Accounting Case Study: Cost-Volume-Profit Analysis and Decision Making

VerifiedAdded on 2023/06/15

|15

|2324

|372

Case Study

AI Summary

This assignment presents a detailed solution to three case studies related to managerial accounting. The first case study involves estimating the contribution to a charity event by analyzing variable and fixed costs using the high-low method, and determining the optimal bidding strategy for a catering contract. The second case study focuses on break-even analysis, contribution margin calculations, and deciding between hiring an internal sales force versus external agents based on profitability. The third case study examines the impact of acquiring an automated milling machine on overhead rates, product costs, and the accuracy of cost savings calculations, revealing potential errors in initial assessments and the consequences of increased overhead costs. The document is available on Desklib, a platform offering a range of study tools and solved assignments for students.

Running head: ACCOUNTS

ACCOUNTS

Name of the Student

Name of the University

Author Note

ACCOUNTS

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTS

Table of Contents

Case study 1:....................................................................................................................................3

Answer to Question 1..................................................................................................................3

Answer to Question 2..................................................................................................................4

Answer to Question 3..................................................................................................................4

Case study 2.....................................................................................................................................5

Answer to Question 1..................................................................................................................5

Answer to Question 2..................................................................................................................5

Answer to Question 3..................................................................................................................6

Answer to Question 4..................................................................................................................6

Answer to Question 5..................................................................................................................6

Answer to Question 6..................................................................................................................7

Case study 3.....................................................................................................................................8

Answer to Question 1..................................................................................................................8

Answer to Question 2..................................................................................................................8

Answer to Question 3..................................................................................................................8

Answer to Question 4..................................................................................................................8

References......................................................................................................................................10

Appendices....................................................................................................................................11

Appendix 1.................................................................................................................................11

Table of Contents

Case study 1:....................................................................................................................................3

Answer to Question 1..................................................................................................................3

Answer to Question 2..................................................................................................................4

Answer to Question 3..................................................................................................................4

Case study 2.....................................................................................................................................5

Answer to Question 1..................................................................................................................5

Answer to Question 2..................................................................................................................5

Answer to Question 3..................................................................................................................6

Answer to Question 4..................................................................................................................6

Answer to Question 5..................................................................................................................6

Answer to Question 6..................................................................................................................7

Case study 3.....................................................................................................................................8

Answer to Question 1..................................................................................................................8

Answer to Question 2..................................................................................................................8

Answer to Question 3..................................................................................................................8

Answer to Question 4..................................................................................................................8

References......................................................................................................................................10

Appendices....................................................................................................................................11

Appendix 1.................................................................................................................................11

2ACCOUNTS

Appendix 2.................................................................................................................................11

Appendix 3.................................................................................................................................13

Appendix 4.................................................................................................................................14

Appendix 2.................................................................................................................................11

Appendix 3.................................................................................................................................13

Appendix 4.................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTS

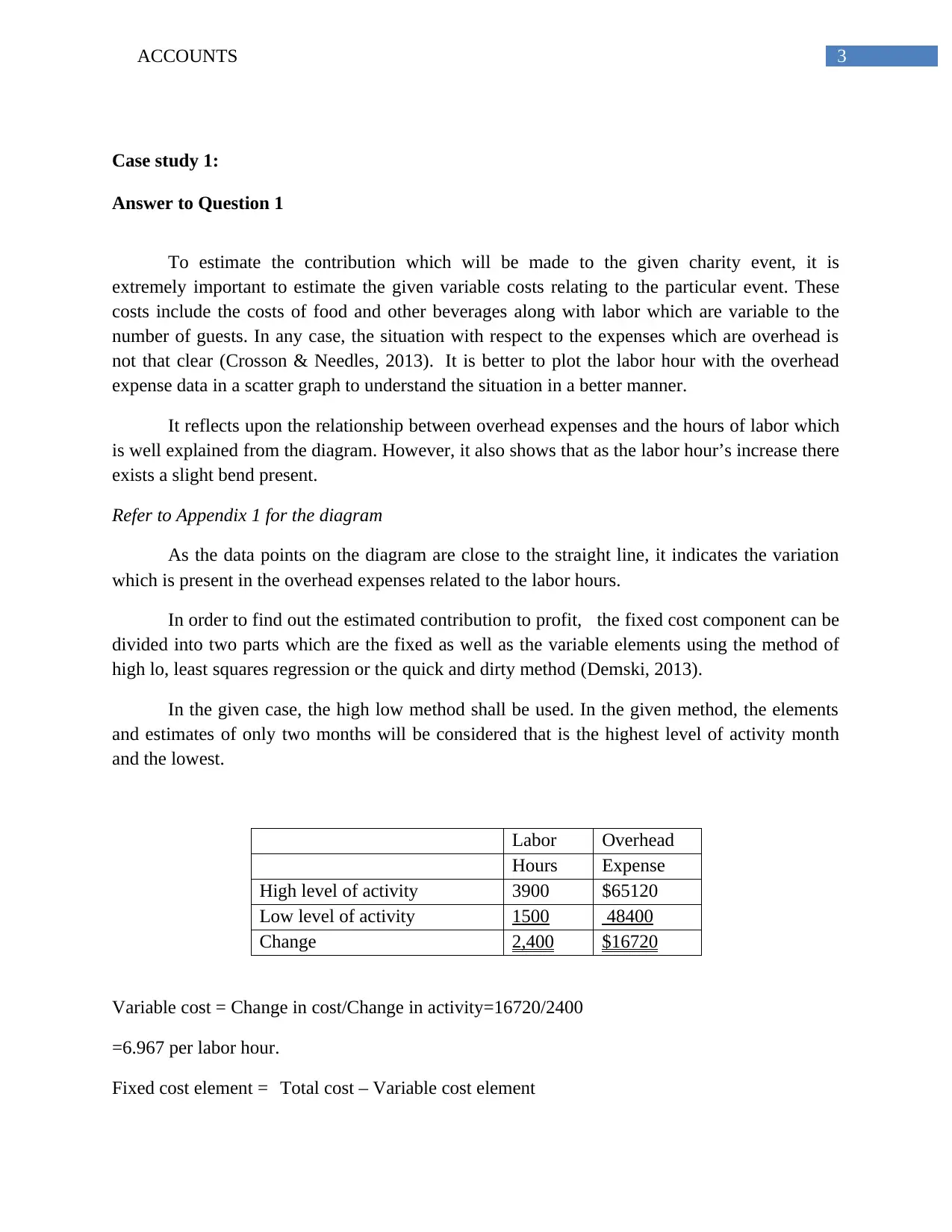

Case study 1:

Answer to Question 1

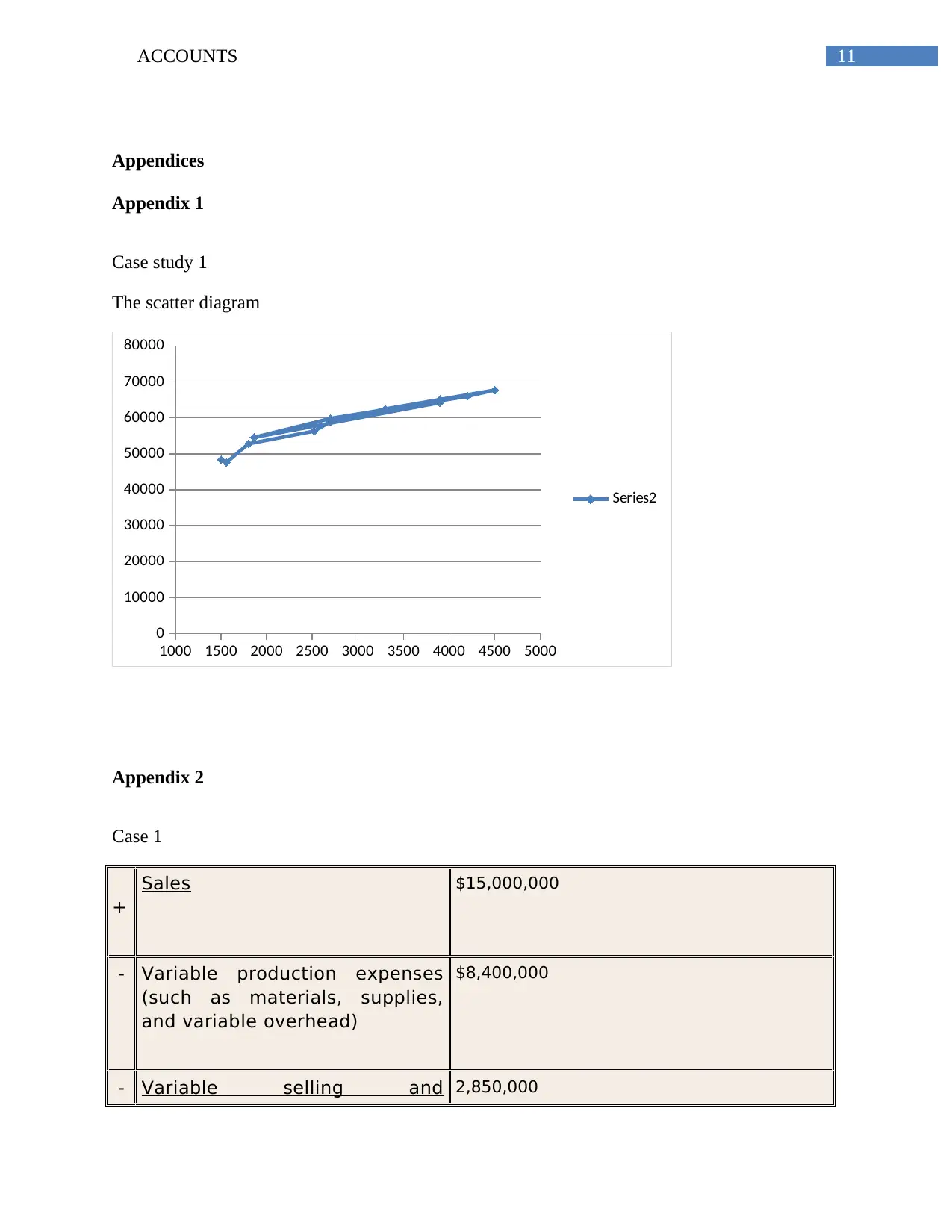

To estimate the contribution which will be made to the given charity event, it is

extremely important to estimate the given variable costs relating to the particular event. These

costs include the costs of food and other beverages along with labor which are variable to the

number of guests. In any case, the situation with respect to the expenses which are overhead is

not that clear (Crosson & Needles, 2013). It is better to plot the labor hour with the overhead

expense data in a scatter graph to understand the situation in a better manner.

It reflects upon the relationship between overhead expenses and the hours of labor which

is well explained from the diagram. However, it also shows that as the labor hour’s increase there

exists a slight bend present.

Refer to Appendix 1 for the diagram

As the data points on the diagram are close to the straight line, it indicates the variation

which is present in the overhead expenses related to the labor hours.

In order to find out the estimated contribution to profit, the fixed cost component can be

divided into two parts which are the fixed as well as the variable elements using the method of

high lo, least squares regression or the quick and dirty method (Demski, 2013).

In the given case, the high low method shall be used. In the given method, the elements

and estimates of only two months will be considered that is the highest level of activity month

and the lowest.

Labor Overhead

Hours Expense

High level of activity 3900 $65120

Low level of activity 1500 48400

Change 2,400 $16720

Variable cost = Change in cost/Change in activity=16720/2400

=6.967 per labor hour.

Fixed cost element = Total cost – Variable cost element

Case study 1:

Answer to Question 1

To estimate the contribution which will be made to the given charity event, it is

extremely important to estimate the given variable costs relating to the particular event. These

costs include the costs of food and other beverages along with labor which are variable to the

number of guests. In any case, the situation with respect to the expenses which are overhead is

not that clear (Crosson & Needles, 2013). It is better to plot the labor hour with the overhead

expense data in a scatter graph to understand the situation in a better manner.

It reflects upon the relationship between overhead expenses and the hours of labor which

is well explained from the diagram. However, it also shows that as the labor hour’s increase there

exists a slight bend present.

Refer to Appendix 1 for the diagram

As the data points on the diagram are close to the straight line, it indicates the variation

which is present in the overhead expenses related to the labor hours.

In order to find out the estimated contribution to profit, the fixed cost component can be

divided into two parts which are the fixed as well as the variable elements using the method of

high lo, least squares regression or the quick and dirty method (Demski, 2013).

In the given case, the high low method shall be used. In the given method, the elements

and estimates of only two months will be considered that is the highest level of activity month

and the lowest.

Labor Overhead

Hours Expense

High level of activity 3900 $65120

Low level of activity 1500 48400

Change 2,400 $16720

Variable cost = Change in cost/Change in activity=16720/2400

=6.967 per labor hour.

Fixed cost element = Total cost – Variable cost element

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTS

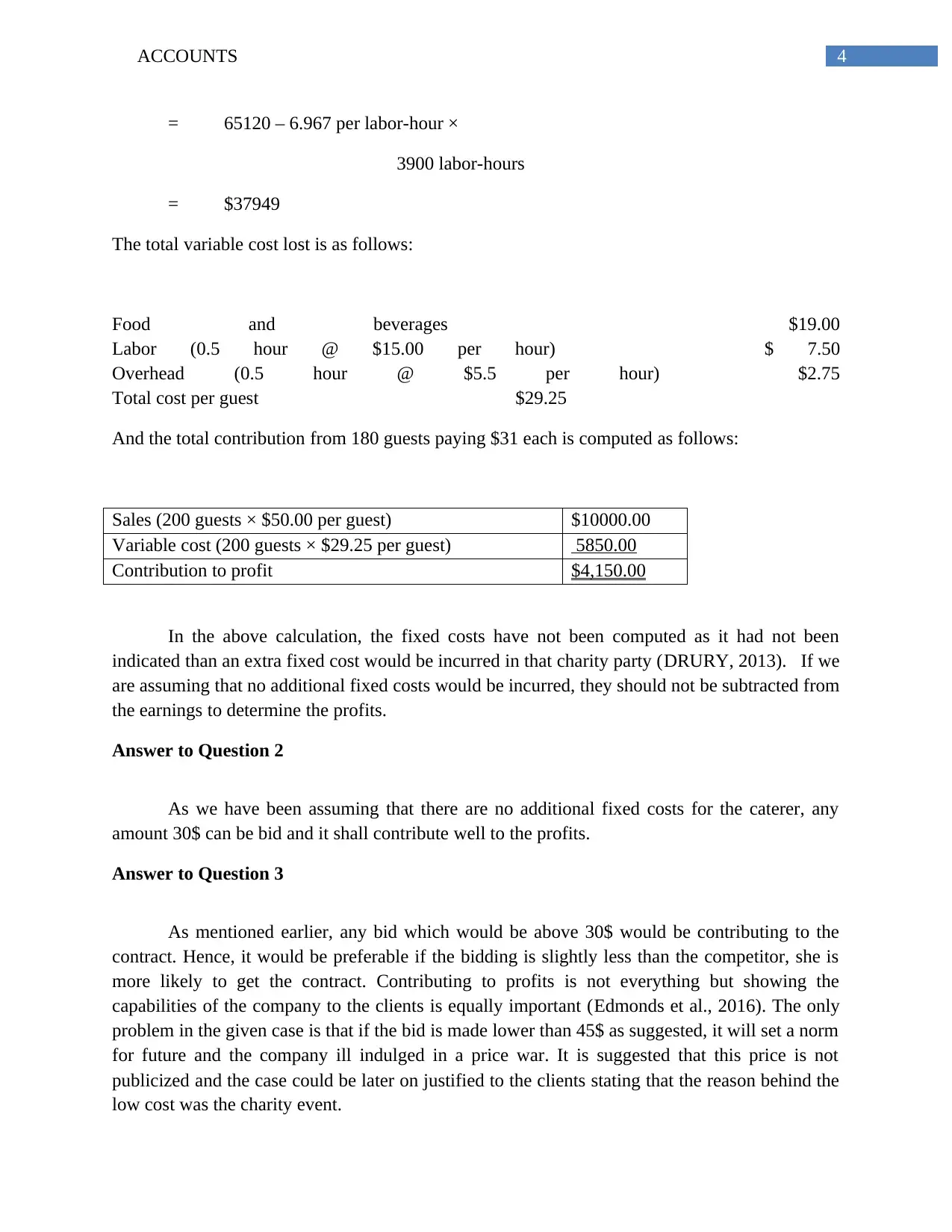

= 65120 – 6.967 per labor-hour ×

3900 labor-hours

= $37949

The total variable cost lost is as follows:

Food and beverages $19.00

Labor (0.5 hour @ $15.00 per hour) $ 7.50

Overhead (0.5 hour @ $5.5 per hour) $2.75

Total cost per guest $29.25

And the total contribution from 180 guests paying $31 each is computed as follows:

Sales (200 guests × $50.00 per guest) $10000.00

Variable cost (200 guests × $29.25 per guest) 5850.00

Contribution to profit $4,150.00

In the above calculation, the fixed costs have not been computed as it had not been

indicated than an extra fixed cost would be incurred in that charity party (DRURY, 2013). If we

are assuming that no additional fixed costs would be incurred, they should not be subtracted from

the earnings to determine the profits.

Answer to Question 2

As we have been assuming that there are no additional fixed costs for the caterer, any

amount 30$ can be bid and it shall contribute well to the profits.

Answer to Question 3

As mentioned earlier, any bid which would be above 30$ would be contributing to the

contract. Hence, it would be preferable if the bidding is slightly less than the competitor, she is

more likely to get the contract. Contributing to profits is not everything but showing the

capabilities of the company to the clients is equally important (Edmonds et al., 2016). The only

problem in the given case is that if the bid is made lower than 45$ as suggested, it will set a norm

for future and the company ill indulged in a price war. It is suggested that this price is not

publicized and the case could be later on justified to the clients stating that the reason behind the

low cost was the charity event.

= 65120 – 6.967 per labor-hour ×

3900 labor-hours

= $37949

The total variable cost lost is as follows:

Food and beverages $19.00

Labor (0.5 hour @ $15.00 per hour) $ 7.50

Overhead (0.5 hour @ $5.5 per hour) $2.75

Total cost per guest $29.25

And the total contribution from 180 guests paying $31 each is computed as follows:

Sales (200 guests × $50.00 per guest) $10000.00

Variable cost (200 guests × $29.25 per guest) 5850.00

Contribution to profit $4,150.00

In the above calculation, the fixed costs have not been computed as it had not been

indicated than an extra fixed cost would be incurred in that charity party (DRURY, 2013). If we

are assuming that no additional fixed costs would be incurred, they should not be subtracted from

the earnings to determine the profits.

Answer to Question 2

As we have been assuming that there are no additional fixed costs for the caterer, any

amount 30$ can be bid and it shall contribute well to the profits.

Answer to Question 3

As mentioned earlier, any bid which would be above 30$ would be contributing to the

contract. Hence, it would be preferable if the bidding is slightly less than the competitor, she is

more likely to get the contract. Contributing to profits is not everything but showing the

capabilities of the company to the clients is equally important (Edmonds et al., 2016). The only

problem in the given case is that if the bid is made lower than 45$ as suggested, it will set a norm

for future and the company ill indulged in a price war. It is suggested that this price is not

publicized and the case could be later on justified to the clients stating that the reason behind the

low cost was the charity event.

5ACCOUNTS

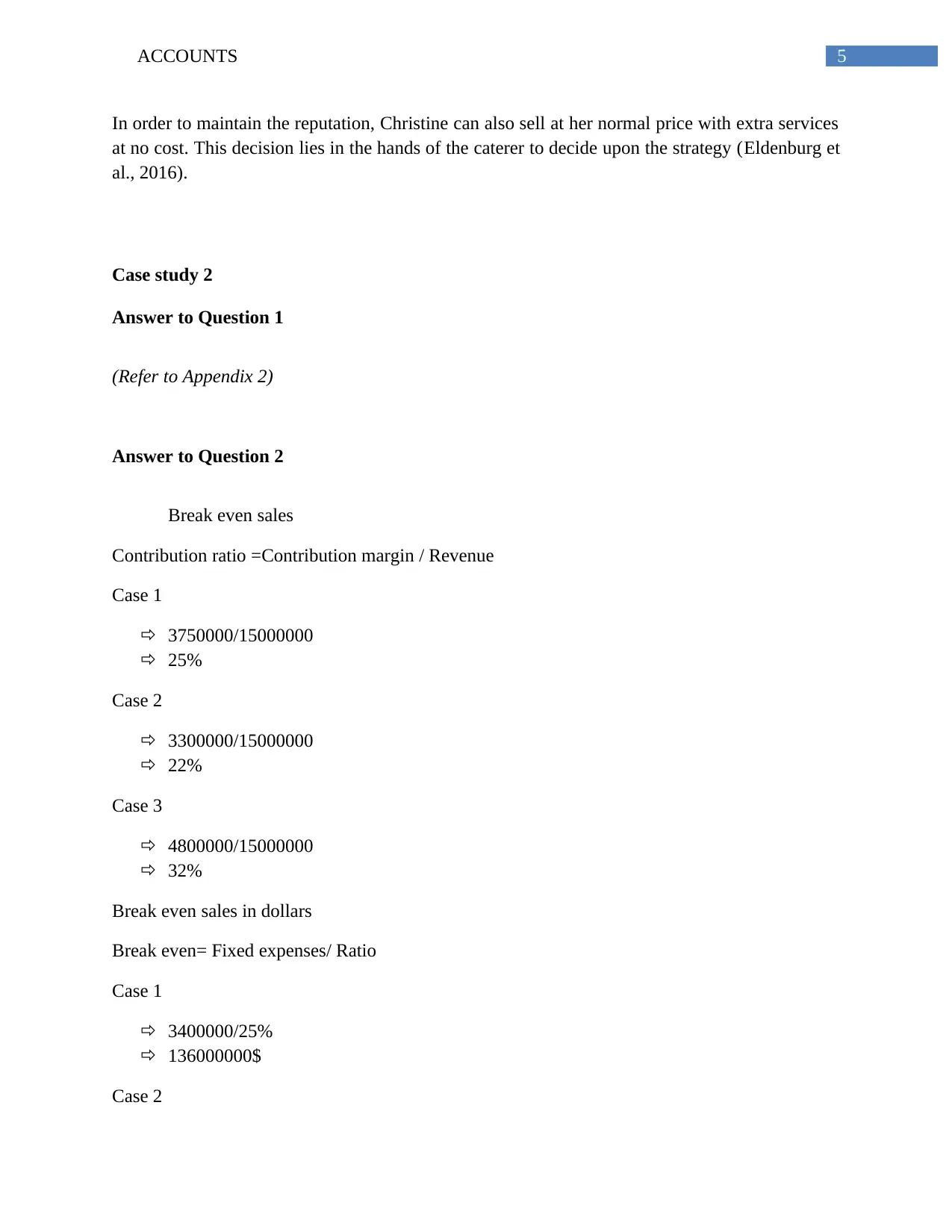

In order to maintain the reputation, Christine can also sell at her normal price with extra services

at no cost. This decision lies in the hands of the caterer to decide upon the strategy (Eldenburg et

al., 2016).

Case study 2

Answer to Question 1

(Refer to Appendix 2)

Answer to Question 2

Break even sales

Contribution ratio =Contribution margin / Revenue

Case 1

3750000/15000000

25%

Case 2

3300000/15000000

22%

Case 3

4800000/15000000

32%

Break even sales in dollars

Break even= Fixed expenses/ Ratio

Case 1

3400000/25%

136000000$

Case 2

In order to maintain the reputation, Christine can also sell at her normal price with extra services

at no cost. This decision lies in the hands of the caterer to decide upon the strategy (Eldenburg et

al., 2016).

Case study 2

Answer to Question 1

(Refer to Appendix 2)

Answer to Question 2

Break even sales

Contribution ratio =Contribution margin / Revenue

Case 1

3750000/15000000

25%

Case 2

3300000/15000000

22%

Case 3

4800000/15000000

32%

Break even sales in dollars

Break even= Fixed expenses/ Ratio

Case 1

3400000/25%

136000000$

Case 2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTS

3400000/22%

15454545$

Case 3

4300000/32%

13437500$

Answer to Question 3

Dollar sales to attain profit= target profit+ Fixed expenses/ the CM ratio

= -100000+3400000/0.22

= 15909091$

Answer to Question 4

Case 2

The net operating income at outside commission

= 0.22*3400000

=$748000

Case 3

The net operating income at own force

=0.22*4300000

=946000

Therefore equating,

=946000=748000

=126470500$

Answer to Question 5

Refer to Appendix 3

3400000/22%

15454545$

Case 3

4300000/32%

13437500$

Answer to Question 3

Dollar sales to attain profit= target profit+ Fixed expenses/ the CM ratio

= -100000+3400000/0.22

= 15909091$

Answer to Question 4

Case 2

The net operating income at outside commission

= 0.22*3400000

=$748000

Case 3

The net operating income at own force

=0.22*4300000

=946000

Therefore equating,

=946000=748000

=126470500$

Answer to Question 5

Refer to Appendix 3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTS

Answer to Question 6

Letter Memo

To the President,

XYZ Company,

XYZ City

Dear Sir,

Subject: SALES FORCE OR EXTERNAL AGENTS

This is with regard to the situation which related to the hiring of an internal sales force versus

hiring external agent’s matter which is bringing about a huge cost difference for the organization.

After analyzing the situation, it can be recommended that the company should employee its own

sales force instead of hiring one on commission (Weygandt, Kimmel & Kieso, 2015). . This has

been stated because, although the fixed cost component of the company will be increasing once a

permanent sales force is hired, but there will not be any variable costs that will derive from the

particular commission aspect. When the company is hiring a separate sales force for its selling it

is earning a profit of $500000. On the other hand, if it continuous to pay a commission of 22% to

the agents, the company will incur a loss of $100000. This is not acceptable and therefore, it is

suggested that the company keeps its own sales force.

Yours gratefully,

XYZ.

Answer to Question 6

Letter Memo

To the President,

XYZ Company,

XYZ City

Dear Sir,

Subject: SALES FORCE OR EXTERNAL AGENTS

This is with regard to the situation which related to the hiring of an internal sales force versus

hiring external agent’s matter which is bringing about a huge cost difference for the organization.

After analyzing the situation, it can be recommended that the company should employee its own

sales force instead of hiring one on commission (Weygandt, Kimmel & Kieso, 2015). . This has

been stated because, although the fixed cost component of the company will be increasing once a

permanent sales force is hired, but there will not be any variable costs that will derive from the

particular commission aspect. When the company is hiring a separate sales force for its selling it

is earning a profit of $500000. On the other hand, if it continuous to pay a commission of 22% to

the agents, the company will incur a loss of $100000. This is not acceptable and therefore, it is

suggested that the company keeps its own sales force.

Yours gratefully,

XYZ.

8ACCOUNTS

Case study 3

Answer to Question 1

Refer to Appendix 4

Therefore, the predetermined overhead rate=

Estimated total manufacturing overhead/ estimated total amount of allocation base

=$3800000/57000 DLHs

=$66.67 per DLH

Answer to Question 2

The predetermined overhead rate which was revised is more than the original rate, the

reason being that the automated milling machine will be increasing the overhead for the year and

this shall be decreasing the direct labor hours. Due to this double whammy effect, the

predetermined overhead rate increases.

The milling machine acquisition which is automated will be increasing the costs of all the

jobs and not just the ones which will be affected by the new machine (Warren, Reeve, & Duchac,

2015). The reason behind this is that the organization makes use of a plant overhead rate, had it

been using a different rate, this would not have been the case.

Answer to Question 3

The predetermined overhead rate is much higher than it was earlier. This will have a

penalizing effect on the products which will be using the similar kind of direct labor hours.

These products will presently deem to be less profitable and the present managers will be appear

to be performing not so well (Gitman, Juchau & Flanagan, 2015). There may exist pressure to

increase the given prices of the products although there has not been any increase in the real

costs of the product.

Answer to Question 4

The calculation of the costs savings was in an error. Although it may be a good idea to

buy a new equipment because of better capabilities. The earlier calculations assumed that the

overhead would go down because of the reduced labor hours. However, actually the overheads

Case study 3

Answer to Question 1

Refer to Appendix 4

Therefore, the predetermined overhead rate=

Estimated total manufacturing overhead/ estimated total amount of allocation base

=$3800000/57000 DLHs

=$66.67 per DLH

Answer to Question 2

The predetermined overhead rate which was revised is more than the original rate, the

reason being that the automated milling machine will be increasing the overhead for the year and

this shall be decreasing the direct labor hours. Due to this double whammy effect, the

predetermined overhead rate increases.

The milling machine acquisition which is automated will be increasing the costs of all the

jobs and not just the ones which will be affected by the new machine (Warren, Reeve, & Duchac,

2015). The reason behind this is that the organization makes use of a plant overhead rate, had it

been using a different rate, this would not have been the case.

Answer to Question 3

The predetermined overhead rate is much higher than it was earlier. This will have a

penalizing effect on the products which will be using the similar kind of direct labor hours.

These products will presently deem to be less profitable and the present managers will be appear

to be performing not so well (Gitman, Juchau & Flanagan, 2015). There may exist pressure to

increase the given prices of the products although there has not been any increase in the real

costs of the product.

Answer to Question 4

The calculation of the costs savings was in an error. Although it may be a good idea to

buy a new equipment because of better capabilities. The earlier calculations assumed that the

overhead would go down because of the reduced labor hours. However, actually the overheads

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTS

increased because the machine was new equipment (Schaltegger & Burritt, 2017). A cost

analysis which would be differential in nature would reveal that the machine has increased the

cost by around 316000$ in a year in a case where the labor reduction is only by 2000 hours.

Consequences of cost of leasing the automated equipment

Increase in the overhead of manufacturing

Leasing cost of new machine $348000

Cost of the new programmer 50000

398000

Less: Labor cost savings(2000*41 per hour) 82000

Net increase in annual costs 316000$

It can be seen that even though there has been a reduction in the labor hours, which

would have added only $164000(4000*41) in the savings of the cost. The net increase in the

costs annually would have been just $152000 and the machine would have remained as

unattractive option (Hilton & Platt, 2013). This is by no measure automatic as the 6000 hour

reduction may be achieved in case the workers retire or quit.

First of all, pre determined overhead rates should not be assumed to be similar as the

variable costs, and a reduction in labor requirements does not always lead to a reduction in the

hours paid.

increased because the machine was new equipment (Schaltegger & Burritt, 2017). A cost

analysis which would be differential in nature would reveal that the machine has increased the

cost by around 316000$ in a year in a case where the labor reduction is only by 2000 hours.

Consequences of cost of leasing the automated equipment

Increase in the overhead of manufacturing

Leasing cost of new machine $348000

Cost of the new programmer 50000

398000

Less: Labor cost savings(2000*41 per hour) 82000

Net increase in annual costs 316000$

It can be seen that even though there has been a reduction in the labor hours, which

would have added only $164000(4000*41) in the savings of the cost. The net increase in the

costs annually would have been just $152000 and the machine would have remained as

unattractive option (Hilton & Platt, 2013). This is by no measure automatic as the 6000 hour

reduction may be achieved in case the workers retire or quit.

First of all, pre determined overhead rates should not be assumed to be similar as the

variable costs, and a reduction in labor requirements does not always lead to a reduction in the

hours paid.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTS

References

Crosson, S. V., & Needles, B. E. (2013). Managerial accounting. Cengage Learning.

Demski, J. (2013). Managerial uses of accounting information. Springer Science & Business

Media.

DRURY, C. M. (2013). Management and cost accounting. Springer.

Edmonds, T. P., Edmonds, C. D., Tsay, B. Y., & Olds, P. R. (2016). Fundamental managerial

accounting concepts. McGraw-Hill Education.

Eldenburg, L. G., Wolcott, S. K., Chen, L. H., & Cook, G. (2016). Cost management:

Measuring, monitoring, and motivating performance. Wiley Global Education.

Gitman, L. J., Juchau, R., & Flanagan, J. (2015). Principles of managerial finance. Pearson

Higher Education AU.

Hilton, R. W., & Platt, D. E. (2013). Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Schaltegger, S., & Burritt, R. (2017). Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Warren, C. S., Reeve, J. M., & Duchac, J. (2015). Managerial accounting. Nelson Education.

Weygandt, J. J., Kimmel, P. D., & Kieso, D. E. (2015). Financial & managerial accounting.

John Wiley & Sons.

References

Crosson, S. V., & Needles, B. E. (2013). Managerial accounting. Cengage Learning.

Demski, J. (2013). Managerial uses of accounting information. Springer Science & Business

Media.

DRURY, C. M. (2013). Management and cost accounting. Springer.

Edmonds, T. P., Edmonds, C. D., Tsay, B. Y., & Olds, P. R. (2016). Fundamental managerial

accounting concepts. McGraw-Hill Education.

Eldenburg, L. G., Wolcott, S. K., Chen, L. H., & Cook, G. (2016). Cost management:

Measuring, monitoring, and motivating performance. Wiley Global Education.

Gitman, L. J., Juchau, R., & Flanagan, J. (2015). Principles of managerial finance. Pearson

Higher Education AU.

Hilton, R. W., & Platt, D. E. (2013). Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Schaltegger, S., & Burritt, R. (2017). Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Warren, C. S., Reeve, J. M., & Duchac, J. (2015). Managerial accounting. Nelson Education.

Weygandt, J. J., Kimmel, P. D., & Kieso, D. E. (2015). Financial & managerial accounting.

John Wiley & Sons.

11ACCOUNTS

Appendices

Appendix 1

Case study 1

The scatter diagram

1000 1500 2000 2500 3000 3500 4000 4500 5000

0

10000

20000

30000

40000

50000

60000

70000

80000

Series2

Appendix 2

Case 1

+

Sales $15,000,000

- Variable production expenses

(such as materials, supplies,

and variable overhead)

$8,400,000

- Variable selling and 2,850,000

Appendices

Appendix 1

Case study 1

The scatter diagram

1000 1500 2000 2500 3000 3500 4000 4500 5000

0

10000

20000

30000

40000

50000

60000

70000

80000

Series2

Appendix 2

Case 1

+

Sales $15,000,000

- Variable production expenses

(such as materials, supplies,

and variable overhead)

$8,400,000

- Variable selling and 2,850,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.