Accounting for Managers Assignment 1: Flash Cleaning Services Analysis

VerifiedAdded on 2023/04/21

|17

|4867

|127

Homework Assignment

AI Summary

This document presents a comprehensive solution to an accounting assignment, focusing on the financial analysis of Flash Cleaning Services. It includes detailed journal entries, ledger accounts, and a trial balance, culminating in the preparation of a statement of profit and loss, a statement of financial position, and a statement of changes in equity. The assignment also delves into ratio analysis, calculating and interpreting the current and debt ratios, along with an analysis of the impact of loan repayment on these ratios. Furthermore, the document provides a historical overview of accounting, specifically focusing on the evolution and significance of double-entry bookkeeping, tracing its origins and impact on modern accounting practices. The solution is structured to provide a clear understanding of accounting principles and their practical application.

ACCOUNTING FOR

MANAGERS

ASSIGNMENT

MANAGERS

ASSIGNMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

2

Contents

Question 1: Preparation of accounting records – using spreadsheets.........................................................3

Question 2: History of accounting - essay..................................................................................................10

Question 3: ABC Learning Case Study........................................................................................................12

References.................................................................................................................................................15

2 | P a g e

Contents

Question 1: Preparation of accounting records – using spreadsheets.........................................................3

Question 2: History of accounting - essay..................................................................................................10

Question 3: ABC Learning Case Study........................................................................................................12

References.................................................................................................................................................15

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

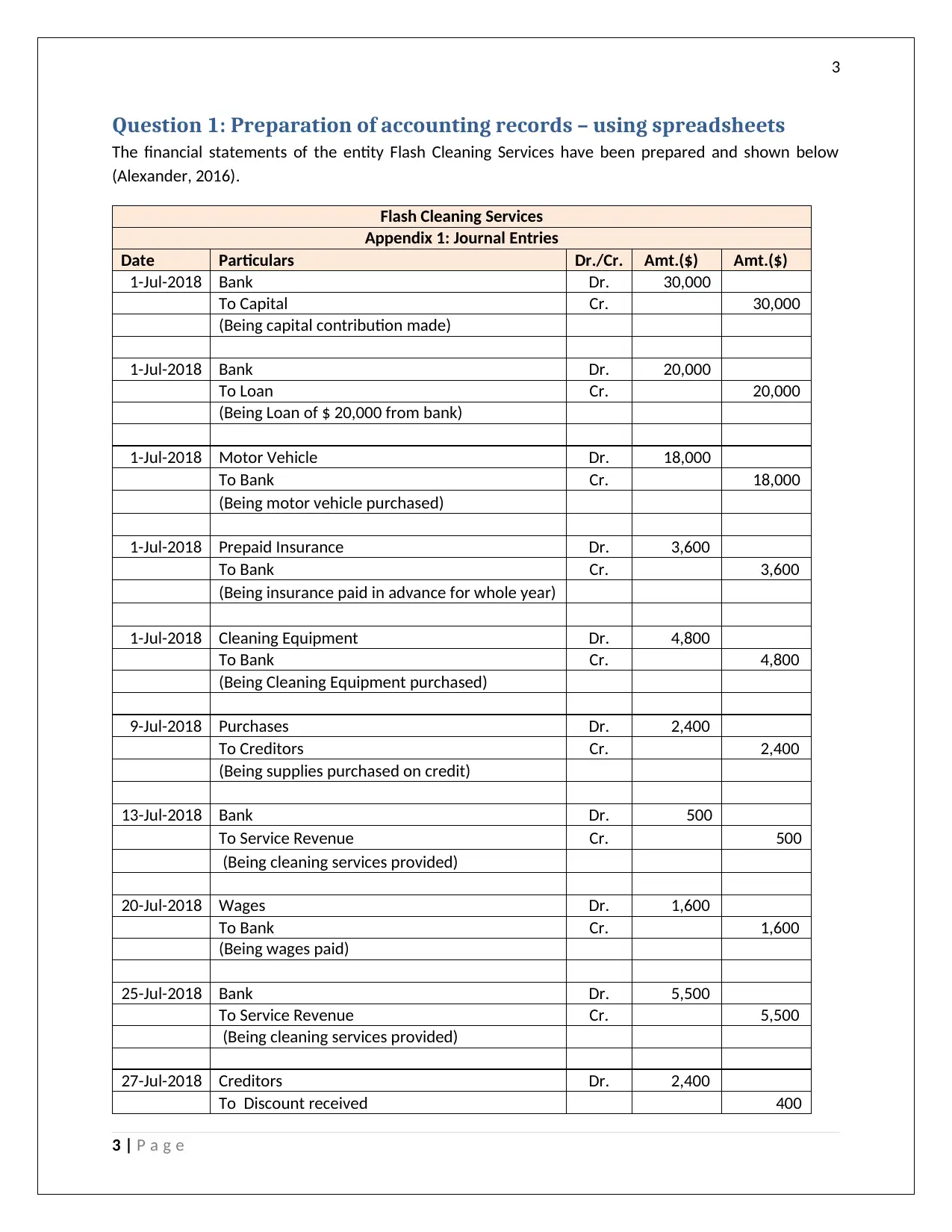

Question 1: Preparation of accounting records – using spreadsheets

The financial statements of the entity Flash Cleaning Services have been prepared and shown below

(Alexander, 2016).

Flash Cleaning Services

Appendix 1: Journal Entries

Date Particulars Dr./Cr. Amt.($) Amt.($)

1-Jul-2018 Bank Dr. 30,000

To Capital Cr. 30,000

(Being capital contribution made)

1-Jul-2018 Bank Dr. 20,000

To Loan Cr. 20,000

(Being Loan of $ 20,000 from bank)

1-Jul-2018 Motor Vehicle Dr. 18,000

To Bank Cr. 18,000

(Being motor vehicle purchased)

1-Jul-2018 Prepaid Insurance Dr. 3,600

To Bank Cr. 3,600

(Being insurance paid in advance for whole year)

1-Jul-2018 Cleaning Equipment Dr. 4,800

To Bank Cr. 4,800

(Being Cleaning Equipment purchased)

9-Jul-2018 Purchases Dr. 2,400

To Creditors Cr. 2,400

(Being supplies purchased on credit)

13-Jul-2018 Bank Dr. 500

To Service Revenue Cr. 500

(Being cleaning services provided)

20-Jul-2018 Wages Dr. 1,600

To Bank Cr. 1,600

(Being wages paid)

25-Jul-2018 Bank Dr. 5,500

To Service Revenue Cr. 5,500

(Being cleaning services provided)

27-Jul-2018 Creditors Dr. 2,400

To Discount received 400

3 | P a g e

Question 1: Preparation of accounting records – using spreadsheets

The financial statements of the entity Flash Cleaning Services have been prepared and shown below

(Alexander, 2016).

Flash Cleaning Services

Appendix 1: Journal Entries

Date Particulars Dr./Cr. Amt.($) Amt.($)

1-Jul-2018 Bank Dr. 30,000

To Capital Cr. 30,000

(Being capital contribution made)

1-Jul-2018 Bank Dr. 20,000

To Loan Cr. 20,000

(Being Loan of $ 20,000 from bank)

1-Jul-2018 Motor Vehicle Dr. 18,000

To Bank Cr. 18,000

(Being motor vehicle purchased)

1-Jul-2018 Prepaid Insurance Dr. 3,600

To Bank Cr. 3,600

(Being insurance paid in advance for whole year)

1-Jul-2018 Cleaning Equipment Dr. 4,800

To Bank Cr. 4,800

(Being Cleaning Equipment purchased)

9-Jul-2018 Purchases Dr. 2,400

To Creditors Cr. 2,400

(Being supplies purchased on credit)

13-Jul-2018 Bank Dr. 500

To Service Revenue Cr. 500

(Being cleaning services provided)

20-Jul-2018 Wages Dr. 1,600

To Bank Cr. 1,600

(Being wages paid)

25-Jul-2018 Bank Dr. 5,500

To Service Revenue Cr. 5,500

(Being cleaning services provided)

27-Jul-2018 Creditors Dr. 2,400

To Discount received 400

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

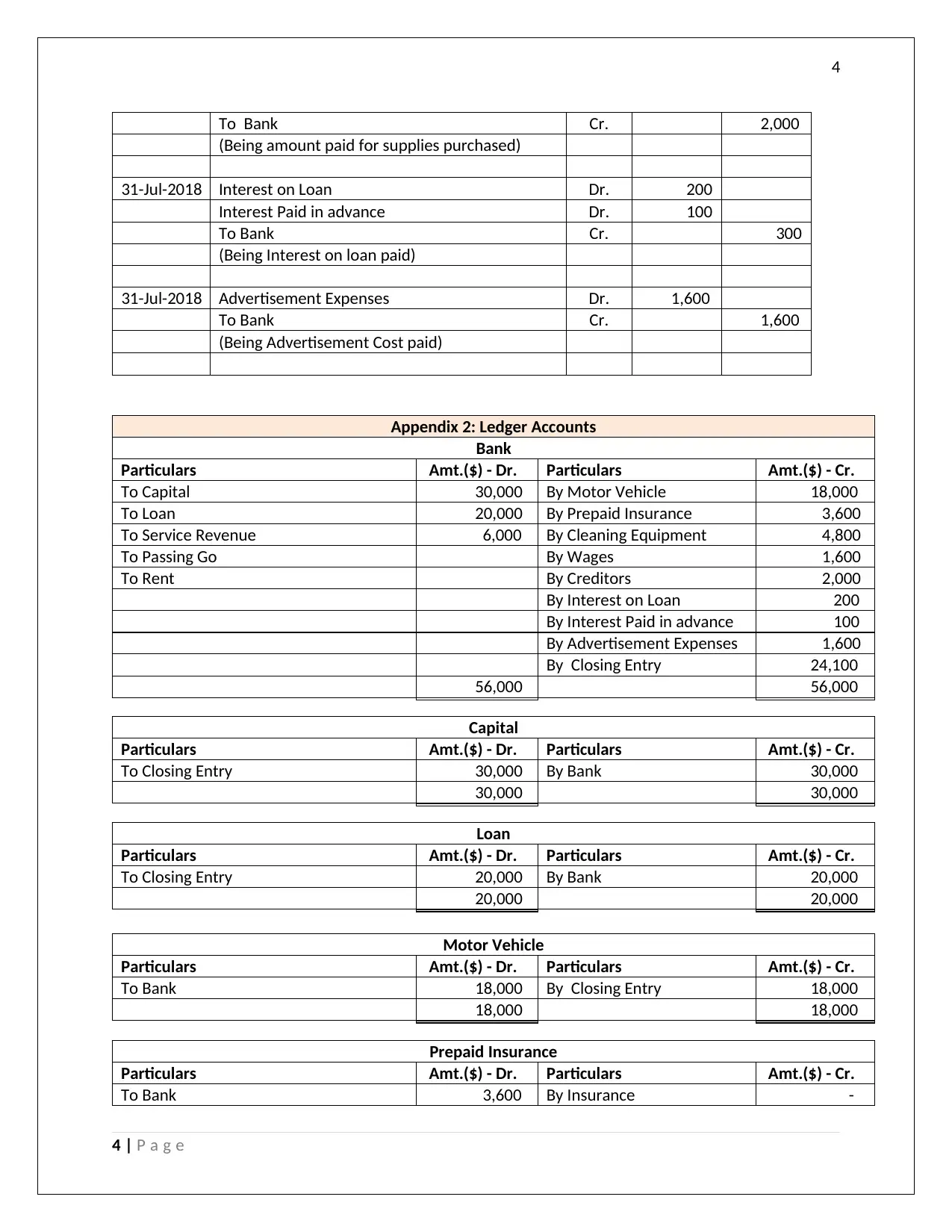

4

To Bank Cr. 2,000

(Being amount paid for supplies purchased)

31-Jul-2018 Interest on Loan Dr. 200

Interest Paid in advance Dr. 100

To Bank Cr. 300

(Being Interest on loan paid)

31-Jul-2018 Advertisement Expenses Dr. 1,600

To Bank Cr. 1,600

(Being Advertisement Cost paid)

Appendix 2: Ledger Accounts

Bank

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Capital 30,000 By Motor Vehicle 18,000

To Loan 20,000 By Prepaid Insurance 3,600

To Service Revenue 6,000 By Cleaning Equipment 4,800

To Passing Go By Wages 1,600

To Rent By Creditors 2,000

By Interest on Loan 200

By Interest Paid in advance 100

By Advertisement Expenses 1,600

By Closing Entry 24,100

56,000 56,000

Capital

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry 30,000 By Bank 30,000

30,000 30,000

Loan

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry 20,000 By Bank 20,000

20,000 20,000

Motor Vehicle

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 18,000 By Closing Entry 18,000

18,000 18,000

Prepaid Insurance

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 3,600 By Insurance -

4 | P a g e

To Bank Cr. 2,000

(Being amount paid for supplies purchased)

31-Jul-2018 Interest on Loan Dr. 200

Interest Paid in advance Dr. 100

To Bank Cr. 300

(Being Interest on loan paid)

31-Jul-2018 Advertisement Expenses Dr. 1,600

To Bank Cr. 1,600

(Being Advertisement Cost paid)

Appendix 2: Ledger Accounts

Bank

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Capital 30,000 By Motor Vehicle 18,000

To Loan 20,000 By Prepaid Insurance 3,600

To Service Revenue 6,000 By Cleaning Equipment 4,800

To Passing Go By Wages 1,600

To Rent By Creditors 2,000

By Interest on Loan 200

By Interest Paid in advance 100

By Advertisement Expenses 1,600

By Closing Entry 24,100

56,000 56,000

Capital

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry 30,000 By Bank 30,000

30,000 30,000

Loan

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry 20,000 By Bank 20,000

20,000 20,000

Motor Vehicle

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 18,000 By Closing Entry 18,000

18,000 18,000

Prepaid Insurance

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 3,600 By Insurance -

4 | P a g e

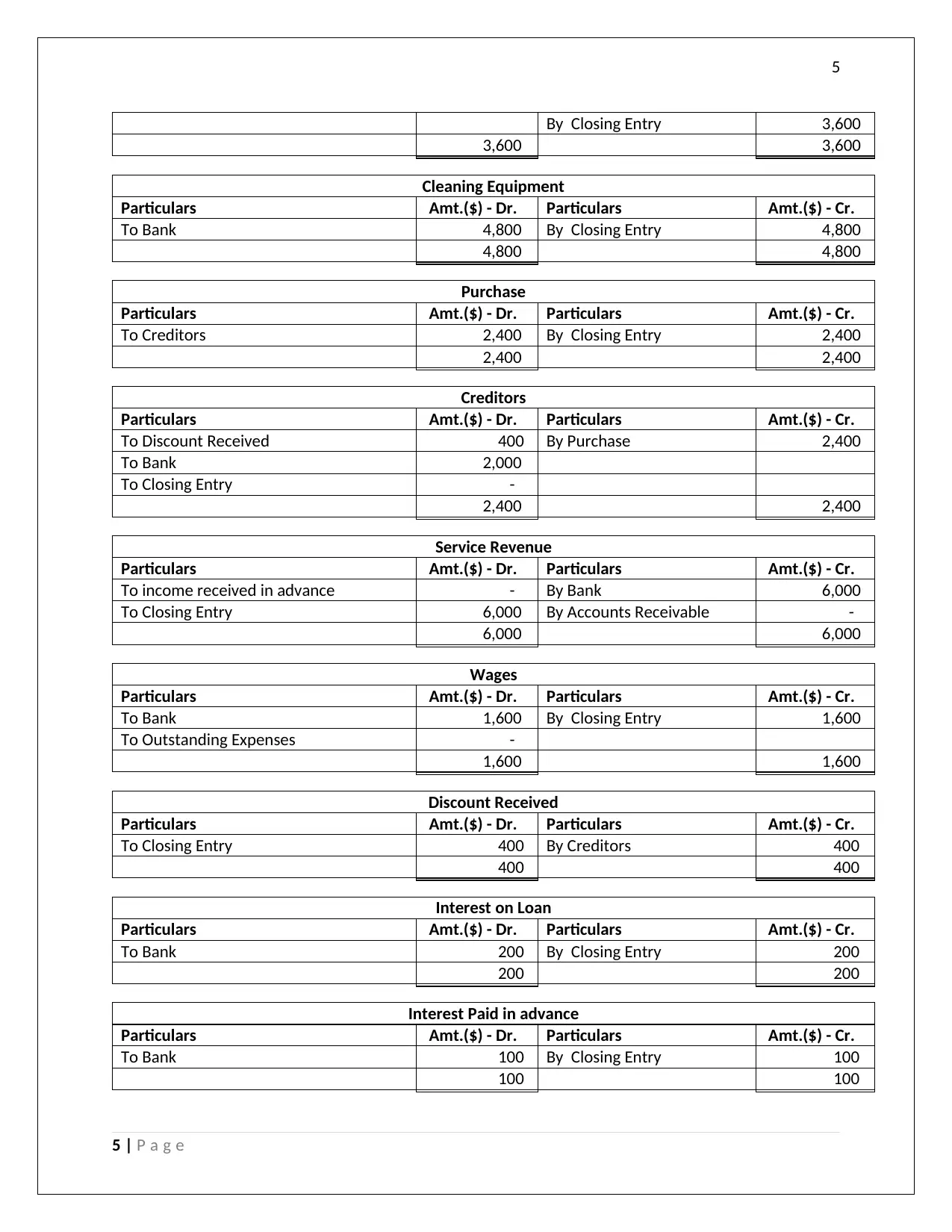

5

By Closing Entry 3,600

3,600 3,600

Cleaning Equipment

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 4,800 By Closing Entry 4,800

4,800 4,800

Purchase

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Creditors 2,400 By Closing Entry 2,400

2,400 2,400

Creditors

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Discount Received 400 By Purchase 2,400

To Bank 2,000

To Closing Entry -

2,400 2,400

Service Revenue

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To income received in advance - By Bank 6,000

To Closing Entry 6,000 By Accounts Receivable -

6,000 6,000

Wages

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 1,600 By Closing Entry 1,600

To Outstanding Expenses -

1,600 1,600

Discount Received

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry 400 By Creditors 400

400 400

Interest on Loan

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 200 By Closing Entry 200

200 200

Interest Paid in advance

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 100 By Closing Entry 100

100 100

5 | P a g e

By Closing Entry 3,600

3,600 3,600

Cleaning Equipment

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 4,800 By Closing Entry 4,800

4,800 4,800

Purchase

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Creditors 2,400 By Closing Entry 2,400

2,400 2,400

Creditors

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Discount Received 400 By Purchase 2,400

To Bank 2,000

To Closing Entry -

2,400 2,400

Service Revenue

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To income received in advance - By Bank 6,000

To Closing Entry 6,000 By Accounts Receivable -

6,000 6,000

Wages

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 1,600 By Closing Entry 1,600

To Outstanding Expenses -

1,600 1,600

Discount Received

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry 400 By Creditors 400

400 400

Interest on Loan

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 200 By Closing Entry 200

200 200

Interest Paid in advance

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 100 By Closing Entry 100

100 100

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

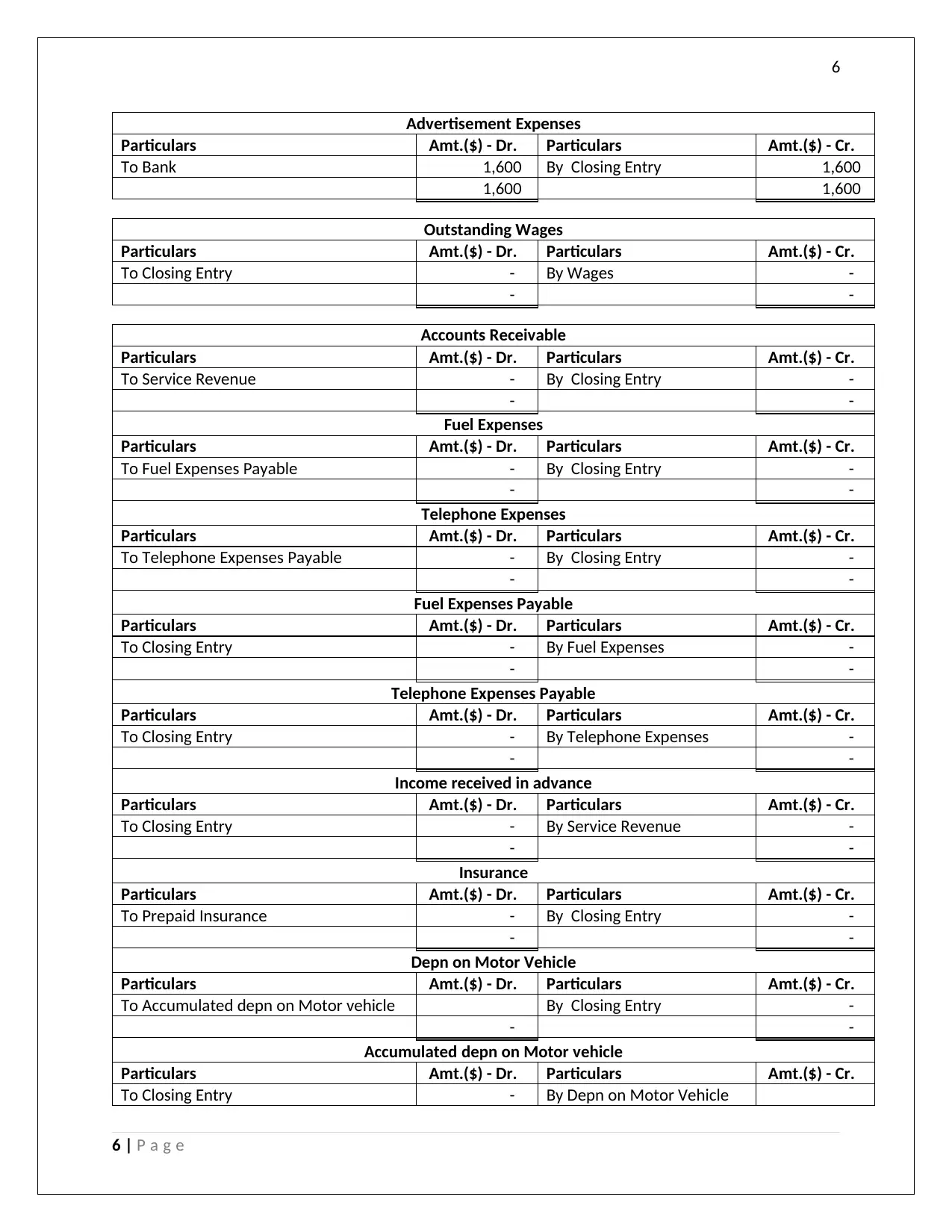

Advertisement Expenses

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 1,600 By Closing Entry 1,600

1,600 1,600

Outstanding Wages

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry - By Wages -

- -

Accounts Receivable

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Service Revenue - By Closing Entry -

- -

Fuel Expenses

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Fuel Expenses Payable - By Closing Entry -

- -

Telephone Expenses

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Telephone Expenses Payable - By Closing Entry -

- -

Fuel Expenses Payable

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry - By Fuel Expenses -

- -

Telephone Expenses Payable

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry - By Telephone Expenses -

- -

Income received in advance

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry - By Service Revenue -

- -

Insurance

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Prepaid Insurance - By Closing Entry -

- -

Depn on Motor Vehicle

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Accumulated depn on Motor vehicle By Closing Entry -

- -

Accumulated depn on Motor vehicle

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry - By Depn on Motor Vehicle

6 | P a g e

Advertisement Expenses

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Bank 1,600 By Closing Entry 1,600

1,600 1,600

Outstanding Wages

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry - By Wages -

- -

Accounts Receivable

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Service Revenue - By Closing Entry -

- -

Fuel Expenses

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Fuel Expenses Payable - By Closing Entry -

- -

Telephone Expenses

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Telephone Expenses Payable - By Closing Entry -

- -

Fuel Expenses Payable

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry - By Fuel Expenses -

- -

Telephone Expenses Payable

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry - By Telephone Expenses -

- -

Income received in advance

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry - By Service Revenue -

- -

Insurance

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Prepaid Insurance - By Closing Entry -

- -

Depn on Motor Vehicle

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Accumulated depn on Motor vehicle By Closing Entry -

- -

Accumulated depn on Motor vehicle

Particulars Amt.($) - Dr. Particulars Amt.($) - Cr.

To Closing Entry - By Depn on Motor Vehicle

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

- -

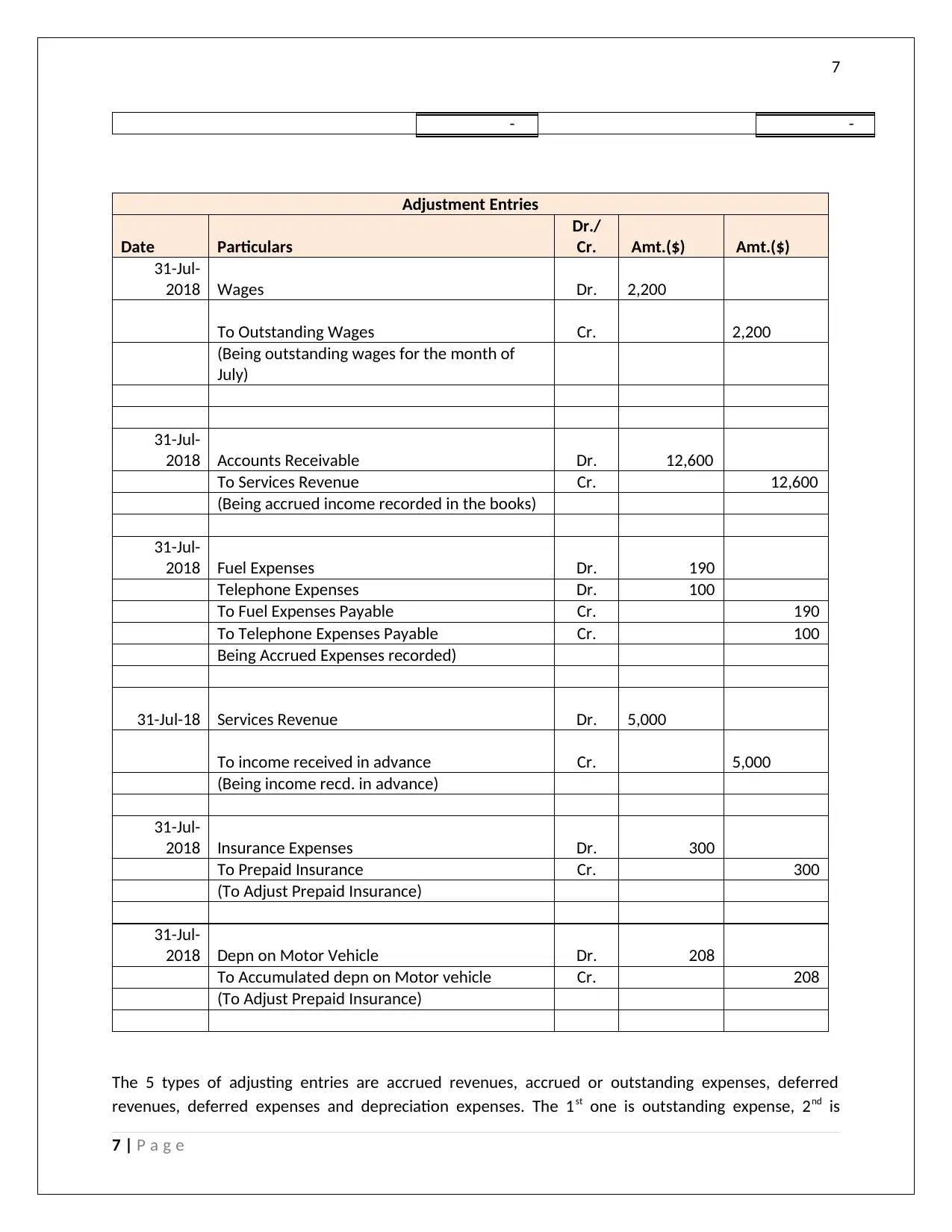

Adjustment Entries

Date Particulars

Dr./

Cr. Amt.($) Amt.($)

31-Jul-

2018 Wages Dr. 2,200

To Outstanding Wages Cr. 2,200

(Being outstanding wages for the month of

July)

31-Jul-

2018 Accounts Receivable Dr. 12,600

To Services Revenue Cr. 12,600

(Being accrued income recorded in the books)

31-Jul-

2018 Fuel Expenses Dr. 190

Telephone Expenses Dr. 100

To Fuel Expenses Payable Cr. 190

To Telephone Expenses Payable Cr. 100

Being Accrued Expenses recorded)

31-Jul-18 Services Revenue Dr. 5,000

To income received in advance Cr. 5,000

(Being income recd. in advance)

31-Jul-

2018 Insurance Expenses Dr. 300

To Prepaid Insurance Cr. 300

(To Adjust Prepaid Insurance)

31-Jul-

2018 Depn on Motor Vehicle Dr. 208

To Accumulated depn on Motor vehicle Cr. 208

(To Adjust Prepaid Insurance)

The 5 types of adjusting entries are accrued revenues, accrued or outstanding expenses, deferred

revenues, deferred expenses and depreciation expenses. The 1st one is outstanding expense, 2nd is

7 | P a g e

- -

Adjustment Entries

Date Particulars

Dr./

Cr. Amt.($) Amt.($)

31-Jul-

2018 Wages Dr. 2,200

To Outstanding Wages Cr. 2,200

(Being outstanding wages for the month of

July)

31-Jul-

2018 Accounts Receivable Dr. 12,600

To Services Revenue Cr. 12,600

(Being accrued income recorded in the books)

31-Jul-

2018 Fuel Expenses Dr. 190

Telephone Expenses Dr. 100

To Fuel Expenses Payable Cr. 190

To Telephone Expenses Payable Cr. 100

Being Accrued Expenses recorded)

31-Jul-18 Services Revenue Dr. 5,000

To income received in advance Cr. 5,000

(Being income recd. in advance)

31-Jul-

2018 Insurance Expenses Dr. 300

To Prepaid Insurance Cr. 300

(To Adjust Prepaid Insurance)

31-Jul-

2018 Depn on Motor Vehicle Dr. 208

To Accumulated depn on Motor vehicle Cr. 208

(To Adjust Prepaid Insurance)

The 5 types of adjusting entries are accrued revenues, accrued or outstanding expenses, deferred

revenues, deferred expenses and depreciation expenses. The 1st one is outstanding expense, 2nd is

7 | P a g e

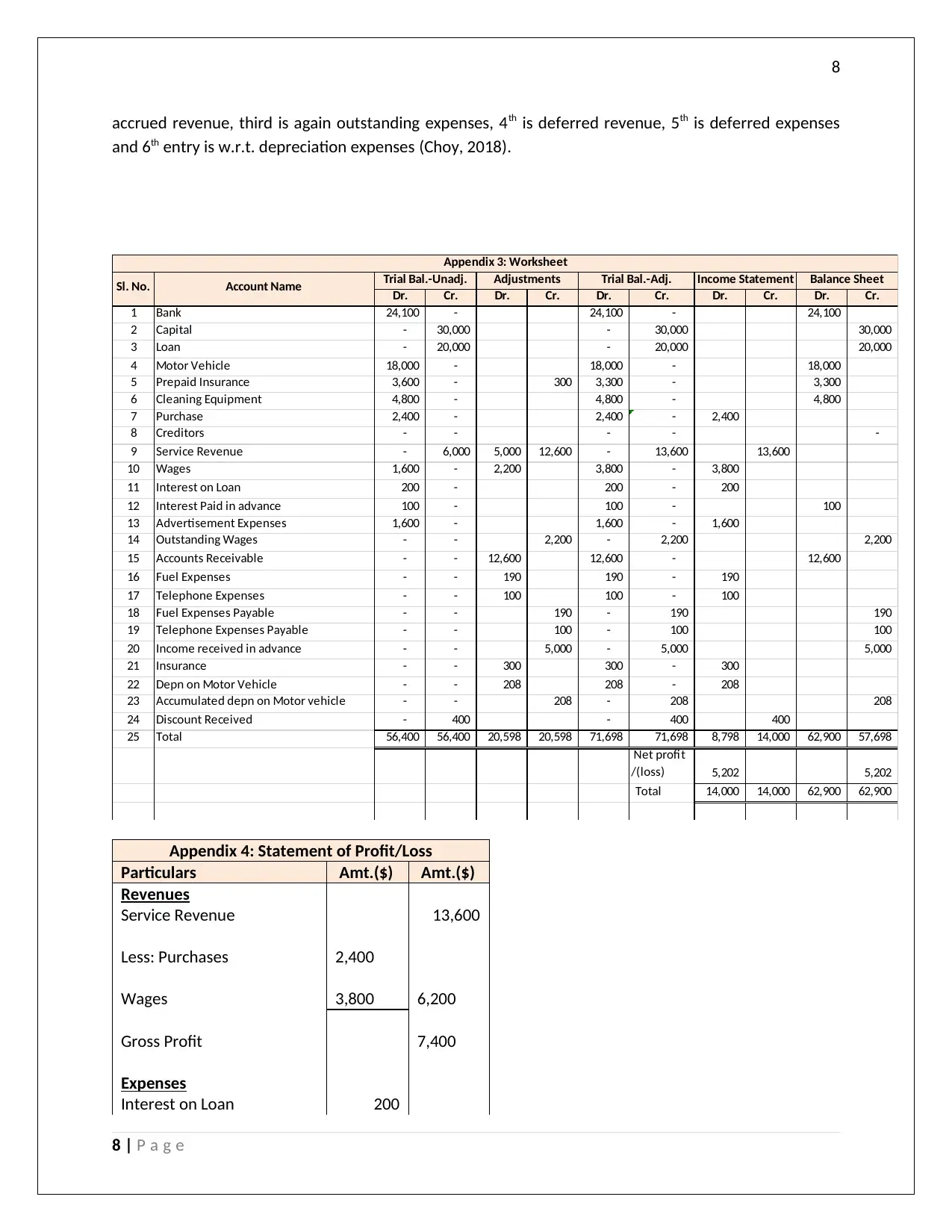

8

accrued revenue, third is again outstanding expenses, 4th is deferred revenue, 5th is deferred expenses

and 6th entry is w.r.t. depreciation expenses (Choy, 2018).

Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr.

1 Bank 24,100 - 24,100 - 24,100

2 Capital - 30,000 - 30,000 30,000

3 Loan - 20,000 - 20,000 20,000

4 Motor Vehicle 18,000 - 18,000 - 18,000

5 Prepaid Insurance 3,600 - 300 3,300 - 3,300

6 Cleaning Equipment 4,800 - 4,800 - 4,800

7 Purchase 2,400 - 2,400 - 2,400

8 Creditors - - - - -

9 Service Revenue - 6,000 5,000 12,600 - 13,600 13,600

10 Wages 1,600 - 2,200 3,800 - 3,800

11 Interest on Loan 200 - 200 - 200

12 Interest Paid in advance 100 - 100 - 100

13 Advertisement Expenses 1,600 - 1,600 - 1,600

14 Outstanding Wages - - 2,200 - 2,200 2,200

15 Accounts Receivable - - 12,600 12,600 - 12,600

16 Fuel Expenses - - 190 190 - 190

17 Telephone Expenses - - 100 100 - 100

18 Fuel Expenses Payable - - 190 - 190 190

19 Telephone Expenses Payable - - 100 - 100 100

20 Income received in advance - - 5,000 - 5,000 5,000

21 Insurance - - 300 300 - 300

22 Depn on Motor Vehicle - - 208 208 - 208

23 Accumulated depn on Motor vehicle - - 208 - 208 208

24 Discount Received - 400 - 400 400

25 Total 56,400 56,400 20,598 20,598 71,698 71,698 8,798 14,000 62,900 57,698

Net profit

/(loss) 5,202 5,202

Total 14,000 14,000 62,900 62,900

Account NameSl. No.

Appendix 3: Worksheet

Trial Bal.-Adj.Trial Bal.-Unadj. Adjustments Income Statement Balance Sheet

Appendix 4: Statement of Profit/Loss

Particulars Amt.($) Amt.($)

Revenues

Service Revenue 13,600

Less: Purchases 2,400

Wages 3,800 6,200

Gross Profit 7,400

Expenses

Interest on Loan 200

8 | P a g e

accrued revenue, third is again outstanding expenses, 4th is deferred revenue, 5th is deferred expenses

and 6th entry is w.r.t. depreciation expenses (Choy, 2018).

Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr.

1 Bank 24,100 - 24,100 - 24,100

2 Capital - 30,000 - 30,000 30,000

3 Loan - 20,000 - 20,000 20,000

4 Motor Vehicle 18,000 - 18,000 - 18,000

5 Prepaid Insurance 3,600 - 300 3,300 - 3,300

6 Cleaning Equipment 4,800 - 4,800 - 4,800

7 Purchase 2,400 - 2,400 - 2,400

8 Creditors - - - - -

9 Service Revenue - 6,000 5,000 12,600 - 13,600 13,600

10 Wages 1,600 - 2,200 3,800 - 3,800

11 Interest on Loan 200 - 200 - 200

12 Interest Paid in advance 100 - 100 - 100

13 Advertisement Expenses 1,600 - 1,600 - 1,600

14 Outstanding Wages - - 2,200 - 2,200 2,200

15 Accounts Receivable - - 12,600 12,600 - 12,600

16 Fuel Expenses - - 190 190 - 190

17 Telephone Expenses - - 100 100 - 100

18 Fuel Expenses Payable - - 190 - 190 190

19 Telephone Expenses Payable - - 100 - 100 100

20 Income received in advance - - 5,000 - 5,000 5,000

21 Insurance - - 300 300 - 300

22 Depn on Motor Vehicle - - 208 208 - 208

23 Accumulated depn on Motor vehicle - - 208 - 208 208

24 Discount Received - 400 - 400 400

25 Total 56,400 56,400 20,598 20,598 71,698 71,698 8,798 14,000 62,900 57,698

Net profit

/(loss) 5,202 5,202

Total 14,000 14,000 62,900 62,900

Account NameSl. No.

Appendix 3: Worksheet

Trial Bal.-Adj.Trial Bal.-Unadj. Adjustments Income Statement Balance Sheet

Appendix 4: Statement of Profit/Loss

Particulars Amt.($) Amt.($)

Revenues

Service Revenue 13,600

Less: Purchases 2,400

Wages 3,800 6,200

Gross Profit 7,400

Expenses

Interest on Loan 200

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

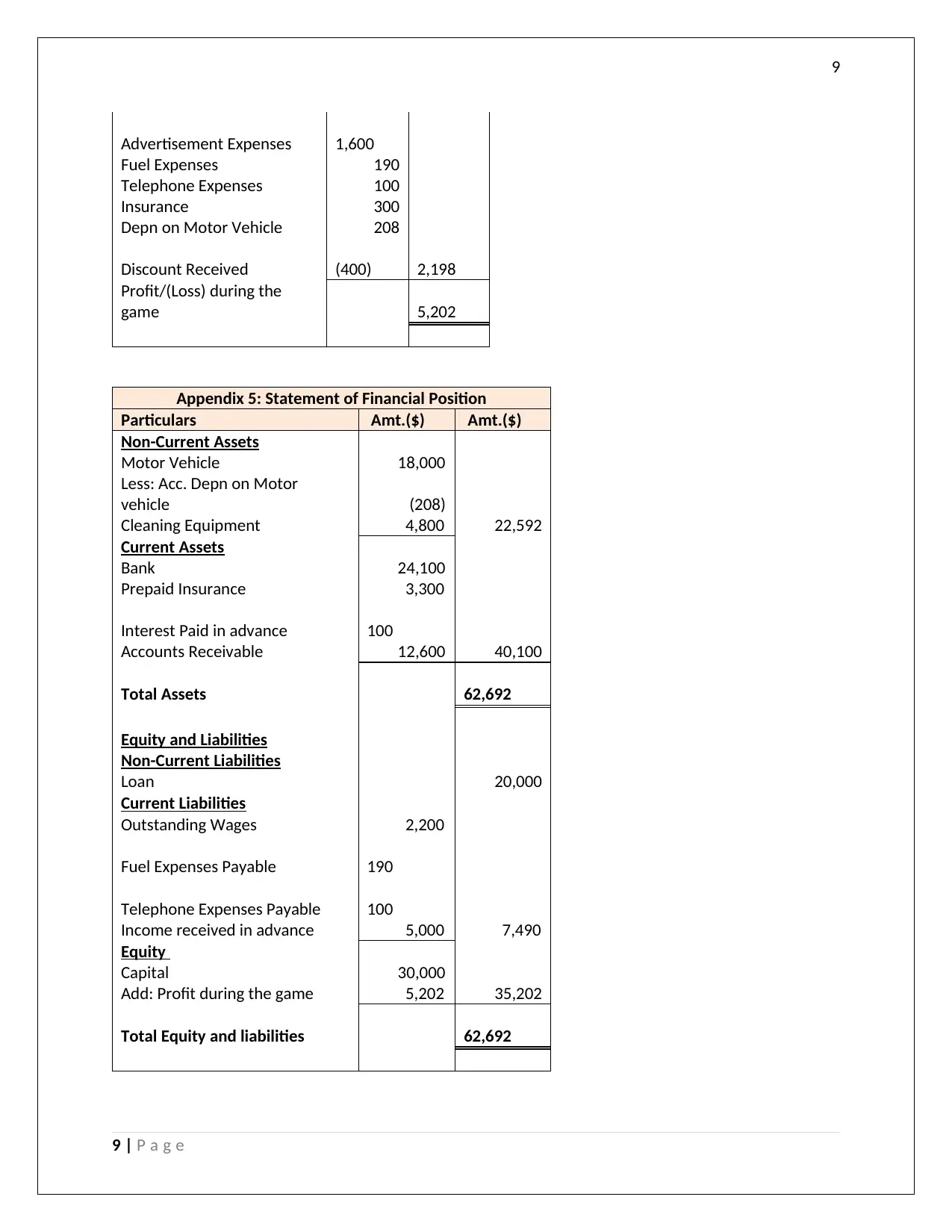

Advertisement Expenses 1,600

Fuel Expenses 190

Telephone Expenses 100

Insurance 300

Depn on Motor Vehicle 208

Discount Received (400) 2,198

Profit/(Loss) during the

game 5,202

Appendix 5: Statement of Financial Position

Particulars Amt.($) Amt.($)

Non-Current Assets

Motor Vehicle 18,000

Less: Acc. Depn on Motor

vehicle (208)

Cleaning Equipment 4,800 22,592

Current Assets

Bank 24,100

Prepaid Insurance 3,300

Interest Paid in advance 100

Accounts Receivable 12,600 40,100

Total Assets 62,692

Equity and Liabilities

Non-Current Liabilities

Loan 20,000

Current Liabilities

Outstanding Wages 2,200

Fuel Expenses Payable 190

Telephone Expenses Payable 100

Income received in advance 5,000 7,490

Equity

Capital 30,000

Add: Profit during the game 5,202 35,202

Total Equity and liabilities 62,692

9 | P a g e

Advertisement Expenses 1,600

Fuel Expenses 190

Telephone Expenses 100

Insurance 300

Depn on Motor Vehicle 208

Discount Received (400) 2,198

Profit/(Loss) during the

game 5,202

Appendix 5: Statement of Financial Position

Particulars Amt.($) Amt.($)

Non-Current Assets

Motor Vehicle 18,000

Less: Acc. Depn on Motor

vehicle (208)

Cleaning Equipment 4,800 22,592

Current Assets

Bank 24,100

Prepaid Insurance 3,300

Interest Paid in advance 100

Accounts Receivable 12,600 40,100

Total Assets 62,692

Equity and Liabilities

Non-Current Liabilities

Loan 20,000

Current Liabilities

Outstanding Wages 2,200

Fuel Expenses Payable 190

Telephone Expenses Payable 100

Income received in advance 5,000 7,490

Equity

Capital 30,000

Add: Profit during the game 5,202 35,202

Total Equity and liabilities 62,692

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

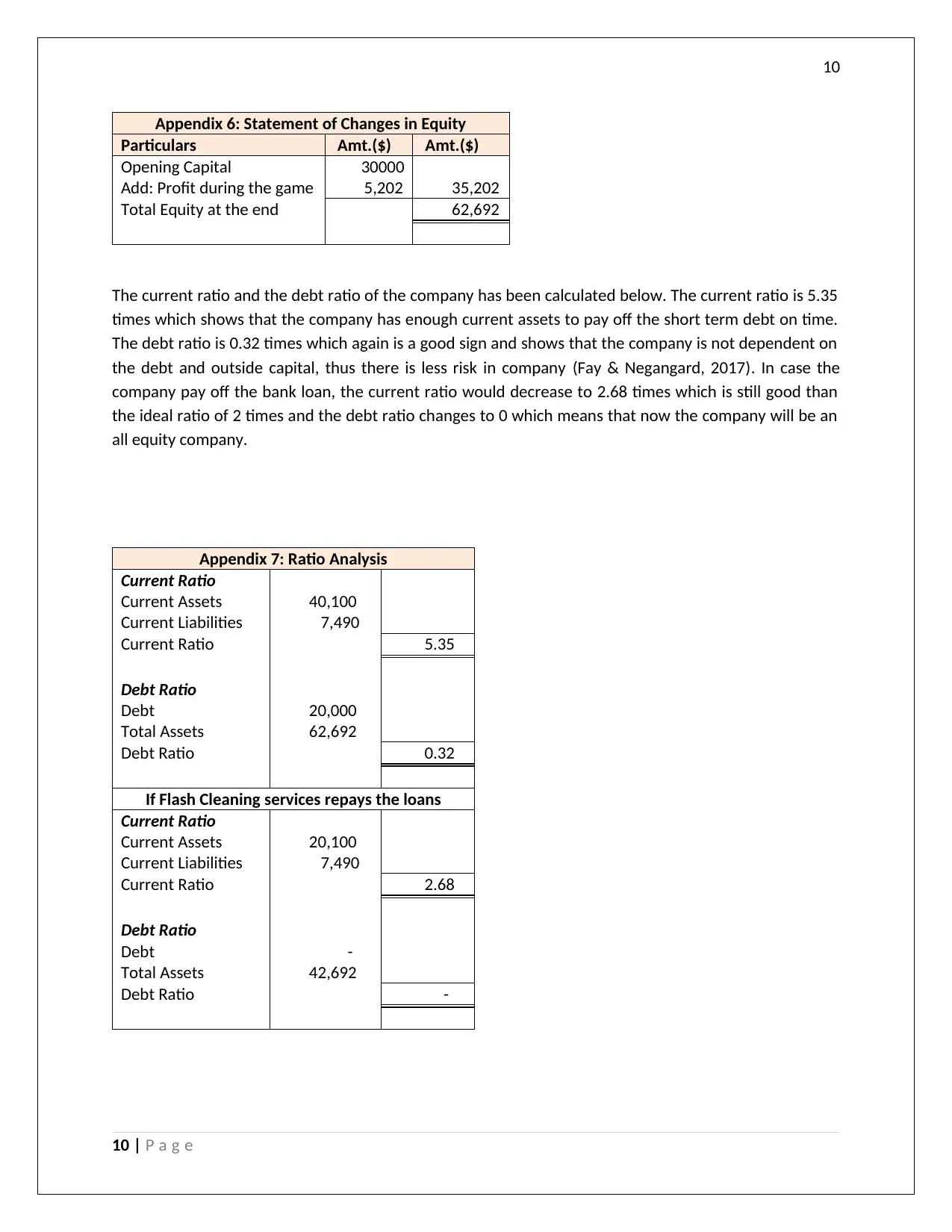

Appendix 6: Statement of Changes in Equity

Particulars Amt.($) Amt.($)

Opening Capital 30000

Add: Profit during the game 5,202 35,202

Total Equity at the end 62,692

The current ratio and the debt ratio of the company has been calculated below. The current ratio is 5.35

times which shows that the company has enough current assets to pay off the short term debt on time.

The debt ratio is 0.32 times which again is a good sign and shows that the company is not dependent on

the debt and outside capital, thus there is less risk in company (Fay & Negangard, 2017). In case the

company pay off the bank loan, the current ratio would decrease to 2.68 times which is still good than

the ideal ratio of 2 times and the debt ratio changes to 0 which means that now the company will be an

all equity company.

Appendix 7: Ratio Analysis

Current Ratio

Current Assets 40,100

Current Liabilities 7,490

Current Ratio 5.35

Debt Ratio

Debt 20,000

Total Assets 62,692

Debt Ratio 0.32

If Flash Cleaning services repays the loans

Current Ratio

Current Assets 20,100

Current Liabilities 7,490

Current Ratio 2.68

Debt Ratio

Debt -

Total Assets 42,692

Debt Ratio -

10 | P a g e

Appendix 6: Statement of Changes in Equity

Particulars Amt.($) Amt.($)

Opening Capital 30000

Add: Profit during the game 5,202 35,202

Total Equity at the end 62,692

The current ratio and the debt ratio of the company has been calculated below. The current ratio is 5.35

times which shows that the company has enough current assets to pay off the short term debt on time.

The debt ratio is 0.32 times which again is a good sign and shows that the company is not dependent on

the debt and outside capital, thus there is less risk in company (Fay & Negangard, 2017). In case the

company pay off the bank loan, the current ratio would decrease to 2.68 times which is still good than

the ideal ratio of 2 times and the debt ratio changes to 0 which means that now the company will be an

all equity company.

Appendix 7: Ratio Analysis

Current Ratio

Current Assets 40,100

Current Liabilities 7,490

Current Ratio 5.35

Debt Ratio

Debt 20,000

Total Assets 62,692

Debt Ratio 0.32

If Flash Cleaning services repays the loans

Current Ratio

Current Assets 20,100

Current Liabilities 7,490

Current Ratio 2.68

Debt Ratio

Debt -

Total Assets 42,692

Debt Ratio -

10 | P a g e

11

Question 2: History of accounting - essay

Double Entry bookkeeping is one of the concepts of recording the accounting transaction in the books of

accounts which has an impact on the two sides of company finances. It has two legs of the transaction,

which can be an asset, liability, income, expense or equity. For example, if the company sells the goods,

it has an impact on the revenue and also the cash account (Jefferson, 2017).

The Italian Luca Pacioli, who is considered to be the Father of Accounting and Bookkeeping was the first

person to introduce the concept of double entry book keeping and introduced it in Italy. In the 13 th

century, when medieval Europe moved towards the monetary transaction, most of the merchants were

dependent on the bookkeeping for effecting and recording the multiple transactions with the bank. It

was at that time that one of the most important breakthrough in the field of accounting took place and

double entry bookkeeping got introduced where each transaction had 2 legs namely debit and the credit

leg (Heminway, 2017). The words are derived from the Latin words debitum and creditum which means

“what is due” and “something entrusted to another or loan”. The double entry book keeping system

replaced the earlier used single entry book keeping system. It is believed that the double entry

bookkeeping was pioneered in the Jewish community and when the Italian merchants discussed on this

system with the Jewish counterparts, they implemented the same. The earliest evidence of the same is

found in Farolfi ledger in 1299-1300 period (Linden & Freeman, 2017). The oldest discovered record

which has been found on the given subject is Messari (Treasurer’s in Italian) accounts in Genoa city in

1340. It contains debits and credits being recorded in the bilateral form and the carry forward balances

from the previous year and hence the complete evidence of double entry system. Luca Pacioli's

renowned works namely Summa de Arithmetica, Geometria, Proportioni et Proportionalità (early Italian:

"Review of Arithmetic, Geometry, Ratio and Proportion") which were first printed and published in

Venice in 1494 are considered to be the first known printed material on bookkeeping rules and

regulations. Although he did not invent the double entry system but his 27 page work on bookkeeping,

"Particularis de Computis et Scripturis" (Latin: "Details of Calculation and Recording") is considered to

have laid foundation for what is being practiced today as double entry bookkeeping (Goldmann, 2016).

Off late the double entry system has become profoundly significant and important in the world of

accounting due to the complete cycle of transaction being recorded under this system. This is simple and

easy to understand and interpret. It has approaches namely traditional approach and the accounting

equation approach. The benefit with this system is that multiple debits and credits can be posted at the

same time such the sum total of all the debits and the credits is same. It thus also acts as a check of the

correct recording of the entries (Van Rinsum, 2018). Since both the debit and credit aspect of the entry

have the same date so the error if any can be identified quickly for both the legs of the transaction and

thus it also serves as the audit trail. The two approaches to accounting are mentioned below:

1. Traditional Approach: Also called as British Approach, it classifies all the accounts into real,

personal and nominal accounts and the following rule is used while accounting.

“Real account: Debit what comes in and credit what goes out.

Personal account: Debit the receiver and credit the giver.

Nominal account: Debit all expenses & losses and credit all incomes & gains”

11 | P a g e

Question 2: History of accounting - essay

Double Entry bookkeeping is one of the concepts of recording the accounting transaction in the books of

accounts which has an impact on the two sides of company finances. It has two legs of the transaction,

which can be an asset, liability, income, expense or equity. For example, if the company sells the goods,

it has an impact on the revenue and also the cash account (Jefferson, 2017).

The Italian Luca Pacioli, who is considered to be the Father of Accounting and Bookkeeping was the first

person to introduce the concept of double entry book keeping and introduced it in Italy. In the 13 th

century, when medieval Europe moved towards the monetary transaction, most of the merchants were

dependent on the bookkeeping for effecting and recording the multiple transactions with the bank. It

was at that time that one of the most important breakthrough in the field of accounting took place and

double entry bookkeeping got introduced where each transaction had 2 legs namely debit and the credit

leg (Heminway, 2017). The words are derived from the Latin words debitum and creditum which means

“what is due” and “something entrusted to another or loan”. The double entry book keeping system

replaced the earlier used single entry book keeping system. It is believed that the double entry

bookkeeping was pioneered in the Jewish community and when the Italian merchants discussed on this

system with the Jewish counterparts, they implemented the same. The earliest evidence of the same is

found in Farolfi ledger in 1299-1300 period (Linden & Freeman, 2017). The oldest discovered record

which has been found on the given subject is Messari (Treasurer’s in Italian) accounts in Genoa city in

1340. It contains debits and credits being recorded in the bilateral form and the carry forward balances

from the previous year and hence the complete evidence of double entry system. Luca Pacioli's

renowned works namely Summa de Arithmetica, Geometria, Proportioni et Proportionalità (early Italian:

"Review of Arithmetic, Geometry, Ratio and Proportion") which were first printed and published in

Venice in 1494 are considered to be the first known printed material on bookkeeping rules and

regulations. Although he did not invent the double entry system but his 27 page work on bookkeeping,

"Particularis de Computis et Scripturis" (Latin: "Details of Calculation and Recording") is considered to

have laid foundation for what is being practiced today as double entry bookkeeping (Goldmann, 2016).

Off late the double entry system has become profoundly significant and important in the world of

accounting due to the complete cycle of transaction being recorded under this system. This is simple and

easy to understand and interpret. It has approaches namely traditional approach and the accounting

equation approach. The benefit with this system is that multiple debits and credits can be posted at the

same time such the sum total of all the debits and the credits is same. It thus also acts as a check of the

correct recording of the entries (Van Rinsum, 2018). Since both the debit and credit aspect of the entry

have the same date so the error if any can be identified quickly for both the legs of the transaction and

thus it also serves as the audit trail. The two approaches to accounting are mentioned below:

1. Traditional Approach: Also called as British Approach, it classifies all the accounts into real,

personal and nominal accounts and the following rule is used while accounting.

“Real account: Debit what comes in and credit what goes out.

Personal account: Debit the receiver and credit the giver.

Nominal account: Debit all expenses & losses and credit all incomes & gains”

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.