Comprehensive Financial Project: Analysis of Investment and Taxation

VerifiedAdded on 2023/06/08

|10

|2077

|299

Project

AI Summary

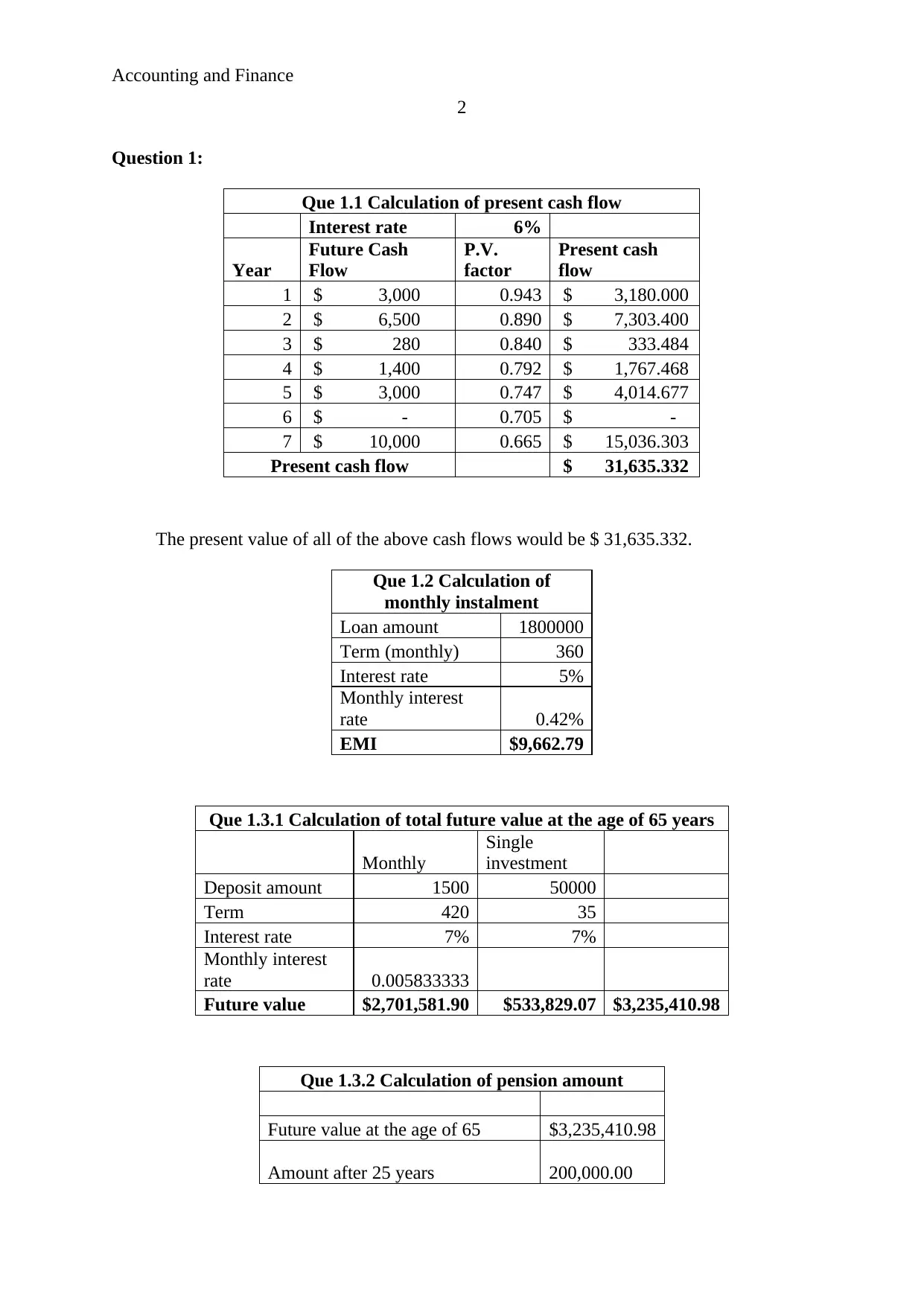

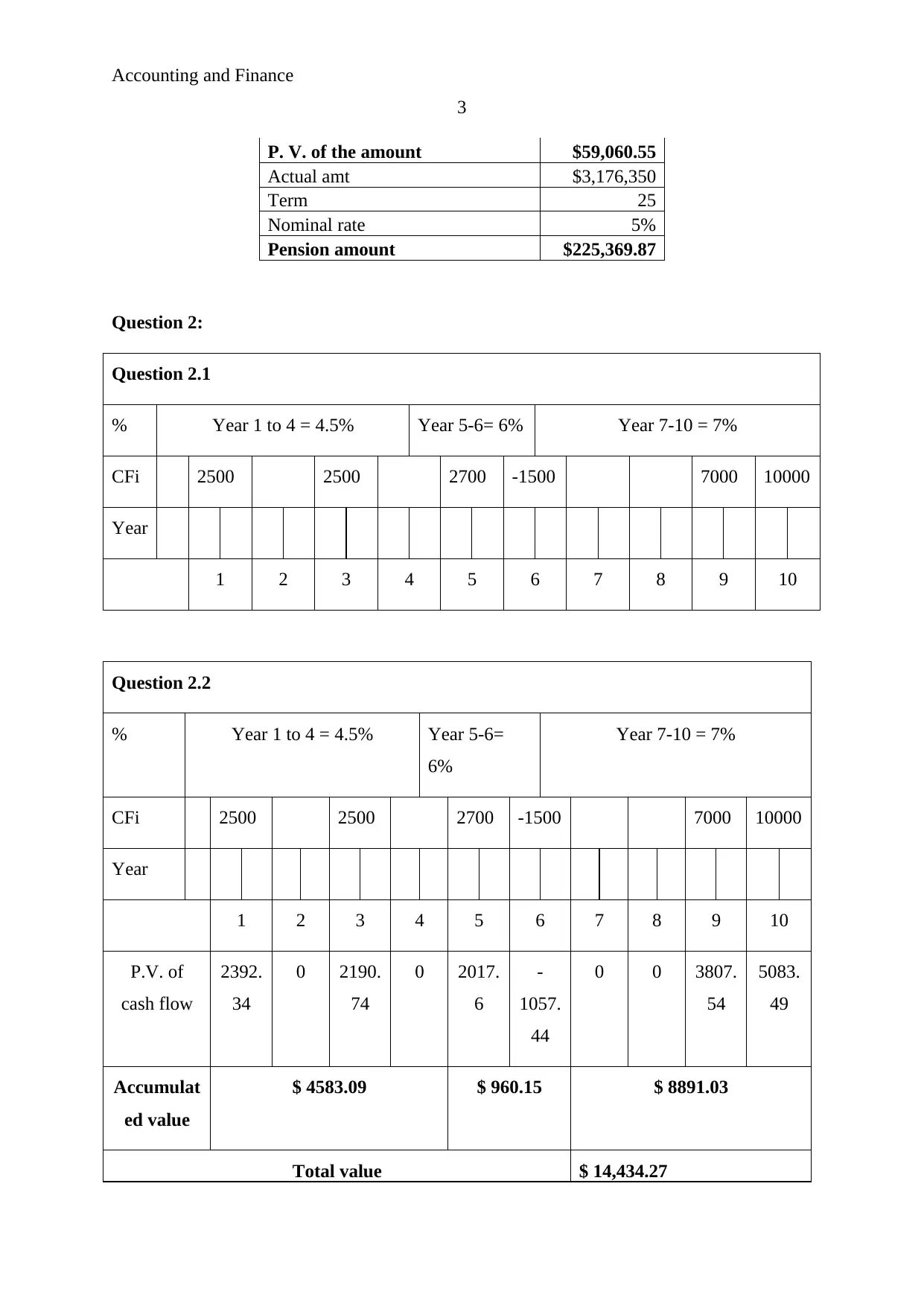

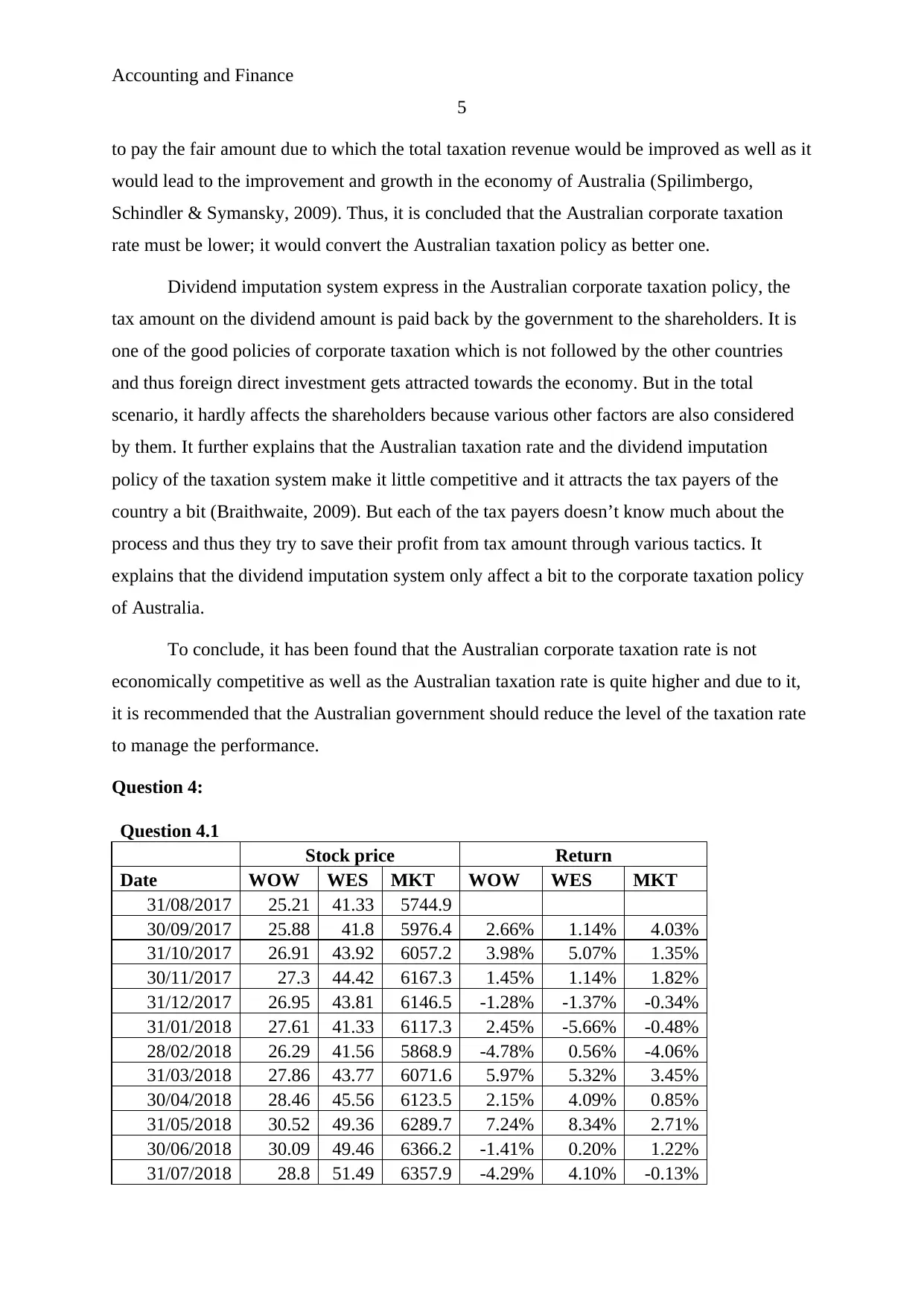

This finance project report includes a comprehensive analysis of various financial concepts and calculations. It begins with calculating the present value of cash flows, followed by determining the monthly EMI for a loan. The project then explores future value calculations for single and monthly investments, along with the estimation of pension amounts. Furthermore, it discusses the impact of corporate taxation, particularly in the Australian context, and analyzes stock returns for WOW and WES, including cost of equity using the CAPM model and portfolio beta calculations. The report concludes with an overview of the CAPM and SML calculations, providing insights into investment decisions and portfolio management. Desklib offers a wealth of similar solved assignments and study resources for students.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.