Corporate Accounting Report Analysis: Tax Treatment of a Company

VerifiedAdded on 2020/05/16

|11

|1942

|303

Report

AI Summary

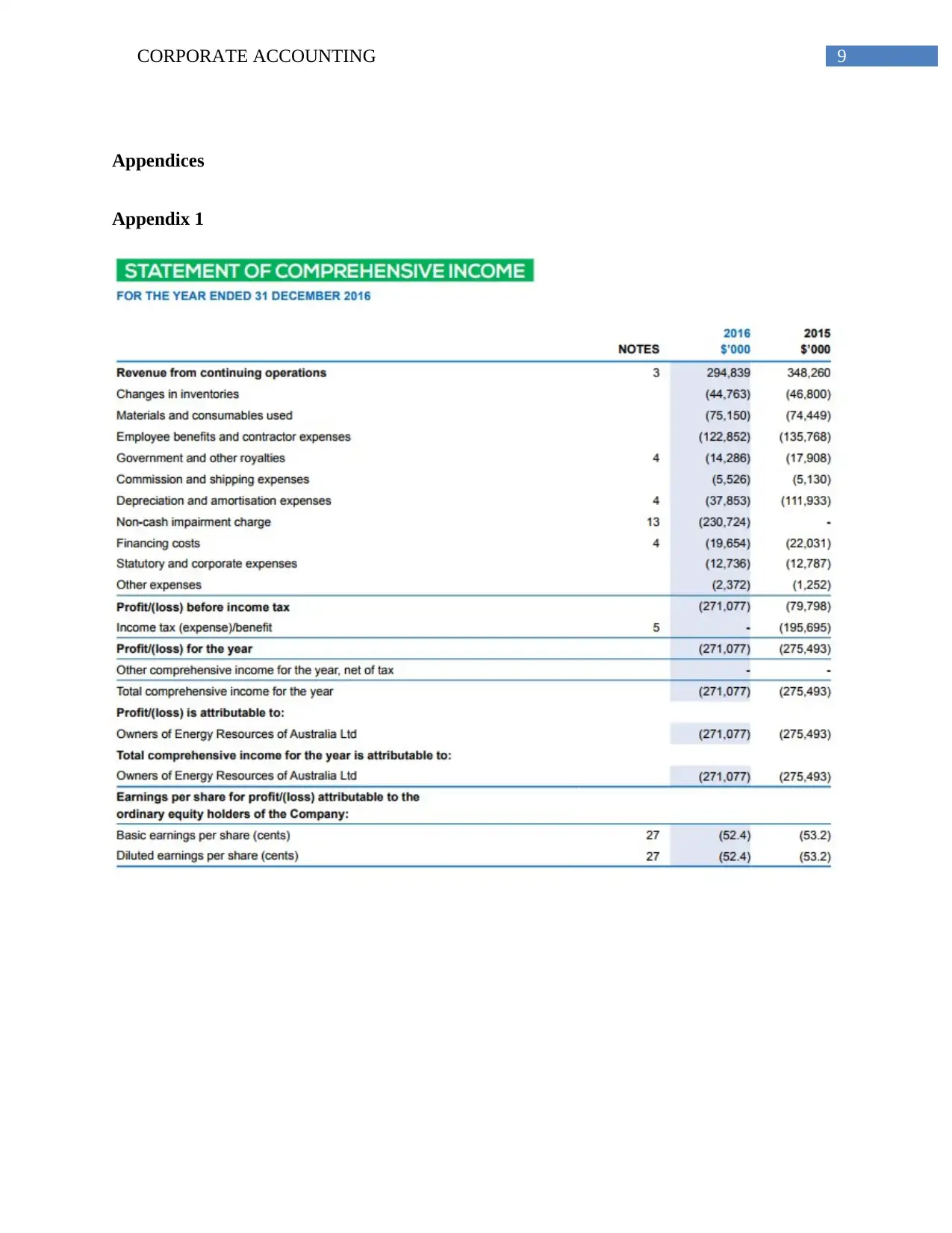

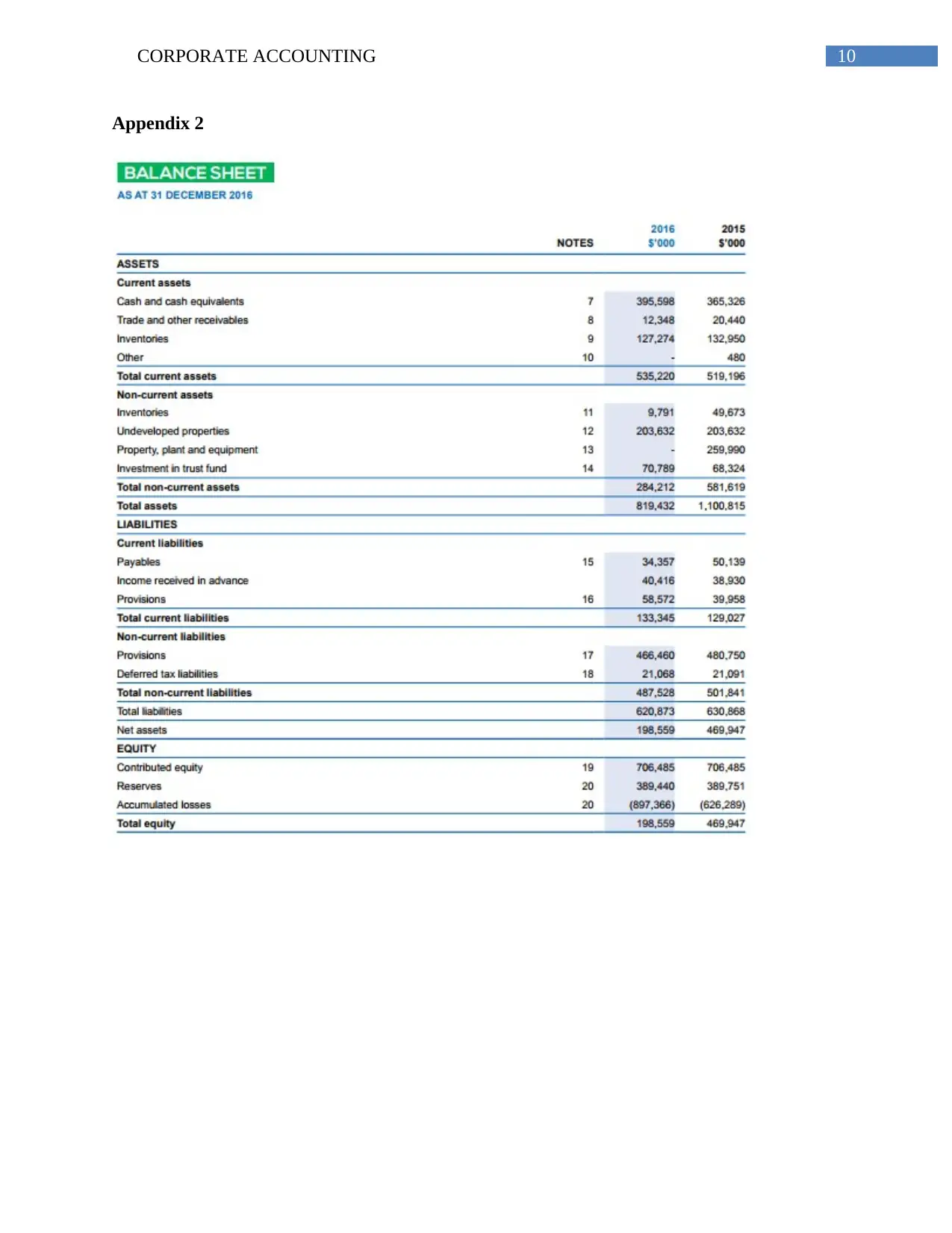

This report provides a comprehensive analysis of a corporate accounting report, focusing on the financial statements of Energy Resources Australia Ltd. The report examines key components of the balance sheet, including equity (reserves, retained earnings, and issued capital), and analyzes the company's earnings per share. It delves into the treatment of tax expenses, comparing the calculated tax expenses with the actual tax expenses recorded in the financial statements, and explores potential reasons for any discrepancies, such as differences in tax rates and amortization. The report also investigates deferred tax liabilities and assets, highlighting their significance in corporate tax management. Furthermore, the report addresses the treatment of current tax assets and liabilities, and how income tax expenses are presented in both the statement of income and the cash flow statement. Finally, the analysis concludes by summarizing the company's tax practices, noting areas of potential confusion and the importance of proper reconciliation and understanding of international tax rates.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.