Finance and Accounting Report - Bes Taste Analysis

VerifiedAdded on 2020/01/28

|10

|2845

|300

Report

AI Summary

This report provides a comprehensive analysis of accounting and finance principles, focusing on a case study involving Bes Taste. It begins by identifying and evaluating various sources of finance available to the company, considering both internal and external options like retained earnings, selling assets, and bank overdrafts. The report then delves into the significance of final accounts, including income statements, cash flow statements, and balance sheets, and how they provide crucial information for effective decision-making. It also examines the information needs of different stakeholders, such as investors, lenders, employees, customers, and the general public. Furthermore, the report analyzes different sources of finance like bank overdrafts, trade credit, term loans, ordinary shares, and retained profits, discussing their advantages and disadvantages. The report also includes an analysis of trial balances and journal entries, illustrating how to record financial transactions. This report provides a solid understanding of financial concepts and their practical application in a business context.

Understanding Accounting and

Finance

1

Finance

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION................................................................................................................................1

TASK 1.................................................................................................................................................1

A. Stating the sources of finance which are available to the board of Directors of Bes Taste.........1

B. Stating the information which is offered by final accounts.........................................................1

C. Information need of different stakeholders..................................................................................2

TASK 2.................................................................................................................................................2

TASK 3.................................................................................................................................................4

A. Indicating the side such as debit or credit in which balance of the different accounts appear....4

B. Stating the purpose of trial balance..............................................................................................6

C. Computing the journal entries......................................................................................................6

TASK 4.................................................................................................................................................7

References............................................................................................................................................9

2

INTRODUCTION................................................................................................................................1

TASK 1.................................................................................................................................................1

A. Stating the sources of finance which are available to the board of Directors of Bes Taste.........1

B. Stating the information which is offered by final accounts.........................................................1

C. Information need of different stakeholders..................................................................................2

TASK 2.................................................................................................................................................2

TASK 3.................................................................................................................................................4

A. Indicating the side such as debit or credit in which balance of the different accounts appear....4

B. Stating the purpose of trial balance..............................................................................................6

C. Computing the journal entries......................................................................................................6

TASK 4.................................................................................................................................................7

References............................................................................................................................................9

2

INTRODUCTION

Accounting is most important part of finance which serves information about the

transactions which are made by the firm during the accounting year. Through this, business entity is

able to frame strategic financial framework for the near future by evaluating the past performance

(Newell and Seabrook, 2006). The present report is based on the different case scenario which will

develop understanding about the sources of finance. Besides this, report will also shed light on the

various financial aspects which facilitate quick or effective decision making.

TASK 1

A. Stating the sources of finance which are available to the board of Directors of Bes Taste

On the basis the cited case scenario Bes taste which is the medium sized business

organization will invest in the building and other non-current assets to maximize the profit. In this,

company requires financial assistance for meeting the working capital requirements. In this,

business enterprise can raise finance by taking into consideration the internal and external sources

of finance (Nilsson, 2008). Bes Taste can make use of retained earnings which helps them in

performing the day to day activities in an effectual manner. Further, company can fulfil its financial

requirements by selling the non-profitable assets. Besides this, bank overdraft is also the most

suitable external source which offers financial assistance to the firm to the large extent. On the basis

of this aspect, it is suggested to the director of Bes Taste that they need to sale the fixed assets

which have no use in the further productive activities. It enables them to raise finance without

imposing huge monetary cost in front of the firm (Bennouna, Meredith and Marchant, 2010).

B. Stating the information which is offered by final accounts

Final accounts include income and cash flow statement as well as balance sheet. These

statements serve wide range of information to the management which helps them in making most

profitable and suitable business decisions. Income statement provides deeper insight about the

revenue which is generated by the firm over the expenses (Ondraczek, Komendantova and Patt,

2015). It helps business unit in assessing the areas of expenses which they need to control for

enhancing the profitability. Further, cash flow statement furnishes information about the operating,

investing and financing activities. Cash flow statement provides deeper insight about the inflow and

outflow of cash. On the basis of this, manager can determine the amount which they need to raise

for performing the business activities and functions. Along with it, balance sheet renders

information about the financial health and position of firm. By keeping this fact in mind manager of

the corporation is able to frame competent strategies and policies which help them in achieving

1

Accounting is most important part of finance which serves information about the

transactions which are made by the firm during the accounting year. Through this, business entity is

able to frame strategic financial framework for the near future by evaluating the past performance

(Newell and Seabrook, 2006). The present report is based on the different case scenario which will

develop understanding about the sources of finance. Besides this, report will also shed light on the

various financial aspects which facilitate quick or effective decision making.

TASK 1

A. Stating the sources of finance which are available to the board of Directors of Bes Taste

On the basis the cited case scenario Bes taste which is the medium sized business

organization will invest in the building and other non-current assets to maximize the profit. In this,

company requires financial assistance for meeting the working capital requirements. In this,

business enterprise can raise finance by taking into consideration the internal and external sources

of finance (Nilsson, 2008). Bes Taste can make use of retained earnings which helps them in

performing the day to day activities in an effectual manner. Further, company can fulfil its financial

requirements by selling the non-profitable assets. Besides this, bank overdraft is also the most

suitable external source which offers financial assistance to the firm to the large extent. On the basis

of this aspect, it is suggested to the director of Bes Taste that they need to sale the fixed assets

which have no use in the further productive activities. It enables them to raise finance without

imposing huge monetary cost in front of the firm (Bennouna, Meredith and Marchant, 2010).

B. Stating the information which is offered by final accounts

Final accounts include income and cash flow statement as well as balance sheet. These

statements serve wide range of information to the management which helps them in making most

profitable and suitable business decisions. Income statement provides deeper insight about the

revenue which is generated by the firm over the expenses (Ondraczek, Komendantova and Patt,

2015). It helps business unit in assessing the areas of expenses which they need to control for

enhancing the profitability. Further, cash flow statement furnishes information about the operating,

investing and financing activities. Cash flow statement provides deeper insight about the inflow and

outflow of cash. On the basis of this, manager can determine the amount which they need to raise

for performing the business activities and functions. Along with it, balance sheet renders

information about the financial health and position of firm. By keeping this fact in mind manager of

the corporation is able to frame competent strategies and policies which help them in achieving

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

success in the strategic business area (Thomas, 2009).

C. Information need of different stakeholders Investors: Shareholders makes assessment of the earning as well dividend per share in order

to determine the risk and return which is associated with the investment. Moreover,

investors invest money with the aim to aim to generate high return (Viviers and Cohen,

2011). Thus, shareholders do ratio analysis with the help of financial statements which helps

them in making suitable decision. Lenders: Financial and other lending institutions make assessment of the balance sheet to

evaluate the assets and financial obligations of the firm. By this, institution can assess the

financial capability of the business unit in an effectual manner. Employees: Income statement is undertaken by the personnel with the aim to assess the

profitability aspect of the business unit. By making evaluation of the income statement

employees can identify the monetary benefits which they will get in near future in terms of

highly salary, allowances and other fringe benefits (Pogue, 2010). Through this, human

resources of the firm is able to make decision about their career or future growth.

Customers: B2B customers make assessment of the financial statements in order to evaluate

the liquidity and solvency position of firm. Moreover, if profit and cash position of the firm

decreases then it also place impact on the growth and success of B2B customers.

General public: They are also the major stakeholders who make regular assessment of the

financial statements. It includes the potential shareholders who willing to invest in the shares

and securities of the business organization (Murphy and Yetmar, 2010).

TASK 2

A. Bank overdraft: It may be defined as a short term source of finance in which business entity can

withdraw money up to a certain limit when the current bank balance is drop out to zero. In this,

bank extends credit limit up to the maximum amount by taking into account the creditworthiness of

the customer or business entity. Advantage: It is the most effectual source of finance which helps business unit in meeting

their working capital requirements within the shorter time period (Nga and Yien 2013).

Disadvantage: Bank charges high interest for the overdraft facility which is offered by them.

This aspect impose high level of influence on the profitability aspect of the firm.

B: Trade credit: In this arrangement, business organization has opportunity to purchase the goods

on a credit basis. Under trade credit, company makes payment to supplier on a later date. Usually,

2

C. Information need of different stakeholders Investors: Shareholders makes assessment of the earning as well dividend per share in order

to determine the risk and return which is associated with the investment. Moreover,

investors invest money with the aim to aim to generate high return (Viviers and Cohen,

2011). Thus, shareholders do ratio analysis with the help of financial statements which helps

them in making suitable decision. Lenders: Financial and other lending institutions make assessment of the balance sheet to

evaluate the assets and financial obligations of the firm. By this, institution can assess the

financial capability of the business unit in an effectual manner. Employees: Income statement is undertaken by the personnel with the aim to assess the

profitability aspect of the business unit. By making evaluation of the income statement

employees can identify the monetary benefits which they will get in near future in terms of

highly salary, allowances and other fringe benefits (Pogue, 2010). Through this, human

resources of the firm is able to make decision about their career or future growth.

Customers: B2B customers make assessment of the financial statements in order to evaluate

the liquidity and solvency position of firm. Moreover, if profit and cash position of the firm

decreases then it also place impact on the growth and success of B2B customers.

General public: They are also the major stakeholders who make regular assessment of the

financial statements. It includes the potential shareholders who willing to invest in the shares

and securities of the business organization (Murphy and Yetmar, 2010).

TASK 2

A. Bank overdraft: It may be defined as a short term source of finance in which business entity can

withdraw money up to a certain limit when the current bank balance is drop out to zero. In this,

bank extends credit limit up to the maximum amount by taking into account the creditworthiness of

the customer or business entity. Advantage: It is the most effectual source of finance which helps business unit in meeting

their working capital requirements within the shorter time period (Nga and Yien 2013).

Disadvantage: Bank charges high interest for the overdraft facility which is offered by them.

This aspect impose high level of influence on the profitability aspect of the firm.

B: Trade credit: In this arrangement, business organization has opportunity to purchase the goods

on a credit basis. Under trade credit, company makes payment to supplier on a later date. Usually,

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

trade credit is given by supplier for 30, 60 and 90 days. Usually, suppliers offer such arrangement to

B2B customers to maximize their sales. Thus, this sources provides assistance to the business unit

in fulfilling their financial requirements to the great extent (Singh, Jain andYadav, 2012). Advantage: Trade credit system does not involve legal procedure which encourage business

entity to make use of this source of finance. Besides this, lower cost of finance is also one of

the main benefits which are offered by the trade credit system.

Disadvantage: This source of finance is highly expensive if business unit fails to make

payment on time.

C. Term loans: Business unit can also take financial assistance from bank in terms of short and long

term loan. Short term loan is provided by the bank for 0-1 year, whereas financial support which is

offered by the institution for more than one year then it is considered as long term loan. Interest is

the major income source of bank so they are always ready to give financial assistance to the

borrowers who are able to repay the amount on time (Rohrich, 2007). Thus, by approaching bank

for the loan on the basis of collateral security business entity can meet its financial need. Advantage: Tax concession and benefits influence organization to take loan for meeting the

financial needs or requirements.

Disadvantage: In bank loan, company has to repay the amount of loan in instalments with

interest on a periodical basis. This aspect imposes high financial burden in front of the

business unit (Hussain and Matlay, 2007).

D. Ordinary shares: Company can also raise finance by issuing the ordinary shares to the existing

and potential shareholders. In the present time, investors prefer to invest their money in shares with

the desire to earn high return. Thus, by issuing shares business unit is become able to raise fund in

an effectual manner.

Advantage: It is the cheaper source of finance because when company already has strategic

presence in the market then they do not require to spend more on advertisement and other

aspects (Kihn, 2011).

Disadvantage: In ordinary shares, business unit is obliged to involve their shareholders in

the decision making aspects. Due to this, interference of the shareholders increase in the

business affairs and practices.

E. Retained profits: This earning shows the capital which is available to the business unit after

making payment of dividend and taxes. Now, business unit prefers to keep the certain amount of

profit with itself to meet the contingent situation or obligations. Thus, business enterprise can meet

its financial need or requirements by making use of profit or amount which is retained by itself.

This source of finance does not impose any financial cost on the firm but it has opportunity cost.

3

B2B customers to maximize their sales. Thus, this sources provides assistance to the business unit

in fulfilling their financial requirements to the great extent (Singh, Jain andYadav, 2012). Advantage: Trade credit system does not involve legal procedure which encourage business

entity to make use of this source of finance. Besides this, lower cost of finance is also one of

the main benefits which are offered by the trade credit system.

Disadvantage: This source of finance is highly expensive if business unit fails to make

payment on time.

C. Term loans: Business unit can also take financial assistance from bank in terms of short and long

term loan. Short term loan is provided by the bank for 0-1 year, whereas financial support which is

offered by the institution for more than one year then it is considered as long term loan. Interest is

the major income source of bank so they are always ready to give financial assistance to the

borrowers who are able to repay the amount on time (Rohrich, 2007). Thus, by approaching bank

for the loan on the basis of collateral security business entity can meet its financial need. Advantage: Tax concession and benefits influence organization to take loan for meeting the

financial needs or requirements.

Disadvantage: In bank loan, company has to repay the amount of loan in instalments with

interest on a periodical basis. This aspect imposes high financial burden in front of the

business unit (Hussain and Matlay, 2007).

D. Ordinary shares: Company can also raise finance by issuing the ordinary shares to the existing

and potential shareholders. In the present time, investors prefer to invest their money in shares with

the desire to earn high return. Thus, by issuing shares business unit is become able to raise fund in

an effectual manner.

Advantage: It is the cheaper source of finance because when company already has strategic

presence in the market then they do not require to spend more on advertisement and other

aspects (Kihn, 2011).

Disadvantage: In ordinary shares, business unit is obliged to involve their shareholders in

the decision making aspects. Due to this, interference of the shareholders increase in the

business affairs and practices.

E. Retained profits: This earning shows the capital which is available to the business unit after

making payment of dividend and taxes. Now, business unit prefers to keep the certain amount of

profit with itself to meet the contingent situation or obligations. Thus, business enterprise can meet

its financial need or requirements by making use of profit or amount which is retained by itself.

This source of finance does not impose any financial cost on the firm but it has opportunity cost.

3

Advantage: Retained earning helps business unit in garbing the investment and most

profitable opportunities which aid in the growth and success of it (Dietrich, 2016).

Disadvantage: When, firm retains more profit with itself then it is unable to offer high

dividend to the shareholders which closely affects the corporate image of it.

TASK 3

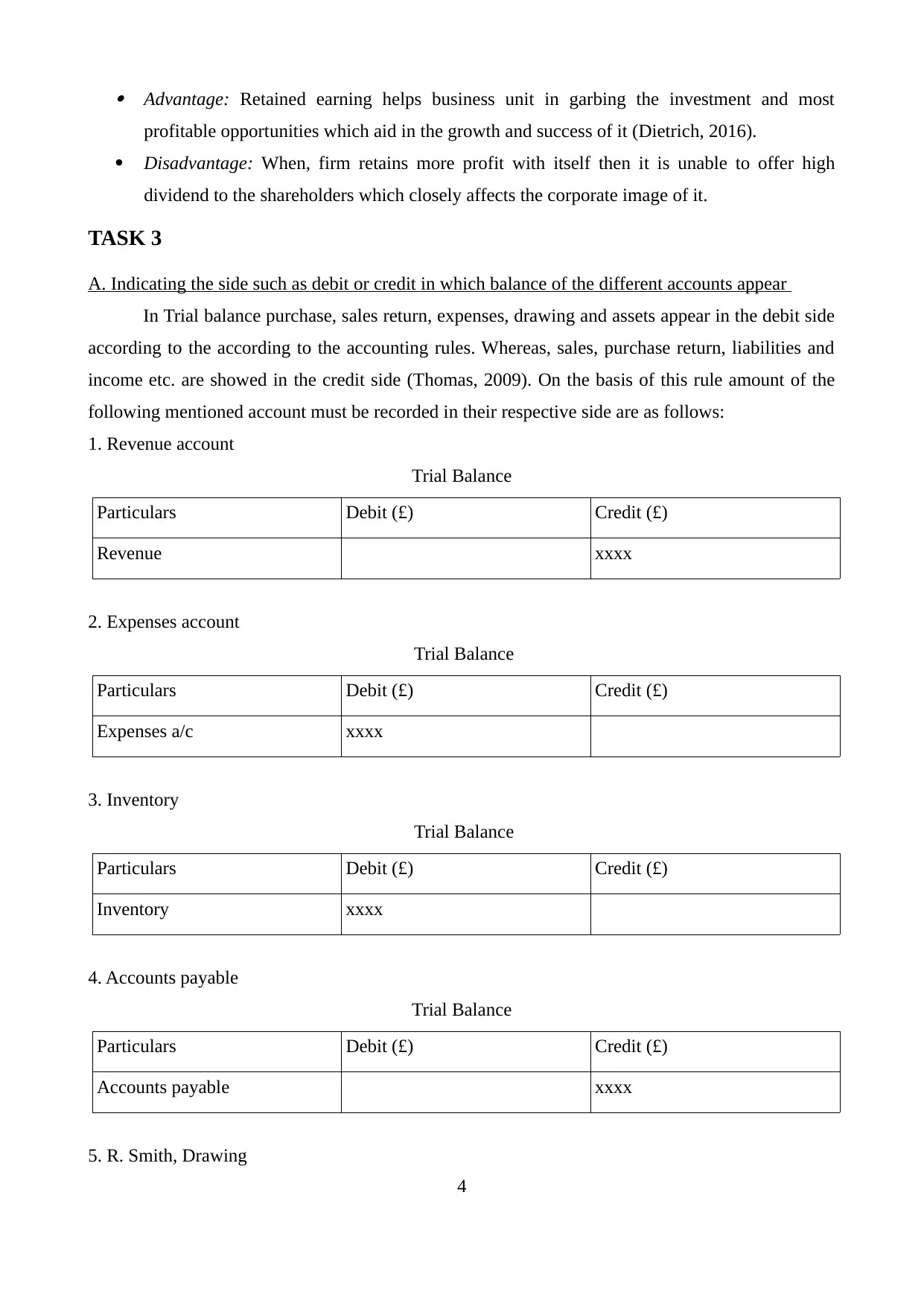

A. Indicating the side such as debit or credit in which balance of the different accounts appear

In Trial balance purchase, sales return, expenses, drawing and assets appear in the debit side

according to the according to the accounting rules. Whereas, sales, purchase return, liabilities and

income etc. are showed in the credit side (Thomas, 2009). On the basis of this rule amount of the

following mentioned account must be recorded in their respective side are as follows:

1. Revenue account

Trial Balance

Particulars Debit (£) Credit (£)

Revenue xxxx

2. Expenses account

Trial Balance

Particulars Debit (£) Credit (£)

Expenses a/c xxxx

3. Inventory

Trial Balance

Particulars Debit (£) Credit (£)

Inventory xxxx

4. Accounts payable

Trial Balance

Particulars Debit (£) Credit (£)

Accounts payable xxxx

5. R. Smith, Drawing

4

profitable opportunities which aid in the growth and success of it (Dietrich, 2016).

Disadvantage: When, firm retains more profit with itself then it is unable to offer high

dividend to the shareholders which closely affects the corporate image of it.

TASK 3

A. Indicating the side such as debit or credit in which balance of the different accounts appear

In Trial balance purchase, sales return, expenses, drawing and assets appear in the debit side

according to the according to the accounting rules. Whereas, sales, purchase return, liabilities and

income etc. are showed in the credit side (Thomas, 2009). On the basis of this rule amount of the

following mentioned account must be recorded in their respective side are as follows:

1. Revenue account

Trial Balance

Particulars Debit (£) Credit (£)

Revenue xxxx

2. Expenses account

Trial Balance

Particulars Debit (£) Credit (£)

Expenses a/c xxxx

3. Inventory

Trial Balance

Particulars Debit (£) Credit (£)

Inventory xxxx

4. Accounts payable

Trial Balance

Particulars Debit (£) Credit (£)

Accounts payable xxxx

5. R. Smith, Drawing

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

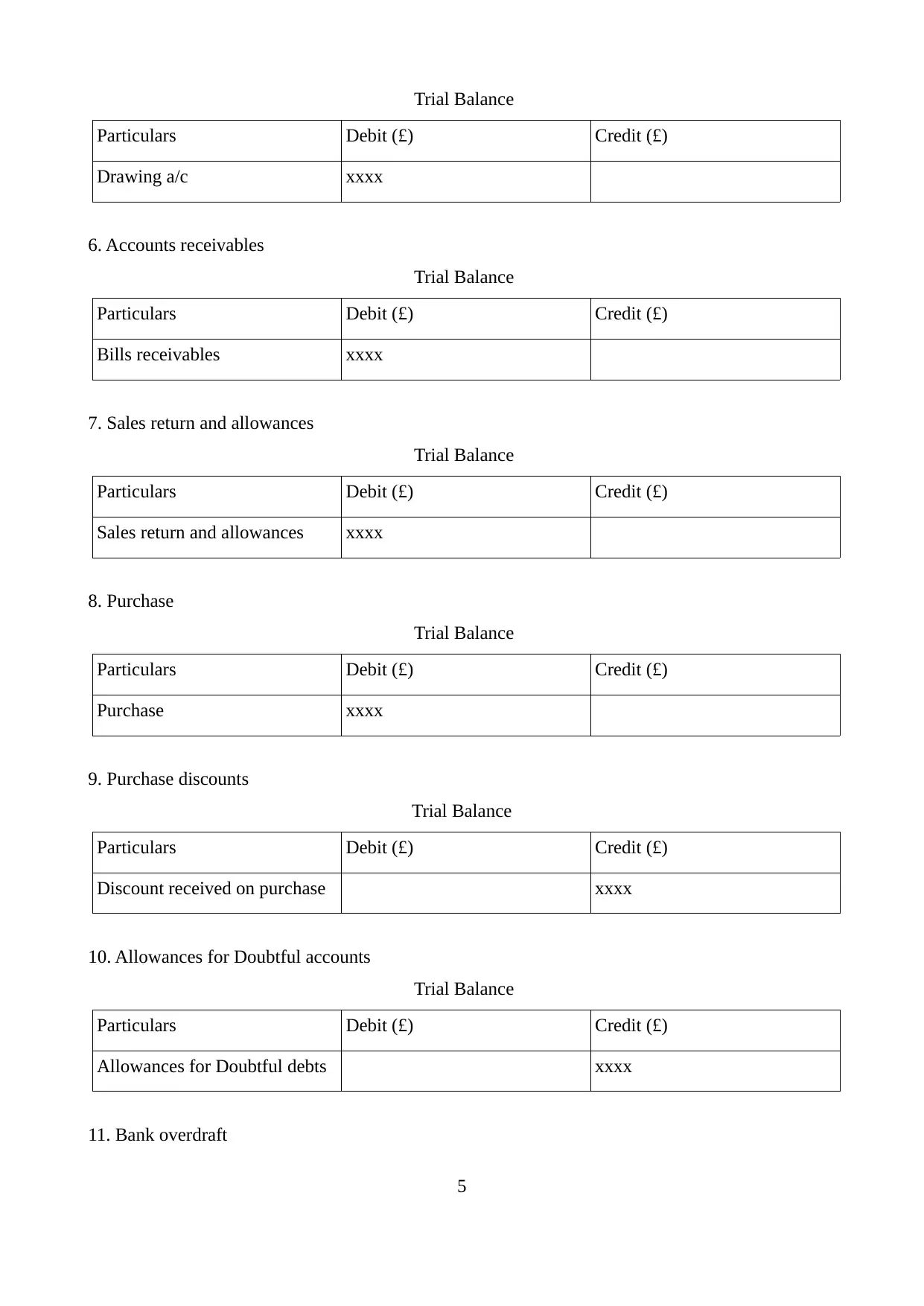

Trial Balance

Particulars Debit (£) Credit (£)

Drawing a/c xxxx

6. Accounts receivables

Trial Balance

Particulars Debit (£) Credit (£)

Bills receivables xxxx

7. Sales return and allowances

Trial Balance

Particulars Debit (£) Credit (£)

Sales return and allowances xxxx

8. Purchase

Trial Balance

Particulars Debit (£) Credit (£)

Purchase xxxx

9. Purchase discounts

Trial Balance

Particulars Debit (£) Credit (£)

Discount received on purchase xxxx

10. Allowances for Doubtful accounts

Trial Balance

Particulars Debit (£) Credit (£)

Allowances for Doubtful debts xxxx

11. Bank overdraft

5

Particulars Debit (£) Credit (£)

Drawing a/c xxxx

6. Accounts receivables

Trial Balance

Particulars Debit (£) Credit (£)

Bills receivables xxxx

7. Sales return and allowances

Trial Balance

Particulars Debit (£) Credit (£)

Sales return and allowances xxxx

8. Purchase

Trial Balance

Particulars Debit (£) Credit (£)

Purchase xxxx

9. Purchase discounts

Trial Balance

Particulars Debit (£) Credit (£)

Discount received on purchase xxxx

10. Allowances for Doubtful accounts

Trial Balance

Particulars Debit (£) Credit (£)

Allowances for Doubtful debts xxxx

11. Bank overdraft

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Trial Balance

Particulars Debit (£) Credit (£)

Bank overdraft xxxx

B. Stating the purpose of trial balance

Trial balance may be defined as a statement which present the summarized balance of ledger

account. It clearly provides information about the financial transactions which are made by the firm

during the accounting year. The main purpose behind the preparation of trial balance is to detect the

errors which are prevailed in the double entry system (Nga and Yien, 2013). By preparing trial

balance business unit can identify the mathematical errors in the best possible manner. In this, assets

and expenses are shown in the debit side whereas, liabilities as well as income is appeared in the

credit side. It is the prior step of the preparation of financial statements. Thus, each and every

business unit prepares trial balance which helps them in designing the final accounts more

effectively.

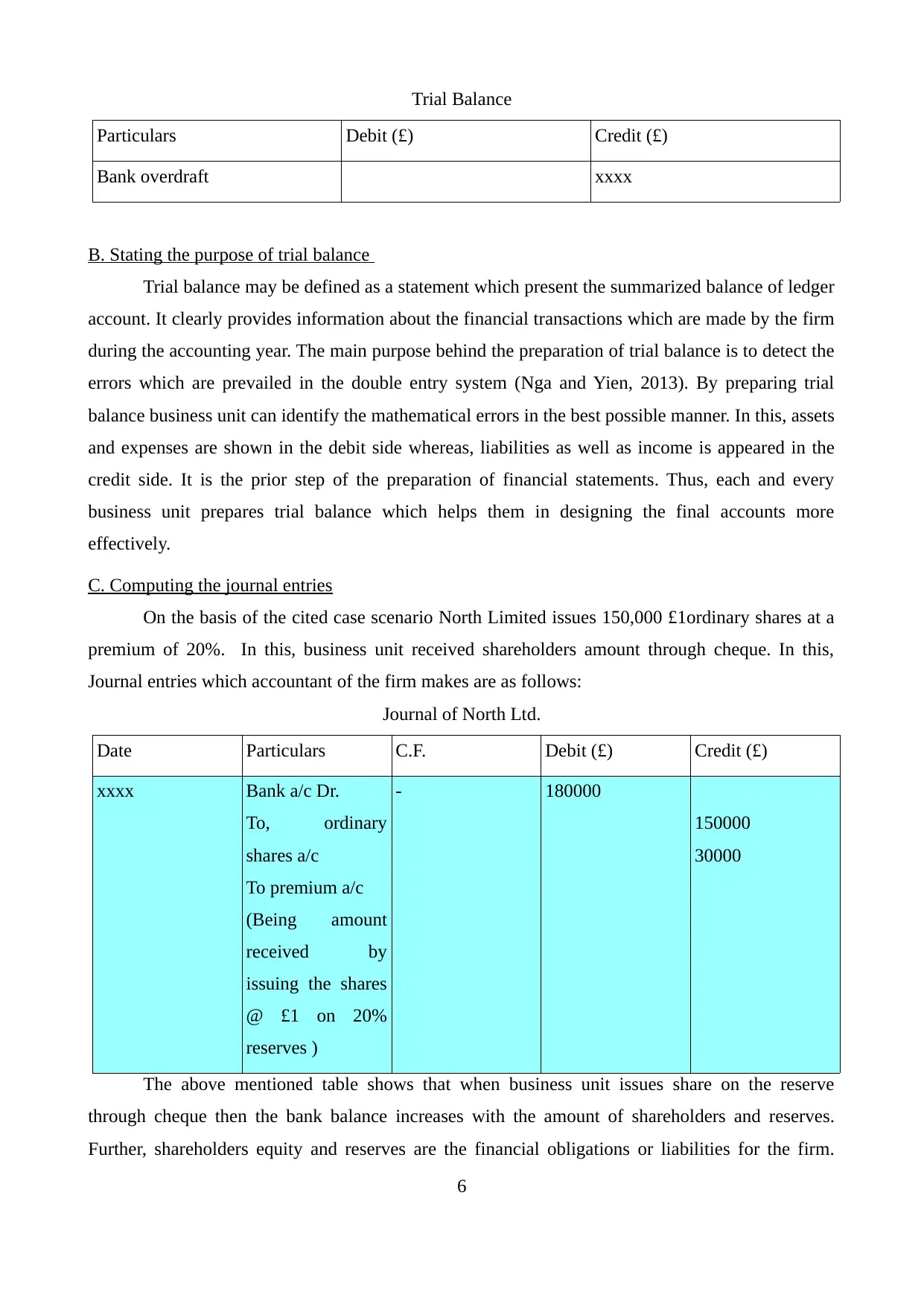

C. Computing the journal entries

On the basis of the cited case scenario North Limited issues 150,000 £1ordinary shares at a

premium of 20%. In this, business unit received shareholders amount through cheque. In this,

Journal entries which accountant of the firm makes are as follows:

Journal of North Ltd.

Date Particulars C.F. Debit (£) Credit (£)

xxxx Bank a/c Dr.

To, ordinary

shares a/c

To premium a/c

(Being amount

received by

issuing the shares

@ £1 on 20%

reserves )

- 180000

150000

30000

The above mentioned table shows that when business unit issues share on the reserve

through cheque then the bank balance increases with the amount of shareholders and reserves.

Further, shareholders equity and reserves are the financial obligations or liabilities for the firm.

6

Particulars Debit (£) Credit (£)

Bank overdraft xxxx

B. Stating the purpose of trial balance

Trial balance may be defined as a statement which present the summarized balance of ledger

account. It clearly provides information about the financial transactions which are made by the firm

during the accounting year. The main purpose behind the preparation of trial balance is to detect the

errors which are prevailed in the double entry system (Nga and Yien, 2013). By preparing trial

balance business unit can identify the mathematical errors in the best possible manner. In this, assets

and expenses are shown in the debit side whereas, liabilities as well as income is appeared in the

credit side. It is the prior step of the preparation of financial statements. Thus, each and every

business unit prepares trial balance which helps them in designing the final accounts more

effectively.

C. Computing the journal entries

On the basis of the cited case scenario North Limited issues 150,000 £1ordinary shares at a

premium of 20%. In this, business unit received shareholders amount through cheque. In this,

Journal entries which accountant of the firm makes are as follows:

Journal of North Ltd.

Date Particulars C.F. Debit (£) Credit (£)

xxxx Bank a/c Dr.

To, ordinary

shares a/c

To premium a/c

(Being amount

received by

issuing the shares

@ £1 on 20%

reserves )

- 180000

150000

30000

The above mentioned table shows that when business unit issues share on the reserve

through cheque then the bank balance increases with the amount of shareholders and reserves.

Further, shareholders equity and reserves are the financial obligations or liabilities for the firm.

6

Therefore, they are credited in the account of north Ltd.

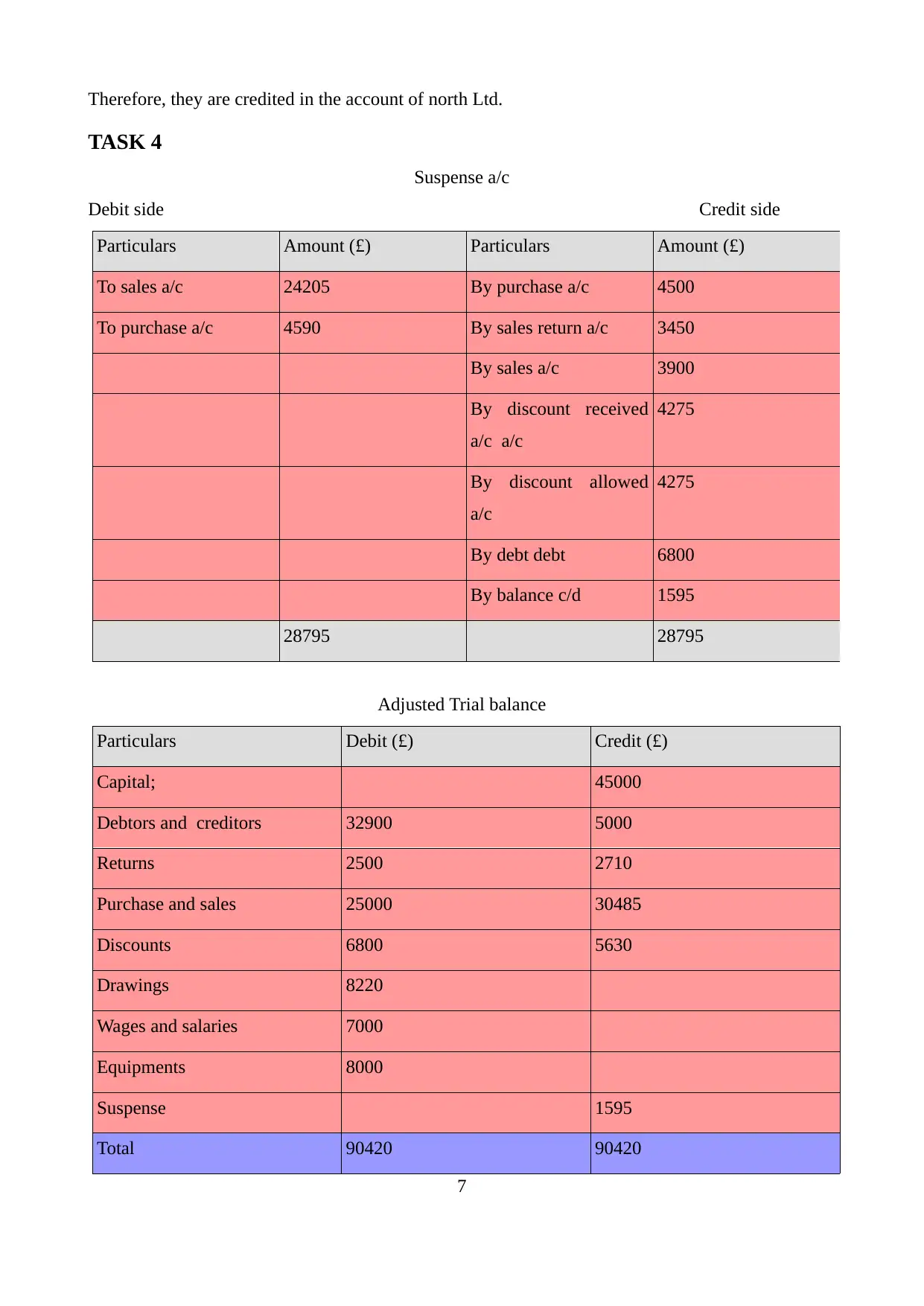

TASK 4

Suspense a/c

Debit side Credit side

Particulars Amount (£) Particulars Amount (£)

To sales a/c 24205 By purchase a/c 4500

To purchase a/c 4590 By sales return a/c 3450

By sales a/c 3900

By discount received

a/c a/c

4275

By discount allowed

a/c

4275

By debt debt 6800

By balance c/d 1595

28795 28795

Adjusted Trial balance

Particulars Debit (£) Credit (£)

Capital; 45000

Debtors and creditors 32900 5000

Returns 2500 2710

Purchase and sales 25000 30485

Discounts 6800 5630

Drawings 8220

Wages and salaries 7000

Equipments 8000

Suspense 1595

Total 90420 90420

7

TASK 4

Suspense a/c

Debit side Credit side

Particulars Amount (£) Particulars Amount (£)

To sales a/c 24205 By purchase a/c 4500

To purchase a/c 4590 By sales return a/c 3450

By sales a/c 3900

By discount received

a/c a/c

4275

By discount allowed

a/c

4275

By debt debt 6800

By balance c/d 1595

28795 28795

Adjusted Trial balance

Particulars Debit (£) Credit (£)

Capital; 45000

Debtors and creditors 32900 5000

Returns 2500 2710

Purchase and sales 25000 30485

Discounts 6800 5630

Drawings 8220

Wages and salaries 7000

Equipments 8000

Suspense 1595

Total 90420 90420

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

On the basis of the above mentioned table business unit needs to open suspense account with

the amount of £1595 which helps them in balancing both debit and credit side. With the help of this

trial balance business entity is become able to prepare appropriate financial statements in an

effectual manner.

8

the amount of £1595 which helps them in balancing both debit and credit side. With the help of this

trial balance business entity is become able to prepare appropriate financial statements in an

effectual manner.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.