Accounting and Finance Project: Business Valuation Methods

VerifiedAdded on 2022/08/20

|7

|1266

|10

Project

AI Summary

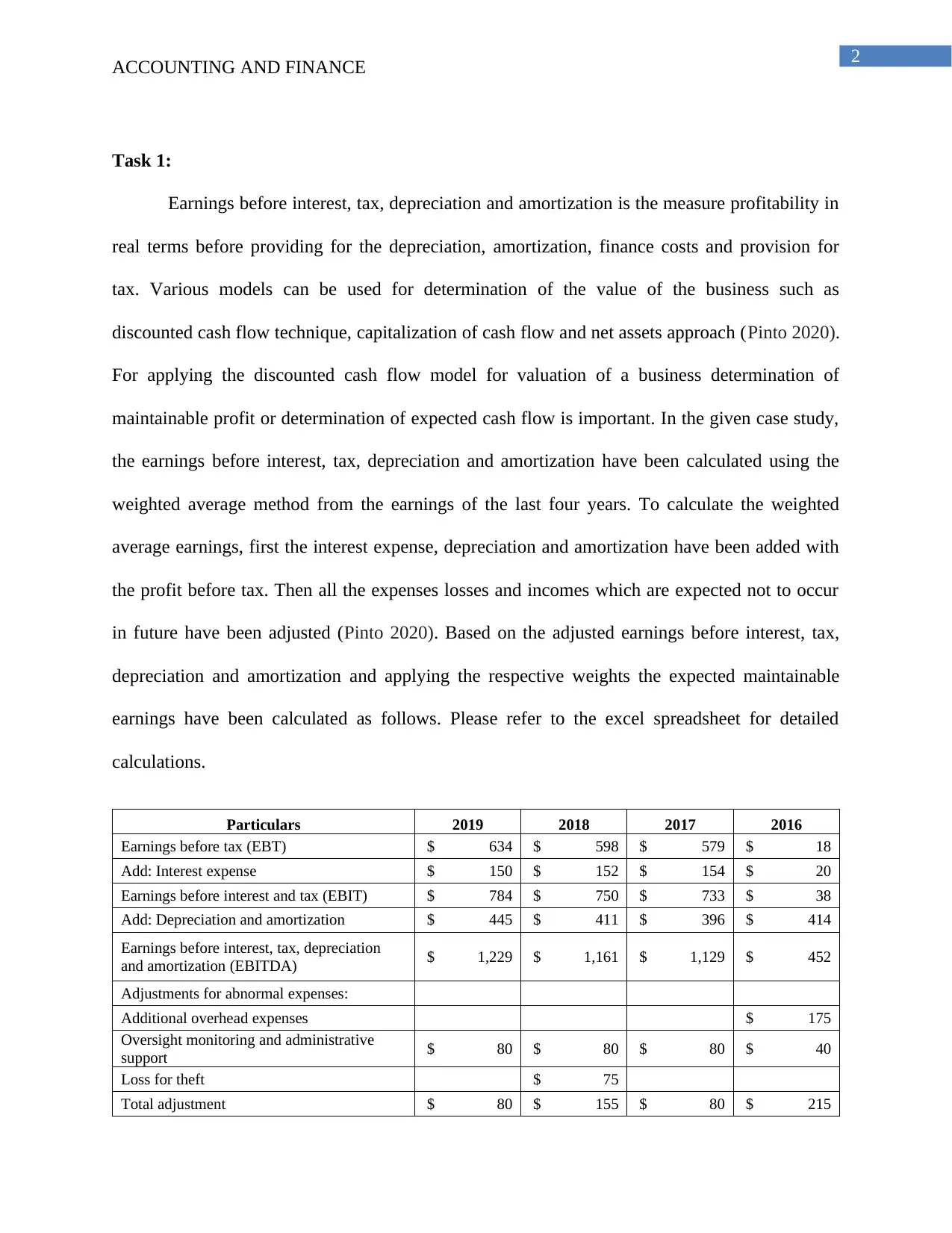

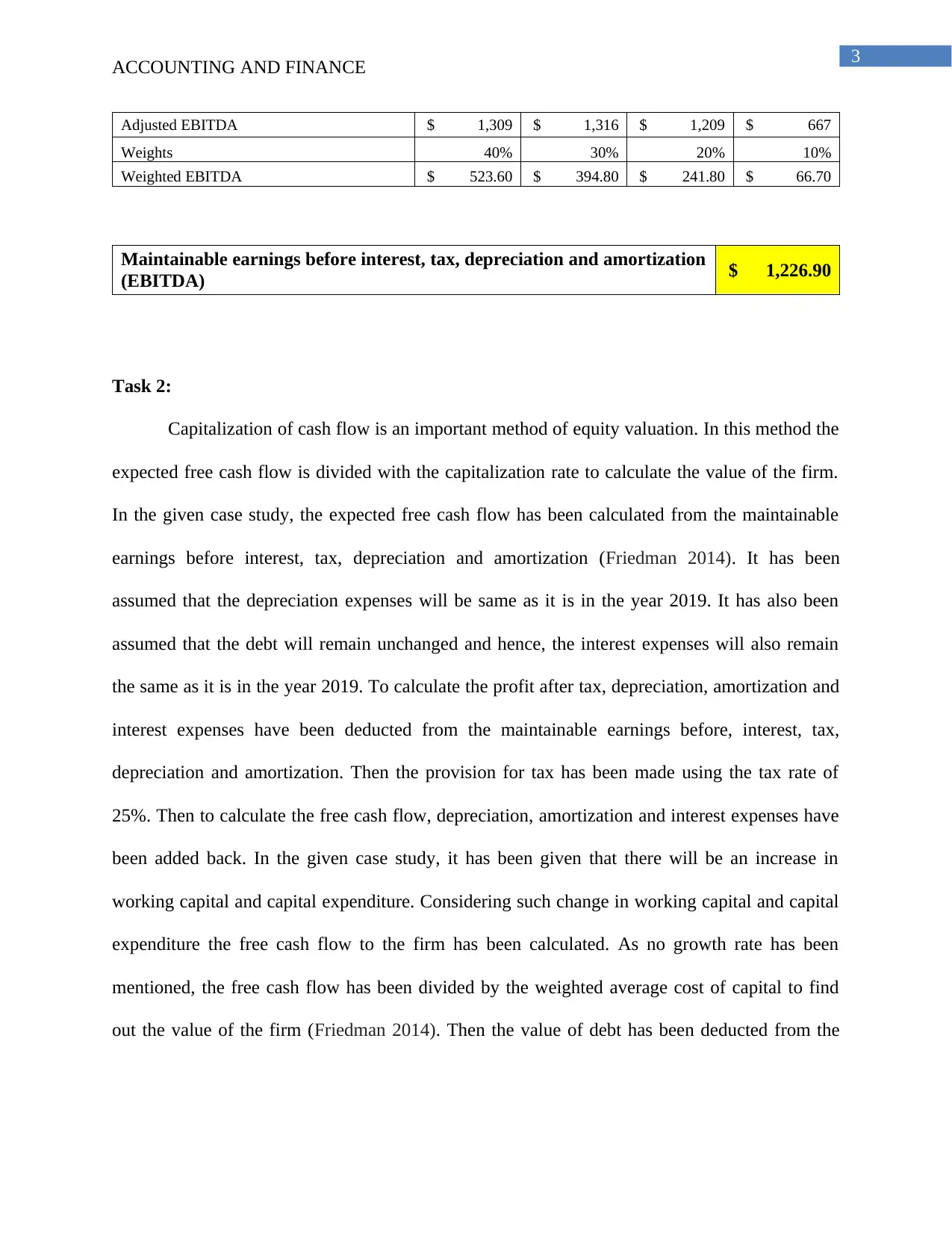

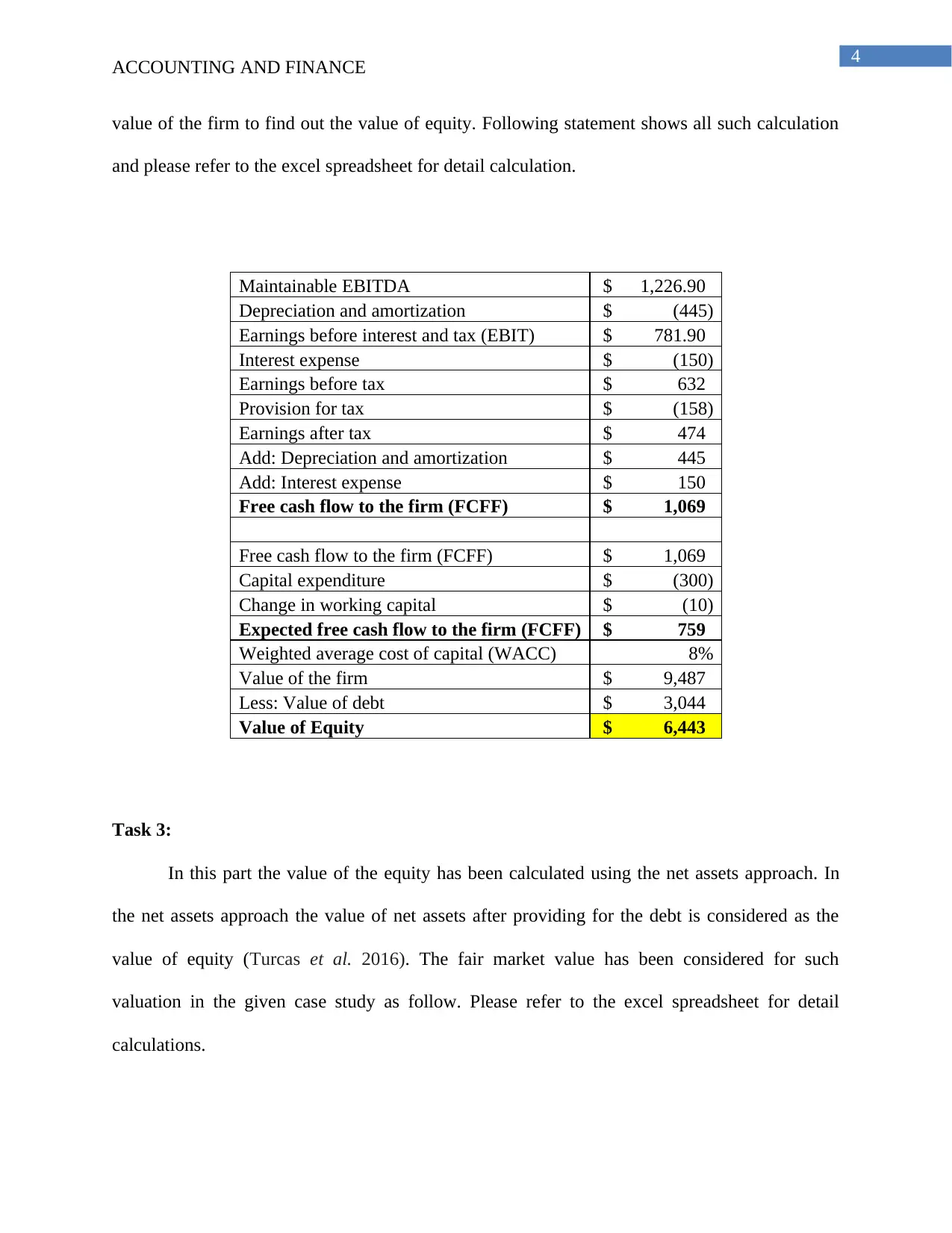

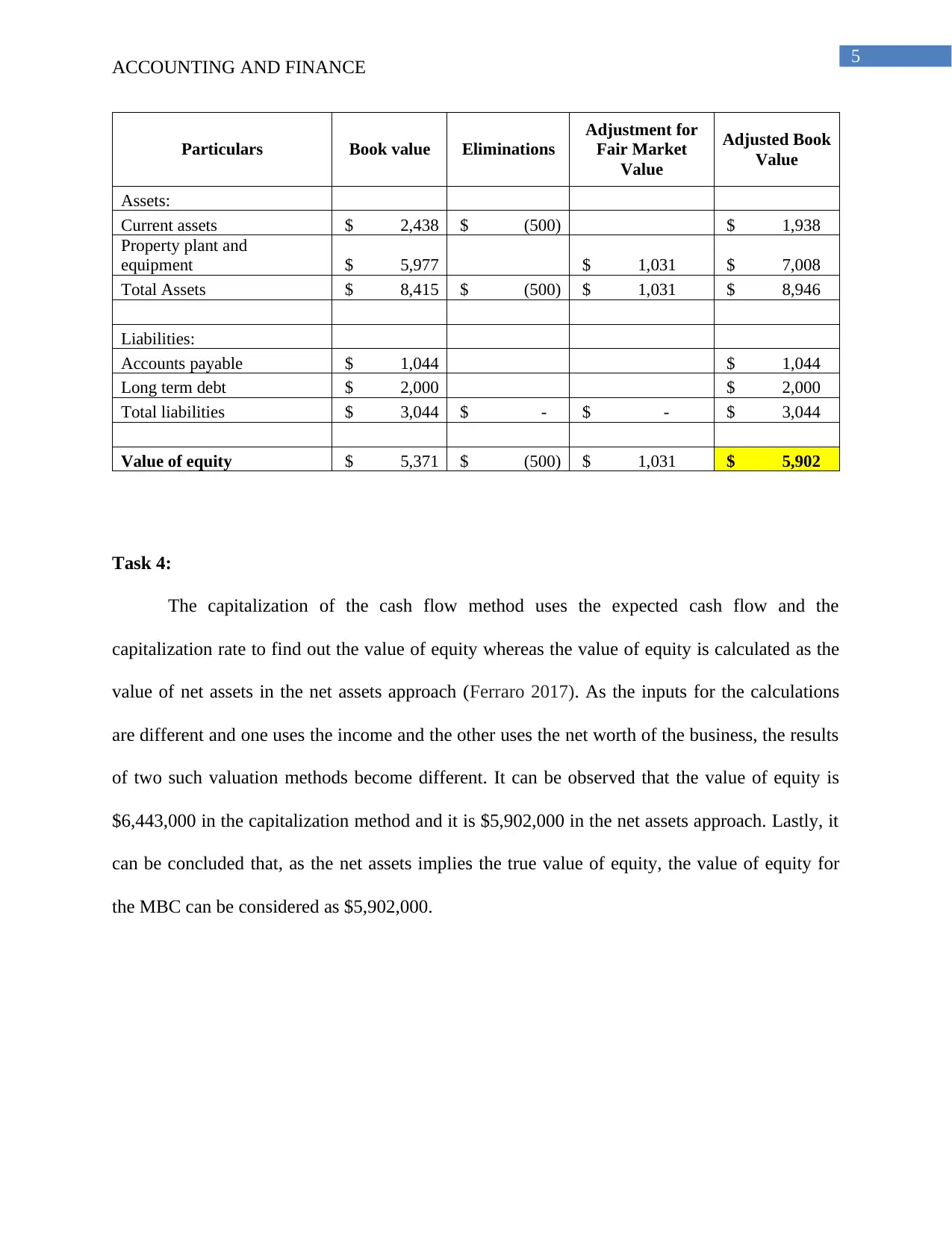

This finance project analyzes the valuation of a business using several methods. Task 1 focuses on calculating the maintainable earnings before interest, tax, depreciation, and amortization (EBITDA) using a weighted average approach, adjusting for abnormal expenses. Task 2 employs the capitalization of cash flow method to determine the firm's value, calculating the expected free cash flow, and the weighted average cost of capital (WACC) to find the equity value. Task 3 utilizes the net assets approach, considering fair market values to ascertain the value of equity. Finally, Task 4 compares the outcomes of the capitalization of cash flow and net assets methods, highlighting the differences arising from varied inputs and concluding with a final equity value based on the net assets approach. The project includes detailed calculations and references to relevant financial literature.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.