Accounting and Finance Report: Saturn and ARB Limited Analysis

VerifiedAdded on 2021/06/17

|16

|2336

|30

Report

AI Summary

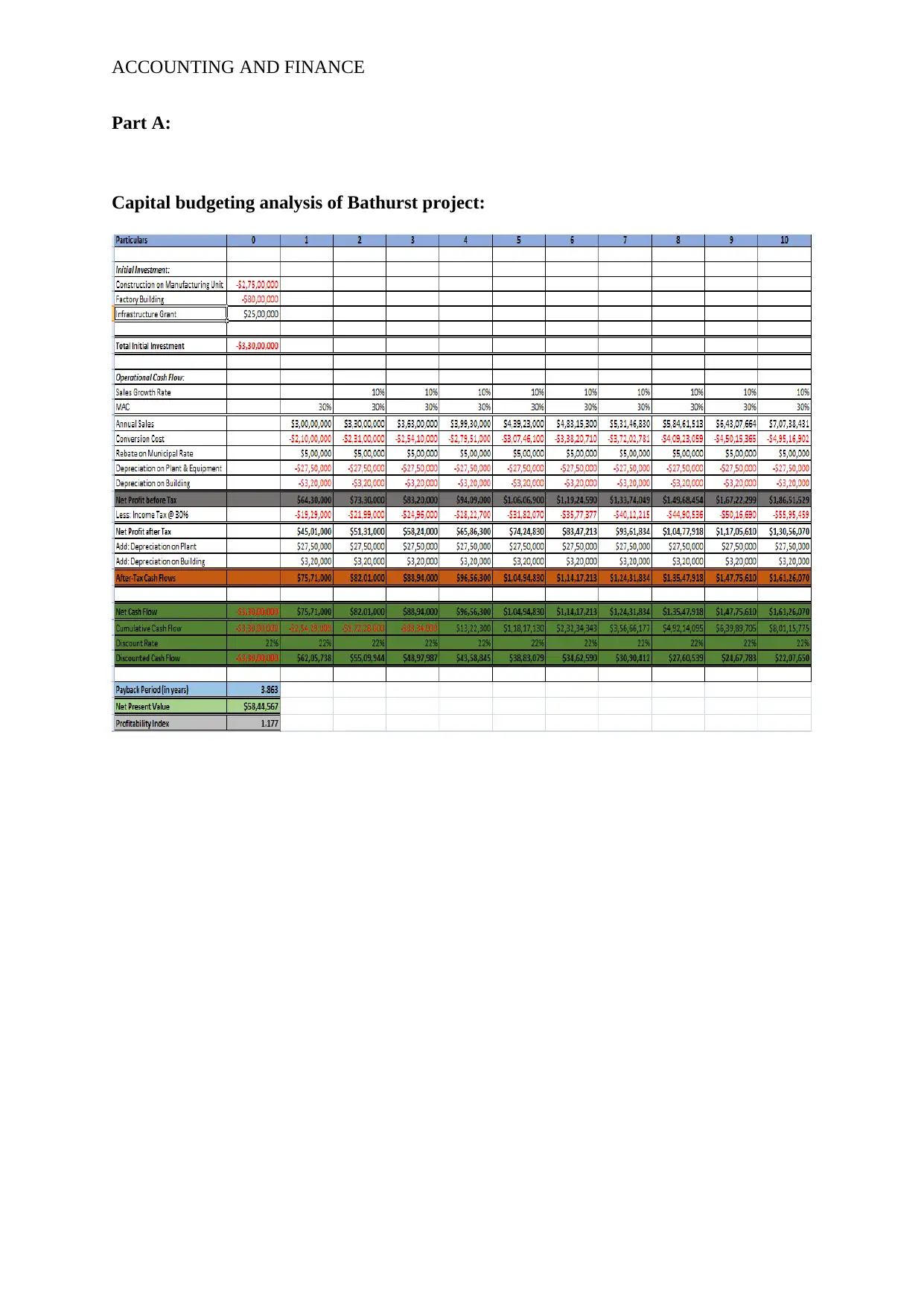

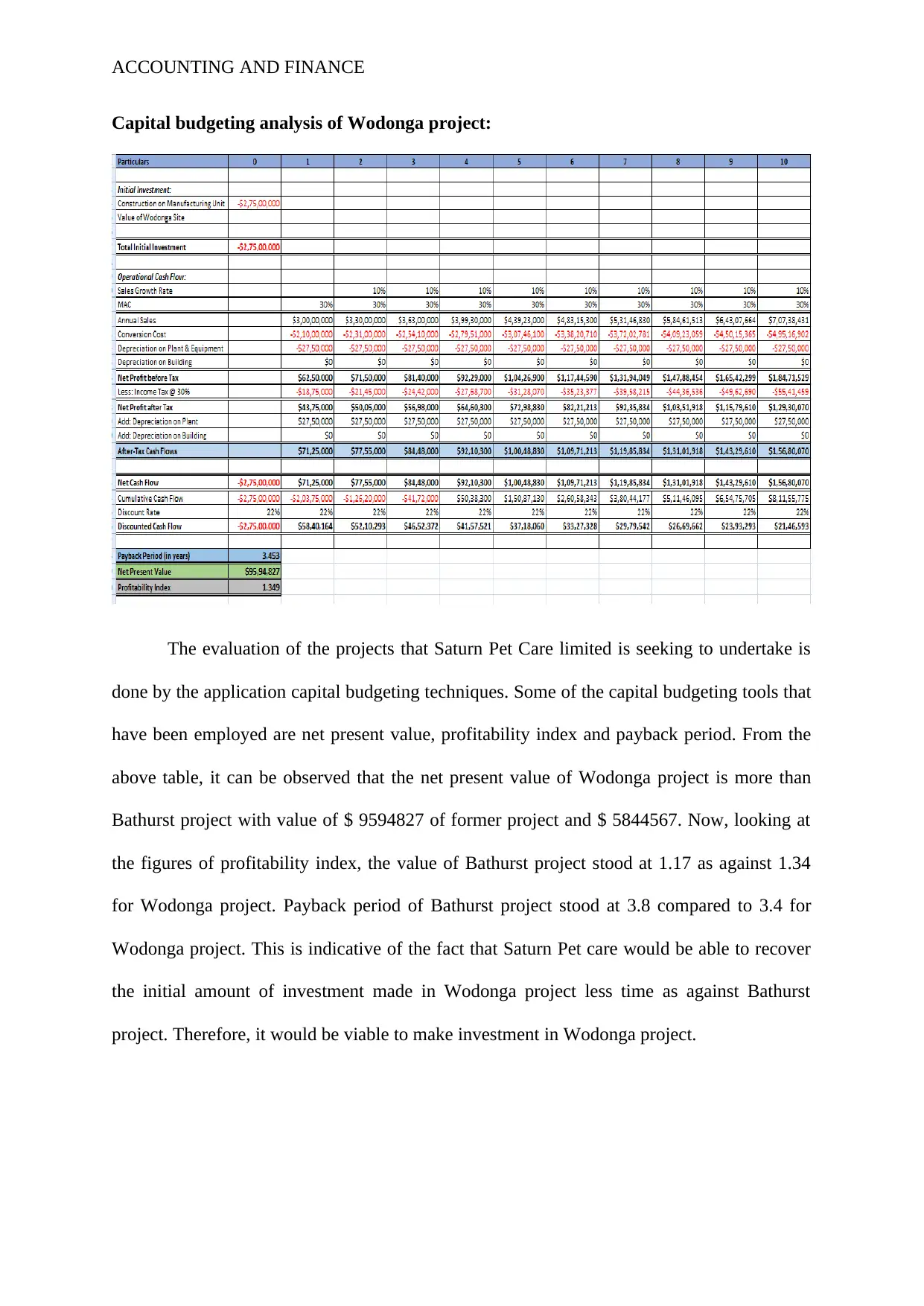

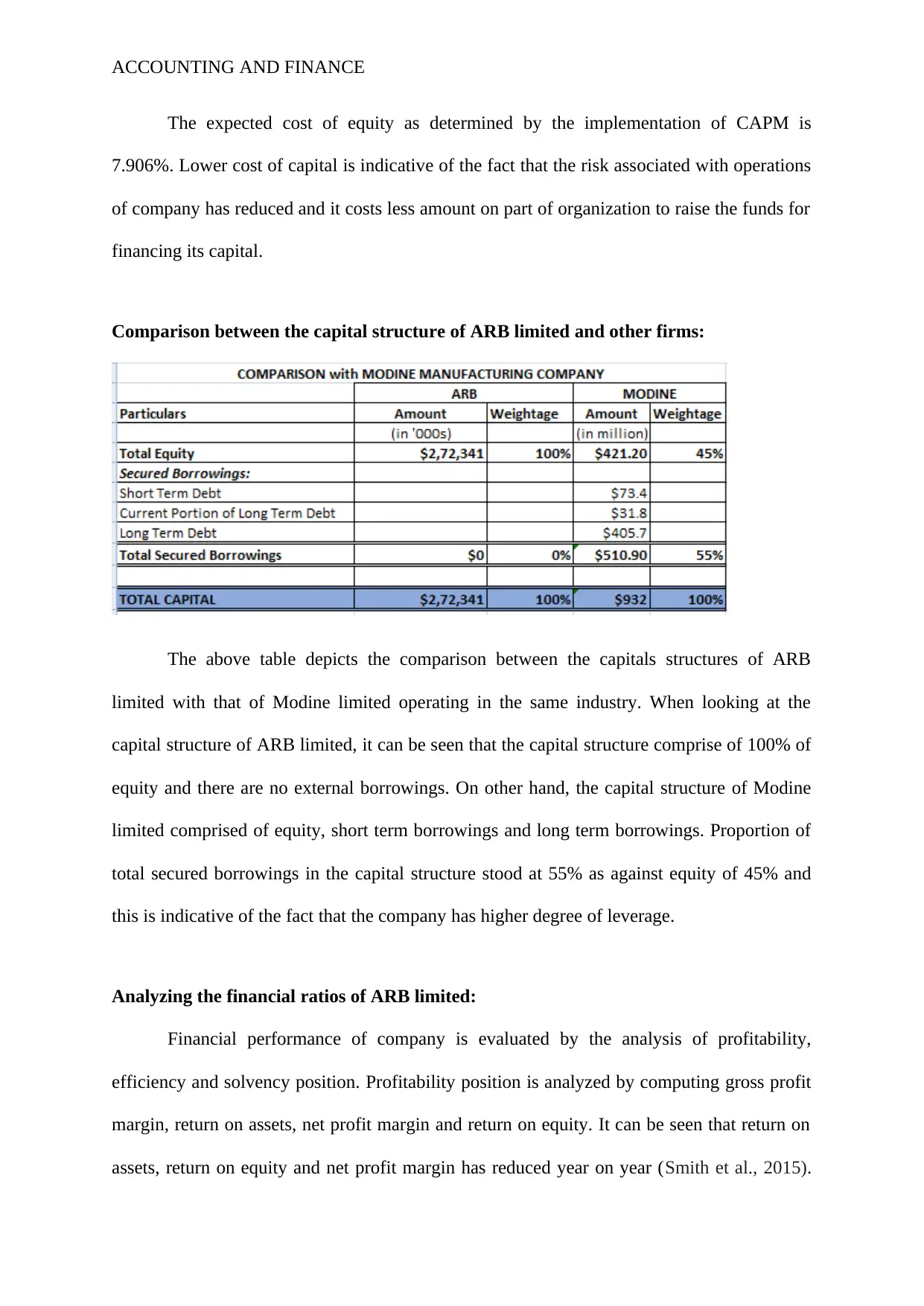

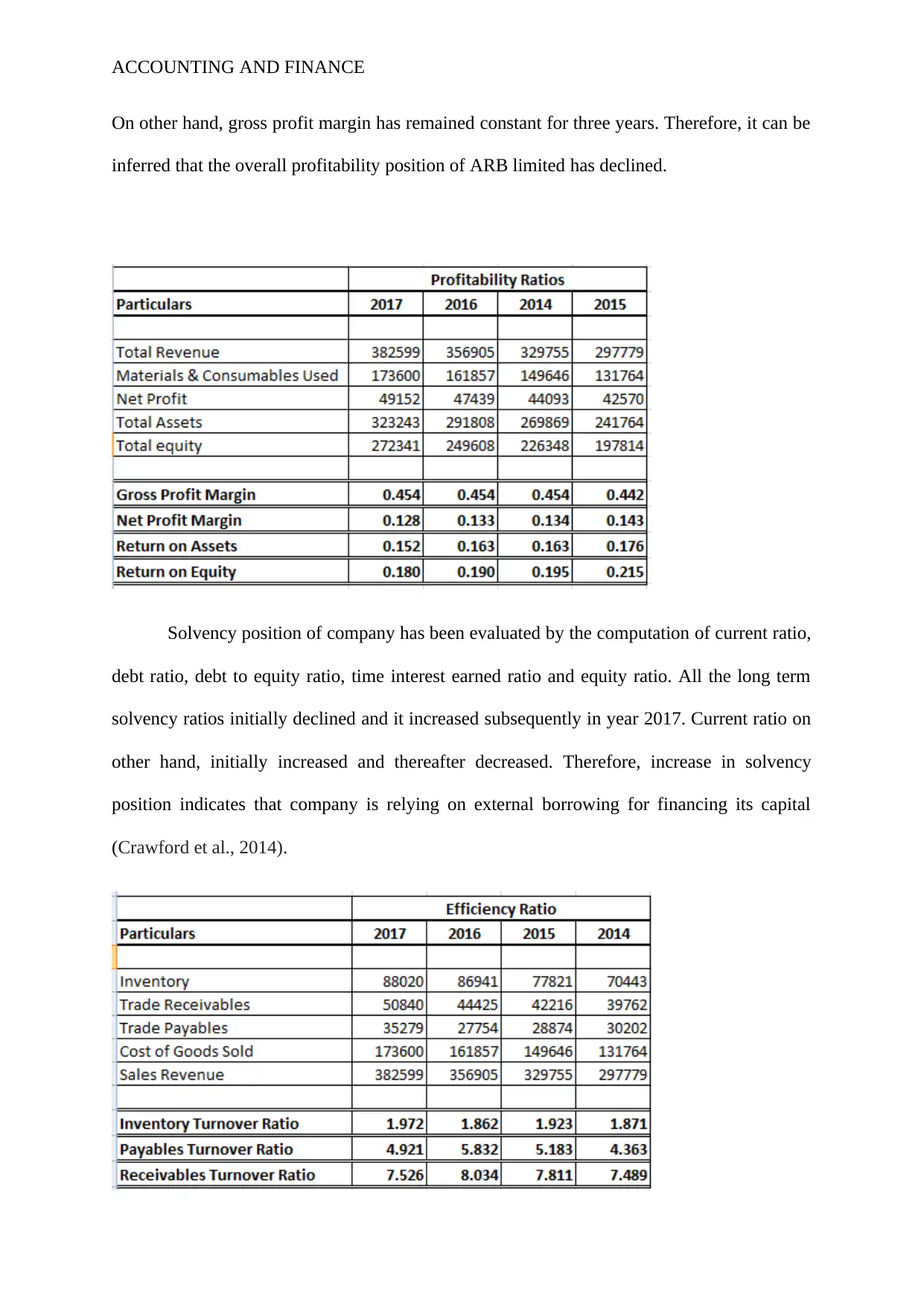

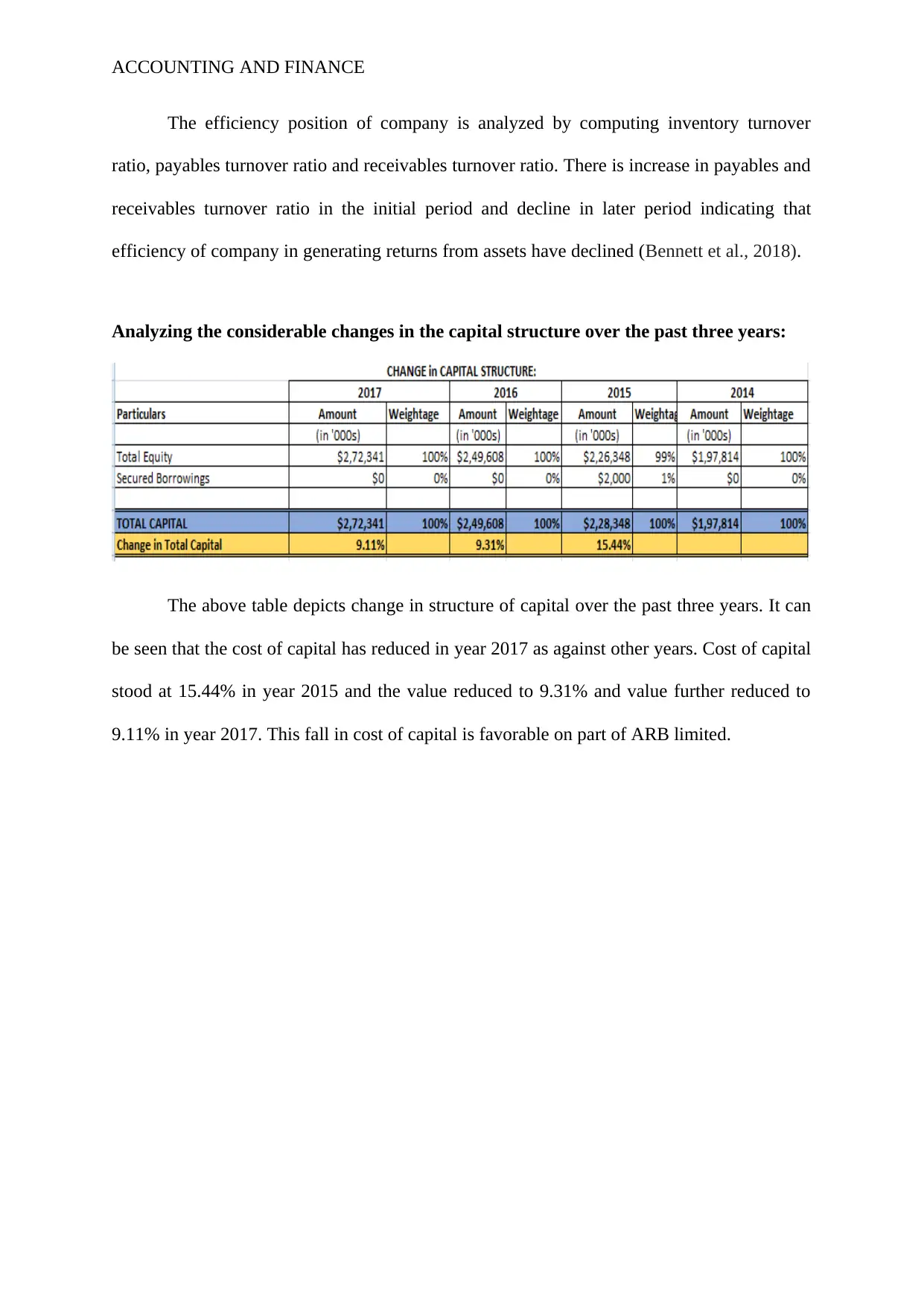

This report presents a comprehensive analysis of accounting and finance principles through two case studies. Part A focuses on Saturn Pet Care, evaluating capital budgeting decisions for the Bathurst and Wodonga projects using techniques like net present value, profitability index, and payback period. It also addresses product cannibalization, sales budget errors, and the inclusion of original factory costs. Part B analyzes ARB Limited's capital structure, calculating WACC, determining the appropriate return using CAPM, and comparing the company's structure with industry peers. The report examines financial ratios, analyzes changes in capital structure over three years, and assesses shareholder wealth maximization, providing recommendations for improvement. The report uses various financial tools and techniques to assess the financial health of the companies.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.