Accounting and Finance Report: Cornpeace Ltd and Dane Jones Ltd

VerifiedAdded on 2020/10/05

|15

|4109

|202

Report

AI Summary

This report provides a comprehensive analysis of accounting and finance principles through the examination of three case studies: Gravepals Plc, Cornpeace Ltd, and Dane Jones Ltd. The analysis begins with the preparation of financial statements, including the income statement and balance sheet for Gravepals Plc. It then proceeds to calculate key metrics for Cornpeace Ltd, such as contribution per unit, break-even point, and profit, along with an analysis of strategic decisions. The report also discusses the assumptions of the break-even model and its applicability across different businesses. Finally, for Dane Jones Ltd, the report calculates the payback period, accounting rate of return, and net present value, alongside a discussion of the merits and limitations of various investment appraisal techniques and the advantages and disadvantages of using budgets as a tool for strategic planning. The report concludes with a summary of the key findings and insights gained from the analysis of each case study, providing a well-rounded understanding of financial analysis and management.

ACCOUNTING AND

FINANCE

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART A – Gravepals Plc.................................................................................................................1

PART B – Cornpeace Ltd................................................................................................................2

a. Calculation of contribution per unit........................................................................................2

b. Calculation of break-even point and margin of safety ...........................................................3

c. Calculation of profit at 48000 tables at £13 per shelf.............................................................4

d. Analysis of strategy.................................................................................................................4

e. Assumptions of Break-even model and its utilization by different businesses.......................5

PART C – Dane Jones Ltd ..............................................................................................................6

a. Calculation of Payback period, accounting rate of return and net present value....................6

b. Merits and limitations of various investment appraisal techniques........................................8

c. Advantages and disadvantages of using budgets as tool for strategic planning....................10

CONCLUSION .............................................................................................................................11

REFERENCES .............................................................................................................................11

INTRODUCTION...........................................................................................................................1

PART A – Gravepals Plc.................................................................................................................1

PART B – Cornpeace Ltd................................................................................................................2

a. Calculation of contribution per unit........................................................................................2

b. Calculation of break-even point and margin of safety ...........................................................3

c. Calculation of profit at 48000 tables at £13 per shelf.............................................................4

d. Analysis of strategy.................................................................................................................4

e. Assumptions of Break-even model and its utilization by different businesses.......................5

PART C – Dane Jones Ltd ..............................................................................................................6

a. Calculation of Payback period, accounting rate of return and net present value....................6

b. Merits and limitations of various investment appraisal techniques........................................8

c. Advantages and disadvantages of using budgets as tool for strategic planning....................10

CONCLUSION .............................................................................................................................11

REFERENCES .............................................................................................................................11

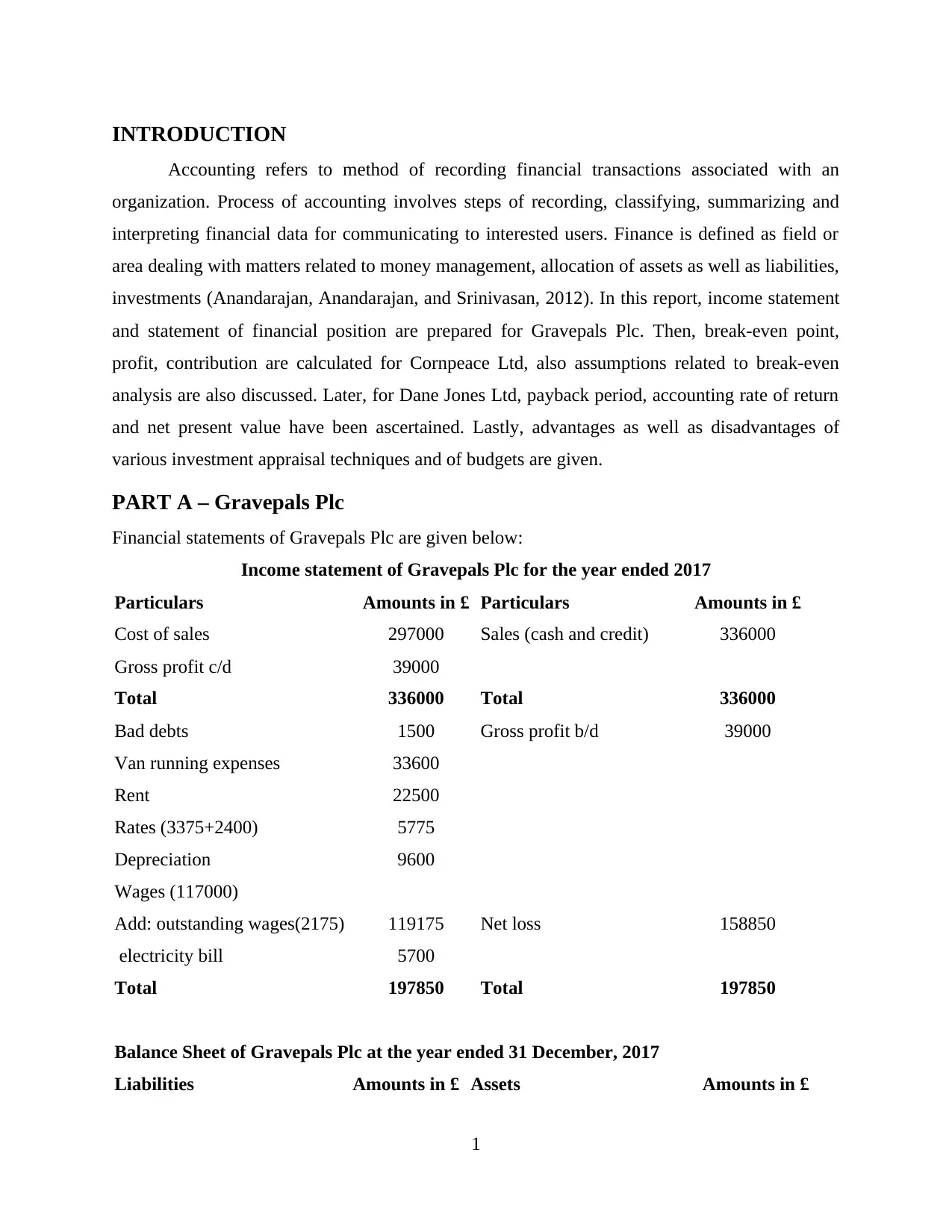

INTRODUCTION

Accounting refers to method of recording financial transactions associated with an

organization. Process of accounting involves steps of recording, classifying, summarizing and

interpreting financial data for communicating to interested users. Finance is defined as field or

area dealing with matters related to money management, allocation of assets as well as liabilities,

investments (Anandarajan, Anandarajan, and Srinivasan, 2012). In this report, income statement

and statement of financial position are prepared for Gravepals Plc. Then, break-even point,

profit, contribution are calculated for Cornpeace Ltd, also assumptions related to break-even

analysis are also discussed. Later, for Dane Jones Ltd, payback period, accounting rate of return

and net present value have been ascertained. Lastly, advantages as well as disadvantages of

various investment appraisal techniques and of budgets are given.

PART A – Gravepals Plc

Financial statements of Gravepals Plc are given below:

Income statement of Gravepals Plc for the year ended 2017

Particulars Amounts in £ Particulars Amounts in £

Cost of sales 297000 Sales (cash and credit) 336000

Gross profit c/d 39000

Total 336000 Total 336000

Bad debts 1500 Gross profit b/d 39000

Van running expenses 33600

Rent 22500

Rates (3375+2400) 5775

Depreciation 9600

Wages (117000)

Add: outstanding wages(2175) 119175 Net loss 158850

electricity bill 5700

Total 197850 Total 197850

Balance Sheet of Gravepals Plc at the year ended 31 December, 2017

Liabilities Amounts in £ Assets Amounts in £

1

Accounting refers to method of recording financial transactions associated with an

organization. Process of accounting involves steps of recording, classifying, summarizing and

interpreting financial data for communicating to interested users. Finance is defined as field or

area dealing with matters related to money management, allocation of assets as well as liabilities,

investments (Anandarajan, Anandarajan, and Srinivasan, 2012). In this report, income statement

and statement of financial position are prepared for Gravepals Plc. Then, break-even point,

profit, contribution are calculated for Cornpeace Ltd, also assumptions related to break-even

analysis are also discussed. Later, for Dane Jones Ltd, payback period, accounting rate of return

and net present value have been ascertained. Lastly, advantages as well as disadvantages of

various investment appraisal techniques and of budgets are given.

PART A – Gravepals Plc

Financial statements of Gravepals Plc are given below:

Income statement of Gravepals Plc for the year ended 2017

Particulars Amounts in £ Particulars Amounts in £

Cost of sales 297000 Sales (cash and credit) 336000

Gross profit c/d 39000

Total 336000 Total 336000

Bad debts 1500 Gross profit b/d 39000

Van running expenses 33600

Rent 22500

Rates (3375+2400) 5775

Depreciation 9600

Wages (117000)

Add: outstanding wages(2175) 119175 Net loss 158850

electricity bill 5700

Total 197850 Total 197850

Balance Sheet of Gravepals Plc at the year ended 31 December, 2017

Liabilities Amounts in £ Assets Amounts in £

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

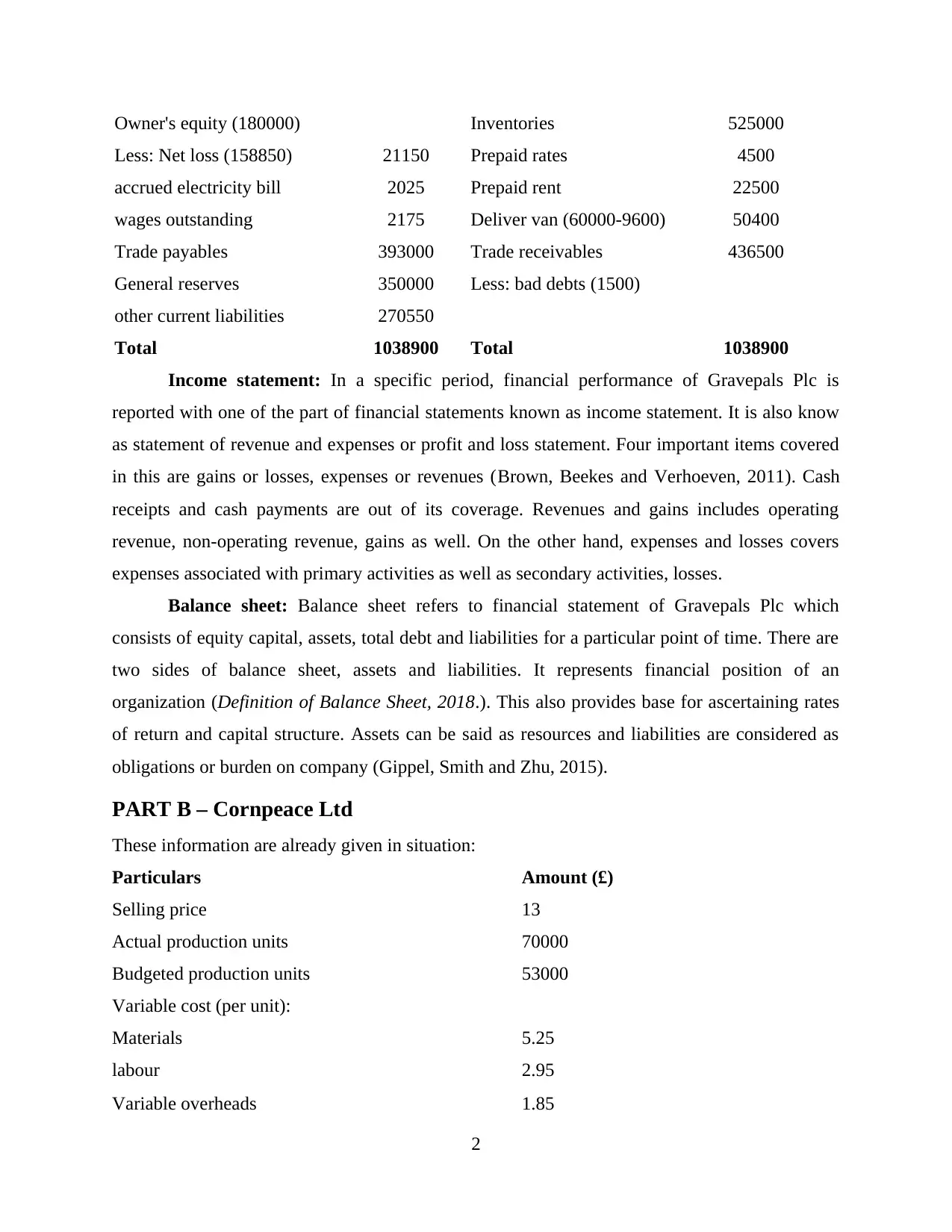

Owner's equity (180000) Inventories 525000

Less: Net loss (158850) 21150 Prepaid rates 4500

accrued electricity bill 2025 Prepaid rent 22500

wages outstanding 2175 Deliver van (60000-9600) 50400

Trade payables 393000 Trade receivables 436500

General reserves 350000 Less: bad debts (1500)

other current liabilities 270550

Total 1038900 Total 1038900

Income statement: In a specific period, financial performance of Gravepals Plc is

reported with one of the part of financial statements known as income statement. It is also know

as statement of revenue and expenses or profit and loss statement. Four important items covered

in this are gains or losses, expenses or revenues (Brown, Beekes and Verhoeven, 2011). Cash

receipts and cash payments are out of its coverage. Revenues and gains includes operating

revenue, non-operating revenue, gains as well. On the other hand, expenses and losses covers

expenses associated with primary activities as well as secondary activities, losses.

Balance sheet: Balance sheet refers to financial statement of Gravepals Plc which

consists of equity capital, assets, total debt and liabilities for a particular point of time. There are

two sides of balance sheet, assets and liabilities. It represents financial position of an

organization (Definition of Balance Sheet, 2018.). This also provides base for ascertaining rates

of return and capital structure. Assets can be said as resources and liabilities are considered as

obligations or burden on company (Gippel, Smith and Zhu, 2015).

PART B – Cornpeace Ltd

These information are already given in situation:

Particulars Amount (£)

Selling price 13

Actual production units 70000

Budgeted production units 53000

Variable cost (per unit):

Materials 5.25

labour 2.95

Variable overheads 1.85

2

Less: Net loss (158850) 21150 Prepaid rates 4500

accrued electricity bill 2025 Prepaid rent 22500

wages outstanding 2175 Deliver van (60000-9600) 50400

Trade payables 393000 Trade receivables 436500

General reserves 350000 Less: bad debts (1500)

other current liabilities 270550

Total 1038900 Total 1038900

Income statement: In a specific period, financial performance of Gravepals Plc is

reported with one of the part of financial statements known as income statement. It is also know

as statement of revenue and expenses or profit and loss statement. Four important items covered

in this are gains or losses, expenses or revenues (Brown, Beekes and Verhoeven, 2011). Cash

receipts and cash payments are out of its coverage. Revenues and gains includes operating

revenue, non-operating revenue, gains as well. On the other hand, expenses and losses covers

expenses associated with primary activities as well as secondary activities, losses.

Balance sheet: Balance sheet refers to financial statement of Gravepals Plc which

consists of equity capital, assets, total debt and liabilities for a particular point of time. There are

two sides of balance sheet, assets and liabilities. It represents financial position of an

organization (Definition of Balance Sheet, 2018.). This also provides base for ascertaining rates

of return and capital structure. Assets can be said as resources and liabilities are considered as

obligations or burden on company (Gippel, Smith and Zhu, 2015).

PART B – Cornpeace Ltd

These information are already given in situation:

Particulars Amount (£)

Selling price 13

Actual production units 70000

Budgeted production units 53000

Variable cost (per unit):

Materials 5.25

labour 2.95

Variable overheads 1.85

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

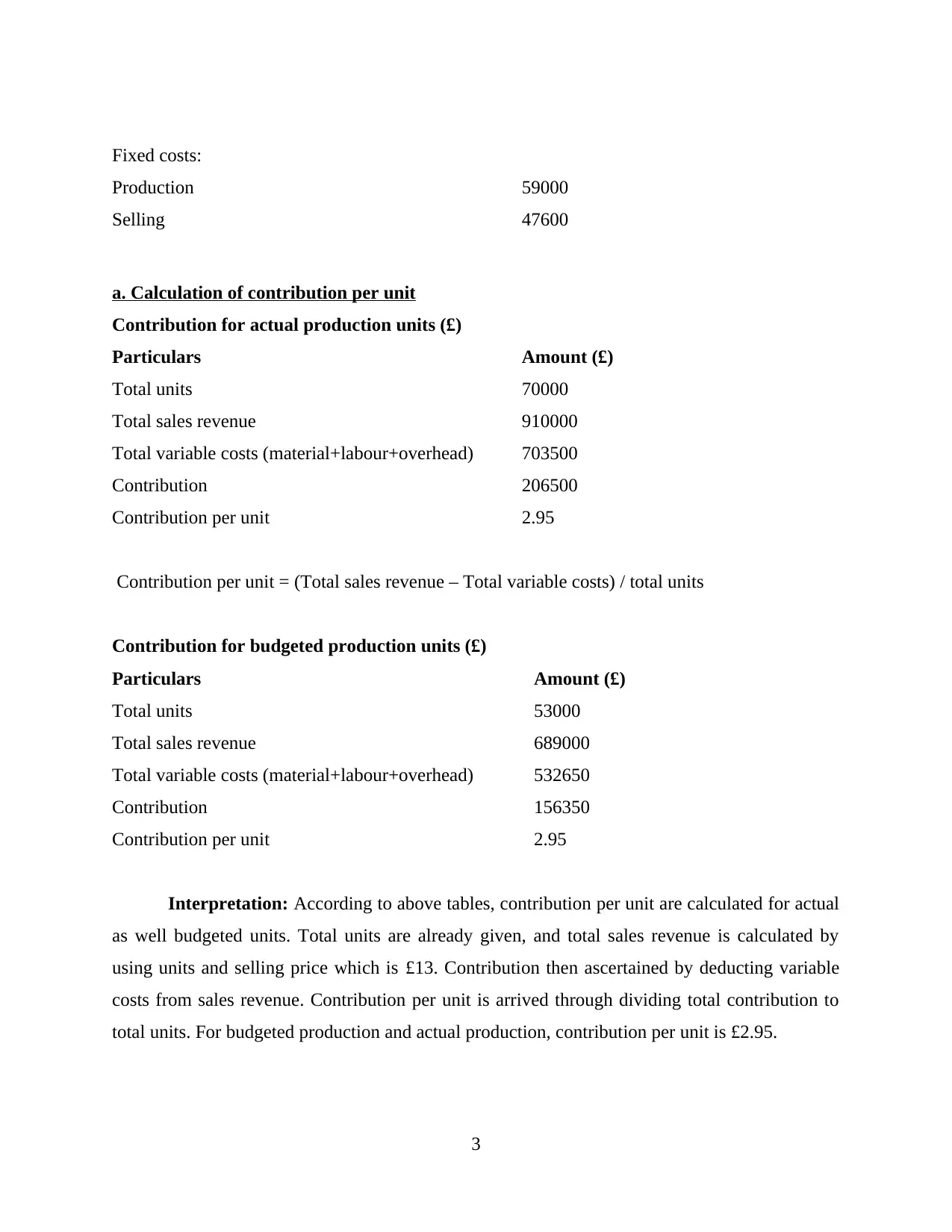

Fixed costs:

Production 59000

Selling 47600

a. Calculation of contribution per unit

Contribution for actual production units (£)

Particulars Amount (£)

Total units 70000

Total sales revenue 910000

Total variable costs (material+labour+overhead) 703500

Contribution 206500

Contribution per unit 2.95

Contribution per unit = (Total sales revenue – Total variable costs) / total units

Contribution for budgeted production units (£)

Particulars Amount (£)

Total units 53000

Total sales revenue 689000

Total variable costs (material+labour+overhead) 532650

Contribution 156350

Contribution per unit 2.95

Interpretation: According to above tables, contribution per unit are calculated for actual

as well budgeted units. Total units are already given, and total sales revenue is calculated by

using units and selling price which is £13. Contribution then ascertained by deducting variable

costs from sales revenue. Contribution per unit is arrived through dividing total contribution to

total units. For budgeted production and actual production, contribution per unit is £2.95.

3

Production 59000

Selling 47600

a. Calculation of contribution per unit

Contribution for actual production units (£)

Particulars Amount (£)

Total units 70000

Total sales revenue 910000

Total variable costs (material+labour+overhead) 703500

Contribution 206500

Contribution per unit 2.95

Contribution per unit = (Total sales revenue – Total variable costs) / total units

Contribution for budgeted production units (£)

Particulars Amount (£)

Total units 53000

Total sales revenue 689000

Total variable costs (material+labour+overhead) 532650

Contribution 156350

Contribution per unit 2.95

Interpretation: According to above tables, contribution per unit are calculated for actual

as well budgeted units. Total units are already given, and total sales revenue is calculated by

using units and selling price which is £13. Contribution then ascertained by deducting variable

costs from sales revenue. Contribution per unit is arrived through dividing total contribution to

total units. For budgeted production and actual production, contribution per unit is £2.95.

3

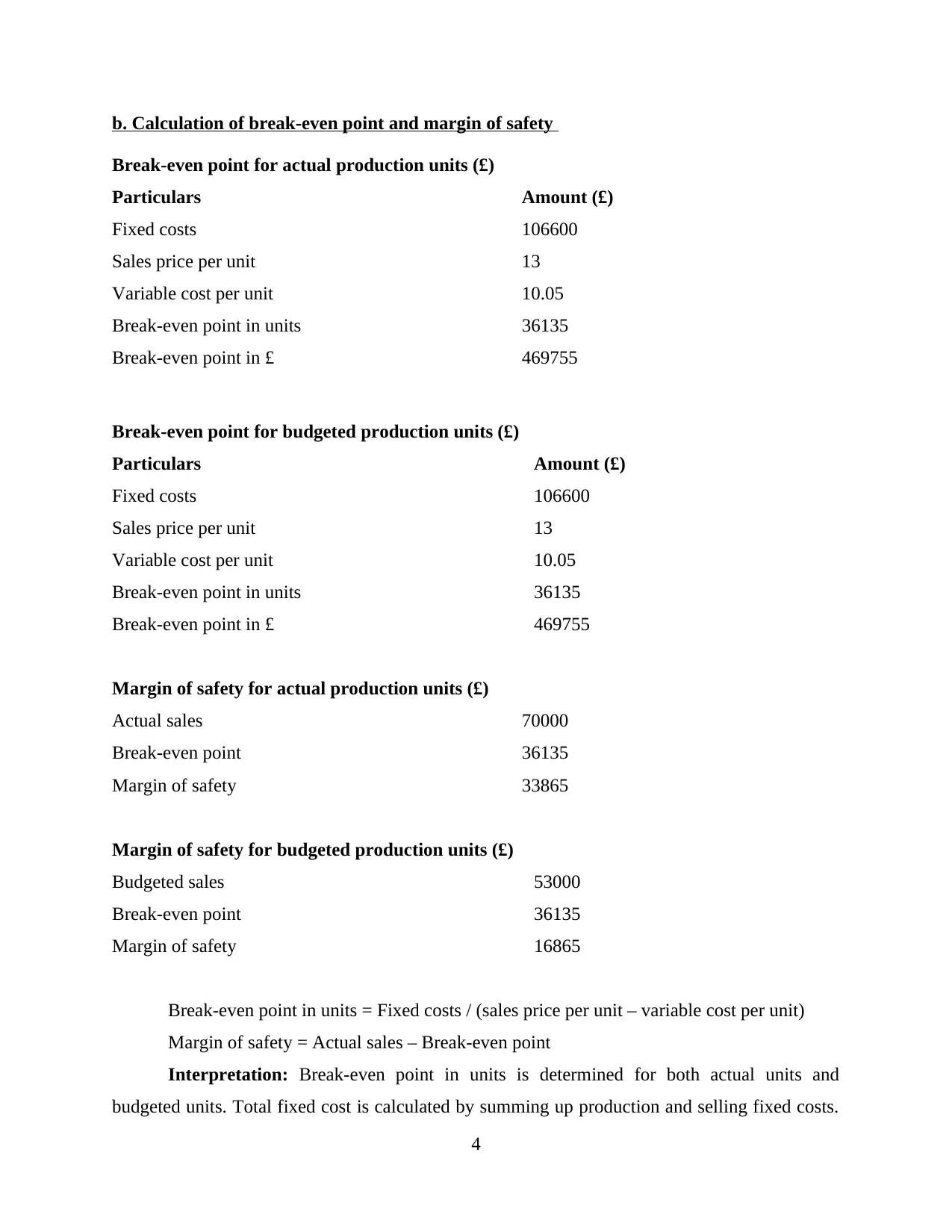

b. Calculation of break-even point and margin of safety

Break-even point for actual production units (£)

Particulars Amount (£)

Fixed costs 106600

Sales price per unit 13

Variable cost per unit 10.05

Break-even point in units 36135

Break-even point in £ 469755

Break-even point for budgeted production units (£)

Particulars Amount (£)

Fixed costs 106600

Sales price per unit 13

Variable cost per unit 10.05

Break-even point in units 36135

Break-even point in £ 469755

Margin of safety for actual production units (£)

Actual sales 70000

Break-even point 36135

Margin of safety 33865

Margin of safety for budgeted production units (£)

Budgeted sales 53000

Break-even point 36135

Margin of safety 16865

Break-even point in units = Fixed costs / (sales price per unit – variable cost per unit)

Margin of safety = Actual sales – Break-even point

Interpretation: Break-even point in units is determined for both actual units and

budgeted units. Total fixed cost is calculated by summing up production and selling fixed costs.

4

Break-even point for actual production units (£)

Particulars Amount (£)

Fixed costs 106600

Sales price per unit 13

Variable cost per unit 10.05

Break-even point in units 36135

Break-even point in £ 469755

Break-even point for budgeted production units (£)

Particulars Amount (£)

Fixed costs 106600

Sales price per unit 13

Variable cost per unit 10.05

Break-even point in units 36135

Break-even point in £ 469755

Margin of safety for actual production units (£)

Actual sales 70000

Break-even point 36135

Margin of safety 33865

Margin of safety for budgeted production units (£)

Budgeted sales 53000

Break-even point 36135

Margin of safety 16865

Break-even point in units = Fixed costs / (sales price per unit – variable cost per unit)

Margin of safety = Actual sales – Break-even point

Interpretation: Break-even point in units is determined for both actual units and

budgeted units. Total fixed cost is calculated by summing up production and selling fixed costs.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

After that, variable cost per unit is arrived after accumulating material, labour and variable

overheads. Margin of safety is also calculated after break-even point.

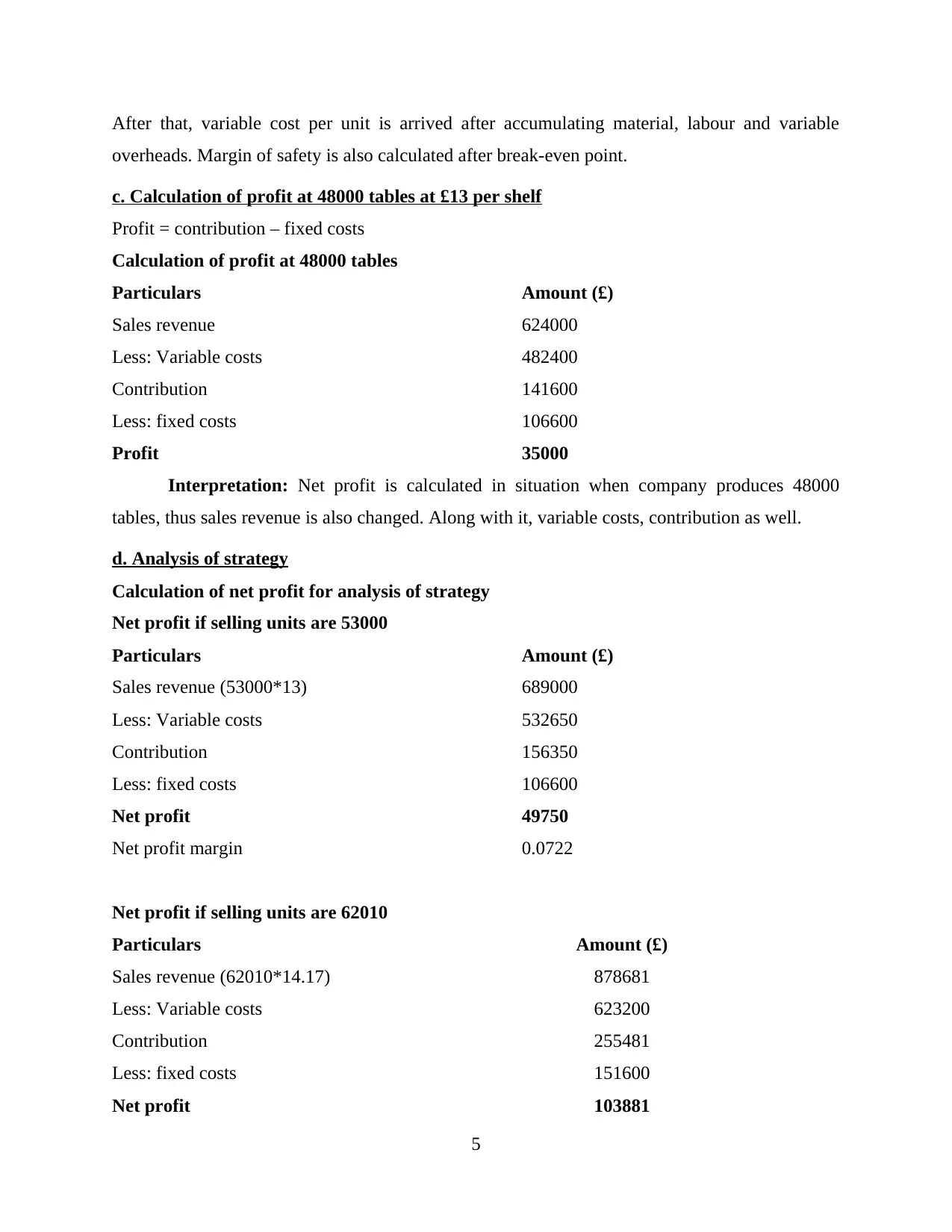

c. Calculation of profit at 48000 tables at £13 per shelf

Profit = contribution – fixed costs

Calculation of profit at 48000 tables

Particulars Amount (£)

Sales revenue 624000

Less: Variable costs 482400

Contribution 141600

Less: fixed costs 106600

Profit 35000

Interpretation: Net profit is calculated in situation when company produces 48000

tables, thus sales revenue is also changed. Along with it, variable costs, contribution as well.

d. Analysis of strategy

Calculation of net profit for analysis of strategy

Net profit if selling units are 53000

Particulars Amount (£)

Sales revenue (53000*13) 689000

Less: Variable costs 532650

Contribution 156350

Less: fixed costs 106600

Net profit 49750

Net profit margin 0.0722

Net profit if selling units are 62010

Particulars Amount (£)

Sales revenue (62010*14.17) 878681

Less: Variable costs 623200

Contribution 255481

Less: fixed costs 151600

Net profit 103881

5

overheads. Margin of safety is also calculated after break-even point.

c. Calculation of profit at 48000 tables at £13 per shelf

Profit = contribution – fixed costs

Calculation of profit at 48000 tables

Particulars Amount (£)

Sales revenue 624000

Less: Variable costs 482400

Contribution 141600

Less: fixed costs 106600

Profit 35000

Interpretation: Net profit is calculated in situation when company produces 48000

tables, thus sales revenue is also changed. Along with it, variable costs, contribution as well.

d. Analysis of strategy

Calculation of net profit for analysis of strategy

Net profit if selling units are 53000

Particulars Amount (£)

Sales revenue (53000*13) 689000

Less: Variable costs 532650

Contribution 156350

Less: fixed costs 106600

Net profit 49750

Net profit margin 0.0722

Net profit if selling units are 62010

Particulars Amount (£)

Sales revenue (62010*14.17) 878681

Less: Variable costs 623200

Contribution 255481

Less: fixed costs 151600

Net profit 103881

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

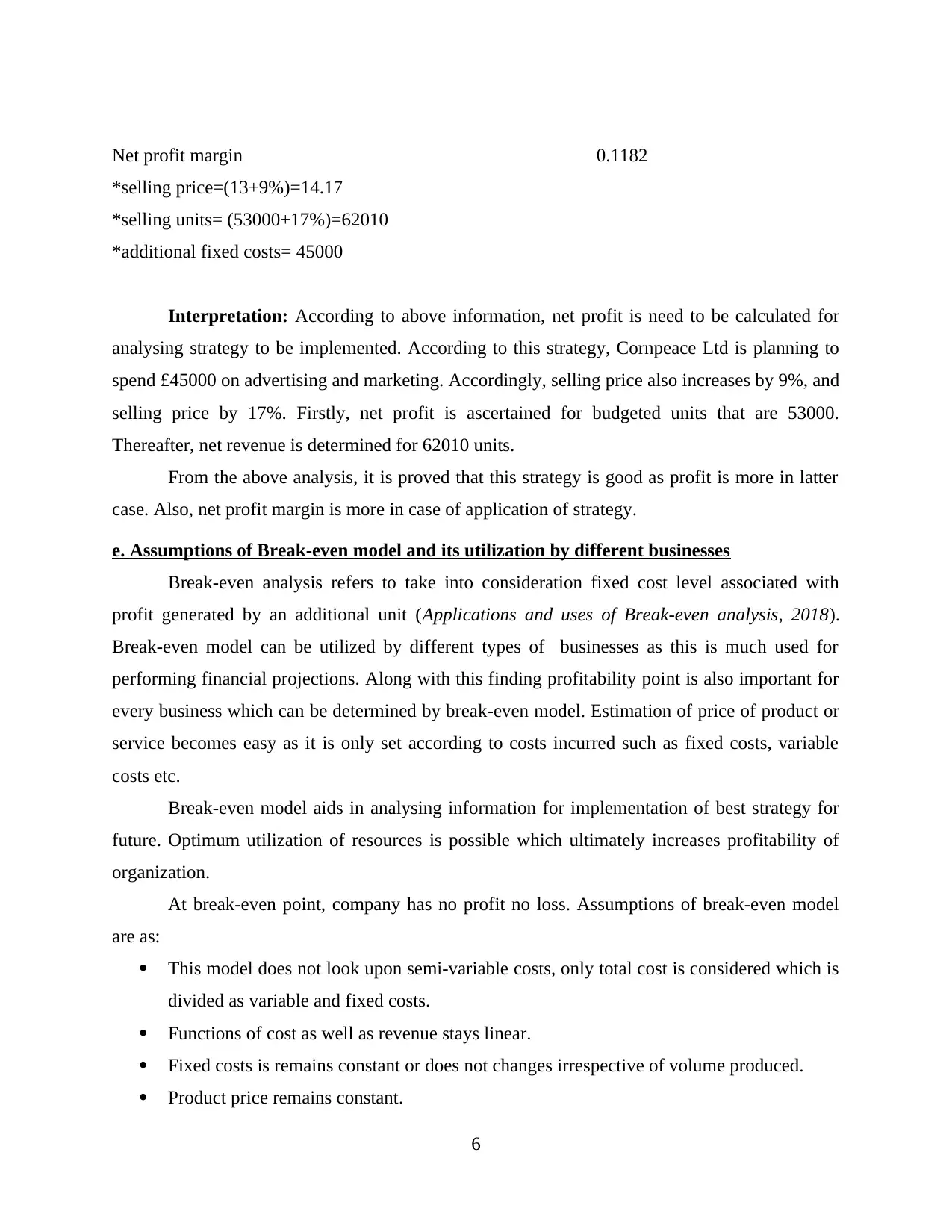

Net profit margin 0.1182

*selling price=(13+9%)=14.17

*selling units= (53000+17%)=62010

*additional fixed costs= 45000

Interpretation: According to above information, net profit is need to be calculated for

analysing strategy to be implemented. According to this strategy, Cornpeace Ltd is planning to

spend £45000 on advertising and marketing. Accordingly, selling price also increases by 9%, and

selling price by 17%. Firstly, net profit is ascertained for budgeted units that are 53000.

Thereafter, net revenue is determined for 62010 units.

From the above analysis, it is proved that this strategy is good as profit is more in latter

case. Also, net profit margin is more in case of application of strategy.

e. Assumptions of Break-even model and its utilization by different businesses

Break-even analysis refers to take into consideration fixed cost level associated with

profit generated by an additional unit (Applications and uses of Break-even analysis, 2018).

Break-even model can be utilized by different types of businesses as this is much used for

performing financial projections. Along with this finding profitability point is also important for

every business which can be determined by break-even model. Estimation of price of product or

service becomes easy as it is only set according to costs incurred such as fixed costs, variable

costs etc.

Break-even model aids in analysing information for implementation of best strategy for

future. Optimum utilization of resources is possible which ultimately increases profitability of

organization.

At break-even point, company has no profit no loss. Assumptions of break-even model

are as:

This model does not look upon semi-variable costs, only total cost is considered which is

divided as variable and fixed costs.

Functions of cost as well as revenue stays linear.

Fixed costs is remains constant or does not changes irrespective of volume produced.

Product price remains constant.

6

*selling price=(13+9%)=14.17

*selling units= (53000+17%)=62010

*additional fixed costs= 45000

Interpretation: According to above information, net profit is need to be calculated for

analysing strategy to be implemented. According to this strategy, Cornpeace Ltd is planning to

spend £45000 on advertising and marketing. Accordingly, selling price also increases by 9%, and

selling price by 17%. Firstly, net profit is ascertained for budgeted units that are 53000.

Thereafter, net revenue is determined for 62010 units.

From the above analysis, it is proved that this strategy is good as profit is more in latter

case. Also, net profit margin is more in case of application of strategy.

e. Assumptions of Break-even model and its utilization by different businesses

Break-even analysis refers to take into consideration fixed cost level associated with

profit generated by an additional unit (Applications and uses of Break-even analysis, 2018).

Break-even model can be utilized by different types of businesses as this is much used for

performing financial projections. Along with this finding profitability point is also important for

every business which can be determined by break-even model. Estimation of price of product or

service becomes easy as it is only set according to costs incurred such as fixed costs, variable

costs etc.

Break-even model aids in analysing information for implementation of best strategy for

future. Optimum utilization of resources is possible which ultimately increases profitability of

organization.

At break-even point, company has no profit no loss. Assumptions of break-even model

are as:

This model does not look upon semi-variable costs, only total cost is considered which is

divided as variable and fixed costs.

Functions of cost as well as revenue stays linear.

Fixed costs is remains constant or does not changes irrespective of volume produced.

Product price remains constant.

6

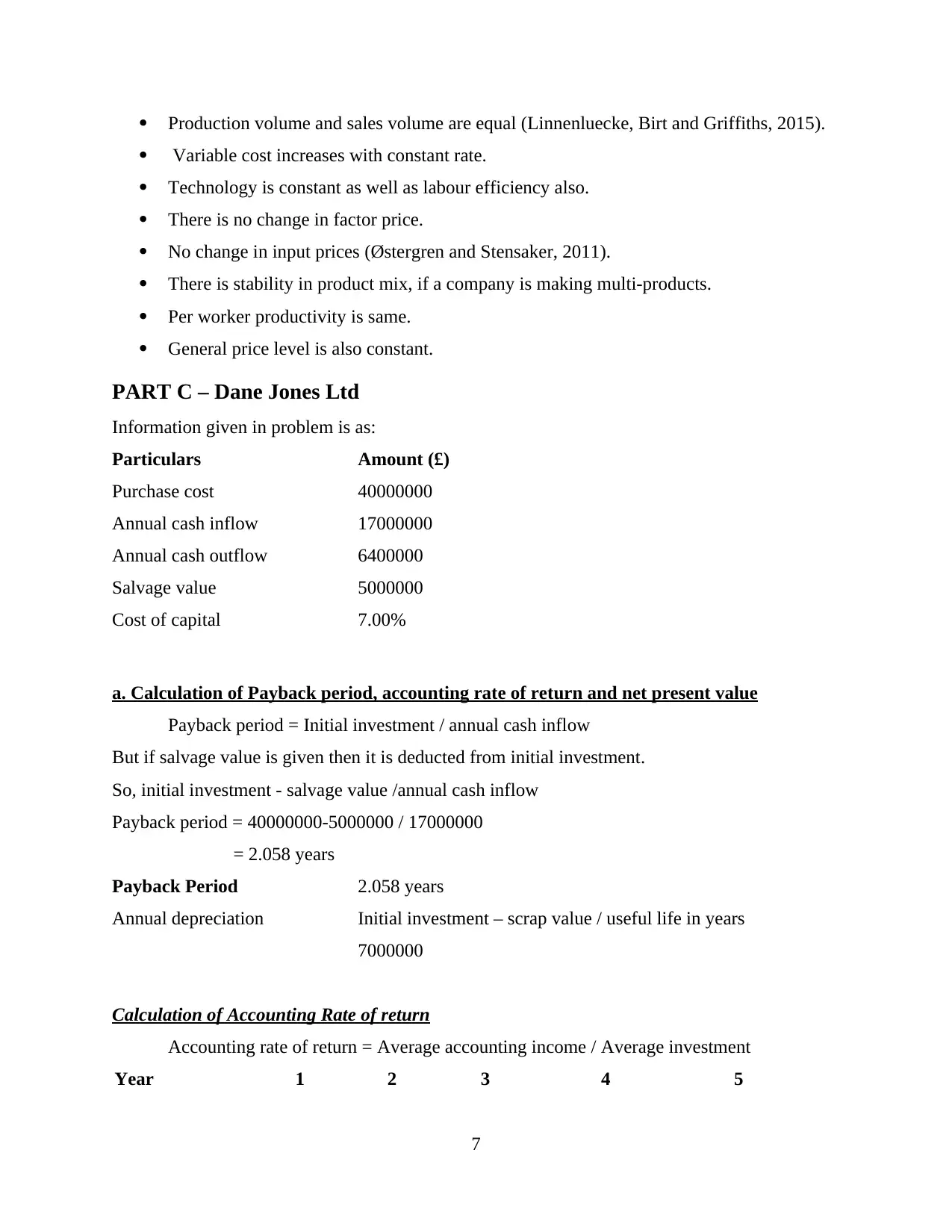

Production volume and sales volume are equal (Linnenluecke, Birt and Griffiths, 2015).

Variable cost increases with constant rate.

Technology is constant as well as labour efficiency also.

There is no change in factor price.

No change in input prices (Østergren and Stensaker, 2011).

There is stability in product mix, if a company is making multi-products.

Per worker productivity is same.

General price level is also constant.

PART C – Dane Jones Ltd

Information given in problem is as:

Particulars Amount (£)

Purchase cost 40000000

Annual cash inflow 17000000

Annual cash outflow 6400000

Salvage value 5000000

Cost of capital 7.00%

a. Calculation of Payback period, accounting rate of return and net present value

Payback period = Initial investment / annual cash inflow

But if salvage value is given then it is deducted from initial investment.

So, initial investment - salvage value /annual cash inflow

Payback period = 40000000-5000000 / 17000000

= 2.058 years

Payback Period 2.058 years

Annual depreciation Initial investment – scrap value / useful life in years

7000000

Calculation of Accounting Rate of return

Accounting rate of return = Average accounting income / Average investment

Year 1 2 3 4 5

7

Variable cost increases with constant rate.

Technology is constant as well as labour efficiency also.

There is no change in factor price.

No change in input prices (Østergren and Stensaker, 2011).

There is stability in product mix, if a company is making multi-products.

Per worker productivity is same.

General price level is also constant.

PART C – Dane Jones Ltd

Information given in problem is as:

Particulars Amount (£)

Purchase cost 40000000

Annual cash inflow 17000000

Annual cash outflow 6400000

Salvage value 5000000

Cost of capital 7.00%

a. Calculation of Payback period, accounting rate of return and net present value

Payback period = Initial investment / annual cash inflow

But if salvage value is given then it is deducted from initial investment.

So, initial investment - salvage value /annual cash inflow

Payback period = 40000000-5000000 / 17000000

= 2.058 years

Payback Period 2.058 years

Annual depreciation Initial investment – scrap value / useful life in years

7000000

Calculation of Accounting Rate of return

Accounting rate of return = Average accounting income / Average investment

Year 1 2 3 4 5

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

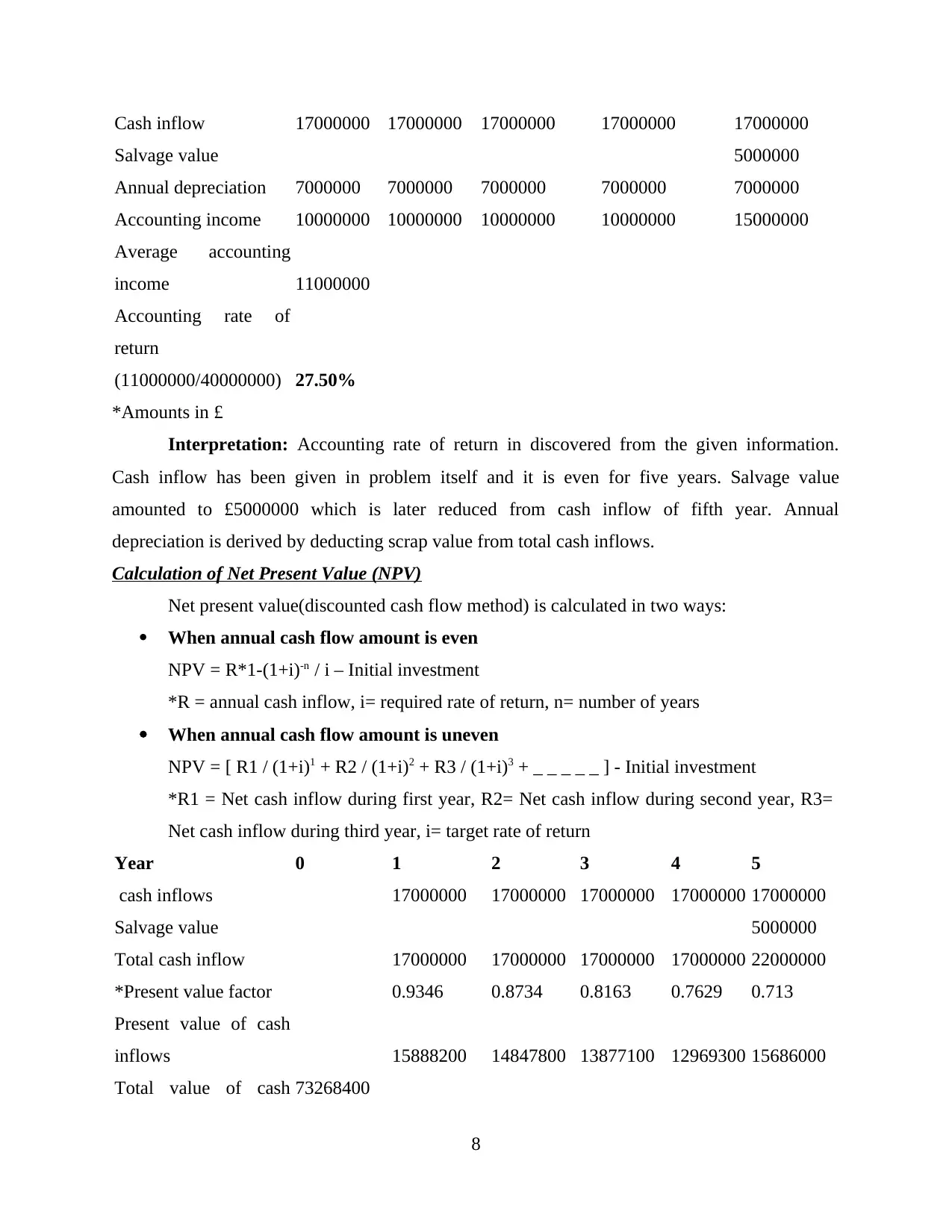

Cash inflow 17000000 17000000 17000000 17000000 17000000

Salvage value 5000000

Annual depreciation 7000000 7000000 7000000 7000000 7000000

Accounting income 10000000 10000000 10000000 10000000 15000000

Average accounting

income 11000000

Accounting rate of

return

(11000000/40000000) 27.50%

*Amounts in £

Interpretation: Accounting rate of return in discovered from the given information.

Cash inflow has been given in problem itself and it is even for five years. Salvage value

amounted to £5000000 which is later reduced from cash inflow of fifth year. Annual

depreciation is derived by deducting scrap value from total cash inflows.

Calculation of Net Present Value (NPV)

Net present value(discounted cash flow method) is calculated in two ways:

When annual cash flow amount is even

NPV = R*1-(1+i)-n / i – Initial investment

*R = annual cash inflow, i= required rate of return, n= number of years

When annual cash flow amount is uneven

NPV = [ R1 / (1+i)1 + R2 / (1+i)2 + R3 / (1+i)3 + _ _ _ _ _ ] - Initial investment

*R1 = Net cash inflow during first year, R2= Net cash inflow during second year, R3=

Net cash inflow during third year, i= target rate of return

Year 0 1 2 3 4 5

cash inflows 17000000 17000000 17000000 17000000 17000000

Salvage value 5000000

Total cash inflow 17000000 17000000 17000000 17000000 22000000

*Present value factor 0.9346 0.8734 0.8163 0.7629 0.713

Present value of cash

inflows 15888200 14847800 13877100 12969300 15686000

Total value of cash 73268400

8

Salvage value 5000000

Annual depreciation 7000000 7000000 7000000 7000000 7000000

Accounting income 10000000 10000000 10000000 10000000 15000000

Average accounting

income 11000000

Accounting rate of

return

(11000000/40000000) 27.50%

*Amounts in £

Interpretation: Accounting rate of return in discovered from the given information.

Cash inflow has been given in problem itself and it is even for five years. Salvage value

amounted to £5000000 which is later reduced from cash inflow of fifth year. Annual

depreciation is derived by deducting scrap value from total cash inflows.

Calculation of Net Present Value (NPV)

Net present value(discounted cash flow method) is calculated in two ways:

When annual cash flow amount is even

NPV = R*1-(1+i)-n / i – Initial investment

*R = annual cash inflow, i= required rate of return, n= number of years

When annual cash flow amount is uneven

NPV = [ R1 / (1+i)1 + R2 / (1+i)2 + R3 / (1+i)3 + _ _ _ _ _ ] - Initial investment

*R1 = Net cash inflow during first year, R2= Net cash inflow during second year, R3=

Net cash inflow during third year, i= target rate of return

Year 0 1 2 3 4 5

cash inflows 17000000 17000000 17000000 17000000 17000000

Salvage value 5000000

Total cash inflow 17000000 17000000 17000000 17000000 22000000

*Present value factor 0.9346 0.8734 0.8163 0.7629 0.713

Present value of cash

inflows 15888200 14847800 13877100 12969300 15686000

Total value of cash 73268400

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

inflows

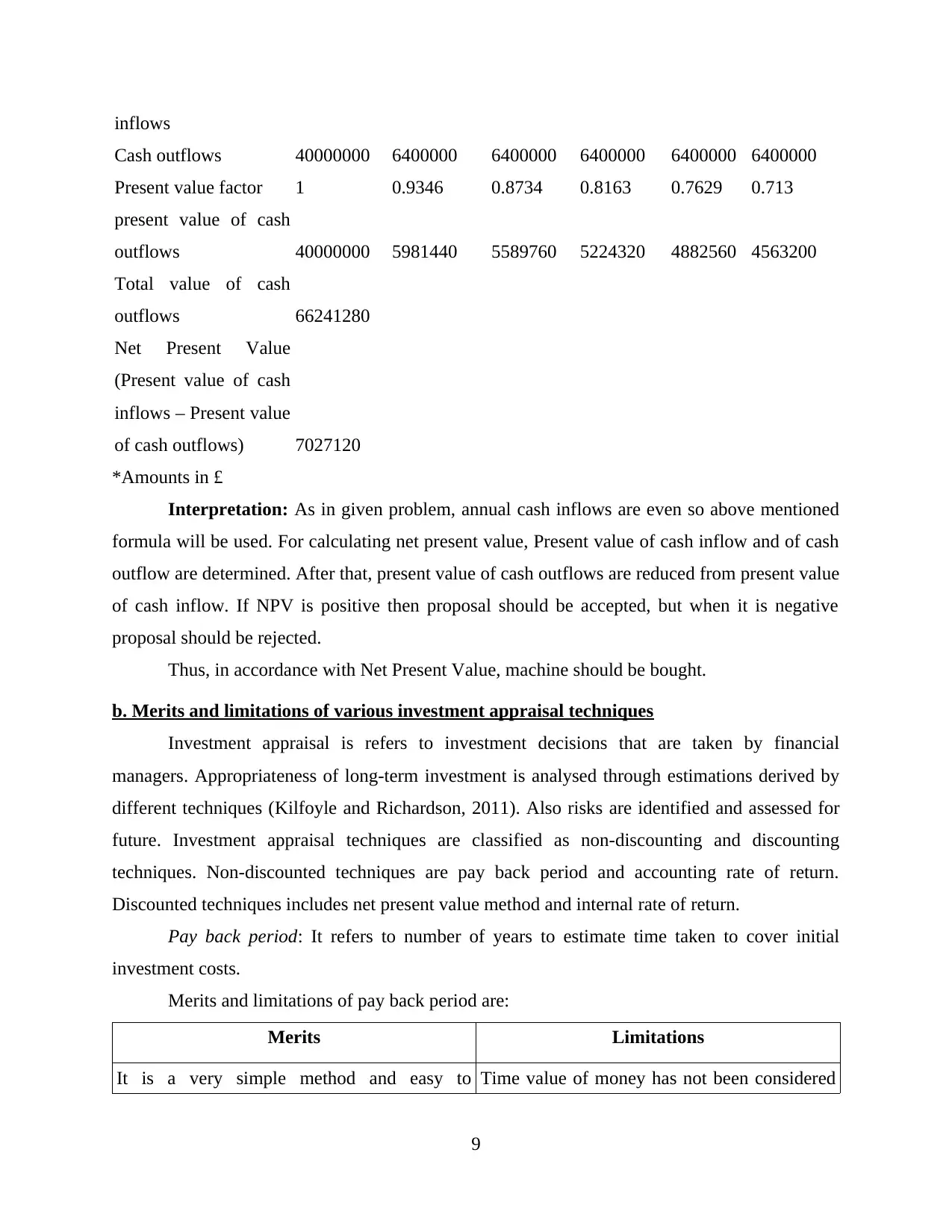

Cash outflows 40000000 6400000 6400000 6400000 6400000 6400000

Present value factor 1 0.9346 0.8734 0.8163 0.7629 0.713

present value of cash

outflows 40000000 5981440 5589760 5224320 4882560 4563200

Total value of cash

outflows 66241280

Net Present Value

(Present value of cash

inflows – Present value

of cash outflows) 7027120

*Amounts in £

Interpretation: As in given problem, annual cash inflows are even so above mentioned

formula will be used. For calculating net present value, Present value of cash inflow and of cash

outflow are determined. After that, present value of cash outflows are reduced from present value

of cash inflow. If NPV is positive then proposal should be accepted, but when it is negative

proposal should be rejected.

Thus, in accordance with Net Present Value, machine should be bought.

b. Merits and limitations of various investment appraisal techniques

Investment appraisal is refers to investment decisions that are taken by financial

managers. Appropriateness of long-term investment is analysed through estimations derived by

different techniques (Kilfoyle and Richardson, 2011). Also risks are identified and assessed for

future. Investment appraisal techniques are classified as non-discounting and discounting

techniques. Non-discounted techniques are pay back period and accounting rate of return.

Discounted techniques includes net present value method and internal rate of return.

Pay back period: It refers to number of years to estimate time taken to cover initial

investment costs.

Merits and limitations of pay back period are:

Merits Limitations

It is a very simple method and easy to Time value of money has not been considered

9

Cash outflows 40000000 6400000 6400000 6400000 6400000 6400000

Present value factor 1 0.9346 0.8734 0.8163 0.7629 0.713

present value of cash

outflows 40000000 5981440 5589760 5224320 4882560 4563200

Total value of cash

outflows 66241280

Net Present Value

(Present value of cash

inflows – Present value

of cash outflows) 7027120

*Amounts in £

Interpretation: As in given problem, annual cash inflows are even so above mentioned

formula will be used. For calculating net present value, Present value of cash inflow and of cash

outflow are determined. After that, present value of cash outflows are reduced from present value

of cash inflow. If NPV is positive then proposal should be accepted, but when it is negative

proposal should be rejected.

Thus, in accordance with Net Present Value, machine should be bought.

b. Merits and limitations of various investment appraisal techniques

Investment appraisal is refers to investment decisions that are taken by financial

managers. Appropriateness of long-term investment is analysed through estimations derived by

different techniques (Kilfoyle and Richardson, 2011). Also risks are identified and assessed for

future. Investment appraisal techniques are classified as non-discounting and discounting

techniques. Non-discounted techniques are pay back period and accounting rate of return.

Discounted techniques includes net present value method and internal rate of return.

Pay back period: It refers to number of years to estimate time taken to cover initial

investment costs.

Merits and limitations of pay back period are:

Merits Limitations

It is a very simple method and easy to Time value of money has not been considered

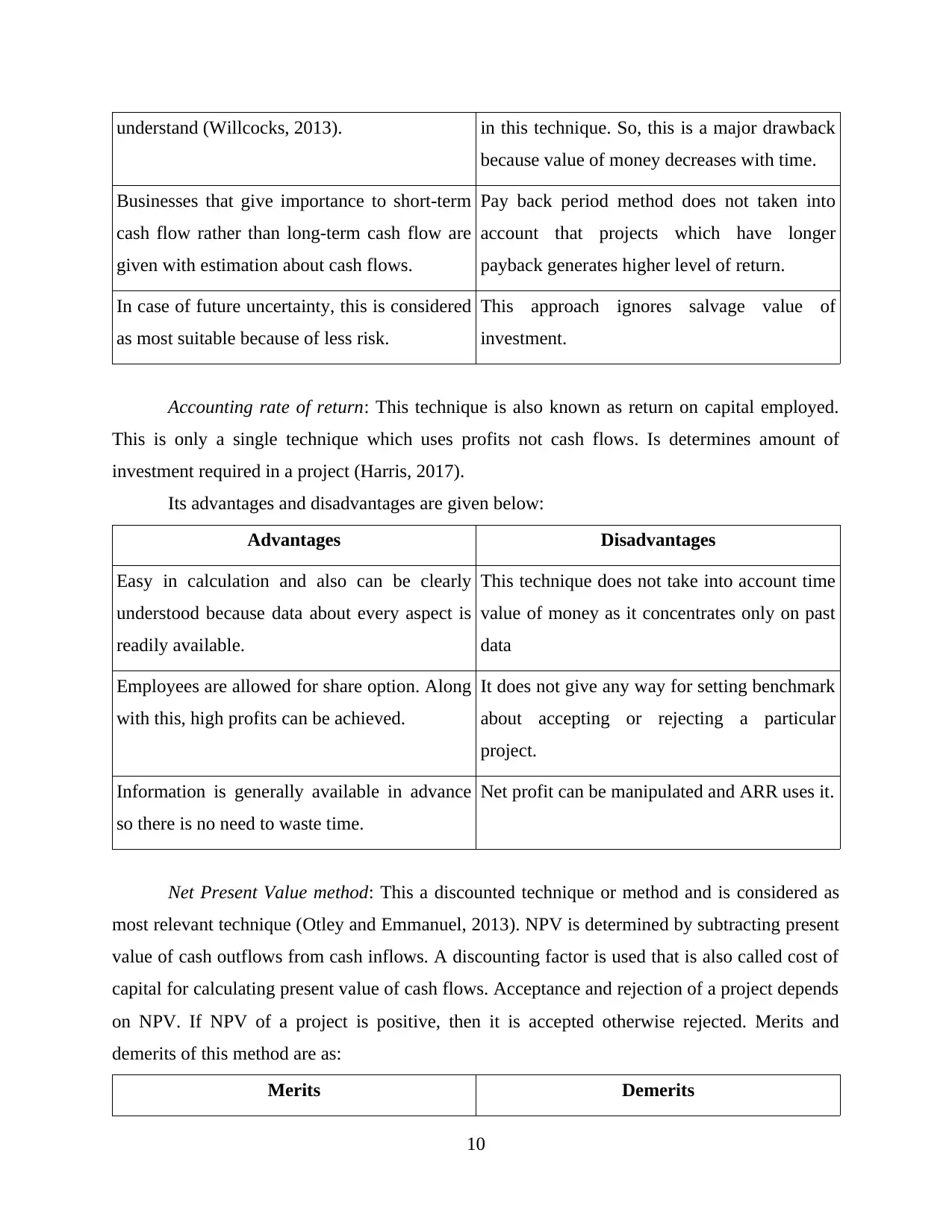

9

understand (Willcocks, 2013). in this technique. So, this is a major drawback

because value of money decreases with time.

Businesses that give importance to short-term

cash flow rather than long-term cash flow are

given with estimation about cash flows.

Pay back period method does not taken into

account that projects which have longer

payback generates higher level of return.

In case of future uncertainty, this is considered

as most suitable because of less risk.

This approach ignores salvage value of

investment.

Accounting rate of return: This technique is also known as return on capital employed.

This is only a single technique which uses profits not cash flows. Is determines amount of

investment required in a project (Harris, 2017).

Its advantages and disadvantages are given below:

Advantages Disadvantages

Easy in calculation and also can be clearly

understood because data about every aspect is

readily available.

This technique does not take into account time

value of money as it concentrates only on past

data

Employees are allowed for share option. Along

with this, high profits can be achieved.

It does not give any way for setting benchmark

about accepting or rejecting a particular

project.

Information is generally available in advance

so there is no need to waste time.

Net profit can be manipulated and ARR uses it.

Net Present Value method: This a discounted technique or method and is considered as

most relevant technique (Otley and Emmanuel, 2013). NPV is determined by subtracting present

value of cash outflows from cash inflows. A discounting factor is used that is also called cost of

capital for calculating present value of cash flows. Acceptance and rejection of a project depends

on NPV. If NPV of a project is positive, then it is accepted otherwise rejected. Merits and

demerits of this method are as:

Merits Demerits

10

because value of money decreases with time.

Businesses that give importance to short-term

cash flow rather than long-term cash flow are

given with estimation about cash flows.

Pay back period method does not taken into

account that projects which have longer

payback generates higher level of return.

In case of future uncertainty, this is considered

as most suitable because of less risk.

This approach ignores salvage value of

investment.

Accounting rate of return: This technique is also known as return on capital employed.

This is only a single technique which uses profits not cash flows. Is determines amount of

investment required in a project (Harris, 2017).

Its advantages and disadvantages are given below:

Advantages Disadvantages

Easy in calculation and also can be clearly

understood because data about every aspect is

readily available.

This technique does not take into account time

value of money as it concentrates only on past

data

Employees are allowed for share option. Along

with this, high profits can be achieved.

It does not give any way for setting benchmark

about accepting or rejecting a particular

project.

Information is generally available in advance

so there is no need to waste time.

Net profit can be manipulated and ARR uses it.

Net Present Value method: This a discounted technique or method and is considered as

most relevant technique (Otley and Emmanuel, 2013). NPV is determined by subtracting present

value of cash outflows from cash inflows. A discounting factor is used that is also called cost of

capital for calculating present value of cash flows. Acceptance and rejection of a project depends

on NPV. If NPV of a project is positive, then it is accepted otherwise rejected. Merits and

demerits of this method are as:

Merits Demerits

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.