Accounting for Managers: Analysis of Financial Statements Report

VerifiedAdded on 2020/03/28

|14

|3720

|38

Report

AI Summary

This report, prepared for an accounting for managers course, provides a comprehensive analysis of financial statements, ethical considerations, and accounting software solutions. The report begins with an analysis of Efficient Distributors Ltd's financial performance using ratio analysis, highlighting profitability, liquidity, and efficiency trends over three years. It then addresses ethical dilemmas faced by an accountant, Tom, at Allandale Ltd, focusing on the implications of asset valuation and debt recovery on financial reporting and compliance with loan agreements. The report recommends ethical courses of action. Finally, the report explores accounting software options for Giggling Brothers, detailing system benefits, implementation recommendations, stakeholder involvement, and competitor analysis. The analysis covers financial performance, ethical decision-making, and technological solutions, making it a valuable resource for understanding key aspects of accounting and financial management.

Running head: Accounting for Managers

ACCOUNTING FOR MANAGERS

ACCOUNTING FOR MANAGERS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting for Managers 2

Table of Contents

Question 1........................................................................................................................................4

Introduction..................................................................................................................................4

A) Description of business operations: Analysis of financial statements....................................4

Analysis:......................................................................................................................................6

B) Limitations of the analysis......................................................................................................7

C) Additional information in context to the financial analysis....................................................7

Conclusion and Recommendations..............................................................................................8

Question 2........................................................................................................................................8

a) Ethical problems faced by Tom:..............................................................................................8

Facts.........................................................................................................................................8

Stakeholders.............................................................................................................................8

Problems..................................................................................................................................9

Values & Principles.................................................................................................................9

b) Recommendations:..................................................................................................................9

Possible Courses of Action......................................................................................................9

Evaluation of Each Action.....................................................................................................10

Principles & Consequences Raised.......................................................................................10

Choose a Plan........................................................................................................................10

Justification for Selection......................................................................................................10

Question 3......................................................................................................................................10

Types of accounting software to be designed by Giggling Brothers.........................................10

Benefits of the system and its incorporation with the planning process....................................11

Recommendations for Giggling Brothers for implementation of new system..........................11

Stakeholders involvement in the development of new system..................................................12

Table of Contents

Question 1........................................................................................................................................4

Introduction..................................................................................................................................4

A) Description of business operations: Analysis of financial statements....................................4

Analysis:......................................................................................................................................6

B) Limitations of the analysis......................................................................................................7

C) Additional information in context to the financial analysis....................................................7

Conclusion and Recommendations..............................................................................................8

Question 2........................................................................................................................................8

a) Ethical problems faced by Tom:..............................................................................................8

Facts.........................................................................................................................................8

Stakeholders.............................................................................................................................8

Problems..................................................................................................................................9

Values & Principles.................................................................................................................9

b) Recommendations:..................................................................................................................9

Possible Courses of Action......................................................................................................9

Evaluation of Each Action.....................................................................................................10

Principles & Consequences Raised.......................................................................................10

Choose a Plan........................................................................................................................10

Justification for Selection......................................................................................................10

Question 3......................................................................................................................................10

Types of accounting software to be designed by Giggling Brothers.........................................10

Benefits of the system and its incorporation with the planning process....................................11

Recommendations for Giggling Brothers for implementation of new system..........................11

Stakeholders involvement in the development of new system..................................................12

Accounting for Managers 3

Competitors analysis for Giggling Brothers..............................................................................12

Reference list.................................................................................................................................13

Competitors analysis for Giggling Brothers..............................................................................12

Reference list.................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting for Managers 4

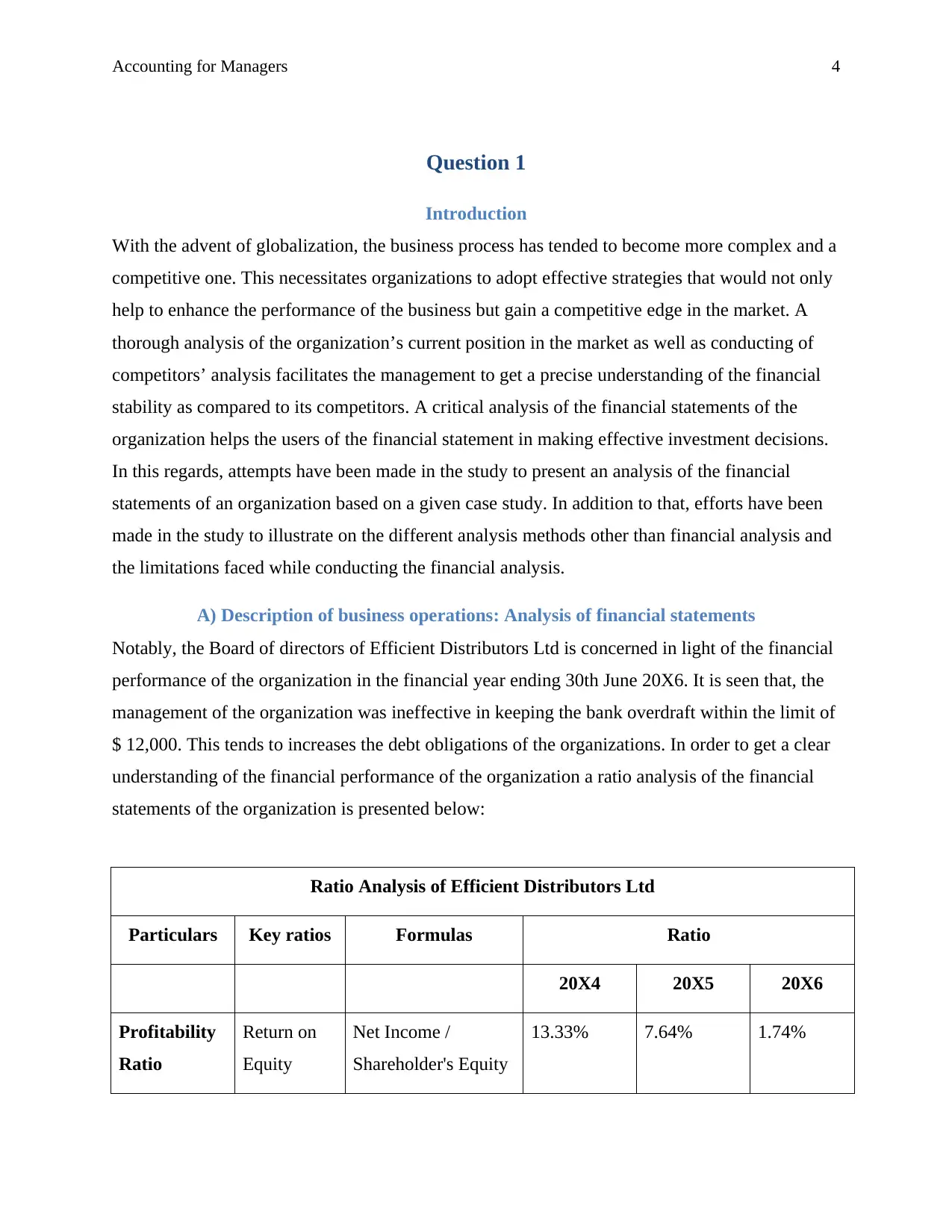

Question 1

Introduction

With the advent of globalization, the business process has tended to become more complex and a

competitive one. This necessitates organizations to adopt effective strategies that would not only

help to enhance the performance of the business but gain a competitive edge in the market. A

thorough analysis of the organization’s current position in the market as well as conducting of

competitors’ analysis facilitates the management to get a precise understanding of the financial

stability as compared to its competitors. A critical analysis of the financial statements of the

organization helps the users of the financial statement in making effective investment decisions.

In this regards, attempts have been made in the study to present an analysis of the financial

statements of an organization based on a given case study. In addition to that, efforts have been

made in the study to illustrate on the different analysis methods other than financial analysis and

the limitations faced while conducting the financial analysis.

A) Description of business operations: Analysis of financial statements

Notably, the Board of directors of Efficient Distributors Ltd is concerned in light of the financial

performance of the organization in the financial year ending 30th June 20X6. It is seen that, the

management of the organization was ineffective in keeping the bank overdraft within the limit of

$ 12,000. This tends to increases the debt obligations of the organizations. In order to get a clear

understanding of the financial performance of the organization a ratio analysis of the financial

statements of the organization is presented below:

Ratio Analysis of Efficient Distributors Ltd

Particulars Key ratios Formulas Ratio

20X4 20X5 20X6

Profitability

Ratio

Return on

Equity

Net Income /

Shareholder's Equity

13.33% 7.64% 1.74%

Question 1

Introduction

With the advent of globalization, the business process has tended to become more complex and a

competitive one. This necessitates organizations to adopt effective strategies that would not only

help to enhance the performance of the business but gain a competitive edge in the market. A

thorough analysis of the organization’s current position in the market as well as conducting of

competitors’ analysis facilitates the management to get a precise understanding of the financial

stability as compared to its competitors. A critical analysis of the financial statements of the

organization helps the users of the financial statement in making effective investment decisions.

In this regards, attempts have been made in the study to present an analysis of the financial

statements of an organization based on a given case study. In addition to that, efforts have been

made in the study to illustrate on the different analysis methods other than financial analysis and

the limitations faced while conducting the financial analysis.

A) Description of business operations: Analysis of financial statements

Notably, the Board of directors of Efficient Distributors Ltd is concerned in light of the financial

performance of the organization in the financial year ending 30th June 20X6. It is seen that, the

management of the organization was ineffective in keeping the bank overdraft within the limit of

$ 12,000. This tends to increases the debt obligations of the organizations. In order to get a clear

understanding of the financial performance of the organization a ratio analysis of the financial

statements of the organization is presented below:

Ratio Analysis of Efficient Distributors Ltd

Particulars Key ratios Formulas Ratio

20X4 20X5 20X6

Profitability

Ratio

Return on

Equity

Net Income /

Shareholder's Equity

13.33% 7.64% 1.74%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting for Managers 5

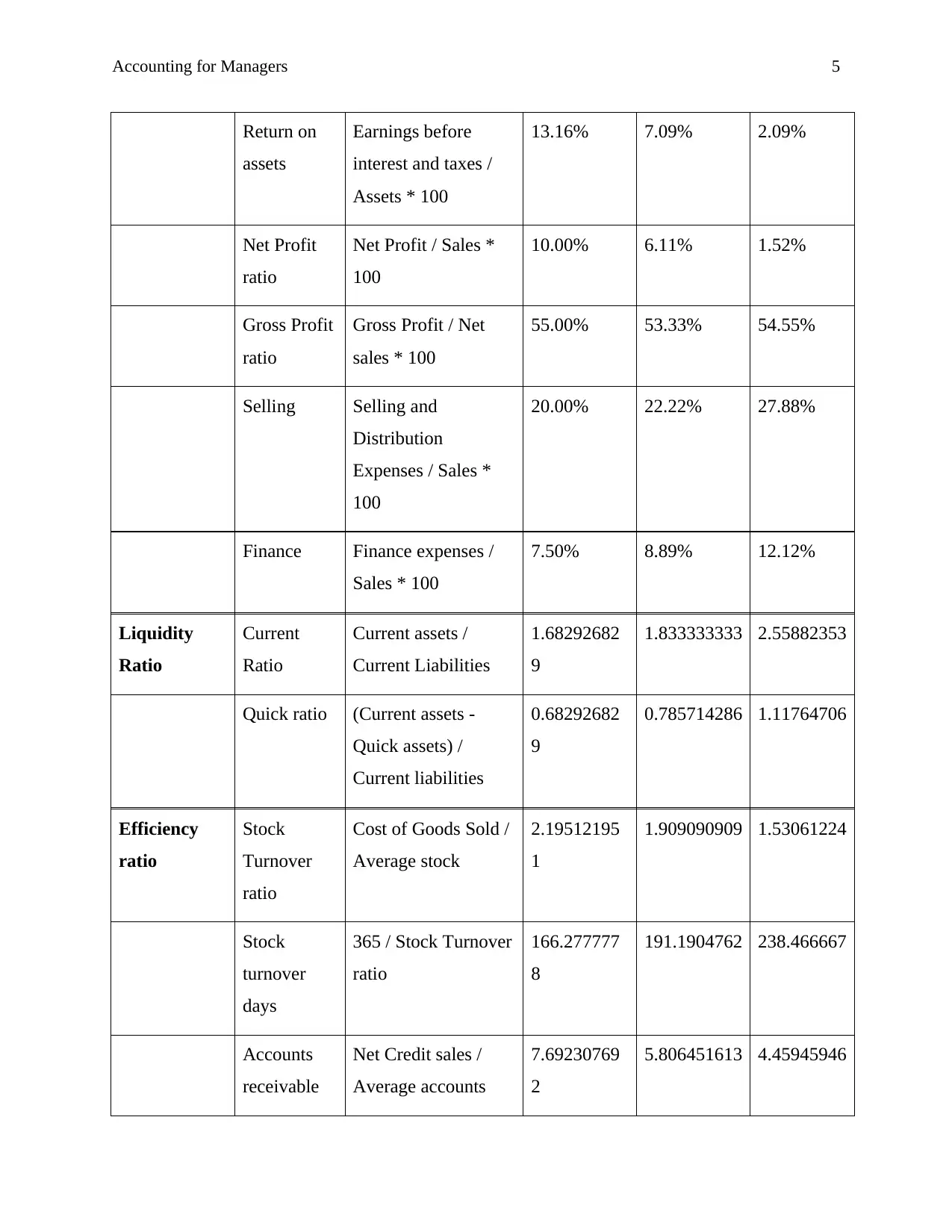

Return on

assets

Earnings before

interest and taxes /

Assets * 100

13.16% 7.09% 2.09%

Net Profit

ratio

Net Profit / Sales *

100

10.00% 6.11% 1.52%

Gross Profit

ratio

Gross Profit / Net

sales * 100

55.00% 53.33% 54.55%

Selling Selling and

Distribution

Expenses / Sales *

100

20.00% 22.22% 27.88%

Finance Finance expenses /

Sales * 100

7.50% 8.89% 12.12%

Liquidity

Ratio

Current

Ratio

Current assets /

Current Liabilities

1.68292682

9

1.833333333 2.55882353

Quick ratio (Current assets -

Quick assets) /

Current liabilities

0.68292682

9

0.785714286 1.11764706

Efficiency

ratio

Stock

Turnover

ratio

Cost of Goods Sold /

Average stock

2.19512195

1

1.909090909 1.53061224

Stock

turnover

days

365 / Stock Turnover

ratio

166.277777

8

191.1904762 238.466667

Accounts

receivable

Net Credit sales /

Average accounts

7.69230769

2

5.806451613 4.45945946

Return on

assets

Earnings before

interest and taxes /

Assets * 100

13.16% 7.09% 2.09%

Net Profit

ratio

Net Profit / Sales *

100

10.00% 6.11% 1.52%

Gross Profit

ratio

Gross Profit / Net

sales * 100

55.00% 53.33% 54.55%

Selling Selling and

Distribution

Expenses / Sales *

100

20.00% 22.22% 27.88%

Finance Finance expenses /

Sales * 100

7.50% 8.89% 12.12%

Liquidity

Ratio

Current

Ratio

Current assets /

Current Liabilities

1.68292682

9

1.833333333 2.55882353

Quick ratio (Current assets -

Quick assets) /

Current liabilities

0.68292682

9

0.785714286 1.11764706

Efficiency

ratio

Stock

Turnover

ratio

Cost of Goods Sold /

Average stock

2.19512195

1

1.909090909 1.53061224

Stock

turnover

days

365 / Stock Turnover

ratio

166.277777

8

191.1904762 238.466667

Accounts

receivable

Net Credit sales /

Average accounts

7.69230769

2

5.806451613 4.45945946

Accounting for Managers 6

receivable

Analysis:

i) Profitability ratios:

From the above analysis it is evident that, the profitability of the organization has significantly

decreased over the period of three years. It is se4en that in the year 20X4, the organization had a

good profitability. However, in the next two financial years, the profitability level has gradually

decreased and is a major cause of concern of the organization. This may be due to several factors

like increase in the operation expenses. It is noted that the financial expenses of the organization

has increased significantly in the current financial year. The management of the organization

needs to identify the key issues and accordingly formulate action plan in order to revive from the

current situation (Abu-Bakar et al. 2014).

ii) Liquidity ratios:

On contrary to the profitability level of the organization over the past few years, the liquidity of

the organization has gradually increased. For any organization, the ideal current ratio and quick

ratio is 2:1 and 1.1 respectively. This ratio determines the ability of the organization to

effectively meet its short term obligations. From the analysis made above, it can be apprehended

that, in the current financial year, the liquidity of the organization has increased and is over the

head ratio. This indicates that the organization will face no problem in meeting its short-term

payment obligations (Damodaran, 2016).

iii) Efficiency ratios:

The efficiency ratio helps to determine the ability of an organization to effectively use its assets

in order to generate the maximum revenue. It is evident from the analysis, that the efficiency

ratio of the organization shows a mixed result. It is seen that, the stock turnover ratio of the

organization has decreased over the years. This indicates that, the management is able to

effectively turnover or sale its stock in the market. On the other hand, the stock turnover days

reflects an increasing trend that indicates that the organization is not able to turnover its stocks.

receivable

Analysis:

i) Profitability ratios:

From the above analysis it is evident that, the profitability of the organization has significantly

decreased over the period of three years. It is se4en that in the year 20X4, the organization had a

good profitability. However, in the next two financial years, the profitability level has gradually

decreased and is a major cause of concern of the organization. This may be due to several factors

like increase in the operation expenses. It is noted that the financial expenses of the organization

has increased significantly in the current financial year. The management of the organization

needs to identify the key issues and accordingly formulate action plan in order to revive from the

current situation (Abu-Bakar et al. 2014).

ii) Liquidity ratios:

On contrary to the profitability level of the organization over the past few years, the liquidity of

the organization has gradually increased. For any organization, the ideal current ratio and quick

ratio is 2:1 and 1.1 respectively. This ratio determines the ability of the organization to

effectively meet its short term obligations. From the analysis made above, it can be apprehended

that, in the current financial year, the liquidity of the organization has increased and is over the

head ratio. This indicates that the organization will face no problem in meeting its short-term

payment obligations (Damodaran, 2016).

iii) Efficiency ratios:

The efficiency ratio helps to determine the ability of an organization to effectively use its assets

in order to generate the maximum revenue. It is evident from the analysis, that the efficiency

ratio of the organization shows a mixed result. It is seen that, the stock turnover ratio of the

organization has decreased over the years. This indicates that, the management is able to

effectively turnover or sale its stock in the market. On the other hand, the stock turnover days

reflects an increasing trend that indicates that the organization is not able to turnover its stocks.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting for Managers 7

Additionally, the Accounts receivable days indicates that, the management of the organization is

ineffective in recover the dues from the debtors (Delen, Kuzey & Uyar, 2013).

B) Limitations of the analysis

It is evident that the financial statements of an organization are prepared based on certain

destinations and estimates. Thus, the resultant factors may not be correct in context to the actual

scenario and thus, may mislead the users of the information in making wrong investment

decisions. In addition to that, since the financial reports of an organization are prepared based on

historical financial data, they may not be as useful while corporate planning (Dewachter, Iania,

Lyrio & de Sola Perea, 2015).

C) Additional information in context to the financial analysis

In context to the financial analysis made above, it can be apprehended that the profitability of the

organization has decreased significantly. A comparison of the sales of te4hn year and the net

profit earned has been presented in the form of chart below:

1 2 3

200000

180000 165000

20000 11000 2500

Profitability

Sales for the year Net profit for the year

Figure: Comparison between the sales revenue made and the net profit earned

(Source: Self developed)

Additionally, the Accounts receivable days indicates that, the management of the organization is

ineffective in recover the dues from the debtors (Delen, Kuzey & Uyar, 2013).

B) Limitations of the analysis

It is evident that the financial statements of an organization are prepared based on certain

destinations and estimates. Thus, the resultant factors may not be correct in context to the actual

scenario and thus, may mislead the users of the information in making wrong investment

decisions. In addition to that, since the financial reports of an organization are prepared based on

historical financial data, they may not be as useful while corporate planning (Dewachter, Iania,

Lyrio & de Sola Perea, 2015).

C) Additional information in context to the financial analysis

In context to the financial analysis made above, it can be apprehended that the profitability of the

organization has decreased significantly. A comparison of the sales of te4hn year and the net

profit earned has been presented in the form of chart below:

1 2 3

200000

180000 165000

20000 11000 2500

Profitability

Sales for the year Net profit for the year

Figure: Comparison between the sales revenue made and the net profit earned

(Source: Self developed)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting for Managers 8

From the above diagram, it is noted that, the profitability of the organization has decreased

significantly. This may be due to the increase in the financial expenses of the organization. The

management of the organization needs to conduct a thorough analysis of the financial

requirements of the entity, identify any key issues and accordingly adopt policies that will help

the organization to generate more revenue (El Kasmioui & Ceulemans, 2013).

Conclusion and Recommendations

In light of the analysis made above, it can be established that, analysis of the financial statements

of an organization forms an integral part while making decisions. It helps the management to get

a clear understanding of the current financial position of the organization and thereby make an

evaluation of the performance of the organization. Additionally, it will help the organization to

improve on the key areas.

Question 2

a) Ethical problems faced by Tom:

Facts

It is evident from the case study that, in recent times Allandale Ltd is facing financial insecurity

insights of the events identified. It is noted that, in accordance with their business expansion plan

the organization has procured a loan of $ 20 million. Notably, the loan agreement stated that the

organization must be able to maintain a current ratio of 2:1 and an after-tax return on assets of at

least 10 percent. Failure to comply with the loan agreement at any point of time will compile the

organization to pay back the principal loan amount to the bank. This may lead to significant

financial instability for the organization. Although it is noted that, in the current financial year,

the organization was able to comply with the loan agreement and maintained a current ratio of

2:1 and a return on assets of 11 percent, it is noted that, certain issues have arisen that may

hamper the financial stability of the organization significantly (Johnson, Gruntowicz, Chua &

Morlock, 2015).

Stakeholders

The stakeholders involved here are as follows:

From the above diagram, it is noted that, the profitability of the organization has decreased

significantly. This may be due to the increase in the financial expenses of the organization. The

management of the organization needs to conduct a thorough analysis of the financial

requirements of the entity, identify any key issues and accordingly adopt policies that will help

the organization to generate more revenue (El Kasmioui & Ceulemans, 2013).

Conclusion and Recommendations

In light of the analysis made above, it can be established that, analysis of the financial statements

of an organization forms an integral part while making decisions. It helps the management to get

a clear understanding of the current financial position of the organization and thereby make an

evaluation of the performance of the organization. Additionally, it will help the organization to

improve on the key areas.

Question 2

a) Ethical problems faced by Tom:

Facts

It is evident from the case study that, in recent times Allandale Ltd is facing financial insecurity

insights of the events identified. It is noted that, in accordance with their business expansion plan

the organization has procured a loan of $ 20 million. Notably, the loan agreement stated that the

organization must be able to maintain a current ratio of 2:1 and an after-tax return on assets of at

least 10 percent. Failure to comply with the loan agreement at any point of time will compile the

organization to pay back the principal loan amount to the bank. This may lead to significant

financial instability for the organization. Although it is noted that, in the current financial year,

the organization was able to comply with the loan agreement and maintained a current ratio of

2:1 and a return on assets of 11 percent, it is noted that, certain issues have arisen that may

hamper the financial stability of the organization significantly (Johnson, Gruntowicz, Chua &

Morlock, 2015).

Stakeholders

The stakeholders involved here are as follows:

Accounting for Managers 9

The management of the organization

Tom, the accountant

The Bank

The shareholders of the organization

Problems

In this regards, Tom, the accountant of the organization noted that, an unsold stock of the

organization has a net realizable value of $ 350,000 while the book value of the asset is at $

500,000. Additionally, a debtor of the organization is seen to be facing a financial crisis and

offers to make half payments against their dues of $ 1 million. However, the balance in the

provision for doubtful debt is at $ 300,000. In light of this, the accountant of the organization is

faced with a dilemma of whether to take into consideration of the losses that the organization. In

case Tom recognizes the implications of the issues in the books of accounts, then both the

current ratio as well as the return on assets would reduce significantly and as a result, the

organization will have to pay back the loan amount. This may significantly hamper the

operations of the business and may also lead to loss of jobs for Tom and his best friends.

Notably, the current situation gives rise to ethical implications that Tom needs to consider while

making the decision regarding recognizing the reduction in the net realizable value of the assets

(Kallala et al. 2015).

Values & Principles

The values and the principles involved in relation to the given case study is maintaining a ethical

code of conduct while evaluating the books of accounts of the organization. Tom is faced with an

ethical dilemma of whether to consider the losses incurred by the organization or to alter the

books of accounts in order to cover up the losses. In this regards, Tom needs to adopt ethical

approaches and accordingly make a decision.

b) Recommendations:

Possible Courses of Action

It is noted that Tom has two possible course of action. They include:

Take into consideration the losses incurred by the organization

Alter the books of accounts of the organization

The management of the organization

Tom, the accountant

The Bank

The shareholders of the organization

Problems

In this regards, Tom, the accountant of the organization noted that, an unsold stock of the

organization has a net realizable value of $ 350,000 while the book value of the asset is at $

500,000. Additionally, a debtor of the organization is seen to be facing a financial crisis and

offers to make half payments against their dues of $ 1 million. However, the balance in the

provision for doubtful debt is at $ 300,000. In light of this, the accountant of the organization is

faced with a dilemma of whether to take into consideration of the losses that the organization. In

case Tom recognizes the implications of the issues in the books of accounts, then both the

current ratio as well as the return on assets would reduce significantly and as a result, the

organization will have to pay back the loan amount. This may significantly hamper the

operations of the business and may also lead to loss of jobs for Tom and his best friends.

Notably, the current situation gives rise to ethical implications that Tom needs to consider while

making the decision regarding recognizing the reduction in the net realizable value of the assets

(Kallala et al. 2015).

Values & Principles

The values and the principles involved in relation to the given case study is maintaining a ethical

code of conduct while evaluating the books of accounts of the organization. Tom is faced with an

ethical dilemma of whether to consider the losses incurred by the organization or to alter the

books of accounts in order to cover up the losses. In this regards, Tom needs to adopt ethical

approaches and accordingly make a decision.

b) Recommendations:

Possible Courses of Action

It is noted that Tom has two possible course of action. They include:

Take into consideration the losses incurred by the organization

Alter the books of accounts of the organization

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting for Managers 10

Evaluation of Each Action

If Tom decides to show the implications in the books of accounts of the organization, then not

only it will lead to bankruptcy of the organization but may also lead Tom and his friends to loss

their job. However, as an accountant of an organization, he must be ethical in his practices and

always deter from frauds or material misstatements in the books of accounts.

Principles & Consequences Raised

In light of the issues identified above, it can be established that, the current financial instability

of Allandale Ltd has lead to ethical obligations that needs to be considered while making any

significant decision. In context to this, Tom is faced with two options. He can either recognize

the reduction is the net realizable value of the identified assets or he can just simply alter the

books of accounts as per the needs of the organization (Kou, Peng & Wang, 2014).

Choose a Plan

It would be feasible for Tom to recognize the reduction in net realizable value of the assets in the

books of accounts of the organization (Nesticò & Pipolo, 2015).

Justification for Selection

Apparently it may seem that, Tom must alter the books of accounts of the organization in order

to save it from indebtedness. However, manipulation of the books of accounts of the organization

is not an ethical practice and may alter the credibility of the organization. In this regards, it is

feasible for Tom to report the losses in the books of accounts.

Question 3

Types of accounting software to be designed by Giggling Brothers

In light of the light of the complexity in the business process, organizations need to maintain

extensive system of records and other documents. In case of manual record of data, there remains

a probability of misstatements in the financial reports or improper recording of the information.

In addition to that, if the records of the organization are not maintained safely, then in that case it

may lead to serious implications and may hamper the business operations significantly (Vogel,

2014). It is noted that, Giggling Brothers in recent times are facing certain difficulties in regards

Evaluation of Each Action

If Tom decides to show the implications in the books of accounts of the organization, then not

only it will lead to bankruptcy of the organization but may also lead Tom and his friends to loss

their job. However, as an accountant of an organization, he must be ethical in his practices and

always deter from frauds or material misstatements in the books of accounts.

Principles & Consequences Raised

In light of the issues identified above, it can be established that, the current financial instability

of Allandale Ltd has lead to ethical obligations that needs to be considered while making any

significant decision. In context to this, Tom is faced with two options. He can either recognize

the reduction is the net realizable value of the identified assets or he can just simply alter the

books of accounts as per the needs of the organization (Kou, Peng & Wang, 2014).

Choose a Plan

It would be feasible for Tom to recognize the reduction in net realizable value of the assets in the

books of accounts of the organization (Nesticò & Pipolo, 2015).

Justification for Selection

Apparently it may seem that, Tom must alter the books of accounts of the organization in order

to save it from indebtedness. However, manipulation of the books of accounts of the organization

is not an ethical practice and may alter the credibility of the organization. In this regards, it is

feasible for Tom to report the losses in the books of accounts.

Question 3

Types of accounting software to be designed by Giggling Brothers

In light of the light of the complexity in the business process, organizations need to maintain

extensive system of records and other documents. In case of manual record of data, there remains

a probability of misstatements in the financial reports or improper recording of the information.

In addition to that, if the records of the organization are not maintained safely, then in that case it

may lead to serious implications and may hamper the business operations significantly (Vogel,

2014). It is noted that, Giggling Brothers in recent times are facing certain difficulties in regards

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting for Managers 11

to proper maintenance of records and data. In view of this, it would be feasible for the

organization to opt for computerized accounting system that would facilitate the management to

keep proper records of large amount data and information. ERP is noted to be widely used

software especially among small organization. Adopting of computerized software like that of

ERP with not only help the organization to maintain accurate data but maintain an extensive

reporting system of a large database (Stone et al. 2016).

Benefits of the system and its incorporation with the planning process

It is seen that, there lies an interdepartmental conflict within the organizational structure of

Giggling Brothers. Notably, due to lack of availability of proper information from the accounting

the other departments of the organizations tend to suffer and sometimes significantly hamper

their operations. In this regard, it would be feasible for v tech organization to adopt ERP san

integrated accounting software (Vogel, 2014). This would benefit the organization in several

ways and will help to reduce the interdepartmental conflicts. In addition to that, this would help

the management in ensuring smooth flow of information within the organization. This in turn

would facilitate smooth running of the business operations of the organizations. Additionally, it

would help the organization enhance the visibility of the information, maintain an automated

workflow, prevalence of a single reporting system, proper unification of data and reduce the

operational costs of the organization. Adoption of ERP will help the management to maintain a

level of efficiency among all the departments of the organization as well as make forecasts about

the future and thereby, formulate policies in order to avoid any contingencies (Yarbro &

Mehlenbeck, 2015).

Recommendations for Giggling Brothers for implementation of new system

It is noted that, there lies certain organizational disputes within the organization structure of

Giggling brothers. This not only affects the operations of the department but also leads to

hampering of the operations as a whole. It is seen that, the account department of the

organization are not able to effectively maintain proper records of the financial data. Thus,

providing wrong information to other departments of the organization might lead to ambiguity

and at certain times intra-organizational conflicts. In this regards, it is recommended to the

management of the organization to implement computerized accounting system. In this context,

they needs to conduct a market research in order to gather information about the best available

to proper maintenance of records and data. In view of this, it would be feasible for the

organization to opt for computerized accounting system that would facilitate the management to

keep proper records of large amount data and information. ERP is noted to be widely used

software especially among small organization. Adopting of computerized software like that of

ERP with not only help the organization to maintain accurate data but maintain an extensive

reporting system of a large database (Stone et al. 2016).

Benefits of the system and its incorporation with the planning process

It is seen that, there lies an interdepartmental conflict within the organizational structure of

Giggling Brothers. Notably, due to lack of availability of proper information from the accounting

the other departments of the organizations tend to suffer and sometimes significantly hamper

their operations. In this regard, it would be feasible for v tech organization to adopt ERP san

integrated accounting software (Vogel, 2014). This would benefit the organization in several

ways and will help to reduce the interdepartmental conflicts. In addition to that, this would help

the management in ensuring smooth flow of information within the organization. This in turn

would facilitate smooth running of the business operations of the organizations. Additionally, it

would help the organization enhance the visibility of the information, maintain an automated

workflow, prevalence of a single reporting system, proper unification of data and reduce the

operational costs of the organization. Adoption of ERP will help the management to maintain a

level of efficiency among all the departments of the organization as well as make forecasts about

the future and thereby, formulate policies in order to avoid any contingencies (Yarbro &

Mehlenbeck, 2015).

Recommendations for Giggling Brothers for implementation of new system

It is noted that, there lies certain organizational disputes within the organization structure of

Giggling brothers. This not only affects the operations of the department but also leads to

hampering of the operations as a whole. It is seen that, the account department of the

organization are not able to effectively maintain proper records of the financial data. Thus,

providing wrong information to other departments of the organization might lead to ambiguity

and at certain times intra-organizational conflicts. In this regards, it is recommended to the

management of the organization to implement computerized accounting system. In this context,

they needs to conduct a market research in order to gather information about the best available

Accounting for Managers 12

accounting software and select the best possible that meets the requirements of the organization

(Johnson, Gruntowicz, Chua & Morlock, 2015).

Stakeholders involvement in the development of new system

For any organizations, it is very important to cater to the needs and the expectations of the

various stakeholders of the organization. The primary stakeholders of an organization are its

shareholders and thus, it is important for the management of the organization to look after the

needs and demands of the shareholders (Vogel, 2014). In regards to the proposed plan of

Giggling Brothers, the stakeholders that needs to be included in the development and

implementation of the new accounting system includes, the shareholders of the organization, the

board of directors of the organization, the employees of all the department and the management.

In addition to that, the management of the organization need to take into consideration the

suggestions of the shareholders of the organization as well as the board of directors and

accordingly formulates policies for the implementation of the proposed plan. This would help the

management of the organization in effective implementation of the new computerized

accounting system (Nesticò & Pipolo, 2015).

Competitors analysis for Giggling Brothers

Using Accounting would be of great help to the Giggling Brothers that may help the company to

work in an effective way and know the works that are being done by the competitors of the

company. The software would be helpful in maintaining the accounting performance of the

company, knowing the strategies and the software that are being done by the other companies

(Delen, Kuzey & Uyar, 2013). Wine supplies that are being made by the companies are to be

well maintained and would need to be recorded on a daily basis, working on manual terms may

cause conflict within the companies as it may happen that the records may not be recorded in an

effective way and every branch of a company may go through different calculations that may be

hard for the company to calculate the works that are being done. In this way using a same type of

software may help the company to work in an effective manner and calculations that are being

done would be equal and good for the company to work effectively (El Kasmioui & Ceulemans,

2013).

accounting software and select the best possible that meets the requirements of the organization

(Johnson, Gruntowicz, Chua & Morlock, 2015).

Stakeholders involvement in the development of new system

For any organizations, it is very important to cater to the needs and the expectations of the

various stakeholders of the organization. The primary stakeholders of an organization are its

shareholders and thus, it is important for the management of the organization to look after the

needs and demands of the shareholders (Vogel, 2014). In regards to the proposed plan of

Giggling Brothers, the stakeholders that needs to be included in the development and

implementation of the new accounting system includes, the shareholders of the organization, the

board of directors of the organization, the employees of all the department and the management.

In addition to that, the management of the organization need to take into consideration the

suggestions of the shareholders of the organization as well as the board of directors and

accordingly formulates policies for the implementation of the proposed plan. This would help the

management of the organization in effective implementation of the new computerized

accounting system (Nesticò & Pipolo, 2015).

Competitors analysis for Giggling Brothers

Using Accounting would be of great help to the Giggling Brothers that may help the company to

work in an effective way and know the works that are being done by the competitors of the

company. The software would be helpful in maintaining the accounting performance of the

company, knowing the strategies and the software that are being done by the other companies

(Delen, Kuzey & Uyar, 2013). Wine supplies that are being made by the companies are to be

well maintained and would need to be recorded on a daily basis, working on manual terms may

cause conflict within the companies as it may happen that the records may not be recorded in an

effective way and every branch of a company may go through different calculations that may be

hard for the company to calculate the works that are being done. In this way using a same type of

software may help the company to work in an effective manner and calculations that are being

done would be equal and good for the company to work effectively (El Kasmioui & Ceulemans,

2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.