Accounting and Finance Project: Investment, Loan & Tax Analysis

VerifiedAdded on 2023/06/07

|10

|2178

|248

Project

AI Summary

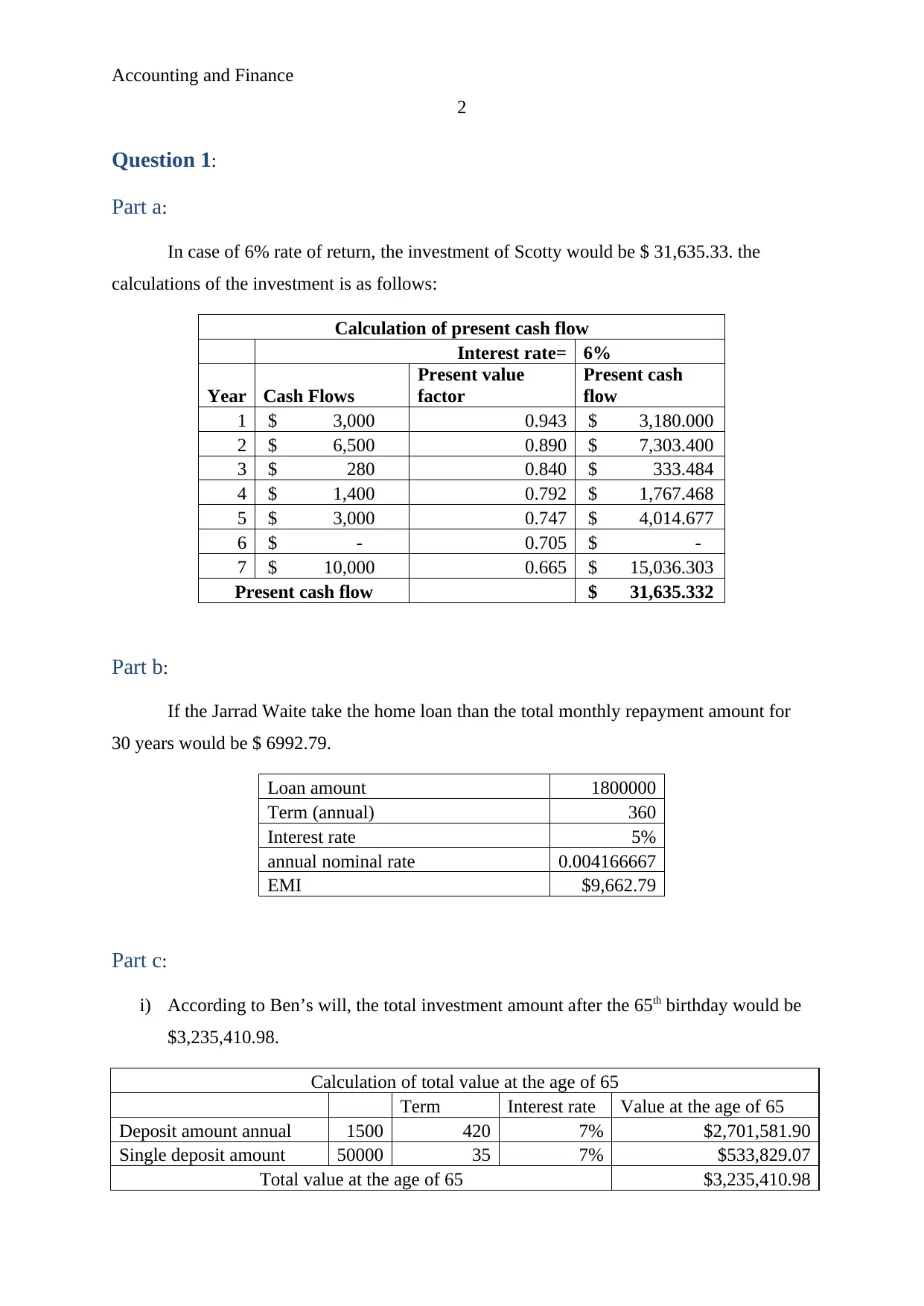

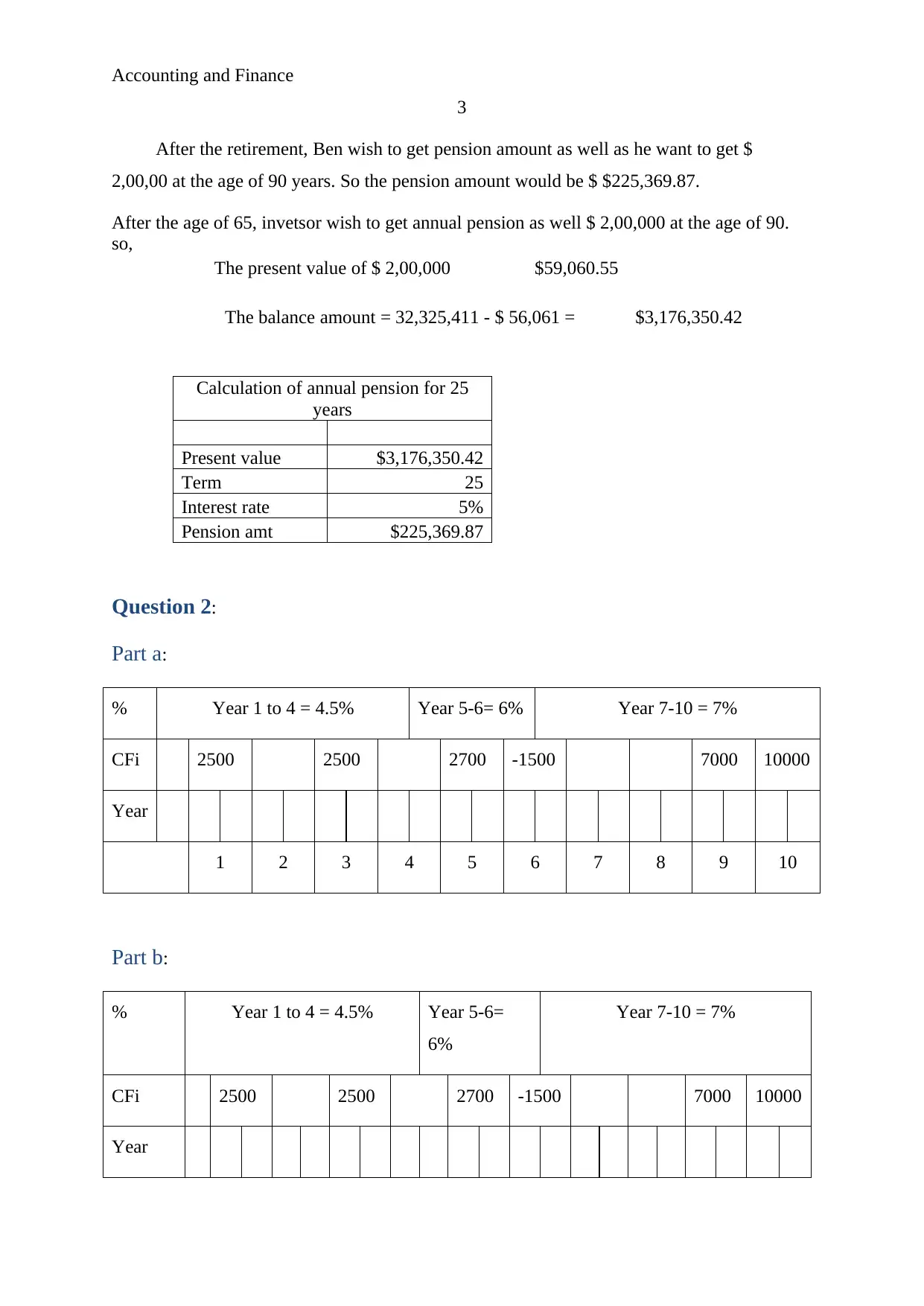

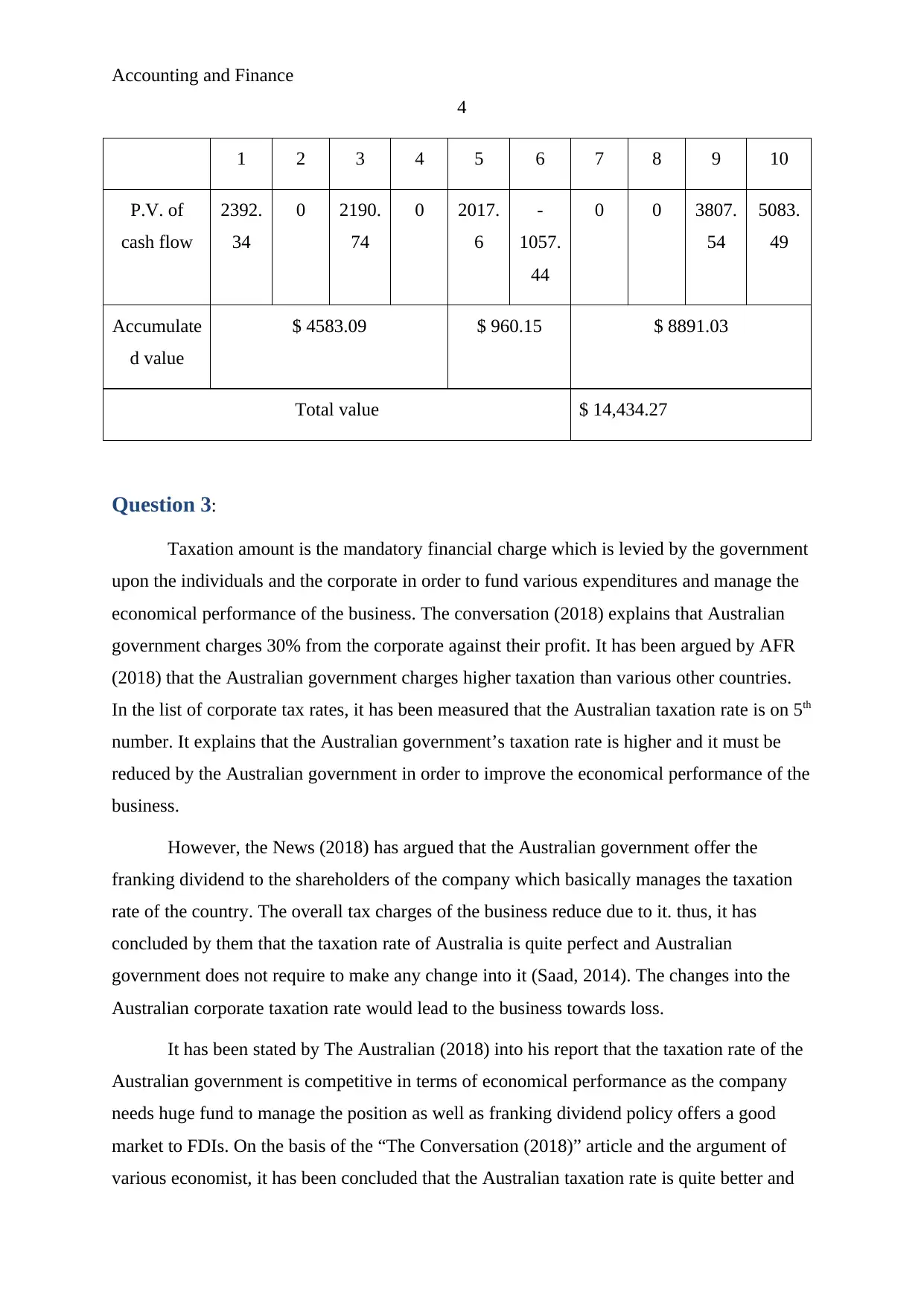

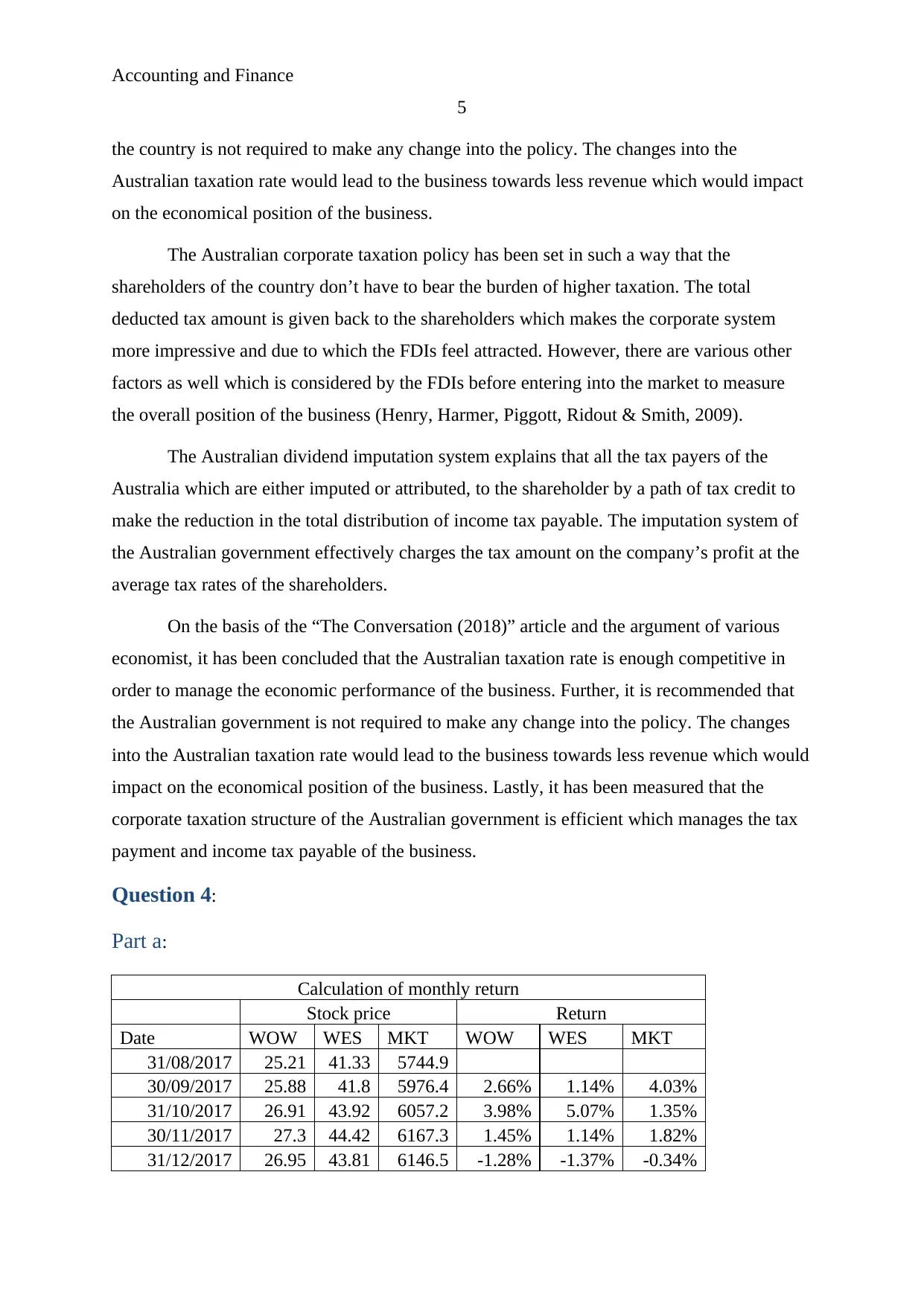

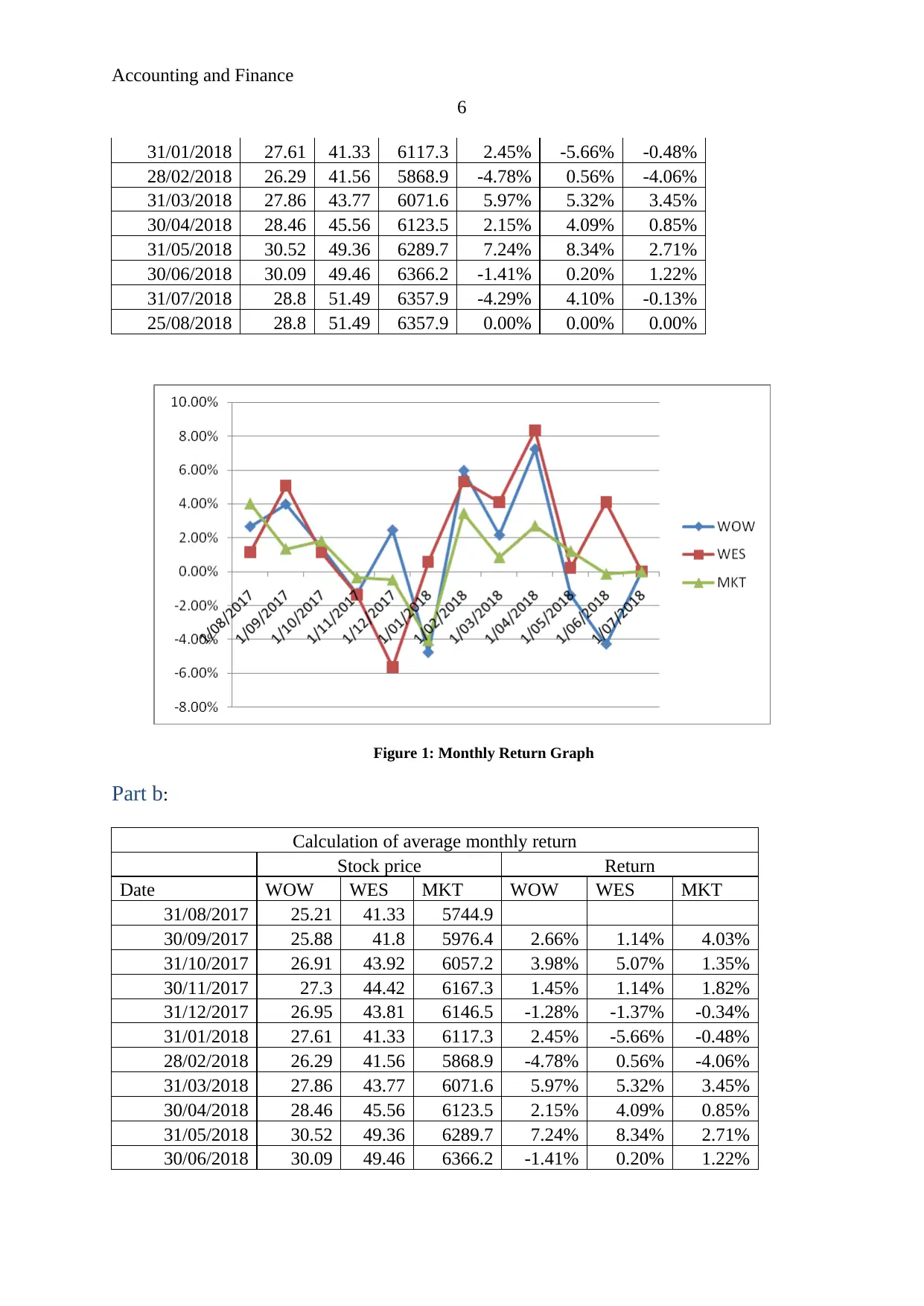

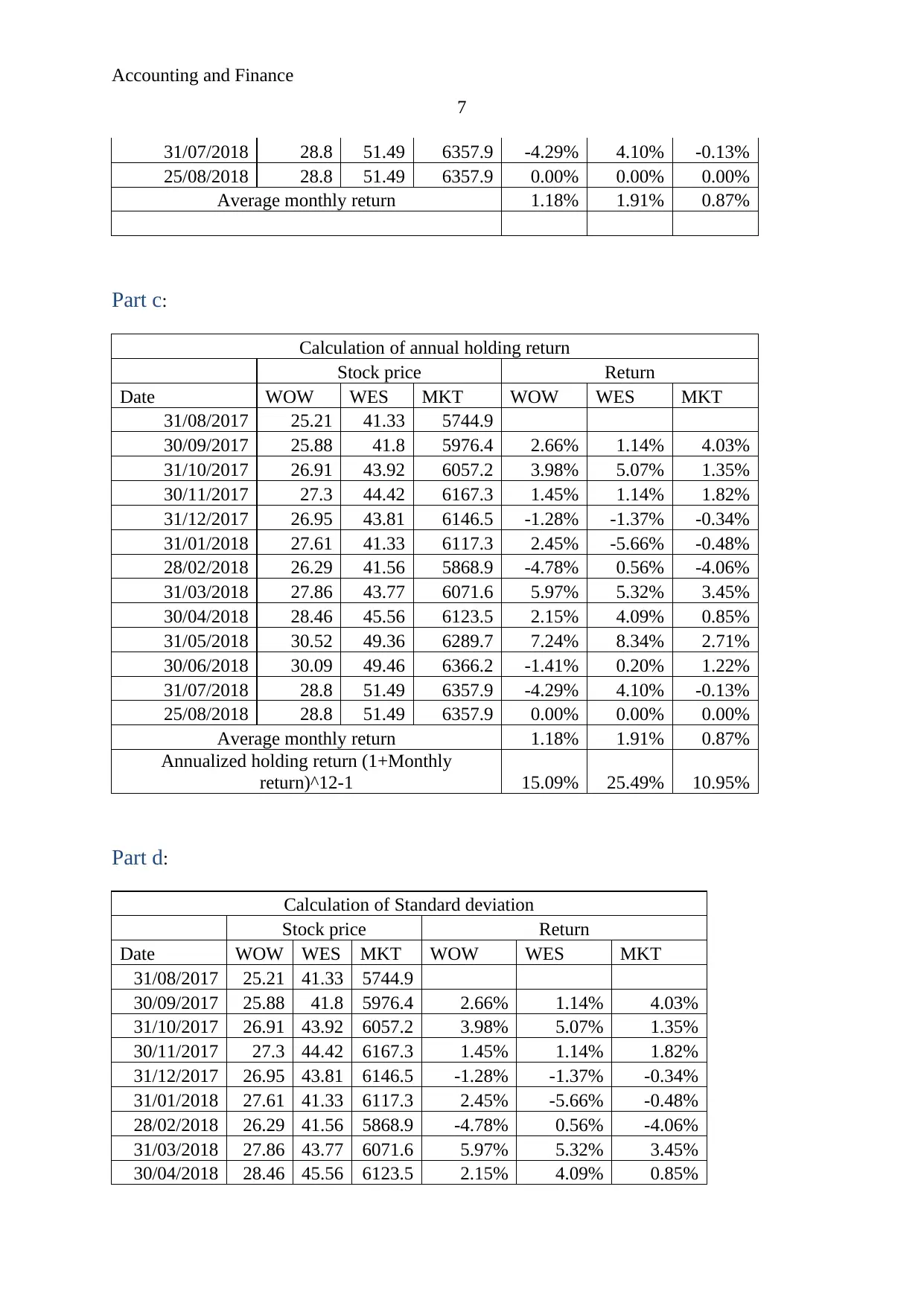

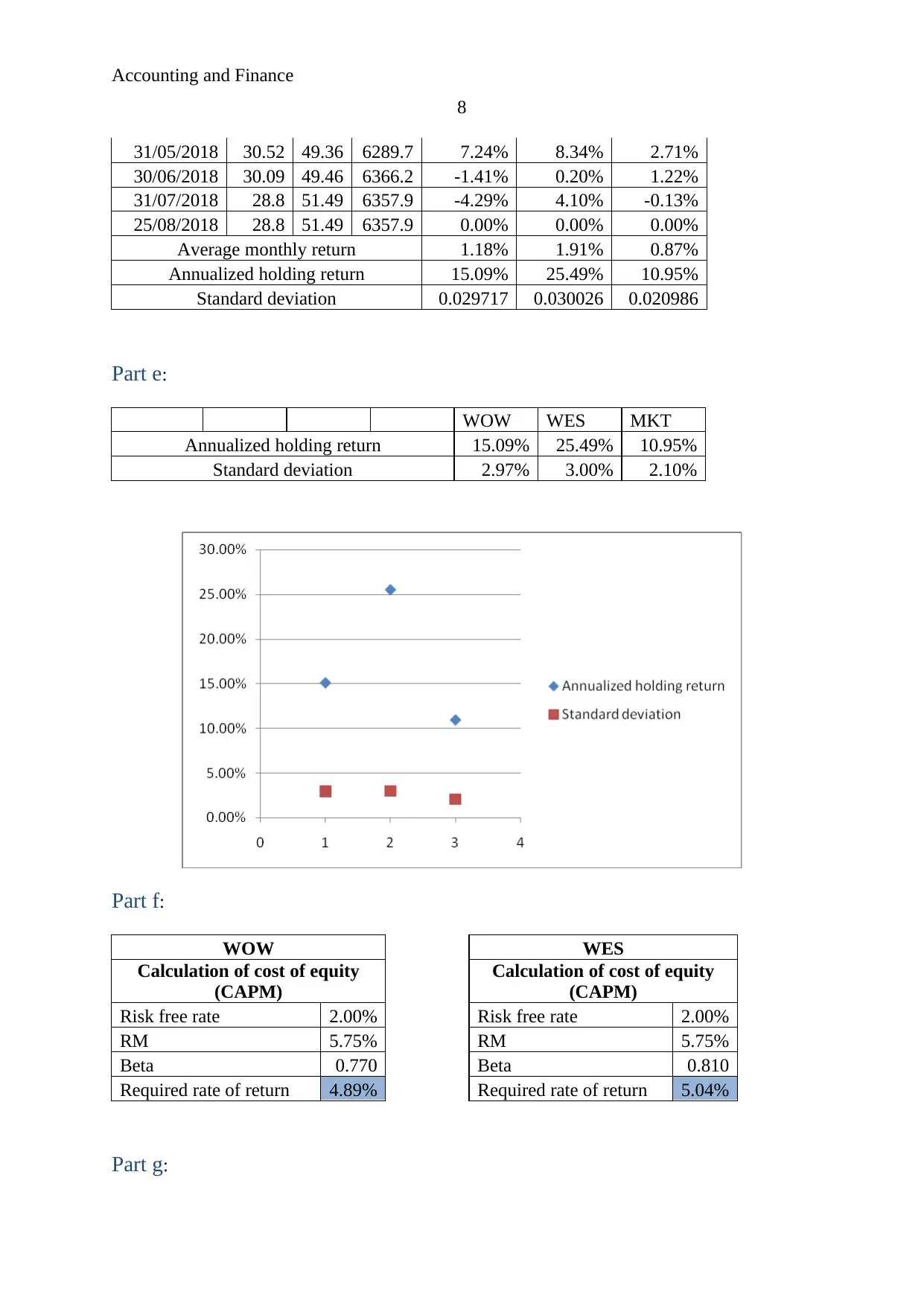

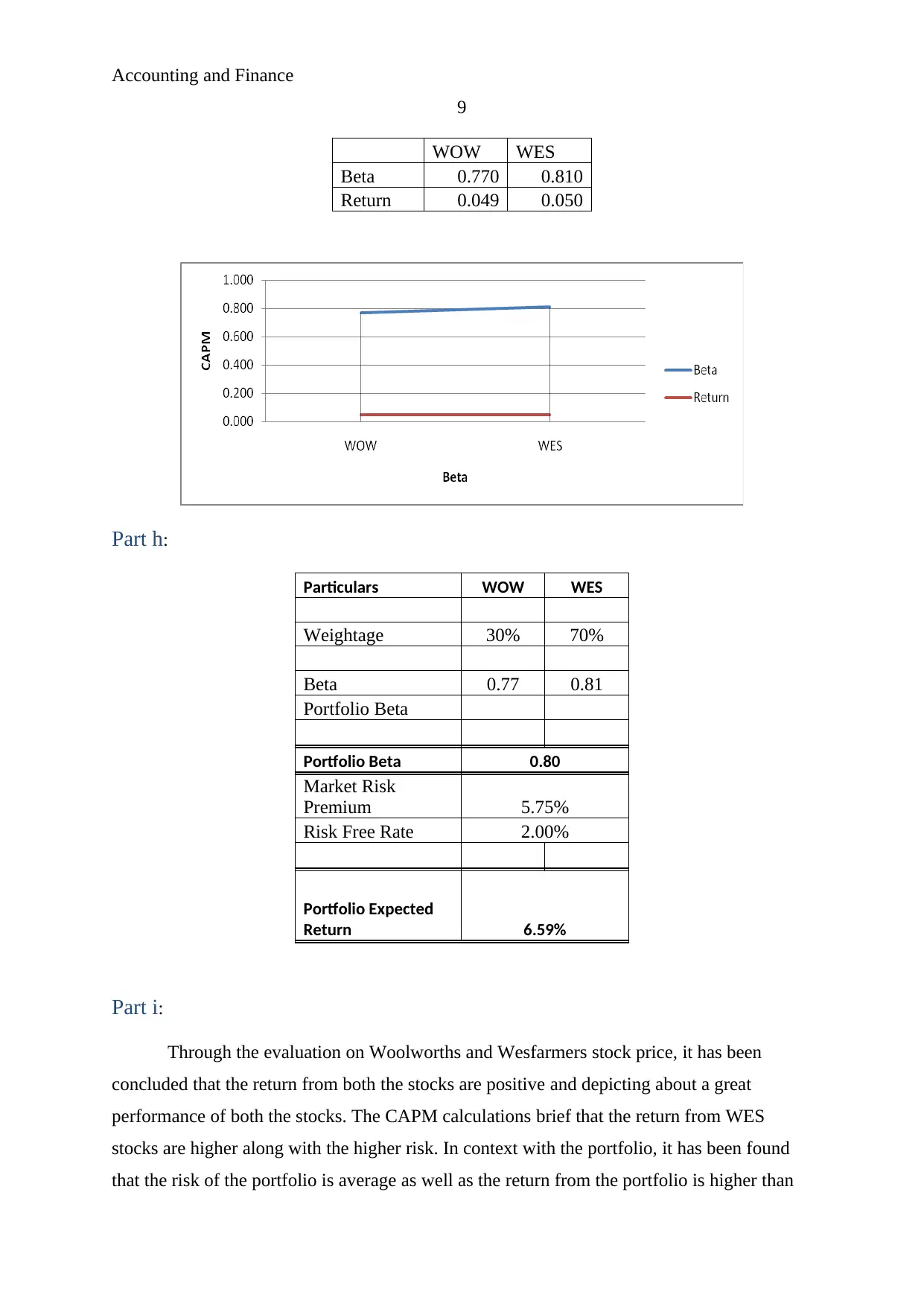

This project report on Accounting and Finance covers several key areas including investment analysis, loan calculations, retirement planning, and stock valuation. It begins by calculating the present value of an investment opportunity with a 6% required rate of return, determining the monthly repayment for a home loan, and projecting the total investment amount after retirement, along with the sustainable pension amount. The report then analyzes the percentage change in cash flow, calculates the present value of cash flows, and discusses the impact of Australian corporate taxation rates, considering arguments for and against changes to the current policy. Furthermore, the project evaluates the monthly returns, average monthly returns, annualized holding returns, and standard deviation for WOW, WES, and market stocks. Finally, it calculates the cost of equity using the Capital Asset Pricing Model (CAPM) for WOW and WES, determines portfolio beta, and recommends investment in the portfolio based on risk and return analysis. Desklib provides access to similar solved assignments for students.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.