Financial Statement Analysis and Project Evaluation Report

VerifiedAdded on 2023/06/10

|12

|862

|454

Report

AI Summary

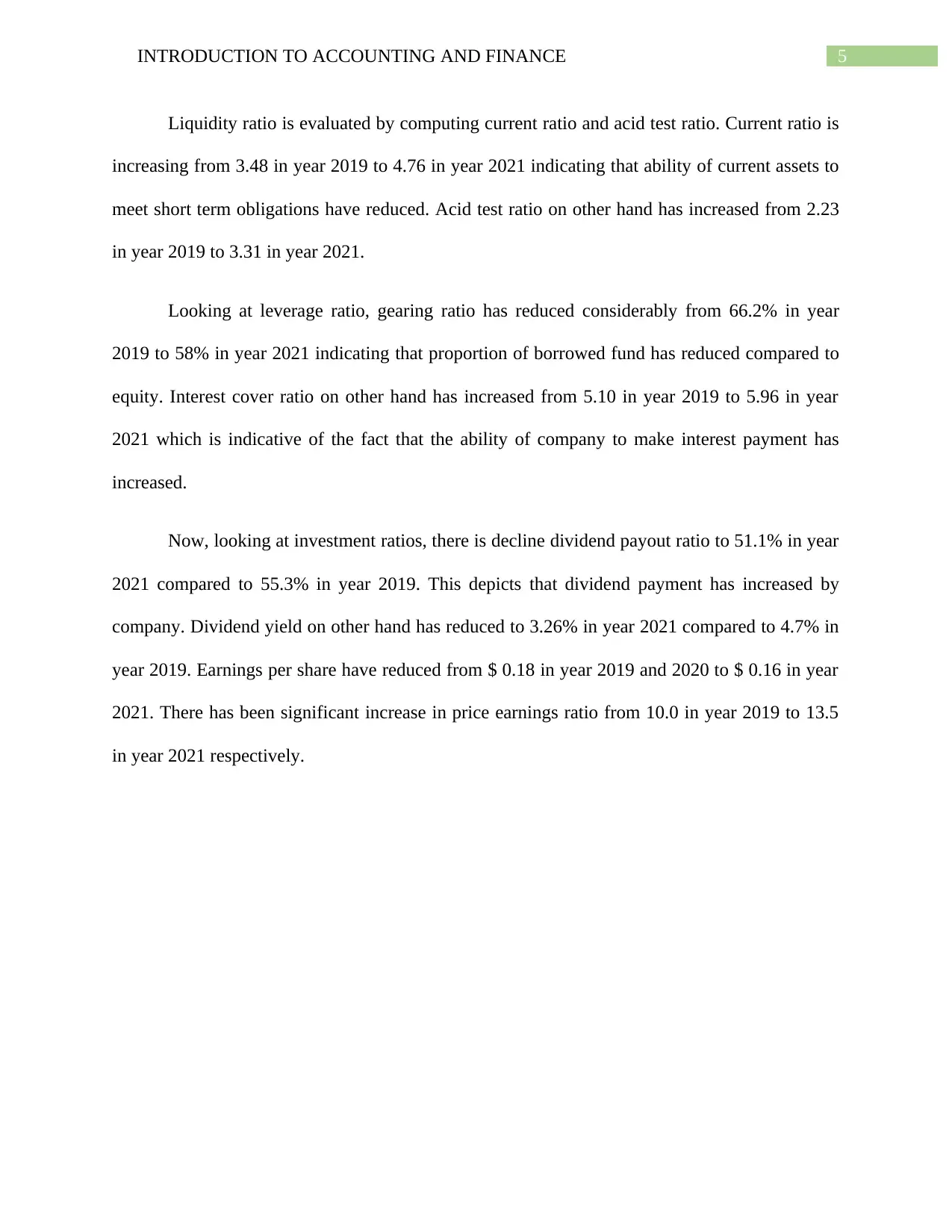

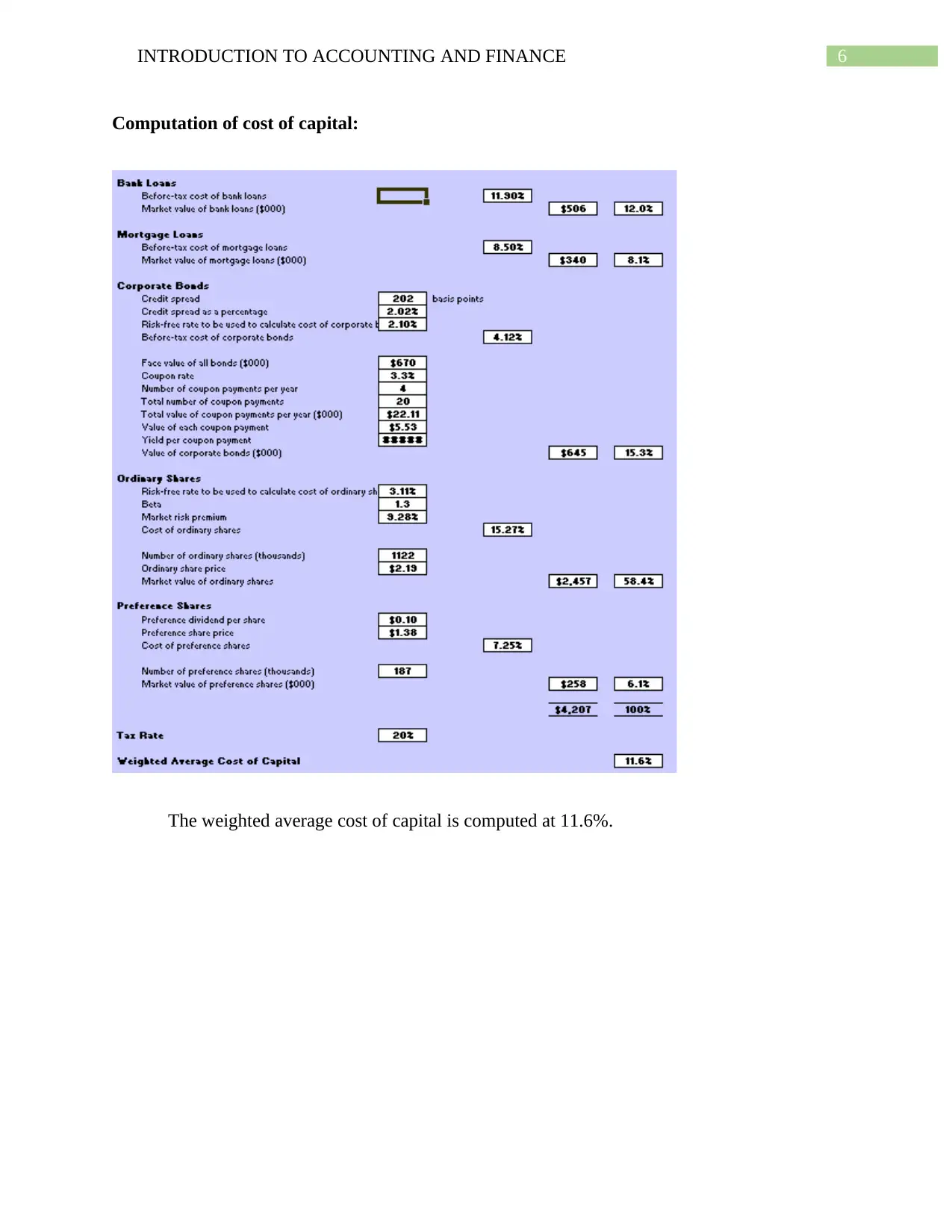

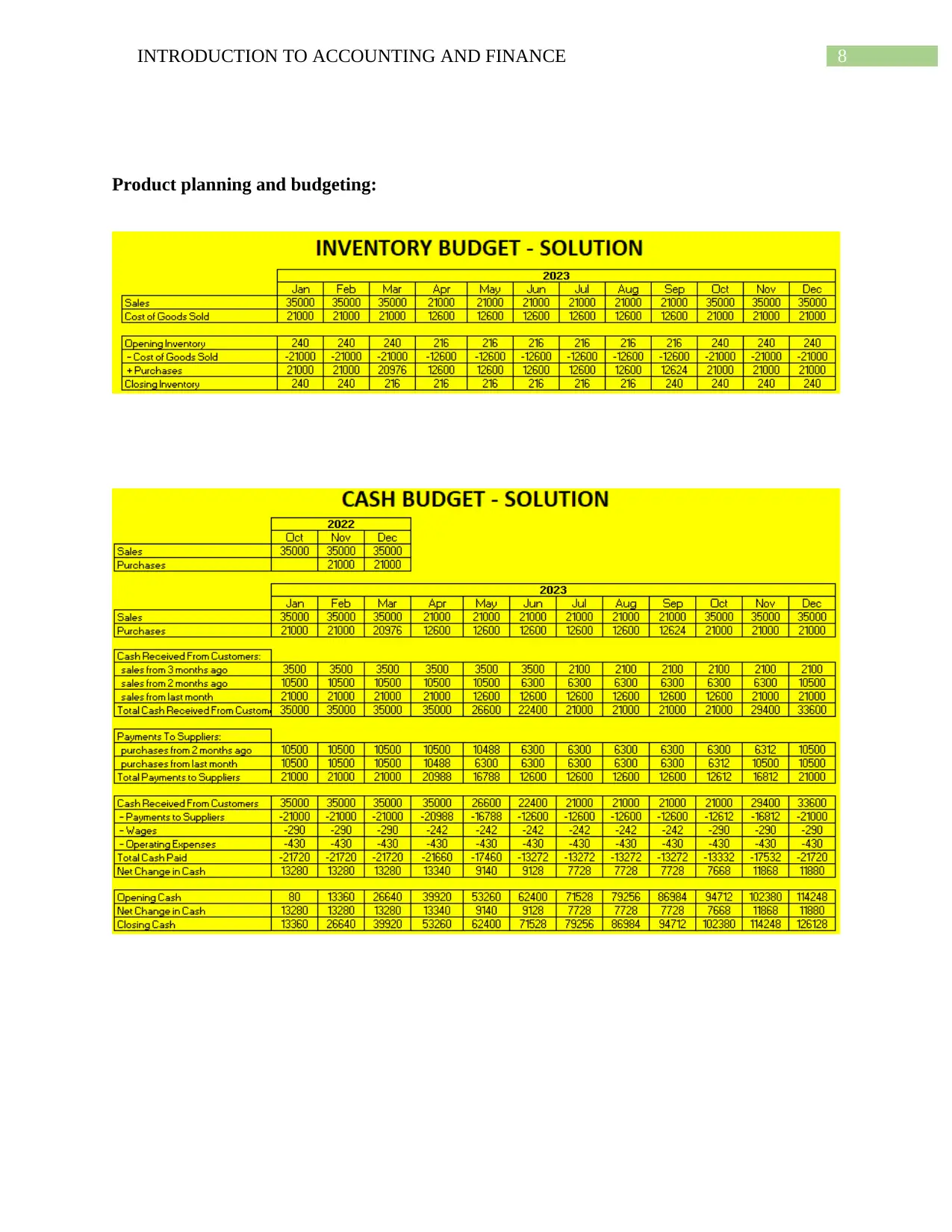

This report provides a comprehensive analysis of the financial statements of Track Lock Stones Ltd, evaluating profitability, efficiency, liquidity, leverage, and investment ratios. It computes the weighted average cost of capital and evaluates a project using capital budgeting tools, including the net present value. The report also covers product planning and budgeting, including break-even analysis. Based on the financial analysis, the report offers recommendations to improve the company's financial performance, emphasizing the need to lower the weighted average cost of capital and improve profitability while maintaining efficiency. The analysis includes relevant financial ratios, calculations, and interpretations to support the recommendations and conclusions.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.