Finance Report: Accounting and Finance Module, Semester 1

VerifiedAdded on 2022/09/14

|16

|2222

|11

Report

AI Summary

This finance report comprehensively addresses various aspects of accounting and finance. It begins with an analysis of future value calculations, followed by a detailed examination of net present value (NPV) under different discount rates. The report then delves into personal financial planning, including retirement savings and the calculation of future asset values. Furthermore, it explores real and nominal interest rates, notional interest, and their implications. The report also covers topics like demand-pull inflation, the dividend imputation system, and holding period returns for stocks. The report also includes the Capital Asset Pricing Model (CAPM) and portfolio beta calculations. It concludes with an overview of portfolio weighting and return analysis.

Running head: ACCOUNTING AND FINANCE

-

Accounting and Finance

Name of the Student:

Name of the University:

Author’s Note:

-

Accounting and Finance

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING AND FINANCE

Table of Contents

Answer to question 1:......................................................................................................................3

Part (a):........................................................................................................................................3

Part (b):........................................................................................................................................3

Sub part (i):..............................................................................................................................3

Sub part (ii):.............................................................................................................................4

Part (c):........................................................................................................................................5

Sub part (i):..............................................................................................................................5

Sub part (ii):.............................................................................................................................6

Answer to question 2:......................................................................................................................6

Part (a):........................................................................................................................................6

Sub part (i):..............................................................................................................................6

Sub part (ii):.............................................................................................................................7

Sub part (iii):............................................................................................................................7

Sub part (iv):............................................................................................................................7

Part (b):........................................................................................................................................7

Answer to question 3:......................................................................................................................7

Part (a):........................................................................................................................................7

Sub part (i):..............................................................................................................................7

Table of Contents

Answer to question 1:......................................................................................................................3

Part (a):........................................................................................................................................3

Part (b):........................................................................................................................................3

Sub part (i):..............................................................................................................................3

Sub part (ii):.............................................................................................................................4

Part (c):........................................................................................................................................5

Sub part (i):..............................................................................................................................5

Sub part (ii):.............................................................................................................................6

Answer to question 2:......................................................................................................................6

Part (a):........................................................................................................................................6

Sub part (i):..............................................................................................................................6

Sub part (ii):.............................................................................................................................7

Sub part (iii):............................................................................................................................7

Sub part (iv):............................................................................................................................7

Part (b):........................................................................................................................................7

Answer to question 3:......................................................................................................................7

Part (a):........................................................................................................................................7

Sub part (i):..............................................................................................................................7

2ACCOUNTING AND FINANCE

Sub part (ii):.............................................................................................................................8

Part (b):........................................................................................................................................8

Part (c):........................................................................................................................................9

Sub part (i) & (ii):....................................................................................................................9

Sub part (iii):............................................................................................................................9

Part (d):......................................................................................................................................10

Sub part (i) & (ii):..................................................................................................................10

Sub part (iii):..........................................................................................................................10

Sub part (iv):..........................................................................................................................11

Sub part (v):...........................................................................................................................11

Sub part (vi):..........................................................................................................................11

Sub part (vii):.........................................................................................................................11

Sub part (viii):........................................................................................................................12

Sub part (ix):..........................................................................................................................13

Sub part (x):...........................................................................................................................13

References and bibliography:........................................................................................................14

Sub part (ii):.............................................................................................................................8

Part (b):........................................................................................................................................8

Part (c):........................................................................................................................................9

Sub part (i) & (ii):....................................................................................................................9

Sub part (iii):............................................................................................................................9

Part (d):......................................................................................................................................10

Sub part (i) & (ii):..................................................................................................................10

Sub part (iii):..........................................................................................................................10

Sub part (iv):..........................................................................................................................11

Sub part (v):...........................................................................................................................11

Sub part (vi):..........................................................................................................................11

Sub part (vii):.........................................................................................................................11

Sub part (viii):........................................................................................................................12

Sub part (ix):..........................................................................................................................13

Sub part (x):...........................................................................................................................13

References and bibliography:........................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING AND FINANCE

Answer to question 1:

Part (a):

Number of years till the expected date of admission (n) = 5

Annual interest rate applicable (i) = 4% (Interest is compounded monthly)

Formula for Future Value of annuity due (FV) = PMT ×

( (1+ 4 %

12 )5× 12

−1

4 %

12 )=$ 60000

Where Future value will be 60000, Interest Rate will be 4% and the time period will be around 5

years of time.

Annual deposit to be made to build the fund (PMT) =

$ 60,000

( (1+ 4 %

12 )5× 12

−1

4 %

12 )=$ 904.99

Part (b):

Sub part (i):

Formula NPV = ⨊(P/ (1+i)t ) – C, where P = Net Period Cash Flow, i = Discount Rate (or rate

of return), t = Number of time periods and C = Initial Investment.

End of year Cash inflows ($mil) Present Value Factor

@10%

PV of cash inflows

($mil)

Answer to question 1:

Part (a):

Number of years till the expected date of admission (n) = 5

Annual interest rate applicable (i) = 4% (Interest is compounded monthly)

Formula for Future Value of annuity due (FV) = PMT ×

( (1+ 4 %

12 )5× 12

−1

4 %

12 )=$ 60000

Where Future value will be 60000, Interest Rate will be 4% and the time period will be around 5

years of time.

Annual deposit to be made to build the fund (PMT) =

$ 60,000

( (1+ 4 %

12 )5× 12

−1

4 %

12 )=$ 904.99

Part (b):

Sub part (i):

Formula NPV = ⨊(P/ (1+i)t ) – C, where P = Net Period Cash Flow, i = Discount Rate (or rate

of return), t = Number of time periods and C = Initial Investment.

End of year Cash inflows ($mil) Present Value Factor

@10%

PV of cash inflows

($mil)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING AND FINANCE

1 1.8 1

( 1+ 10 % )1 1.64

2 3.0 1

( 1+ 10 % )2 2.48

3 6.5 1

( 1+ 10 % ) 3 4.88

4 8.4 1

( 1+ 10 % )4 5.74

5 12.3 1

( 1+ 10 % ) 5 7.64

Total of present value of cash inflows. 32

Total Investment made at the beginning. 20

Net present value (NPV) of the investment = (22.38−20) 2.38

It can be observed that, the expected rate of in the given case study is 10%. Therefore, the

project appraisal can be conducted using the net present value techniques by discounting the cash

inflows and outflows at a discount rate of 10%. The computed net present value for the

investment considering a 10% discounting rate is positive; hence, the investment option can be

accepted.

Sub part (ii):

End of year Cash inflow ($mil) Present Value Factor

@15%

PV of cash inflow

($mil)

1 1.8 1

( 1+ 15 % ) 1 1.57

1 1.8 1

( 1+ 10 % )1 1.64

2 3.0 1

( 1+ 10 % )2 2.48

3 6.5 1

( 1+ 10 % ) 3 4.88

4 8.4 1

( 1+ 10 % )4 5.74

5 12.3 1

( 1+ 10 % ) 5 7.64

Total of present value of cash inflows. 32

Total Investment made at the beginning. 20

Net present value (NPV) of the investment = (22.38−20) 2.38

It can be observed that, the expected rate of in the given case study is 10%. Therefore, the

project appraisal can be conducted using the net present value techniques by discounting the cash

inflows and outflows at a discount rate of 10%. The computed net present value for the

investment considering a 10% discounting rate is positive; hence, the investment option can be

accepted.

Sub part (ii):

End of year Cash inflow ($mil) Present Value Factor

@15%

PV of cash inflow

($mil)

1 1.8 1

( 1+ 15 % ) 1 1.57

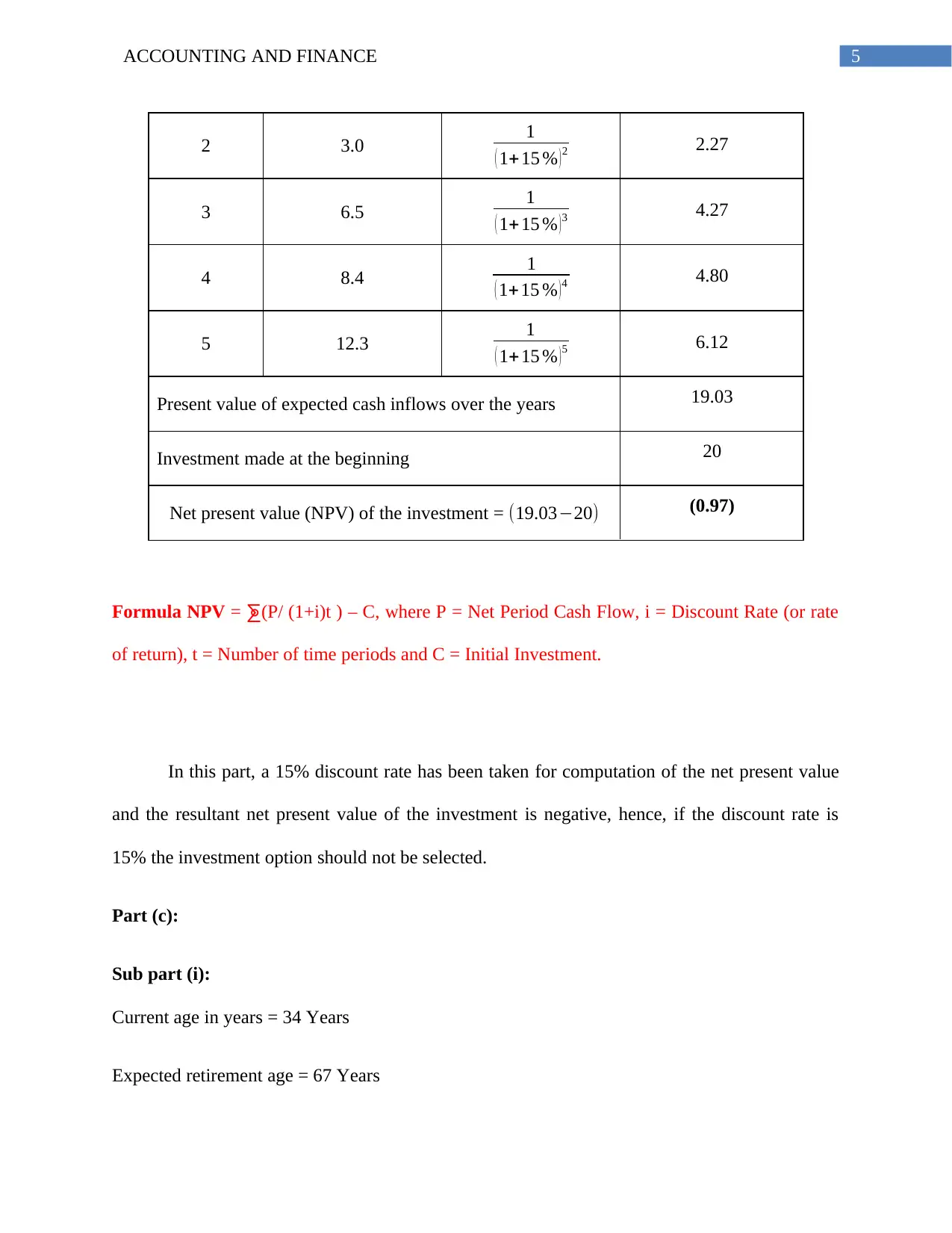

5ACCOUNTING AND FINANCE

2 3.0 1

( 1+ 15 % )2 2.27

3 6.5 1

( 1+ 15 % ) 3 4.27

4 8.4 1

( 1+ 15 % )4 4.80

5 12.3 1

( 1+ 15 % ) 5 6.12

Present value of expected cash inflows over the years 19.03

Investment made at the beginning 20

Net present value (NPV) of the investment = (19.03−20) (0.97)

Formula NPV = ⨊(P/ (1+i)t ) – C, where P = Net Period Cash Flow, i = Discount Rate (or rate

of return), t = Number of time periods and C = Initial Investment.

In this part, a 15% discount rate has been taken for computation of the net present value

and the resultant net present value of the investment is negative, hence, if the discount rate is

15% the investment option should not be selected.

Part (c):

Sub part (i):

Current age in years = 34 Years

Expected retirement age = 67 Years

2 3.0 1

( 1+ 15 % )2 2.27

3 6.5 1

( 1+ 15 % ) 3 4.27

4 8.4 1

( 1+ 15 % )4 4.80

5 12.3 1

( 1+ 15 % ) 5 6.12

Present value of expected cash inflows over the years 19.03

Investment made at the beginning 20

Net present value (NPV) of the investment = (19.03−20) (0.97)

Formula NPV = ⨊(P/ (1+i)t ) – C, where P = Net Period Cash Flow, i = Discount Rate (or rate

of return), t = Number of time periods and C = Initial Investment.

In this part, a 15% discount rate has been taken for computation of the net present value

and the resultant net present value of the investment is negative, hence, if the discount rate is

15% the investment option should not be selected.

Part (c):

Sub part (i):

Current age in years = 34 Years

Expected retirement age = 67 Years

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING AND FINANCE

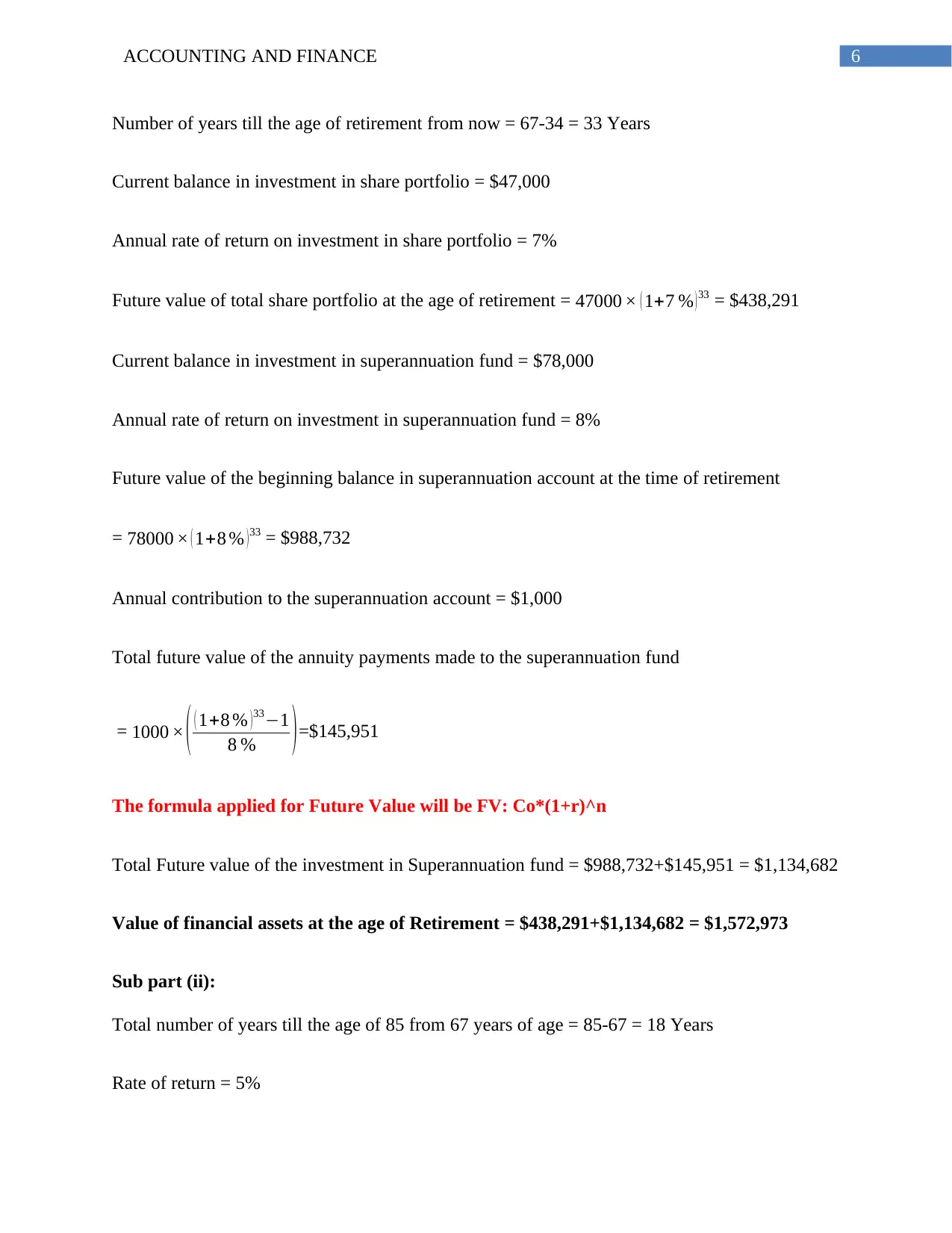

Number of years till the age of retirement from now = 67-34 = 33 Years

Current balance in investment in share portfolio = $47,000

Annual rate of return on investment in share portfolio = 7%

Future value of total share portfolio at the age of retirement = 47000 × ( 1+7 % ) 33 = $438,291

Current balance in investment in superannuation fund = $78,000

Annual rate of return on investment in superannuation fund = 8%

Future value of the beginning balance in superannuation account at the time of retirement

= 78000 × ( 1+8 % ) 33 = $988,732

Annual contribution to the superannuation account = $1,000

Total future value of the annuity payments made to the superannuation fund

= 1000 × ( ( 1+8 % ) 33−1

8 % )=$145,951

The formula applied for Future Value will be FV: Co*(1+r)^n

Total Future value of the investment in Superannuation fund = $988,732+$145,951 = $1,134,682

Value of financial assets at the age of Retirement = $438,291+$1,134,682 = $1,572,973

Sub part (ii):

Total number of years till the age of 85 from 67 years of age = 85-67 = 18 Years

Rate of return = 5%

Number of years till the age of retirement from now = 67-34 = 33 Years

Current balance in investment in share portfolio = $47,000

Annual rate of return on investment in share portfolio = 7%

Future value of total share portfolio at the age of retirement = 47000 × ( 1+7 % ) 33 = $438,291

Current balance in investment in superannuation fund = $78,000

Annual rate of return on investment in superannuation fund = 8%

Future value of the beginning balance in superannuation account at the time of retirement

= 78000 × ( 1+8 % ) 33 = $988,732

Annual contribution to the superannuation account = $1,000

Total future value of the annuity payments made to the superannuation fund

= 1000 × ( ( 1+8 % ) 33−1

8 % )=$145,951

The formula applied for Future Value will be FV: Co*(1+r)^n

Total Future value of the investment in Superannuation fund = $988,732+$145,951 = $1,134,682

Value of financial assets at the age of Retirement = $438,291+$1,134,682 = $1,572,973

Sub part (ii):

Total number of years till the age of 85 from 67 years of age = 85-67 = 18 Years

Rate of return = 5%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING AND FINANCE

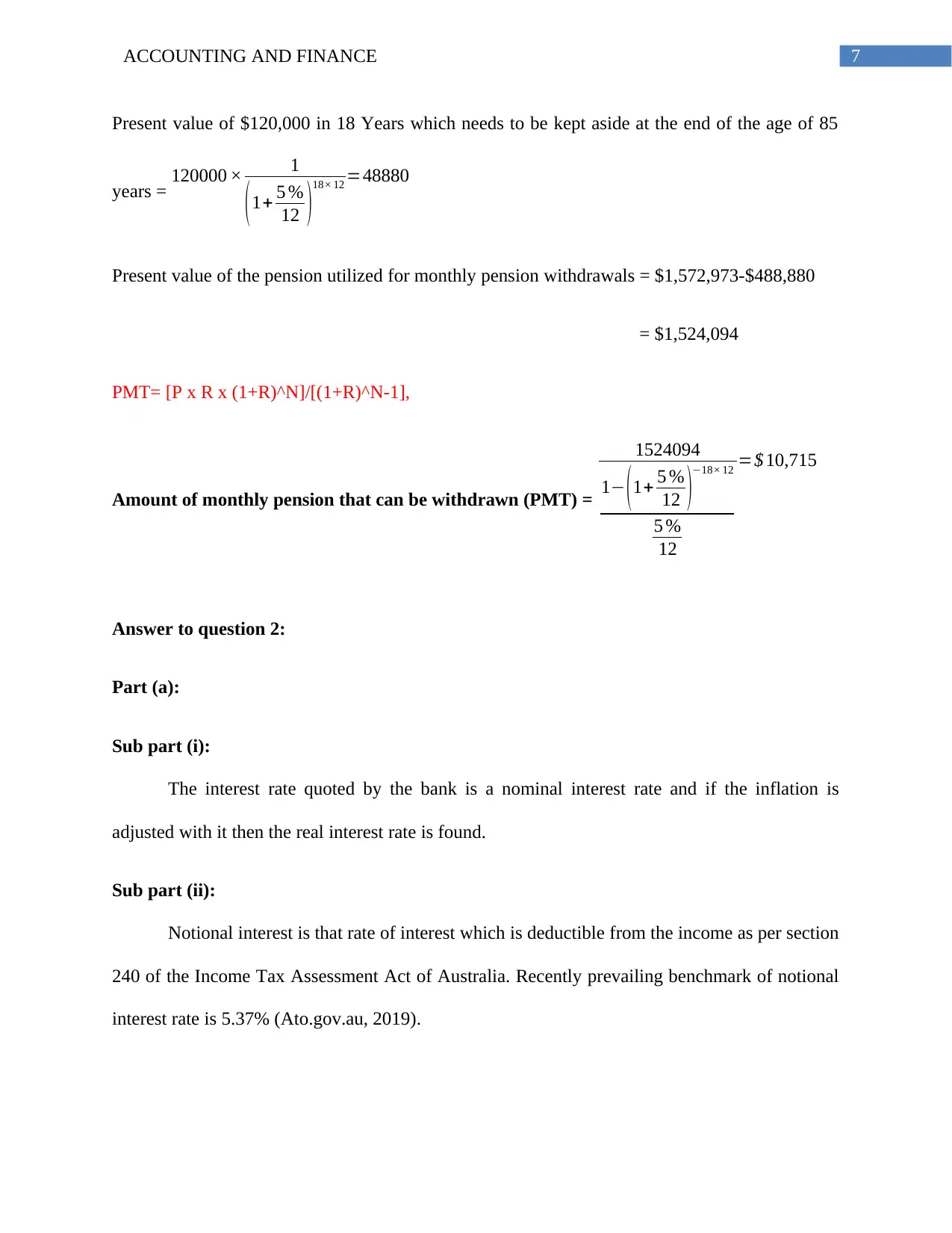

Present value of $120,000 in 18 Years which needs to be kept aside at the end of the age of 85

years = 120000 × 1

( 1+ 5 %

12 )

18× 12 =48880

Present value of the pension utilized for monthly pension withdrawals = $1,572,973-$488,880

= $1,524,094

PMT= [P x R x (1+R)^N]/[(1+R)^N-1],

Amount of monthly pension that can be withdrawn (PMT) =

1524094

1− (1+ 5 %

12 )−18× 12

5 %

12

=$ 10,715

Answer to question 2:

Part (a):

Sub part (i):

The interest rate quoted by the bank is a nominal interest rate and if the inflation is

adjusted with it then the real interest rate is found.

Sub part (ii):

Notional interest is that rate of interest which is deductible from the income as per section

240 of the Income Tax Assessment Act of Australia. Recently prevailing benchmark of notional

interest rate is 5.37% (Ato.gov.au, 2019).

Present value of $120,000 in 18 Years which needs to be kept aside at the end of the age of 85

years = 120000 × 1

( 1+ 5 %

12 )

18× 12 =48880

Present value of the pension utilized for monthly pension withdrawals = $1,572,973-$488,880

= $1,524,094

PMT= [P x R x (1+R)^N]/[(1+R)^N-1],

Amount of monthly pension that can be withdrawn (PMT) =

1524094

1− (1+ 5 %

12 )−18× 12

5 %

12

=$ 10,715

Answer to question 2:

Part (a):

Sub part (i):

The interest rate quoted by the bank is a nominal interest rate and if the inflation is

adjusted with it then the real interest rate is found.

Sub part (ii):

Notional interest is that rate of interest which is deductible from the income as per section

240 of the Income Tax Assessment Act of Australia. Recently prevailing benchmark of notional

interest rate is 5.37% (Ato.gov.au, 2019).

8ACCOUNTING AND FINANCE

Sub part (iii):

IF there is an inflation rate of 1.6%, then the real interest rate would be 1.6%+4% equals

to 5.6%. on the other hand the declared notional rate is 5.37%

Sub part (iv):

If the assumptions are same in computing he notional interest rate and real interest and a

same inflation rate is also considered, then these two could be very close to each other.

Part (b):

Decrease in cash makes and easy availability of cash hence, the spending power of the

consumers increases as a result there might be a demand-pull inflation in the economy (Shah,

2015). In such a situation the consumers get benefitted as they can borrow funds at a very lower

interest rate.

Answer to question 3:

Part (a):

Sub part (i):

Bank guaranteed interest rate on the investment = 1%

Annual Inflation rate to be considered = 2.5%

Real Interest Rate applicable for the investment = 1%+2.5% = 3.5%

Tax rate = 32.5%

Medicare levy on Marginal tax = 2%

Sub part (iii):

IF there is an inflation rate of 1.6%, then the real interest rate would be 1.6%+4% equals

to 5.6%. on the other hand the declared notional rate is 5.37%

Sub part (iv):

If the assumptions are same in computing he notional interest rate and real interest and a

same inflation rate is also considered, then these two could be very close to each other.

Part (b):

Decrease in cash makes and easy availability of cash hence, the spending power of the

consumers increases as a result there might be a demand-pull inflation in the economy (Shah,

2015). In such a situation the consumers get benefitted as they can borrow funds at a very lower

interest rate.

Answer to question 3:

Part (a):

Sub part (i):

Bank guaranteed interest rate on the investment = 1%

Annual Inflation rate to be considered = 2.5%

Real Interest Rate applicable for the investment = 1%+2.5% = 3.5%

Tax rate = 32.5%

Medicare levy on Marginal tax = 2%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING AND FINANCE

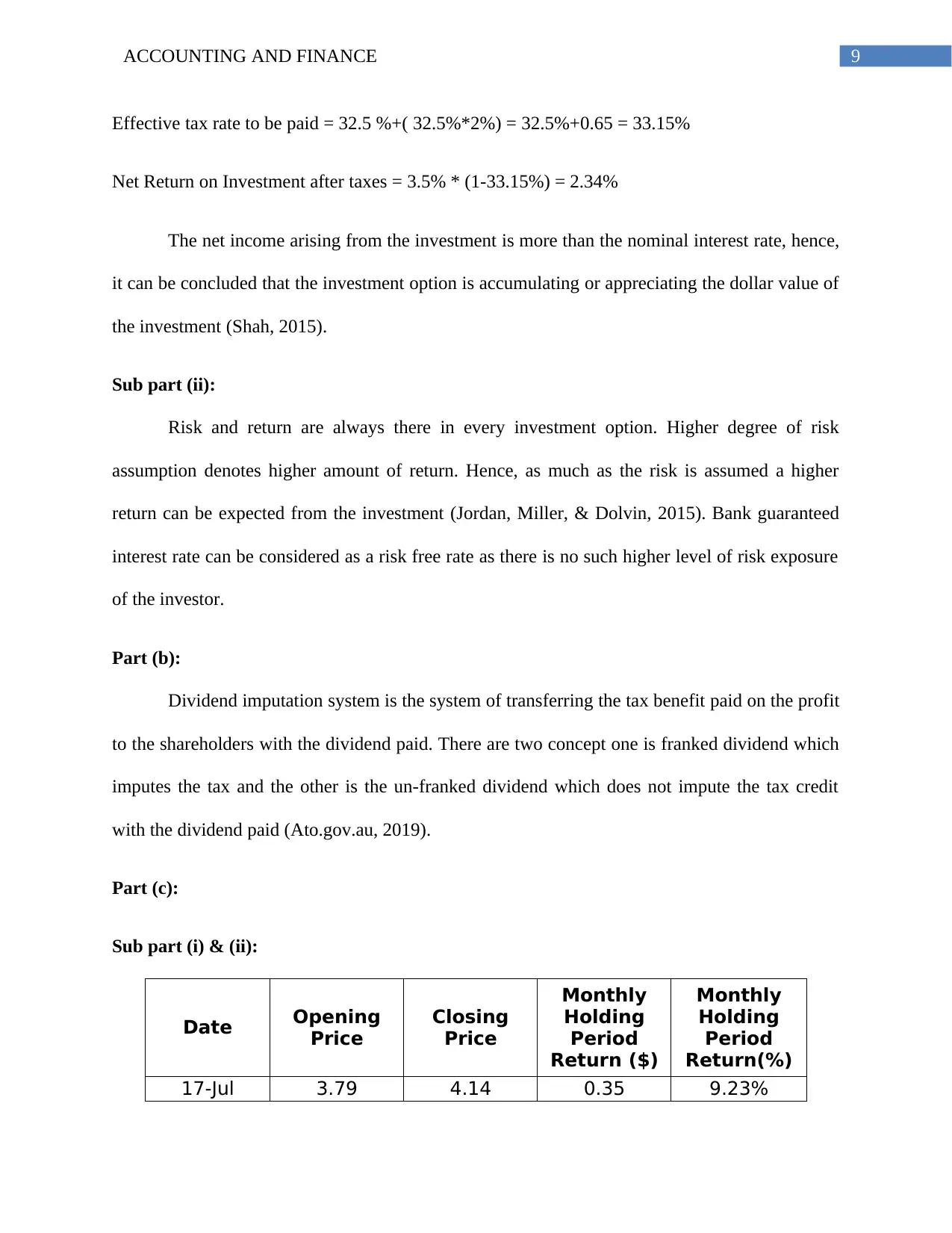

Effective tax rate to be paid = 32.5 %+( 32.5%*2%) = 32.5%+0.65 = 33.15%

Net Return on Investment after taxes = 3.5% * (1-33.15%) = 2.34%

The net income arising from the investment is more than the nominal interest rate, hence,

it can be concluded that the investment option is accumulating or appreciating the dollar value of

the investment (Shah, 2015).

Sub part (ii):

Risk and return are always there in every investment option. Higher degree of risk

assumption denotes higher amount of return. Hence, as much as the risk is assumed a higher

return can be expected from the investment (Jordan, Miller, & Dolvin, 2015). Bank guaranteed

interest rate can be considered as a risk free rate as there is no such higher level of risk exposure

of the investor.

Part (b):

Dividend imputation system is the system of transferring the tax benefit paid on the profit

to the shareholders with the dividend paid. There are two concept one is franked dividend which

imputes the tax and the other is the un-franked dividend which does not impute the tax credit

with the dividend paid (Ato.gov.au, 2019).

Part (c):

Sub part (i) & (ii):

Date Opening

Price

Closing

Price

Monthly

Holding

Period

Return ($)

Monthly

Holding

Period

Return(%)

17-Jul 3.79 4.14 0.35 9.23%

Effective tax rate to be paid = 32.5 %+( 32.5%*2%) = 32.5%+0.65 = 33.15%

Net Return on Investment after taxes = 3.5% * (1-33.15%) = 2.34%

The net income arising from the investment is more than the nominal interest rate, hence,

it can be concluded that the investment option is accumulating or appreciating the dollar value of

the investment (Shah, 2015).

Sub part (ii):

Risk and return are always there in every investment option. Higher degree of risk

assumption denotes higher amount of return. Hence, as much as the risk is assumed a higher

return can be expected from the investment (Jordan, Miller, & Dolvin, 2015). Bank guaranteed

interest rate can be considered as a risk free rate as there is no such higher level of risk exposure

of the investor.

Part (b):

Dividend imputation system is the system of transferring the tax benefit paid on the profit

to the shareholders with the dividend paid. There are two concept one is franked dividend which

imputes the tax and the other is the un-franked dividend which does not impute the tax credit

with the dividend paid (Ato.gov.au, 2019).

Part (c):

Sub part (i) & (ii):

Date Opening

Price

Closing

Price

Monthly

Holding

Period

Return ($)

Monthly

Holding

Period

Return(%)

17-Jul 3.79 4.14 0.35 9.23%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING AND FINANCE

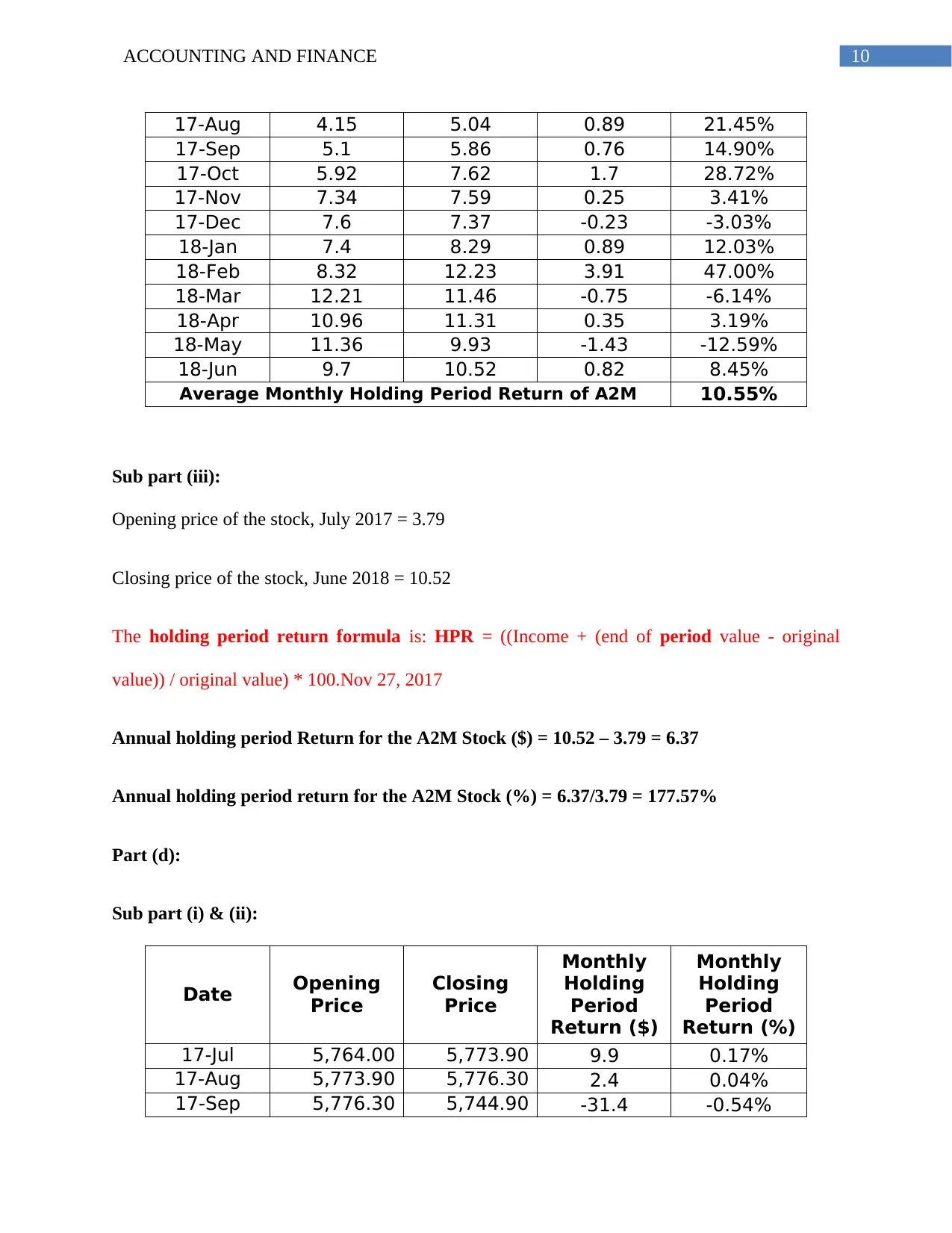

17-Aug 4.15 5.04 0.89 21.45%

17-Sep 5.1 5.86 0.76 14.90%

17-Oct 5.92 7.62 1.7 28.72%

17-Nov 7.34 7.59 0.25 3.41%

17-Dec 7.6 7.37 -0.23 -3.03%

18-Jan 7.4 8.29 0.89 12.03%

18-Feb 8.32 12.23 3.91 47.00%

18-Mar 12.21 11.46 -0.75 -6.14%

18-Apr 10.96 11.31 0.35 3.19%

18-May 11.36 9.93 -1.43 -12.59%

18-Jun 9.7 10.52 0.82 8.45%

Average Monthly Holding Period Return of A2M 10.55%

Sub part (iii):

Opening price of the stock, July 2017 = 3.79

Closing price of the stock, June 2018 = 10.52

The holding period return formula is: HPR = ((Income + (end of period value - original

value)) / original value) * 100.Nov 27, 2017

Annual holding period Return for the A2M Stock ($) = 10.52 – 3.79 = 6.37

Annual holding period return for the A2M Stock (%) = 6.37/3.79 = 177.57%

Part (d):

Sub part (i) & (ii):

Date Opening

Price

Closing

Price

Monthly

Holding

Period

Return ($)

Monthly

Holding

Period

Return (%)

17-Jul 5,764.00 5,773.90 9.9 0.17%

17-Aug 5,773.90 5,776.30 2.4 0.04%

17-Sep 5,776.30 5,744.90 -31.4 -0.54%

17-Aug 4.15 5.04 0.89 21.45%

17-Sep 5.1 5.86 0.76 14.90%

17-Oct 5.92 7.62 1.7 28.72%

17-Nov 7.34 7.59 0.25 3.41%

17-Dec 7.6 7.37 -0.23 -3.03%

18-Jan 7.4 8.29 0.89 12.03%

18-Feb 8.32 12.23 3.91 47.00%

18-Mar 12.21 11.46 -0.75 -6.14%

18-Apr 10.96 11.31 0.35 3.19%

18-May 11.36 9.93 -1.43 -12.59%

18-Jun 9.7 10.52 0.82 8.45%

Average Monthly Holding Period Return of A2M 10.55%

Sub part (iii):

Opening price of the stock, July 2017 = 3.79

Closing price of the stock, June 2018 = 10.52

The holding period return formula is: HPR = ((Income + (end of period value - original

value)) / original value) * 100.Nov 27, 2017

Annual holding period Return for the A2M Stock ($) = 10.52 – 3.79 = 6.37

Annual holding period return for the A2M Stock (%) = 6.37/3.79 = 177.57%

Part (d):

Sub part (i) & (ii):

Date Opening

Price

Closing

Price

Monthly

Holding

Period

Return ($)

Monthly

Holding

Period

Return (%)

17-Jul 5,764.00 5,773.90 9.9 0.17%

17-Aug 5,773.90 5,776.30 2.4 0.04%

17-Sep 5,776.30 5,744.90 -31.4 -0.54%

11ACCOUNTING AND FINANCE

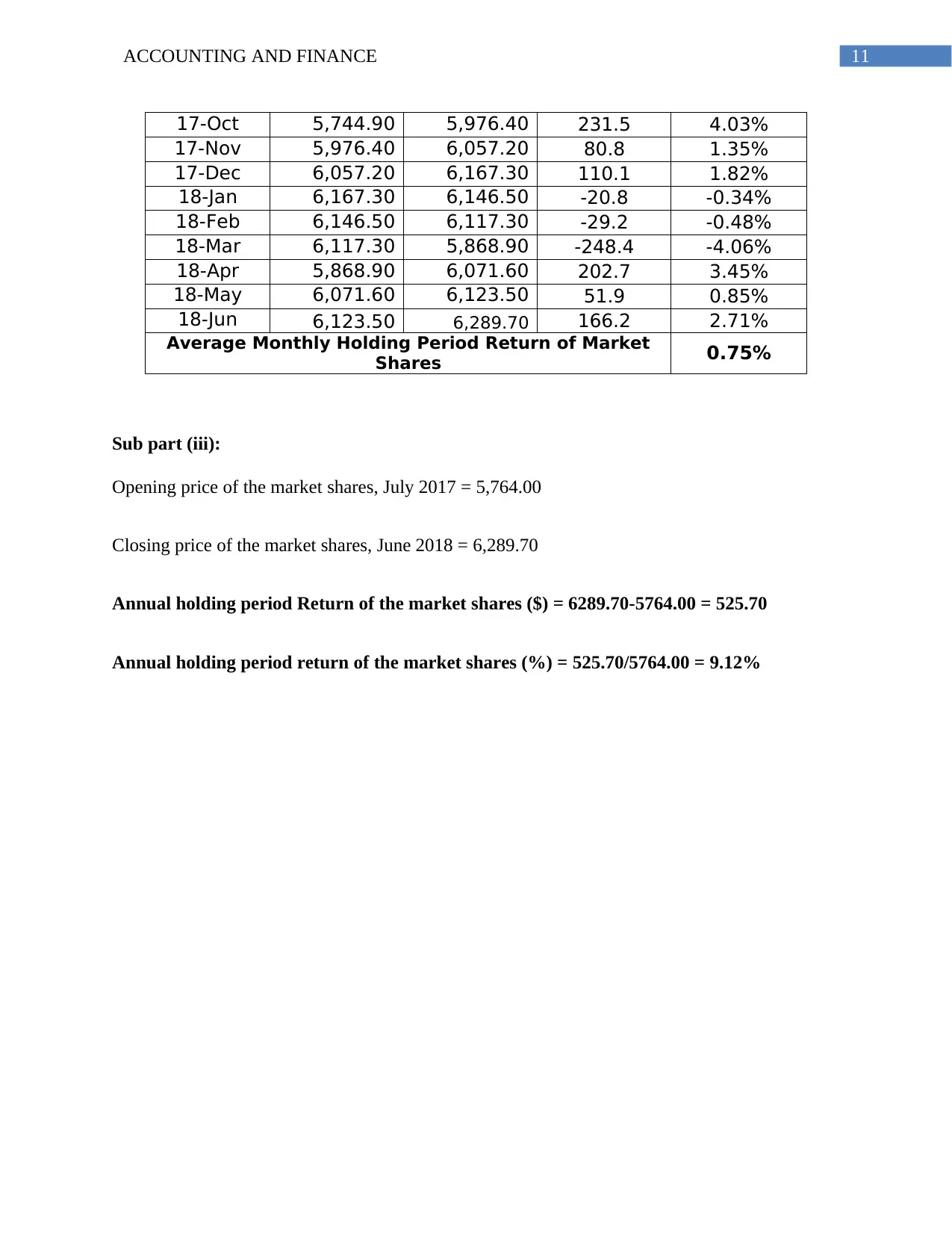

17-Oct 5,744.90 5,976.40 231.5 4.03%

17-Nov 5,976.40 6,057.20 80.8 1.35%

17-Dec 6,057.20 6,167.30 110.1 1.82%

18-Jan 6,167.30 6,146.50 -20.8 -0.34%

18-Feb 6,146.50 6,117.30 -29.2 -0.48%

18-Mar 6,117.30 5,868.90 -248.4 -4.06%

18-Apr 5,868.90 6,071.60 202.7 3.45%

18-May 6,071.60 6,123.50 51.9 0.85%

18-Jun 6,123.50 6,289.70 166.2 2.71%

Average Monthly Holding Period Return of Market

Shares 0.75%

Sub part (iii):

Opening price of the market shares, July 2017 = 5,764.00

Closing price of the market shares, June 2018 = 6,289.70

Annual holding period Return of the market shares ($) = 6289.70-5764.00 = 525.70

Annual holding period return of the market shares (%) = 525.70/5764.00 = 9.12%

17-Oct 5,744.90 5,976.40 231.5 4.03%

17-Nov 5,976.40 6,057.20 80.8 1.35%

17-Dec 6,057.20 6,167.30 110.1 1.82%

18-Jan 6,167.30 6,146.50 -20.8 -0.34%

18-Feb 6,146.50 6,117.30 -29.2 -0.48%

18-Mar 6,117.30 5,868.90 -248.4 -4.06%

18-Apr 5,868.90 6,071.60 202.7 3.45%

18-May 6,071.60 6,123.50 51.9 0.85%

18-Jun 6,123.50 6,289.70 166.2 2.71%

Average Monthly Holding Period Return of Market

Shares 0.75%

Sub part (iii):

Opening price of the market shares, July 2017 = 5,764.00

Closing price of the market shares, June 2018 = 6,289.70

Annual holding period Return of the market shares ($) = 6289.70-5764.00 = 525.70

Annual holding period return of the market shares (%) = 525.70/5764.00 = 9.12%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.