Detailed Accounting and Finance Report: University Name

VerifiedAdded on 2022/09/14

|16

|2415

|12

Report

AI Summary

This comprehensive finance and accounting report delves into various aspects of financial analysis and investment strategies. It begins by examining the future value of an annuity due and net present value calculations, assessing the viability of investment proposals under different interest rate scenarios. The report then explores personal finance, calculating the future value of share portfolios and superannuation accounts, providing insights into retirement planning. It further analyzes nominal, real, and notional interest rates, discussing the impact of cash rates on the economy and inflation. The report also covers tax implications, including the net return on investment after tax and Medicare levy and dividend imputation systems. It presents a detailed analysis of the A2M stock, calculating monthly and annual holding period returns, and compares it with market returns, including risk coefficients and beta calculations. The report concludes with an application of the Capital Asset Pricing Model (CAPM) and portfolio beta calculations, offering a holistic view of financial analysis and investment management.

Running head: ACCOUNTING AND FINANCE

Accounting and Finance

Name of the Student:

Name of the University:

Author’s Note:

Accounting and Finance

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING AND FINANCE

Table of Contents

Answer to question 1:......................................................................................................................3

Part (a):........................................................................................................................................3

Part (b):........................................................................................................................................3

Sub part (i):..............................................................................................................................3

Sub part (ii):.............................................................................................................................4

Part (c):........................................................................................................................................5

Sub part (i):..............................................................................................................................5

Sub part (ii):.............................................................................................................................6

Answer to question 2:......................................................................................................................6

Part (a):........................................................................................................................................6

Sub part (i):..............................................................................................................................6

Sub part (ii):.............................................................................................................................7

Sub part (iii):............................................................................................................................7

Sub part (iv):............................................................................................................................7

Part (b):........................................................................................................................................7

Answer to question 3:......................................................................................................................8

Part (a):........................................................................................................................................8

Sub part (i):..............................................................................................................................8

Table of Contents

Answer to question 1:......................................................................................................................3

Part (a):........................................................................................................................................3

Part (b):........................................................................................................................................3

Sub part (i):..............................................................................................................................3

Sub part (ii):.............................................................................................................................4

Part (c):........................................................................................................................................5

Sub part (i):..............................................................................................................................5

Sub part (ii):.............................................................................................................................6

Answer to question 2:......................................................................................................................6

Part (a):........................................................................................................................................6

Sub part (i):..............................................................................................................................6

Sub part (ii):.............................................................................................................................7

Sub part (iii):............................................................................................................................7

Sub part (iv):............................................................................................................................7

Part (b):........................................................................................................................................7

Answer to question 3:......................................................................................................................8

Part (a):........................................................................................................................................8

Sub part (i):..............................................................................................................................8

2ACCOUNTING AND FINANCE

Sub part (ii):.............................................................................................................................9

Part (b):........................................................................................................................................9

Part (c):........................................................................................................................................9

Sub part (i) & (ii):....................................................................................................................9

Sub part (iii):..........................................................................................................................10

Part (d):......................................................................................................................................10

Sub part (i) & (ii):..................................................................................................................10

Sub part (iii):..........................................................................................................................11

Sub part (iv):..........................................................................................................................11

Sub part (v):...........................................................................................................................11

Sub part (vi):..........................................................................................................................12

Sub part (vii):.........................................................................................................................12

Sub part (viii):........................................................................................................................12

Sub part (ix):..........................................................................................................................13

Sub part (x):...........................................................................................................................13

References and bibliography:........................................................................................................14

Sub part (ii):.............................................................................................................................9

Part (b):........................................................................................................................................9

Part (c):........................................................................................................................................9

Sub part (i) & (ii):....................................................................................................................9

Sub part (iii):..........................................................................................................................10

Part (d):......................................................................................................................................10

Sub part (i) & (ii):..................................................................................................................10

Sub part (iii):..........................................................................................................................11

Sub part (iv):..........................................................................................................................11

Sub part (v):...........................................................................................................................11

Sub part (vi):..........................................................................................................................12

Sub part (vii):.........................................................................................................................12

Sub part (viii):........................................................................................................................12

Sub part (ix):..........................................................................................................................13

Sub part (x):...........................................................................................................................13

References and bibliography:........................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING AND FINANCE

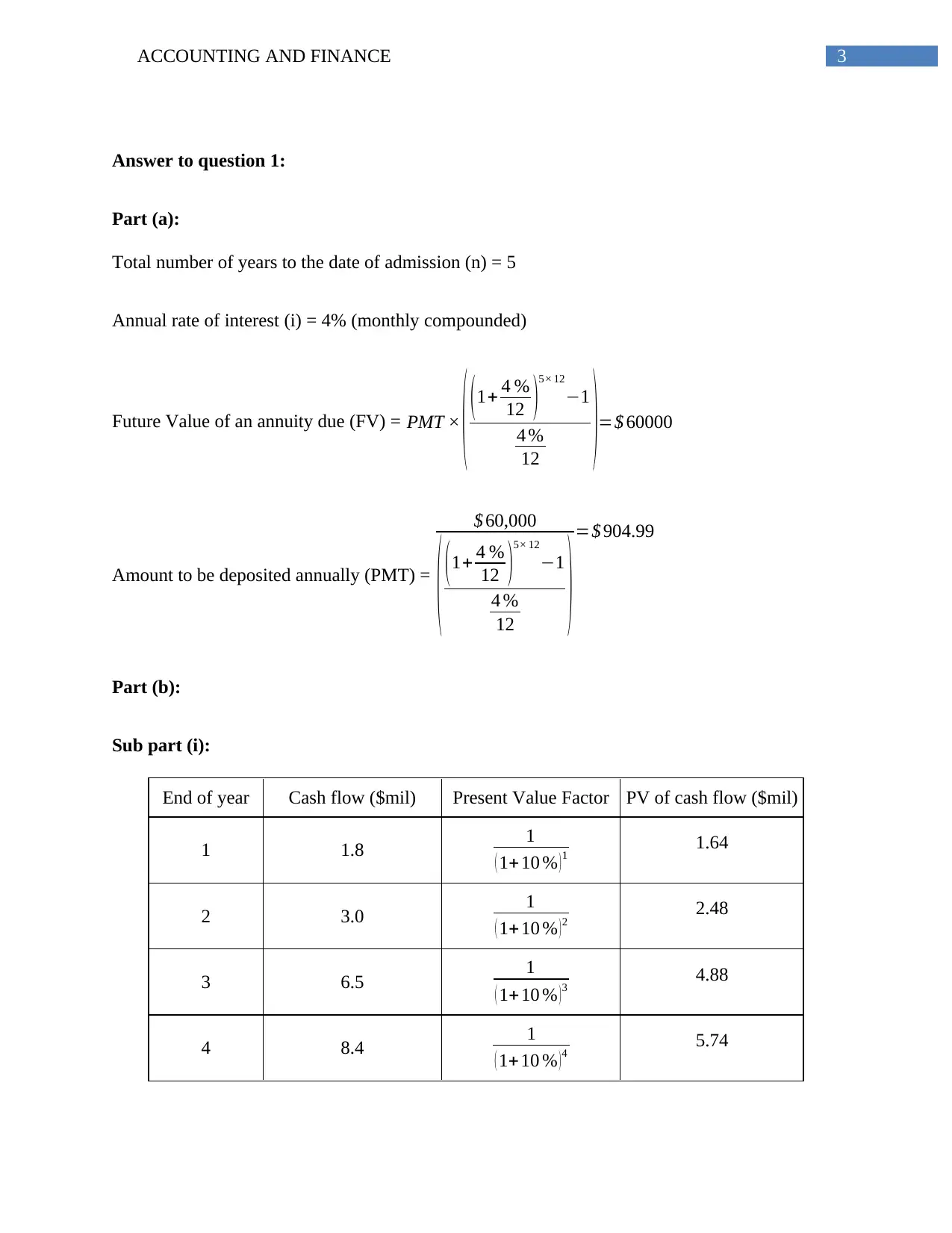

Answer to question 1:

Part (a):

Total number of years to the date of admission (n) = 5

Annual rate of interest (i) = 4% (monthly compounded)

Future Value of an annuity due (FV) = PMT ×

( (1+ 4 %

12 )5× 12

−1

4 %

12 )=$ 60000

Amount to be deposited annually (PMT) =

$ 60,000

( (1+ 4 %

12 )5× 12

−1

4 %

12 )=$ 904.99

Part (b):

Sub part (i):

End of year Cash flow ($mil) Present Value Factor PV of cash flow ($mil)

1 1.8 1

( 1+ 10 % ) 1 1.64

2 3.0 1

( 1+ 10 % ) 2 2.48

3 6.5 1

( 1+ 10 % ) 3 4.88

4 8.4 1

( 1+ 10 % ) 4 5.74

Answer to question 1:

Part (a):

Total number of years to the date of admission (n) = 5

Annual rate of interest (i) = 4% (monthly compounded)

Future Value of an annuity due (FV) = PMT ×

( (1+ 4 %

12 )5× 12

−1

4 %

12 )=$ 60000

Amount to be deposited annually (PMT) =

$ 60,000

( (1+ 4 %

12 )5× 12

−1

4 %

12 )=$ 904.99

Part (b):

Sub part (i):

End of year Cash flow ($mil) Present Value Factor PV of cash flow ($mil)

1 1.8 1

( 1+ 10 % ) 1 1.64

2 3.0 1

( 1+ 10 % ) 2 2.48

3 6.5 1

( 1+ 10 % ) 3 4.88

4 8.4 1

( 1+ 10 % ) 4 5.74

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING AND FINANCE

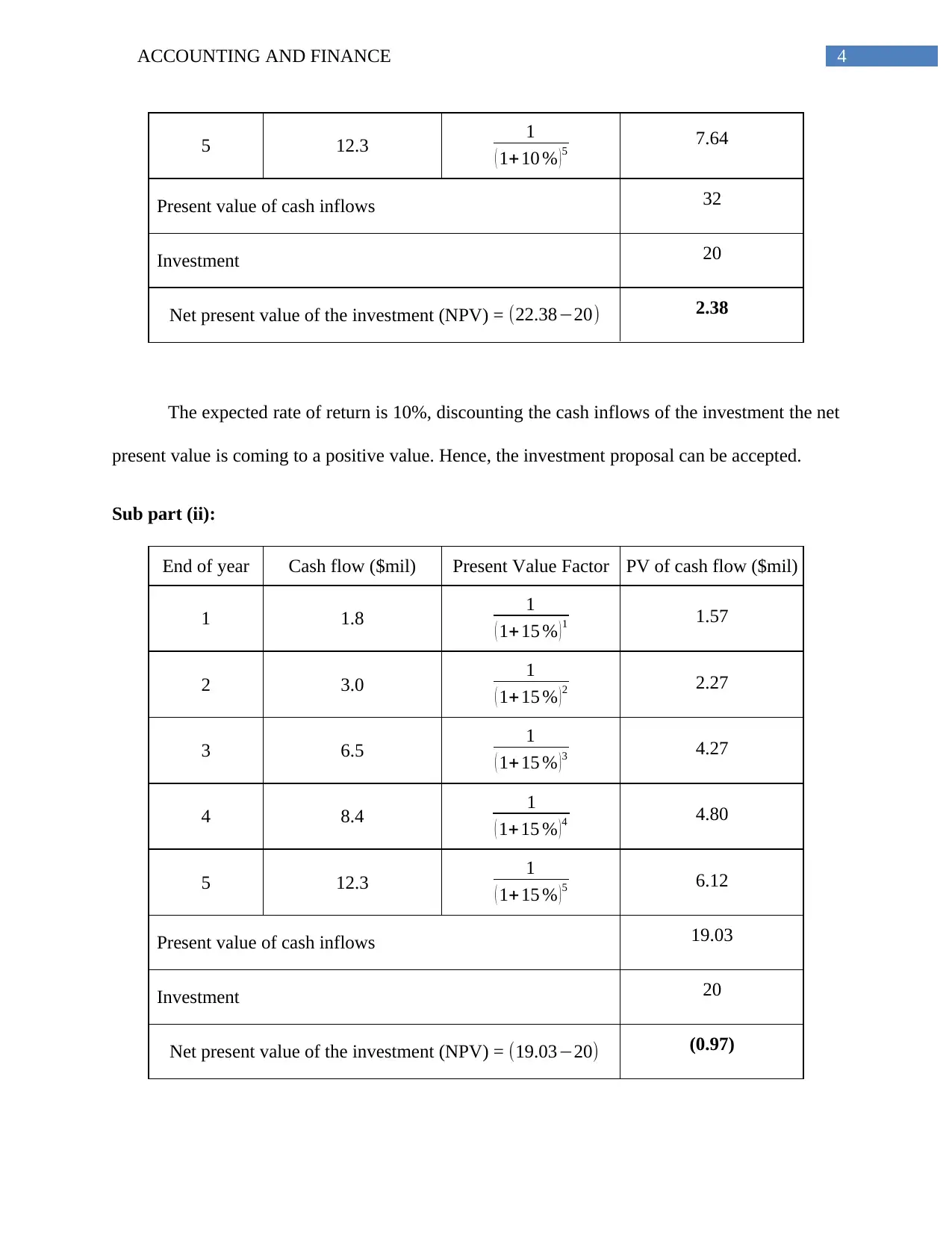

5 12.3 1

( 1+ 10 % ) 5 7.64

Present value of cash inflows 32

Investment 20

Net present value of the investment (NPV) = (22.38−20) 2.38

The expected rate of return is 10%, discounting the cash inflows of the investment the net

present value is coming to a positive value. Hence, the investment proposal can be accepted.

Sub part (ii):

End of year Cash flow ($mil) Present Value Factor PV of cash flow ($mil)

1 1.8 1

( 1+ 15 % ) 1 1.57

2 3.0 1

( 1+ 15 % ) 2 2.27

3 6.5 1

( 1+ 15 % ) 3 4.27

4 8.4 1

( 1+ 15 % ) 4 4.80

5 12.3 1

( 1+ 15 % ) 5 6.12

Present value of cash inflows 19.03

Investment 20

Net present value of the investment (NPV) = (19.03−20) (0.97)

5 12.3 1

( 1+ 10 % ) 5 7.64

Present value of cash inflows 32

Investment 20

Net present value of the investment (NPV) = (22.38−20) 2.38

The expected rate of return is 10%, discounting the cash inflows of the investment the net

present value is coming to a positive value. Hence, the investment proposal can be accepted.

Sub part (ii):

End of year Cash flow ($mil) Present Value Factor PV of cash flow ($mil)

1 1.8 1

( 1+ 15 % ) 1 1.57

2 3.0 1

( 1+ 15 % ) 2 2.27

3 6.5 1

( 1+ 15 % ) 3 4.27

4 8.4 1

( 1+ 15 % ) 4 4.80

5 12.3 1

( 1+ 15 % ) 5 6.12

Present value of cash inflows 19.03

Investment 20

Net present value of the investment (NPV) = (19.03−20) (0.97)

5ACCOUNTING AND FINANCE

The expected rate of return is 15%. Therefore, expected cash inflows need to be

discounted by 15%. Applying the net present value technique considering a 15% discount rate,

the net present value of the investment is negative. Hence, the investment proposal should not be

accepted with an expected rate of return of 15%.

Part (c):

Sub part (i):

Current age of the individual = 34 Years

Age of retirement of the individual = 67 Years

Total number of years till the age of maturity from now = 67-34 = 33 Years

Current balance in share portfolio = $47,000

Annual rate of return on share portfolio = 7%

Future value share portfolio at the age of maturity = 47000 × ( 1+7 % ) 33 = $438,291

Current balance of superannuation account = $78,000

Annual rate of return on superannuation fund = 8%

Future value of the balance in superannuation account at the time of maturity

= 78000 × ( 1+8 % ) 33 = $988,732

Annual contribution to be made to the superannuation account = $1,000

Total future value of the annuity payment to the superannuation account

The expected rate of return is 15%. Therefore, expected cash inflows need to be

discounted by 15%. Applying the net present value technique considering a 15% discount rate,

the net present value of the investment is negative. Hence, the investment proposal should not be

accepted with an expected rate of return of 15%.

Part (c):

Sub part (i):

Current age of the individual = 34 Years

Age of retirement of the individual = 67 Years

Total number of years till the age of maturity from now = 67-34 = 33 Years

Current balance in share portfolio = $47,000

Annual rate of return on share portfolio = 7%

Future value share portfolio at the age of maturity = 47000 × ( 1+7 % ) 33 = $438,291

Current balance of superannuation account = $78,000

Annual rate of return on superannuation fund = 8%

Future value of the balance in superannuation account at the time of maturity

= 78000 × ( 1+8 % ) 33 = $988,732

Annual contribution to be made to the superannuation account = $1,000

Total future value of the annuity payment to the superannuation account

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING AND FINANCE

= 1000 × ( ( 1+8 % ) 33−1

8 % )=$145,951

Future value of the Superannuation fund = $988,732+$145,951 = $1,134,682

Value of financial assets at the age of Retirement = $438,291+$1,134,682 = $1,572,973

Sub part (ii):

Total number of years till the age of 85 from 67 years of age = 85-67 = 18 Years

Rate of return = 5%

Present value of $120,000 in 18 Years which needs to be kept aside at the end of the age of 85

years = 120000 × 1

( 1+ 5 %

12 )

18× 12 =48880

Present value of the pension utilized for monthly pension withdrawals = $1,572,973-$488,880

= $1,524,094

Amount of monthly pension that can be withdrawn (PMT) =

1524094

1− (1+ 5 %

12 )−18× 12

5 %

12

=$ 10,715

= 1000 × ( ( 1+8 % ) 33−1

8 % )=$145,951

Future value of the Superannuation fund = $988,732+$145,951 = $1,134,682

Value of financial assets at the age of Retirement = $438,291+$1,134,682 = $1,572,973

Sub part (ii):

Total number of years till the age of 85 from 67 years of age = 85-67 = 18 Years

Rate of return = 5%

Present value of $120,000 in 18 Years which needs to be kept aside at the end of the age of 85

years = 120000 × 1

( 1+ 5 %

12 )

18× 12 =48880

Present value of the pension utilized for monthly pension withdrawals = $1,572,973-$488,880

= $1,524,094

Amount of monthly pension that can be withdrawn (PMT) =

1524094

1− (1+ 5 %

12 )−18× 12

5 %

12

=$ 10,715

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING AND FINANCE

Answer to question 2:

Part (a):

Sub part (i):

In the given case study, the bank has quoted an interest for lending funds. The interest

rate quoted by the bank is a nominal interest rate. The real interest rate is the inflation-adjusted

rate of interest. For example, if the interest rate quoted by the bank is 4% and there is an inflation

rate of 2.5%, then the real interest rate is 4% and the inflation rate of 2.5% equals 6.5%.

Therefore, the interest rate quoted by the bank is a nominal interest rate and if the inflation rate is

added with the nominal interest rate, then the real interest rate can be found.

Sub part (ii):

Nominal rate of interest is the basic interest that is charged on the borrowed amount. It is

charged on the borrowed amount to compute the interest to be charged on the borrowed amount.

Real interest rate is the inflation adjusted nominal interest rate. Notional interest rate is that rate

of interest, which the Australian Taxation Act allows the taxpayers to claim as a deductible

expense for interest on borrowed capital. As per section 240 of the Income Tax Assessment Act

of Australia, an interest, which is computed, based on the arm’s length principle and considering

the inflation rate prevailing in the market by the taxation authority and notified as tax deductible.

Recently declared benchmark notional interest rate is 5.37% (Ato.gov.au, 2019).

Sub part (iii):

In Australia the prevailing inflation rate is 1.6%, if that rate is considered for computation

of the interest rate, then the real interest rate can be computed as 4%+1.6% equals 5.6%.

Answer to question 2:

Part (a):

Sub part (i):

In the given case study, the bank has quoted an interest for lending funds. The interest

rate quoted by the bank is a nominal interest rate. The real interest rate is the inflation-adjusted

rate of interest. For example, if the interest rate quoted by the bank is 4% and there is an inflation

rate of 2.5%, then the real interest rate is 4% and the inflation rate of 2.5% equals 6.5%.

Therefore, the interest rate quoted by the bank is a nominal interest rate and if the inflation rate is

added with the nominal interest rate, then the real interest rate can be found.

Sub part (ii):

Nominal rate of interest is the basic interest that is charged on the borrowed amount. It is

charged on the borrowed amount to compute the interest to be charged on the borrowed amount.

Real interest rate is the inflation adjusted nominal interest rate. Notional interest rate is that rate

of interest, which the Australian Taxation Act allows the taxpayers to claim as a deductible

expense for interest on borrowed capital. As per section 240 of the Income Tax Assessment Act

of Australia, an interest, which is computed, based on the arm’s length principle and considering

the inflation rate prevailing in the market by the taxation authority and notified as tax deductible.

Recently declared benchmark notional interest rate is 5.37% (Ato.gov.au, 2019).

Sub part (iii):

In Australia the prevailing inflation rate is 1.6%, if that rate is considered for computation

of the interest rate, then the real interest rate can be computed as 4%+1.6% equals 5.6%.

8ACCOUNTING AND FINANCE

Notional interest rate is computed by the taxation authority and declared by them. They also

consider the inflation rate as well as various other market factors.

Sub part (iv):

If the assumptions and period of computation of the real interest rate and notional interest

rate is same then the computed value of real interest rate and notional interest rate might become

equal (Ato.gov.au, 2019).

Part (b):

Cash rate is the rate charged by the reserve bank on the debt of the commercial banks. If

the cash rate is decreased by the Reserve bank then cost of fund to the commercial banks will be

lower and they will be having excess amount to lend. Therefore, they will be offering loans at a

lower rate of interest. If such situation arises then the fund flow in the economy will be higher,

hence there will be excess funds available to the individuals, which in turn will cause a higher

demand for the products and services. If demand increases, sellers will charge a higher price, as a

result a demand-pull inflation may arise in the market. By decreasing the cash rate, the interest

rate for borrowings will be lower, hence the individuals will be benefited from such activities

(Shah, 2015).

Answer to question 3:

Part (a):

Sub part (i):

Interest rate on bank guaranteed investment = 1%

Annual Inflation rate = 2.5%

Notional interest rate is computed by the taxation authority and declared by them. They also

consider the inflation rate as well as various other market factors.

Sub part (iv):

If the assumptions and period of computation of the real interest rate and notional interest

rate is same then the computed value of real interest rate and notional interest rate might become

equal (Ato.gov.au, 2019).

Part (b):

Cash rate is the rate charged by the reserve bank on the debt of the commercial banks. If

the cash rate is decreased by the Reserve bank then cost of fund to the commercial banks will be

lower and they will be having excess amount to lend. Therefore, they will be offering loans at a

lower rate of interest. If such situation arises then the fund flow in the economy will be higher,

hence there will be excess funds available to the individuals, which in turn will cause a higher

demand for the products and services. If demand increases, sellers will charge a higher price, as a

result a demand-pull inflation may arise in the market. By decreasing the cash rate, the interest

rate for borrowings will be lower, hence the individuals will be benefited from such activities

(Shah, 2015).

Answer to question 3:

Part (a):

Sub part (i):

Interest rate on bank guaranteed investment = 1%

Annual Inflation rate = 2.5%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING AND FINANCE

Real Interest Rate = 1%+2.5% = 3.5%

Tax rate = 32.5%

Medicare levy on Marginal tax = 2%

Effective tax rate including Medicare Levy = 32.5 %+( 32.5%*2%) = 32.5%+0.65 = 33.15%

Net Return on Investment after tax and Medicare levy = 3.5% * (1-33.15%) = 2.34%

It can be observed from the above calculation, that the net income after tax and Medicare

levy is more than the nominal interest rate, hence, it will be appreciating the real dollar value of

the investment (Shah, 2015).

Sub part (ii):

Every investment has two aspects, one is the return expectation and the other is the risk

assumption. If higher degree of risk is assumed then a higher return from the investment can be

expected. There are two types of risks, one is systematic risk and the other is unsystematic risks.

Systematic risks cannot be diversified through the construction of portfolio; on the other hand,

the unsystematic risk can be diversified through diversification of the portfolio. Beta is the

coefficient of risk, if beta is more than one then; the stock price is more volatile than the market.

It implies the movement on stock price is more than the movement in the market index. The bank

guaranteed interest rate is only 1% as it is assuming lower degree of risk. Hence, it can be

considered as a risk free investment (Jordan, Miller, & Dolvin, 2015).

Part (b):

Companies pay tax on their profit and at the time of payment of dividend to the owners of

the company, if such tax amount is transferred to the owners with the dividend, then such system

Real Interest Rate = 1%+2.5% = 3.5%

Tax rate = 32.5%

Medicare levy on Marginal tax = 2%

Effective tax rate including Medicare Levy = 32.5 %+( 32.5%*2%) = 32.5%+0.65 = 33.15%

Net Return on Investment after tax and Medicare levy = 3.5% * (1-33.15%) = 2.34%

It can be observed from the above calculation, that the net income after tax and Medicare

levy is more than the nominal interest rate, hence, it will be appreciating the real dollar value of

the investment (Shah, 2015).

Sub part (ii):

Every investment has two aspects, one is the return expectation and the other is the risk

assumption. If higher degree of risk is assumed then a higher return from the investment can be

expected. There are two types of risks, one is systematic risk and the other is unsystematic risks.

Systematic risks cannot be diversified through the construction of portfolio; on the other hand,

the unsystematic risk can be diversified through diversification of the portfolio. Beta is the

coefficient of risk, if beta is more than one then; the stock price is more volatile than the market.

It implies the movement on stock price is more than the movement in the market index. The bank

guaranteed interest rate is only 1% as it is assuming lower degree of risk. Hence, it can be

considered as a risk free investment (Jordan, Miller, & Dolvin, 2015).

Part (b):

Companies pay tax on their profit and at the time of payment of dividend to the owners of

the company, if such tax amount is transferred to the owners with the dividend, then such system

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING AND FINANCE

of allocation of tax credit is known as dividend imputation system. In this system the tax paid on

profit is transferred to the shareholders as a tax credit, which will be reducing their net tax

liability (Ato.gov.au, 2019)..

Part (c):

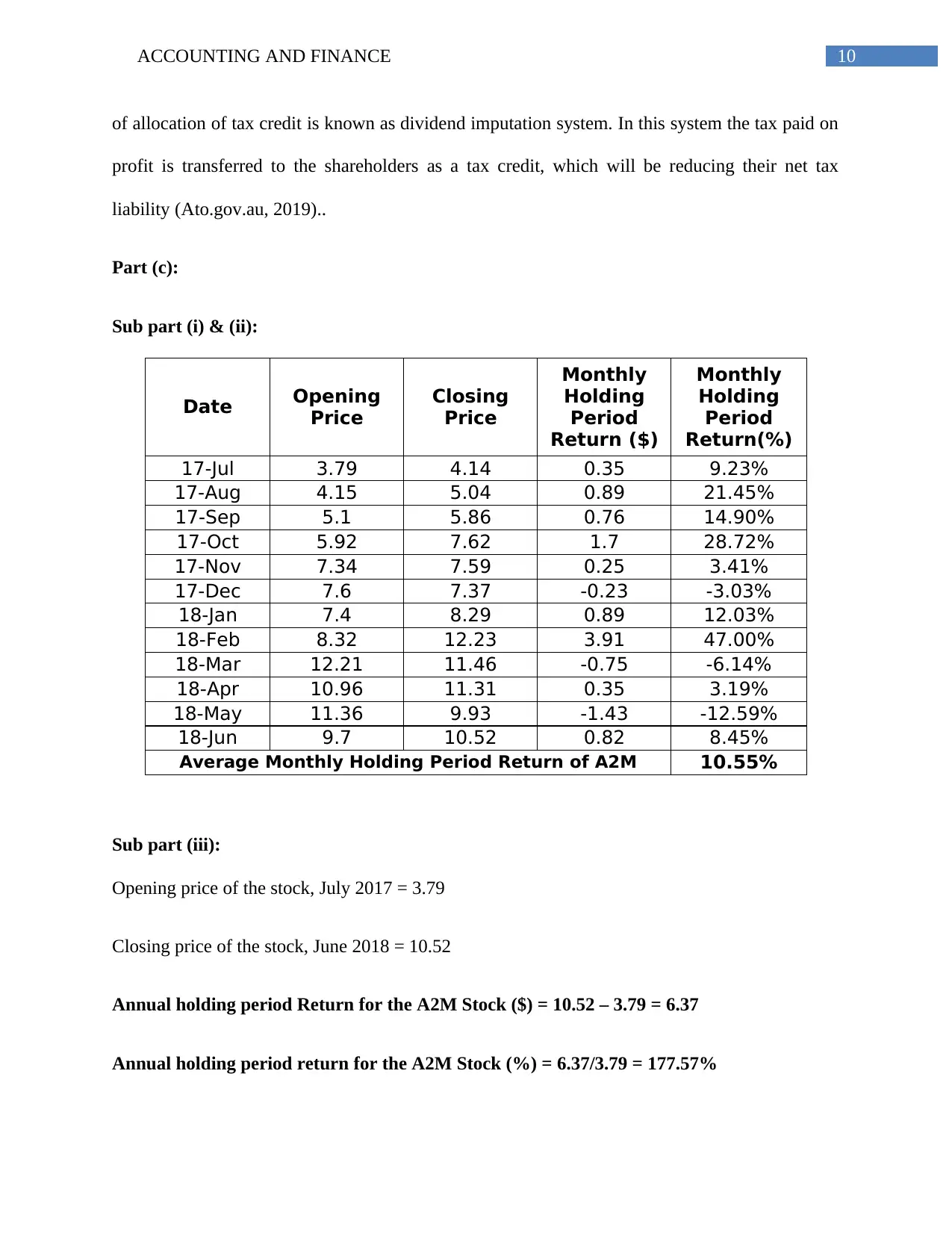

Sub part (i) & (ii):

Date Opening

Price

Closing

Price

Monthly

Holding

Period

Return ($)

Monthly

Holding

Period

Return(%)

17-Jul 3.79 4.14 0.35 9.23%

17-Aug 4.15 5.04 0.89 21.45%

17-Sep 5.1 5.86 0.76 14.90%

17-Oct 5.92 7.62 1.7 28.72%

17-Nov 7.34 7.59 0.25 3.41%

17-Dec 7.6 7.37 -0.23 -3.03%

18-Jan 7.4 8.29 0.89 12.03%

18-Feb 8.32 12.23 3.91 47.00%

18-Mar 12.21 11.46 -0.75 -6.14%

18-Apr 10.96 11.31 0.35 3.19%

18-May 11.36 9.93 -1.43 -12.59%

18-Jun 9.7 10.52 0.82 8.45%

Average Monthly Holding Period Return of A2M 10.55%

Sub part (iii):

Opening price of the stock, July 2017 = 3.79

Closing price of the stock, June 2018 = 10.52

Annual holding period Return for the A2M Stock ($) = 10.52 – 3.79 = 6.37

Annual holding period return for the A2M Stock (%) = 6.37/3.79 = 177.57%

of allocation of tax credit is known as dividend imputation system. In this system the tax paid on

profit is transferred to the shareholders as a tax credit, which will be reducing their net tax

liability (Ato.gov.au, 2019)..

Part (c):

Sub part (i) & (ii):

Date Opening

Price

Closing

Price

Monthly

Holding

Period

Return ($)

Monthly

Holding

Period

Return(%)

17-Jul 3.79 4.14 0.35 9.23%

17-Aug 4.15 5.04 0.89 21.45%

17-Sep 5.1 5.86 0.76 14.90%

17-Oct 5.92 7.62 1.7 28.72%

17-Nov 7.34 7.59 0.25 3.41%

17-Dec 7.6 7.37 -0.23 -3.03%

18-Jan 7.4 8.29 0.89 12.03%

18-Feb 8.32 12.23 3.91 47.00%

18-Mar 12.21 11.46 -0.75 -6.14%

18-Apr 10.96 11.31 0.35 3.19%

18-May 11.36 9.93 -1.43 -12.59%

18-Jun 9.7 10.52 0.82 8.45%

Average Monthly Holding Period Return of A2M 10.55%

Sub part (iii):

Opening price of the stock, July 2017 = 3.79

Closing price of the stock, June 2018 = 10.52

Annual holding period Return for the A2M Stock ($) = 10.52 – 3.79 = 6.37

Annual holding period return for the A2M Stock (%) = 6.37/3.79 = 177.57%

11ACCOUNTING AND FINANCE

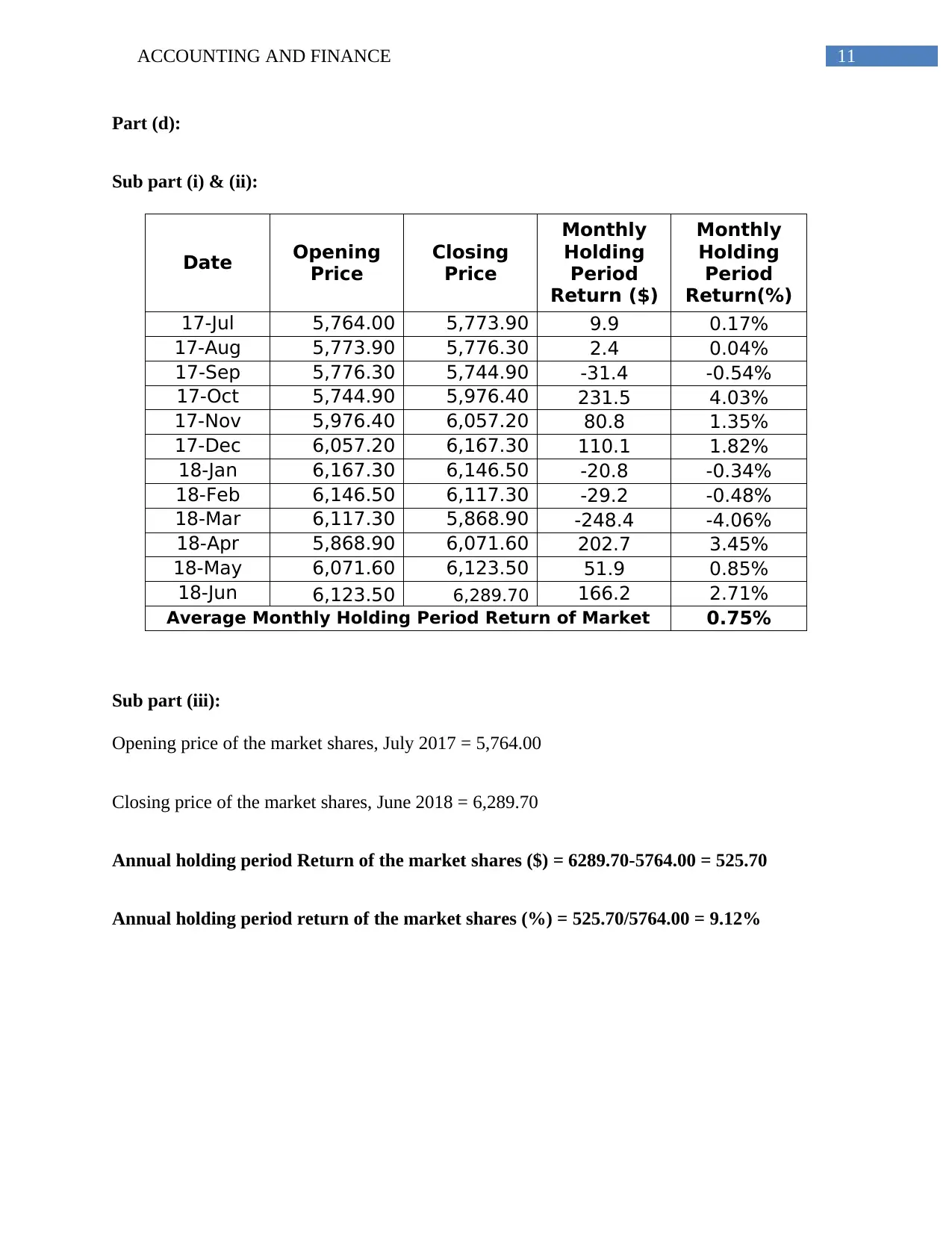

Part (d):

Sub part (i) & (ii):

Date Opening

Price

Closing

Price

Monthly

Holding

Period

Return ($)

Monthly

Holding

Period

Return(%)

17-Jul 5,764.00 5,773.90 9.9 0.17%

17-Aug 5,773.90 5,776.30 2.4 0.04%

17-Sep 5,776.30 5,744.90 -31.4 -0.54%

17-Oct 5,744.90 5,976.40 231.5 4.03%

17-Nov 5,976.40 6,057.20 80.8 1.35%

17-Dec 6,057.20 6,167.30 110.1 1.82%

18-Jan 6,167.30 6,146.50 -20.8 -0.34%

18-Feb 6,146.50 6,117.30 -29.2 -0.48%

18-Mar 6,117.30 5,868.90 -248.4 -4.06%

18-Apr 5,868.90 6,071.60 202.7 3.45%

18-May 6,071.60 6,123.50 51.9 0.85%

18-Jun 6,123.50 6,289.70 166.2 2.71%

Average Monthly Holding Period Return of Market 0.75%

Sub part (iii):

Opening price of the market shares, July 2017 = 5,764.00

Closing price of the market shares, June 2018 = 6,289.70

Annual holding period Return of the market shares ($) = 6289.70-5764.00 = 525.70

Annual holding period return of the market shares (%) = 525.70/5764.00 = 9.12%

Part (d):

Sub part (i) & (ii):

Date Opening

Price

Closing

Price

Monthly

Holding

Period

Return ($)

Monthly

Holding

Period

Return(%)

17-Jul 5,764.00 5,773.90 9.9 0.17%

17-Aug 5,773.90 5,776.30 2.4 0.04%

17-Sep 5,776.30 5,744.90 -31.4 -0.54%

17-Oct 5,744.90 5,976.40 231.5 4.03%

17-Nov 5,976.40 6,057.20 80.8 1.35%

17-Dec 6,057.20 6,167.30 110.1 1.82%

18-Jan 6,167.30 6,146.50 -20.8 -0.34%

18-Feb 6,146.50 6,117.30 -29.2 -0.48%

18-Mar 6,117.30 5,868.90 -248.4 -4.06%

18-Apr 5,868.90 6,071.60 202.7 3.45%

18-May 6,071.60 6,123.50 51.9 0.85%

18-Jun 6,123.50 6,289.70 166.2 2.71%

Average Monthly Holding Period Return of Market 0.75%

Sub part (iii):

Opening price of the market shares, July 2017 = 5,764.00

Closing price of the market shares, June 2018 = 6,289.70

Annual holding period Return of the market shares ($) = 6289.70-5764.00 = 525.70

Annual holding period return of the market shares (%) = 525.70/5764.00 = 9.12%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.