Corporate Accounting: Finance Lease by Manufacturer - Report Analysis

VerifiedAdded on 2023/01/11

|11

|2541

|97

Report

AI Summary

This report delves into the intricacies of accounting for finance leases, specifically focusing on the perspectives of manufacturers and dealer lessors. It begins by outlining the fundamental principles of lease accounting, including the definition of a finance lease and the roles of the lessor and lessee. The report then examines the specific accounting treatments required under AASB 16, the revised standard, highlighting the importance of recognizing receivables, residual values, and sales profit for manufacturers. It contrasts these treatments with those for third-party lessors. The practical challenges of implementing AASB 16, such as data collection, validation, and stakeholder scrutiny, are discussed. The report also covers the recognition of income, impairment requirements, and accounting for lease modifications. Part B of the assignment includes calculations and journal entries for a case study involving asset impairment within a company's fine china division. The report provides a comprehensive overview of the topic, equipping readers with a thorough understanding of finance lease accounting in a corporate setting.

Running head: CORPORATE ACCOUNTING

Corporate accounting

Name of the student

Name of the university

Student ID

Author note

Corporate accounting

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING

Part A

Accounting for finance lease by the manufacturer or the dealer lessor

Lease finance in Australia is mature product that is been offered as part of the

portfolio as the technique of equipment financing for more than 60 years all over

Australia. Predominant lessor group in Australia are the banks and finance entities.

Over the recent decades the utilization of lease product is impacted by the policies of

government reflected through regulation. It further included the tax benefit status of

transfer and treatment of consumption tax that is GST, as against input tax (Capital-

markets-intelligence.com 2019)

Lease is the contract that outlines terms where one party agrees for renting the

property that is owned by any other party. It provides guarantee for the lessee who is

also known as tenant for using the asset and provides guarantee to the lessor who is

also known as the owner of the property. The owner receives regular payment from

lessee over the term of lease. However, the lessee as well as the lessor both faces the

consequences if any of the parties fails in upholding the contract terms. Leases are

binding as well as legal contracts that expresses terms of the rental agreements. Lessor

in the simple expression is a person who grants the lease. Hence, the lessor is owner of

asset that is leased under the agreement to lessee (Aasb.gov.au 2019)

Manufacturing entities set up the leasing entity for providing support for the sales

finance. Manufacturers produce the goods and have the manufacturing costs related to

sales. While leasing, they do not use the cost of sales as basis for computing terms of

lease. Rather, they compute lease terms based on the normal cash price of asset that is

Part A

Accounting for finance lease by the manufacturer or the dealer lessor

Lease finance in Australia is mature product that is been offered as part of the

portfolio as the technique of equipment financing for more than 60 years all over

Australia. Predominant lessor group in Australia are the banks and finance entities.

Over the recent decades the utilization of lease product is impacted by the policies of

government reflected through regulation. It further included the tax benefit status of

transfer and treatment of consumption tax that is GST, as against input tax (Capital-

markets-intelligence.com 2019)

Lease is the contract that outlines terms where one party agrees for renting the

property that is owned by any other party. It provides guarantee for the lessee who is

also known as tenant for using the asset and provides guarantee to the lessor who is

also known as the owner of the property. The owner receives regular payment from

lessee over the term of lease. However, the lessee as well as the lessor both faces the

consequences if any of the parties fails in upholding the contract terms. Leases are

binding as well as legal contracts that expresses terms of the rental agreements. Lessor

in the simple expression is a person who grants the lease. Hence, the lessor is owner of

asset that is leased under the agreement to lessee (Aasb.gov.au 2019)

Manufacturing entities set up the leasing entity for providing support for the sales

finance. Manufacturers produce the goods and have the manufacturing costs related to

sales. While leasing, they do not use the cost of sales as basis for computing terms of

lease. Rather, they compute lease terms based on the normal cash price of asset that is

2CORPORATE ACCOUNTING

the fair value. Difference among the cost of sales for the manufacturer and normal cash

price of the asset is considered as the manufacturer’s sales profit (Joubert, Garvie and

Parle 2017). For the manufacturer or the dealer lessor de-recognition of lease lead to

recognition of the receivable as well as residual value, if any. Here the sum of

receivables is more as compared to the manufacturer’s cost of asset. However, for the

3rd party lessor no sales profit is there to be recognized as price of asset that is used for

determining rental payment is different to the cost of sales (Aasb.gov.au 2019)

In previous period the leases were used to be treated as per the requirement of

AASB 117. However, owing to increasing misstatement regarding treatment of lease in

the financial reports the revised standard AASB 16 is required to be issued. It is

mandatory from 1st January 2019, however still some organizations are there who wants

to shift to the new standard retrospectively. The new standard will increase its focus on

lease accounting and it is expected that the practical as well as commercial implications

will be significant. Practical challenges that will be faced by the companies are in

collecting the data for all of the leases, validating quality data on continuous basis, re-

assessment on regular bass, increase in the scrutiny from the major stakeholders

including banks, investors, suppliers and customers and combining the knowledge

gathered from various sources (Sieverding 2018)

'Leases' refers to accounting for leases except (a) licensing agreements for such

items as, copyrights, patents, recordings, plays, manuscripts, and motion picture films.

(b) Leases applied for exploring and using minerals, oil, natural gas and similar kind of

non-regenerative wealth. Objective of Accounting Standard AASB 16 is – (1) to

measure, recognize, present, and reveal leases in standard way, so that lessors and

the fair value. Difference among the cost of sales for the manufacturer and normal cash

price of the asset is considered as the manufacturer’s sales profit (Joubert, Garvie and

Parle 2017). For the manufacturer or the dealer lessor de-recognition of lease lead to

recognition of the receivable as well as residual value, if any. Here the sum of

receivables is more as compared to the manufacturer’s cost of asset. However, for the

3rd party lessor no sales profit is there to be recognized as price of asset that is used for

determining rental payment is different to the cost of sales (Aasb.gov.au 2019)

In previous period the leases were used to be treated as per the requirement of

AASB 117. However, owing to increasing misstatement regarding treatment of lease in

the financial reports the revised standard AASB 16 is required to be issued. It is

mandatory from 1st January 2019, however still some organizations are there who wants

to shift to the new standard retrospectively. The new standard will increase its focus on

lease accounting and it is expected that the practical as well as commercial implications

will be significant. Practical challenges that will be faced by the companies are in

collecting the data for all of the leases, validating quality data on continuous basis, re-

assessment on regular bass, increase in the scrutiny from the major stakeholders

including banks, investors, suppliers and customers and combining the knowledge

gathered from various sources (Sieverding 2018)

'Leases' refers to accounting for leases except (a) licensing agreements for such

items as, copyrights, patents, recordings, plays, manuscripts, and motion picture films.

(b) Leases applied for exploring and using minerals, oil, natural gas and similar kind of

non-regenerative wealth. Objective of Accounting Standard AASB 16 is – (1) to

measure, recognize, present, and reveal leases in standard way, so that lessors and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING

lessees provide information pertinent to the transaction. This helps users of financial

report to understand the effect that lease have on cash flow, financial performance and

financial position of an organization. (2) An organization should take those conditions

and terms of contracts as well as all facts pertaining to this while applying this contract.

A lease is termed as the finance lease while it transmits majority of all the

rewards and risks associated with the ownership of the subjected asset. Further, the

finance lease is a kind of lease under which the finance organization is habitually the

legitimate possessor of the asset for the time span of the lease whereas the lessee has

control over the operation of the asset and some proportion of economic risks in

addition to returns from change in the valuation of primary asset. In the financial

statement the lessor needs to show the primary assets which are under finance lease

as an outstanding value which is equal to the total amount invested in the lease (Wong

and Joshi 2015). The lessor should use the rate of interest which is indirect in the

evaluation of the total amount invested in the lease. In matters pertaining to sublease,

when the rate of interest which is indirect in the evaluation of the total amount invested

in the lease cannot be easily found out, then the intervening lessor uses the rate of

discount which was used for the primary lease to calculate the total investment in the

sublease (Fitó et al.2013).

In the beginning the cost which are direct are added to the original calculation of

the total amount of the money invested in the lease and the earning amount is accepted

when the cost is sustained by dealer or manufacturer lessors. The rate of interest which

is indirect in the lease is explained in a method that the original costs which are direct

lessees provide information pertinent to the transaction. This helps users of financial

report to understand the effect that lease have on cash flow, financial performance and

financial position of an organization. (2) An organization should take those conditions

and terms of contracts as well as all facts pertaining to this while applying this contract.

A lease is termed as the finance lease while it transmits majority of all the

rewards and risks associated with the ownership of the subjected asset. Further, the

finance lease is a kind of lease under which the finance organization is habitually the

legitimate possessor of the asset for the time span of the lease whereas the lessee has

control over the operation of the asset and some proportion of economic risks in

addition to returns from change in the valuation of primary asset. In the financial

statement the lessor needs to show the primary assets which are under finance lease

as an outstanding value which is equal to the total amount invested in the lease (Wong

and Joshi 2015). The lessor should use the rate of interest which is indirect in the

evaluation of the total amount invested in the lease. In matters pertaining to sublease,

when the rate of interest which is indirect in the evaluation of the total amount invested

in the lease cannot be easily found out, then the intervening lessor uses the rate of

discount which was used for the primary lease to calculate the total investment in the

sublease (Fitó et al.2013).

In the beginning the cost which are direct are added to the original calculation of

the total amount of the money invested in the lease and the earning amount is accepted

when the cost is sustained by dealer or manufacturer lessors. The rate of interest which

is indirect in the lease is explained in a method that the original costs which are direct

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING

are added mechanically, they are not required to be added one by one (Demir et

al.2014)

At the beginning, the payments for lease are part of the calculation of the total

investment on the lease. The following settlement for the right to use the primary asset

during the course of lease those were not provided at the beginning date they are (a)

payments which are fixed less payable incentives of lease (b) the lease settlement

which are variable which depends on a rate or an index calculated at the starting date

(c) the promise provided by lessee to the lessor on the leftover value, a group pertaining

to 3rd party or the lessee not related to the lessor that is monetarily proficient of carrying

out the duty to fulfil the promise (d) The value at which the primary security can be

bought or sold at of a purchase option if the lessee is fairly sure to exercise that option

and (e) the payment for fine for putting an end to the lease, if the lease agreement

shows that the lessee is putting to use an option to put an end to the lease (Gavana,

Guggiola and Marenzi 2013)

Manufacturer or dealer lessors for its each and every financial leases should

accept the following: (a) the income of the primary asset that is fair value or, if less, the

current amount of the lease payments resulting to the lessor, deducted taking the

interest rate of the market (b) the price of sale is the carrying amount or else the value if

not the same, with that of the primary assets less current price of the residual price

without any financial security and (c) the disparity between the cost of sale and revenue

is the loss or the profit in conformity with its guidelines for complete sale to which AASB

15 pertain to. A dealer or manufacturing lessor should accept selling loss or profit on a

are added mechanically, they are not required to be added one by one (Demir et

al.2014)

At the beginning, the payments for lease are part of the calculation of the total

investment on the lease. The following settlement for the right to use the primary asset

during the course of lease those were not provided at the beginning date they are (a)

payments which are fixed less payable incentives of lease (b) the lease settlement

which are variable which depends on a rate or an index calculated at the starting date

(c) the promise provided by lessee to the lessor on the leftover value, a group pertaining

to 3rd party or the lessee not related to the lessor that is monetarily proficient of carrying

out the duty to fulfil the promise (d) The value at which the primary security can be

bought or sold at of a purchase option if the lessee is fairly sure to exercise that option

and (e) the payment for fine for putting an end to the lease, if the lease agreement

shows that the lessee is putting to use an option to put an end to the lease (Gavana,

Guggiola and Marenzi 2013)

Manufacturer or dealer lessors for its each and every financial leases should

accept the following: (a) the income of the primary asset that is fair value or, if less, the

current amount of the lease payments resulting to the lessor, deducted taking the

interest rate of the market (b) the price of sale is the carrying amount or else the value if

not the same, with that of the primary assets less current price of the residual price

without any financial security and (c) the disparity between the cost of sale and revenue

is the loss or the profit in conformity with its guidelines for complete sale to which AASB

15 pertain to. A dealer or manufacturing lessor should accept selling loss or profit on a

5CORPORATE ACCOUNTING

finance lease at the beginning day, despite of if the lessor hand over the primary asset.

(Lin et el. 2013).

Dealers or manufacturers regularly recommend the alternative of either leasing

or purchasing an asset to consumers. A finance lease of an asset by a dealer or

manufacturer lessor brings the same loss or profit that of the loss or profit arising with a

complete sale of the primary asset, at selling prices which is normal , showing ant trade

rebates or applicable volume (Morales-Díaz and Zamora-Ramírez 2018 ).

Dealers occasionally bid false rate of interest very low so that they can pull in a

lot of consumer. Putting to use such low rate of interest at the beginning of the period

would lead to a lessor allowing an unrestrained part of the total earnings from the deal.

If false rate of interest are bided dealer or manufacturer lessor should stop selling profit

to that which would apply if the interest rate of the market were changed (Barone et al.

2014).

Manufacturers at the beginning day shall acknowledge as a cost of expense to

sustain in relation with getting a finance lease as they are solely linked with to get the

selling profit of the dealer or manufacturer.( Kindleberger 2015). The value sustained by

the dealer or manufacturer lessors pertaining in getting a finance lease are not taken

part of the original direct cost, and hence not a part of the total investment in the lease

(Rai and Sigrin 2013) lessor should acknowledge finance income over the course of

lease, established on a systematic basis showing a steady rate of return on the total

investment of the lessor in the lease. A lessor focuses on assigning finance earning on

a rational and methodical basis over the lease term. Concerning to the time frame a

finance lease at the beginning day, despite of if the lessor hand over the primary asset.

(Lin et el. 2013).

Dealers or manufacturers regularly recommend the alternative of either leasing

or purchasing an asset to consumers. A finance lease of an asset by a dealer or

manufacturer lessor brings the same loss or profit that of the loss or profit arising with a

complete sale of the primary asset, at selling prices which is normal , showing ant trade

rebates or applicable volume (Morales-Díaz and Zamora-Ramírez 2018 ).

Dealers occasionally bid false rate of interest very low so that they can pull in a

lot of consumer. Putting to use such low rate of interest at the beginning of the period

would lead to a lessor allowing an unrestrained part of the total earnings from the deal.

If false rate of interest are bided dealer or manufacturer lessor should stop selling profit

to that which would apply if the interest rate of the market were changed (Barone et al.

2014).

Manufacturers at the beginning day shall acknowledge as a cost of expense to

sustain in relation with getting a finance lease as they are solely linked with to get the

selling profit of the dealer or manufacturer.( Kindleberger 2015). The value sustained by

the dealer or manufacturer lessors pertaining in getting a finance lease are not taken

part of the original direct cost, and hence not a part of the total investment in the lease

(Rai and Sigrin 2013) lessor should acknowledge finance income over the course of

lease, established on a systematic basis showing a steady rate of return on the total

investment of the lessor in the lease. A lessor focuses on assigning finance earning on

a rational and methodical basis over the lease term. Concerning to the time frame a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING

lessor should put the lease payments against the gross investment in the lease to lower

the unearned finance income and the principal (Fatima 2016).

A lessor is required to apply the impairment as well as identification requirements

in AASB 9 to the total amount invested in the lease. A lessor should analysis frequently

that part of the residual value of the underlying asset, the realization of which by a

lessor is not assured or is guaranteed solely by a party related to the lessor in

calculating the gross investment in the lease. If there has been decrease in the

approximation of not guaranteed residual value, the lessor should amend the earning

allotment over the lease tenor and admit instantly any decrease with view of money

accumulated.

A lessor who segregates an asset under held for sale (or is a part of it in a

disposal group that groups as held for sale) under a finance lease applying AASB 5

Non-current Assets Held for sale and Discontinued Operations should account for the

asset in compliance with that protocol. A lessor should consider for alteration to a

finance lease as a different lease if both (a) the alteration improves the extent of the

lease by adding the right to use one or more than one primary assets and (b) the

payment for the lease grows by the value equal to the only price for the increase in

scope and any suitable changes in the stand –alone price to show the situation of that

specific deed.

In adjustment for a finance lease which is not considered as a different lease, a

lessor should consider the alterations which are firstly had the lease been grouped as a

new lease from the effective date of the alteration and secondly calculate the recorded

lessor should put the lease payments against the gross investment in the lease to lower

the unearned finance income and the principal (Fatima 2016).

A lessor is required to apply the impairment as well as identification requirements

in AASB 9 to the total amount invested in the lease. A lessor should analysis frequently

that part of the residual value of the underlying asset, the realization of which by a

lessor is not assured or is guaranteed solely by a party related to the lessor in

calculating the gross investment in the lease. If there has been decrease in the

approximation of not guaranteed residual value, the lessor should amend the earning

allotment over the lease tenor and admit instantly any decrease with view of money

accumulated.

A lessor who segregates an asset under held for sale (or is a part of it in a

disposal group that groups as held for sale) under a finance lease applying AASB 5

Non-current Assets Held for sale and Discontinued Operations should account for the

asset in compliance with that protocol. A lessor should consider for alteration to a

finance lease as a different lease if both (a) the alteration improves the extent of the

lease by adding the right to use one or more than one primary assets and (b) the

payment for the lease grows by the value equal to the only price for the increase in

scope and any suitable changes in the stand –alone price to show the situation of that

specific deed.

In adjustment for a finance lease which is not considered as a different lease, a

lessor should consider the alterations which are firstly had the lease been grouped as a

new lease from the effective date of the alteration and secondly calculate the recorded

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

cost of the primary asset, net of any accumulated depreciation and impairment losses

as the total amount invested in the lease instantly prior the effective date of the lease

modification; or else the lessor should put to use the requirements of AASB 9

(Aasb.gov.au 2019).

cost of the primary asset, net of any accumulated depreciation and impairment losses

as the total amount invested in the lease instantly prior the effective date of the lease

modification; or else the lessor should put to use the requirements of AASB 9

(Aasb.gov.au 2019).

8CORPORATE ACCOUNTING

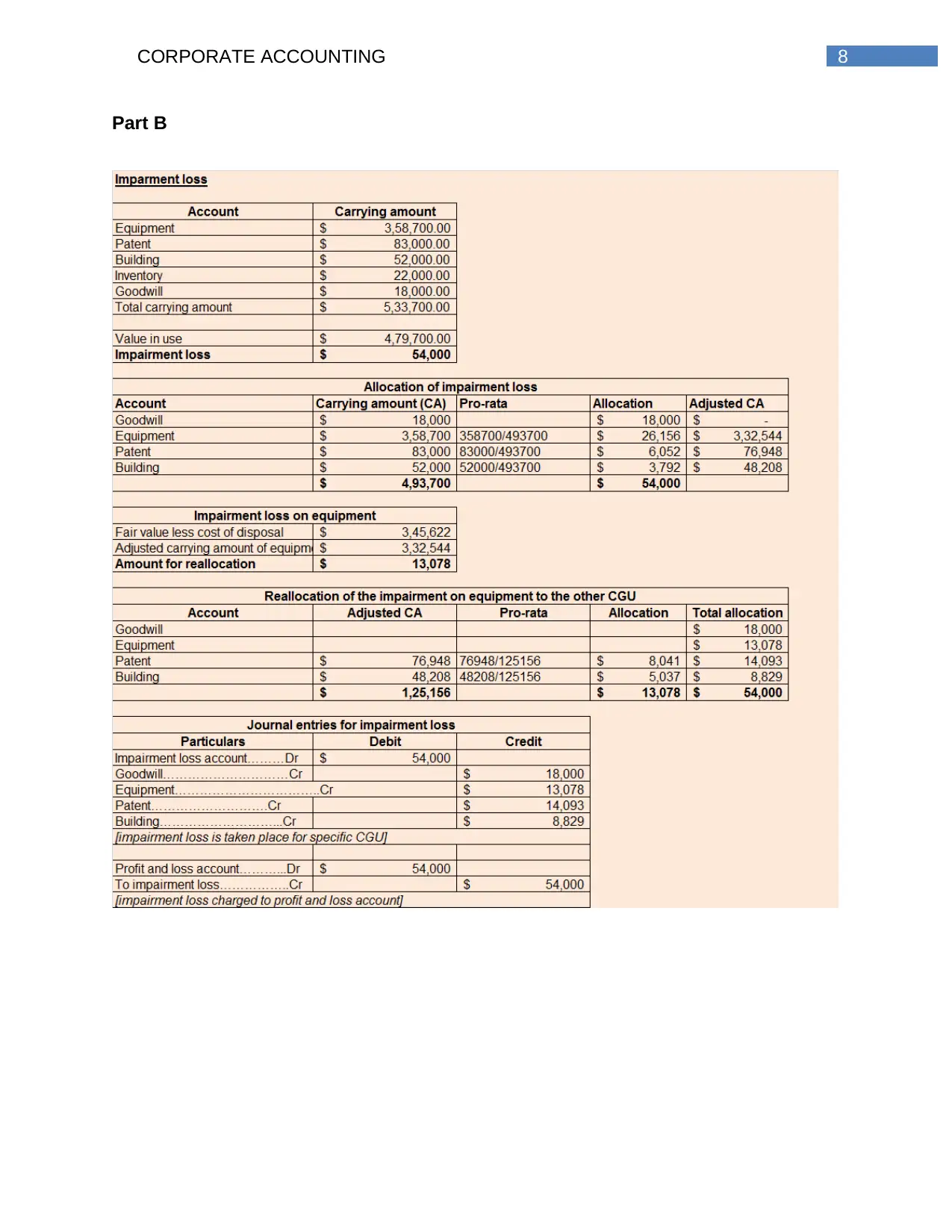

Part B

Part B

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTING

Reference

Aasb.gov.au. 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB16_02-16.pdf [Accessed 7 Jun.

2019].

Barone, E., Birt, J. and Moya, S., 2014. Lease accounting: A review of recent

literature. Accounting in Europe, 11(1), pp.35-54.

Capital-markets-intelligence.com. 2019. [online] Available at: https://www.capital-

markets-intelligence.com/wp-content/uploads/2019/01/WLY-2019-Australia.pdf

[Accessed 7 Jun. 2019].

Demir, V. and Bahadir, O., 2014. An investigation of compliance with International

Financial Reporting Standards by listed companies in Turkey. Accounting and

Management Information Systems, 13(1), p.4.

Fatima, M., 2016. Differences and similarities between Ijara and conventional operating

lease contracts. Market Forces, 1(4).

Fitó, M.À., Moya, S. and Orgaz, N., 2013. Considering the effects of operating lease

capitalization on key financial ratios. Spanish Journal of Finance and

Accounting/Revista Española de Financiación y Contabilidad, 42(159), pp.341-369.

Gavana, G., Guggiola, G. and Marenzi, A., 2013. Evolving connections between tax and

financial reporting in Italy. Accounting in Europe, 10(1), pp.43-70.

Reference

Aasb.gov.au. 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB16_02-16.pdf [Accessed 7 Jun.

2019].

Barone, E., Birt, J. and Moya, S., 2014. Lease accounting: A review of recent

literature. Accounting in Europe, 11(1), pp.35-54.

Capital-markets-intelligence.com. 2019. [online] Available at: https://www.capital-

markets-intelligence.com/wp-content/uploads/2019/01/WLY-2019-Australia.pdf

[Accessed 7 Jun. 2019].

Demir, V. and Bahadir, O., 2014. An investigation of compliance with International

Financial Reporting Standards by listed companies in Turkey. Accounting and

Management Information Systems, 13(1), p.4.

Fatima, M., 2016. Differences and similarities between Ijara and conventional operating

lease contracts. Market Forces, 1(4).

Fitó, M.À., Moya, S. and Orgaz, N., 2013. Considering the effects of operating lease

capitalization on key financial ratios. Spanish Journal of Finance and

Accounting/Revista Española de Financiación y Contabilidad, 42(159), pp.341-369.

Gavana, G., Guggiola, G. and Marenzi, A., 2013. Evolving connections between tax and

financial reporting in Italy. Accounting in Europe, 10(1), pp.43-70.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE ACCOUNTING

Joubert, M., Garvie, L. and Parle, G., 2017. Implications of the New Accounting

Standard for Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the

Balance Sheet. The Journal of New Business Ideas & Trends, 15(2), pp.1-11.

Kindleberger, C.P., 2015. A financial history of Western Europe. Routledge.

Lin, J.R., Wang, C.J., Chou, D.W. and Chueh, F.C., 2013. Financial constraint and the

choice between leasing and debt. International Review of Economics & Finance, 27,

pp.171-182.

Morales-Díaz, J. and Zamora-Ramírez, C., 2018. The impact of IFRS 16 on key

financial ratios: a new methodological approach. Accounting in Europe, 15(1), pp.105-

133.

Rai, V. and Sigrin, B., 2013. Diffusion of environmentally-friendly energy technologies:

buy versus lease differences in residential PV markets. Environmental Research

Letters, 8(1), p.014022.

Sieverding, A., 2018. A critical analysis of the accounting for sale and lease back

transactions under the new IFRS 16(Doctoral dissertation).

Wong, K. and Joshi, M., 2015. The impact of lease capitalisation on financial statements

and key ratios: Evidence from Australia. Australasian Accounting, Business and

Finance Journal, 9(3), pp.27-44.

Joubert, M., Garvie, L. and Parle, G., 2017. Implications of the New Accounting

Standard for Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the

Balance Sheet. The Journal of New Business Ideas & Trends, 15(2), pp.1-11.

Kindleberger, C.P., 2015. A financial history of Western Europe. Routledge.

Lin, J.R., Wang, C.J., Chou, D.W. and Chueh, F.C., 2013. Financial constraint and the

choice between leasing and debt. International Review of Economics & Finance, 27,

pp.171-182.

Morales-Díaz, J. and Zamora-Ramírez, C., 2018. The impact of IFRS 16 on key

financial ratios: a new methodological approach. Accounting in Europe, 15(1), pp.105-

133.

Rai, V. and Sigrin, B., 2013. Diffusion of environmentally-friendly energy technologies:

buy versus lease differences in residential PV markets. Environmental Research

Letters, 8(1), p.014022.

Sieverding, A., 2018. A critical analysis of the accounting for sale and lease back

transactions under the new IFRS 16(Doctoral dissertation).

Wong, K. and Joshi, M., 2015. The impact of lease capitalisation on financial statements

and key ratios: Evidence from Australia. Australasian Accounting, Business and

Finance Journal, 9(3), pp.27-44.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.