BIZ201: Accounting for Decision Making Report - Sales and Marketing

VerifiedAdded on 2022/12/16

|8

|1147

|450

Report

AI Summary

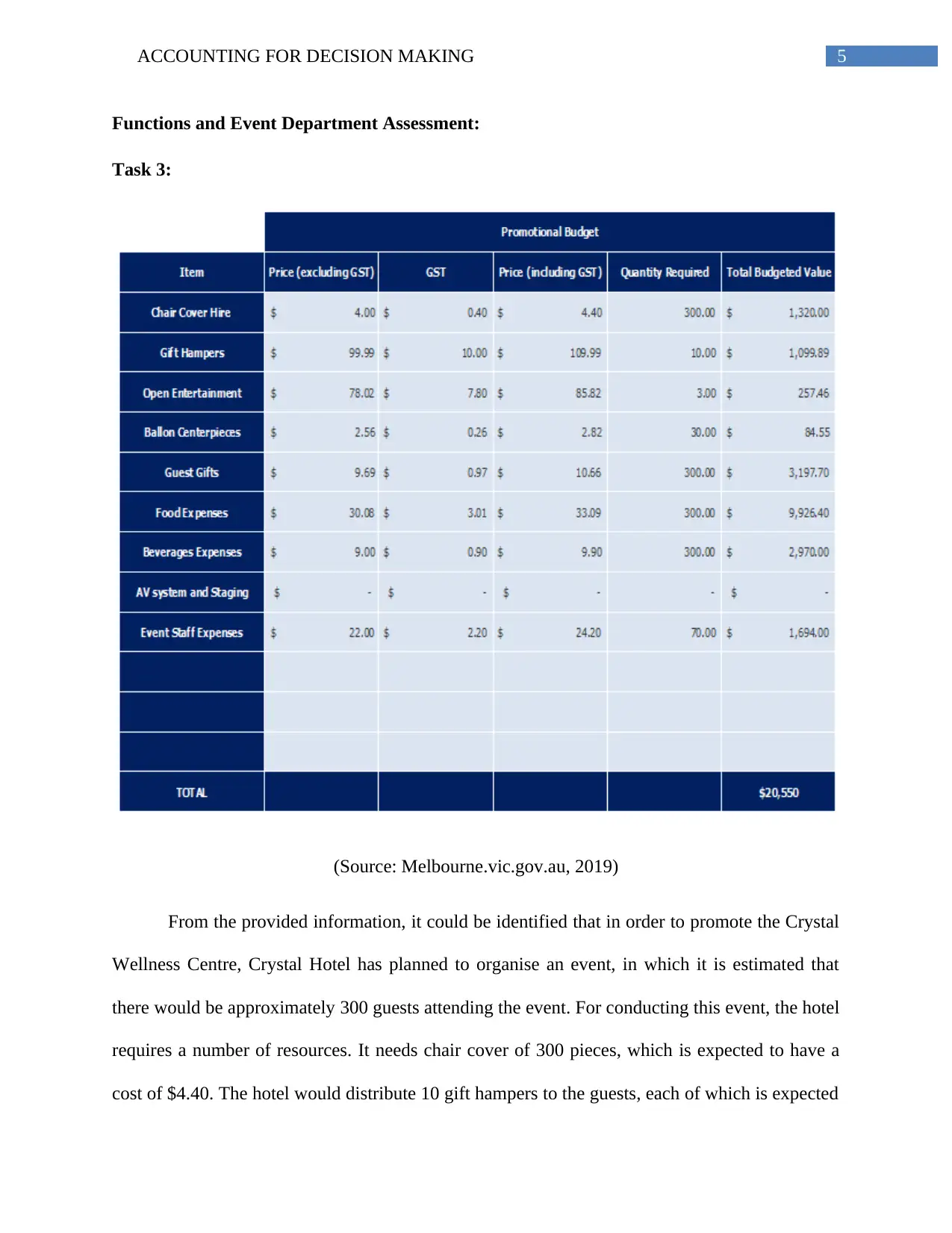

This report analyzes accounting for decision-making, using a case study of Crystal Hotel. It assesses the viability of a membership project using Net Present Value (NPV), highlighting its positive impact on the hotel's return on investment. The report also applies Cost-Volume-Profit (CVP) analysis to determine break-even points and aid in price-setting decisions. Furthermore, it details the planning and budgeting for a Crystal Wellness Centre event, including resource allocation and expense management. The report references financial accounting principles, managerial accounting techniques, and provides a comprehensive overview of financial decision-making processes within the hotel context.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.