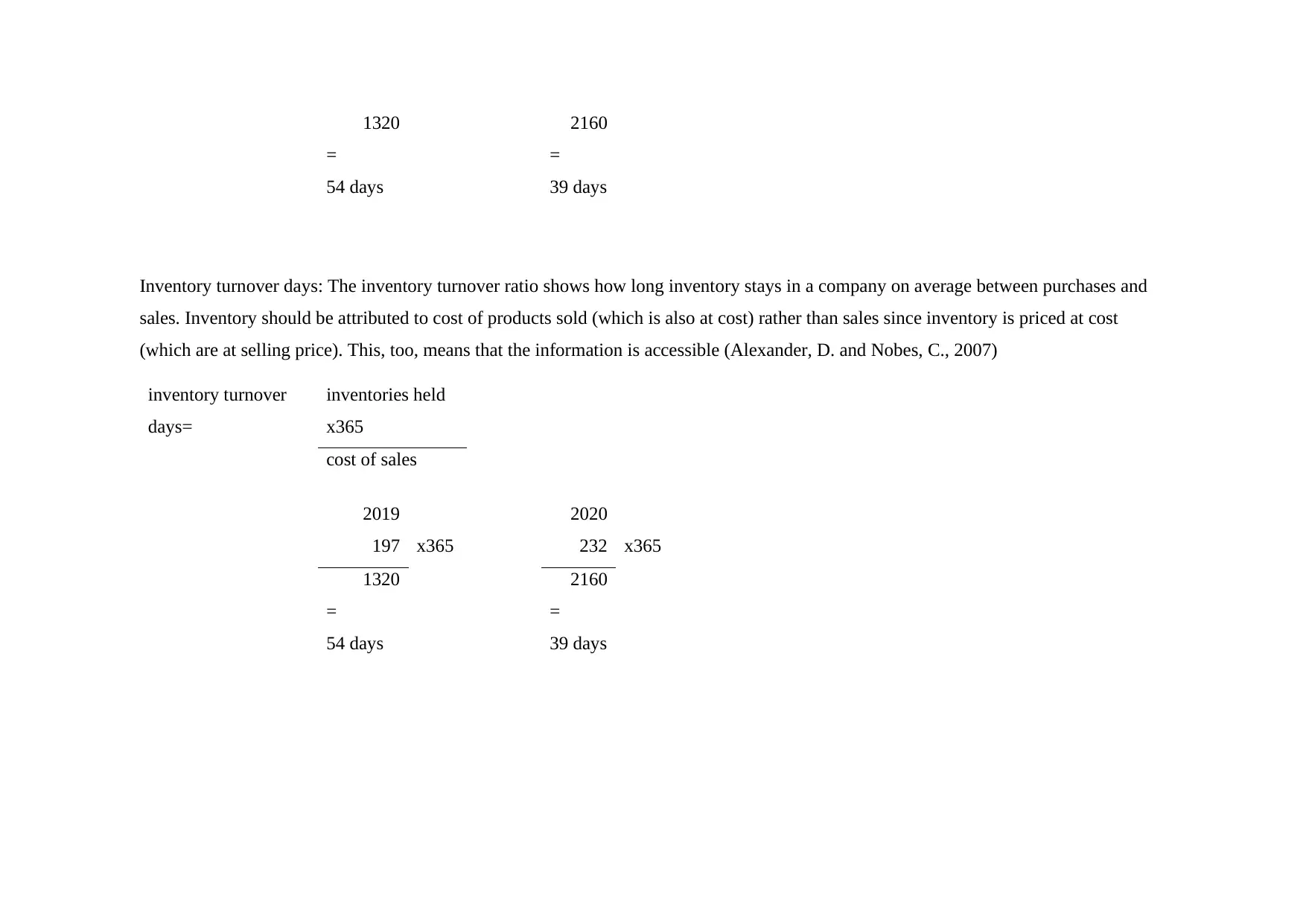

This assignment analyzes financial statements, including the income statement and balance sheet, for Brimwell Ltd. It calculates depreciation, inventories, trade receivables, cash, prepaid expenses, equity, and trade payables. The assignment also assesses Piketown Ltd's financial performance using ratio analysis, including return on capital employed, operating profit margin, gross profit margin, current ratio, quick ratio, receivables collection days, payables payment days, and inventory turnover days. Furthermore, the assignment explores investment appraisal techniques, such as Net Present Value (NPV), payback period, and accounting rate of return (ARR), evaluating their benefits and drawbacks. The report concludes with an assessment of the investment's viability based on these methods.

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.