Accounting and Financial Management Assignment Analysis Report

VerifiedAdded on 2022/08/26

|7

|704

|14

Homework Assignment

AI Summary

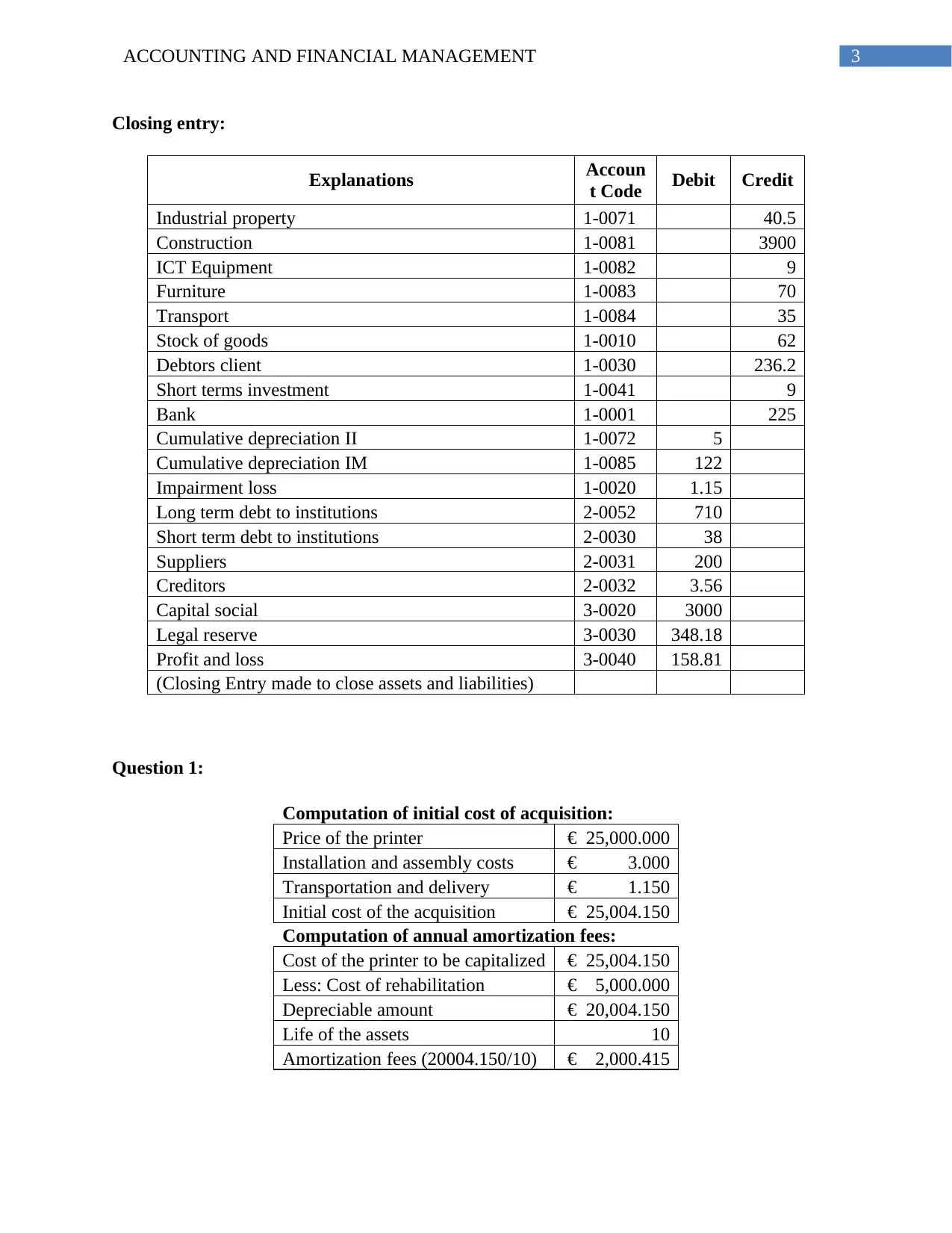

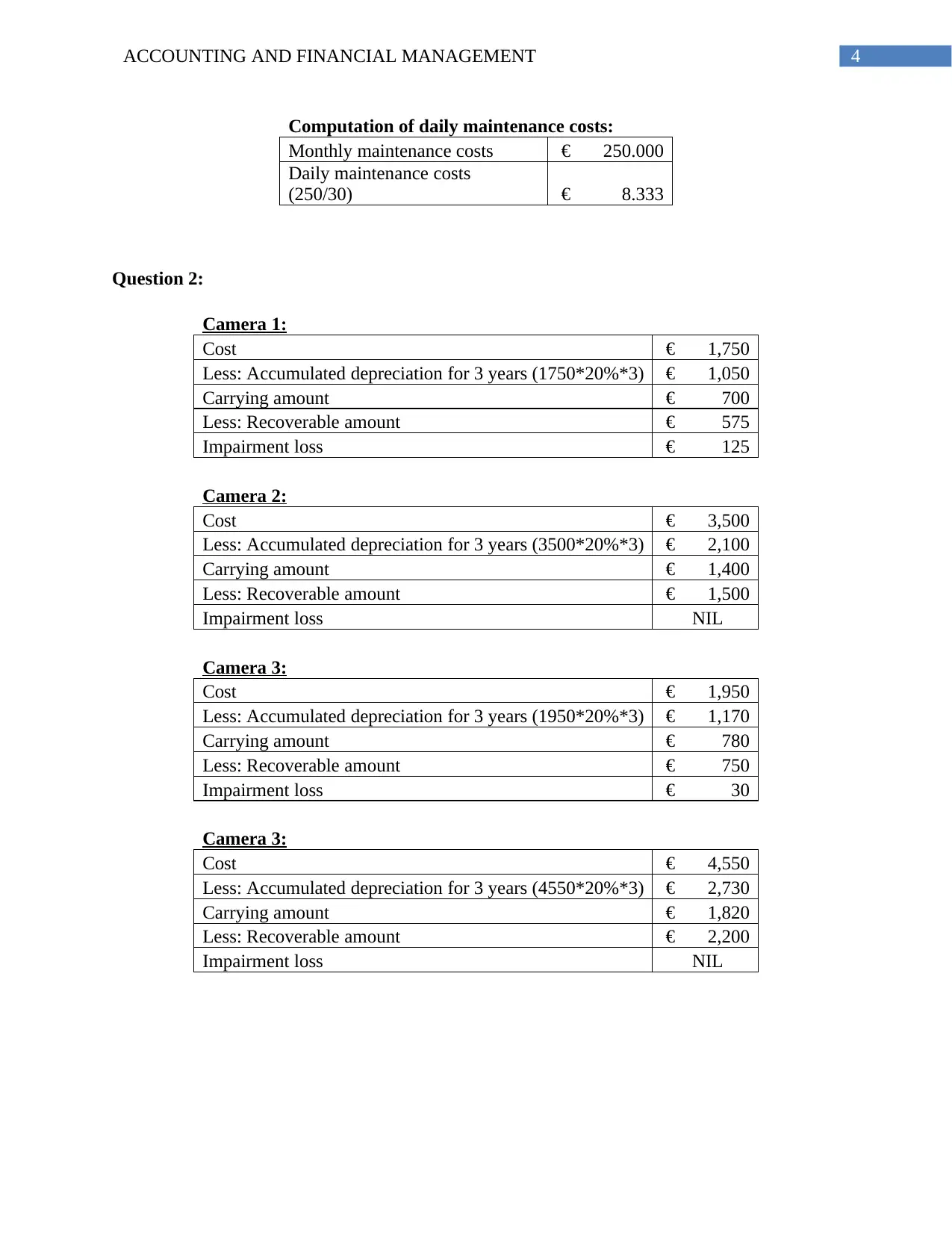

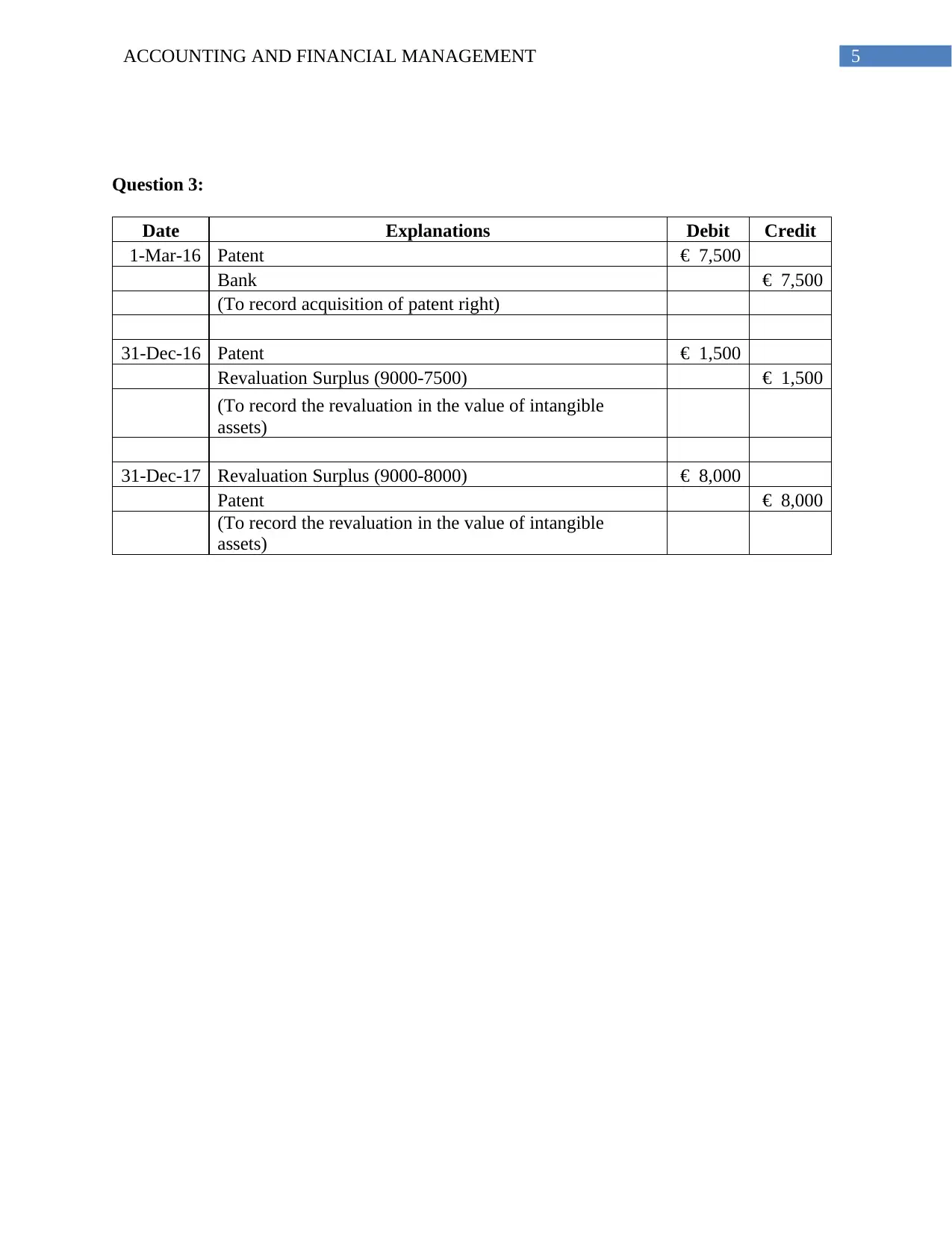

This assignment solution addresses various aspects of accounting and financial management. It begins by presenting a chart of accounts, followed by a detailed closing entry. The solution then tackles three questions: The first question focuses on calculating the initial cost of acquisition and annual amortization fees for a printer. The second question involves calculating impairment losses for multiple cameras, considering their carrying amounts and recoverable amounts. The final question covers the accounting treatment of a patent, including journal entries for its acquisition and revaluation. The assignment incorporates relevant accounting principles and provides clear explanations and calculations. The document also includes a bibliography of related academic sources.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.