Comprehensive Business Accounting Assignment: Financial Analysis

VerifiedAdded on 2021/02/20

|15

|3090

|35

Homework Assignment

AI Summary

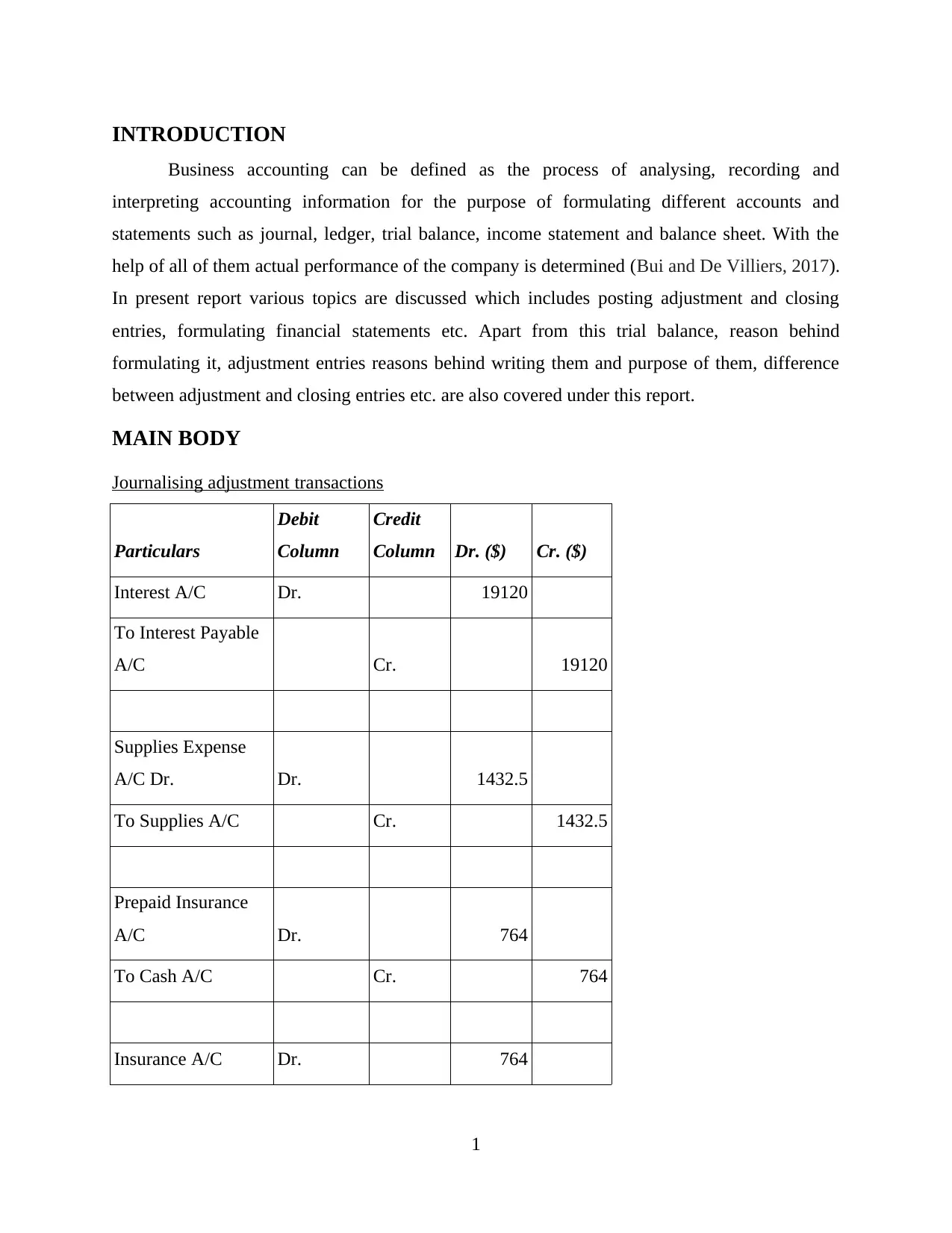

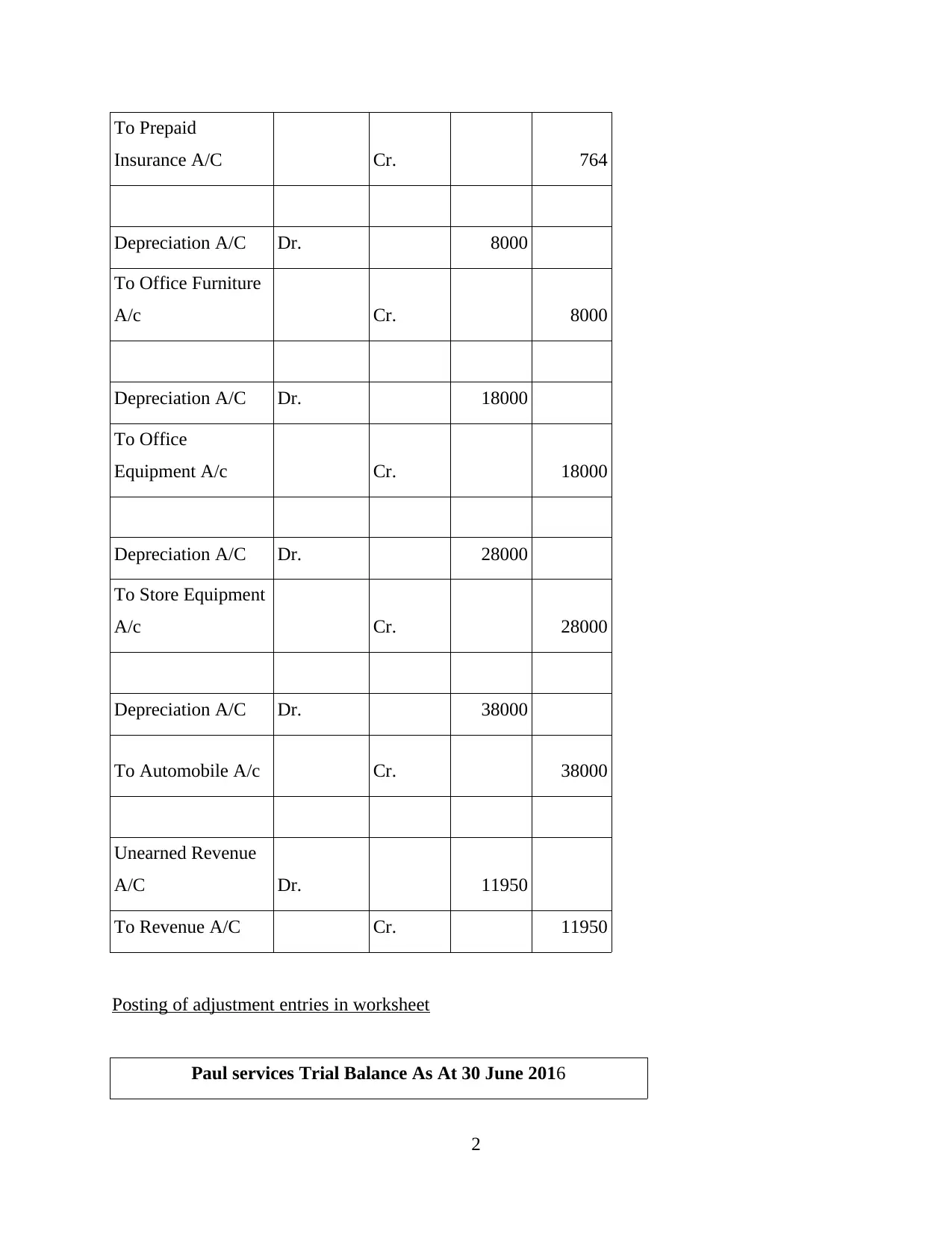

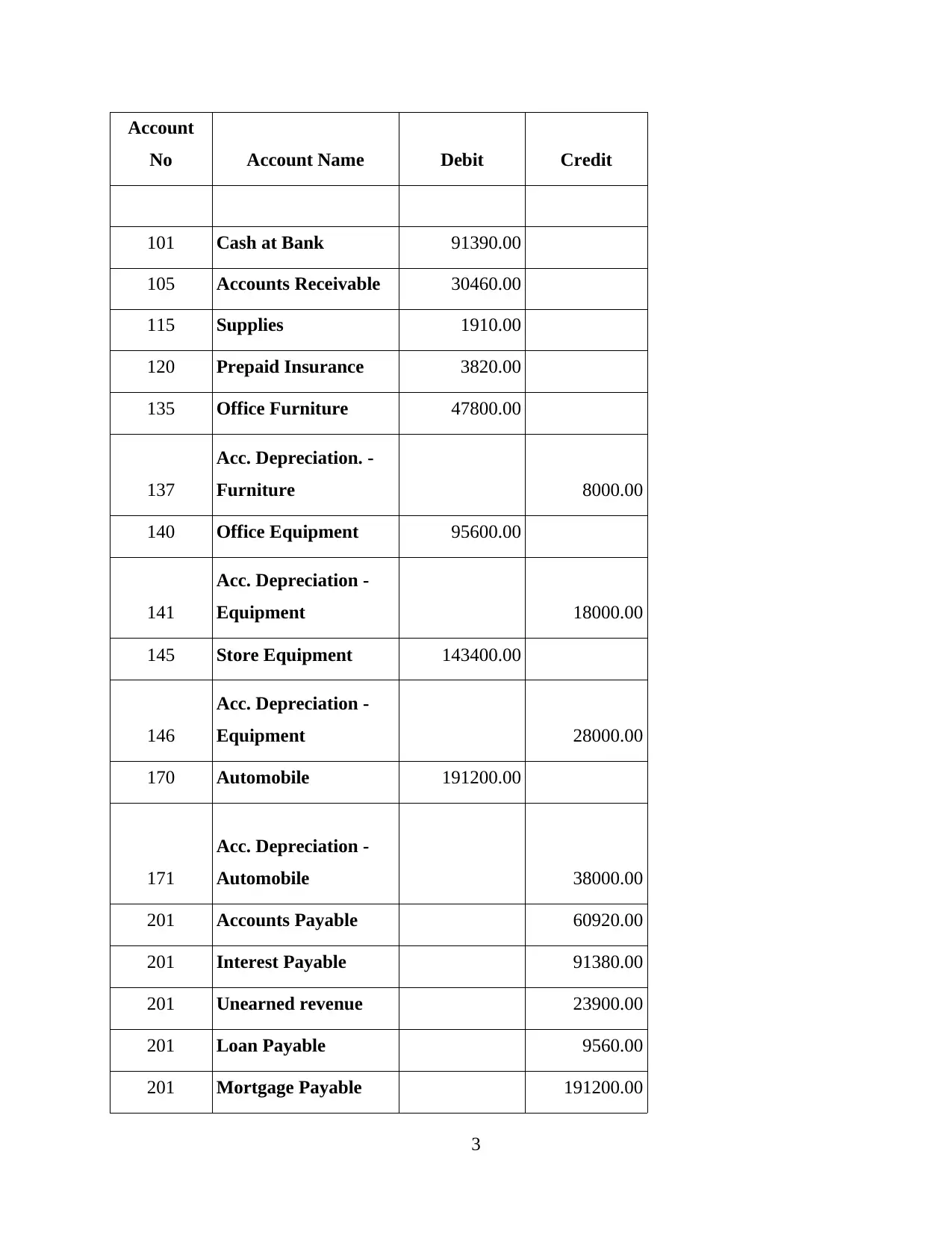

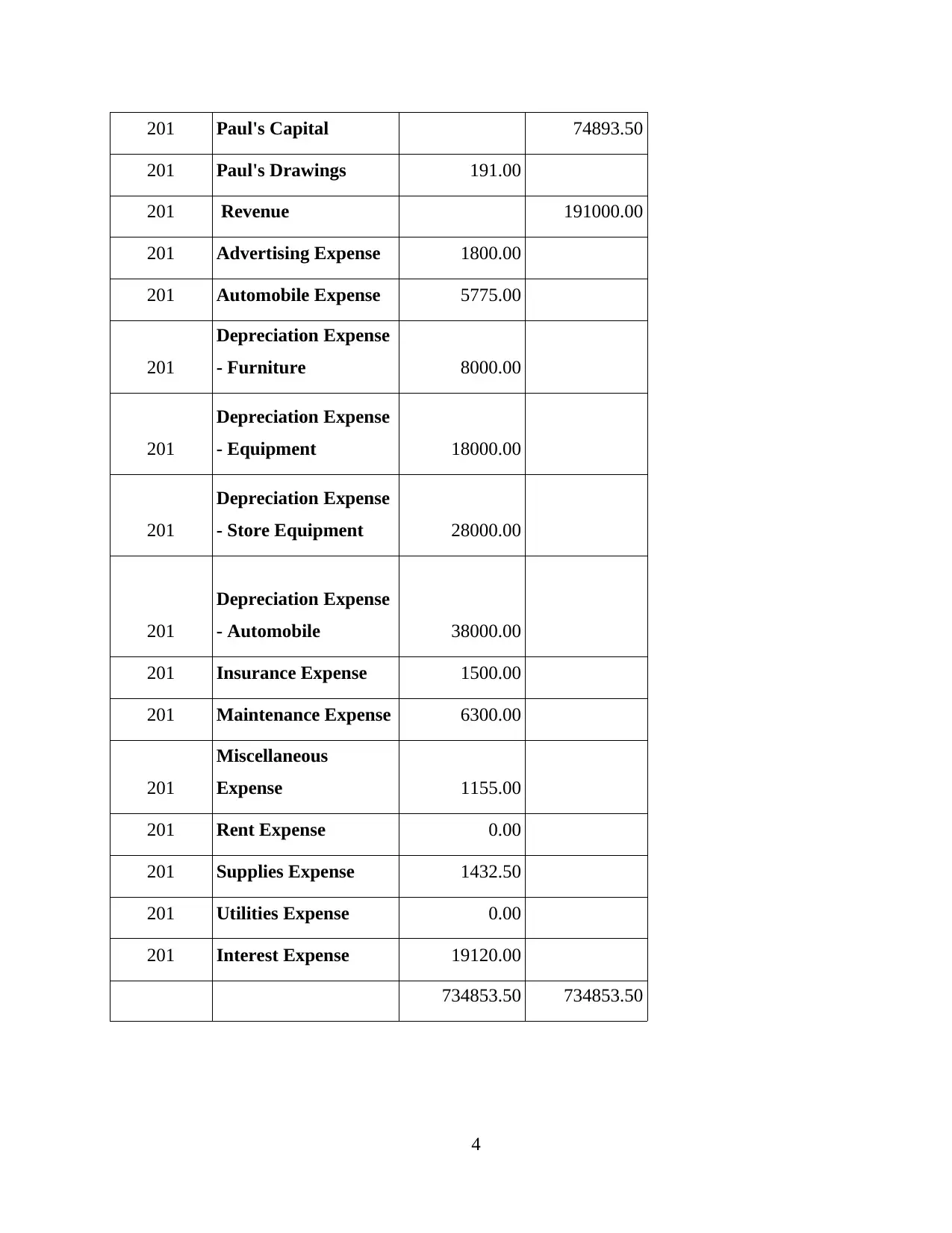

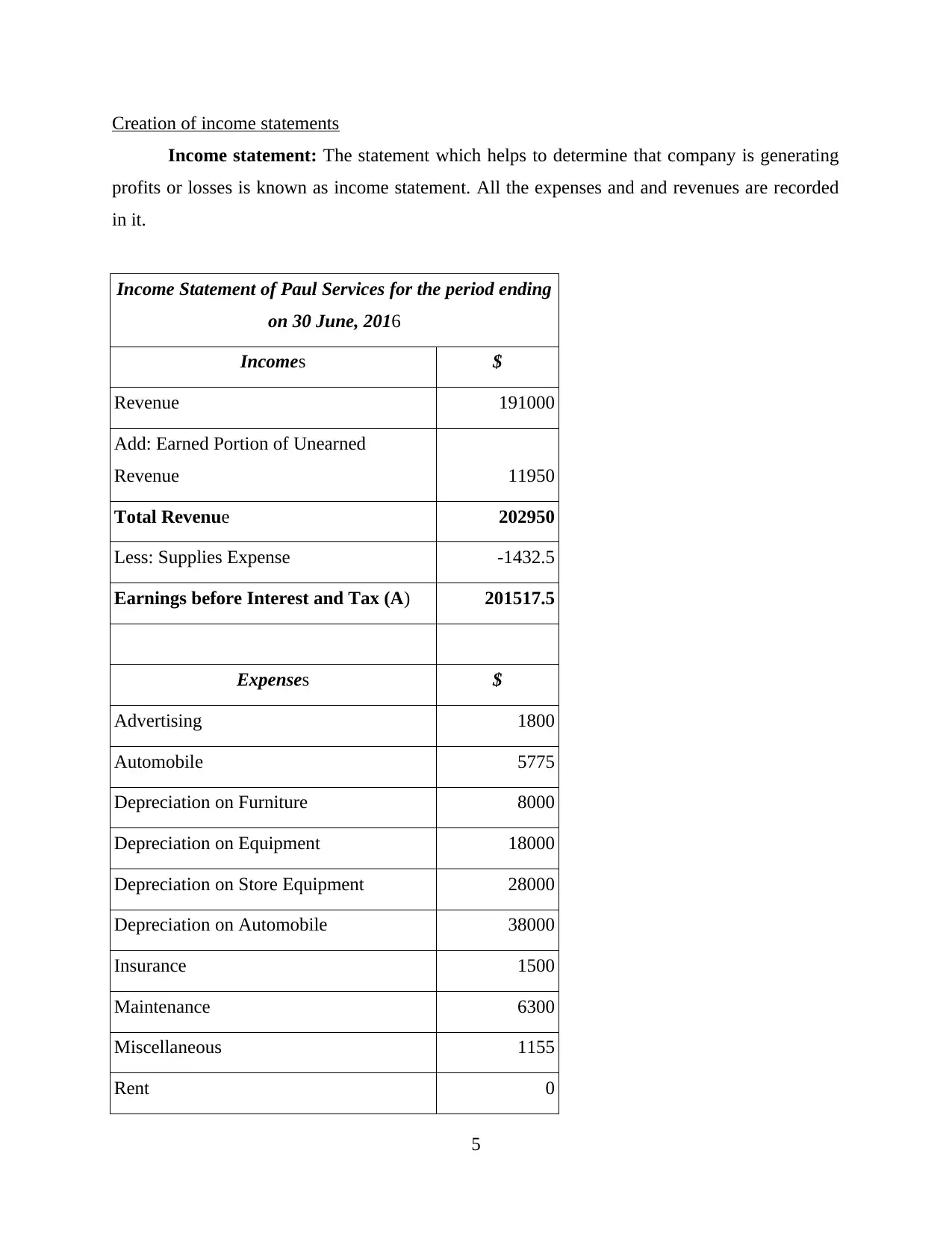

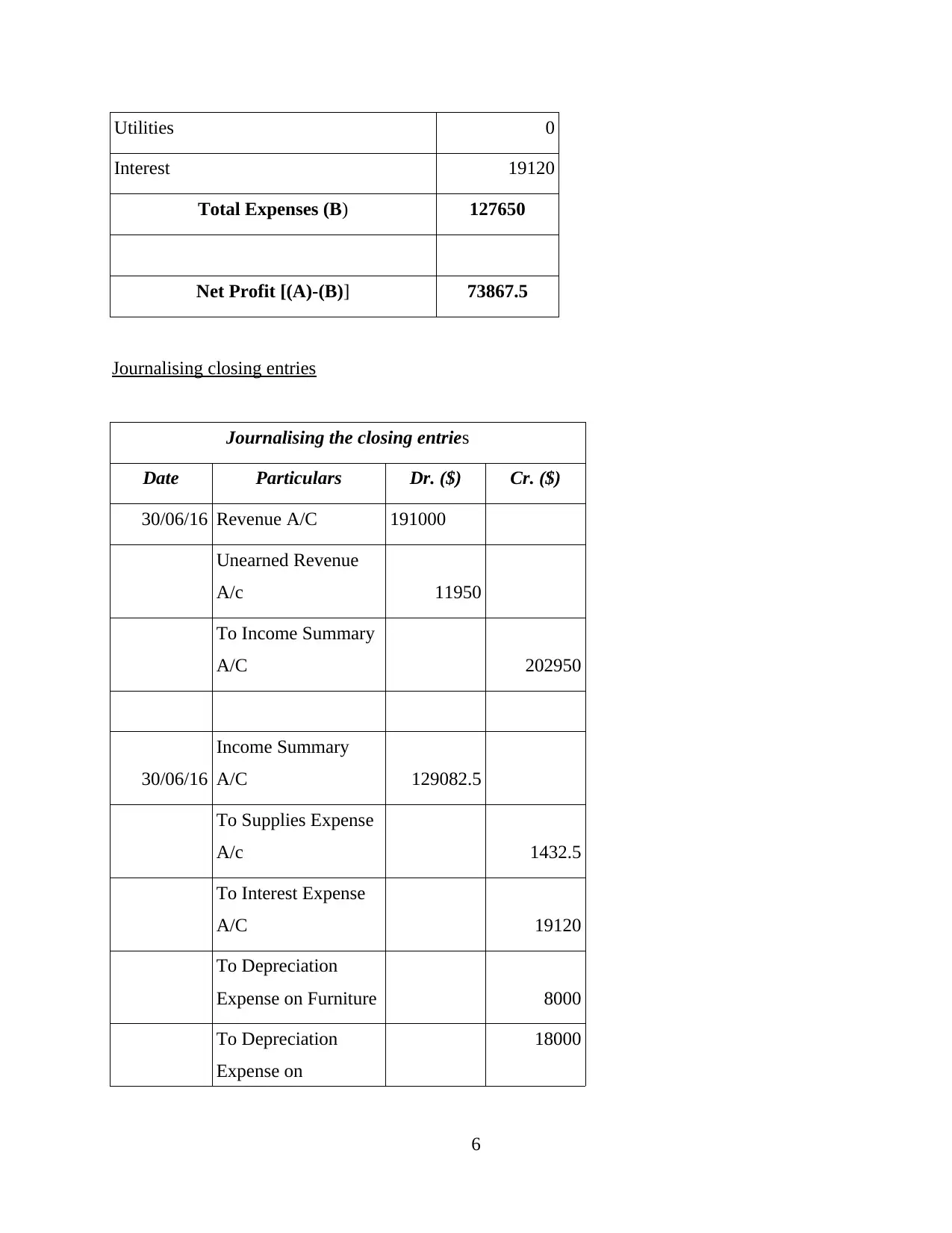

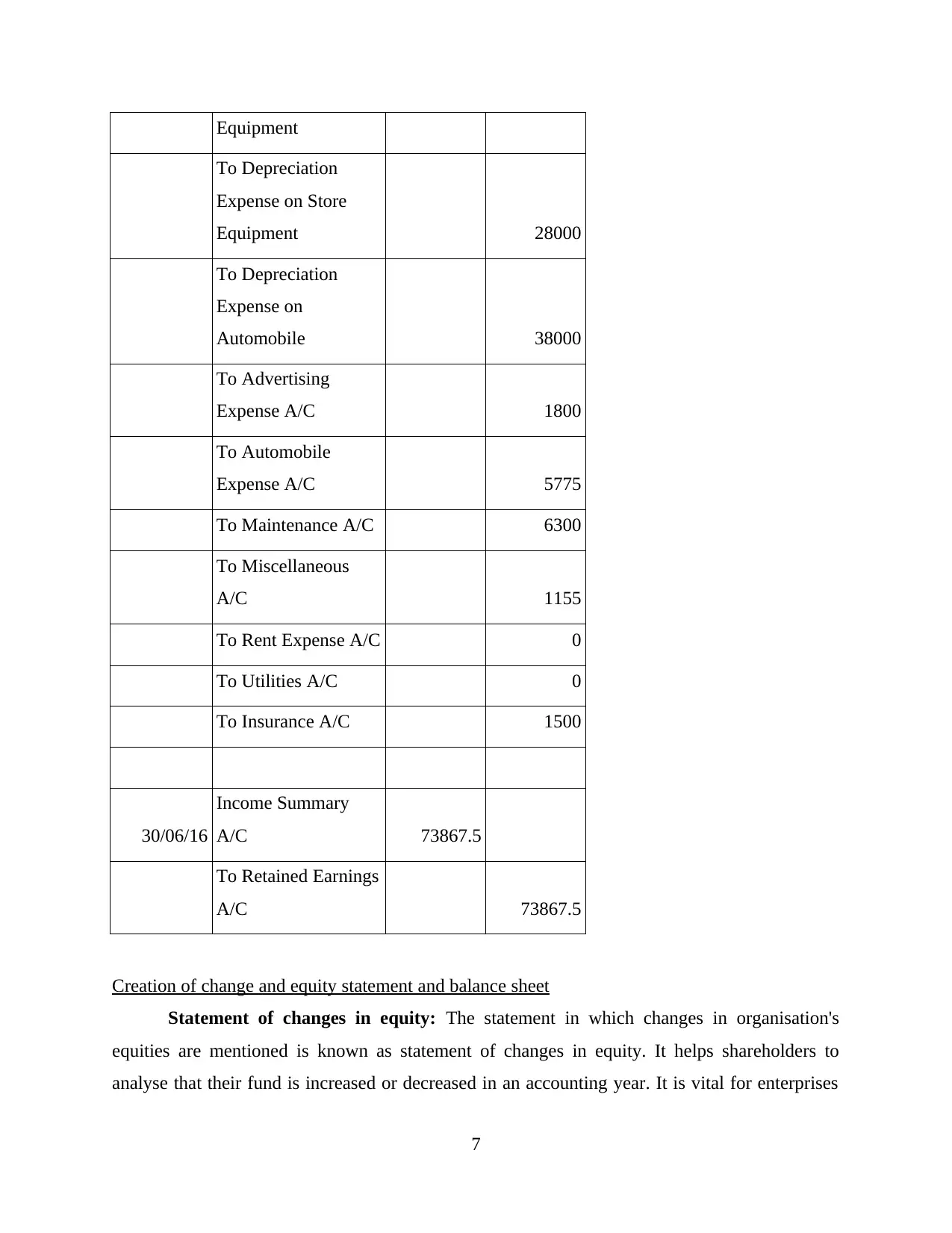

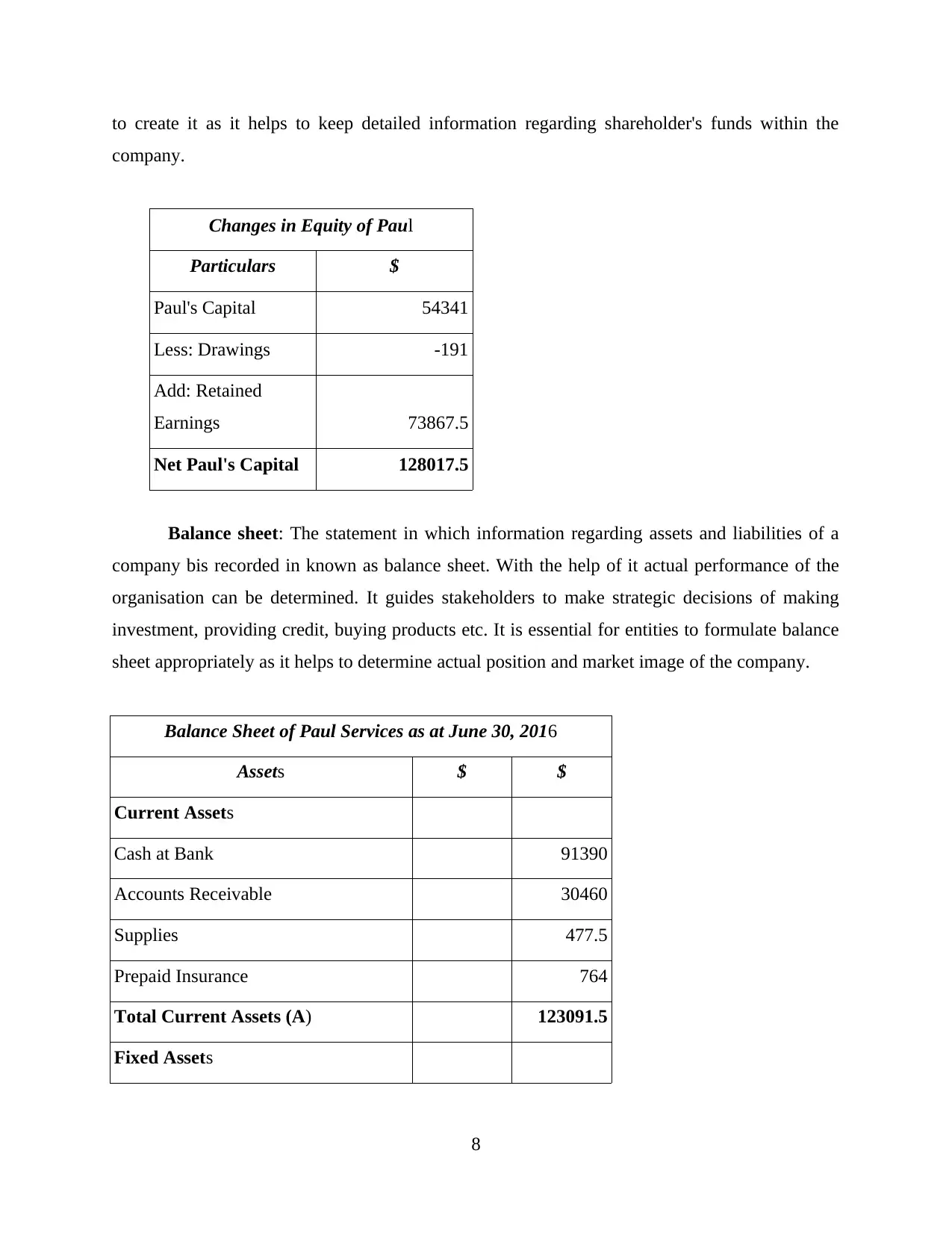

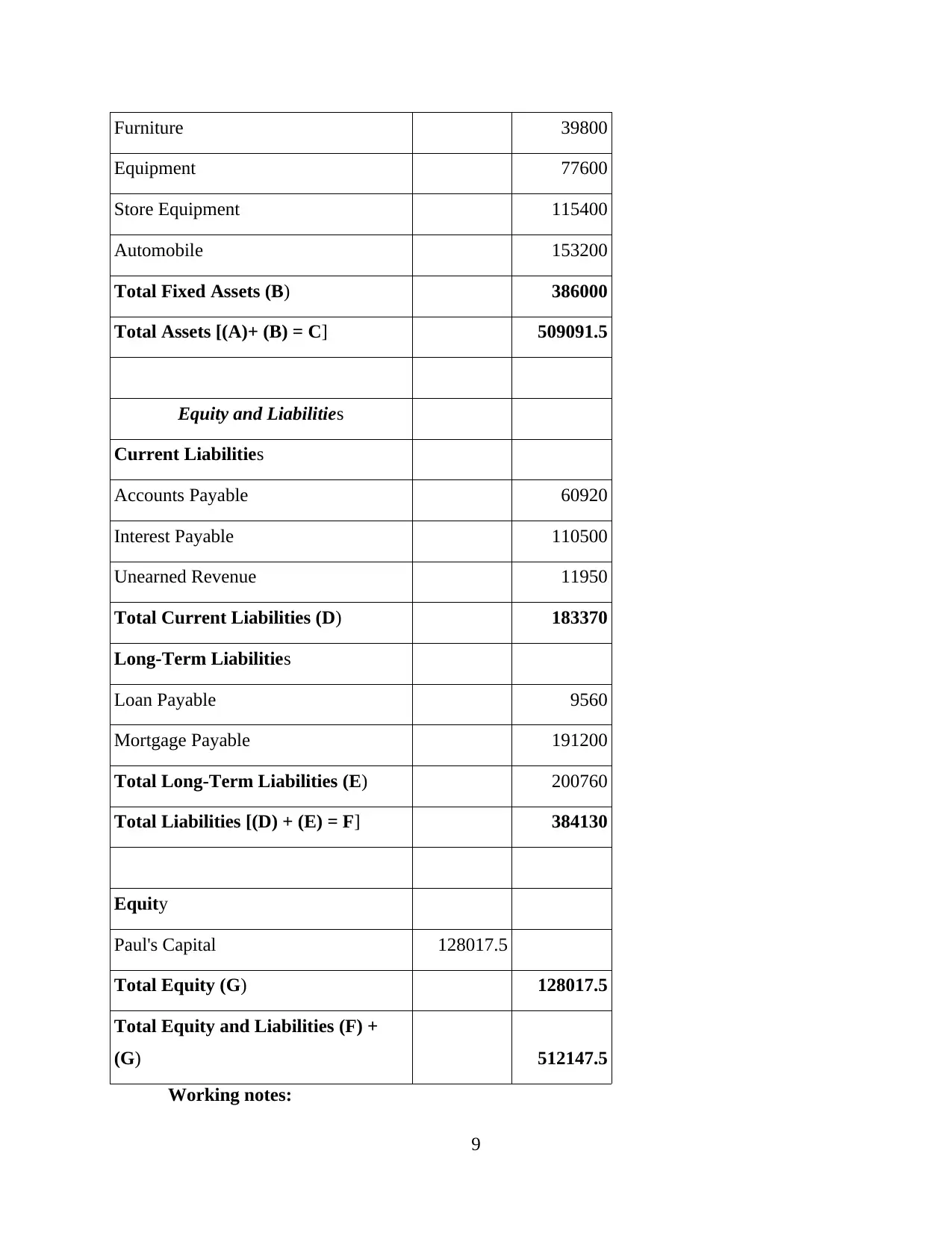

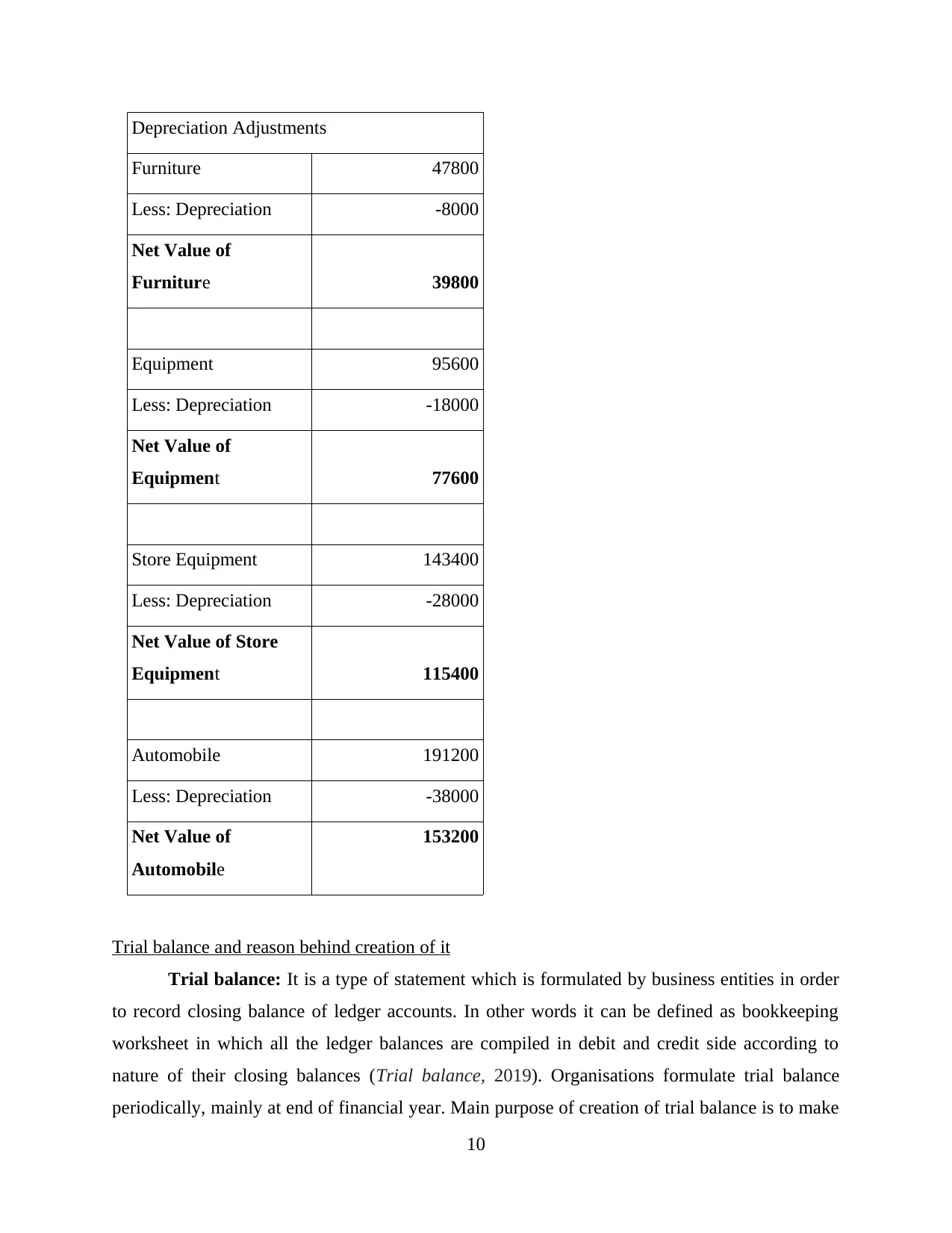

This assignment provides a detailed analysis of business accounting principles. It begins with journalizing adjustment transactions, including interest, supplies, prepaid insurance, depreciation, and unearned revenue. The solution then demonstrates the posting of these adjustments into a worksheet, followed by the creation of an income statement, journalizing closing entries, and constructing a statement of changes in equity and a balance sheet. The assignment also explains the trial balance, its purpose, and the reasons behind its creation, along with the rationale for adjustment entries and their purpose. It clarifies the difference between adjustment and closing journal entries, providing a complete understanding of the accounting cycle. The assignment covers various financial aspects of a company, including assets, liabilities, and equity, and how they are reflected in financial statements. The document is contributed by a student to be published on the website Desklib. Desklib is a platform which provides all the necessary AI based study tools for students.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.