Accounting Assignment 1: Financial Analysis of Profitability and Cost

VerifiedAdded on 2023/04/23

|7

|1434

|442

Homework Assignment

AI Summary

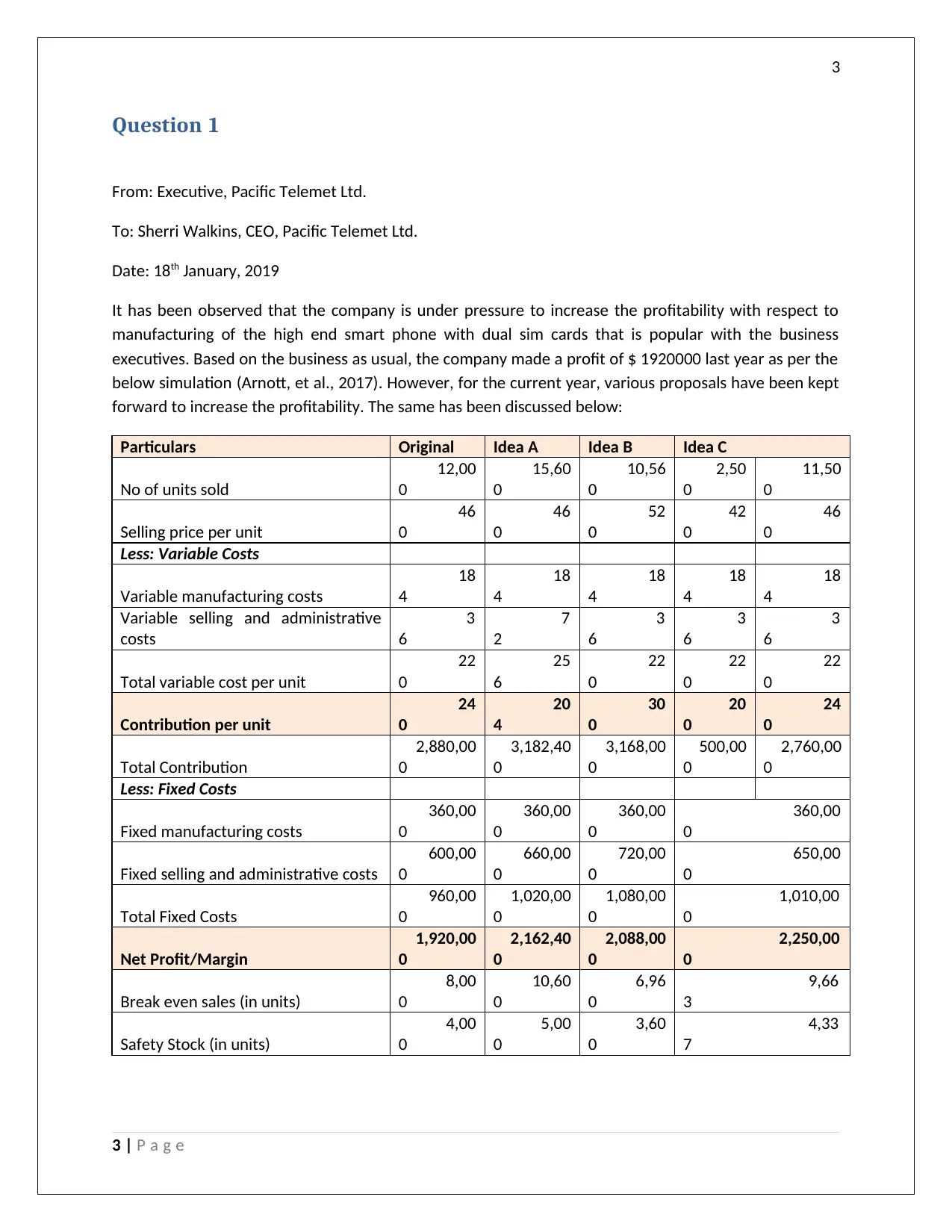

This accounting assignment analyzes the profitability of Pacific Telemet Ltd. and Go-Go-Grow Ltd. by examining different business scenarios and cost structures. The first part of the assignment evaluates various proposals to increase the profitability of a smartphone manufacturing company, considering factors like selling price, variable and fixed costs, and break-even points. The analysis includes the impact of quality improvements, advertising campaigns, and promotional rebates on profit margins and sales. The second part focuses on a special order for Go-Go-Grow Ltd., determining the appropriate bidding price based on factory capacity and opportunity costs, considering direct materials, labor, and overhead costs. The assignment highlights the importance of understanding cost behavior, break-even analysis, and the impact of different strategies on overall profitability and financial decision-making, providing a comprehensive overview of financial analysis and cost management.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.