Management Accounting Analysis: Costing, Profitability and Decisions

VerifiedAdded on 2019/11/25

|8

|1747

|194

Homework Assignment

AI Summary

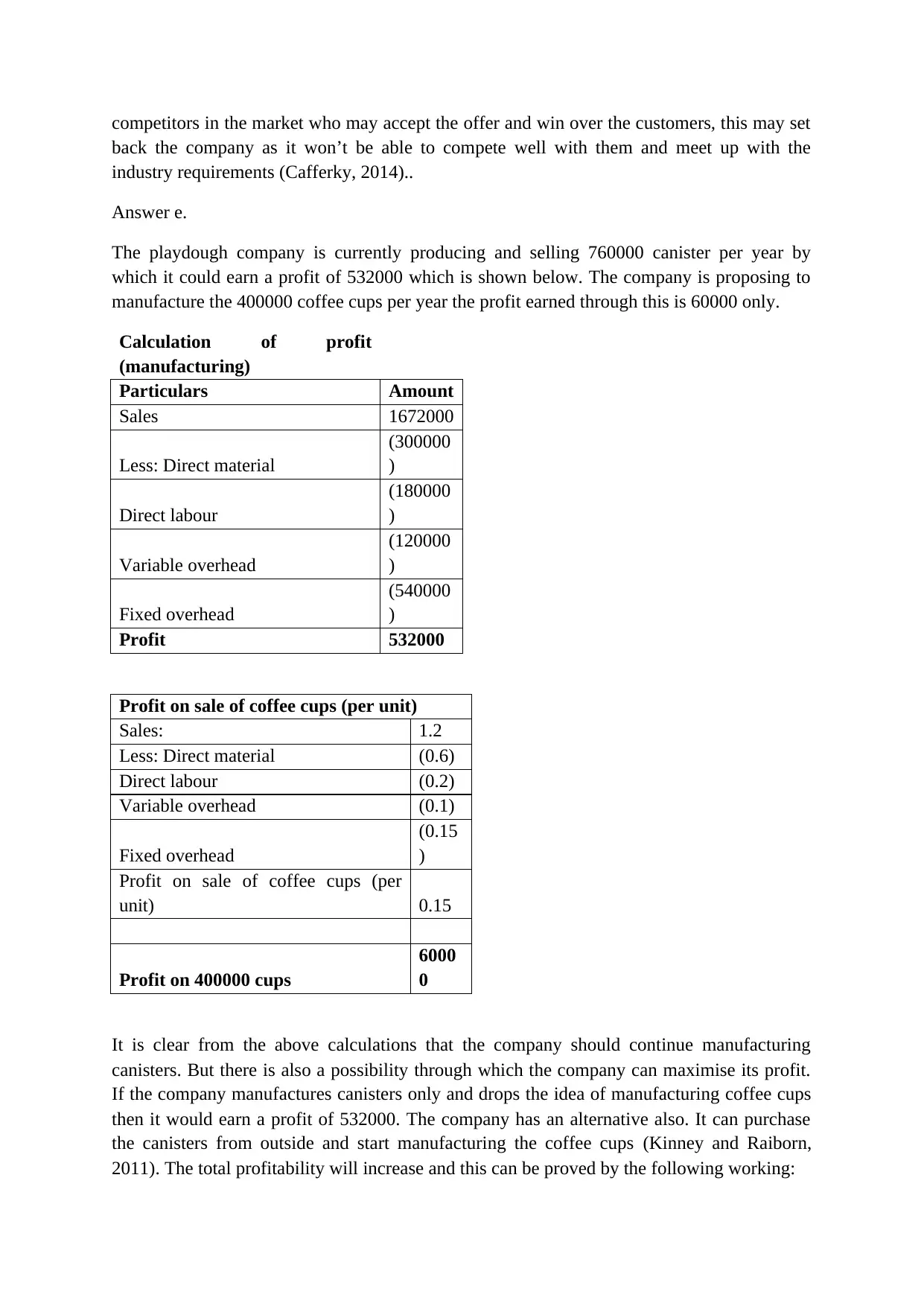

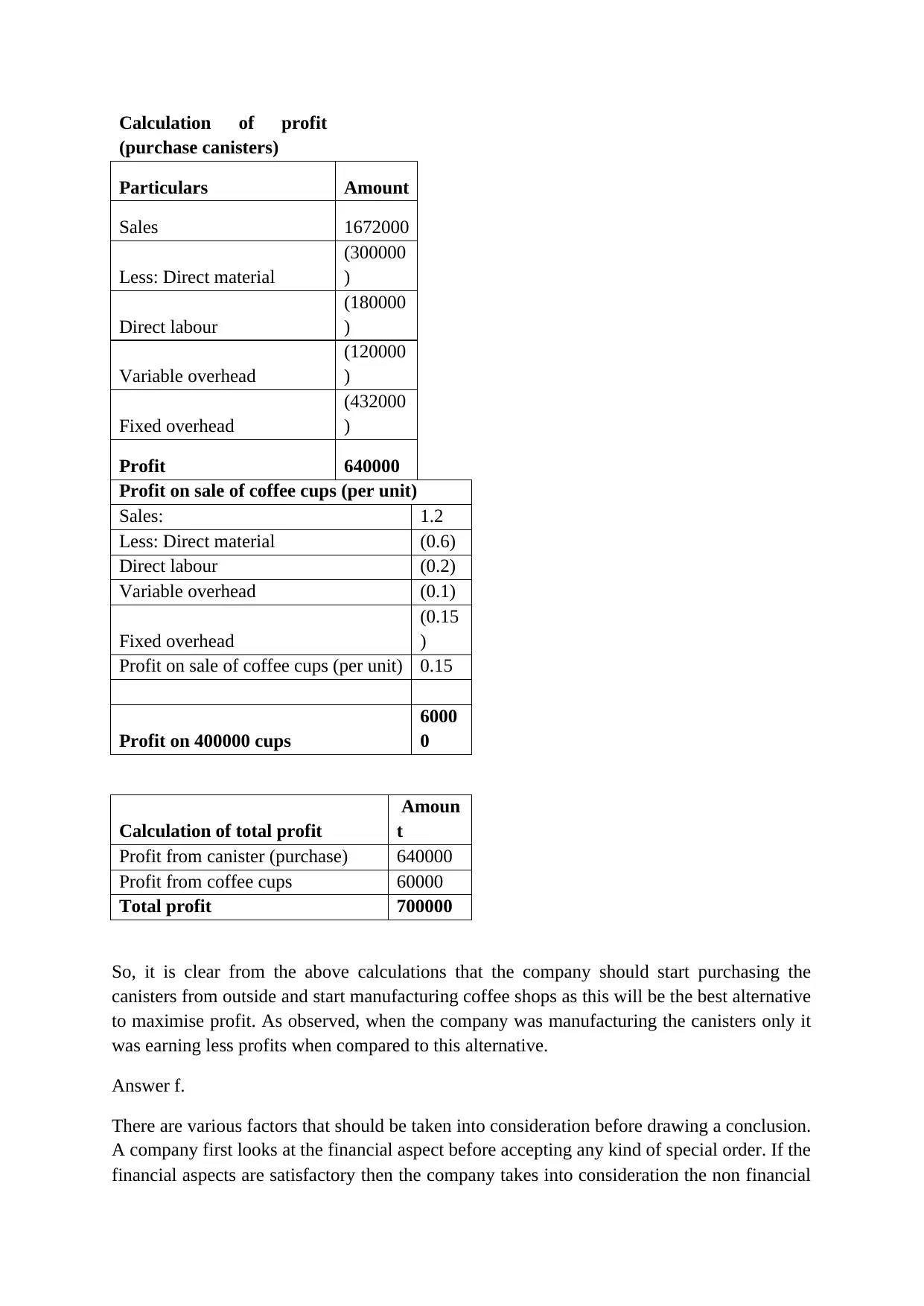

This assignment solution addresses various aspects of management accounting, focusing on cost analysis, profitability, and strategic decision-making. It begins with calculating the cost per unit and then analyzes the profitability of manufacturing versus purchasing. The solution evaluates a special order scenario, comparing contribution margins and profits with and without the order, concluding that the order should be rejected based on financial grounds. The assignment also considers non-financial factors like product quality, delivery time, and reputation. Finally, it compares the profitability of manufacturing canisters versus manufacturing coffee cups, suggesting that the company should purchase canisters and manufacture coffee cups to maximize profits. The solution incorporates relevant financial calculations and references key accounting principles and literature.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.