Accounting Financial Analysis Report: Thomas T Enterprise Performance

VerifiedAdded on 2022/11/24

|13

|1760

|221

Report

AI Summary

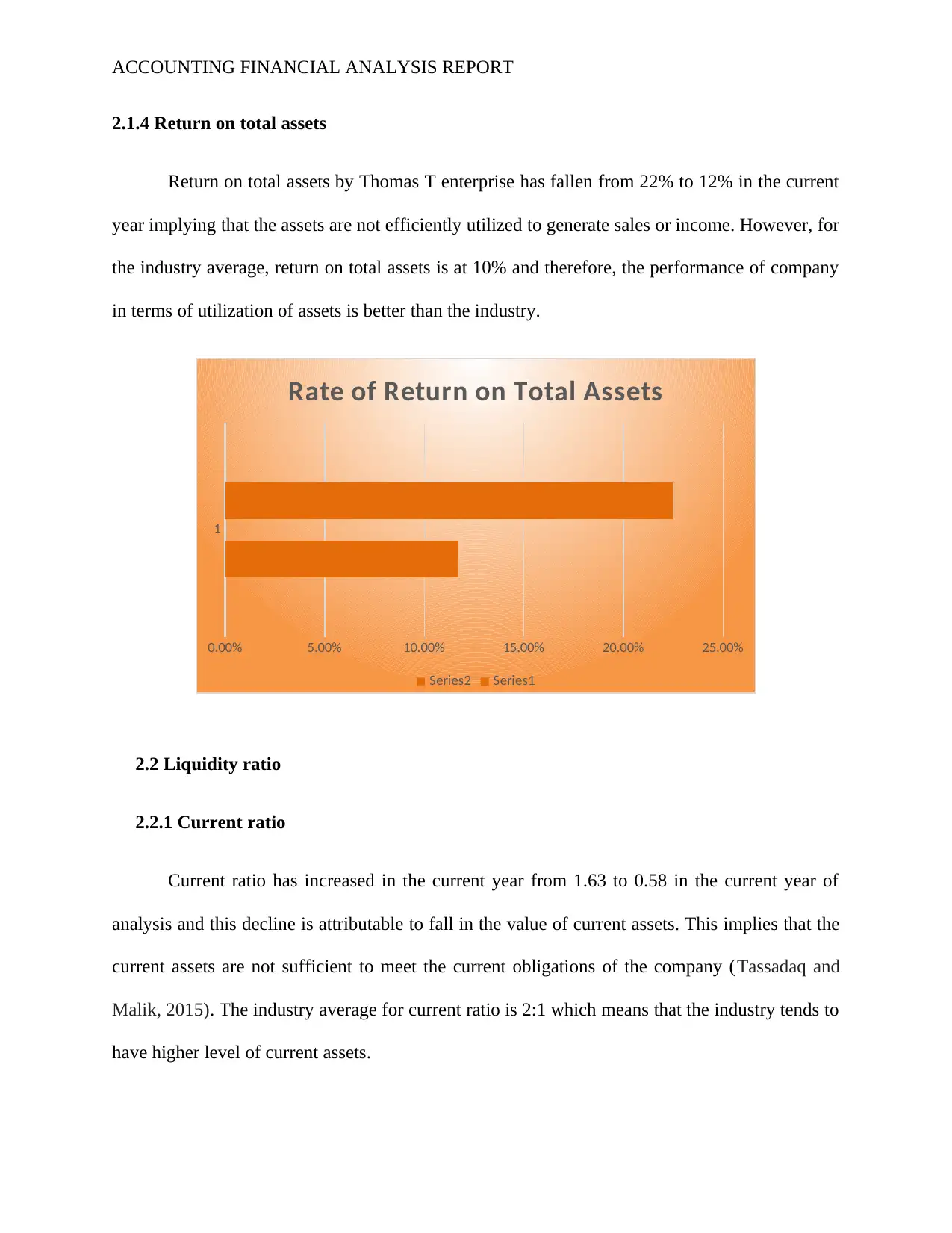

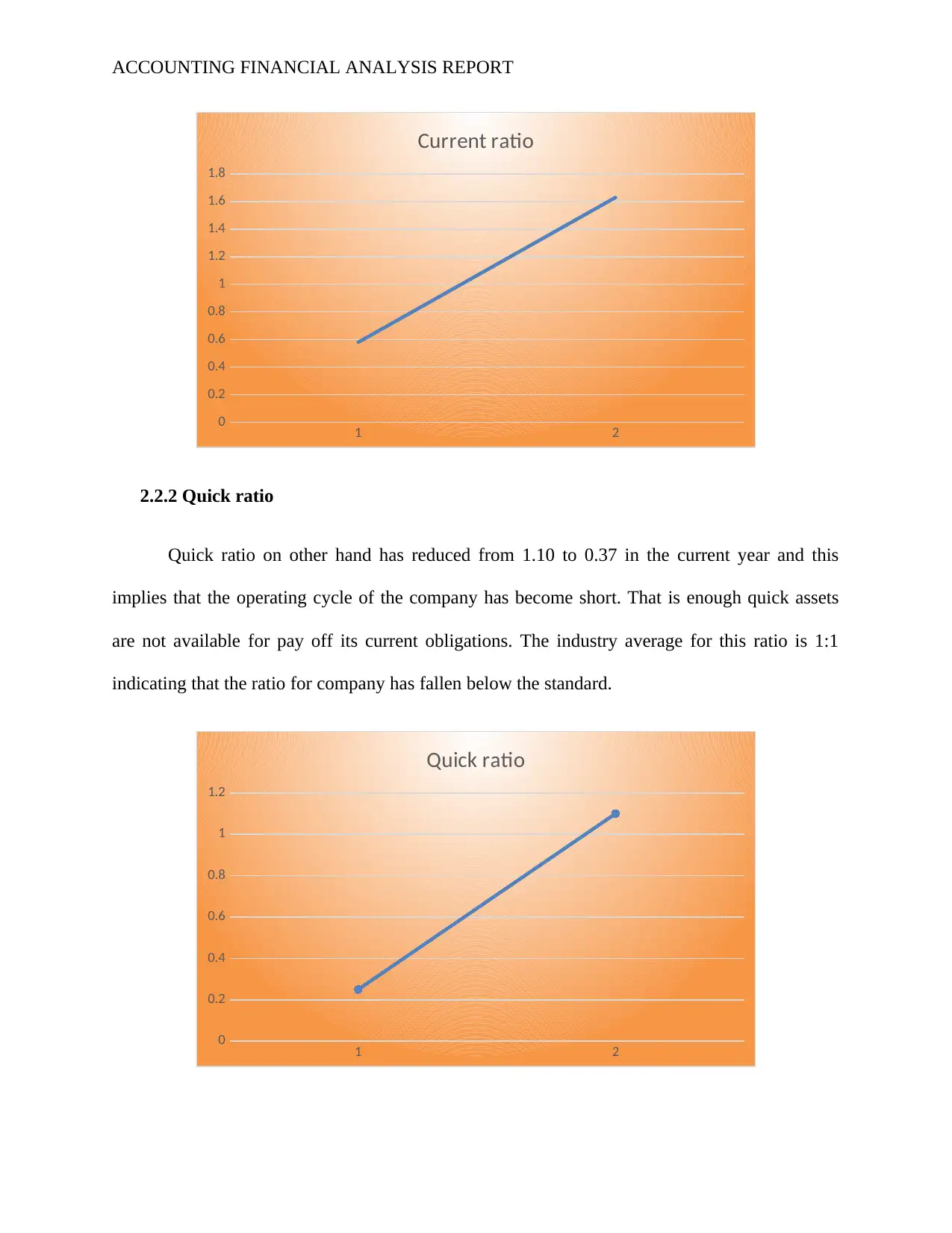

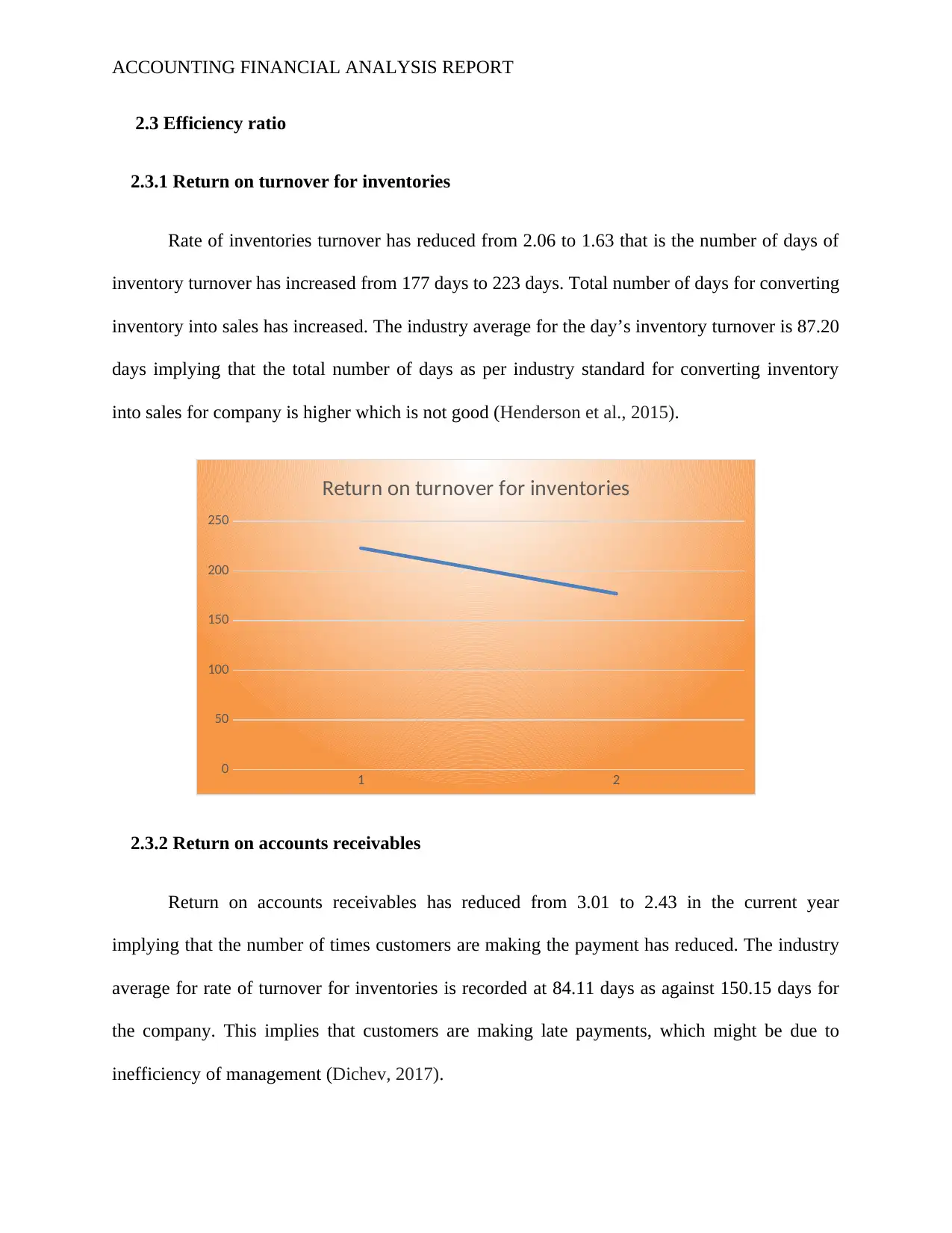

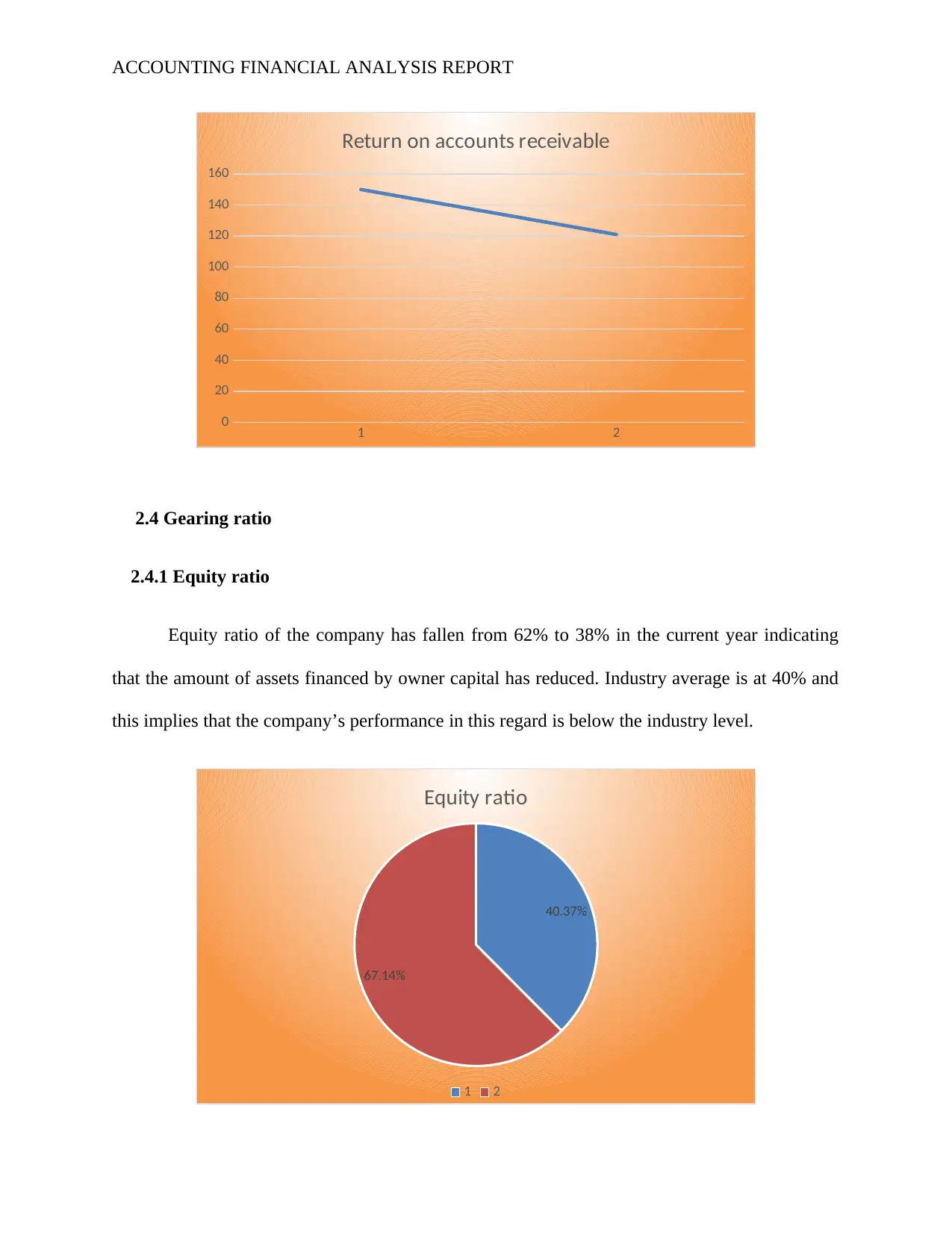

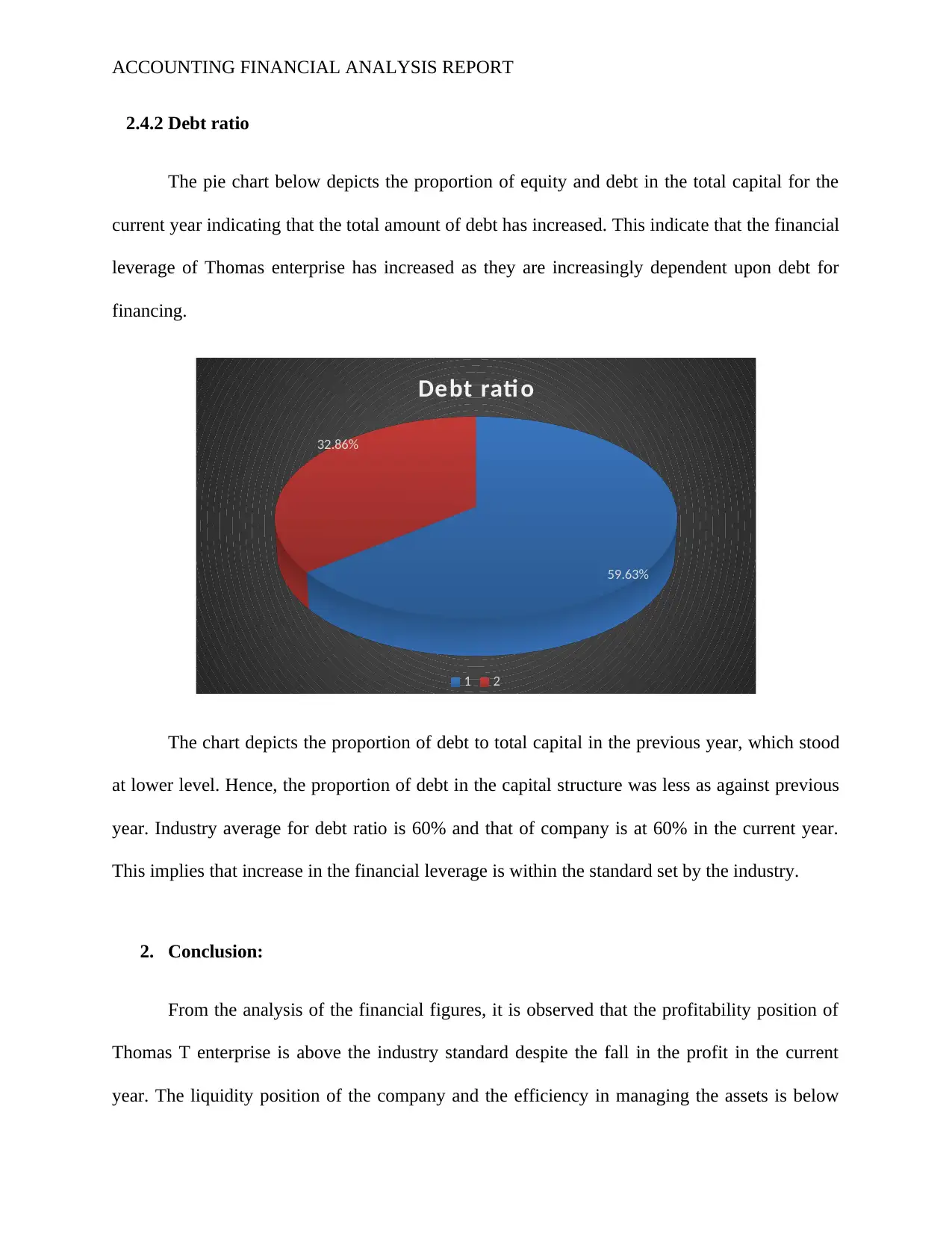

This report presents a financial analysis of Thomas T Enterprise, a wholesale electrical appliance store, based on financial data from two comparative years. The analysis utilizes ratio analysis to evaluate the company's performance, focusing on profitability, liquidity, efficiency, and gearing ratios. The report includes a comparison of the company's performance against industry benchmarks to assess its financial health and identify areas for improvement. The findings reveal the company's strengths and weaknesses in managing its assets, generating profits, and meeting its financial obligations. The report concludes with recommendations for enhancing the company's financial performance, such as monitoring liquidity ratios, controlling expenses, and improving debt collection. The analysis is based on the provided trial balances, income statements, and balance sheets, and it aims to provide insights for stakeholders and guide future business decisions.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.