Accounting 1: Detailed Budgeting, Financial Statements, and Analysis

VerifiedAdded on 2020/05/16

|21

|4412

|132

Homework Assignment

AI Summary

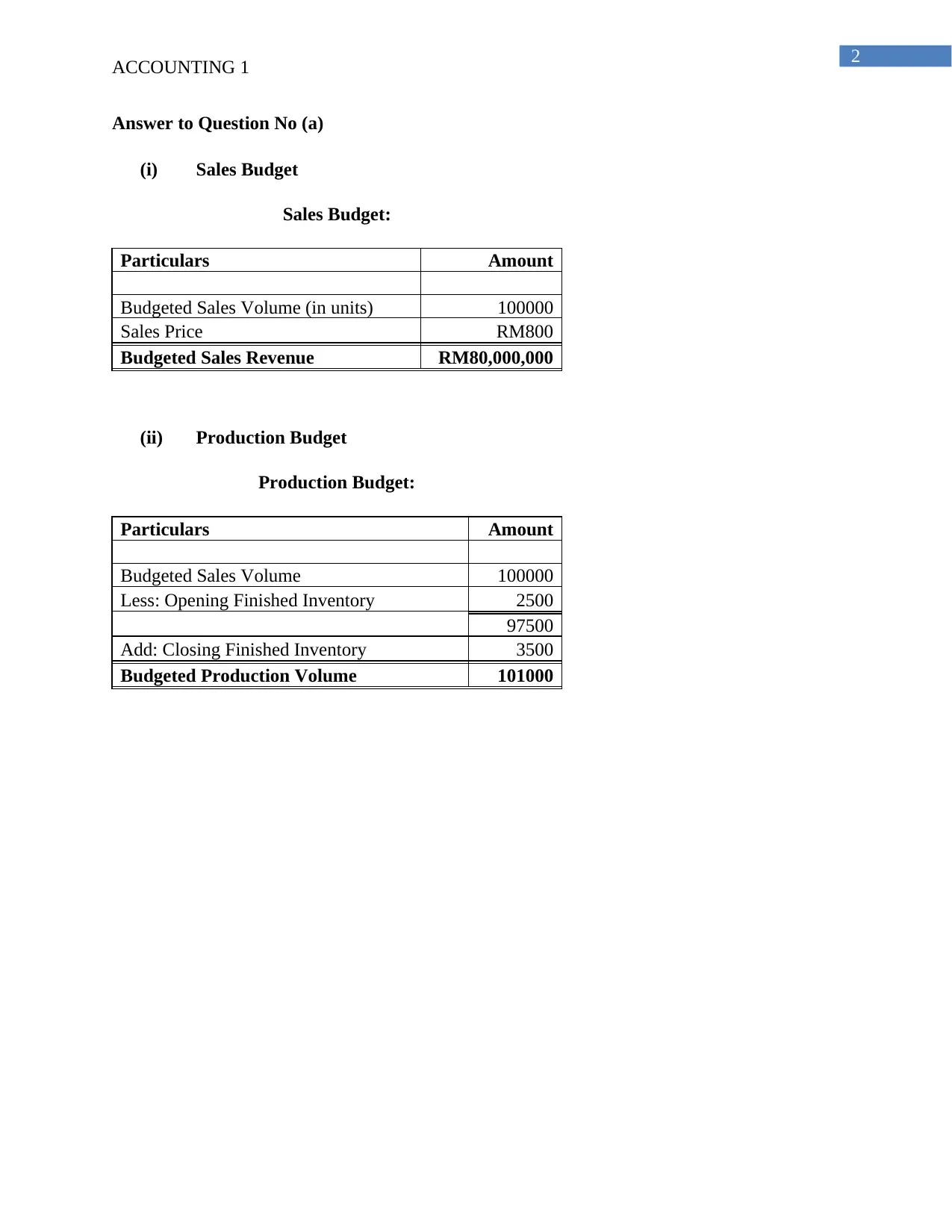

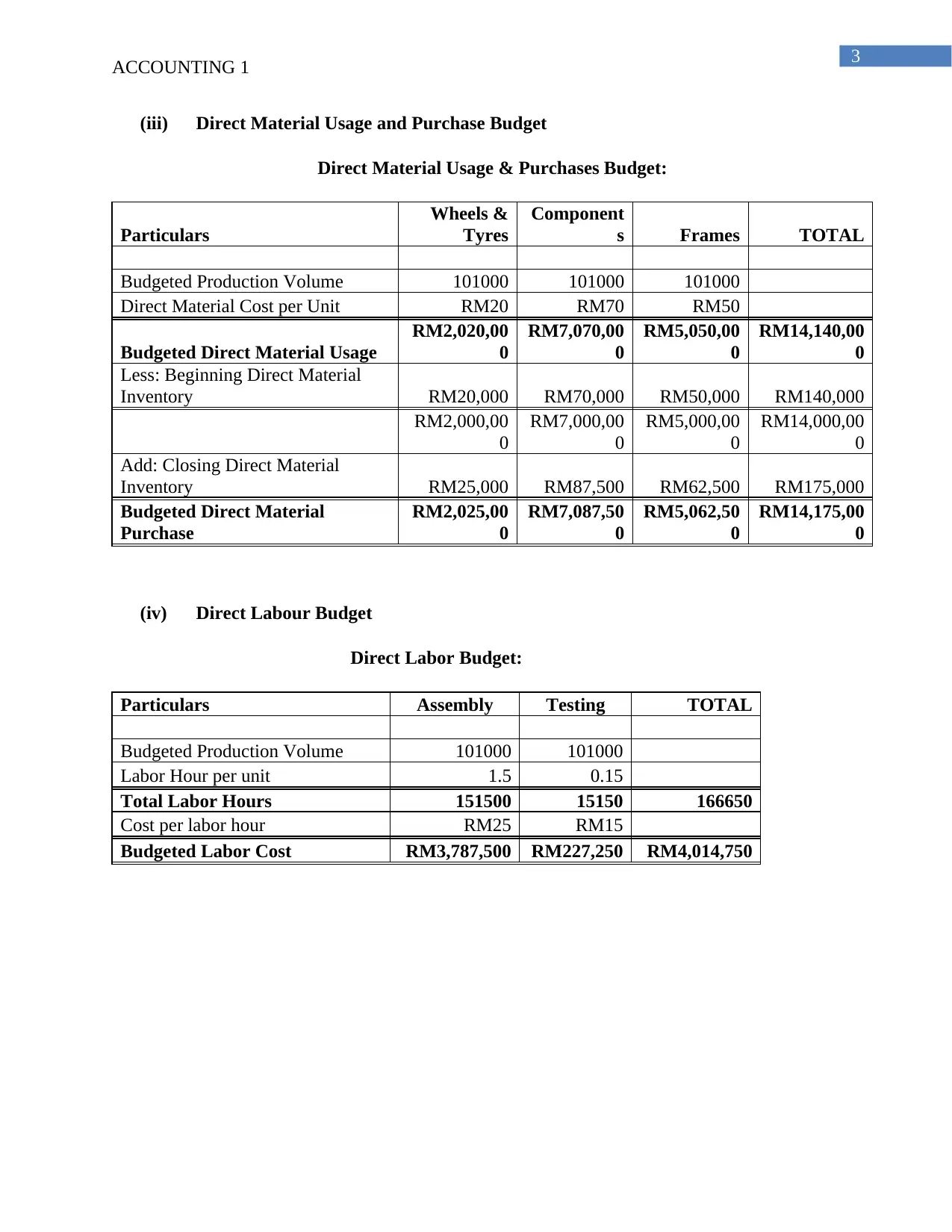

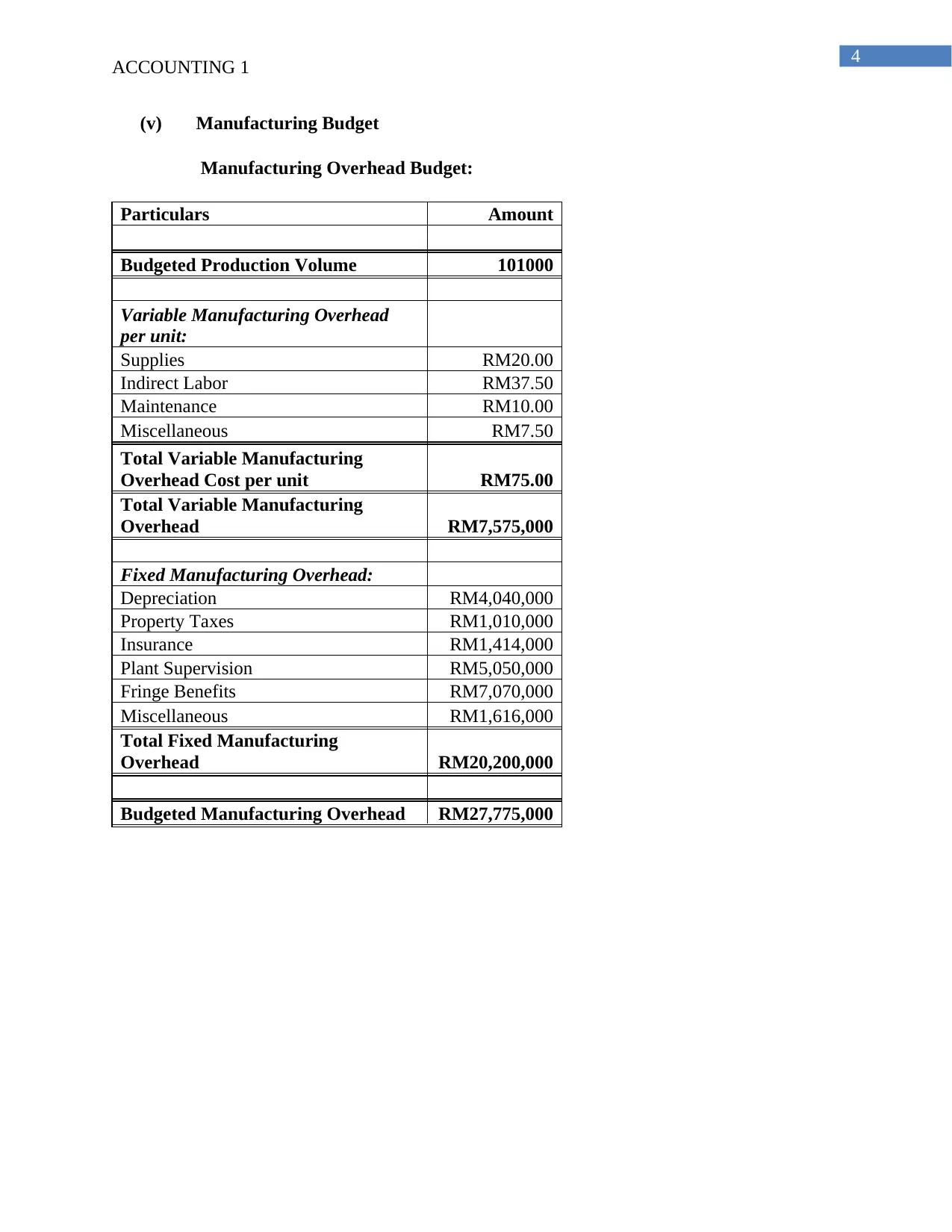

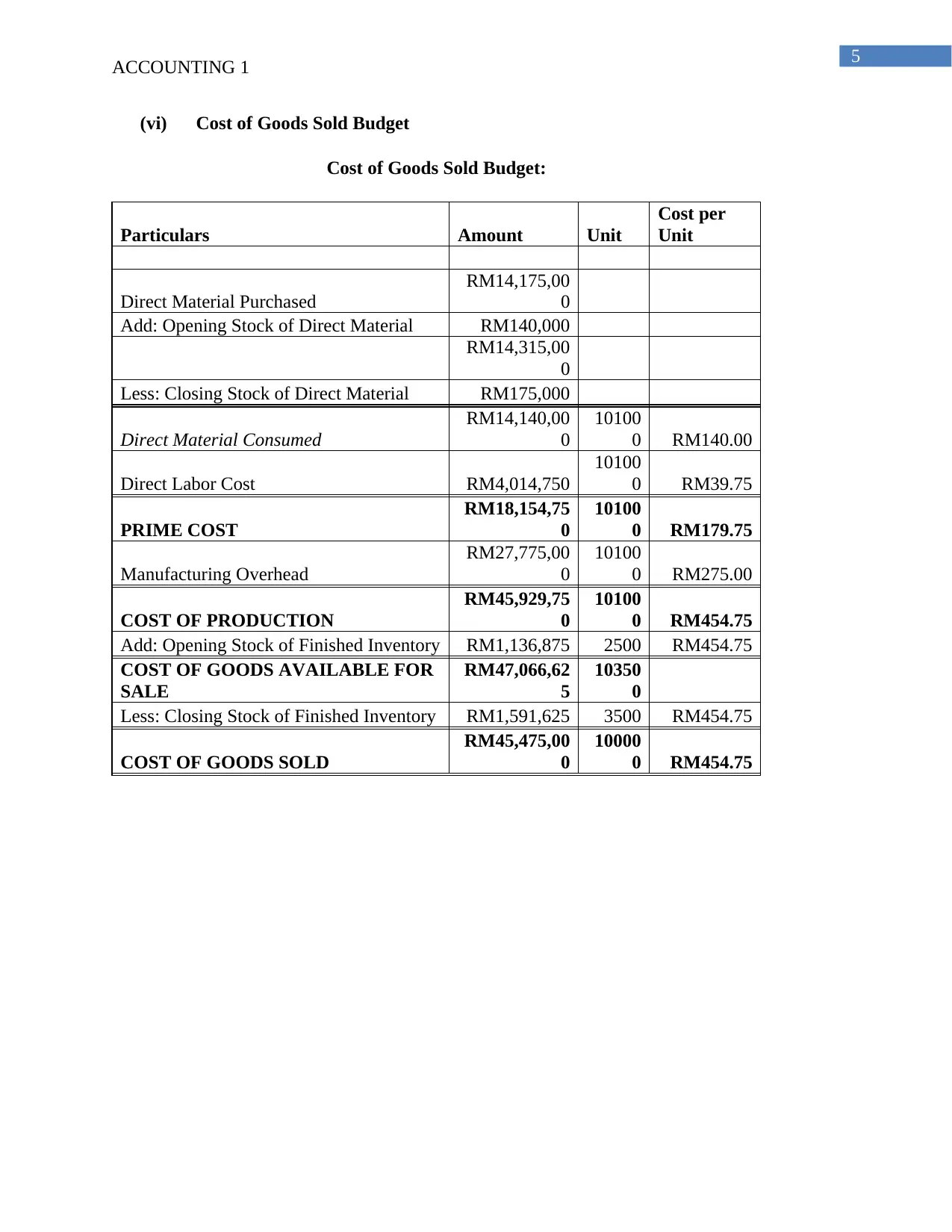

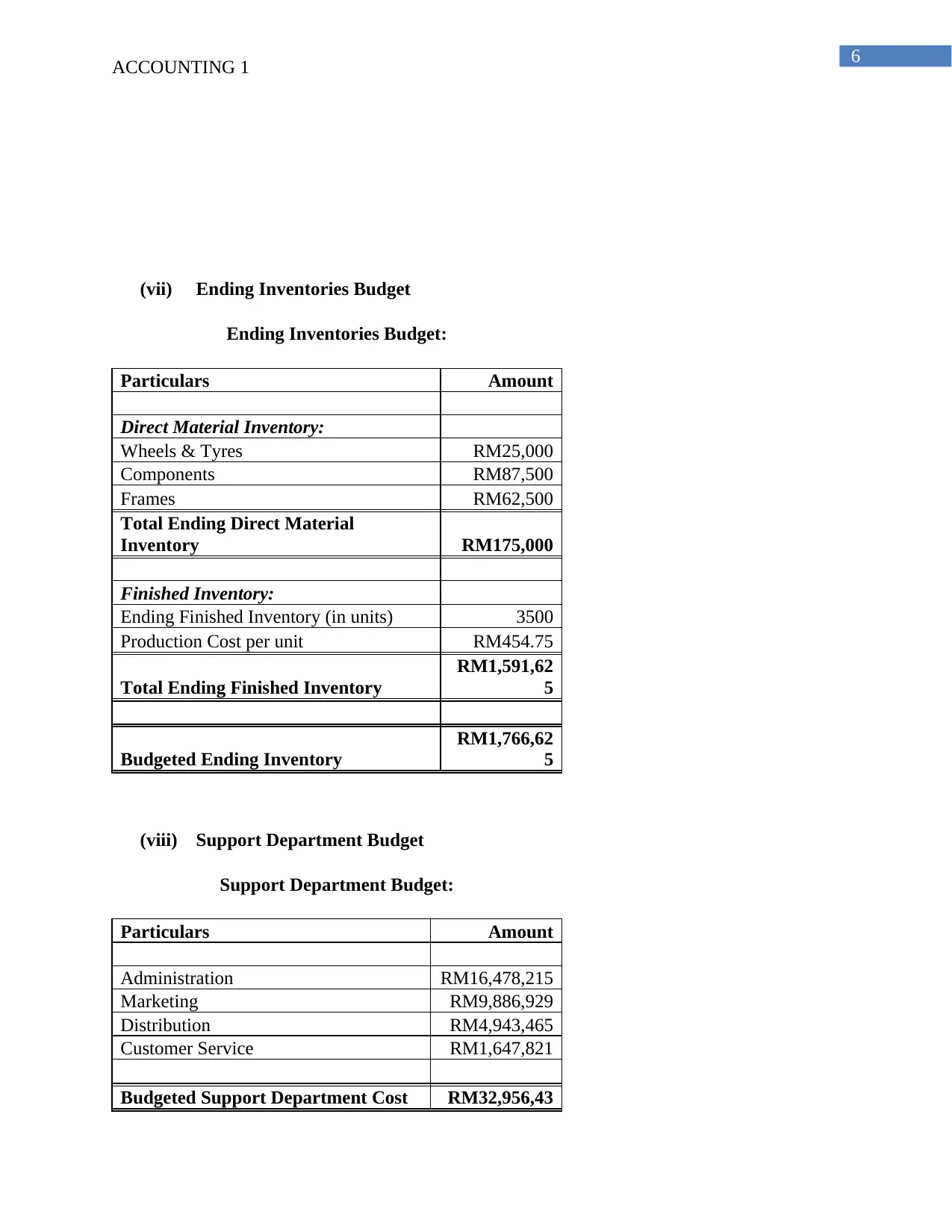

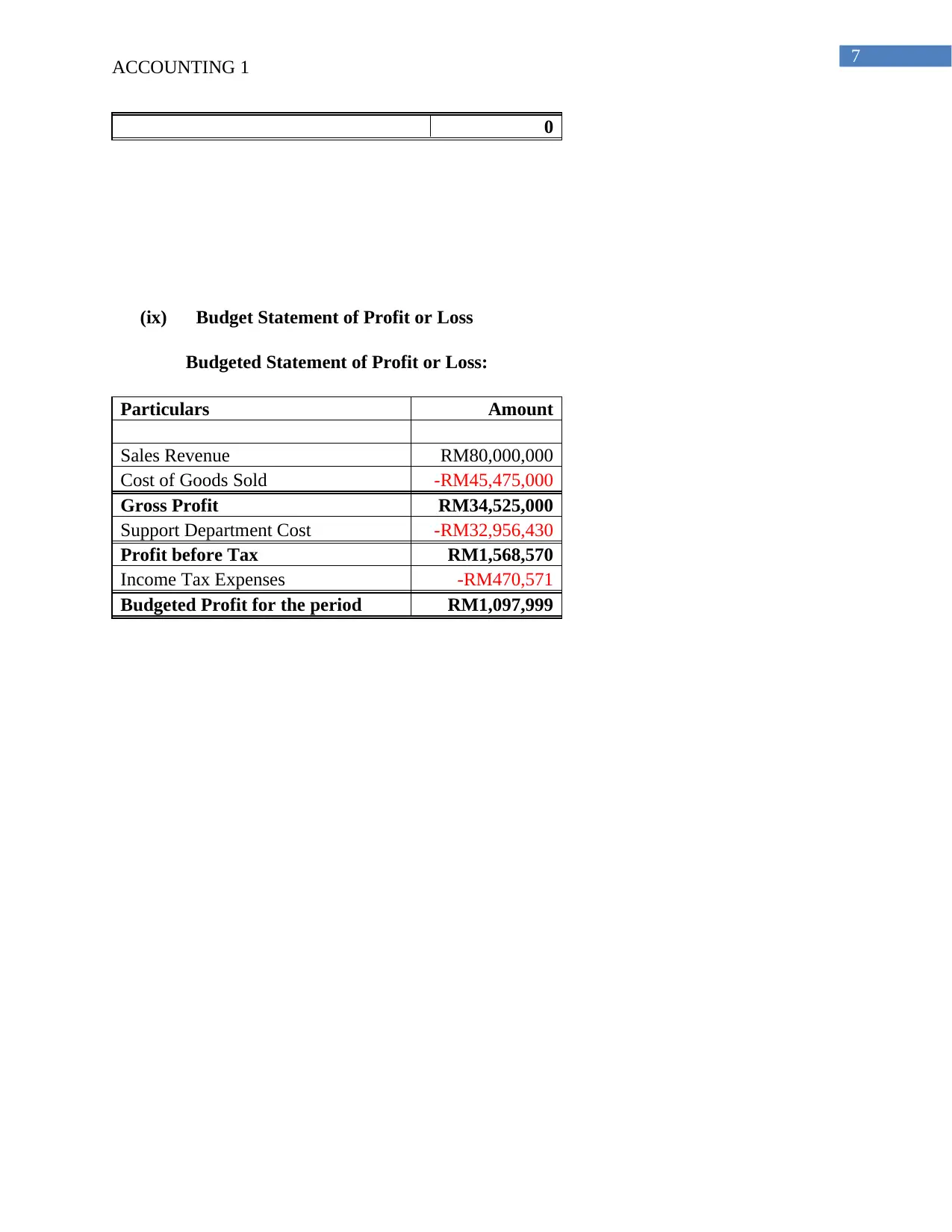

This document presents a comprehensive solution to an Accounting 1 budgeting assignment, encompassing various aspects of financial planning and analysis. The solution includes detailed calculations and explanations for several key budgets, such as the sales budget, production budget, direct material usage and purchase budget, direct labor budget, manufacturing overhead budget, cost of goods sold budget, ending inventories budget, and support department budget. It culminates in a budgeted statement of profit or loss, providing a clear overview of the company's projected financial performance. The assignment also includes a discussion on the importance of a cash budget, outlining its significance in financial management, planning, and control. The discussion emphasizes the cash budget's role in predicting financial needs, enabling corrective actions, assessing company performance, and aiding in effective planning. The document covers the characteristics and significance of cash budgeting, highlighting its importance in ensuring a company's solvency and providing a framework for effective financial decision-making. It discusses the role of budgeting in planning and control, aligning financial goals with operational strategies and emphasizes the importance of a well-structured budgeting process for effective management.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.