Principles of Accounting, Financial Statements, and Ratios

VerifiedAdded on 2022/11/24

|28

|2478

|191

Homework Assignment

AI Summary

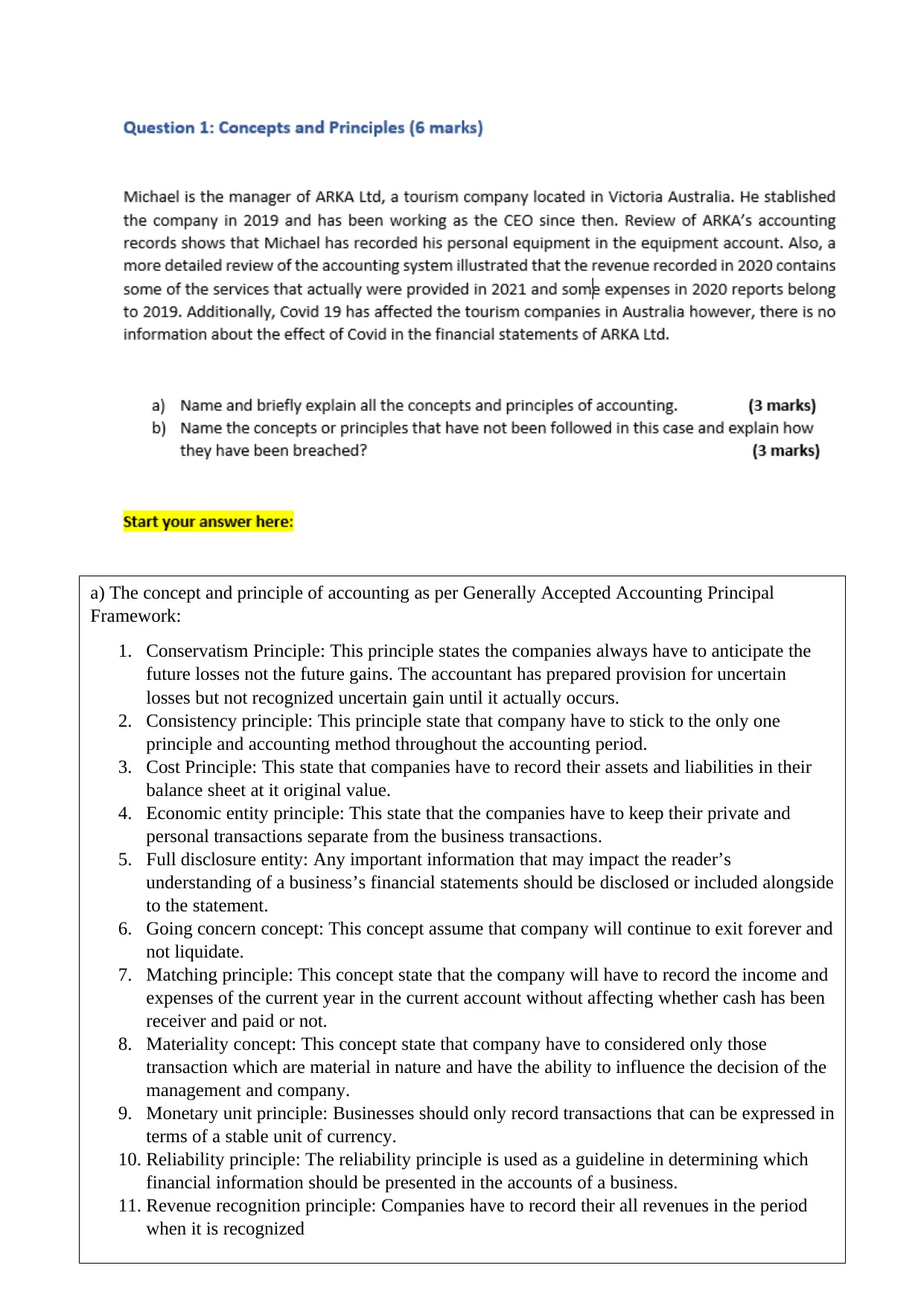

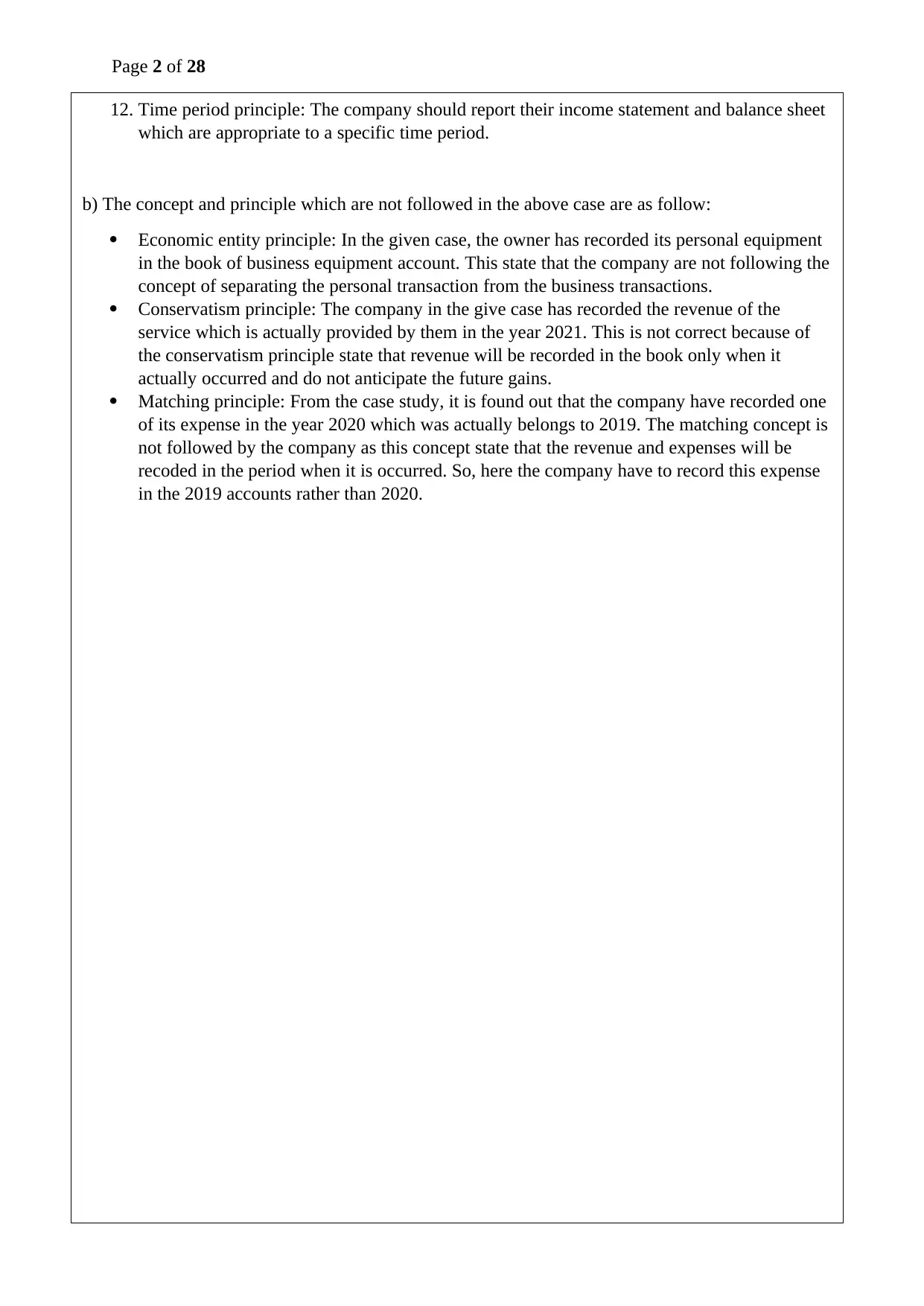

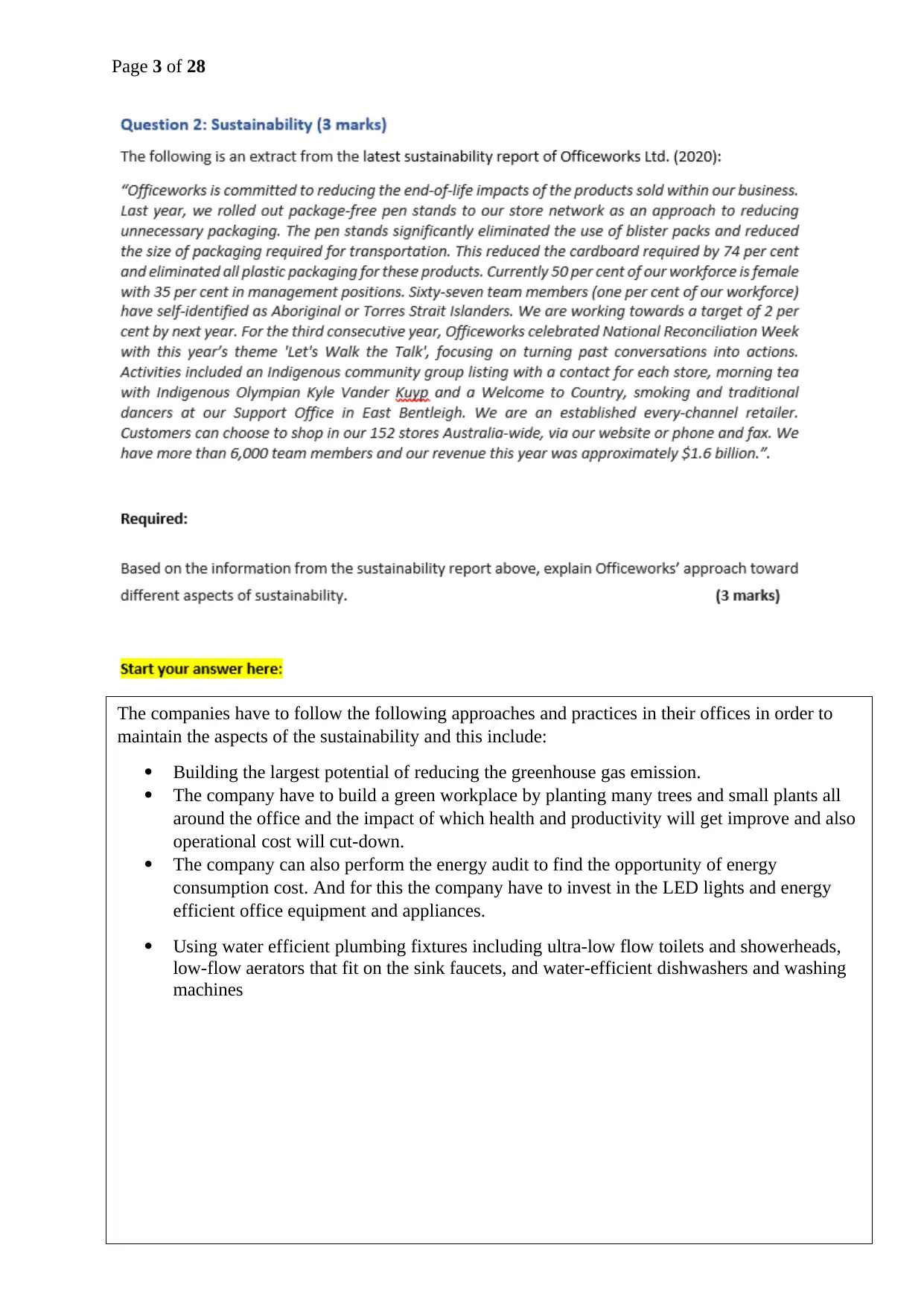

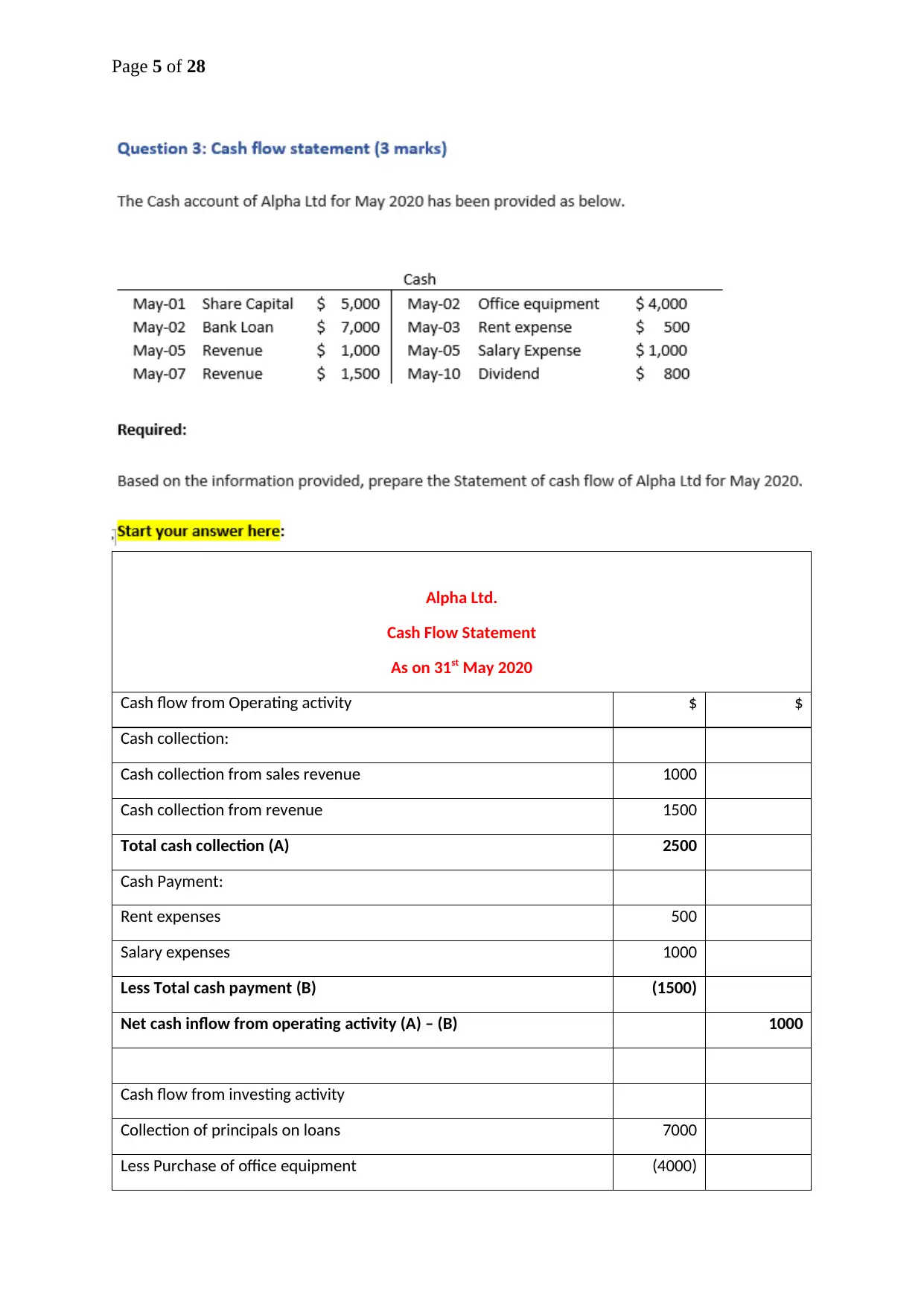

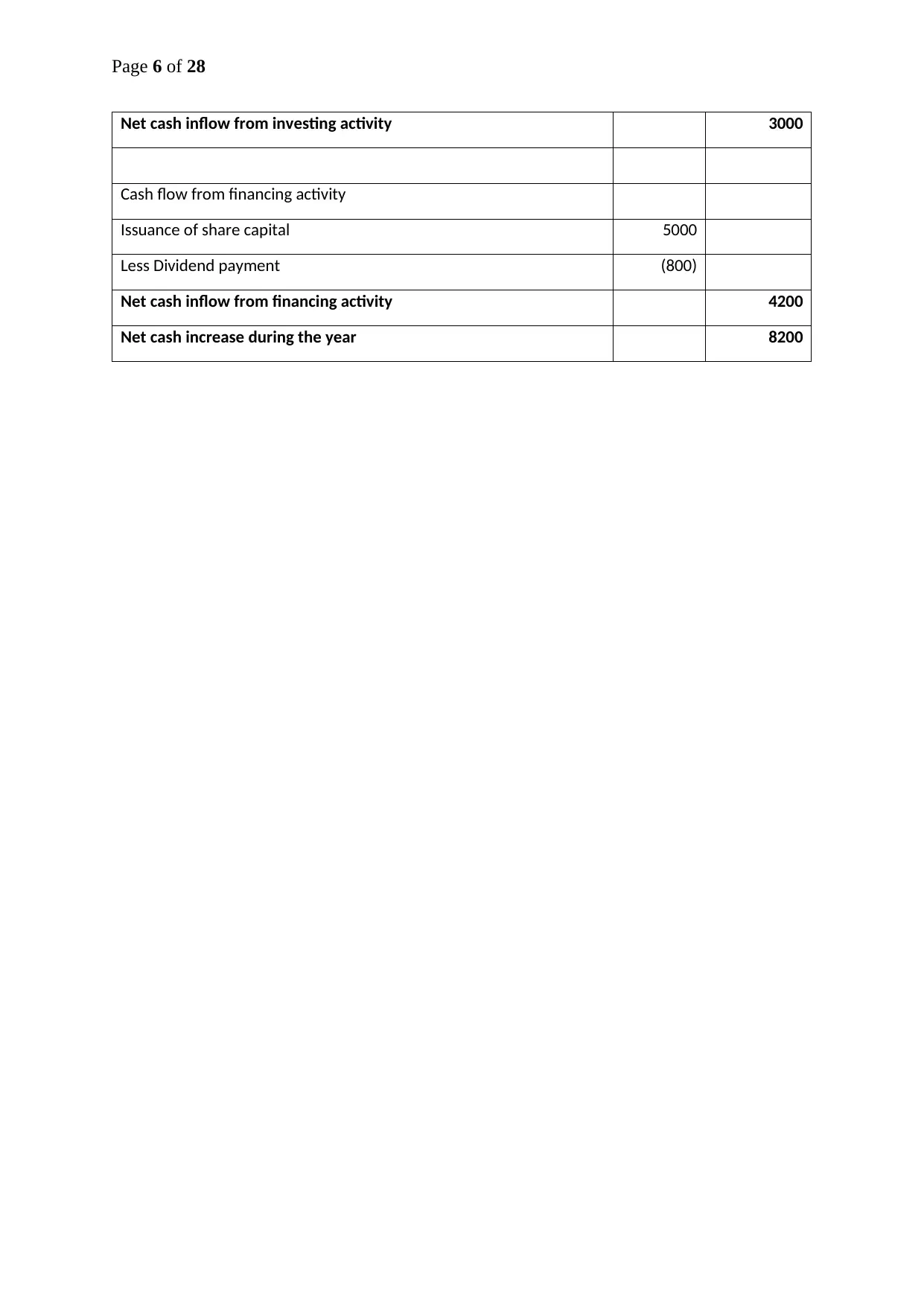

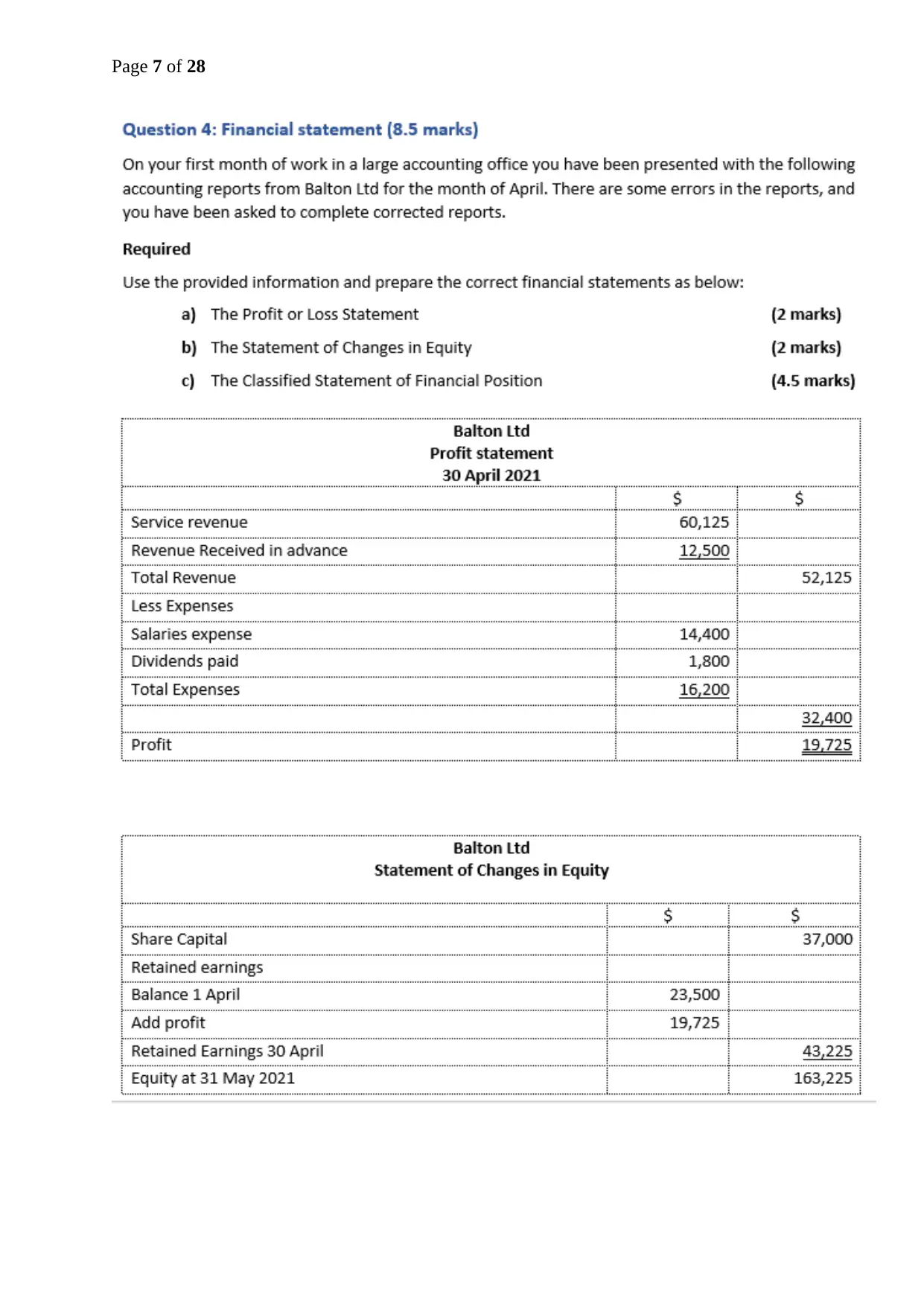

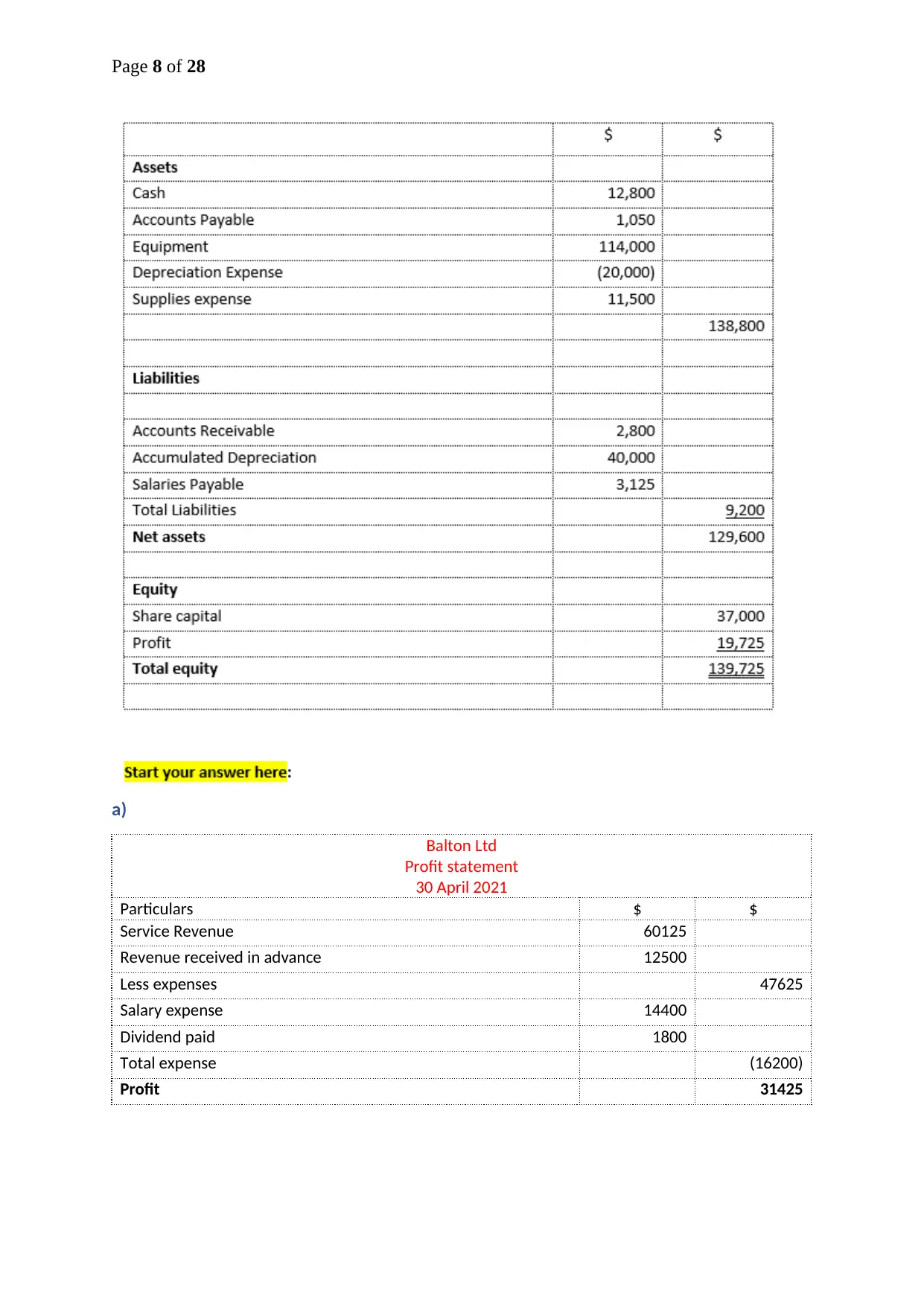

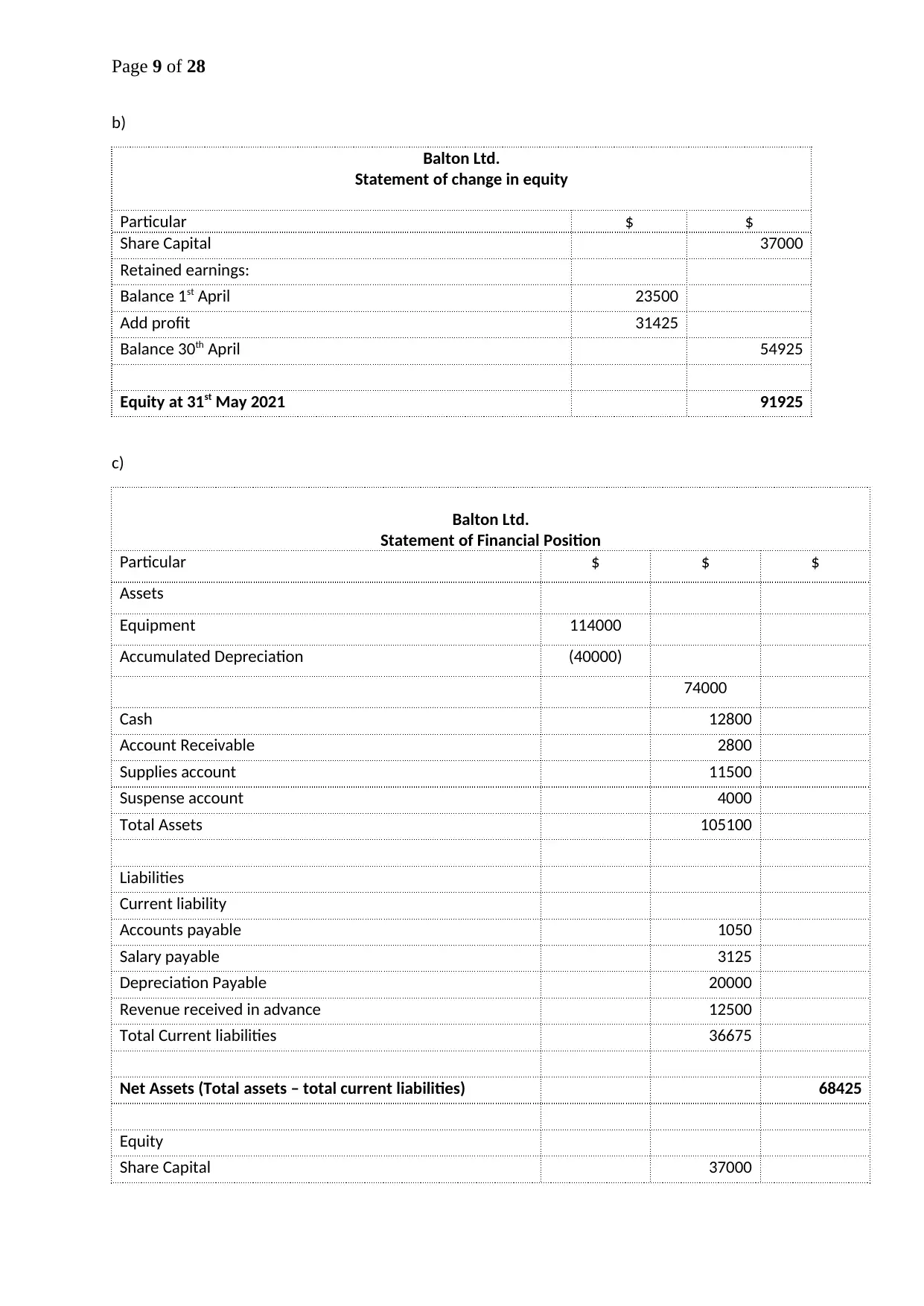

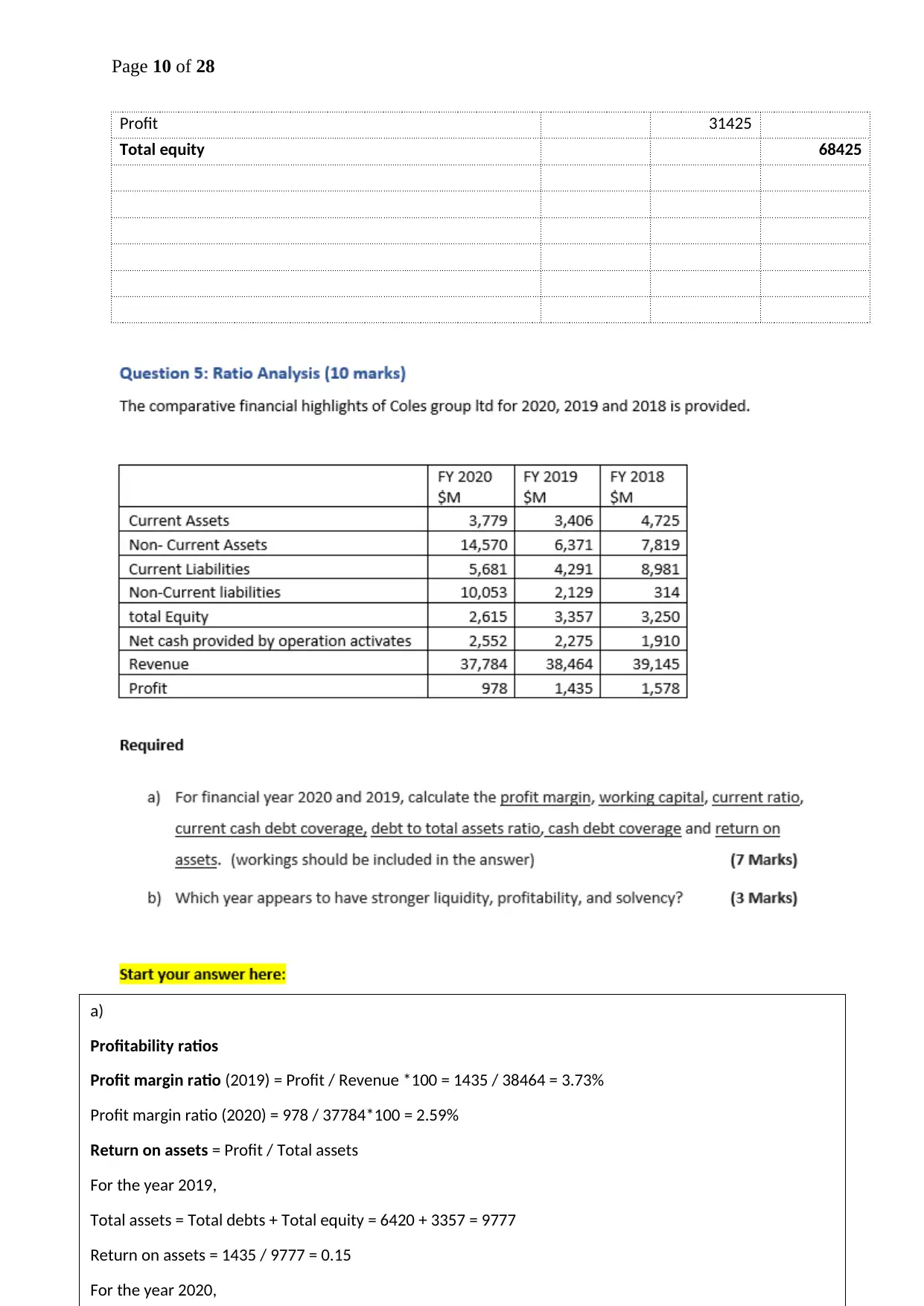

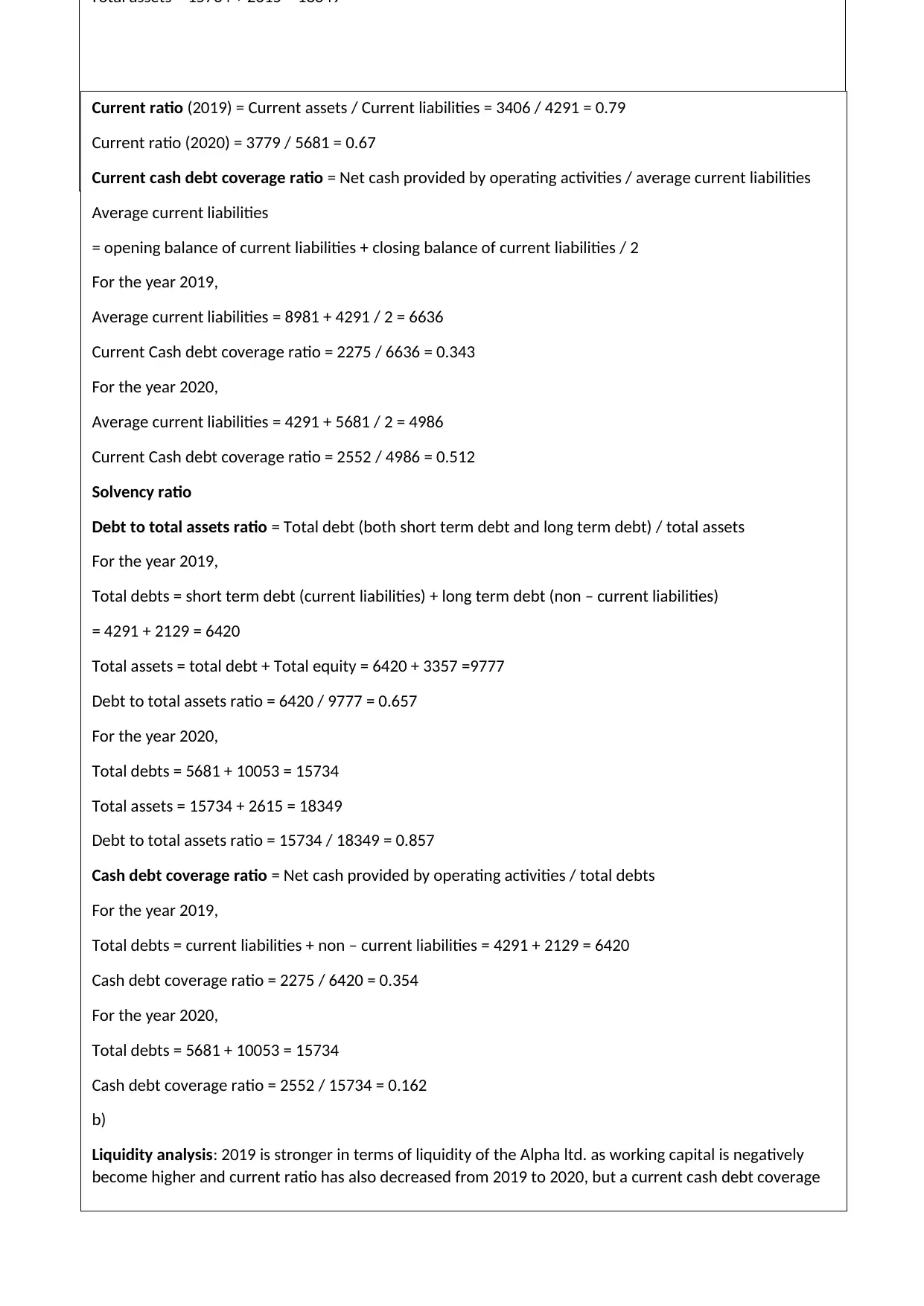

This accounting assignment solution delves into the fundamental principles of accounting, including conservatism, consistency, cost, economic entity, full disclosure, going concern, matching, materiality, monetary unit, reliability, revenue recognition, and time period principles. It identifies instances where these principles were not followed and suggests sustainable business practices. The solution includes a cash flow statement, a profit statement, and a statement of changes in equity for Balton Ltd. It also presents a financial position statement and a detailed ratio analysis (profitability, liquidity, and solvency) for Alpha Ltd., comparing performance over two years. Further, it provides journal entries, a trial balance, and adjusting entries to illustrate accounting procedures. The assignment covers key aspects of financial accounting, providing a comprehensive understanding of the subject.

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.