Accounting and Finance Solutions: Cherry Hill Sports Analysis

VerifiedAdded on 2022/10/14

|6

|1340

|316

Homework Assignment

AI Summary

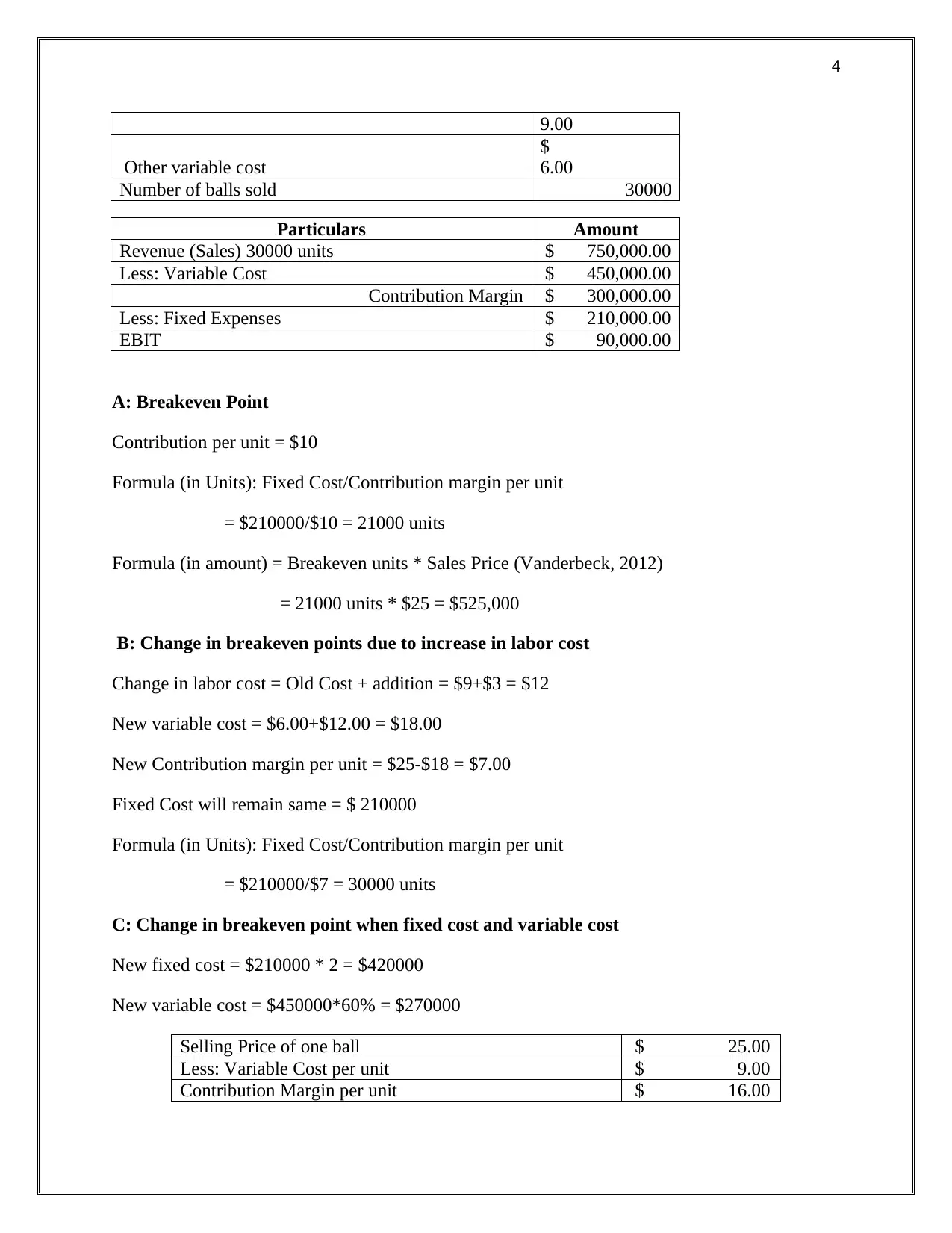

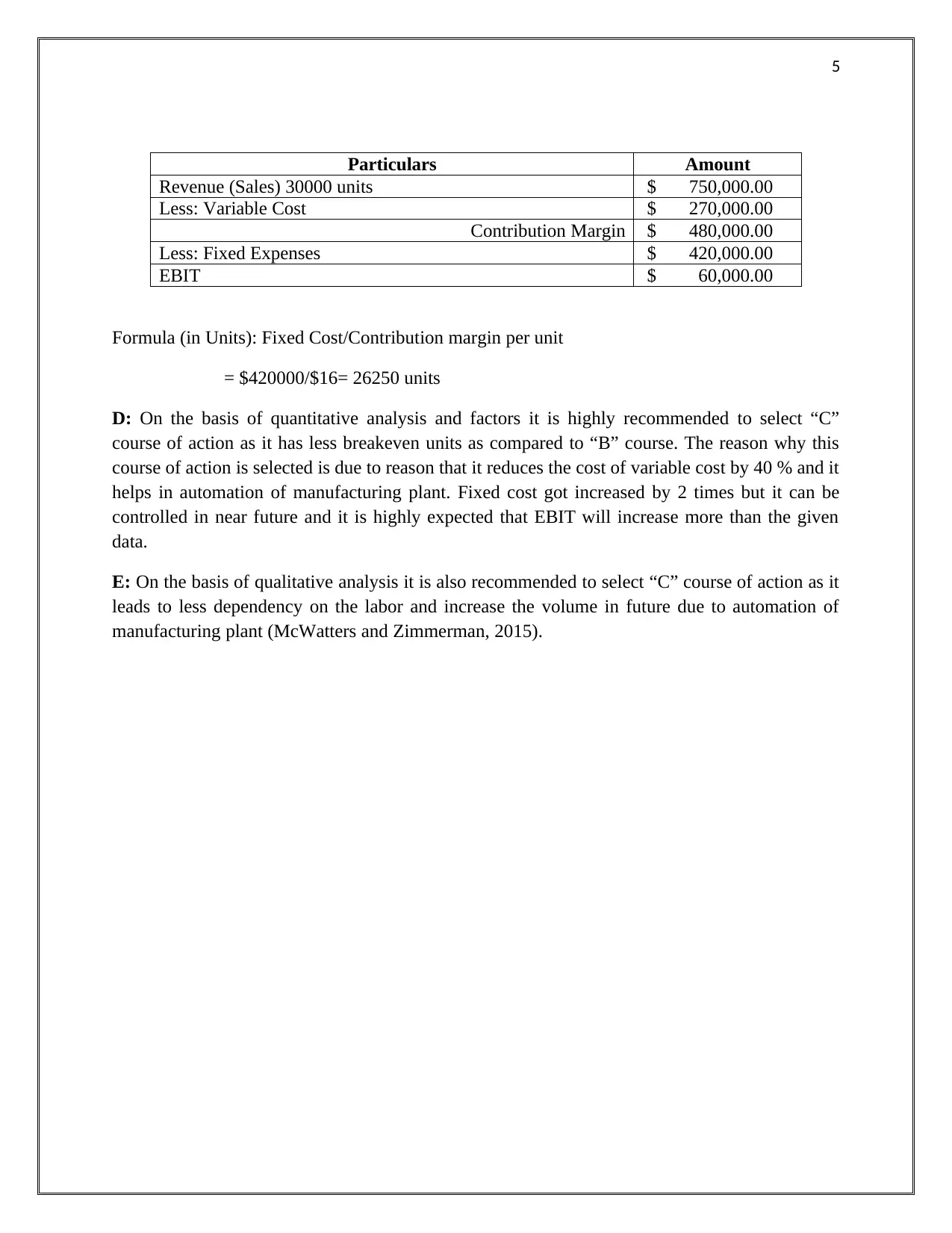

This document presents a comprehensive set of accounting solutions addressing a range of financial concepts and problems. It begins by defining and explaining the significance of EBITDA, detailing its role in assessing a company's operating performance. The solution then clarifies the balance sheet equation and its implications, followed by a comparison of gross profit and contribution margin, highlighting their differences. Further, the document contrasts franchising and licensing under intellectual property and analyzes the impact of depreciation methods on net income. The assignment also explores inventory methods, focusing on the alignment of FIFO with real-life operations. It then outlines the components of original equipment cost and explains the concept of relevant range and its effect on fixed costs. The break-even point and its implications are discussed, along with the disadvantages of the payback period method. Finally, the document provides a detailed solution to a case study involving Cherry Hill Sports Company, including calculations for break-even points, contribution margin, and financial analysis, with recommendations based on quantitative and qualitative factors, and references used.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.