Financial Performance Analysis of Retail Firms Report

VerifiedAdded on 2020/02/05

|17

|4215

|74

Report

AI Summary

This report provides a comprehensive analysis of accounting and finance principles for managers, focusing on the financial performance of two major fashion retail firms, Next PLC and H&M. The report begins with an introduction to the importance of accounting and finance in business operations, followed by a detailed comparative analysis of the two companies' financial strengths using various financial and non-financial ratios. It examines liquidity, profitability, and efficiency ratios, presenting the data in charts and tables for clarity. The analysis includes an assessment of investment appraisal techniques and their limitations. The report also offers recommendations to improve the financial position of the companies based on the findings and concludes with a summary of the key insights. This report provides insights into practical applications of financial analysis, aiding in decision-making processes and offering a valuable resource for students studying accounting and finance.

ACCOUNTING AND FINANCE FOR

MANAGERS

MANAGERS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION 1 & 2. PERFORMANCE ANALYSIS USING CHARTS.........................................1

QUESTION 3. RECOMMENDATIONS TO IMPROVE THE FINANCIAL POSITION............8

QUESTION 4. LIMITATIONS OF RELYING ON FINANCIAL RATIOS.................................9

QUESTION 5. INVESTMENT APPRAISAL TECHNIQUES....................................................10

QUESTION 6. LIMITATIONS OF USING THE INVESTMENT APPRAISAL TECHNIQUES

........................................................................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

QUESTION 1 & 2. PERFORMANCE ANALYSIS USING CHARTS.........................................1

QUESTION 3. RECOMMENDATIONS TO IMPROVE THE FINANCIAL POSITION............8

QUESTION 4. LIMITATIONS OF RELYING ON FINANCIAL RATIOS.................................9

QUESTION 5. INVESTMENT APPRAISAL TECHNIQUES....................................................10

QUESTION 6. LIMITATIONS OF USING THE INVESTMENT APPRAISAL TECHNIQUES

........................................................................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Accounting and finance for managers lays a significant impact on the overall business

operations of a company. The organization operates its business on money, and if it fails to

manage and control its money, the company with no doubt loses its competitive position along

with the financial strength in the global business environment. In this regard, appropriate

accounting of the organization's income and expense is essential which helps to manage and

control the inflows and outflows of money thereby providing the organization with a strategic

direction to conduct its business operations. The present report analyzes the importance of

accounting and finance for the managers within an organization. Furthermore, it also examines

the link between theoretical knowledge as against practical applications. It helps to gain an

insight knowledge about different financial and non financial ratios along with the overall

financial interpretation of companies which helps in the decision making process.

QUESTION 1 & 2: PERFORMANCE ANALYSIS USING CHARTS

Comparative performance analysis of company's financial strength creates a tremendous

impact on the decision making process of the organization. It assists the investors along with the

employees and the management of the company to compare its overall competitive position in

the line of global business environment (Patra, 2006.). In the report, we have analyzed the

financial strength of two large fashion retail firms named Next Plc and H&M in order to analyze

its performance in the competitive market and to examine its investment appraisal techniques.

Comparative analysis of an organization is done by observing, examining, analysing and

finally interpreting the performance of some major financial and non financial ratios in the

following manner. In context with the present case file, company makes use of various financial

and non financial ratios to evaluate its business performance.

Financial ratios- These ratios are broadly segmented into the following categories-

Liquidity ratios- The organization makes use of this ratio to measure the short term credibility of

the firm. It serves the information of meeting the short term financial barriers by a company. The

two most commonly used liquidity ratios are-

1

Accounting and finance for managers lays a significant impact on the overall business

operations of a company. The organization operates its business on money, and if it fails to

manage and control its money, the company with no doubt loses its competitive position along

with the financial strength in the global business environment. In this regard, appropriate

accounting of the organization's income and expense is essential which helps to manage and

control the inflows and outflows of money thereby providing the organization with a strategic

direction to conduct its business operations. The present report analyzes the importance of

accounting and finance for the managers within an organization. Furthermore, it also examines

the link between theoretical knowledge as against practical applications. It helps to gain an

insight knowledge about different financial and non financial ratios along with the overall

financial interpretation of companies which helps in the decision making process.

QUESTION 1 & 2: PERFORMANCE ANALYSIS USING CHARTS

Comparative performance analysis of company's financial strength creates a tremendous

impact on the decision making process of the organization. It assists the investors along with the

employees and the management of the company to compare its overall competitive position in

the line of global business environment (Patra, 2006.). In the report, we have analyzed the

financial strength of two large fashion retail firms named Next Plc and H&M in order to analyze

its performance in the competitive market and to examine its investment appraisal techniques.

Comparative analysis of an organization is done by observing, examining, analysing and

finally interpreting the performance of some major financial and non financial ratios in the

following manner. In context with the present case file, company makes use of various financial

and non financial ratios to evaluate its business performance.

Financial ratios- These ratios are broadly segmented into the following categories-

Liquidity ratios- The organization makes use of this ratio to measure the short term credibility of

the firm. It serves the information of meeting the short term financial barriers by a company. The

two most commonly used liquidity ratios are-

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

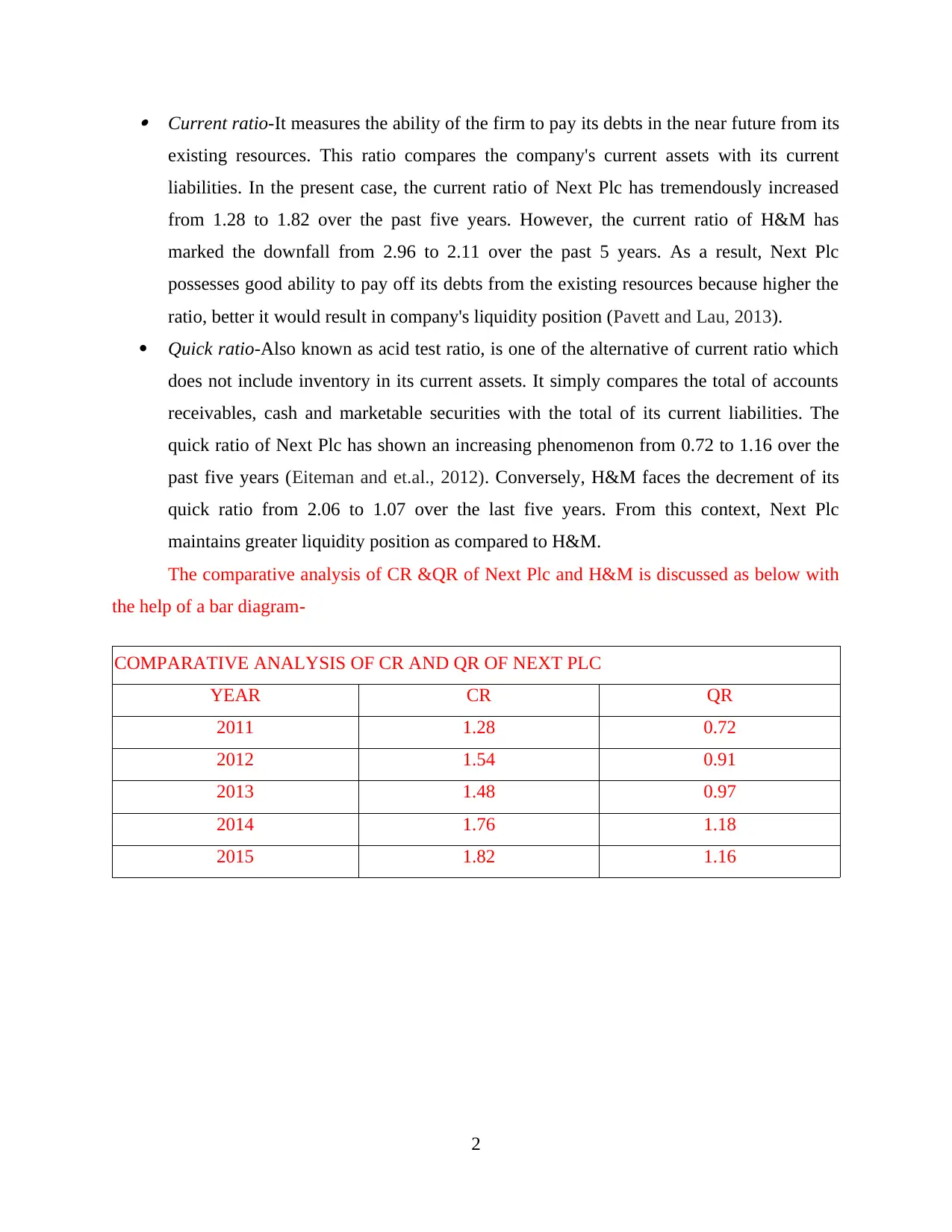

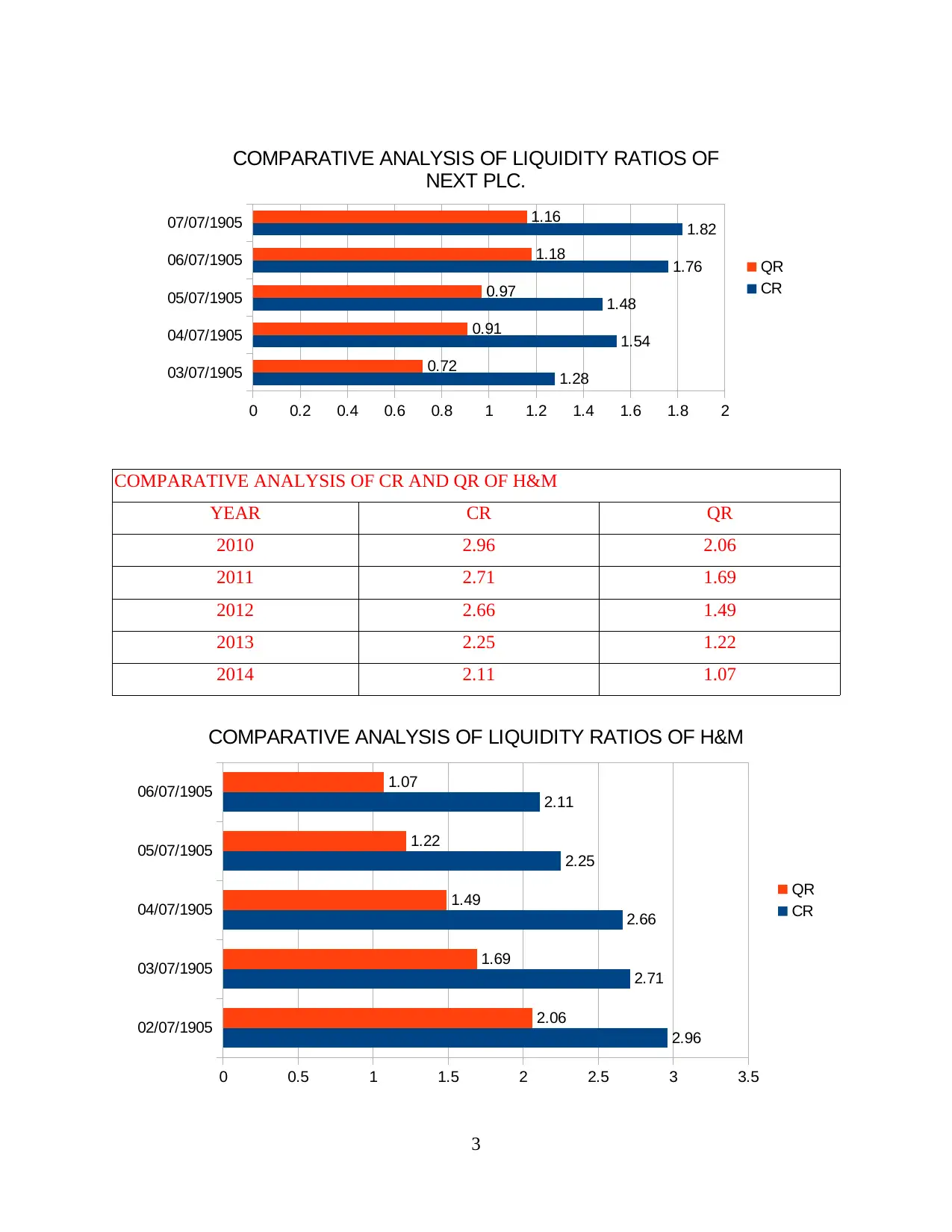

Current ratio-It measures the ability of the firm to pay its debts in the near future from its

existing resources. This ratio compares the company's current assets with its current

liabilities. In the present case, the current ratio of Next Plc has tremendously increased

from 1.28 to 1.82 over the past five years. However, the current ratio of H&M has

marked the downfall from 2.96 to 2.11 over the past 5 years. As a result, Next Plc

possesses good ability to pay off its debts from the existing resources because higher the

ratio, better it would result in company's liquidity position (Pavett and Lau, 2013).

Quick ratio-Also known as acid test ratio, is one of the alternative of current ratio which

does not include inventory in its current assets. It simply compares the total of accounts

receivables, cash and marketable securities with the total of its current liabilities. The

quick ratio of Next Plc has shown an increasing phenomenon from 0.72 to 1.16 over the

past five years (Eiteman and et.al., 2012). Conversely, H&M faces the decrement of its

quick ratio from 2.06 to 1.07 over the last five years. From this context, Next Plc

maintains greater liquidity position as compared to H&M.

The comparative analysis of CR &QR of Next Plc and H&M is discussed as below with

the help of a bar diagram-

COMPARATIVE ANALYSIS OF CR AND QR OF NEXT PLC

YEAR CR QR

2011 1.28 0.72

2012 1.54 0.91

2013 1.48 0.97

2014 1.76 1.18

2015 1.82 1.16

2

existing resources. This ratio compares the company's current assets with its current

liabilities. In the present case, the current ratio of Next Plc has tremendously increased

from 1.28 to 1.82 over the past five years. However, the current ratio of H&M has

marked the downfall from 2.96 to 2.11 over the past 5 years. As a result, Next Plc

possesses good ability to pay off its debts from the existing resources because higher the

ratio, better it would result in company's liquidity position (Pavett and Lau, 2013).

Quick ratio-Also known as acid test ratio, is one of the alternative of current ratio which

does not include inventory in its current assets. It simply compares the total of accounts

receivables, cash and marketable securities with the total of its current liabilities. The

quick ratio of Next Plc has shown an increasing phenomenon from 0.72 to 1.16 over the

past five years (Eiteman and et.al., 2012). Conversely, H&M faces the decrement of its

quick ratio from 2.06 to 1.07 over the last five years. From this context, Next Plc

maintains greater liquidity position as compared to H&M.

The comparative analysis of CR &QR of Next Plc and H&M is discussed as below with

the help of a bar diagram-

COMPARATIVE ANALYSIS OF CR AND QR OF NEXT PLC

YEAR CR QR

2011 1.28 0.72

2012 1.54 0.91

2013 1.48 0.97

2014 1.76 1.18

2015 1.82 1.16

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

COMPARATIVE ANALYSIS OF CR AND QR OF H&M

YEAR CR QR

2010 2.96 2.06

2011 2.71 1.69

2012 2.66 1.49

2013 2.25 1.22

2014 2.11 1.07

3

03/07/1905

04/07/1905

05/07/1905

06/07/1905

07/07/1905

0 0.2 0.4 0.6 0.8 1 1.2 1.4 1.6 1.8 2

1.28

1.54

1.48

1.76

1.82

0.72

0.91

0.97

1.18

1.16

COMPARATIVE ANALYSIS OF LIQUIDITY RATIOS OF

NEXT PLC.

QR

CR

02/07/1905

03/07/1905

04/07/1905

05/07/1905

06/07/1905

0 0.5 1 1.5 2 2.5 3 3.5

2.96

2.71

2.66

2.25

2.11

2.06

1.69

1.49

1.22

1.07

COMPARATIVE ANALYSIS OF LIQUIDITY RATIOS OF H&M

QR

CR

YEAR CR QR

2010 2.96 2.06

2011 2.71 1.69

2012 2.66 1.49

2013 2.25 1.22

2014 2.11 1.07

3

03/07/1905

04/07/1905

05/07/1905

06/07/1905

07/07/1905

0 0.2 0.4 0.6 0.8 1 1.2 1.4 1.6 1.8 2

1.28

1.54

1.48

1.76

1.82

0.72

0.91

0.97

1.18

1.16

COMPARATIVE ANALYSIS OF LIQUIDITY RATIOS OF

NEXT PLC.

QR

CR

02/07/1905

03/07/1905

04/07/1905

05/07/1905

06/07/1905

0 0.5 1 1.5 2 2.5 3 3.5

2.96

2.71

2.66

2.25

2.11

2.06

1.69

1.49

1.22

1.07

COMPARATIVE ANALYSIS OF LIQUIDITY RATIOS OF H&M

QR

CR

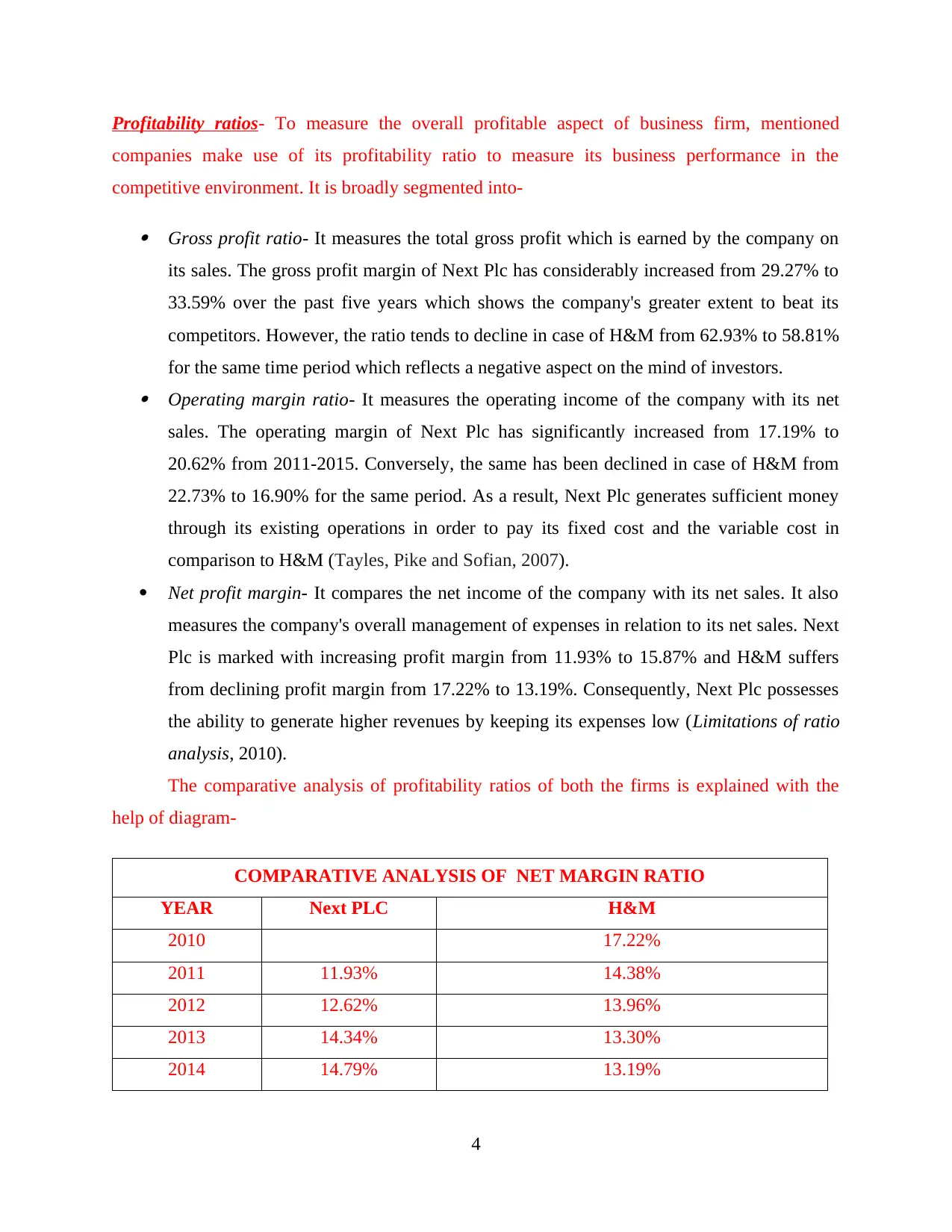

Profitability ratios- To measure the overall profitable aspect of business firm, mentioned

companies make use of its profitability ratio to measure its business performance in the

competitive environment. It is broadly segmented into-

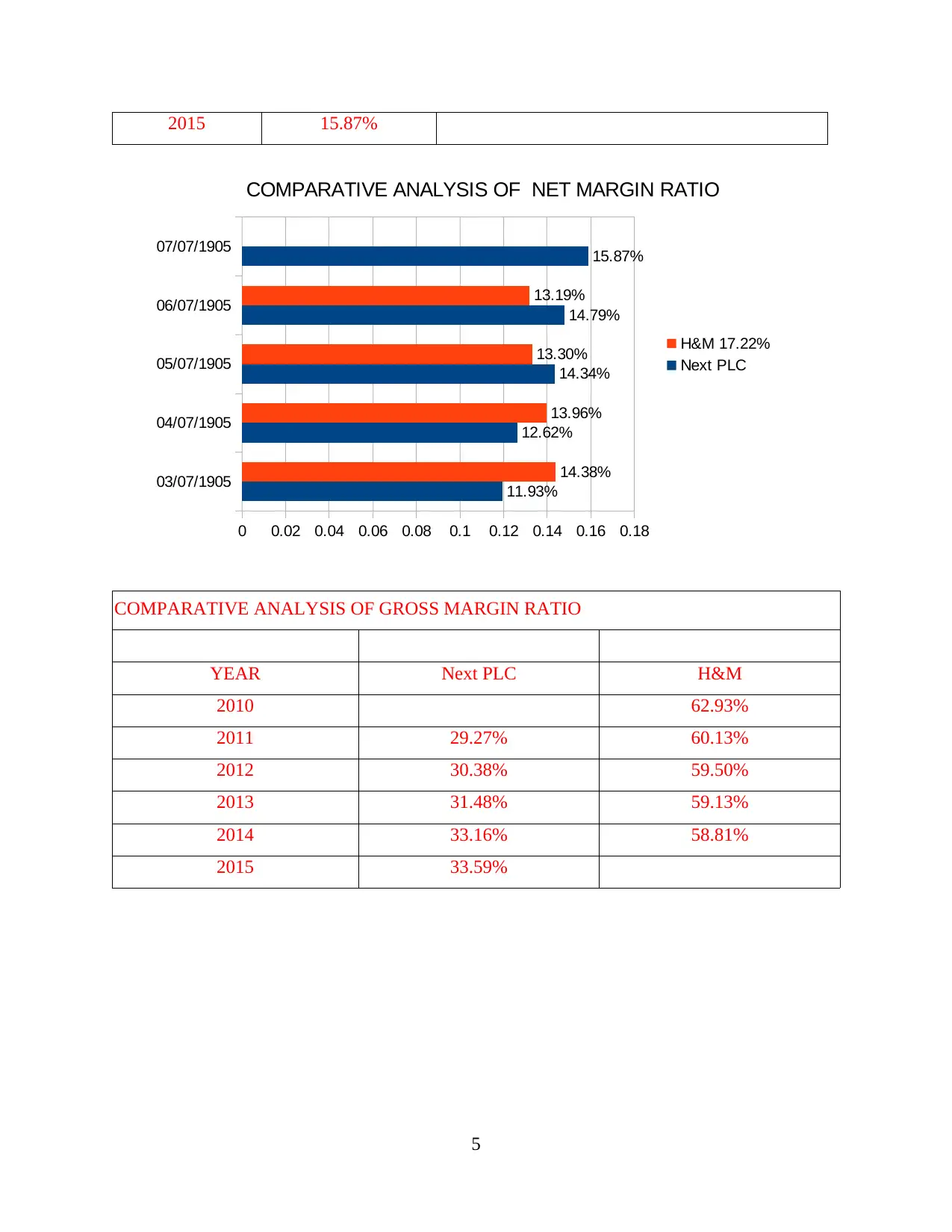

Gross profit ratio- It measures the total gross profit which is earned by the company on

its sales. The gross profit margin of Next Plc has considerably increased from 29.27% to

33.59% over the past five years which shows the company's greater extent to beat its

competitors. However, the ratio tends to decline in case of H&M from 62.93% to 58.81%

for the same time period which reflects a negative aspect on the mind of investors. Operating margin ratio- It measures the operating income of the company with its net

sales. The operating margin of Next Plc has significantly increased from 17.19% to

20.62% from 2011-2015. Conversely, the same has been declined in case of H&M from

22.73% to 16.90% for the same period. As a result, Next Plc generates sufficient money

through its existing operations in order to pay its fixed cost and the variable cost in

comparison to H&M (Tayles, Pike and Sofian, 2007).

Net profit margin- It compares the net income of the company with its net sales. It also

measures the company's overall management of expenses in relation to its net sales. Next

Plc is marked with increasing profit margin from 11.93% to 15.87% and H&M suffers

from declining profit margin from 17.22% to 13.19%. Consequently, Next Plc possesses

the ability to generate higher revenues by keeping its expenses low (Limitations of ratio

analysis, 2010).

The comparative analysis of profitability ratios of both the firms is explained with the

help of diagram-

COMPARATIVE ANALYSIS OF NET MARGIN RATIO

YEAR Next PLC H&M

2010 17.22%

2011 11.93% 14.38%

2012 12.62% 13.96%

2013 14.34% 13.30%

2014 14.79% 13.19%

4

companies make use of its profitability ratio to measure its business performance in the

competitive environment. It is broadly segmented into-

Gross profit ratio- It measures the total gross profit which is earned by the company on

its sales. The gross profit margin of Next Plc has considerably increased from 29.27% to

33.59% over the past five years which shows the company's greater extent to beat its

competitors. However, the ratio tends to decline in case of H&M from 62.93% to 58.81%

for the same time period which reflects a negative aspect on the mind of investors. Operating margin ratio- It measures the operating income of the company with its net

sales. The operating margin of Next Plc has significantly increased from 17.19% to

20.62% from 2011-2015. Conversely, the same has been declined in case of H&M from

22.73% to 16.90% for the same period. As a result, Next Plc generates sufficient money

through its existing operations in order to pay its fixed cost and the variable cost in

comparison to H&M (Tayles, Pike and Sofian, 2007).

Net profit margin- It compares the net income of the company with its net sales. It also

measures the company's overall management of expenses in relation to its net sales. Next

Plc is marked with increasing profit margin from 11.93% to 15.87% and H&M suffers

from declining profit margin from 17.22% to 13.19%. Consequently, Next Plc possesses

the ability to generate higher revenues by keeping its expenses low (Limitations of ratio

analysis, 2010).

The comparative analysis of profitability ratios of both the firms is explained with the

help of diagram-

COMPARATIVE ANALYSIS OF NET MARGIN RATIO

YEAR Next PLC H&M

2010 17.22%

2011 11.93% 14.38%

2012 12.62% 13.96%

2013 14.34% 13.30%

2014 14.79% 13.19%

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2015 15.87%

COMPARATIVE ANALYSIS OF GROSS MARGIN RATIO

YEAR Next PLC H&M

2010 62.93%

2011 29.27% 60.13%

2012 30.38% 59.50%

2013 31.48% 59.13%

2014 33.16% 58.81%

2015 33.59%

5

03/07/1905

04/07/1905

05/07/1905

06/07/1905

07/07/1905

0 0.02 0.04 0.06 0.08 0.1 0.12 0.14 0.16 0.18

11.93%

12.62%

14.34%

14.79%

15.87%

14.38%

13.96%

13.30%

13.19%

COMPARATIVE ANALYSIS OF NET MARGIN RATIO

H&M 17.22%

Next PLC

COMPARATIVE ANALYSIS OF GROSS MARGIN RATIO

YEAR Next PLC H&M

2010 62.93%

2011 29.27% 60.13%

2012 30.38% 59.50%

2013 31.48% 59.13%

2014 33.16% 58.81%

2015 33.59%

5

03/07/1905

04/07/1905

05/07/1905

06/07/1905

07/07/1905

0 0.02 0.04 0.06 0.08 0.1 0.12 0.14 0.16 0.18

11.93%

12.62%

14.34%

14.79%

15.87%

14.38%

13.96%

13.30%

13.19%

COMPARATIVE ANALYSIS OF NET MARGIN RATIO

H&M 17.22%

Next PLC

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Efficiency ratios- It analyzes the efficiency of the company in managing its internal assets and

liabilities in an effective manner. It is further categorised into-

Asset turnover ratio- It measures the company's net sales with its average total assets.

Higher the ratio, higher would be the efficiency of the company in managing its assets

and generating higher sales. In the present case, Next Plc generates a lower ratio of 1.89

in 2015 as compared to H&M (2.14). Inventory turnover ratio-It measures the effectiveness of the company in managing its

inventory with relation to the cost of goods sold. Next Plc has shown a minor fall in its

ratio from 6.89% to 6.62%. Along with it, H&M also shows the same magnitude of fall

from 3.70% to 3.46%. As a result, this shows that both the companies maintain a liquid

inventory (Roe, 2012).

Receivables turnover ratio- It measures the ability of the firm to quickly gain its accounts

receivables. It compares the net credit sales with the average account receivables. The

receivable turnover of Next Plc has declined from 6.14 to 5.45. However, the same ratio

has considerably increased from 32.92 to 33.12 in case of H&M. It shows that H&M is

collecting its receivables in an effective basis.

The comparative analysis of asset turnover ratios of both the firms is systematically

explained by using a bar chart-

6

03/07/1905

04/07/1905

05/07/1905

06/07/1905

07/07/1905

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7

29.27%

30.38%

31.48%

33.16%

33.59%

60.13%

59.50%

59.13%

58.81%

COMPARATIVE ANALYSIS OF GROSS MARGIN

RATIO

H&M 62.93%

Next PLC

Y Axis Title

liabilities in an effective manner. It is further categorised into-

Asset turnover ratio- It measures the company's net sales with its average total assets.

Higher the ratio, higher would be the efficiency of the company in managing its assets

and generating higher sales. In the present case, Next Plc generates a lower ratio of 1.89

in 2015 as compared to H&M (2.14). Inventory turnover ratio-It measures the effectiveness of the company in managing its

inventory with relation to the cost of goods sold. Next Plc has shown a minor fall in its

ratio from 6.89% to 6.62%. Along with it, H&M also shows the same magnitude of fall

from 3.70% to 3.46%. As a result, this shows that both the companies maintain a liquid

inventory (Roe, 2012).

Receivables turnover ratio- It measures the ability of the firm to quickly gain its accounts

receivables. It compares the net credit sales with the average account receivables. The

receivable turnover of Next Plc has declined from 6.14 to 5.45. However, the same ratio

has considerably increased from 32.92 to 33.12 in case of H&M. It shows that H&M is

collecting its receivables in an effective basis.

The comparative analysis of asset turnover ratios of both the firms is systematically

explained by using a bar chart-

6

03/07/1905

04/07/1905

05/07/1905

06/07/1905

07/07/1905

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7

29.27%

30.38%

31.48%

33.16%

33.59%

60.13%

59.50%

59.13%

58.81%

COMPARATIVE ANALYSIS OF GROSS MARGIN

RATIO

H&M 62.93%

Next PLC

Y Axis Title

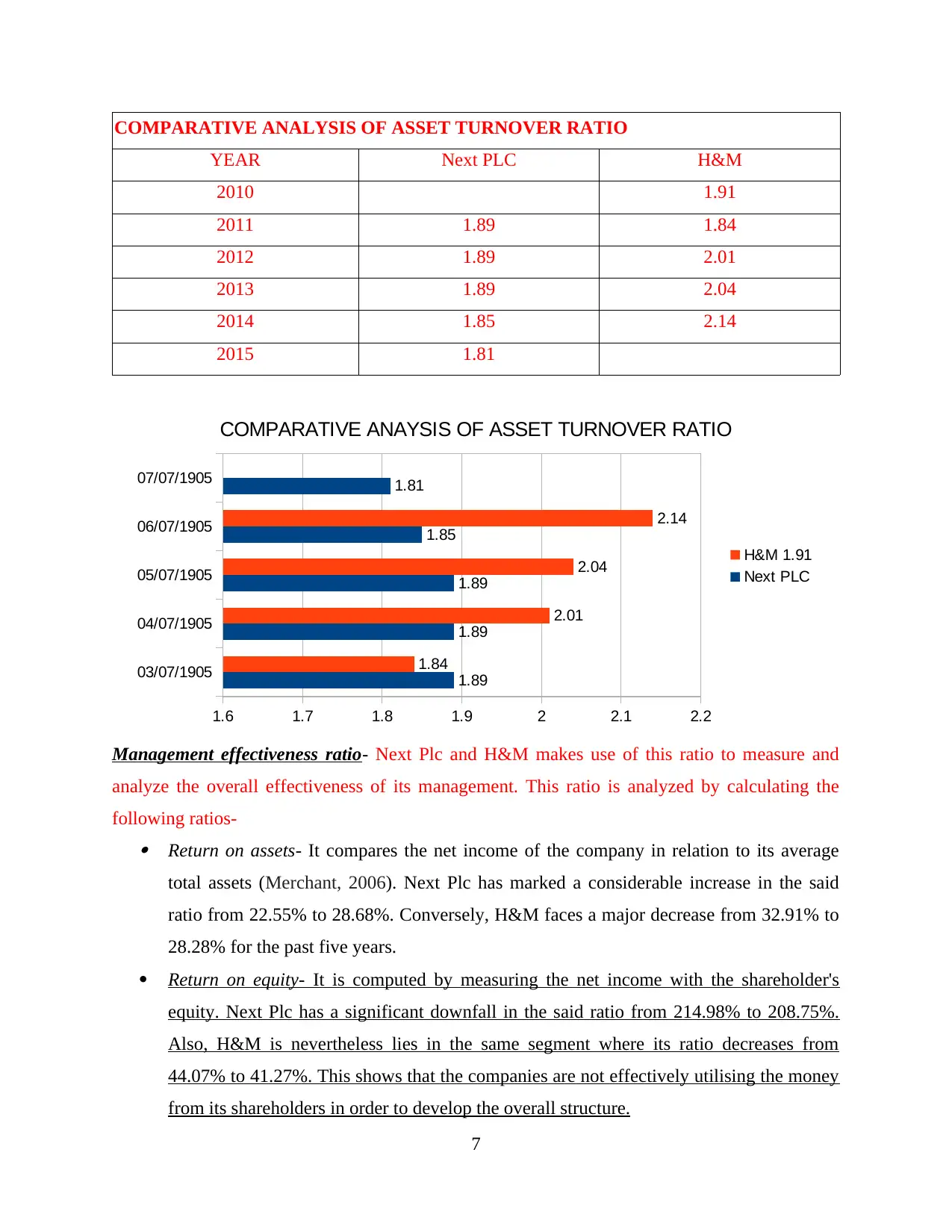

COMPARATIVE ANALYSIS OF ASSET TURNOVER RATIO

YEAR Next PLC H&M

2010 1.91

2011 1.89 1.84

2012 1.89 2.01

2013 1.89 2.04

2014 1.85 2.14

2015 1.81

Management effectiveness ratio- Next Plc and H&M makes use of this ratio to measure and

analyze the overall effectiveness of its management. This ratio is analyzed by calculating the

following ratios- Return on assets- It compares the net income of the company in relation to its average

total assets (Merchant, 2006). Next Plc has marked a considerable increase in the said

ratio from 22.55% to 28.68%. Conversely, H&M faces a major decrease from 32.91% to

28.28% for the past five years.

Return on equity- It is computed by measuring the net income with the shareholder's

equity. Next Plc has a significant downfall in the said ratio from 214.98% to 208.75%.

Also, H&M is nevertheless lies in the same segment where its ratio decreases from

44.07% to 41.27%. This shows that the companies are not effectively utilising the money

from its shareholders in order to develop the overall structure.

7

03/07/1905

04/07/1905

05/07/1905

06/07/1905

07/07/1905

1.6 1.7 1.8 1.9 2 2.1 2.2

1.89

1.89

1.89

1.85

1.81

1.84

2.01

2.04

2.14

COMPARATIVE ANAYSIS OF ASSET TURNOVER RATIO

H&M 1.91

Next PLC

YEAR Next PLC H&M

2010 1.91

2011 1.89 1.84

2012 1.89 2.01

2013 1.89 2.04

2014 1.85 2.14

2015 1.81

Management effectiveness ratio- Next Plc and H&M makes use of this ratio to measure and

analyze the overall effectiveness of its management. This ratio is analyzed by calculating the

following ratios- Return on assets- It compares the net income of the company in relation to its average

total assets (Merchant, 2006). Next Plc has marked a considerable increase in the said

ratio from 22.55% to 28.68%. Conversely, H&M faces a major decrease from 32.91% to

28.28% for the past five years.

Return on equity- It is computed by measuring the net income with the shareholder's

equity. Next Plc has a significant downfall in the said ratio from 214.98% to 208.75%.

Also, H&M is nevertheless lies in the same segment where its ratio decreases from

44.07% to 41.27%. This shows that the companies are not effectively utilising the money

from its shareholders in order to develop the overall structure.

7

03/07/1905

04/07/1905

05/07/1905

06/07/1905

07/07/1905

1.6 1.7 1.8 1.9 2 2.1 2.2

1.89

1.89

1.89

1.85

1.81

1.84

2.01

2.04

2.14

COMPARATIVE ANAYSIS OF ASSET TURNOVER RATIO

H&M 1.91

Next PLC

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

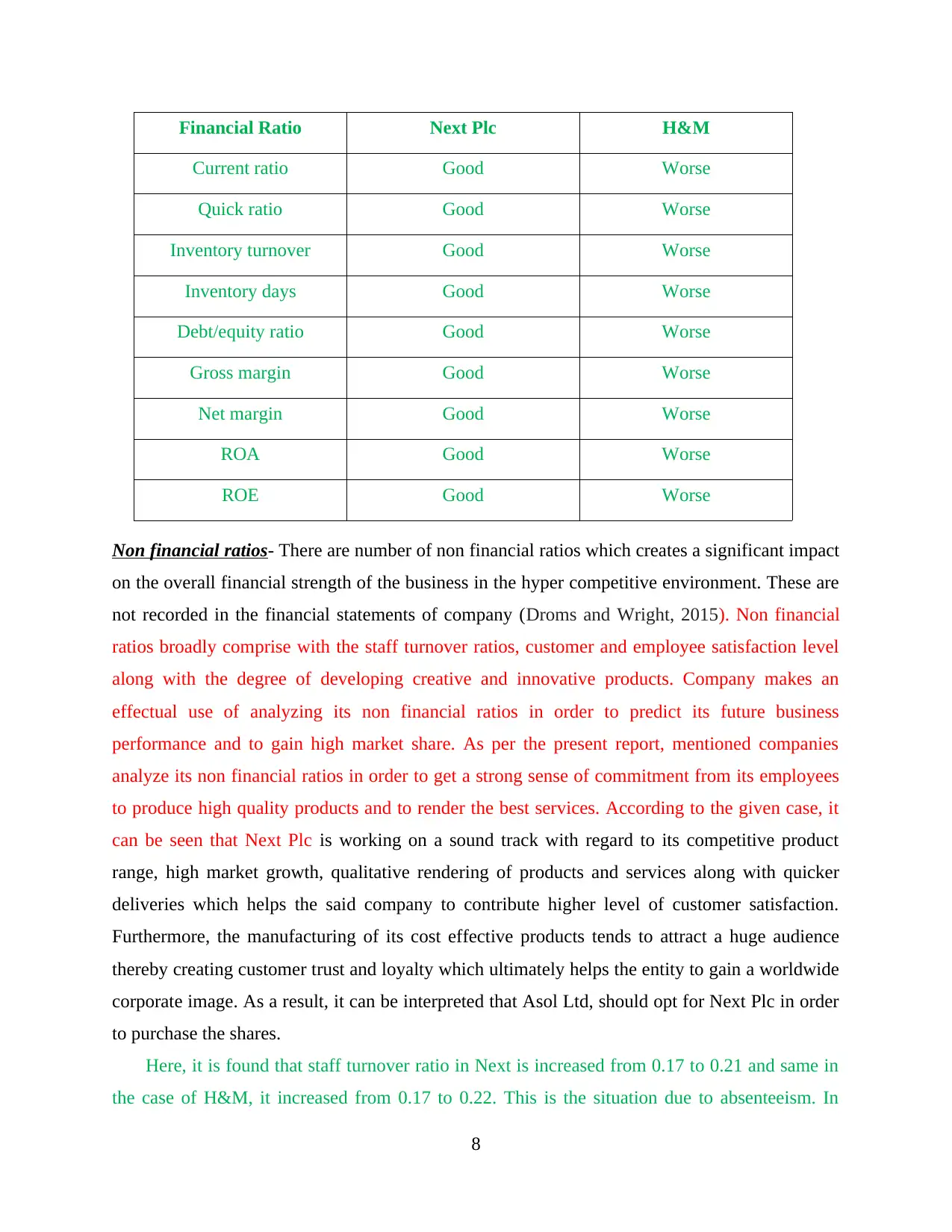

Financial Ratio Next Plc H&M

Current ratio Good Worse

Quick ratio Good Worse

Inventory turnover Good Worse

Inventory days Good Worse

Debt/equity ratio Good Worse

Gross margin Good Worse

Net margin Good Worse

ROA Good Worse

ROE Good Worse

Non financial ratios- There are number of non financial ratios which creates a significant impact

on the overall financial strength of the business in the hyper competitive environment. These are

not recorded in the financial statements of company (Droms and Wright, 2015). Non financial

ratios broadly comprise with the staff turnover ratios, customer and employee satisfaction level

along with the degree of developing creative and innovative products. Company makes an

effectual use of analyzing its non financial ratios in order to predict its future business

performance and to gain high market share. As per the present report, mentioned companies

analyze its non financial ratios in order to get a strong sense of commitment from its employees

to produce high quality products and to render the best services. According to the given case, it

can be seen that Next Plc is working on a sound track with regard to its competitive product

range, high market growth, qualitative rendering of products and services along with quicker

deliveries which helps the said company to contribute higher level of customer satisfaction.

Furthermore, the manufacturing of its cost effective products tends to attract a huge audience

thereby creating customer trust and loyalty which ultimately helps the entity to gain a worldwide

corporate image. As a result, it can be interpreted that Asol Ltd, should opt for Next Plc in order

to purchase the shares.

Here, it is found that staff turnover ratio in Next is increased from 0.17 to 0.21 and same in

the case of H&M, it increased from 0.17 to 0.22. This is the situation due to absenteeism. In

8

Current ratio Good Worse

Quick ratio Good Worse

Inventory turnover Good Worse

Inventory days Good Worse

Debt/equity ratio Good Worse

Gross margin Good Worse

Net margin Good Worse

ROA Good Worse

ROE Good Worse

Non financial ratios- There are number of non financial ratios which creates a significant impact

on the overall financial strength of the business in the hyper competitive environment. These are

not recorded in the financial statements of company (Droms and Wright, 2015). Non financial

ratios broadly comprise with the staff turnover ratios, customer and employee satisfaction level

along with the degree of developing creative and innovative products. Company makes an

effectual use of analyzing its non financial ratios in order to predict its future business

performance and to gain high market share. As per the present report, mentioned companies

analyze its non financial ratios in order to get a strong sense of commitment from its employees

to produce high quality products and to render the best services. According to the given case, it

can be seen that Next Plc is working on a sound track with regard to its competitive product

range, high market growth, qualitative rendering of products and services along with quicker

deliveries which helps the said company to contribute higher level of customer satisfaction.

Furthermore, the manufacturing of its cost effective products tends to attract a huge audience

thereby creating customer trust and loyalty which ultimately helps the entity to gain a worldwide

corporate image. As a result, it can be interpreted that Asol Ltd, should opt for Next Plc in order

to purchase the shares.

Here, it is found that staff turnover ratio in Next is increased from 0.17 to 0.21 and same in

the case of H&M, it increased from 0.17 to 0.22. This is the situation due to absenteeism. In

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Next, absenteeism has risen to 9855 from 7300 and in H&M it is 12045 from 8030. Based on

these states, it can state that Next is operating in effectual manner as compared to H&M.

QUESTION 3: RECOMMENDATIONS TO IMPROVE THE FINANCIAL

POSITION

In context with the above financial analysis of Next Plc and H&M, it can be seen that the

overall financial position of Next plc is far better than H&M. H&M needs to focus its main

attention to increase its sales which in turn leads to increase in revenue thereby tuning an

increment in its overall profit margin. Significant recommendations in order to improve the

overall financial position of H&M and Next PLC are discussed as below-

Company should emphasize on its criteria to first recover the outstanding debts. Before

making a sale, the company should make sure that it maintains the sale agreement in

writing in order to ensure the time period in which its debtors settle the debts.

The said company should start to analyze the expenses which it incurs in the course of

manufacturing and production. It should implement major cost effective techniques in its

plan of action. Along with it, H&M should also focus to switch to cheaper alternatives

for production process. For larger expenses, the company should arrange a deferred

payment plan. Further, it should manage and control its expenses and try to get it

minimized (Healy and Palepu, 2013).

Leasing its main assets or selling the unwanted assets also serve as one of the

recommendation which helps the cited company to minimize its storage cost and helps to

generate maximum cash flows.

Company should introduce new marketing techniques to attract a huge crowd of

audience, which as a result helps the company to attain a worldwide exposure leading to

increased sales and revenue.

QUESTION 4: LIMITATIONS OF RELYING ON FINANCIAL RATIOS.

Financial ratios serve as one of the major tools which help the firm to analyze its

financial performance. However, relying on the same is not a good thought to analyze the overall

financial position of the company in the global environment. The major reasons of not relying

only on the financial ratios are discussed below-

9

these states, it can state that Next is operating in effectual manner as compared to H&M.

QUESTION 3: RECOMMENDATIONS TO IMPROVE THE FINANCIAL

POSITION

In context with the above financial analysis of Next Plc and H&M, it can be seen that the

overall financial position of Next plc is far better than H&M. H&M needs to focus its main

attention to increase its sales which in turn leads to increase in revenue thereby tuning an

increment in its overall profit margin. Significant recommendations in order to improve the

overall financial position of H&M and Next PLC are discussed as below-

Company should emphasize on its criteria to first recover the outstanding debts. Before

making a sale, the company should make sure that it maintains the sale agreement in

writing in order to ensure the time period in which its debtors settle the debts.

The said company should start to analyze the expenses which it incurs in the course of

manufacturing and production. It should implement major cost effective techniques in its

plan of action. Along with it, H&M should also focus to switch to cheaper alternatives

for production process. For larger expenses, the company should arrange a deferred

payment plan. Further, it should manage and control its expenses and try to get it

minimized (Healy and Palepu, 2013).

Leasing its main assets or selling the unwanted assets also serve as one of the

recommendation which helps the cited company to minimize its storage cost and helps to

generate maximum cash flows.

Company should introduce new marketing techniques to attract a huge crowd of

audience, which as a result helps the company to attain a worldwide exposure leading to

increased sales and revenue.

QUESTION 4: LIMITATIONS OF RELYING ON FINANCIAL RATIOS.

Financial ratios serve as one of the major tools which help the firm to analyze its

financial performance. However, relying on the same is not a good thought to analyze the overall

financial position of the company in the global environment. The major reasons of not relying

only on the financial ratios are discussed below-

9

Ratios provide the information subject to the accounting assumption and standards

followed by the company. If the company tends to work on wrong principles, the

accounting ratios will provide information on the basis of such principles and concepts as

adopted by the organization, which is wrong (Warfield and Wild, 2015).

Analysing the ratios becomes preferable if the company adopts a narrow line of its

services and products. In case of complex and large companies, observing the ratios will

be more difficult. As a result, the company should focus its attention to analyze its

investment appraisal and other techniques to examine the overall position of the

company.

The problem related to inflation distorts the balance sheet and as a result such distortion

is then delivered to the ratios which create a negative impact on the entire performance of

the company.

Usually, it becomes difficult to analyze the financial strength of a company by simply

observing the ratios. This is because some ratios draw a perfect picture of the company

and some creates a negative impact. Consequent to this, it becomes difficult as to which

ratio to consider and which is not to be considered to analyze the company.

QUESTION 5: INVESTMENT APPRAISAL TECHNIQUES

Investment appraisal in a broader sense refers to the capital budgeting and planning

process which helps to determine whether the organization's long term investments are worth of

its capital structure (Myers, 2014). There are various techniques adopted by Hilltop in order to

identify its investment appraisal plan between project A and project B. Some major techniques

which help the company to identify the suitable projects are discussed below-

Net cash flows-

NCF can be identified by evaluating and examining all the cash related transactions

as against the non-cash related affairs. It will be eliminated from such calculation like

depreciation.

Table 1: NCF of project A (In £)

Year Profits Depreciation Cash inflows

through sales

Cash outflow

to purchase

Net Cash

inflow

10

followed by the company. If the company tends to work on wrong principles, the

accounting ratios will provide information on the basis of such principles and concepts as

adopted by the organization, which is wrong (Warfield and Wild, 2015).

Analysing the ratios becomes preferable if the company adopts a narrow line of its

services and products. In case of complex and large companies, observing the ratios will

be more difficult. As a result, the company should focus its attention to analyze its

investment appraisal and other techniques to examine the overall position of the

company.

The problem related to inflation distorts the balance sheet and as a result such distortion

is then delivered to the ratios which create a negative impact on the entire performance of

the company.

Usually, it becomes difficult to analyze the financial strength of a company by simply

observing the ratios. This is because some ratios draw a perfect picture of the company

and some creates a negative impact. Consequent to this, it becomes difficult as to which

ratio to consider and which is not to be considered to analyze the company.

QUESTION 5: INVESTMENT APPRAISAL TECHNIQUES

Investment appraisal in a broader sense refers to the capital budgeting and planning

process which helps to determine whether the organization's long term investments are worth of

its capital structure (Myers, 2014). There are various techniques adopted by Hilltop in order to

identify its investment appraisal plan between project A and project B. Some major techniques

which help the company to identify the suitable projects are discussed below-

Net cash flows-

NCF can be identified by evaluating and examining all the cash related transactions

as against the non-cash related affairs. It will be eliminated from such calculation like

depreciation.

Table 1: NCF of project A (In £)

Year Profits Depreciation Cash inflows

through sales

Cash outflow

to purchase

Net Cash

inflow

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.