Accounting Fundamentals: Financial Reporting and Analysis Assignment

VerifiedAdded on 2023/01/10

|13

|3280

|30

Homework Assignment

AI Summary

This document presents a comprehensive solution to an accounting fundamentals assignment. It begins with journal entries for Sandrolia Limited, followed by an updated trial balance and the preparation of profit and loss account and statement of financial position. The assignment then proceeds with similar tasks for Ricardo Limited, including journal entries, trial balance, and financial statement preparation. The solution includes an analysis of the relevance of financial information for various users, such as investors, management, and government entities. Finally, it provides a comparison and contrast of liquidity and profitability, explaining their significance in financial analysis. The document covers key aspects of financial accounting including recording transactions, preparing financial statements, and understanding key financial concepts.

Accounting Fundamentals

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK 1...................................................................................................................................3

Journal Entries in the books of Sandrolia Limited:................................................................3

Updated trial balance of Sandrolia Limited:..........................................................................4

Preparation of profit and loss account and statement of financial position of Sandrolia

Limited:..................................................................................................................................5

TASK 2...................................................................................................................................6

TASK 3...................................................................................................................................6

Completion of Journal entries in the books of Ricardo Limited:...........................................6

Drawing up Updated trial balance of Ricardo Limited:.........................................................7

Preparation of profit and loss account and statement of financial position of Ricardo Limited:

................................................................................................................................................8

TASK 4. Comparing and contrasting liquidity and profitability:...........................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK 1...................................................................................................................................3

Journal Entries in the books of Sandrolia Limited:................................................................3

Updated trial balance of Sandrolia Limited:..........................................................................4

Preparation of profit and loss account and statement of financial position of Sandrolia

Limited:..................................................................................................................................5

TASK 2...................................................................................................................................6

TASK 3...................................................................................................................................6

Completion of Journal entries in the books of Ricardo Limited:...........................................6

Drawing up Updated trial balance of Ricardo Limited:.........................................................7

Preparation of profit and loss account and statement of financial position of Ricardo Limited:

................................................................................................................................................8

TASK 4. Comparing and contrasting liquidity and profitability:...........................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

The current era is age of trading and business. Following globalization, liberalization, and

outsourcing, from day to day business becomes rising and being dynamic as well. An

organisation, for long time, can't remember all dealings and financial events. Hence, keeping a

registered record of any and all commercial transactions with each day becomes important, this

leads to accounting growth. Accounting relates to process which helps to document, sum up,

monitor and evaluate financial transaction related information (Ogneva, Piotroski and

Zakolyukina, 2019). The study covers critical aspects of accounting with help of different tasks

which also includes practical sum of recoding transactions, preparing accounts and finalisation of

annual accounts like profit and loss statement, financial position statement etc. Further it

discusses about principle objects of financial reporting and way to attain transparent as well as

uniform accounting. Moreover, study critically evaluates difference between liquidity and

profitability.

MAIN BODY

TASK 1.

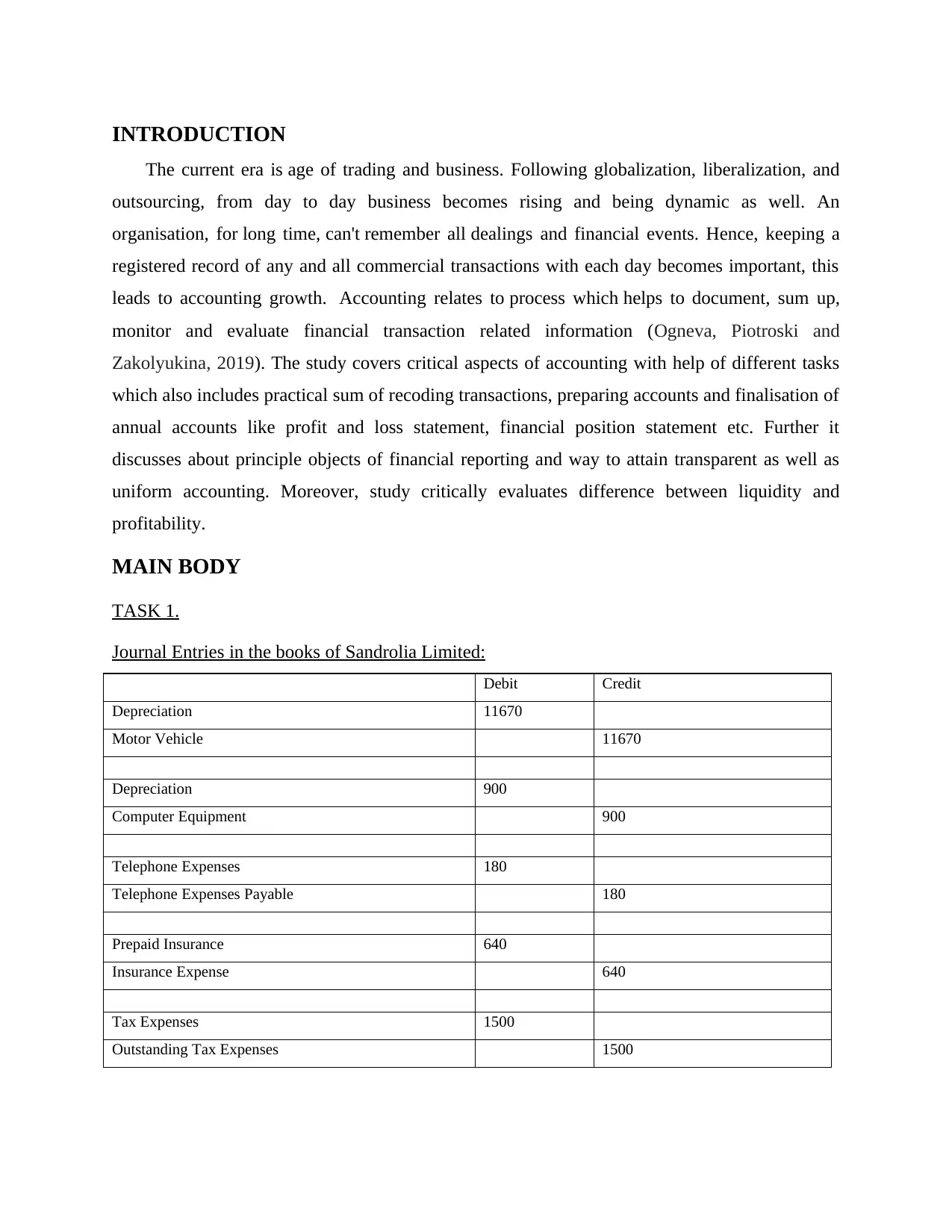

Journal Entries in the books of Sandrolia Limited:

Debit Credit

Depreciation 11670

Motor Vehicle 11670

Depreciation 900

Computer Equipment 900

Telephone Expenses 180

Telephone Expenses Payable 180

Prepaid Insurance 640

Insurance Expense 640

Tax Expenses 1500

Outstanding Tax Expenses 1500

The current era is age of trading and business. Following globalization, liberalization, and

outsourcing, from day to day business becomes rising and being dynamic as well. An

organisation, for long time, can't remember all dealings and financial events. Hence, keeping a

registered record of any and all commercial transactions with each day becomes important, this

leads to accounting growth. Accounting relates to process which helps to document, sum up,

monitor and evaluate financial transaction related information (Ogneva, Piotroski and

Zakolyukina, 2019). The study covers critical aspects of accounting with help of different tasks

which also includes practical sum of recoding transactions, preparing accounts and finalisation of

annual accounts like profit and loss statement, financial position statement etc. Further it

discusses about principle objects of financial reporting and way to attain transparent as well as

uniform accounting. Moreover, study critically evaluates difference between liquidity and

profitability.

MAIN BODY

TASK 1.

Journal Entries in the books of Sandrolia Limited:

Debit Credit

Depreciation 11670

Motor Vehicle 11670

Depreciation 900

Computer Equipment 900

Telephone Expenses 180

Telephone Expenses Payable 180

Prepaid Insurance 640

Insurance Expense 640

Tax Expenses 1500

Outstanding Tax Expenses 1500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

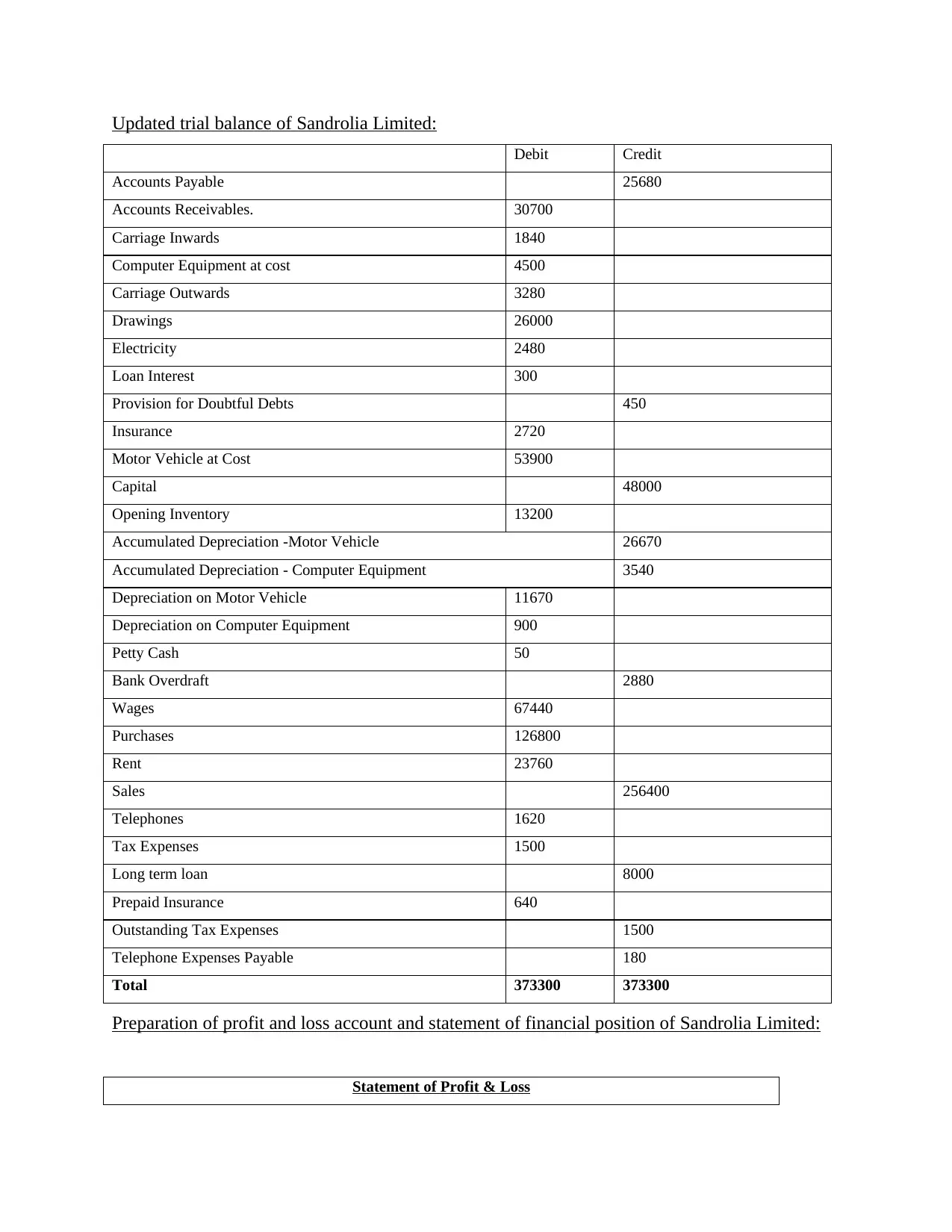

Updated trial balance of Sandrolia Limited:

Debit Credit

Accounts Payable 25680

Accounts Receivables. 30700

Carriage Inwards 1840

Computer Equipment at cost 4500

Carriage Outwards 3280

Drawings 26000

Electricity 2480

Loan Interest 300

Provision for Doubtful Debts 450

Insurance 2720

Motor Vehicle at Cost 53900

Capital 48000

Opening Inventory 13200

Accumulated Depreciation -Motor Vehicle 26670

Accumulated Depreciation - Computer Equipment 3540

Depreciation on Motor Vehicle 11670

Depreciation on Computer Equipment 900

Petty Cash 50

Bank Overdraft 2880

Wages 67440

Purchases 126800

Rent 23760

Sales 256400

Telephones 1620

Tax Expenses 1500

Long term loan 8000

Prepaid Insurance 640

Outstanding Tax Expenses 1500

Telephone Expenses Payable 180

Total 373300 373300

Preparation of profit and loss account and statement of financial position of Sandrolia Limited:

Statement of Profit & Loss

Debit Credit

Accounts Payable 25680

Accounts Receivables. 30700

Carriage Inwards 1840

Computer Equipment at cost 4500

Carriage Outwards 3280

Drawings 26000

Electricity 2480

Loan Interest 300

Provision for Doubtful Debts 450

Insurance 2720

Motor Vehicle at Cost 53900

Capital 48000

Opening Inventory 13200

Accumulated Depreciation -Motor Vehicle 26670

Accumulated Depreciation - Computer Equipment 3540

Depreciation on Motor Vehicle 11670

Depreciation on Computer Equipment 900

Petty Cash 50

Bank Overdraft 2880

Wages 67440

Purchases 126800

Rent 23760

Sales 256400

Telephones 1620

Tax Expenses 1500

Long term loan 8000

Prepaid Insurance 640

Outstanding Tax Expenses 1500

Telephone Expenses Payable 180

Total 373300 373300

Preparation of profit and loss account and statement of financial position of Sandrolia Limited:

Statement of Profit & Loss

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

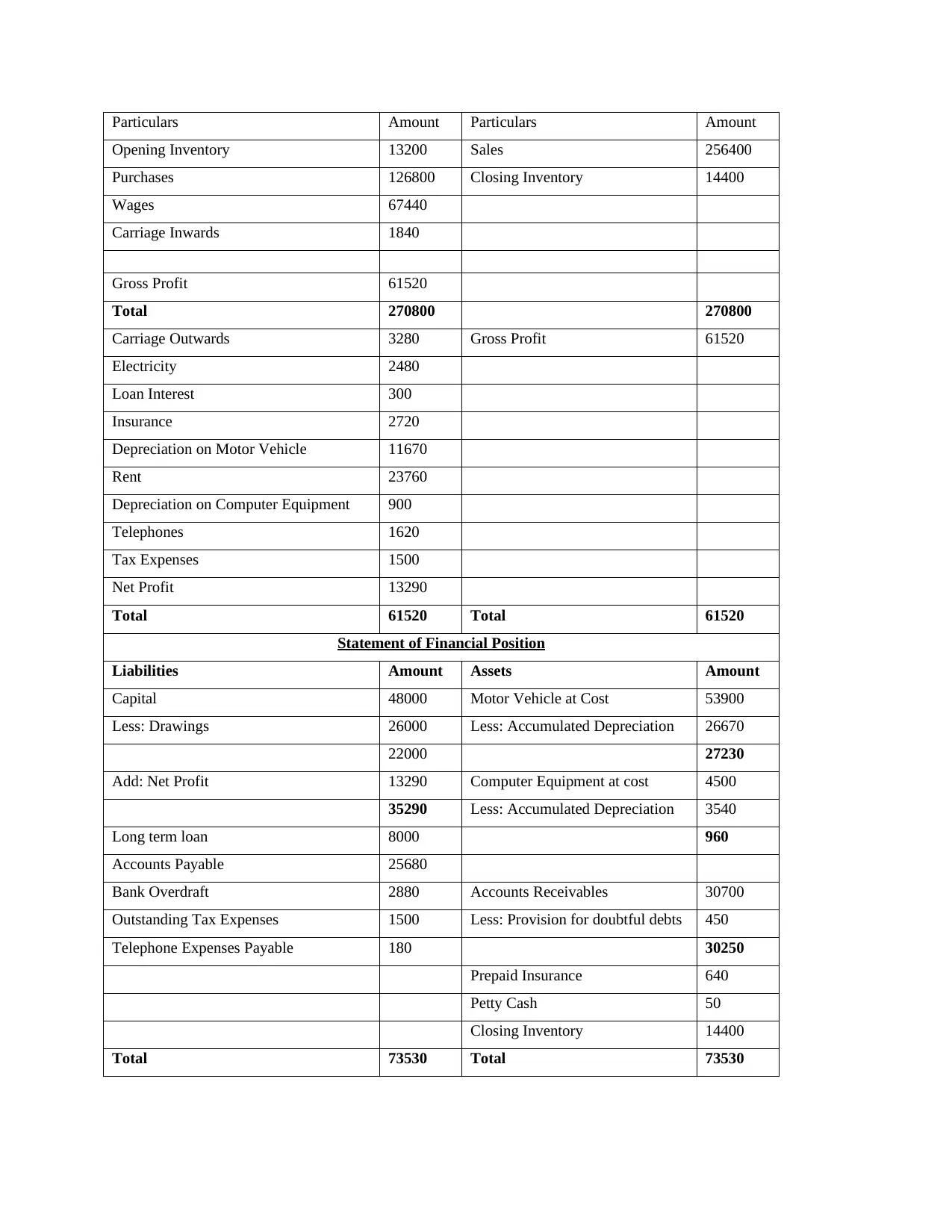

Particulars Amount Particulars Amount

Opening Inventory 13200 Sales 256400

Purchases 126800 Closing Inventory 14400

Wages 67440

Carriage Inwards 1840

Gross Profit 61520

Total 270800 270800

Carriage Outwards 3280 Gross Profit 61520

Electricity 2480

Loan Interest 300

Insurance 2720

Depreciation on Motor Vehicle 11670

Rent 23760

Depreciation on Computer Equipment 900

Telephones 1620

Tax Expenses 1500

Net Profit 13290

Total 61520 Total 61520

Statement of Financial Position

Liabilities Amount Assets Amount

Capital 48000 Motor Vehicle at Cost 53900

Less: Drawings 26000 Less: Accumulated Depreciation 26670

22000 27230

Add: Net Profit 13290 Computer Equipment at cost 4500

35290 Less: Accumulated Depreciation 3540

Long term loan 8000 960

Accounts Payable 25680

Bank Overdraft 2880 Accounts Receivables 30700

Outstanding Tax Expenses 1500 Less: Provision for doubtful debts 450

Telephone Expenses Payable 180 30250

Prepaid Insurance 640

Petty Cash 50

Closing Inventory 14400

Total 73530 Total 73530

Opening Inventory 13200 Sales 256400

Purchases 126800 Closing Inventory 14400

Wages 67440

Carriage Inwards 1840

Gross Profit 61520

Total 270800 270800

Carriage Outwards 3280 Gross Profit 61520

Electricity 2480

Loan Interest 300

Insurance 2720

Depreciation on Motor Vehicle 11670

Rent 23760

Depreciation on Computer Equipment 900

Telephones 1620

Tax Expenses 1500

Net Profit 13290

Total 61520 Total 61520

Statement of Financial Position

Liabilities Amount Assets Amount

Capital 48000 Motor Vehicle at Cost 53900

Less: Drawings 26000 Less: Accumulated Depreciation 26670

22000 27230

Add: Net Profit 13290 Computer Equipment at cost 4500

35290 Less: Accumulated Depreciation 3540

Long term loan 8000 960

Accounts Payable 25680

Bank Overdraft 2880 Accounts Receivables 30700

Outstanding Tax Expenses 1500 Less: Provision for doubtful debts 450

Telephone Expenses Payable 180 30250

Prepaid Insurance 640

Petty Cash 50

Closing Inventory 14400

Total 73530 Total 73530

TASK 2.

Relevance of financial information for users.

Financial Statements focus on providing useful information to a large number of users:

stockholders use financial statements to determine the risk - return of one’s interest in the

business and to take asset decisions on behalf of their assessment (Baksaas and Stenheim, 2019).

The financial statements have been prepared by the firms are being used by distinct classes of

persons, in the context that the firms are appropriate to them. The most prevalent users of the

financial reports are mentioned below:

Management of company- Management team is the first and probably most important

user of the financial reports. Even though they're the individuals who start preparing the

financial reports of the committee and of the board members as whole and, they have to

refer to them while taking into account the advancement and success of the firm. The

company's board analyses the annual report from the point of view of equity,

performance, cash revenues, income and expenses, capital reserves, budget provisions,

loans to be charged, business finance, and numerous other day-to-day activities. Simple

terms, the company must be able financial statements strategic decisions.

Investors-Investors are the shareholder of the firm, they would really like to comprehend

how to keep up-to - date with the company's financial position. They would really like to

start making a decision in terms of an income report about whether they have to keep

investing or start moving out of the company in terms of their productivity (Dewi, Azam

and Yusoff, 2019).

Customers- Customers have to view the financial position of the company where they

buy goods and services. Large customers would want to maintain a long-term

relationship or a deal with the firm, and they would want to interact for a business that is

comfortable financially. In addition, a financially successful business could provide its

clients with trade payables and distribute products and services at a discount rate than the

industry.

Competitors-The competitors would like to calculate the business position of the rival

company. They would want to retain a strategic lead over their rivals and would therefore

like to calculate the business condition of the other business. They also could decide to

rethink their approach by looking at the assertions.

Relevance of financial information for users.

Financial Statements focus on providing useful information to a large number of users:

stockholders use financial statements to determine the risk - return of one’s interest in the

business and to take asset decisions on behalf of their assessment (Baksaas and Stenheim, 2019).

The financial statements have been prepared by the firms are being used by distinct classes of

persons, in the context that the firms are appropriate to them. The most prevalent users of the

financial reports are mentioned below:

Management of company- Management team is the first and probably most important

user of the financial reports. Even though they're the individuals who start preparing the

financial reports of the committee and of the board members as whole and, they have to

refer to them while taking into account the advancement and success of the firm. The

company's board analyses the annual report from the point of view of equity,

performance, cash revenues, income and expenses, capital reserves, budget provisions,

loans to be charged, business finance, and numerous other day-to-day activities. Simple

terms, the company must be able financial statements strategic decisions.

Investors-Investors are the shareholder of the firm, they would really like to comprehend

how to keep up-to - date with the company's financial position. They would really like to

start making a decision in terms of an income report about whether they have to keep

investing or start moving out of the company in terms of their productivity (Dewi, Azam

and Yusoff, 2019).

Customers- Customers have to view the financial position of the company where they

buy goods and services. Large customers would want to maintain a long-term

relationship or a deal with the firm, and they would want to interact for a business that is

comfortable financially. In addition, a financially successful business could provide its

clients with trade payables and distribute products and services at a discount rate than the

industry.

Competitors-The competitors would like to calculate the business position of the rival

company. They would want to retain a strategic lead over their rivals and would therefore

like to calculate the business condition of the other business. They also could decide to

rethink their approach by looking at the assertions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Government-Government entities such as the tax department, the payroll tax Department;

really want to go through the company's balance sheet to check whether the company has

paid the proper taxes. They want to make additional tax forecasts depending on the

success of corporation and rules laid.

Employees-Employees are looking at the statement of financial position from different

points of view. They would really like to know whether the company does the reward and

the amounts rely heavily on the profitability of the company. They would still look to get

a deep overview of the business scenario and the current state of the business sector that

will be users of financial declarations. Therefore, it would like workers to fully

understand the finances of the company. The company can involve staff in decision

making.

Investment analysts- Individual investors keep a keen watch on the company's balance

sheet. We have strong business experience and are held up-to - date with how the

organization is doing. Based on their financial statement analysis, individual investors

decide whether or not to advise the company's shares to their clients.

Lenders- The business would like to check its debt-paying capacity for lenders such as

conventional banks and other financial institutions and lenders. They thus review the

annual financial performance and test if they can make a loan available.

Rating agencies- The credit rating firm shall analyze the annual financial performance in

order to assign credit scores to the firm’s debt measures. The issuer should provide all

data to the ratings agency in order to obtain the credit rating of the financial instruments it

issues. Investors of such financial instruments may make effective choices when the

credit agency has supplied a rating that is clearly based on the company’s financial

position.

Suppliers- Suppliers like clients want to deal with businesses that are healthy financially.

They use the income reports and decide to give the corporation credit. By analysing

proper financial information they take decisions regards to whether they should provide

material on credit or not. In the absence of proper information about financial aspects of a

company, this becomes difficult for suppliers to rely on business entities.

So these are the main users of financial statements. Each of them has own objectives and purpose

in order to evaluate financial information of companies (Sari and Heryanto, 2019). From all these

really want to go through the company's balance sheet to check whether the company has

paid the proper taxes. They want to make additional tax forecasts depending on the

success of corporation and rules laid.

Employees-Employees are looking at the statement of financial position from different

points of view. They would really like to know whether the company does the reward and

the amounts rely heavily on the profitability of the company. They would still look to get

a deep overview of the business scenario and the current state of the business sector that

will be users of financial declarations. Therefore, it would like workers to fully

understand the finances of the company. The company can involve staff in decision

making.

Investment analysts- Individual investors keep a keen watch on the company's balance

sheet. We have strong business experience and are held up-to - date with how the

organization is doing. Based on their financial statement analysis, individual investors

decide whether or not to advise the company's shares to their clients.

Lenders- The business would like to check its debt-paying capacity for lenders such as

conventional banks and other financial institutions and lenders. They thus review the

annual financial performance and test if they can make a loan available.

Rating agencies- The credit rating firm shall analyze the annual financial performance in

order to assign credit scores to the firm’s debt measures. The issuer should provide all

data to the ratings agency in order to obtain the credit rating of the financial instruments it

issues. Investors of such financial instruments may make effective choices when the

credit agency has supplied a rating that is clearly based on the company’s financial

position.

Suppliers- Suppliers like clients want to deal with businesses that are healthy financially.

They use the income reports and decide to give the corporation credit. By analysing

proper financial information they take decisions regards to whether they should provide

material on credit or not. In the absence of proper information about financial aspects of a

company, this becomes difficult for suppliers to rely on business entities.

So these are the main users of financial statements. Each of them has own objectives and purpose

in order to evaluate financial information of companies (Sari and Heryanto, 2019). From all these

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

users of financial statements, this can be stated that management team of company is one of the

main user of financial statement. It is so because on the basis of gathered financial information

they become able to take appropriate actions.

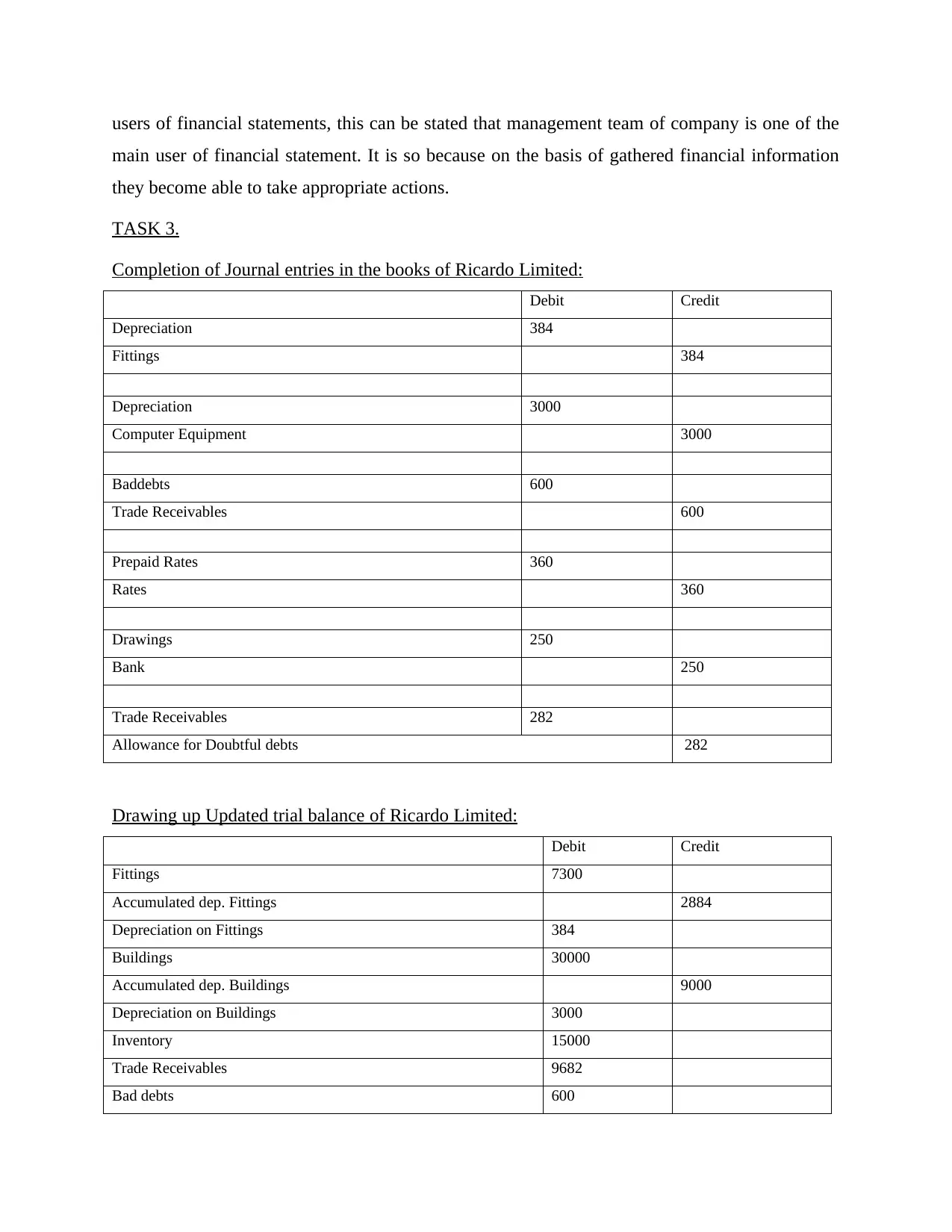

TASK 3.

Completion of Journal entries in the books of Ricardo Limited:

Debit Credit

Depreciation 384

Fittings 384

Depreciation 3000

Computer Equipment 3000

Baddebts 600

Trade Receivables 600

Prepaid Rates 360

Rates 360

Drawings 250

Bank 250

Trade Receivables 282

Allowance for Doubtful debts 282

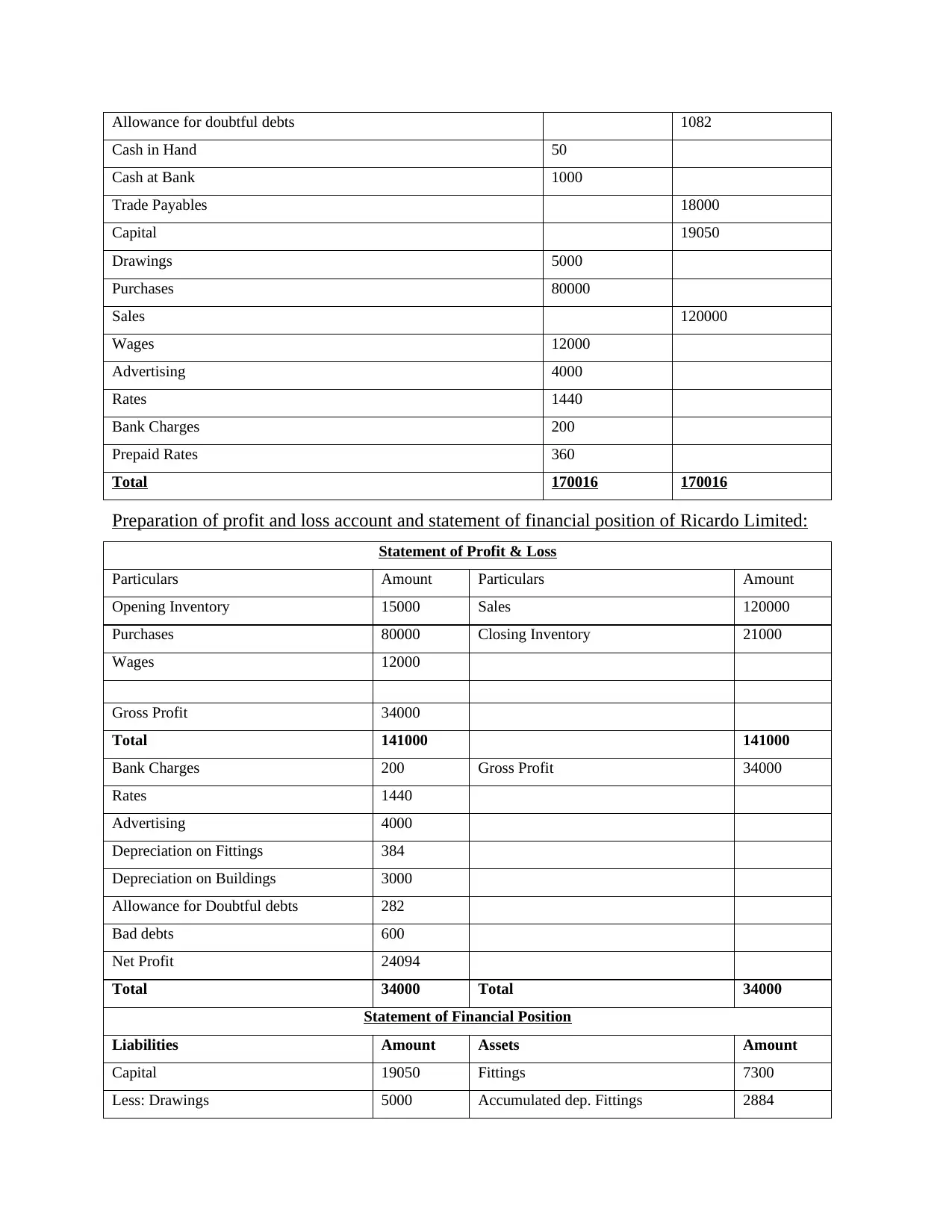

Drawing up Updated trial balance of Ricardo Limited:

Debit Credit

Fittings 7300

Accumulated dep. Fittings 2884

Depreciation on Fittings 384

Buildings 30000

Accumulated dep. Buildings 9000

Depreciation on Buildings 3000

Inventory 15000

Trade Receivables 9682

Bad debts 600

main user of financial statement. It is so because on the basis of gathered financial information

they become able to take appropriate actions.

TASK 3.

Completion of Journal entries in the books of Ricardo Limited:

Debit Credit

Depreciation 384

Fittings 384

Depreciation 3000

Computer Equipment 3000

Baddebts 600

Trade Receivables 600

Prepaid Rates 360

Rates 360

Drawings 250

Bank 250

Trade Receivables 282

Allowance for Doubtful debts 282

Drawing up Updated trial balance of Ricardo Limited:

Debit Credit

Fittings 7300

Accumulated dep. Fittings 2884

Depreciation on Fittings 384

Buildings 30000

Accumulated dep. Buildings 9000

Depreciation on Buildings 3000

Inventory 15000

Trade Receivables 9682

Bad debts 600

Allowance for doubtful debts 1082

Cash in Hand 50

Cash at Bank 1000

Trade Payables 18000

Capital 19050

Drawings 5000

Purchases 80000

Sales 120000

Wages 12000

Advertising 4000

Rates 1440

Bank Charges 200

Prepaid Rates 360

Total 170016 170016

Preparation of profit and loss account and statement of financial position of Ricardo Limited:

Statement of Profit & Loss

Particulars Amount Particulars Amount

Opening Inventory 15000 Sales 120000

Purchases 80000 Closing Inventory 21000

Wages 12000

Gross Profit 34000

Total 141000 141000

Bank Charges 200 Gross Profit 34000

Rates 1440

Advertising 4000

Depreciation on Fittings 384

Depreciation on Buildings 3000

Allowance for Doubtful debts 282

Bad debts 600

Net Profit 24094

Total 34000 Total 34000

Statement of Financial Position

Liabilities Amount Assets Amount

Capital 19050 Fittings 7300

Less: Drawings 5000 Accumulated dep. Fittings 2884

Cash in Hand 50

Cash at Bank 1000

Trade Payables 18000

Capital 19050

Drawings 5000

Purchases 80000

Sales 120000

Wages 12000

Advertising 4000

Rates 1440

Bank Charges 200

Prepaid Rates 360

Total 170016 170016

Preparation of profit and loss account and statement of financial position of Ricardo Limited:

Statement of Profit & Loss

Particulars Amount Particulars Amount

Opening Inventory 15000 Sales 120000

Purchases 80000 Closing Inventory 21000

Wages 12000

Gross Profit 34000

Total 141000 141000

Bank Charges 200 Gross Profit 34000

Rates 1440

Advertising 4000

Depreciation on Fittings 384

Depreciation on Buildings 3000

Allowance for Doubtful debts 282

Bad debts 600

Net Profit 24094

Total 34000 Total 34000

Statement of Financial Position

Liabilities Amount Assets Amount

Capital 19050 Fittings 7300

Less: Drawings 5000 Accumulated dep. Fittings 2884

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

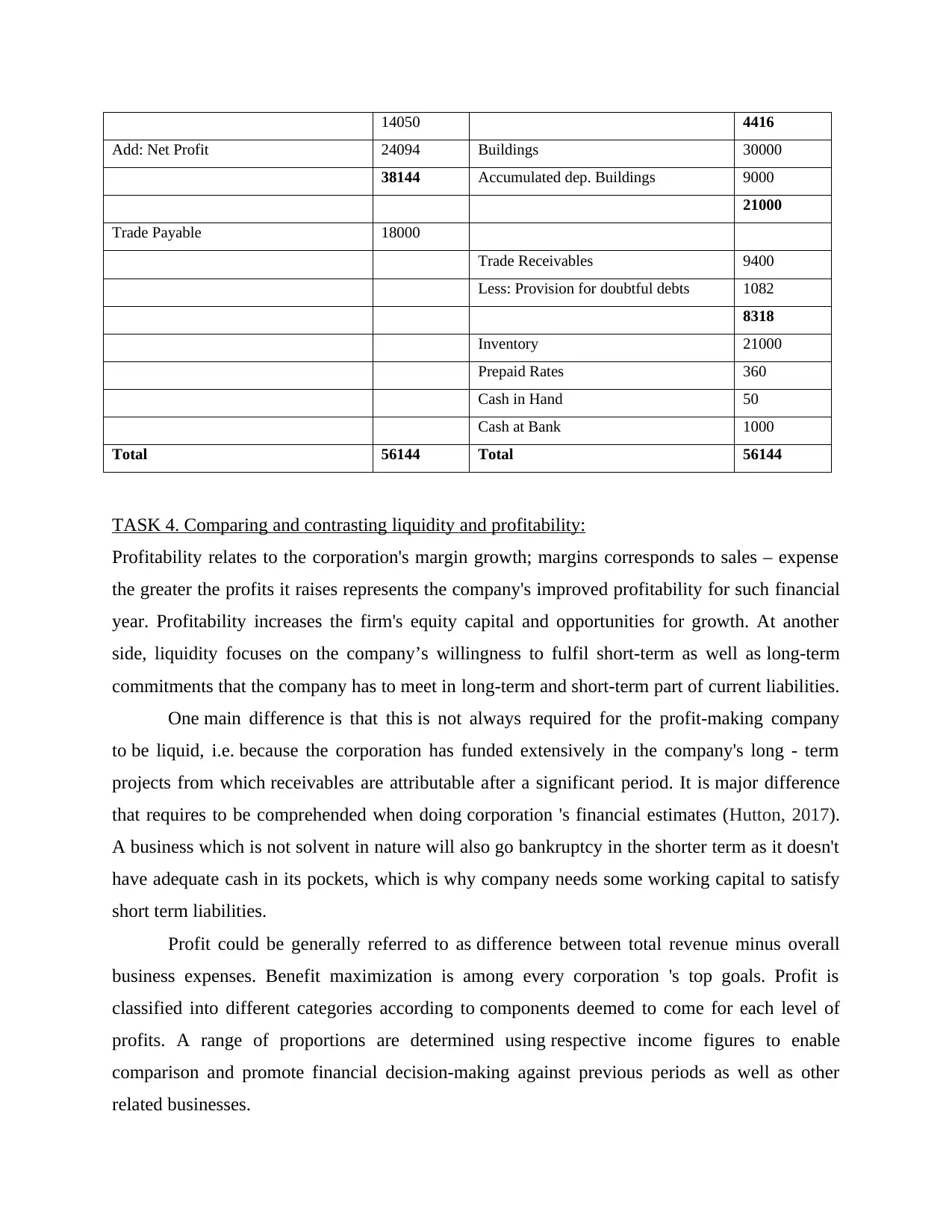

14050 4416

Add: Net Profit 24094 Buildings 30000

38144 Accumulated dep. Buildings 9000

21000

Trade Payable 18000

Trade Receivables 9400

Less: Provision for doubtful debts 1082

8318

Inventory 21000

Prepaid Rates 360

Cash in Hand 50

Cash at Bank 1000

Total 56144 Total 56144

TASK 4. Comparing and contrasting liquidity and profitability:

Profitability relates to the corporation's margin growth; margins corresponds to sales – expense

the greater the profits it raises represents the company's improved profitability for such financial

year. Profitability increases the firm's equity capital and opportunities for growth. At another

side, liquidity focuses on the company’s willingness to fulfil short-term as well as long-term

commitments that the company has to meet in long-term and short-term part of current liabilities.

One main difference is that this is not always required for the profit-making company

to be liquid, i.e. because the corporation has funded extensively in the company's long - term

projects from which receivables are attributable after a significant period. It is major difference

that requires to be comprehended when doing corporation 's financial estimates (Hutton, 2017).

A business which is not solvent in nature will also go bankruptcy in the shorter term as it doesn't

have adequate cash in its pockets, which is why company needs some working capital to satisfy

short term liabilities.

Profit could be generally referred to as difference between total revenue minus overall

business expenses. Benefit maximization is among every corporation 's top goals. Profit is

classified into different categories according to components deemed to come for each level of

profits. A range of proportions are determined using respective income figures to enable

comparison and promote financial decision-making against previous periods as well as other

related businesses.

Add: Net Profit 24094 Buildings 30000

38144 Accumulated dep. Buildings 9000

21000

Trade Payable 18000

Trade Receivables 9400

Less: Provision for doubtful debts 1082

8318

Inventory 21000

Prepaid Rates 360

Cash in Hand 50

Cash at Bank 1000

Total 56144 Total 56144

TASK 4. Comparing and contrasting liquidity and profitability:

Profitability relates to the corporation's margin growth; margins corresponds to sales – expense

the greater the profits it raises represents the company's improved profitability for such financial

year. Profitability increases the firm's equity capital and opportunities for growth. At another

side, liquidity focuses on the company’s willingness to fulfil short-term as well as long-term

commitments that the company has to meet in long-term and short-term part of current liabilities.

One main difference is that this is not always required for the profit-making company

to be liquid, i.e. because the corporation has funded extensively in the company's long - term

projects from which receivables are attributable after a significant period. It is major difference

that requires to be comprehended when doing corporation 's financial estimates (Hutton, 2017).

A business which is not solvent in nature will also go bankruptcy in the shorter term as it doesn't

have adequate cash in its pockets, which is why company needs some working capital to satisfy

short term liabilities.

Profit could be generally referred to as difference between total revenue minus overall

business expenses. Benefit maximization is among every corporation 's top goals. Profit is

classified into different categories according to components deemed to come for each level of

profits. A range of proportions are determined using respective income figures to enable

comparison and promote financial decision-making against previous periods as well as other

related businesses.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Liquidity explains how easily an asset or commodity can be purchased or sold on market,

without changing the price of asset. It is also company's supply of cash/cash equivalents. Cash

alternatives involve treasury notes, corporate debt, and other sellable short-term securities/stocks.

Liquidity is important as productivity, and in short term often even more critical. That's because

the business requires cash to operate day-to-day activities. The company cannot continue to

make profit without performing the above daily activities. Extra sources of financing, like raising

more debt, may be regarded; however, this entails greater risks and greater costs. It is therefore

necessary to be alert about the situation with respect to cash flows and to handle effectively

(Nichols, Wahlen and Wieland, 2017). A liquidity's time dimension concerns the pace at which

any asset can be transformed into cash risk component and the level of confidence at which an

asset could be turned into cash funds without loss in book value. At this view, all assets

would have degree of liquidity as well as most liquid assets implies to those assets that consist of

cash. However, liquidity implies, in firm's context, its prospective abilities to fulfil

obligations/liabilities. The Liquidity of firm, seeks to quantify the capacity of a company to meet

planned and unforeseen cash needs, increase its assets, minimize its obligations or covering any

operational losses.

Profitability is measure of corporate performance as well as being how well corporation

does over period of time but is not an indicator as to how financial-rich the corporation is then it

is impossible to tell the investor the organization 's financial position. Liquidity, but at other side,

informs us the corporation 's cash status, far more cash on balance sheet also implies poor

governance of the corporation's working capital because as corporation bears opportunity cost

of available cash that lies idle on balance sheet. A profitable corporation may not even have

sufficient liquidity since most of company's funds are engaged in project activities and a

corporation that has cash or liquidity might not have been profitable due to lack of chances to put

excess funds (Burger and Curtis, 2017).

Profitability is company's financial performance metric that is implied in income

statement as well as reported in profit and loss statement as Net profit. When this net profit

amount is unfavourable it implies the corporation will bear losses within this period. Liquidity

term is prevalent in balance sheet on current assets portion of any corporation 's balance sheet

that involves marketable financial instruments, prepaid expenses as well as stocks

(Hermuningsih, Kirana and Erawati, 2019).

without changing the price of asset. It is also company's supply of cash/cash equivalents. Cash

alternatives involve treasury notes, corporate debt, and other sellable short-term securities/stocks.

Liquidity is important as productivity, and in short term often even more critical. That's because

the business requires cash to operate day-to-day activities. The company cannot continue to

make profit without performing the above daily activities. Extra sources of financing, like raising

more debt, may be regarded; however, this entails greater risks and greater costs. It is therefore

necessary to be alert about the situation with respect to cash flows and to handle effectively

(Nichols, Wahlen and Wieland, 2017). A liquidity's time dimension concerns the pace at which

any asset can be transformed into cash risk component and the level of confidence at which an

asset could be turned into cash funds without loss in book value. At this view, all assets

would have degree of liquidity as well as most liquid assets implies to those assets that consist of

cash. However, liquidity implies, in firm's context, its prospective abilities to fulfil

obligations/liabilities. The Liquidity of firm, seeks to quantify the capacity of a company to meet

planned and unforeseen cash needs, increase its assets, minimize its obligations or covering any

operational losses.

Profitability is measure of corporate performance as well as being how well corporation

does over period of time but is not an indicator as to how financial-rich the corporation is then it

is impossible to tell the investor the organization 's financial position. Liquidity, but at other side,

informs us the corporation 's cash status, far more cash on balance sheet also implies poor

governance of the corporation's working capital because as corporation bears opportunity cost

of available cash that lies idle on balance sheet. A profitable corporation may not even have

sufficient liquidity since most of company's funds are engaged in project activities and a

corporation that has cash or liquidity might not have been profitable due to lack of chances to put

excess funds (Burger and Curtis, 2017).

Profitability is company's financial performance metric that is implied in income

statement as well as reported in profit and loss statement as Net profit. When this net profit

amount is unfavourable it implies the corporation will bear losses within this period. Liquidity

term is prevalent in balance sheet on current assets portion of any corporation 's balance sheet

that involves marketable financial instruments, prepaid expenses as well as stocks

(Hermuningsih, Kirana and Erawati, 2019).

Both Profitability versus Liquidity are critical to a corporation because it's a crucial factor

to a company. If the corporation doesn't have sufficient cash on hands, working capital

management would go for toss and the corporation would need to search for working capital debt

which would in effect raise the interest costs of any corporation. Profitability also crucial

component since the company requires to evaluate the rationale for low-profit expansion and

focusing on cost decrease as well. The distinction between liquidity and profitability is clearly

that profit is available vs. cash scarcity. Profit is principal measure for assessing a firm 's

consistency and is shareholders' priority focus. Although profit is most significant, this would not

automatically mean sustainability of business operations. In fact, a profitable corporation does

not have adequate liquidity since most of company's assets are allocated in ventures, and a

corporation that has lot of cash-funds or resources may not even be profitable since it hasn't

successfully used excess funds. Consequently, success relies on both profits and cash

management being better. Consequently, as could be seen from above, profitability vs liquidity

are not similar aspects and the corporation must retain a perfect harmony among these same two

as if the corporation concentrates too much towards profitability then this runs risk of not being

able to cover its current liabilities, staff and other parties, while on other hand when the

corporation focuses on the liquidity and then this runs risk of loss (Adekola, Samy and Knight,

2017).

CONCLUSION

Form the above study it has been articulated that Collecting, classifying and summarizing

the reported transaction is important. This is achieved by accounting process. After financial

transaction are identified, these transactions are recorded correctly in books in systematic manner

thru the fundamental accounting procedure. The predominant role of accounting herein is

to properly record all accounting and fiscal transactions entered into by the company. For

accounting purposes, the accountant holds a collection of accounts. Management is accountable

to investors regarding state of affairs of company. The activities which are being funded with

investors' capital have to be reviewed to them regularly. For this purpose, performance of full

year sent to them summarized annually by regular reports.

to a company. If the corporation doesn't have sufficient cash on hands, working capital

management would go for toss and the corporation would need to search for working capital debt

which would in effect raise the interest costs of any corporation. Profitability also crucial

component since the company requires to evaluate the rationale for low-profit expansion and

focusing on cost decrease as well. The distinction between liquidity and profitability is clearly

that profit is available vs. cash scarcity. Profit is principal measure for assessing a firm 's

consistency and is shareholders' priority focus. Although profit is most significant, this would not

automatically mean sustainability of business operations. In fact, a profitable corporation does

not have adequate liquidity since most of company's assets are allocated in ventures, and a

corporation that has lot of cash-funds or resources may not even be profitable since it hasn't

successfully used excess funds. Consequently, success relies on both profits and cash

management being better. Consequently, as could be seen from above, profitability vs liquidity

are not similar aspects and the corporation must retain a perfect harmony among these same two

as if the corporation concentrates too much towards profitability then this runs risk of not being

able to cover its current liabilities, staff and other parties, while on other hand when the

corporation focuses on the liquidity and then this runs risk of loss (Adekola, Samy and Knight,

2017).

CONCLUSION

Form the above study it has been articulated that Collecting, classifying and summarizing

the reported transaction is important. This is achieved by accounting process. After financial

transaction are identified, these transactions are recorded correctly in books in systematic manner

thru the fundamental accounting procedure. The predominant role of accounting herein is

to properly record all accounting and fiscal transactions entered into by the company. For

accounting purposes, the accountant holds a collection of accounts. Management is accountable

to investors regarding state of affairs of company. The activities which are being funded with

investors' capital have to be reviewed to them regularly. For this purpose, performance of full

year sent to them summarized annually by regular reports.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.