Accounting and Finance Report: Financial Analysis of Three Companies

VerifiedAdded on 2023/01/04

|17

|3751

|35

Report

AI Summary

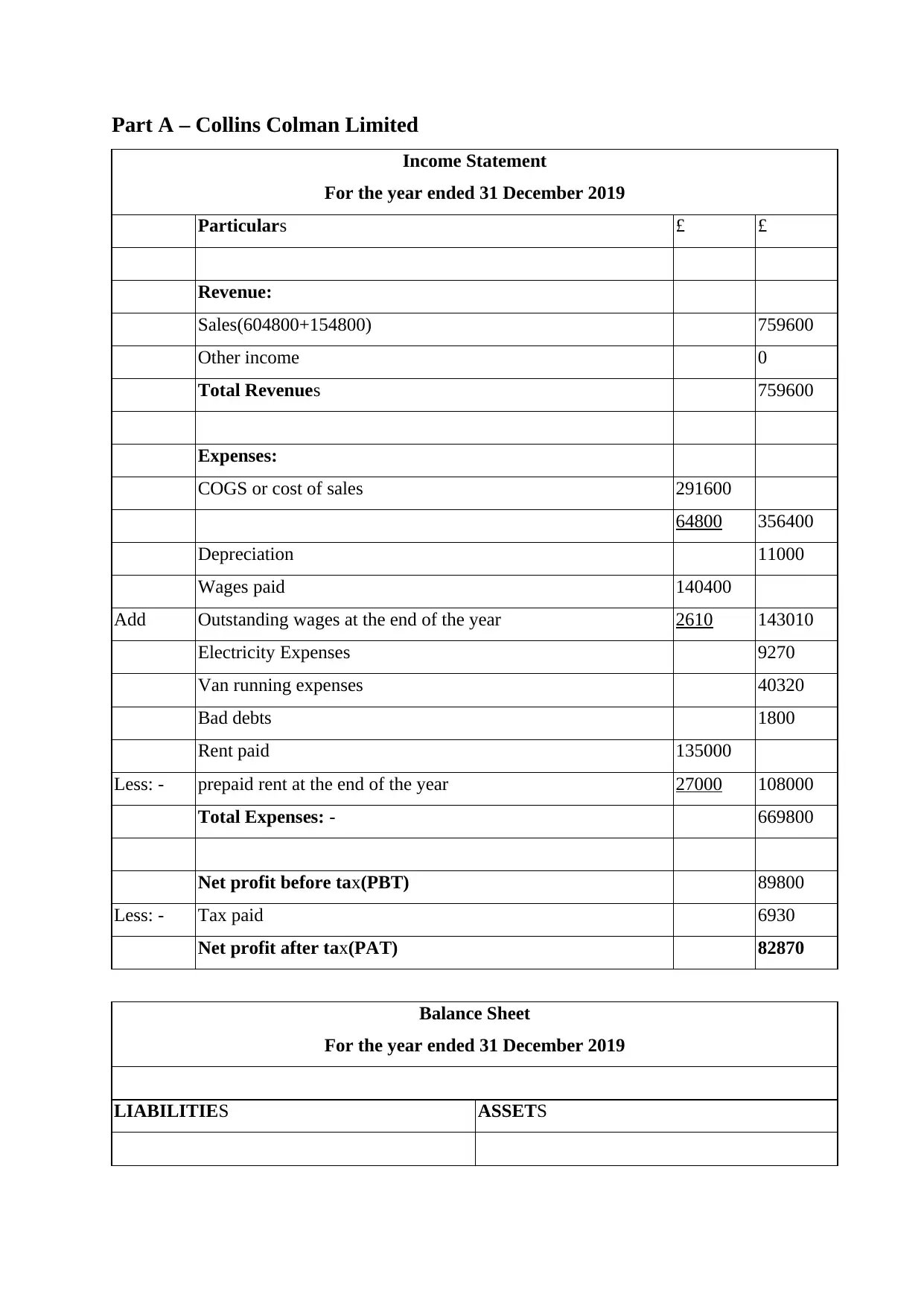

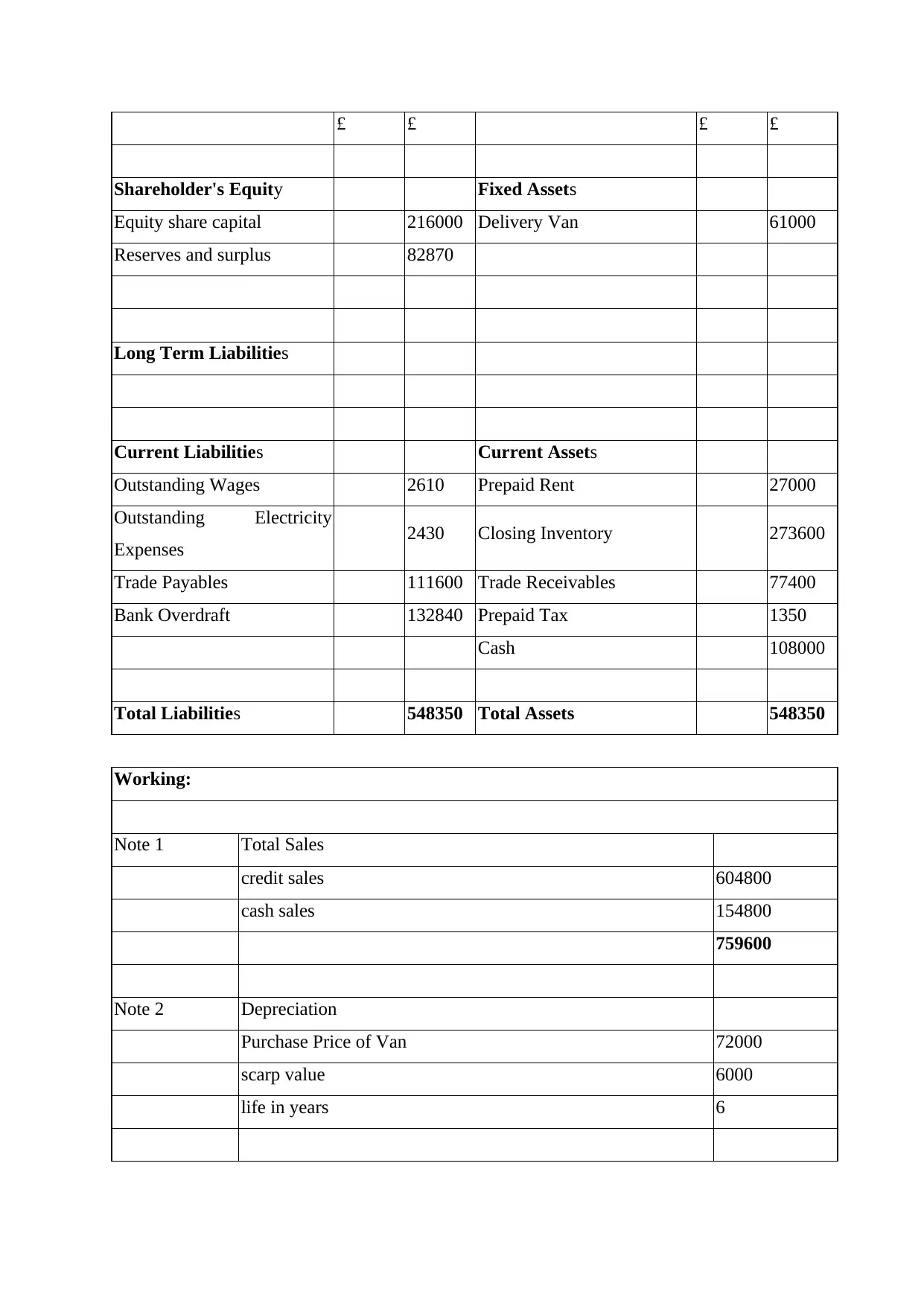

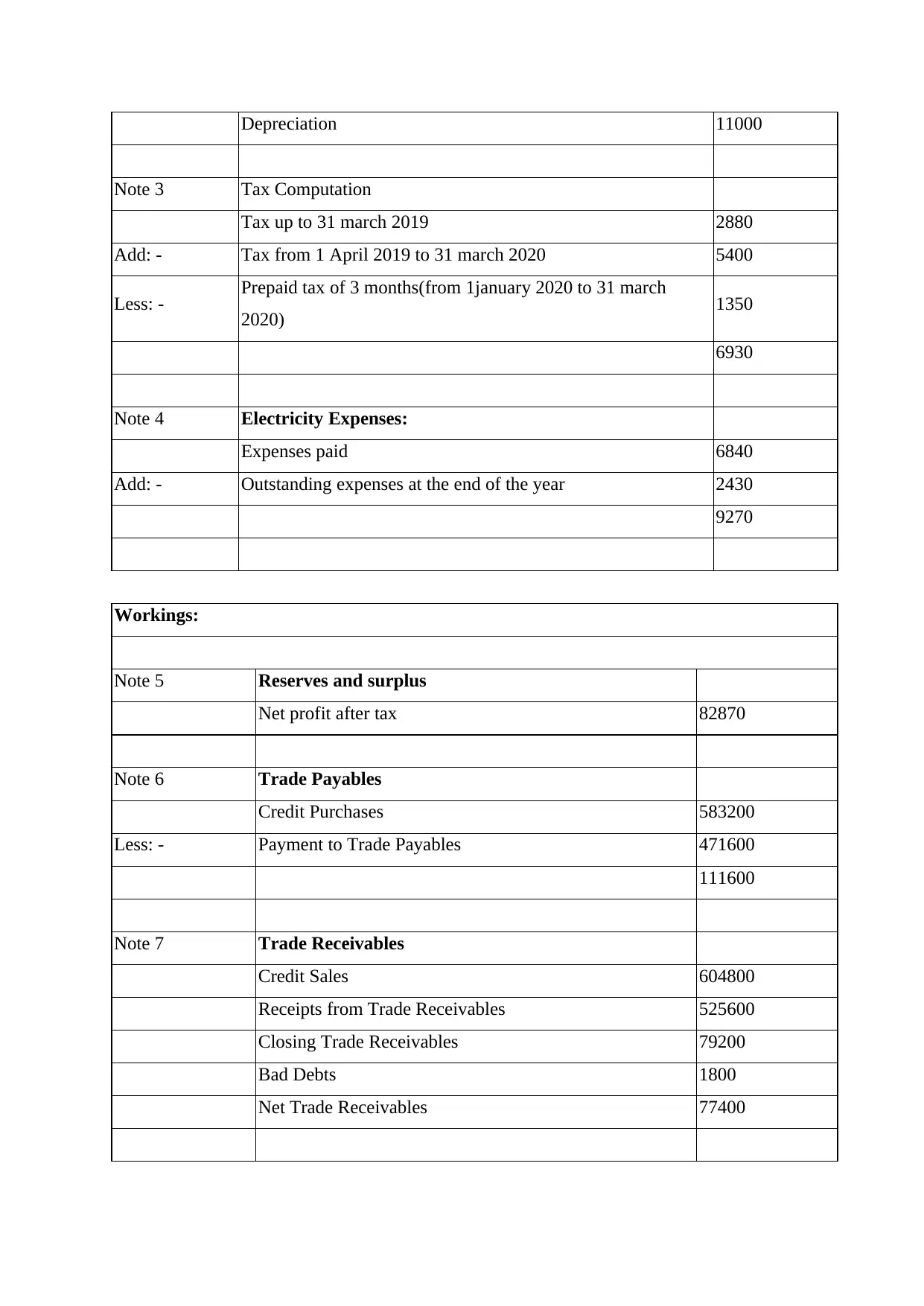

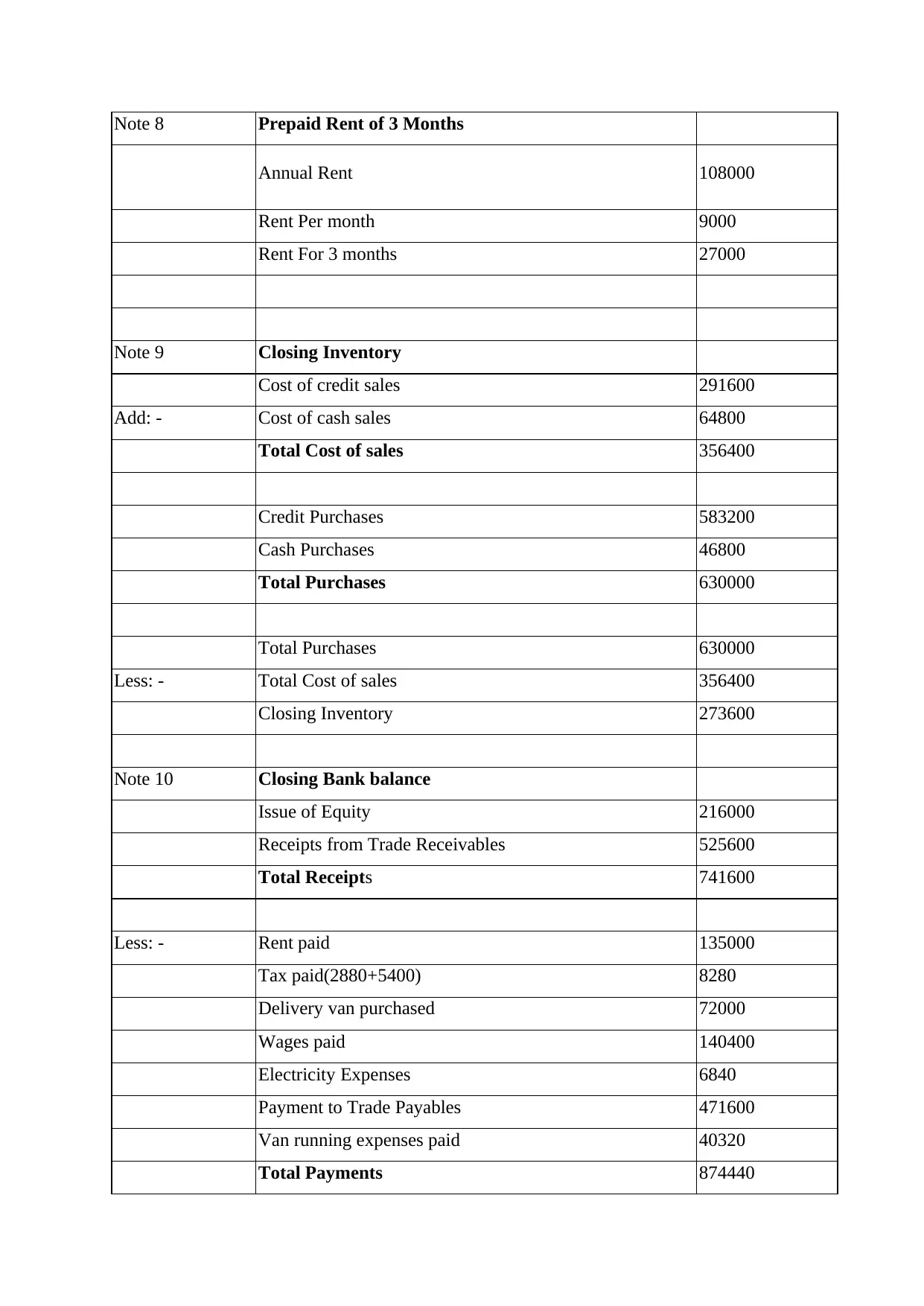

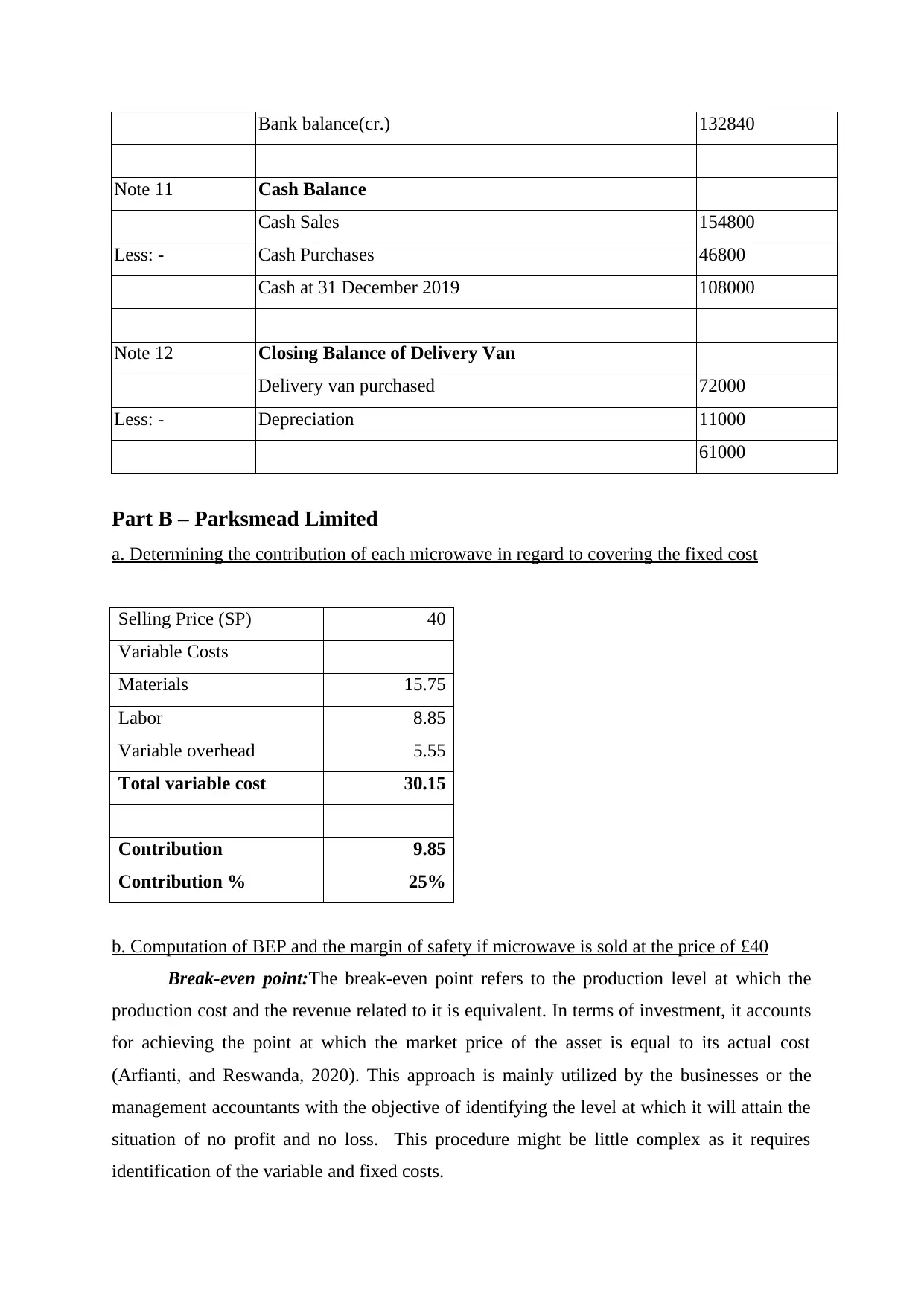

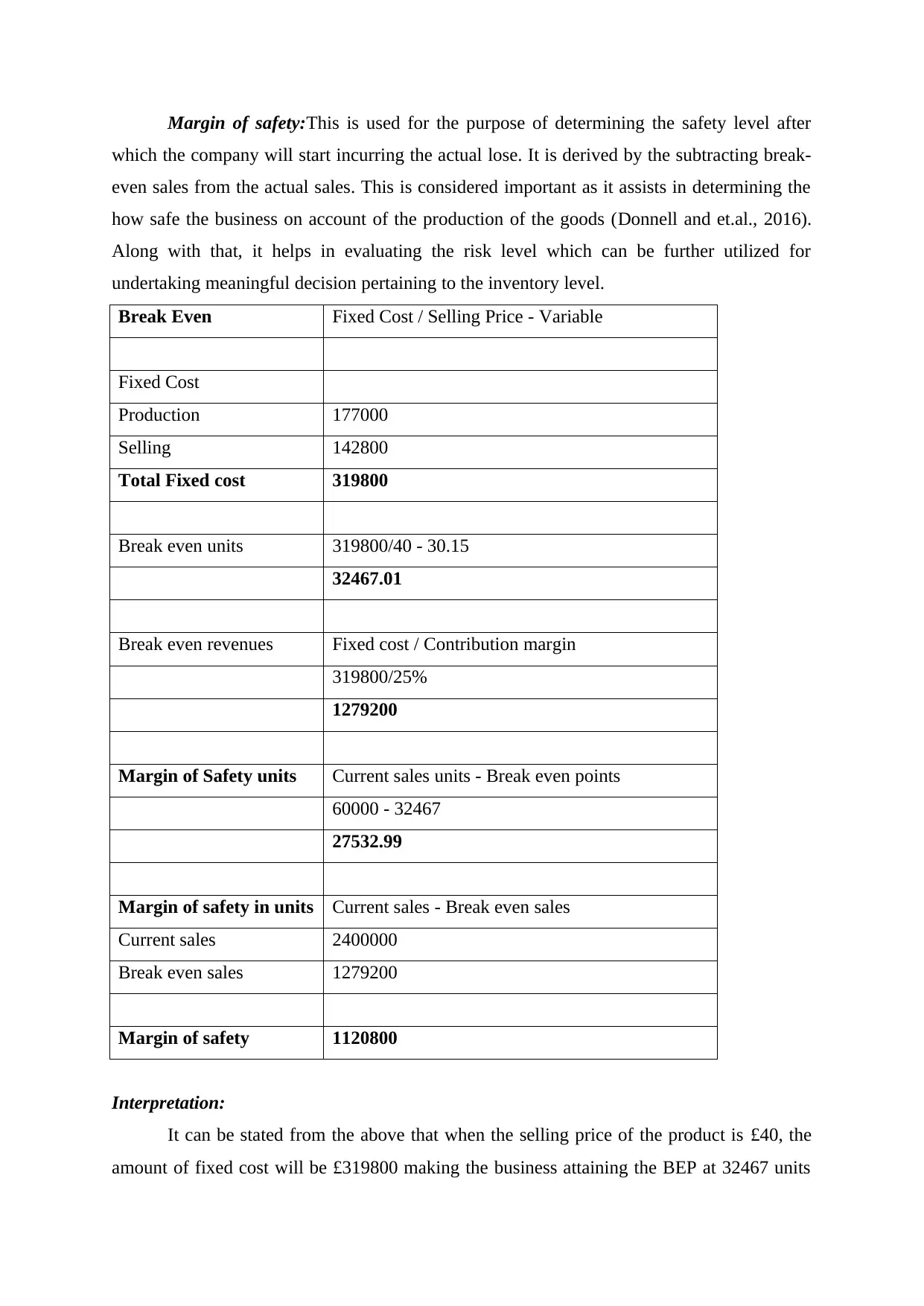

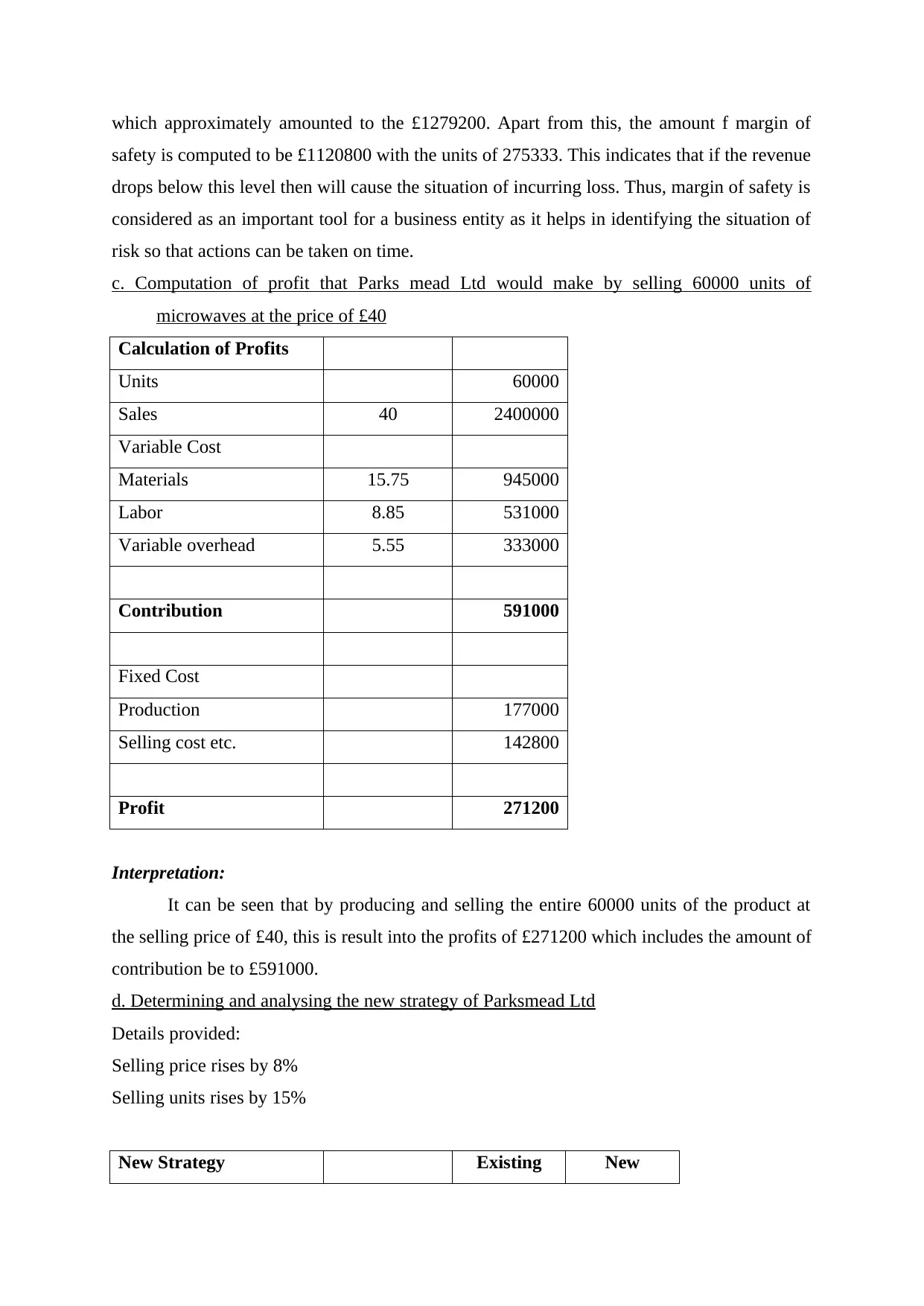

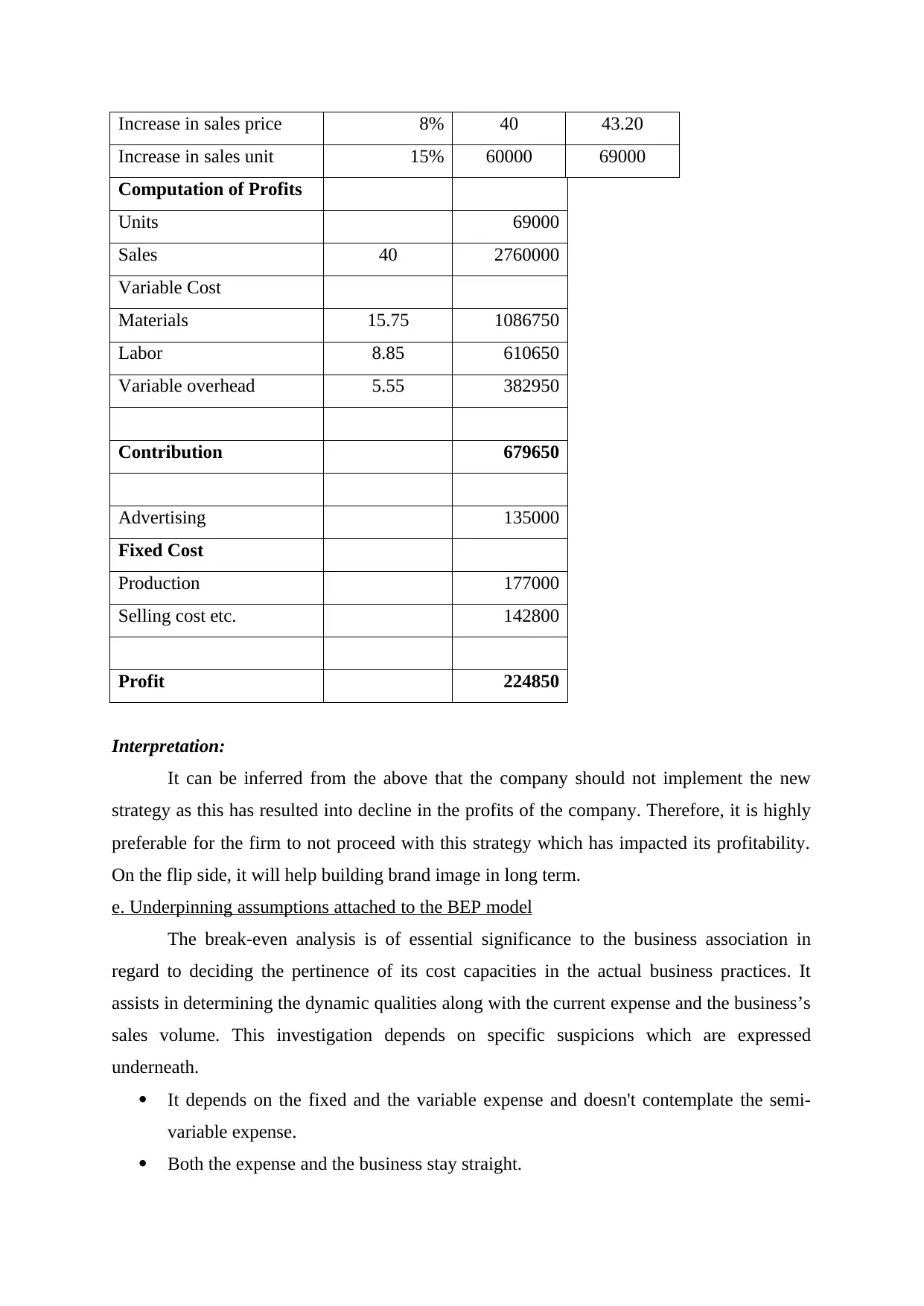

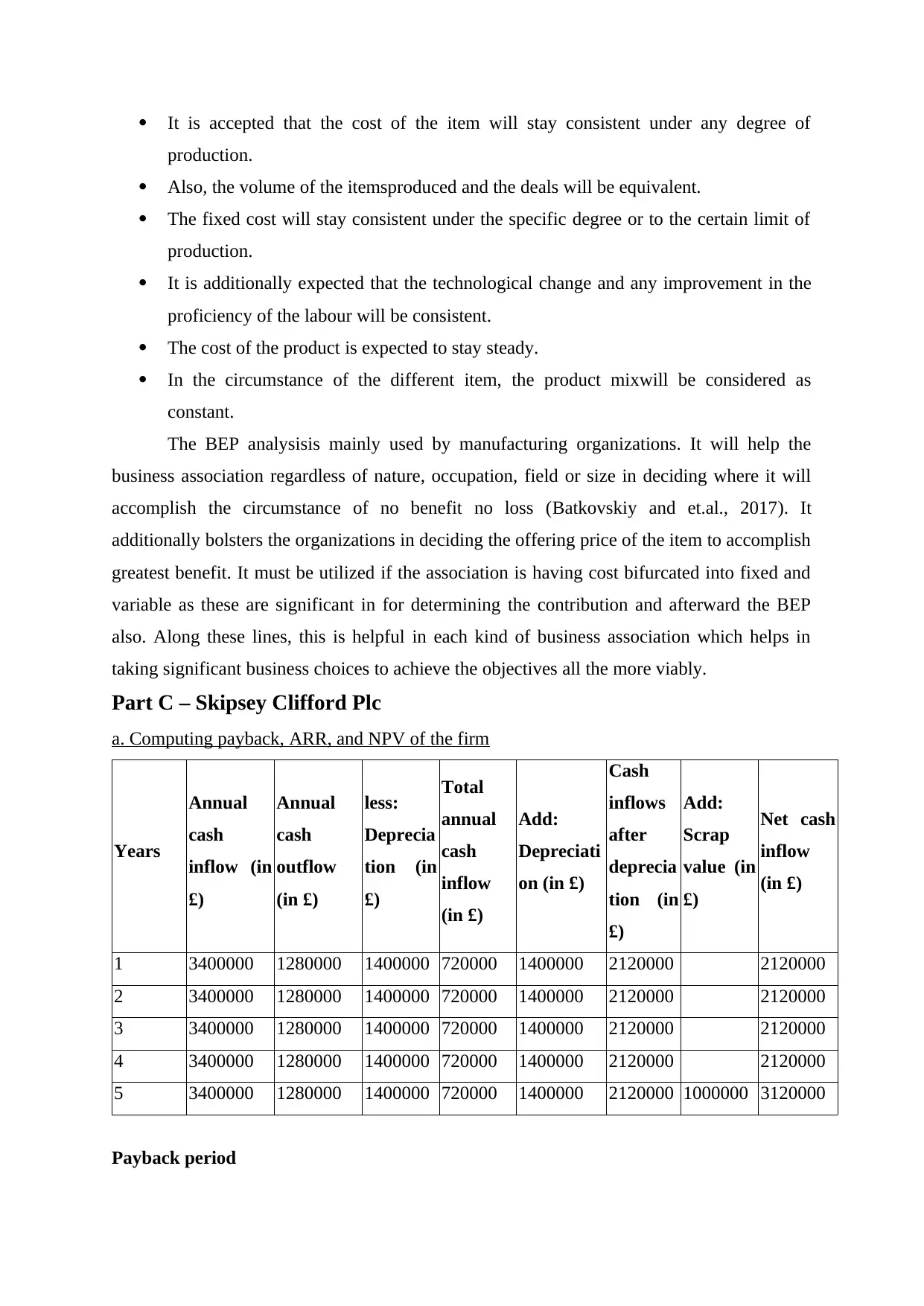

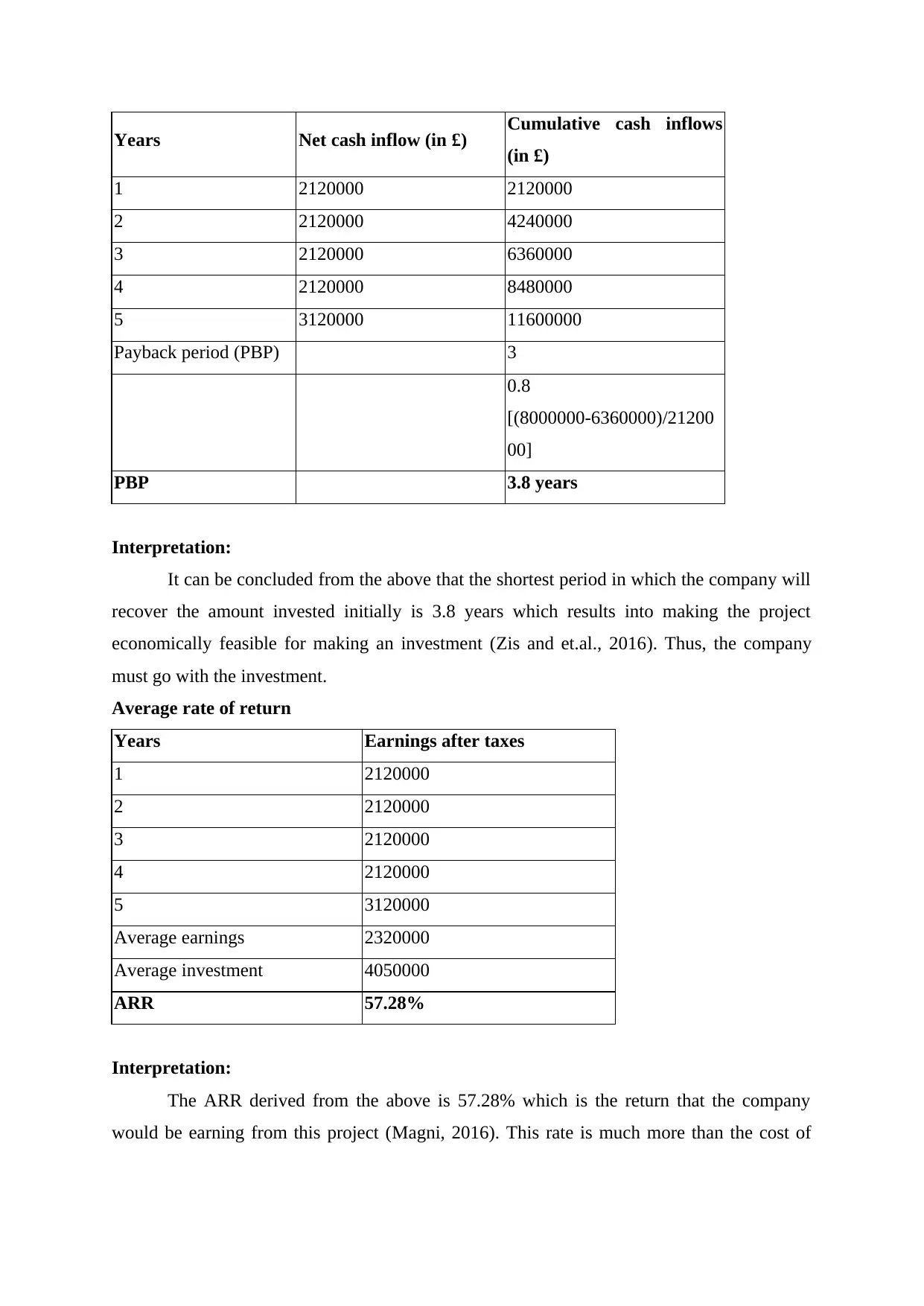

This report provides a comprehensive analysis of financial statements and investment appraisal techniques, focusing on three companies: Collins Colman Limited, Parksmead Limited, and Skipsey Clifford Plc. Part A examines Collins Colman's income statement and balance sheet for 2019, including detailed workings for key figures like sales, depreciation, and tax computation. Part B delves into Parksmead Limited, calculating the contribution margin, break-even point, margin of safety, and profitability analysis, and evaluating the impact of a new sales strategy. Part C analyzes Skipsey Clifford Plc, computing the payback period, accounting rate of return (ARR), and net present value (NPV) of a proposed project, along with a discussion of the merits and demerits of different investment appraisal techniques. The report offers a detailed breakdown of financial calculations and their interpretations, providing insights into financial performance and investment decision-making.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.