Accounting and Finance Report: RACCA, RECKTURK, ROCKHAM PLC Analysis

VerifiedAdded on 2023/01/11

|22

|3891

|60

Report

AI Summary

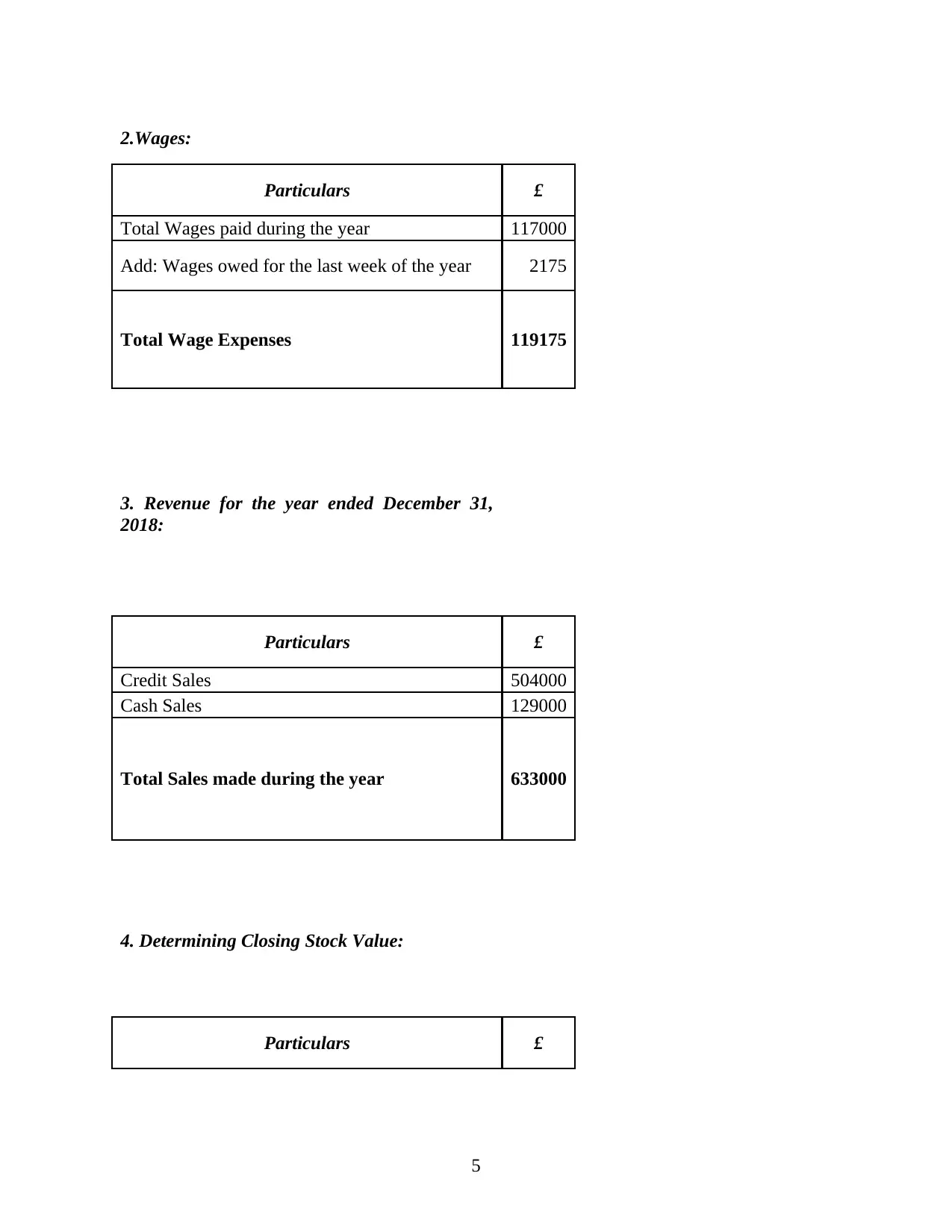

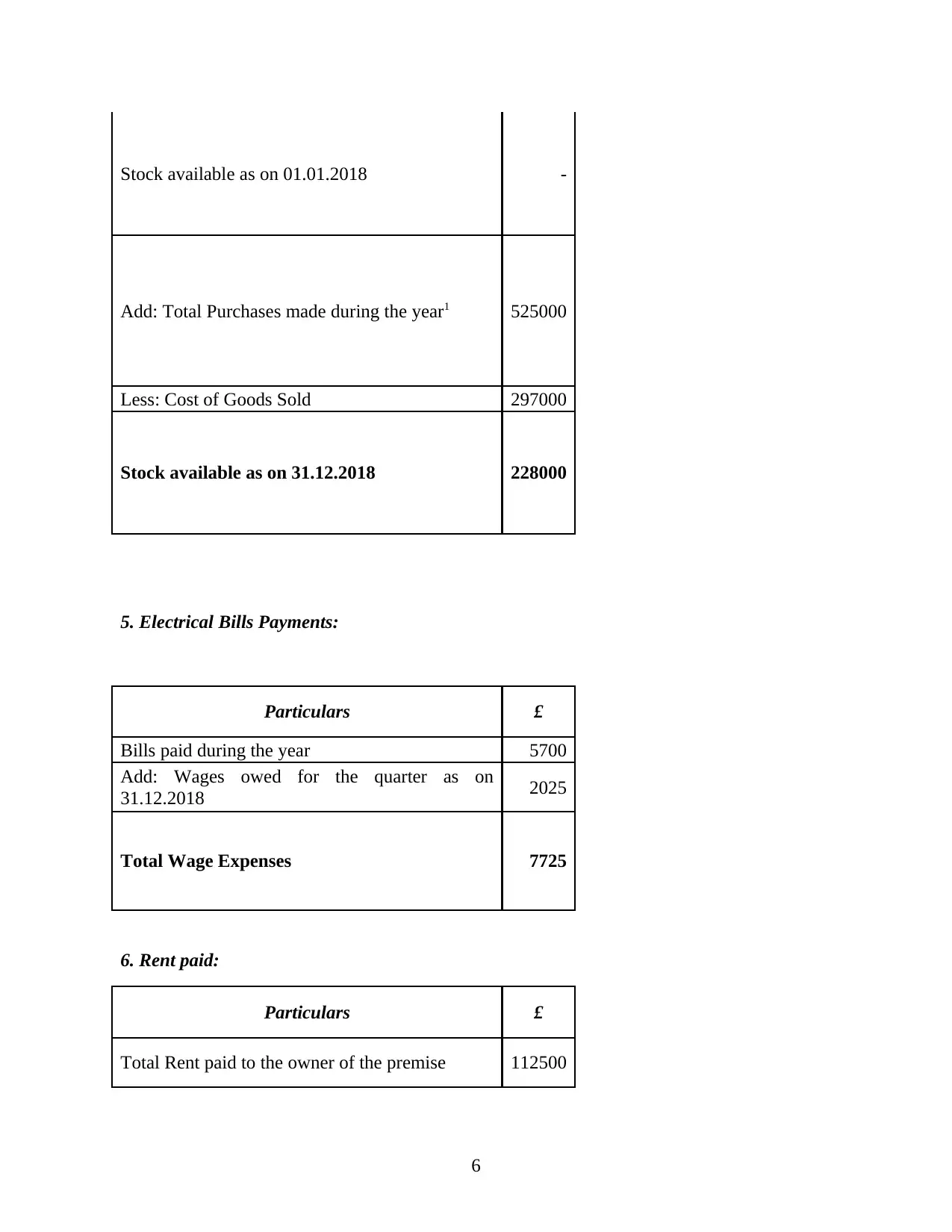

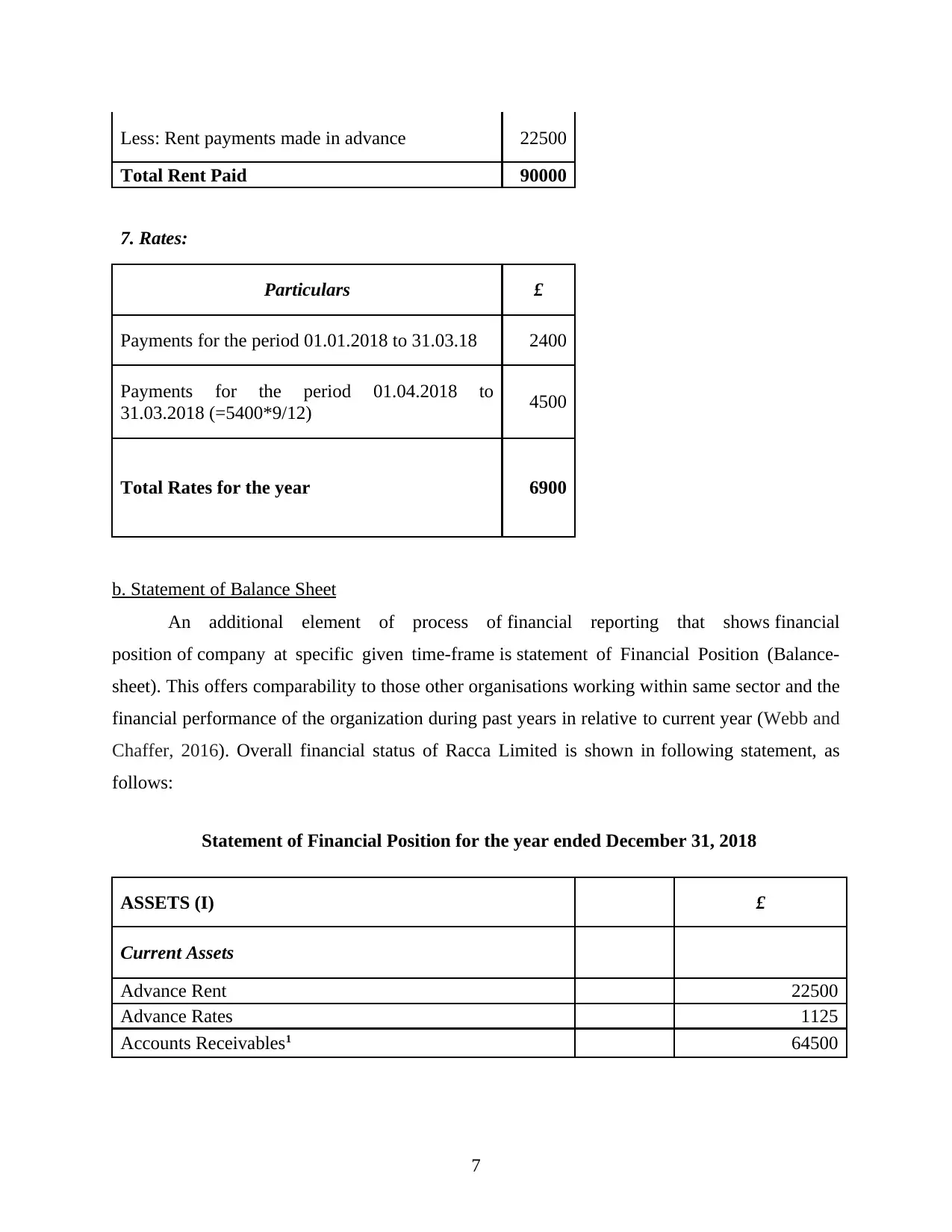

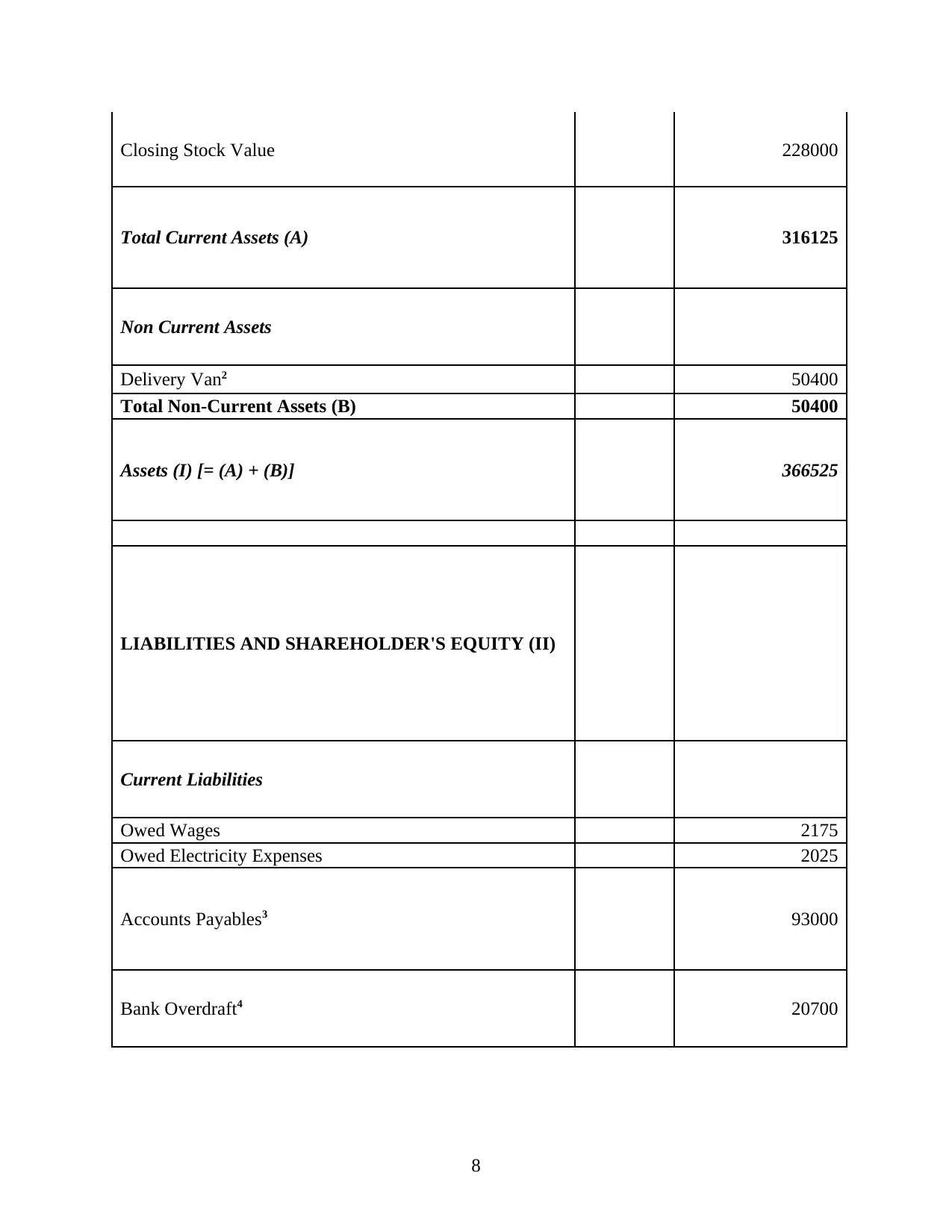

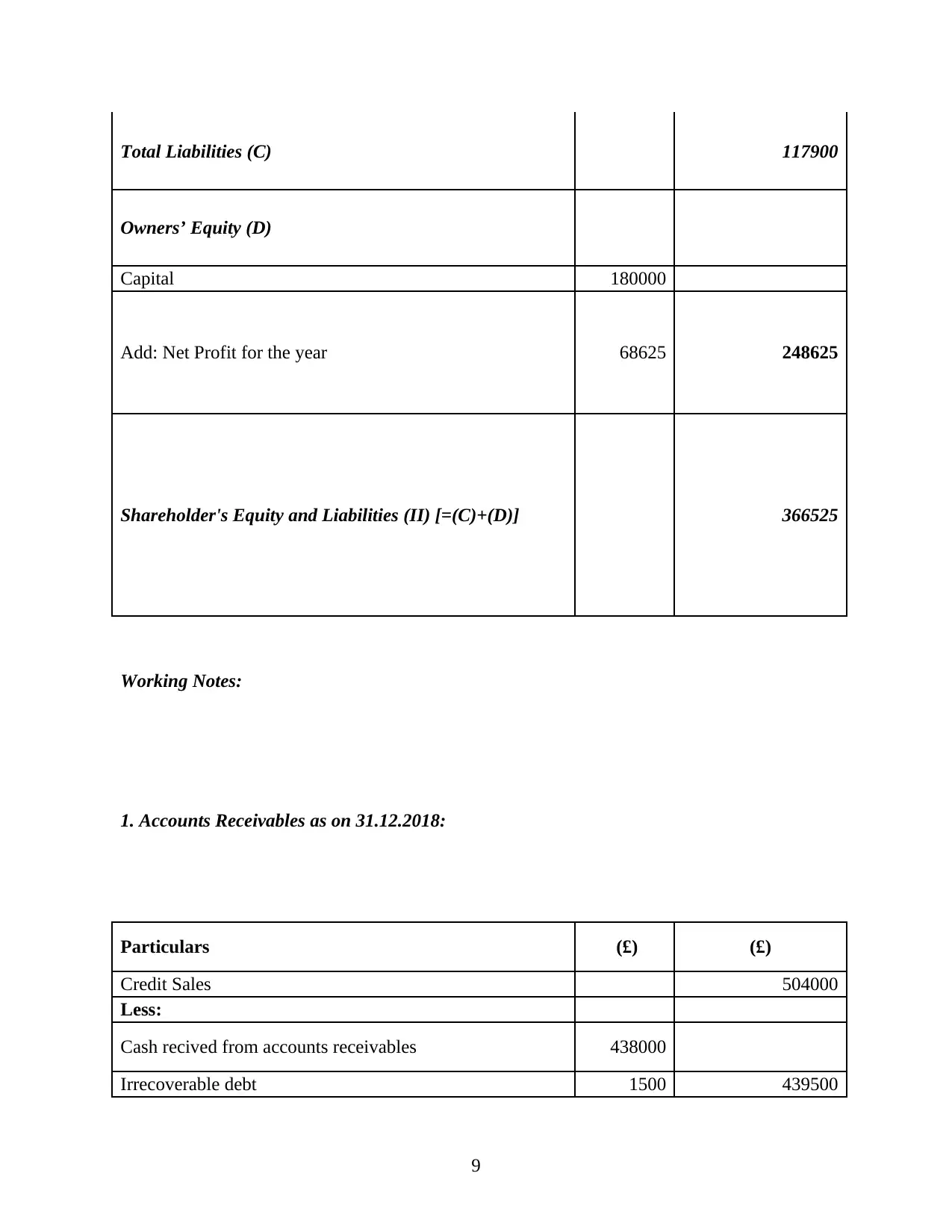

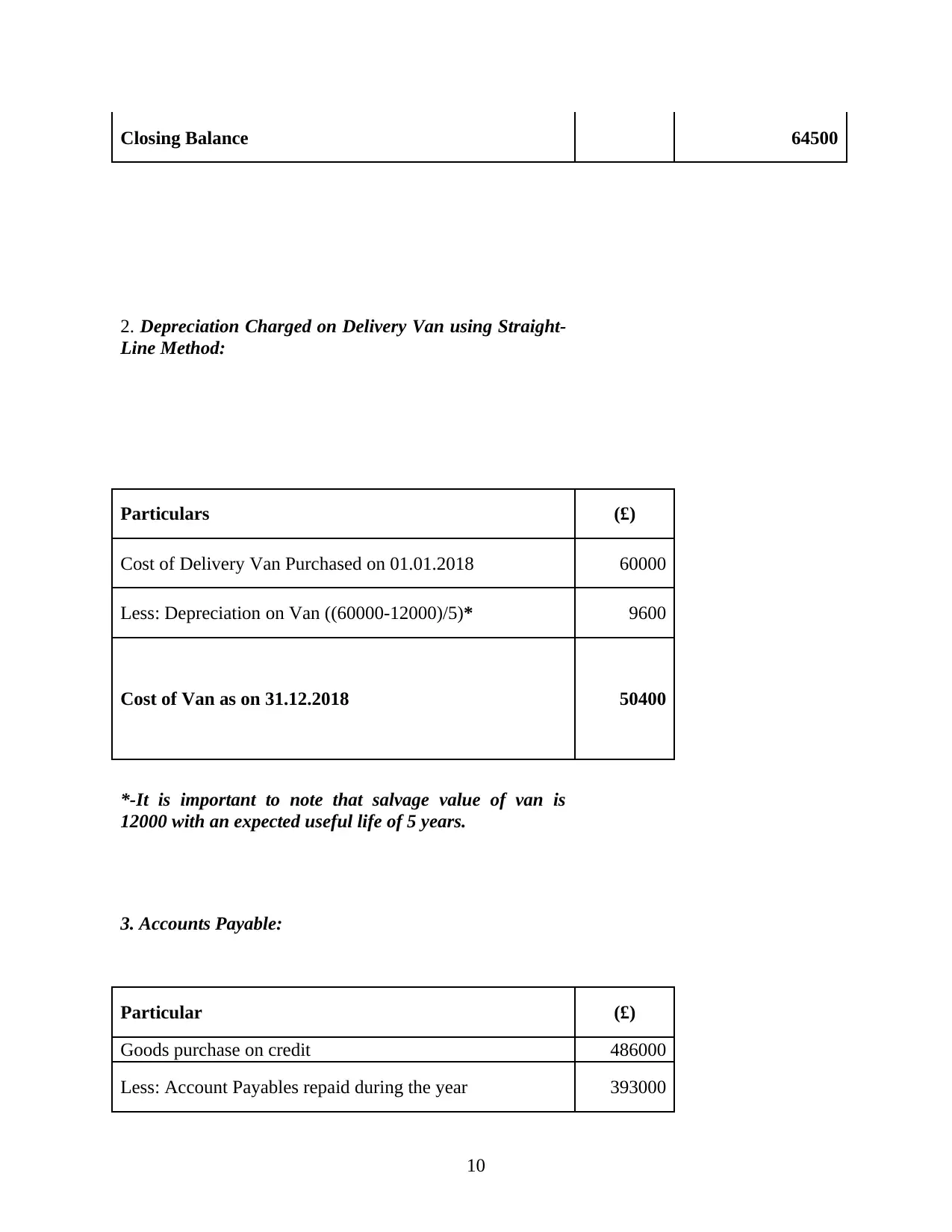

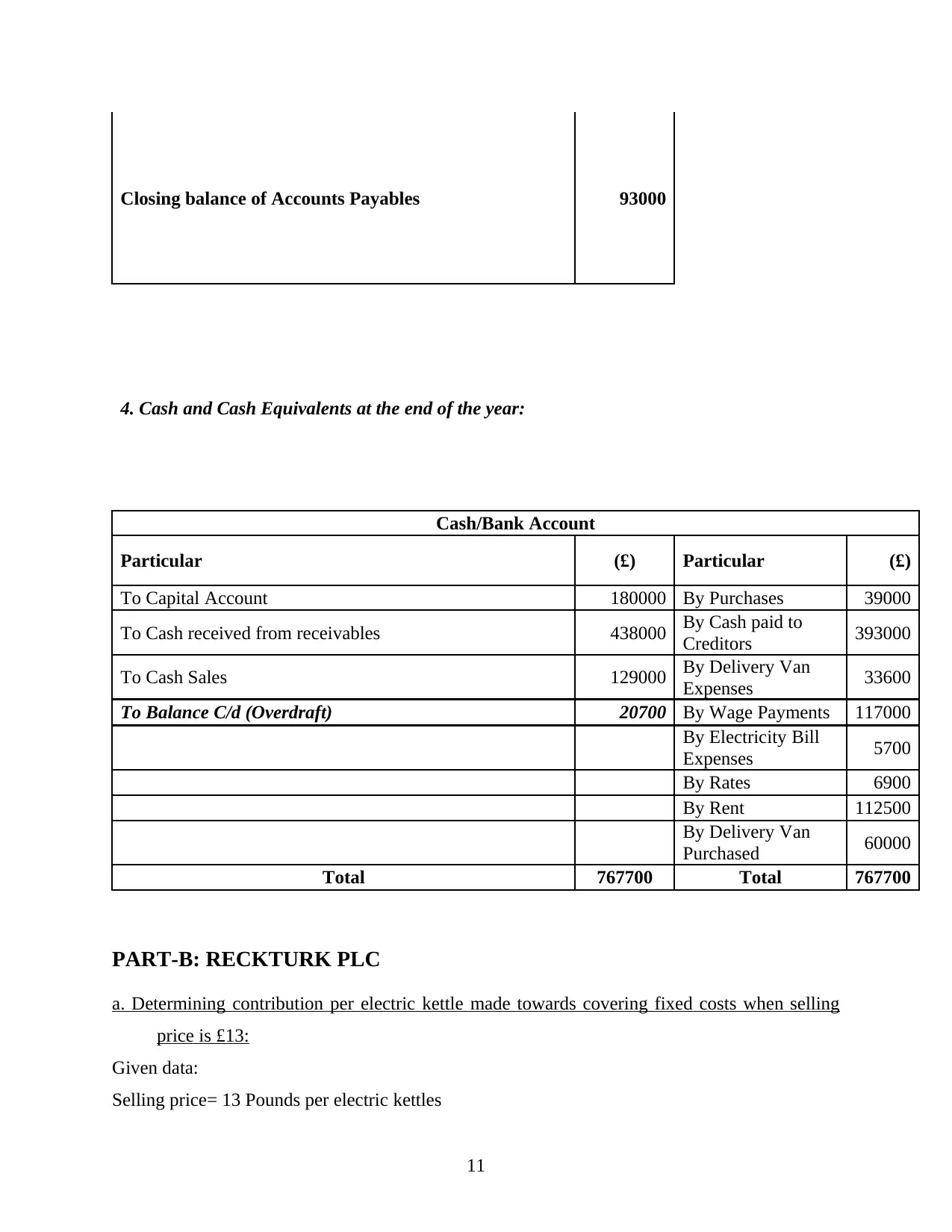

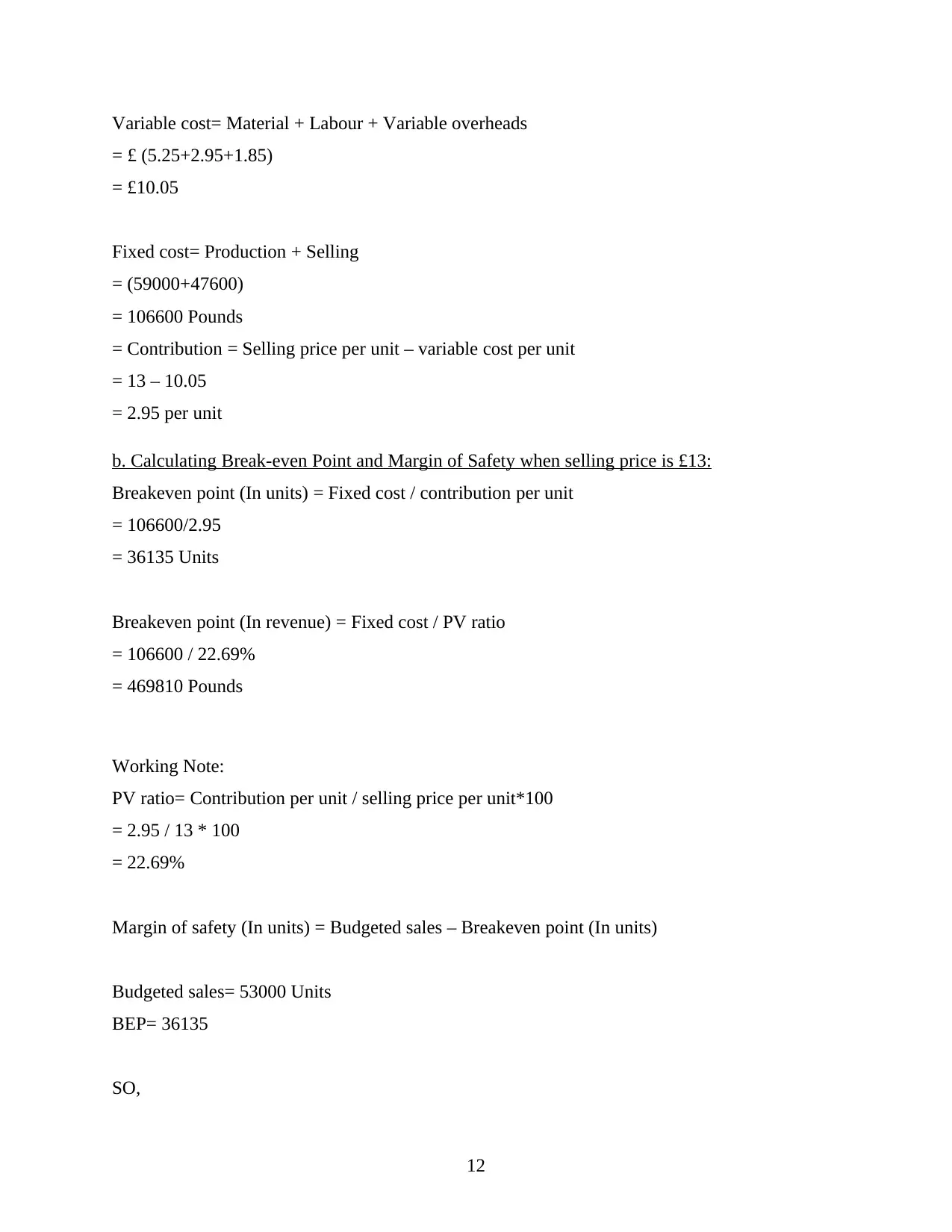

This report offers a detailed analysis of accounting and finance principles, focusing on the financial performance and strategic decisions of RACCA Limited, RECKTURK PLC, and ROCKHAM PLC. The report begins with the preparation of a profit and loss statement and balance sheet for RACCA Limited, providing insights into its financial position. It then delves into RECKTURK PLC, calculating contribution per unit, break-even points, margin of safety, and profit analysis under different scenarios. Furthermore, the report assesses the company's strategy, including an examination of break-even model assumptions. Finally, the report evaluates capital budgeting projects for ROCKHAM PLC using investment appraisal techniques such as payback period, accounting rate of return (ARR), and net present value (NPV), providing recommendations based on the analysis. The report also discusses the merits and limitations of these techniques and the use of budgets as a strategic planning tool.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.