BUS5IAF - Accounting and Finance Business Simulation Report 2019

VerifiedAdded on 2023/04/25

|27

|5564

|267

Report

AI Summary

This report provides a comprehensive analysis of accounting and finance principles within a business simulation context. It explores appropriate sources of finance for a startup, including bank loans, venture capital, and angel investors, while discussing the risks associated with each. The report also examines financing options for future business expansion, such as partnerships, retained earnings, and franchising. Furthermore, it includes detailed financial statements, such as balance sheets, profit and loss statements, and cash flow statements, for Harish Enterprises Ltd, analyzing the company's financial performance and position. The document presents a consultant's perspective, offering insights and recommendations based on the financial data and strategic considerations. Desklib offers a wealth of similar documents and study resources for students.

Running head: INTRODUCTION TO ACCOUNTING AND FINANCE

Introduction to Accounting and Finance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Introduction to Accounting and Finance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1BUSINESS MANAGEMENT TECHNIQUES

Table of Contents

Part 1A:............................................................................................................................................2

Part 1B:............................................................................................................................................3

Part 2:...............................................................................................................................................5

Part 3:.............................................................................................................................................12

Part 4:.............................................................................................................................................15

Part 5:.............................................................................................................................................18

Part 6A:..........................................................................................................................................20

Part 6B:..........................................................................................................................................23

References and Bibliography:........................................................................................................25

Table of Contents

Part 1A:............................................................................................................................................2

Part 1B:............................................................................................................................................3

Part 2:...............................................................................................................................................5

Part 3:.............................................................................................................................................12

Part 4:.............................................................................................................................................15

Part 5:.............................................................................................................................................18

Part 6A:..........................................................................................................................................20

Part 6B:..........................................................................................................................................23

References and Bibliography:........................................................................................................25

2BUSINESS MANAGEMENT TECHNIQUES

Part 1A:

List the most appropriate sources of finance for THIS business in the start-up phase. Briefly

explain why these are the most appropriate, and also discuss the reasons why other sources of

finance would not be appropriate for this company.

Sources of finance for the manufacturing of miscellaneous items:

1.Bank loans: It is completely external and long term finance also secured. It will be approved

against collateral. Repayment method/schedule can also be adjusted. The interest rates can be

less compared to other sources. Also, it guarantees money for longer period and they charge only

interest for the loan amount.

2.Venture Capital: It is a private equity given by firms to startups which have higher growth

potential in exchange for ownership stake or equity. It is a long term investment by the firm.

Investors play a major role in management decision.

3.Personal Investment or Friends & Family: It could be our savings or assets an individual

possess. Also, we can ask our friends or family members to invest or lend the money it is usually

referred as patient capital and it is repaid when startup is profitable.

4.Angel Investors: They are wealthy individuals who can also be retired executives. They also

help by providing their experience in technical and management knowledge. They also can check

your startup management and would look to take part in decisions.

5.Incubators:It is a type of organization which provides you the resources for startup it includes

marketing, cash and consulting. In return they would ask for equity so they can get benefitted from

profits in the future.

6.Bank Overdrafts: It is similar to a bank loan but has completely different structure. Company

will have permission to withdraw more money beyond its balance in the account and they have

pay interest only for the outstanding amount and interest rates are high.

7.Bank Bills: Bank would be the guarantor for this type and risk will lie on bank not on the

borrower for the repayment .They would charge certain amount of fee for being the guarantor or

for taking the risk.

Banks would be the convenient and secured for the finance as we can deposit and withdraw and

interest is very low. Also, they do not interfere in the management. There can be tax benefits

small business owners would highly benefit from this. Loan approval is lengthy and time taking

process. They also disburse only 70-80% of sanctioned amount in parts. For manufacturing of

miscellaneous items main source of funds can be from bank as everything else is sorted out.

Other sources of funds can be risky because of the interest rates, investors will be involved in

decision making where not all will be benefitted by that as they become part owner would look for

returns rather benefit of other people.

Part 1A:

List the most appropriate sources of finance for THIS business in the start-up phase. Briefly

explain why these are the most appropriate, and also discuss the reasons why other sources of

finance would not be appropriate for this company.

Sources of finance for the manufacturing of miscellaneous items:

1.Bank loans: It is completely external and long term finance also secured. It will be approved

against collateral. Repayment method/schedule can also be adjusted. The interest rates can be

less compared to other sources. Also, it guarantees money for longer period and they charge only

interest for the loan amount.

2.Venture Capital: It is a private equity given by firms to startups which have higher growth

potential in exchange for ownership stake or equity. It is a long term investment by the firm.

Investors play a major role in management decision.

3.Personal Investment or Friends & Family: It could be our savings or assets an individual

possess. Also, we can ask our friends or family members to invest or lend the money it is usually

referred as patient capital and it is repaid when startup is profitable.

4.Angel Investors: They are wealthy individuals who can also be retired executives. They also

help by providing their experience in technical and management knowledge. They also can check

your startup management and would look to take part in decisions.

5.Incubators:It is a type of organization which provides you the resources for startup it includes

marketing, cash and consulting. In return they would ask for equity so they can get benefitted from

profits in the future.

6.Bank Overdrafts: It is similar to a bank loan but has completely different structure. Company

will have permission to withdraw more money beyond its balance in the account and they have

pay interest only for the outstanding amount and interest rates are high.

7.Bank Bills: Bank would be the guarantor for this type and risk will lie on bank not on the

borrower for the repayment .They would charge certain amount of fee for being the guarantor or

for taking the risk.

Banks would be the convenient and secured for the finance as we can deposit and withdraw and

interest is very low. Also, they do not interfere in the management. There can be tax benefits

small business owners would highly benefit from this. Loan approval is lengthy and time taking

process. They also disburse only 70-80% of sanctioned amount in parts. For manufacturing of

miscellaneous items main source of funds can be from bank as everything else is sorted out.

Other sources of funds can be risky because of the interest rates, investors will be involved in

decision making where not all will be benefitted by that as they become part owner would look for

returns rather benefit of other people.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3BUSINESS MANAGEMENT TECHNIQUES

Part 1B:

List the most appropriate sources of finance for THIS business for future expansion. Briefly

explain why these are the most appropriate, and also discuss the reasons why other sources of

finance would not be appropriate for this company.

1.Partnership: If there are more partners involved in the business then there will be plenty of

funds. Establishment of the business would be easy with less cost. Management decisions will be

internal, there will be no external involvement. Each person would be responsible for their debts

and shares. Any changes can be faster like increasing the production, wages and more like legal

structure. There might be a disagreement between the partners. Life of partnership depends on

the understanding between them.

2.Retained Earnings: It would be the best option for future expansion as it will not lead to any

change in the structure and everything will be same just a decision has to be made between the

partners or a resolution must be passed. It also increases the market value. It doesn’t add in a

liability. It doesn’t involve any outsiders so control on the firm will be same.

3.Franchising:It is one of the best options and most effective. Profits will be from the extra

sales. Owner gets an equity for using the firm name. It also increases the popularity among the

customers. It would concentrate more on purchases used for manufacturing. Training and

guidance should be given to new employees. Franchisee’s owner also gets a benefit for using the

name of established firm.

4.Venture capital: As the firms are interested to invest in startups they can also invest for

expansion of the business. If they see huge growth and profits or demand in the future of the

company. They would always work towards the betterment of the enterprises. Owner would not

be in the driver's seat anymore as they involve in management decision.

Part 1 mainly comprises of information that is used for the organization to detect the level

of different source of finance, which can help in supporting their operations. The most

appropriate source of finance has been listed in this part, which can be used by the organization

for improving their operations to support the cash requirements. From the overall evaluation, it is

detected that finance source from banks is much more convenient and secured for the

organization, as deposits and withdrawals can be conducted adequately with low interest rates. In

addition, the bank source of finance will not interfere with the management and allow full

control to the owners of the business. Furthermore, adequate benefits are mainly detected for

Part 1B:

List the most appropriate sources of finance for THIS business for future expansion. Briefly

explain why these are the most appropriate, and also discuss the reasons why other sources of

finance would not be appropriate for this company.

1.Partnership: If there are more partners involved in the business then there will be plenty of

funds. Establishment of the business would be easy with less cost. Management decisions will be

internal, there will be no external involvement. Each person would be responsible for their debts

and shares. Any changes can be faster like increasing the production, wages and more like legal

structure. There might be a disagreement between the partners. Life of partnership depends on

the understanding between them.

2.Retained Earnings: It would be the best option for future expansion as it will not lead to any

change in the structure and everything will be same just a decision has to be made between the

partners or a resolution must be passed. It also increases the market value. It doesn’t add in a

liability. It doesn’t involve any outsiders so control on the firm will be same.

3.Franchising:It is one of the best options and most effective. Profits will be from the extra

sales. Owner gets an equity for using the firm name. It also increases the popularity among the

customers. It would concentrate more on purchases used for manufacturing. Training and

guidance should be given to new employees. Franchisee’s owner also gets a benefit for using the

name of established firm.

4.Venture capital: As the firms are interested to invest in startups they can also invest for

expansion of the business. If they see huge growth and profits or demand in the future of the

company. They would always work towards the betterment of the enterprises. Owner would not

be in the driver's seat anymore as they involve in management decision.

Part 1 mainly comprises of information that is used for the organization to detect the level

of different source of finance, which can help in supporting their operations. The most

appropriate source of finance has been listed in this part, which can be used by the organization

for improving their operations to support the cash requirements. From the overall evaluation, it is

detected that finance source from banks is much more convenient and secured for the

organization, as deposits and withdrawals can be conducted adequately with low interest rates. In

addition, the bank source of finance will not interfere with the management and allow full

control to the owners of the business. Furthermore, adequate benefits are mainly detected for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4BUSINESS MANAGEMENT TECHNIQUES

small business owners, as they can get tax benefits after the loans taken from banks. Hence, the

finance source of banks can eventually allow the business to conduct their operations smoothly

with low interest rates, which are mainly imposed by other sources of finance. Lastly, other

forms of business can be risky for the organization, as investors will increase their exposure in

the organization, which will negatively affect its operations (Maskell, Baggaley and Grasso

2016).

The second part mainly provides information regarding the appropriate source of finance

of different business, which can support them during the expansion process. The partnership

firms mainly gather the required funds from partner, where any debt incurred by the organization

will be distributed within the partners. Furthermore, the retained earnings are the best possible

option, which can eventually help the organization to increase their operations. Moreover,

franchising is the best possible option and effective measure, which can improve the operations

of the organization by increasing their operational capability. Lastly, venture capital is mainly

conducted used by start-ups for increasing the expansion condition of the new business, which

can surge operations of the organization. Therefore, specific sources of finance can be used for

improving the level of operations of the organization, which can raise their income in the long

run (Crawford and Wang 2014).

small business owners, as they can get tax benefits after the loans taken from banks. Hence, the

finance source of banks can eventually allow the business to conduct their operations smoothly

with low interest rates, which are mainly imposed by other sources of finance. Lastly, other

forms of business can be risky for the organization, as investors will increase their exposure in

the organization, which will negatively affect its operations (Maskell, Baggaley and Grasso

2016).

The second part mainly provides information regarding the appropriate source of finance

of different business, which can support them during the expansion process. The partnership

firms mainly gather the required funds from partner, where any debt incurred by the organization

will be distributed within the partners. Furthermore, the retained earnings are the best possible

option, which can eventually help the organization to increase their operations. Moreover,

franchising is the best possible option and effective measure, which can improve the operations

of the organization by increasing their operational capability. Lastly, venture capital is mainly

conducted used by start-ups for increasing the expansion condition of the new business, which

can surge operations of the organization. Therefore, specific sources of finance can be used for

improving the level of operations of the organization, which can raise their income in the long

run (Crawford and Wang 2014).

5BUSINESS MANAGEMENT TECHNIQUES

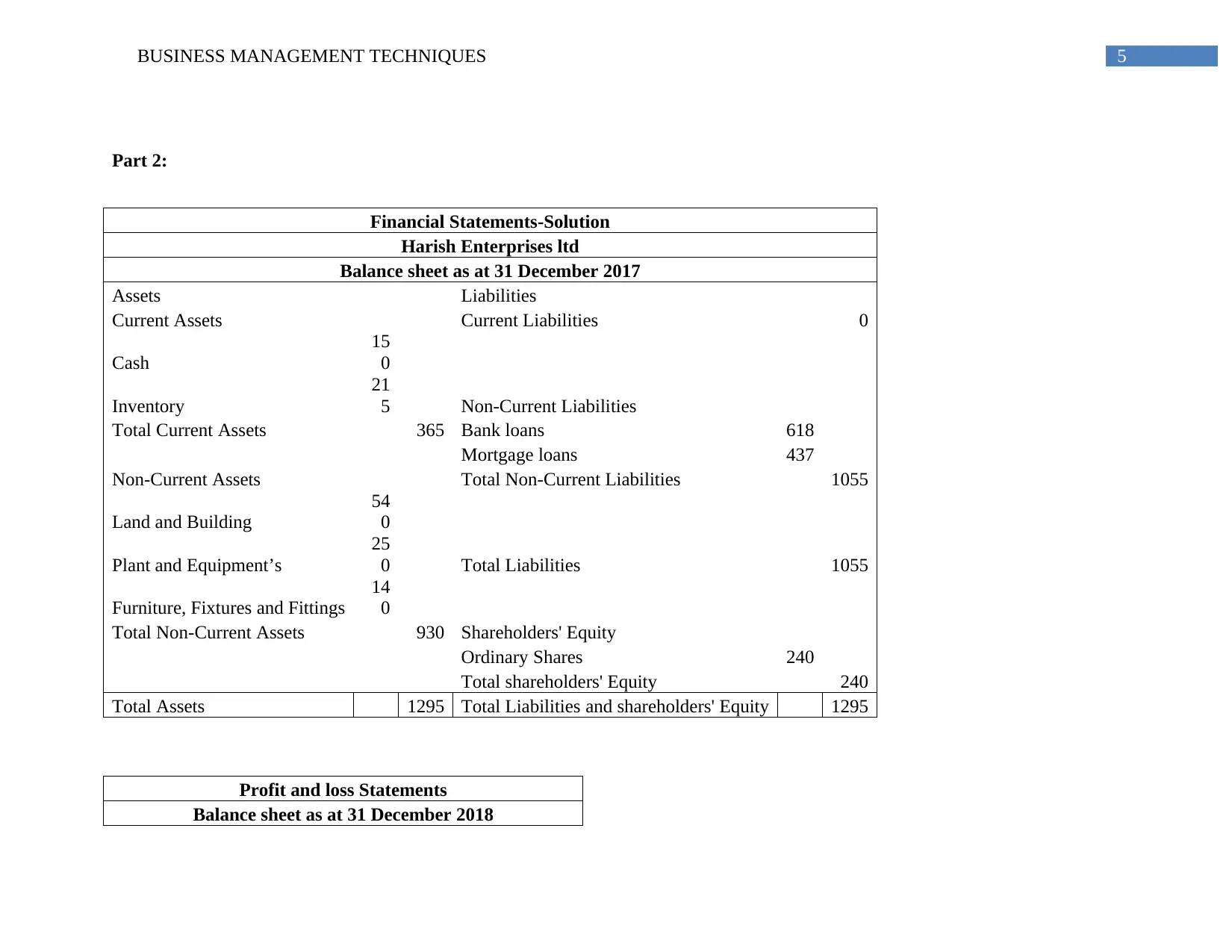

Part 2:

Financial Statements-Solution

Harish Enterprises ltd

Balance sheet as at 31 December 2017

Assets Liabilities

Current Assets Current Liabilities 0

Cash

15

0

Inventory

21

5 Non-Current Liabilities

Total Current Assets 365 Bank loans 618

Mortgage loans 437

Non-Current Assets Total Non-Current Liabilities 1055

Land and Building

54

0

Plant and Equipment’s

25

0 Total Liabilities 1055

Furniture, Fixtures and Fittings

14

0

Total Non-Current Assets 930 Shareholders' Equity

Ordinary Shares 240

Total shareholders' Equity 240

Total Assets 1295 Total Liabilities and shareholders' Equity 1295

Profit and loss Statements

Balance sheet as at 31 December 2018

Part 2:

Financial Statements-Solution

Harish Enterprises ltd

Balance sheet as at 31 December 2017

Assets Liabilities

Current Assets Current Liabilities 0

Cash

15

0

Inventory

21

5 Non-Current Liabilities

Total Current Assets 365 Bank loans 618

Mortgage loans 437

Non-Current Assets Total Non-Current Liabilities 1055

Land and Building

54

0

Plant and Equipment’s

25

0 Total Liabilities 1055

Furniture, Fixtures and Fittings

14

0

Total Non-Current Assets 930 Shareholders' Equity

Ordinary Shares 240

Total shareholders' Equity 240

Total Assets 1295 Total Liabilities and shareholders' Equity 1295

Profit and loss Statements

Balance sheet as at 31 December 2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6BUSINESS MANAGEMENT TECHNIQUES

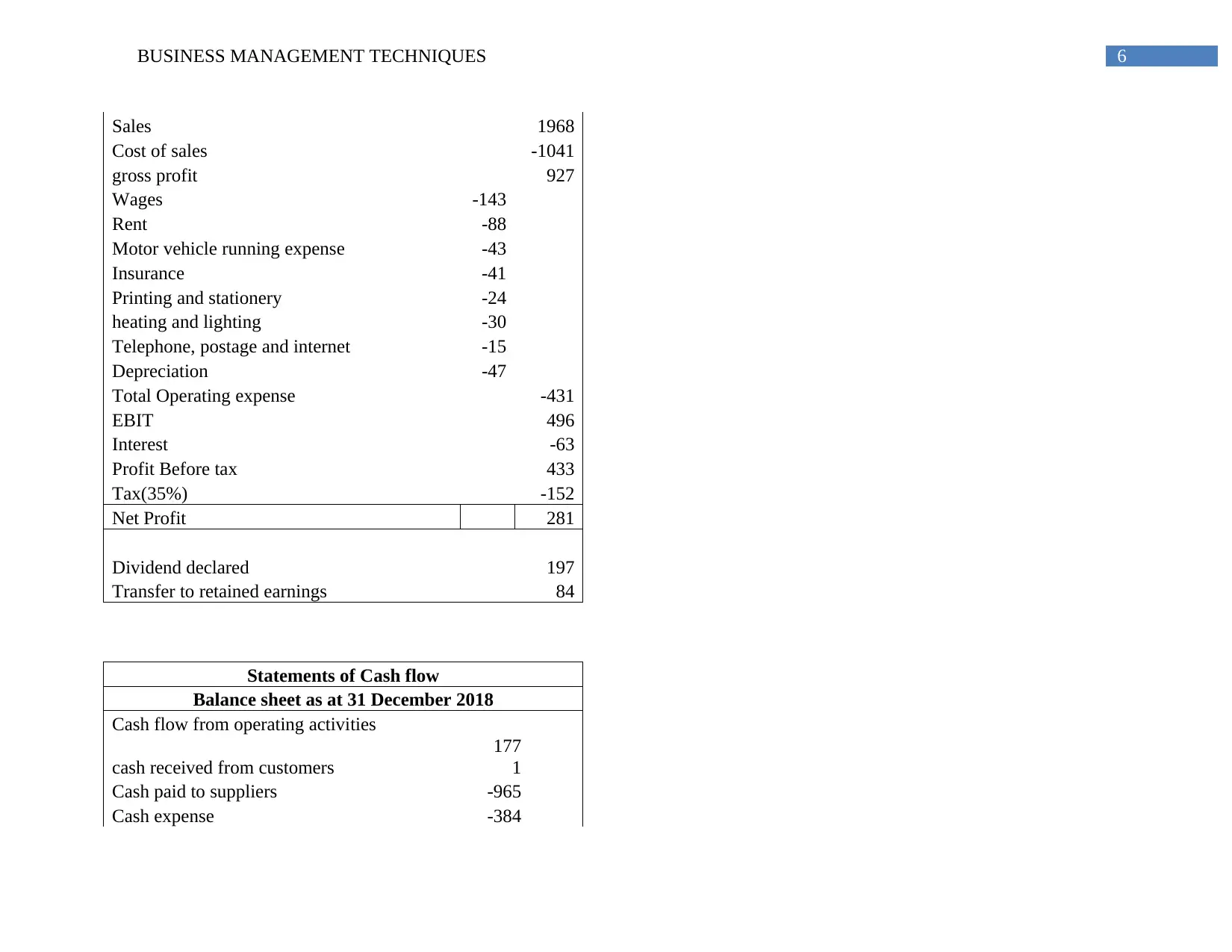

Sales 1968

Cost of sales -1041

gross profit 927

Wages -143

Rent -88

Motor vehicle running expense -43

Insurance -41

Printing and stationery -24

heating and lighting -30

Telephone, postage and internet -15

Depreciation -47

Total Operating expense -431

EBIT 496

Interest -63

Profit Before tax 433

Tax(35%) -152

Net Profit 281

Dividend declared 197

Transfer to retained earnings 84

Statements of Cash flow

Balance sheet as at 31 December 2018

Cash flow from operating activities

cash received from customers

177

1

Cash paid to suppliers -965

Cash expense -384

Sales 1968

Cost of sales -1041

gross profit 927

Wages -143

Rent -88

Motor vehicle running expense -43

Insurance -41

Printing and stationery -24

heating and lighting -30

Telephone, postage and internet -15

Depreciation -47

Total Operating expense -431

EBIT 496

Interest -63

Profit Before tax 433

Tax(35%) -152

Net Profit 281

Dividend declared 197

Transfer to retained earnings 84

Statements of Cash flow

Balance sheet as at 31 December 2018

Cash flow from operating activities

cash received from customers

177

1

Cash paid to suppliers -965

Cash expense -384

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

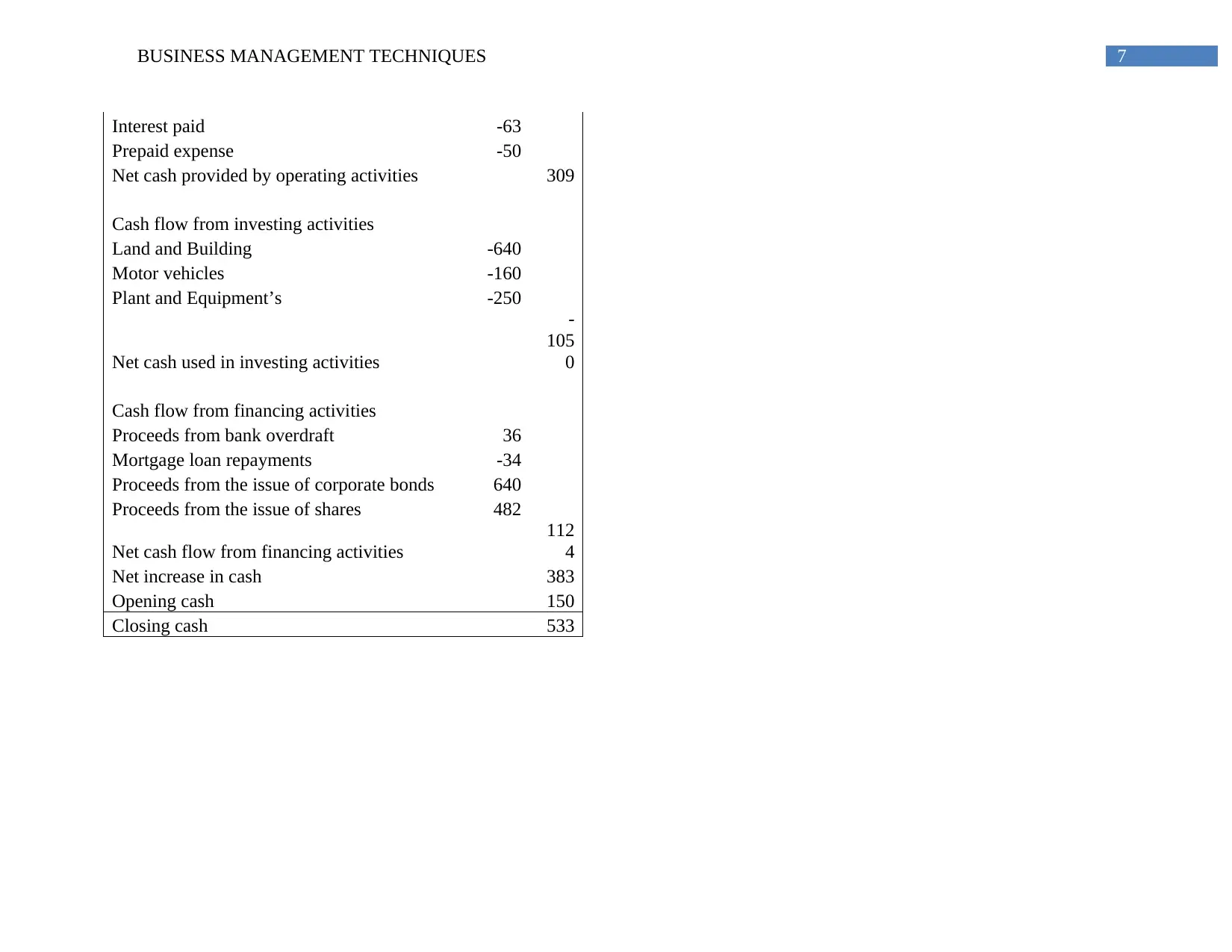

7BUSINESS MANAGEMENT TECHNIQUES

Interest paid -63

Prepaid expense -50

Net cash provided by operating activities 309

Cash flow from investing activities

Land and Building -640

Motor vehicles -160

Plant and Equipment’s -250

Net cash used in investing activities

-

105

0

Cash flow from financing activities

Proceeds from bank overdraft 36

Mortgage loan repayments -34

Proceeds from the issue of corporate bonds 640

Proceeds from the issue of shares 482

Net cash flow from financing activities

112

4

Net increase in cash 383

Opening cash 150

Closing cash 533

Interest paid -63

Prepaid expense -50

Net cash provided by operating activities 309

Cash flow from investing activities

Land and Building -640

Motor vehicles -160

Plant and Equipment’s -250

Net cash used in investing activities

-

105

0

Cash flow from financing activities

Proceeds from bank overdraft 36

Mortgage loan repayments -34

Proceeds from the issue of corporate bonds 640

Proceeds from the issue of shares 482

Net cash flow from financing activities

112

4

Net increase in cash 383

Opening cash 150

Closing cash 533

8BUSINESS MANAGEMENT TECHNIQUES

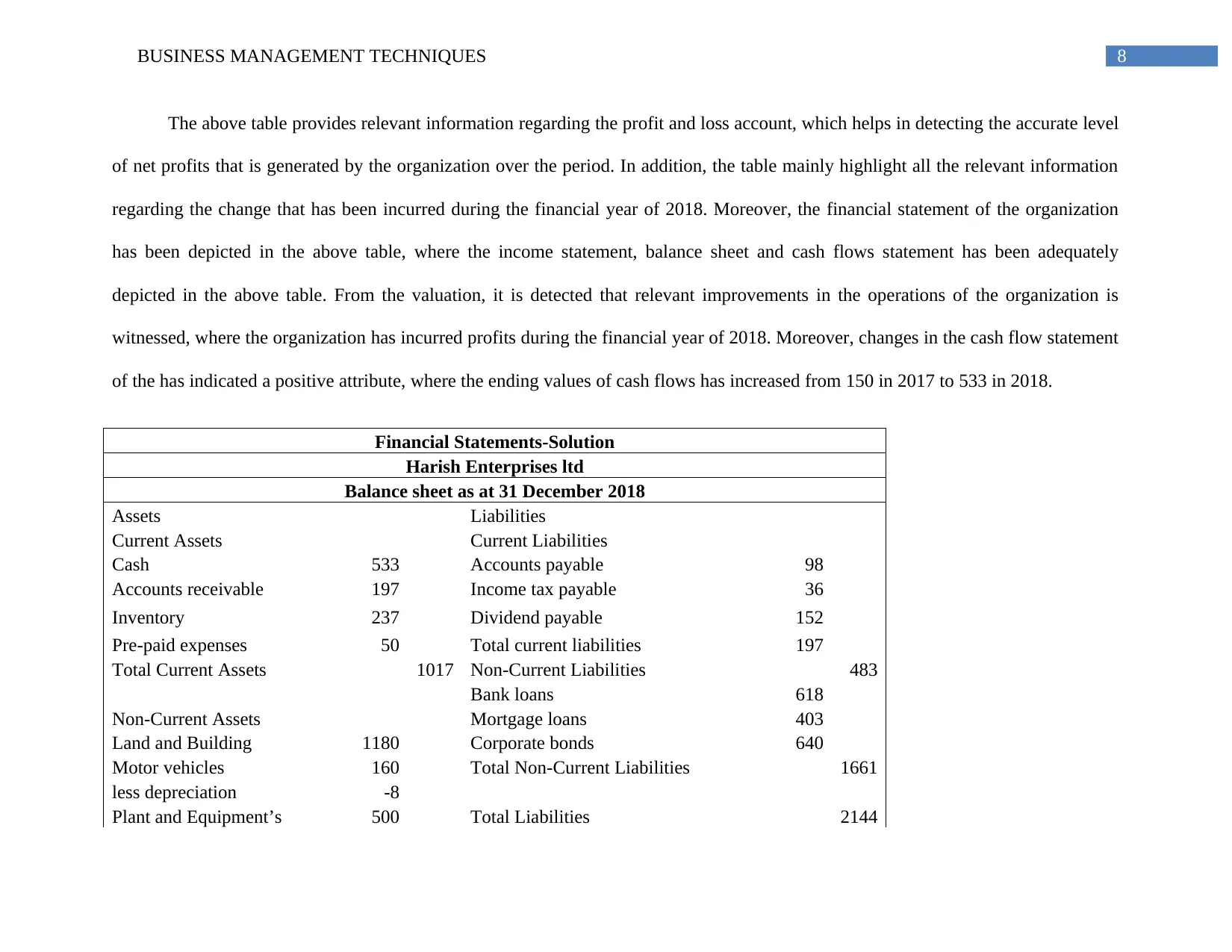

The above table provides relevant information regarding the profit and loss account, which helps in detecting the accurate level

of net profits that is generated by the organization over the period. In addition, the table mainly highlight all the relevant information

regarding the change that has been incurred during the financial year of 2018. Moreover, the financial statement of the organization

has been depicted in the above table, where the income statement, balance sheet and cash flows statement has been adequately

depicted in the above table. From the valuation, it is detected that relevant improvements in the operations of the organization is

witnessed, where the organization has incurred profits during the financial year of 2018. Moreover, changes in the cash flow statement

of the has indicated a positive attribute, where the ending values of cash flows has increased from 150 in 2017 to 533 in 2018.

Financial Statements-Solution

Harish Enterprises ltd

Balance sheet as at 31 December 2018

Assets Liabilities

Current Assets Current Liabilities

Cash 533 Accounts payable 98

Accounts receivable 197 Income tax payable 36

Inventory 237 Dividend payable 152

Pre-paid expenses 50 Total current liabilities 197

Total Current Assets 1017 Non-Current Liabilities 483

Bank loans 618

Non-Current Assets Mortgage loans 403

Land and Building 1180 Corporate bonds 640

Motor vehicles 160 Total Non-Current Liabilities 1661

less depreciation -8

Plant and Equipment’s 500 Total Liabilities 2144

The above table provides relevant information regarding the profit and loss account, which helps in detecting the accurate level

of net profits that is generated by the organization over the period. In addition, the table mainly highlight all the relevant information

regarding the change that has been incurred during the financial year of 2018. Moreover, the financial statement of the organization

has been depicted in the above table, where the income statement, balance sheet and cash flows statement has been adequately

depicted in the above table. From the valuation, it is detected that relevant improvements in the operations of the organization is

witnessed, where the organization has incurred profits during the financial year of 2018. Moreover, changes in the cash flow statement

of the has indicated a positive attribute, where the ending values of cash flows has increased from 150 in 2017 to 533 in 2018.

Financial Statements-Solution

Harish Enterprises ltd

Balance sheet as at 31 December 2018

Assets Liabilities

Current Assets Current Liabilities

Cash 533 Accounts payable 98

Accounts receivable 197 Income tax payable 36

Inventory 237 Dividend payable 152

Pre-paid expenses 50 Total current liabilities 197

Total Current Assets 1017 Non-Current Liabilities 483

Bank loans 618

Non-Current Assets Mortgage loans 403

Land and Building 1180 Corporate bonds 640

Motor vehicles 160 Total Non-Current Liabilities 1661

less depreciation -8

Plant and Equipment’s 500 Total Liabilities 2144

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

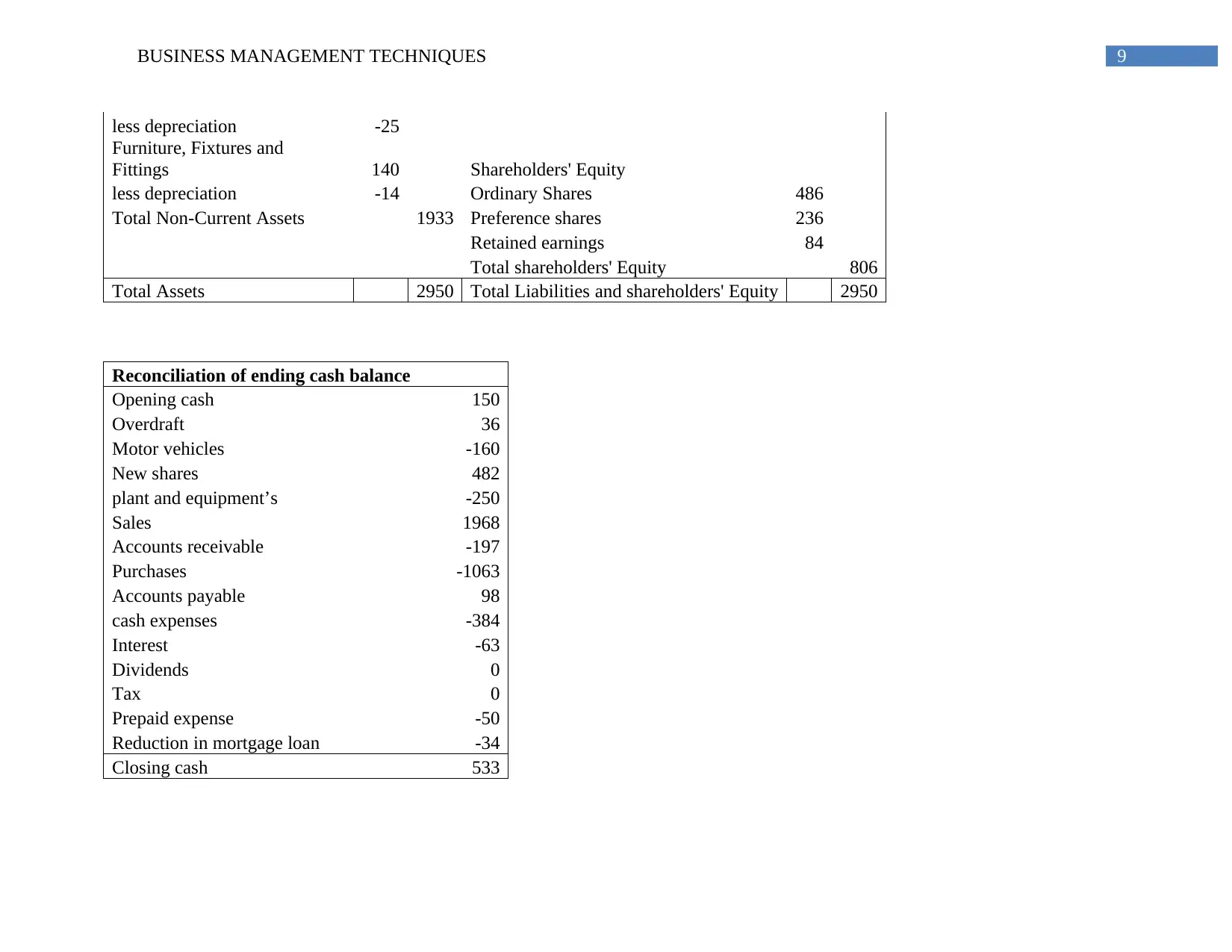

9BUSINESS MANAGEMENT TECHNIQUES

less depreciation -25

Furniture, Fixtures and

Fittings 140 Shareholders' Equity

less depreciation -14 Ordinary Shares 486

Total Non-Current Assets 1933 Preference shares 236

Retained earnings 84

Total shareholders' Equity 806

Total Assets 2950 Total Liabilities and shareholders' Equity 2950

Reconciliation of ending cash balance

Opening cash 150

Overdraft 36

Motor vehicles -160

New shares 482

plant and equipment’s -250

Sales 1968

Accounts receivable -197

Purchases -1063

Accounts payable 98

cash expenses -384

Interest -63

Dividends 0

Tax 0

Prepaid expense -50

Reduction in mortgage loan -34

Closing cash 533

less depreciation -25

Furniture, Fixtures and

Fittings 140 Shareholders' Equity

less depreciation -14 Ordinary Shares 486

Total Non-Current Assets 1933 Preference shares 236

Retained earnings 84

Total shareholders' Equity 806

Total Assets 2950 Total Liabilities and shareholders' Equity 2950

Reconciliation of ending cash balance

Opening cash 150

Overdraft 36

Motor vehicles -160

New shares 482

plant and equipment’s -250

Sales 1968

Accounts receivable -197

Purchases -1063

Accounts payable 98

cash expenses -384

Interest -63

Dividends 0

Tax 0

Prepaid expense -50

Reduction in mortgage loan -34

Closing cash 533

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10BUSINESS MANAGEMENT TECHNIQUES

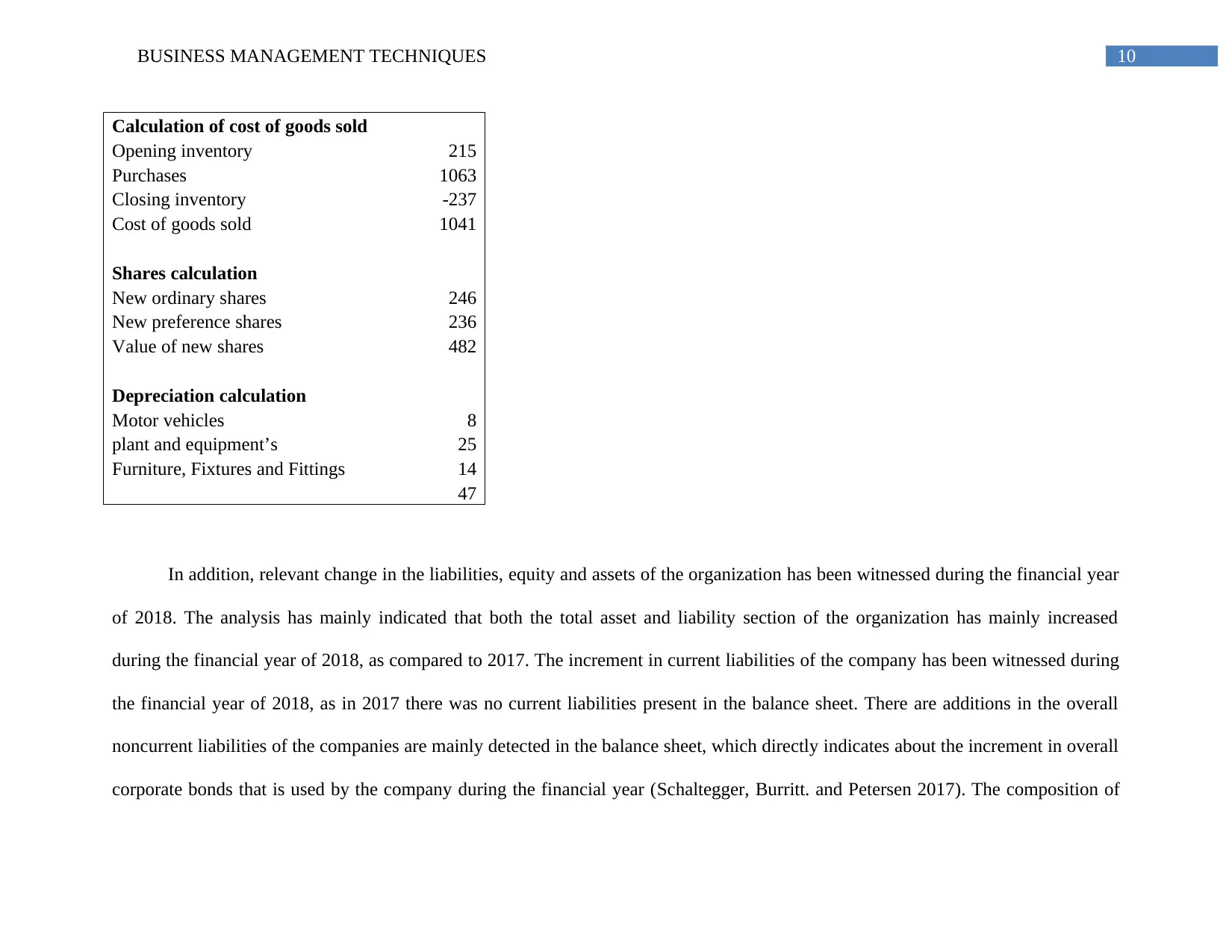

Calculation of cost of goods sold

Opening inventory 215

Purchases 1063

Closing inventory -237

Cost of goods sold 1041

Shares calculation

New ordinary shares 246

New preference shares 236

Value of new shares 482

Depreciation calculation

Motor vehicles 8

plant and equipment’s 25

Furniture, Fixtures and Fittings 14

47

In addition, relevant change in the liabilities, equity and assets of the organization has been witnessed during the financial year

of 2018. The analysis has mainly indicated that both the total asset and liability section of the organization has mainly increased

during the financial year of 2018, as compared to 2017. The increment in current liabilities of the company has been witnessed during

the financial year of 2018, as in 2017 there was no current liabilities present in the balance sheet. There are additions in the overall

noncurrent liabilities of the companies are mainly detected in the balance sheet, which directly indicates about the increment in overall

corporate bonds that is used by the company during the financial year (Schaltegger, Burritt. and Petersen 2017). The composition of

Calculation of cost of goods sold

Opening inventory 215

Purchases 1063

Closing inventory -237

Cost of goods sold 1041

Shares calculation

New ordinary shares 246

New preference shares 236

Value of new shares 482

Depreciation calculation

Motor vehicles 8

plant and equipment’s 25

Furniture, Fixtures and Fittings 14

47

In addition, relevant change in the liabilities, equity and assets of the organization has been witnessed during the financial year

of 2018. The analysis has mainly indicated that both the total asset and liability section of the organization has mainly increased

during the financial year of 2018, as compared to 2017. The increment in current liabilities of the company has been witnessed during

the financial year of 2018, as in 2017 there was no current liabilities present in the balance sheet. There are additions in the overall

noncurrent liabilities of the companies are mainly detected in the balance sheet, which directly indicates about the increment in overall

corporate bonds that is used by the company during the financial year (Schaltegger, Burritt. and Petersen 2017). The composition of

11BUSINESS MANAGEMENT TECHNIQUES

total liabilities is relevantly low than the total assets of the organization, where the equity section has mainly provided adequate

composition in the financial statement. The adequate calculation of cost of goods sold, shares and depreciation is mainly conducted for

preparing the annual report, which can provide adequate information regarding the financial position of the company.

total liabilities is relevantly low than the total assets of the organization, where the equity section has mainly provided adequate

composition in the financial statement. The adequate calculation of cost of goods sold, shares and depreciation is mainly conducted for

preparing the annual report, which can provide adequate information regarding the financial position of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.