Accounting for Managers Report: Financial Performance

VerifiedAdded on 2020/06/06

|19

|4196

|282

Report

AI Summary

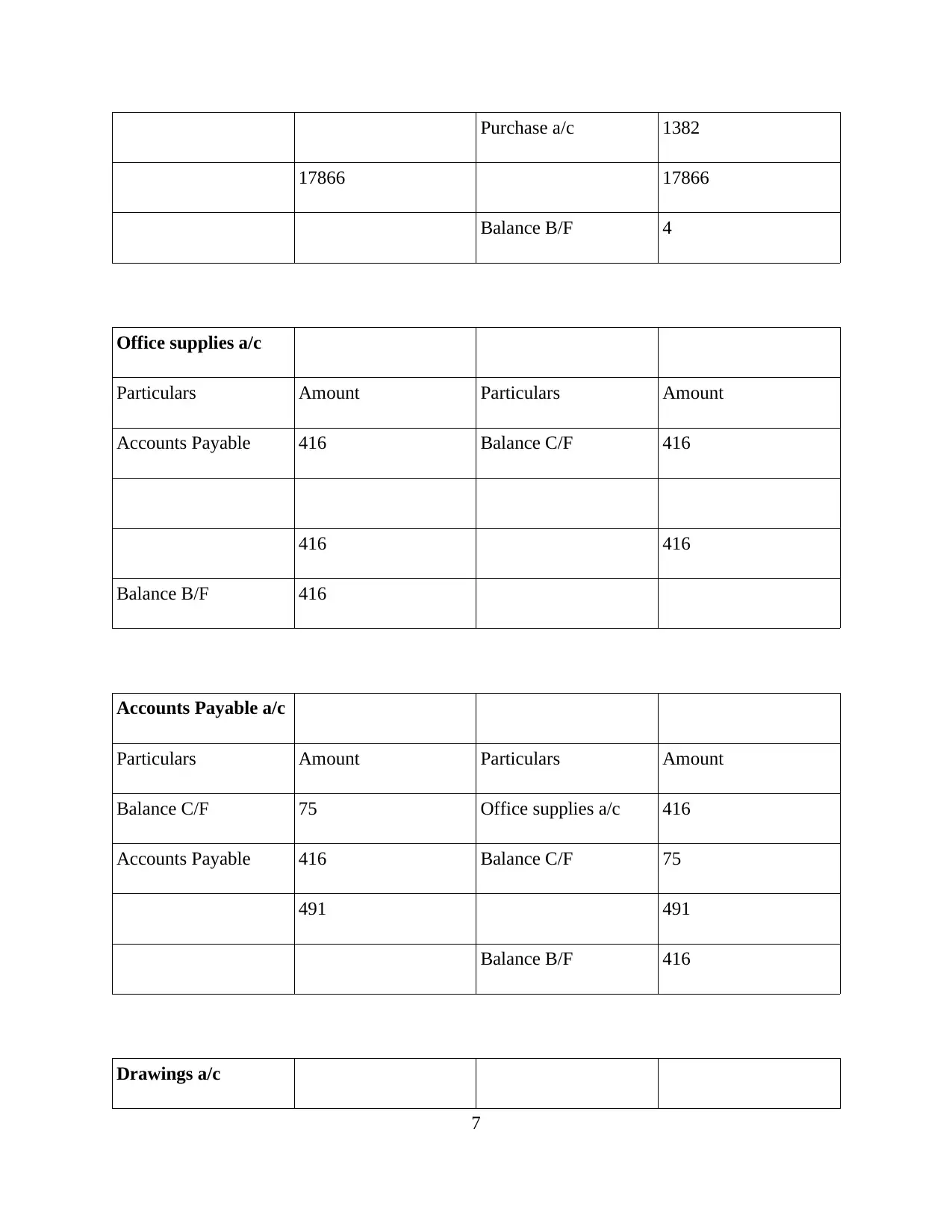

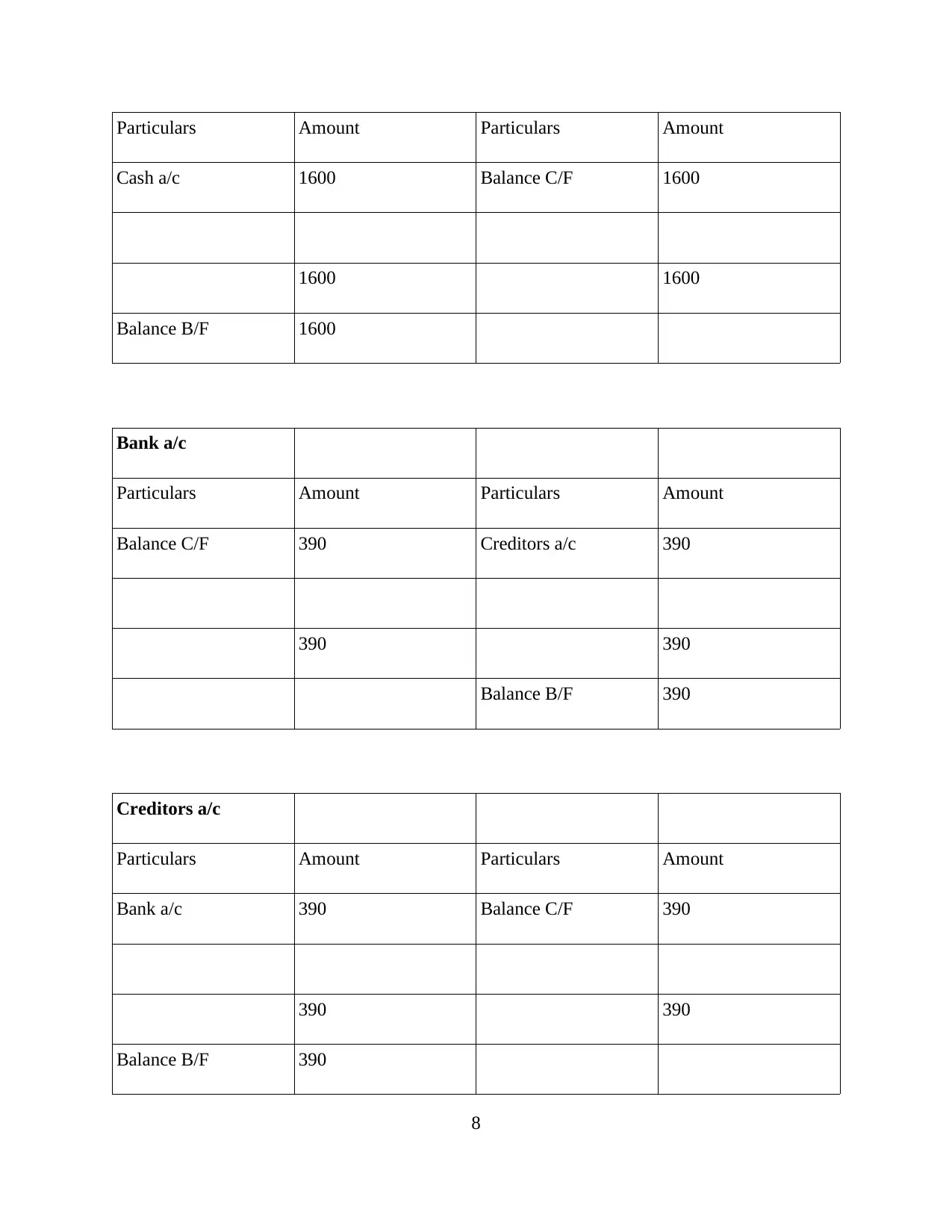

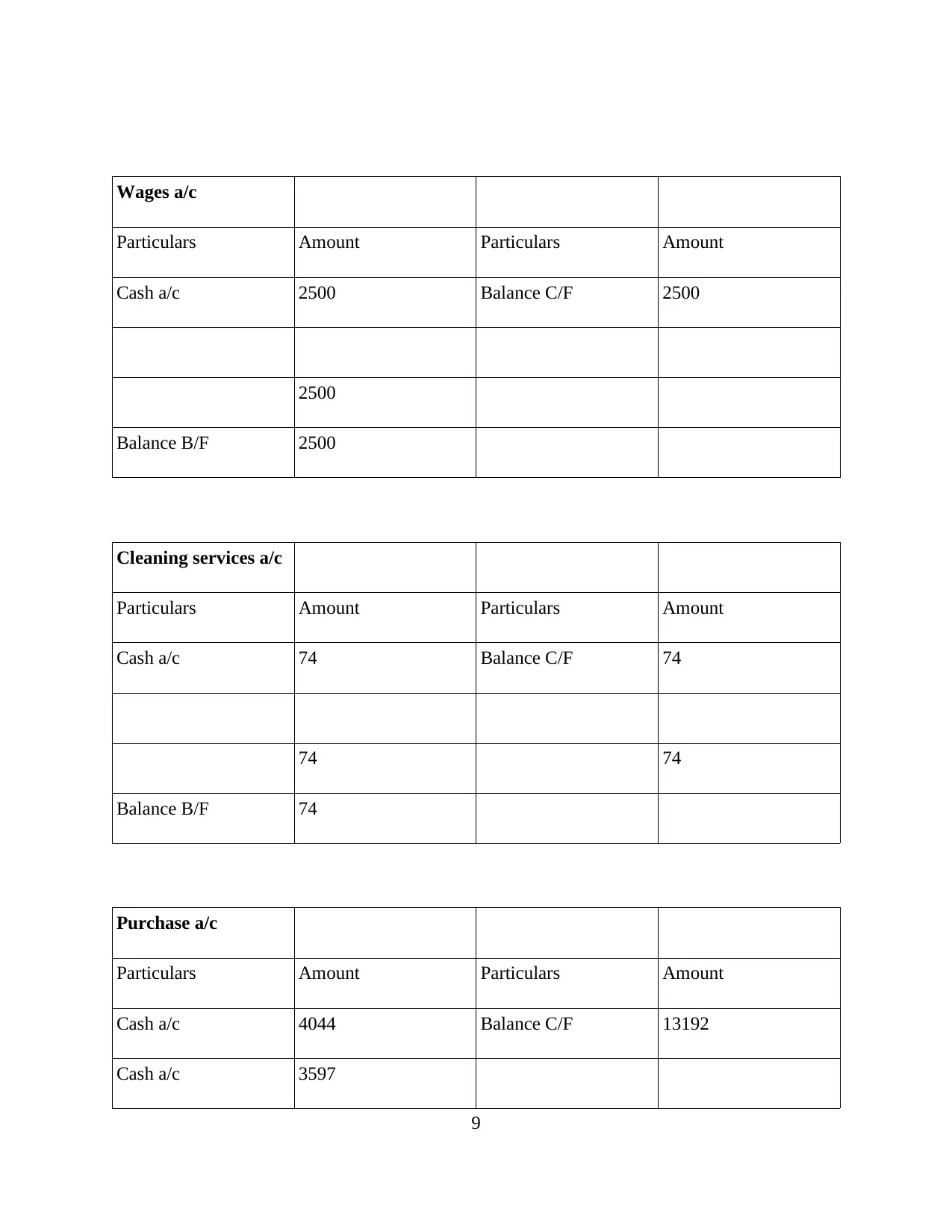

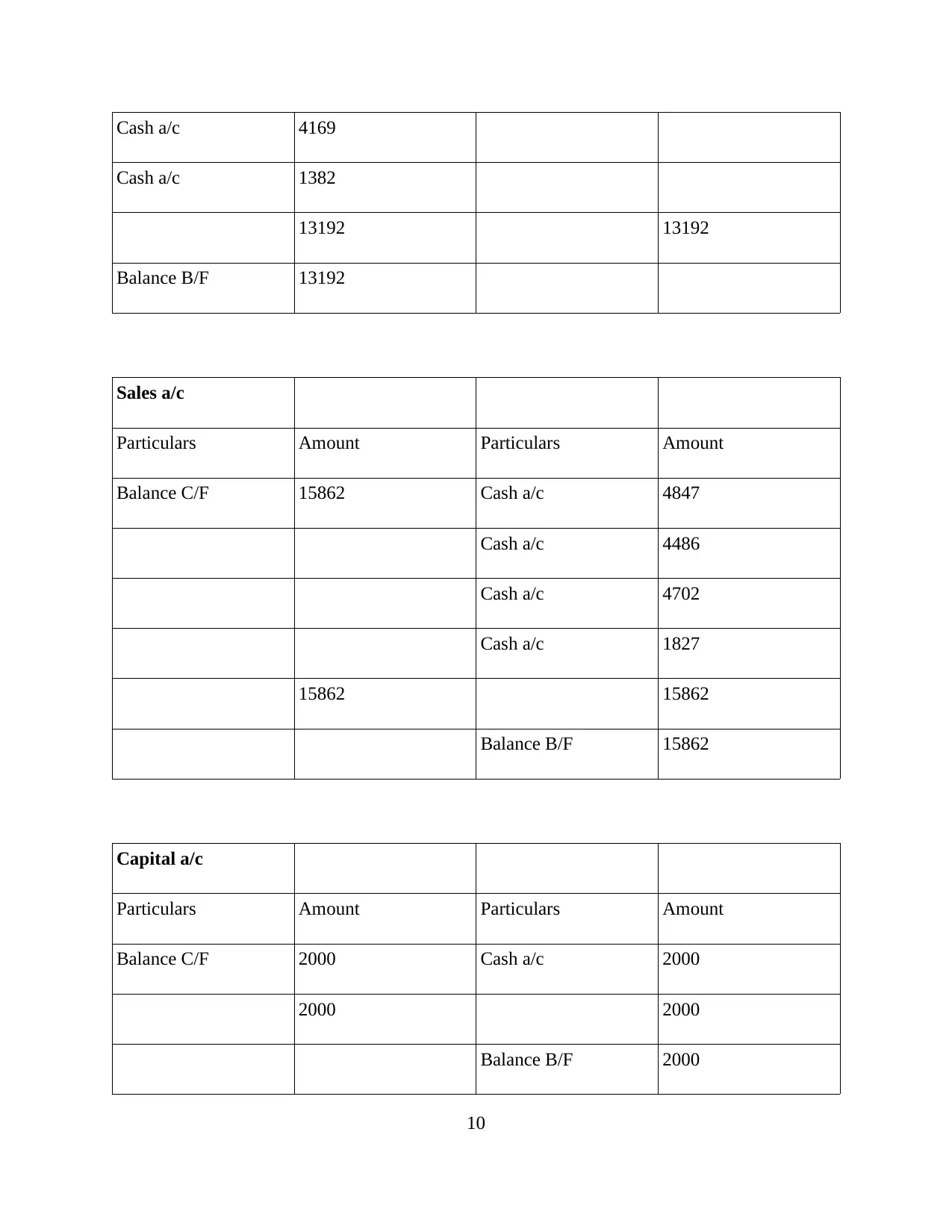

This report provides a comprehensive overview of accounting principles and their application in financial reporting. It begins by discussing the purpose and aims of accounting within an organization, differentiating between financial and management accounting, and highlighting the role of the IASB and SAC. The report then delves into practical accounting tasks, including preparing journal entries, constructing general ledger accounts, and creating a trial balance. It also covers the preparation of key financial statements such as the cash flow statement, income statement, and balance sheet. Furthermore, the report includes the computation of financial ratios to assess the financial performance of the Woody Train Organization, providing valuable insights into the company's profitability, liquidity, and solvency. The content covers a range of accounting concepts and practices essential for understanding financial statements and analyzing business performance.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.