Management Accounting Report - Financial Problem Solutions

VerifiedAdded on 2020/02/05

|18

|5653

|71

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and practices. It begins by defining management accounting and explores various systems, including cost accounting and inventory management. The report then delves into different methods used for management accounting reporting, such as job cost reports, inventory management reports, performance reports, and budget reports. It also includes detailed examples of sales, purchase, expenses, and cash budgets. Furthermore, the report examines cost calculation techniques, comparing marginal and absorption costing to prepare income statements. It also analyzes the advantages and disadvantages of different planning tools and explores how organizations adapt management accounting systems to address financial challenges. The report concludes with a discussion on the importance of effective management accounting for business success and provides a clear understanding of the concepts discussed.

MANAGEMENT

ACCOUNTING

1

ACCOUNTING

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction..........................................................................................................................................3

TASK 1.................................................................................................................................................3

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems.....................................................................................................3

P2 Explain different methods used for management accounting reporting.....................................5

TASK 2.................................................................................................................................................8

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

of marginal and absorption costing..................................................................................................8

TASK 3...............................................................................................................................................11

P4 Explain the advantages and disadvantages of different types of planning tools......................11

P5 Compare how organisations adapt management accounting systems to respond to financial

problems.........................................................................................................................................13

Conclusion..........................................................................................................................................13

References..........................................................................................................................................14

2

Introduction..........................................................................................................................................3

TASK 1.................................................................................................................................................3

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems.....................................................................................................3

P2 Explain different methods used for management accounting reporting.....................................5

TASK 2.................................................................................................................................................8

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

of marginal and absorption costing..................................................................................................8

TASK 3...............................................................................................................................................11

P4 Explain the advantages and disadvantages of different types of planning tools......................11

P5 Compare how organisations adapt management accounting systems to respond to financial

problems.........................................................................................................................................13

Conclusion..........................................................................................................................................13

References..........................................................................................................................................14

2

INTRODUCTION

In today's time, management continue increasing with enhancement of number of interfaces

of complexities in the business which give birth. Small scale entity has been selected for this project

report whose management structures are defined in the report. This project is all about explaining

management accounting system and reports. The cost statements under absorption and marginal

costing along with types of planning and various tools and techniques used in eliminating financial

crisis occurred in the firm.

TASK 1

P1 Different types of management accounting system

Primary concern of management is to reduce its cost as revenue can be generated by

reducing all kinds of cost incurred in the business. Management accounting is a terminology under

which various streams are included such as accounting, finance and management in order to

strengthen the overall business of an individual. Tools and techniques covered in the management

accounting will be used by an entity owner in uplifting the existing business conditions of the firm.

The primary responsibility of the firm is to get rid of all the current problems faced by an entity in

handling complexity in the business (Renz, 2016). The quality of decisions gets improved when

management accounting principles are followed by an individual in improving their business.

Qualified chartered accountants verified as per ICMA will maintain the books of accounts of an

entity.

In the current case scenario, small scale entity has chosen who have 50 employees but poor

performance of the business. The small number of employees is not strong enough in order to face

the external difficulties of the business (Otley and Emmanuel, 2013). Adoption of management

accounting principles will be helpful for all business users in amending their business structure in

order to relieve all their stress. The structure of an entity will be redefine using this kind of

approach under which tasks and duties are delegated to individuals in accomplishing all the desired

aims and targets of the business. There are different kinds of management accounting systems to be

used by an entity in improving their business is given as below:

Cost accounting systems- It is that kind of systems which involves techniques helps in determining

the cost incurred in the business (Otley and Emmanuel, 2013). Cost is regarded as major factor of

every business in which needs to be evaluated in order to eliminate from the business. The cost

accounting systems has categorised into two categories such as process and job order costing.

3

In today's time, management continue increasing with enhancement of number of interfaces

of complexities in the business which give birth. Small scale entity has been selected for this project

report whose management structures are defined in the report. This project is all about explaining

management accounting system and reports. The cost statements under absorption and marginal

costing along with types of planning and various tools and techniques used in eliminating financial

crisis occurred in the firm.

TASK 1

P1 Different types of management accounting system

Primary concern of management is to reduce its cost as revenue can be generated by

reducing all kinds of cost incurred in the business. Management accounting is a terminology under

which various streams are included such as accounting, finance and management in order to

strengthen the overall business of an individual. Tools and techniques covered in the management

accounting will be used by an entity owner in uplifting the existing business conditions of the firm.

The primary responsibility of the firm is to get rid of all the current problems faced by an entity in

handling complexity in the business (Renz, 2016). The quality of decisions gets improved when

management accounting principles are followed by an individual in improving their business.

Qualified chartered accountants verified as per ICMA will maintain the books of accounts of an

entity.

In the current case scenario, small scale entity has chosen who have 50 employees but poor

performance of the business. The small number of employees is not strong enough in order to face

the external difficulties of the business (Otley and Emmanuel, 2013). Adoption of management

accounting principles will be helpful for all business users in amending their business structure in

order to relieve all their stress. The structure of an entity will be redefine using this kind of

approach under which tasks and duties are delegated to individuals in accomplishing all the desired

aims and targets of the business. There are different kinds of management accounting systems to be

used by an entity in improving their business is given as below:

Cost accounting systems- It is that kind of systems which involves techniques helps in determining

the cost incurred in the business (Otley and Emmanuel, 2013). Cost is regarded as major factor of

every business in which needs to be evaluated in order to eliminate from the business. The cost

accounting systems has categorised into two categories such as process and job order costing.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

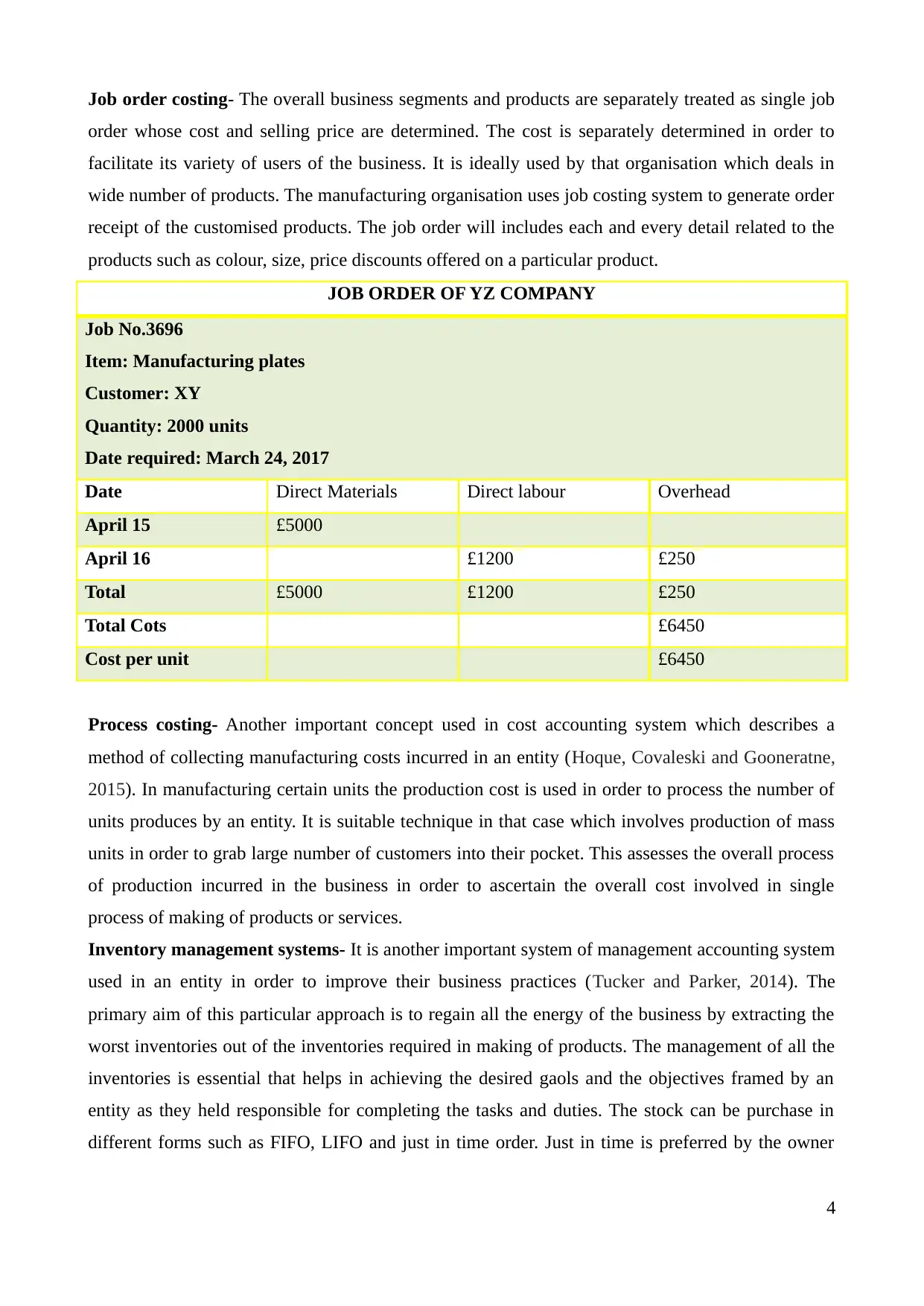

Job order costing- The overall business segments and products are separately treated as single job

order whose cost and selling price are determined. The cost is separately determined in order to

facilitate its variety of users of the business. It is ideally used by that organisation which deals in

wide number of products. The manufacturing organisation uses job costing system to generate order

receipt of the customised products. The job order will includes each and every detail related to the

products such as colour, size, price discounts offered on a particular product.

JOB ORDER OF YZ COMPANY

Job No.3696

Item: Manufacturing plates

Customer: XY

Quantity: 2000 units

Date required: March 24, 2017

Date Direct Materials Direct labour Overhead

April 15 £5000

April 16 £1200 £250

Total £5000 £1200 £250

Total Cots £6450

Cost per unit £6450

Process costing- Another important concept used in cost accounting system which describes a

method of collecting manufacturing costs incurred in an entity (Hoque, Covaleski and Gooneratne,

2015). In manufacturing certain units the production cost is used in order to process the number of

units produces by an entity. It is suitable technique in that case which involves production of mass

units in order to grab large number of customers into their pocket. This assesses the overall process

of production incurred in the business in order to ascertain the overall cost involved in single

process of making of products or services.

Inventory management systems- It is another important system of management accounting system

used in an entity in order to improve their business practices (Tucker and Parker, 2014). The

primary aim of this particular approach is to regain all the energy of the business by extracting the

worst inventories out of the inventories required in making of products. The management of all the

inventories is essential that helps in achieving the desired gaols and the objectives framed by an

entity as they held responsible for completing the tasks and duties. The stock can be purchase in

different forms such as FIFO, LIFO and just in time order. Just in time is preferred by the owner

4

order whose cost and selling price are determined. The cost is separately determined in order to

facilitate its variety of users of the business. It is ideally used by that organisation which deals in

wide number of products. The manufacturing organisation uses job costing system to generate order

receipt of the customised products. The job order will includes each and every detail related to the

products such as colour, size, price discounts offered on a particular product.

JOB ORDER OF YZ COMPANY

Job No.3696

Item: Manufacturing plates

Customer: XY

Quantity: 2000 units

Date required: March 24, 2017

Date Direct Materials Direct labour Overhead

April 15 £5000

April 16 £1200 £250

Total £5000 £1200 £250

Total Cots £6450

Cost per unit £6450

Process costing- Another important concept used in cost accounting system which describes a

method of collecting manufacturing costs incurred in an entity (Hoque, Covaleski and Gooneratne,

2015). In manufacturing certain units the production cost is used in order to process the number of

units produces by an entity. It is suitable technique in that case which involves production of mass

units in order to grab large number of customers into their pocket. This assesses the overall process

of production incurred in the business in order to ascertain the overall cost involved in single

process of making of products or services.

Inventory management systems- It is another important system of management accounting system

used in an entity in order to improve their business practices (Tucker and Parker, 2014). The

primary aim of this particular approach is to regain all the energy of the business by extracting the

worst inventories out of the inventories required in making of products. The management of all the

inventories is essential that helps in achieving the desired gaols and the objectives framed by an

entity as they held responsible for completing the tasks and duties. The stock can be purchase in

different forms such as FIFO, LIFO and just in time order. Just in time is preferred by the owner

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

under which inventories are purchased just to meet out the order as this helps in saving the

warehouse cost to be incurred in the firm (Hoque, Covaleski and Gooneratne, 2015). Several ways

used by an entity owner for inventory management just to procure the inventory for the betterment

of the business. The software can be used to refill the inventory when it reaches the particular to

meet out the order and doesn’t lose their customers due to lack of available resources in the

business. It can be regulated by using barcode scanner which helps in keeping record of each and

every item stored in the business. The bar codes are prepared which includes detail information

regarding the products which can be easily accessed by the owner by just scanning the items entered

into the business. This barcode includes information about seller and buyer of the product, item

size, colour, preferences of the customers. In current business environment mobile devices are also

used by an individual in getting information related to the products or a service currently deals in by

the business owner.

P2 Methods which used in the management accounting

Every business need to understand how they perform through continuous assessment and

reporting to set targets, objectives and goals. In this way, adjustments are also required make where

it is necessary so that business carry blindfolded to plunge to measure key metrics. There are

following reasons explained for management report:

Set benchmarks for enhancing performances: It is the important and immediate benefit

for performance reporting. In this aspect, the enterprise need to set their bench marks from where

entity can base their performance results.

Measure, control and monitor workforce: Further, enterprise also require implement

performance indicators such as KPIs within the command that are existed in top and control

method. It will help to control workers behaviour and their actions which defines performances.

Enhancement and learning from performances: In the day to day operations, business

process management needed for continue development of learning process. It helps to equip

personnel with key information to make better decisions.

Methods that are used in the management accounting report

Accounting of management report assists to the organisation people to monitor

performances and prepare it in accounting period. Following are different methods through

management accounting report can be made:

Report of job cost: This report help to show expenses which incurred in the particular

project. In this way, company match their expenses with revenue so that they can easily evaluate

profitability to assess high earning or not within the business unit. Company can also focus on the

5

warehouse cost to be incurred in the firm (Hoque, Covaleski and Gooneratne, 2015). Several ways

used by an entity owner for inventory management just to procure the inventory for the betterment

of the business. The software can be used to refill the inventory when it reaches the particular to

meet out the order and doesn’t lose their customers due to lack of available resources in the

business. It can be regulated by using barcode scanner which helps in keeping record of each and

every item stored in the business. The bar codes are prepared which includes detail information

regarding the products which can be easily accessed by the owner by just scanning the items entered

into the business. This barcode includes information about seller and buyer of the product, item

size, colour, preferences of the customers. In current business environment mobile devices are also

used by an individual in getting information related to the products or a service currently deals in by

the business owner.

P2 Methods which used in the management accounting

Every business need to understand how they perform through continuous assessment and

reporting to set targets, objectives and goals. In this way, adjustments are also required make where

it is necessary so that business carry blindfolded to plunge to measure key metrics. There are

following reasons explained for management report:

Set benchmarks for enhancing performances: It is the important and immediate benefit

for performance reporting. In this aspect, the enterprise need to set their bench marks from where

entity can base their performance results.

Measure, control and monitor workforce: Further, enterprise also require implement

performance indicators such as KPIs within the command that are existed in top and control

method. It will help to control workers behaviour and their actions which defines performances.

Enhancement and learning from performances: In the day to day operations, business

process management needed for continue development of learning process. It helps to equip

personnel with key information to make better decisions.

Methods that are used in the management accounting report

Accounting of management report assists to the organisation people to monitor

performances and prepare it in accounting period. Following are different methods through

management accounting report can be made:

Report of job cost: This report help to show expenses which incurred in the particular

project. In this way, company match their expenses with revenue so that they can easily evaluate

profitability to assess high earning or not within the business unit. Company can also focus on the

5

efforts that are made for doing effective performances without wasting of time.

Inventory management report: In the organisation, physical inventory use managerial

accounting report to make their manufacturing processed useful and more efficient. It includes

generally items such as inventory waste, labour hour and overhead, etc. The manager can compare

different assembly lines in the enterprise to see their improvements through best performing

department.

Performance report: Performance report include all important things through organisation

getting improvements. Therefore, it will help to undertake roles and responsibilities of person to

cater relevant information at workplace.

Operating budget report: Operating budget report help to the organisation to analysis their

performances. Managers can assess their performances which performed in the department. It is the

best way to control costs with estimation of budget. It is based on the actual expenditure which

incurred due to prior years.

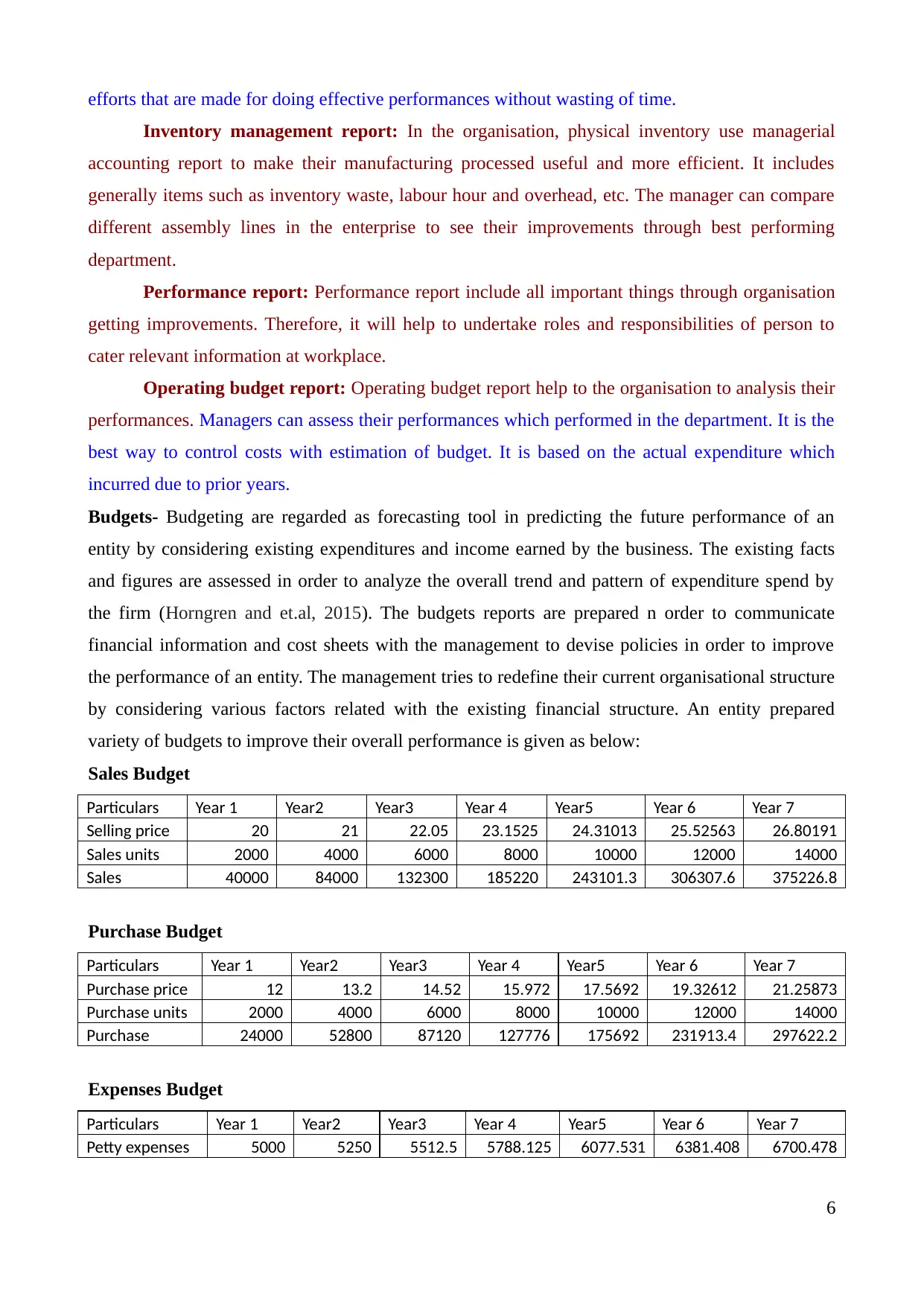

Budgets- Budgeting are regarded as forecasting tool in predicting the future performance of an

entity by considering existing expenditures and income earned by the business. The existing facts

and figures are assessed in order to analyze the overall trend and pattern of expenditure spend by

the firm (Horngren and et.al, 2015). The budgets reports are prepared n order to communicate

financial information and cost sheets with the management to devise policies in order to improve

the performance of an entity. The management tries to redefine their current organisational structure

by considering various factors related with the existing financial structure. An entity prepared

variety of budgets to improve their overall performance is given as below:

Sales Budget

Particulars Year 1 Year2 Year3 Year 4 Year5 Year 6 Year 7

Selling price 20 21 22.05 23.1525 24.31013 25.52563 26.80191

Sales units 2000 4000 6000 8000 10000 12000 14000

Sales 40000 84000 132300 185220 243101.3 306307.6 375226.8

Purchase Budget

Particulars Year 1 Year2 Year3 Year 4 Year5 Year 6 Year 7

Purchase price 12 13.2 14.52 15.972 17.5692 19.32612 21.25873

Purchase units 2000 4000 6000 8000 10000 12000 14000

Purchase 24000 52800 87120 127776 175692 231913.4 297622.2

Expenses Budget

Particulars Year 1 Year2 Year3 Year 4 Year5 Year 6 Year 7

Petty expenses 5000 5250 5512.5 5788.125 6077.531 6381.408 6700.478

6

Inventory management report: In the organisation, physical inventory use managerial

accounting report to make their manufacturing processed useful and more efficient. It includes

generally items such as inventory waste, labour hour and overhead, etc. The manager can compare

different assembly lines in the enterprise to see their improvements through best performing

department.

Performance report: Performance report include all important things through organisation

getting improvements. Therefore, it will help to undertake roles and responsibilities of person to

cater relevant information at workplace.

Operating budget report: Operating budget report help to the organisation to analysis their

performances. Managers can assess their performances which performed in the department. It is the

best way to control costs with estimation of budget. It is based on the actual expenditure which

incurred due to prior years.

Budgets- Budgeting are regarded as forecasting tool in predicting the future performance of an

entity by considering existing expenditures and income earned by the business. The existing facts

and figures are assessed in order to analyze the overall trend and pattern of expenditure spend by

the firm (Horngren and et.al, 2015). The budgets reports are prepared n order to communicate

financial information and cost sheets with the management to devise policies in order to improve

the performance of an entity. The management tries to redefine their current organisational structure

by considering various factors related with the existing financial structure. An entity prepared

variety of budgets to improve their overall performance is given as below:

Sales Budget

Particulars Year 1 Year2 Year3 Year 4 Year5 Year 6 Year 7

Selling price 20 21 22.05 23.1525 24.31013 25.52563 26.80191

Sales units 2000 4000 6000 8000 10000 12000 14000

Sales 40000 84000 132300 185220 243101.3 306307.6 375226.8

Purchase Budget

Particulars Year 1 Year2 Year3 Year 4 Year5 Year 6 Year 7

Purchase price 12 13.2 14.52 15.972 17.5692 19.32612 21.25873

Purchase units 2000 4000 6000 8000 10000 12000 14000

Purchase 24000 52800 87120 127776 175692 231913.4 297622.2

Expenses Budget

Particulars Year 1 Year2 Year3 Year 4 Year5 Year 6 Year 7

Petty expenses 5000 5250 5512.5 5788.125 6077.531 6381.408 6700.478

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

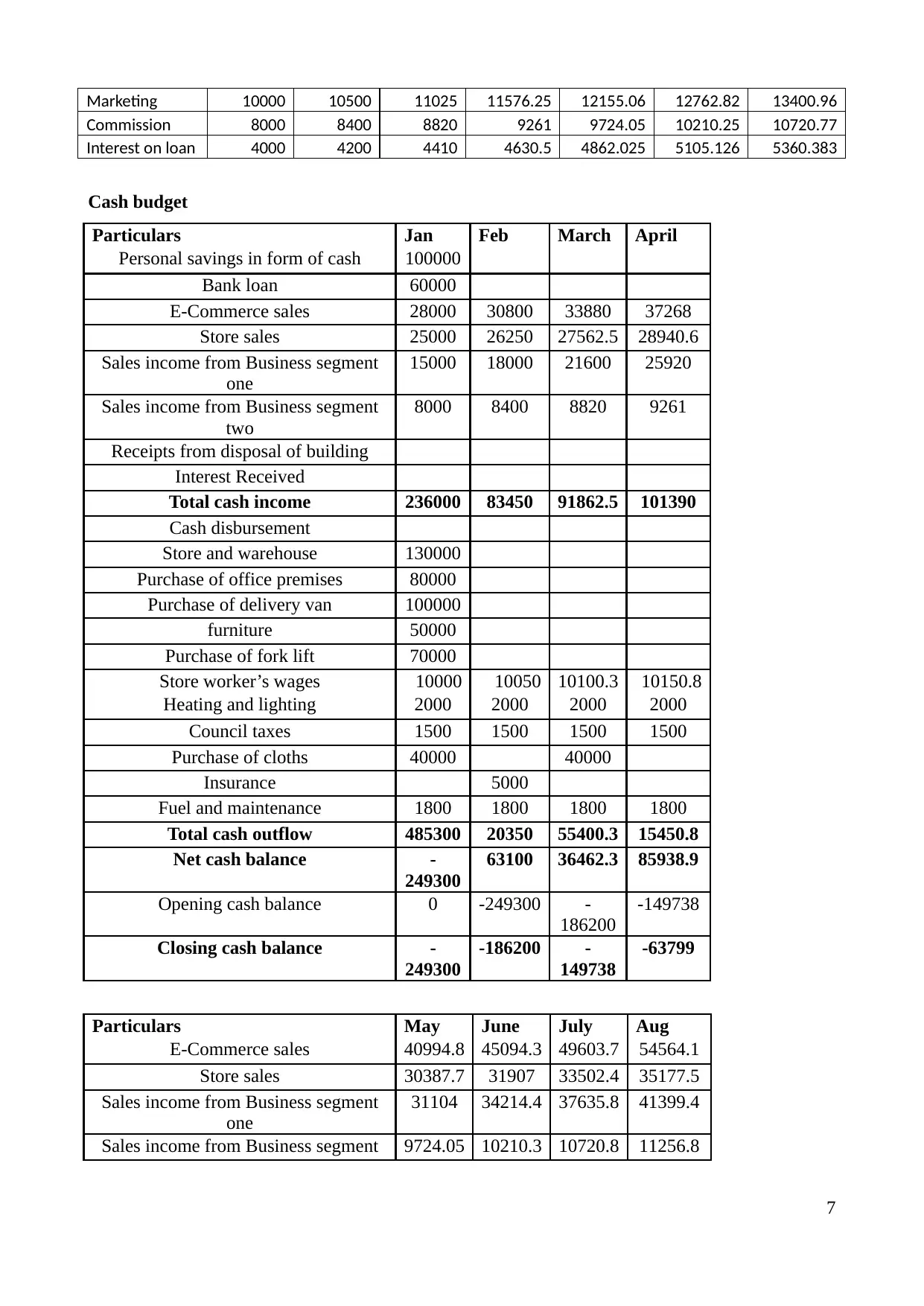

Marketing 10000 10500 11025 11576.25 12155.06 12762.82 13400.96

Commission 8000 8400 8820 9261 9724.05 10210.25 10720.77

Interest on loan 4000 4200 4410 4630.5 4862.025 5105.126 5360.383

Cash budget

Particulars Jan Feb March April

Personal savings in form of cash 100000

Bank loan 60000

E-Commerce sales 28000 30800 33880 37268

Store sales 25000 26250 27562.5 28940.6

Sales income from Business segment

one

15000 18000 21600 25920

Sales income from Business segment

two

8000 8400 8820 9261

Receipts from disposal of building

Interest Received

Total cash income 236000 83450 91862.5 101390

Cash disbursement

Store and warehouse 130000

Purchase of office premises 80000

Purchase of delivery van 100000

furniture 50000

Purchase of fork lift 70000

Store worker’s wages 10000 10050 10100.3 10150.8

Heating and lighting 2000 2000 2000 2000

Council taxes 1500 1500 1500 1500

Purchase of cloths 40000 40000

Insurance 5000

Fuel and maintenance 1800 1800 1800 1800

Total cash outflow 485300 20350 55400.3 15450.8

Net cash balance -

249300

63100 36462.3 85938.9

Opening cash balance 0 -249300 -

186200

-149738

Closing cash balance -

249300

-186200 -

149738

-63799

Particulars May June July Aug

E-Commerce sales 40994.8 45094.3 49603.7 54564.1

Store sales 30387.7 31907 33502.4 35177.5

Sales income from Business segment

one

31104 34214.4 37635.8 41399.4

Sales income from Business segment 9724.05 10210.3 10720.8 11256.8

7

Commission 8000 8400 8820 9261 9724.05 10210.25 10720.77

Interest on loan 4000 4200 4410 4630.5 4862.025 5105.126 5360.383

Cash budget

Particulars Jan Feb March April

Personal savings in form of cash 100000

Bank loan 60000

E-Commerce sales 28000 30800 33880 37268

Store sales 25000 26250 27562.5 28940.6

Sales income from Business segment

one

15000 18000 21600 25920

Sales income from Business segment

two

8000 8400 8820 9261

Receipts from disposal of building

Interest Received

Total cash income 236000 83450 91862.5 101390

Cash disbursement

Store and warehouse 130000

Purchase of office premises 80000

Purchase of delivery van 100000

furniture 50000

Purchase of fork lift 70000

Store worker’s wages 10000 10050 10100.3 10150.8

Heating and lighting 2000 2000 2000 2000

Council taxes 1500 1500 1500 1500

Purchase of cloths 40000 40000

Insurance 5000

Fuel and maintenance 1800 1800 1800 1800

Total cash outflow 485300 20350 55400.3 15450.8

Net cash balance -

249300

63100 36462.3 85938.9

Opening cash balance 0 -249300 -

186200

-149738

Closing cash balance -

249300

-186200 -

149738

-63799

Particulars May June July Aug

E-Commerce sales 40994.8 45094.3 49603.7 54564.1

Store sales 30387.7 31907 33502.4 35177.5

Sales income from Business segment

one

31104 34214.4 37635.8 41399.4

Sales income from Business segment 9724.05 10210.3 10720.8 11256.8

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

two

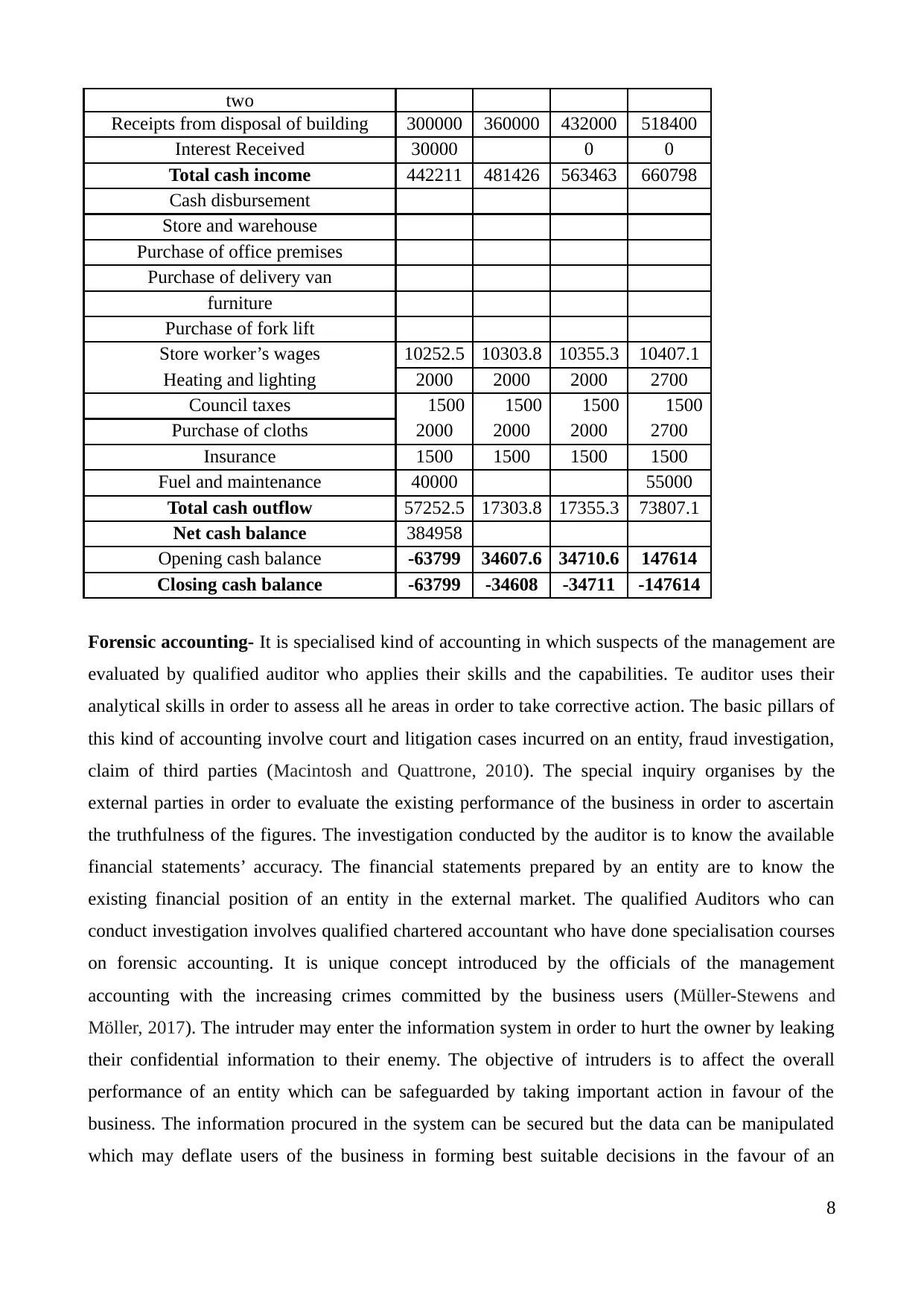

Receipts from disposal of building 300000 360000 432000 518400

Interest Received 30000 0 0

Total cash income 442211 481426 563463 660798

Cash disbursement

Store and warehouse

Purchase of office premises

Purchase of delivery van

furniture

Purchase of fork lift

Store worker’s wages 10252.5 10303.8 10355.3 10407.1

Heating and lighting 2000 2000 2000 2700

Council taxes 1500 1500 1500 1500

Purchase of cloths 2000 2000 2000 2700

Insurance 1500 1500 1500 1500

Fuel and maintenance 40000 55000

Total cash outflow 57252.5 17303.8 17355.3 73807.1

Net cash balance 384958

Opening cash balance -63799 34607.6 34710.6 147614

Closing cash balance -63799 -34608 -34711 -147614

Forensic accounting- It is specialised kind of accounting in which suspects of the management are

evaluated by qualified auditor who applies their skills and the capabilities. Te auditor uses their

analytical skills in order to assess all he areas in order to take corrective action. The basic pillars of

this kind of accounting involve court and litigation cases incurred on an entity, fraud investigation,

claim of third parties (Macintosh and Quattrone, 2010). The special inquiry organises by the

external parties in order to evaluate the existing performance of the business in order to ascertain

the truthfulness of the figures. The investigation conducted by the auditor is to know the available

financial statements’ accuracy. The financial statements prepared by an entity are to know the

existing financial position of an entity in the external market. The qualified Auditors who can

conduct investigation involves qualified chartered accountant who have done specialisation courses

on forensic accounting. It is unique concept introduced by the officials of the management

accounting with the increasing crimes committed by the business users (Müller-Stewens and

Möller, 2017). The intruder may enter the information system in order to hurt the owner by leaking

their confidential information to their enemy. The objective of intruders is to affect the overall

performance of an entity which can be safeguarded by taking important action in favour of the

business. The information procured in the system can be secured but the data can be manipulated

which may deflate users of the business in forming best suitable decisions in the favour of an

8

Receipts from disposal of building 300000 360000 432000 518400

Interest Received 30000 0 0

Total cash income 442211 481426 563463 660798

Cash disbursement

Store and warehouse

Purchase of office premises

Purchase of delivery van

furniture

Purchase of fork lift

Store worker’s wages 10252.5 10303.8 10355.3 10407.1

Heating and lighting 2000 2000 2000 2700

Council taxes 1500 1500 1500 1500

Purchase of cloths 2000 2000 2000 2700

Insurance 1500 1500 1500 1500

Fuel and maintenance 40000 55000

Total cash outflow 57252.5 17303.8 17355.3 73807.1

Net cash balance 384958

Opening cash balance -63799 34607.6 34710.6 147614

Closing cash balance -63799 -34608 -34711 -147614

Forensic accounting- It is specialised kind of accounting in which suspects of the management are

evaluated by qualified auditor who applies their skills and the capabilities. Te auditor uses their

analytical skills in order to assess all he areas in order to take corrective action. The basic pillars of

this kind of accounting involve court and litigation cases incurred on an entity, fraud investigation,

claim of third parties (Macintosh and Quattrone, 2010). The special inquiry organises by the

external parties in order to evaluate the existing performance of the business in order to ascertain

the truthfulness of the figures. The investigation conducted by the auditor is to know the available

financial statements’ accuracy. The financial statements prepared by an entity are to know the

existing financial position of an entity in the external market. The qualified Auditors who can

conduct investigation involves qualified chartered accountant who have done specialisation courses

on forensic accounting. It is unique concept introduced by the officials of the management

accounting with the increasing crimes committed by the business users (Müller-Stewens and

Möller, 2017). The intruder may enter the information system in order to hurt the owner by leaking

their confidential information to their enemy. The objective of intruders is to affect the overall

performance of an entity which can be safeguarded by taking important action in favour of the

business. The information procured in the system can be secured but the data can be manipulated

which may deflate users of the business in forming best suitable decisions in the favour of an

8

individual.

In the modern world of accounting this is regarded as best suitable approach in order to heal

the wounds given by the external parties by leaking the private business information. The curret

business can be protecting against the external threats by focusing on the quality of the information

stored in the business (Schulze and Heidenreich, 2017). The quality of information is important as it

can affect an entity’s objectives as wrong aim gives wrong direction to an entity to in reaching

wrong destination. Reaching destination other than success divert the interest of owner. Claims and

litigation on the owner can be investigated properly to resolve all the matters in a given time frame.

TASK 2

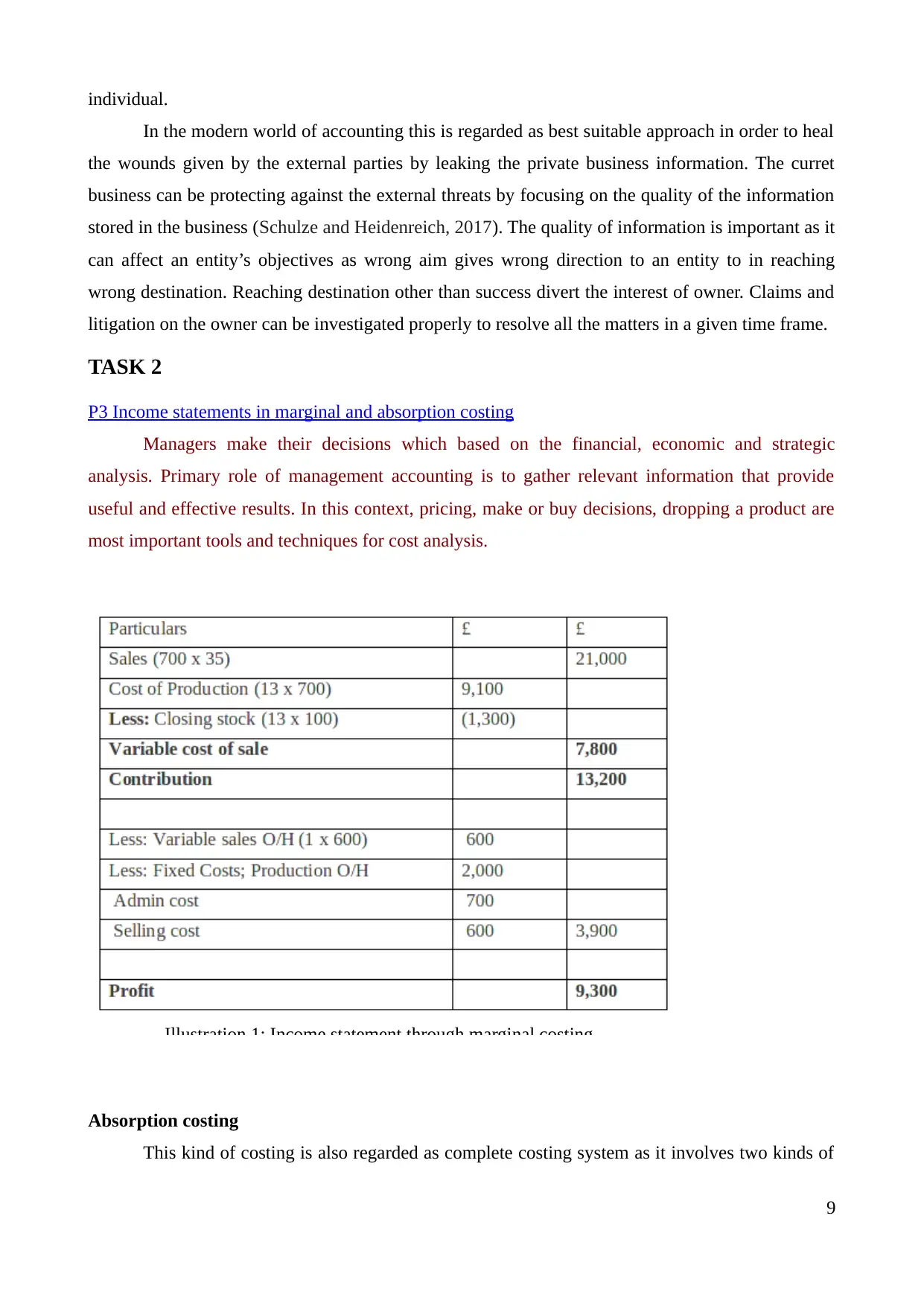

P3 Income statements in marginal and absorption costing

Managers make their decisions which based on the financial, economic and strategic

analysis. Primary role of management accounting is to gather relevant information that provide

useful and effective results. In this context, pricing, make or buy decisions, dropping a product are

most important tools and techniques for cost analysis.

Illustration 1: Income statement through marginal costing

Absorption costing

This kind of costing is also regarded as complete costing system as it involves two kinds of

9

In the modern world of accounting this is regarded as best suitable approach in order to heal

the wounds given by the external parties by leaking the private business information. The curret

business can be protecting against the external threats by focusing on the quality of the information

stored in the business (Schulze and Heidenreich, 2017). The quality of information is important as it

can affect an entity’s objectives as wrong aim gives wrong direction to an entity to in reaching

wrong destination. Reaching destination other than success divert the interest of owner. Claims and

litigation on the owner can be investigated properly to resolve all the matters in a given time frame.

TASK 2

P3 Income statements in marginal and absorption costing

Managers make their decisions which based on the financial, economic and strategic

analysis. Primary role of management accounting is to gather relevant information that provide

useful and effective results. In this context, pricing, make or buy decisions, dropping a product are

most important tools and techniques for cost analysis.

Illustration 1: Income statement through marginal costing

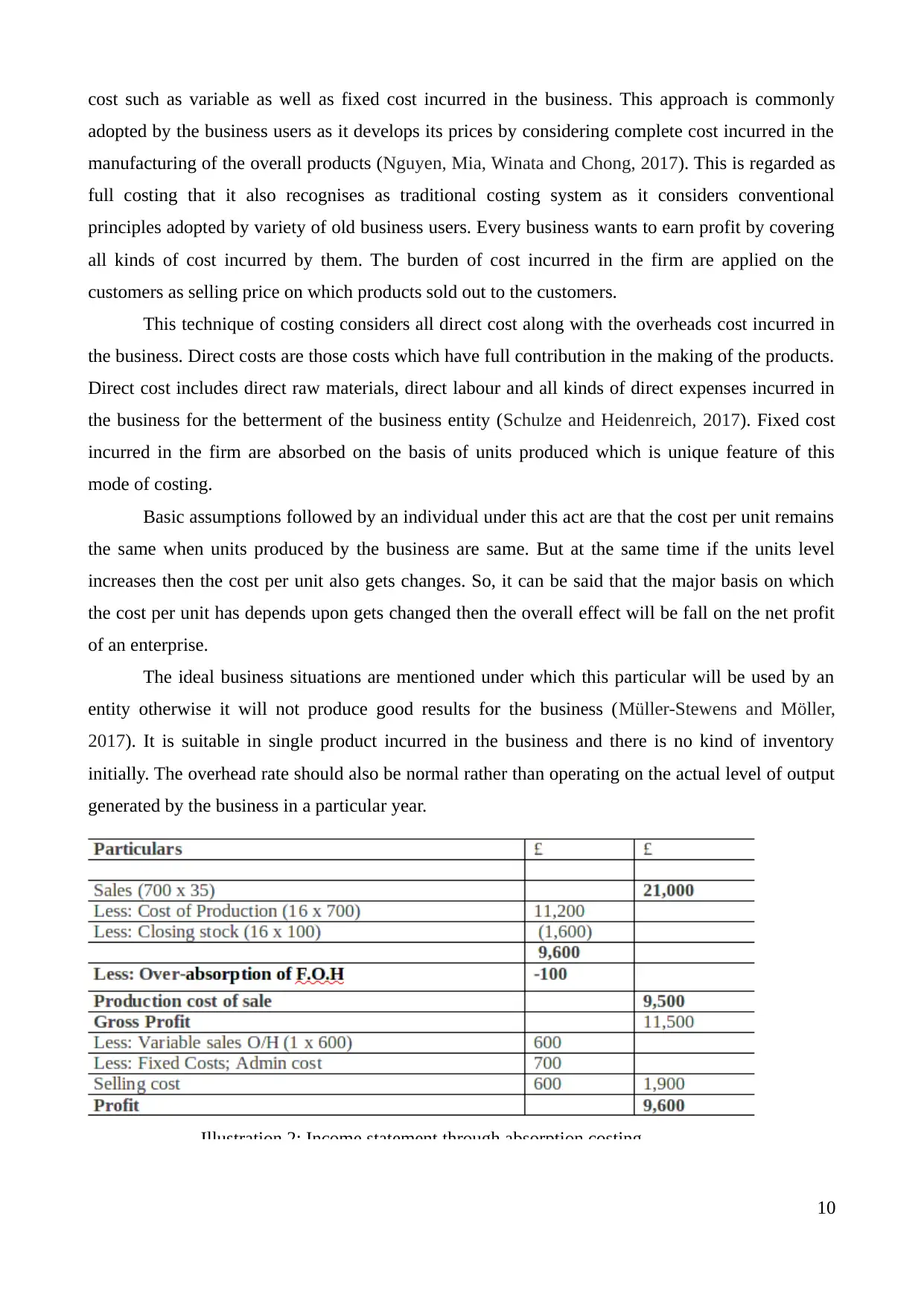

Absorption costing

This kind of costing is also regarded as complete costing system as it involves two kinds of

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

cost such as variable as well as fixed cost incurred in the business. This approach is commonly

adopted by the business users as it develops its prices by considering complete cost incurred in the

manufacturing of the overall products (Nguyen, Mia, Winata and Chong, 2017). This is regarded as

full costing that it also recognises as traditional costing system as it considers conventional

principles adopted by variety of old business users. Every business wants to earn profit by covering

all kinds of cost incurred by them. The burden of cost incurred in the firm are applied on the

customers as selling price on which products sold out to the customers.

This technique of costing considers all direct cost along with the overheads cost incurred in

the business. Direct costs are those costs which have full contribution in the making of the products.

Direct cost includes direct raw materials, direct labour and all kinds of direct expenses incurred in

the business for the betterment of the business entity (Schulze and Heidenreich, 2017). Fixed cost

incurred in the firm are absorbed on the basis of units produced which is unique feature of this

mode of costing.

Basic assumptions followed by an individual under this act are that the cost per unit remains

the same when units produced by the business are same. But at the same time if the units level

increases then the cost per unit also gets changes. So, it can be said that the major basis on which

the cost per unit has depends upon gets changed then the overall effect will be fall on the net profit

of an enterprise.

The ideal business situations are mentioned under which this particular will be used by an

entity otherwise it will not produce good results for the business (Müller-Stewens and Möller,

2017). It is suitable in single product incurred in the business and there is no kind of inventory

initially. The overhead rate should also be normal rather than operating on the actual level of output

generated by the business in a particular year.

Illustration 2: Income statement through absorption costing

10

adopted by the business users as it develops its prices by considering complete cost incurred in the

manufacturing of the overall products (Nguyen, Mia, Winata and Chong, 2017). This is regarded as

full costing that it also recognises as traditional costing system as it considers conventional

principles adopted by variety of old business users. Every business wants to earn profit by covering

all kinds of cost incurred by them. The burden of cost incurred in the firm are applied on the

customers as selling price on which products sold out to the customers.

This technique of costing considers all direct cost along with the overheads cost incurred in

the business. Direct costs are those costs which have full contribution in the making of the products.

Direct cost includes direct raw materials, direct labour and all kinds of direct expenses incurred in

the business for the betterment of the business entity (Schulze and Heidenreich, 2017). Fixed cost

incurred in the firm are absorbed on the basis of units produced which is unique feature of this

mode of costing.

Basic assumptions followed by an individual under this act are that the cost per unit remains

the same when units produced by the business are same. But at the same time if the units level

increases then the cost per unit also gets changes. So, it can be said that the major basis on which

the cost per unit has depends upon gets changed then the overall effect will be fall on the net profit

of an enterprise.

The ideal business situations are mentioned under which this particular will be used by an

entity otherwise it will not produce good results for the business (Müller-Stewens and Möller,

2017). It is suitable in single product incurred in the business and there is no kind of inventory

initially. The overhead rate should also be normal rather than operating on the actual level of output

generated by the business in a particular year.

Illustration 2: Income statement through absorption costing

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Marginal costing

The term marginal refers to additional unit used in the business will results in increase or

decrease in the income of the business enterprise (Nguyen, Mia, Winata and Chong, 2017). It is

important concept of economics under which every additional unit produced by the business will

results higher cost in the business. This terminology depicts that every additional unit in the

business reflects the sign of producing next unit in an entity to boost the existing income and

revenue of the business.

It is renamed as variable costing technique that considers only variable cost in evaluating the

overall cost incurred in the business (Horngren and et.al., 2015). Fixed cost in this technique is

taken as period cost which will be wholly deducted from the contribution earned by the business.

The logic behind considering the variable cost into the costing statements of an entity to bring

changes in the existing organisation structure. It includes variable cost as it changes simultaneously

with the minute changes occurred in the sales units produced by the business. Fixed cost is simply

deducted in total out of the contribution earned by an entity.

Contribution margin has significant role-play in the business as it helps in determining the

actual contribution amount earned by an entity in the future (Schulze and Heidenreich, 2017).

Ascertainment of contribution is essential as it is a clear difference among sales and the variable

cost. Cost volume and profit analysis is important evaluation technique used in verifying three

components. Cost and volume has indirect proportion to each other as increase in cost decreases the

sales and vice and versa. The relationship between cost and sales of an entity will directly affect the

overall impact on the profit of the firm.

Nowadays marginal costing is an important measure used in developing the sales price mix

in order to take important decisions related to the price mix of an entity. Price mixes developed by

the owner is a mixture of various components held by the owner in order to improve their quality of

business (Macintosh and Quattrone, 2010). The major objective of an enterprise owner is to handle

external pressures of the market in meeting desired goals and the objectives develop by an entity.

Profit Volume ratio is another segment involved in the contribution margin in which prices

of various products are develop according to the particular contribution earned by the business.

Higher the contribution higher will be the overall amount received by an entity owner in the near

future. Owner devise prices based on this technique would helpful for the business in attracting

wide number of customers as they held responsible for attaining higher market share in the market

as compared to the existing competitors (Hoque, Covaleski and Gooneratne, 2015). The rivalry of

the market can be eliminated by strengthening the current business operated by the business owner.

It has been observed from the above determination of net profit of the same entity under two

11

The term marginal refers to additional unit used in the business will results in increase or

decrease in the income of the business enterprise (Nguyen, Mia, Winata and Chong, 2017). It is

important concept of economics under which every additional unit produced by the business will

results higher cost in the business. This terminology depicts that every additional unit in the

business reflects the sign of producing next unit in an entity to boost the existing income and

revenue of the business.

It is renamed as variable costing technique that considers only variable cost in evaluating the

overall cost incurred in the business (Horngren and et.al., 2015). Fixed cost in this technique is

taken as period cost which will be wholly deducted from the contribution earned by the business.

The logic behind considering the variable cost into the costing statements of an entity to bring

changes in the existing organisation structure. It includes variable cost as it changes simultaneously

with the minute changes occurred in the sales units produced by the business. Fixed cost is simply

deducted in total out of the contribution earned by an entity.

Contribution margin has significant role-play in the business as it helps in determining the

actual contribution amount earned by an entity in the future (Schulze and Heidenreich, 2017).

Ascertainment of contribution is essential as it is a clear difference among sales and the variable

cost. Cost volume and profit analysis is important evaluation technique used in verifying three

components. Cost and volume has indirect proportion to each other as increase in cost decreases the

sales and vice and versa. The relationship between cost and sales of an entity will directly affect the

overall impact on the profit of the firm.

Nowadays marginal costing is an important measure used in developing the sales price mix

in order to take important decisions related to the price mix of an entity. Price mixes developed by

the owner is a mixture of various components held by the owner in order to improve their quality of

business (Macintosh and Quattrone, 2010). The major objective of an enterprise owner is to handle

external pressures of the market in meeting desired goals and the objectives develop by an entity.

Profit Volume ratio is another segment involved in the contribution margin in which prices

of various products are develop according to the particular contribution earned by the business.

Higher the contribution higher will be the overall amount received by an entity owner in the near

future. Owner devise prices based on this technique would helpful for the business in attracting

wide number of customers as they held responsible for attaining higher market share in the market

as compared to the existing competitors (Hoque, Covaleski and Gooneratne, 2015). The rivalry of

the market can be eliminated by strengthening the current business operated by the business owner.

It has been observed from the above determination of net profit of the same entity under two

11

different manners (Horngren and et.al., 2015). Several methods used to determine the final profit

incurred in the business of small scale enterprise through marginal or absorption costing statements.

It has been noticed that net profit is higher in absorption costing as compared to the results obtained

through marginal costing. The difference among both the methods is due to the treatment of fixed

cost. In absorption costing fixed cost is treated as production cost in the business but on the other

hand same fixed cost is treated as period cost in marginal costing. The reason behind considering

fixed cost as period cost as this is wholly deducted from the contribution of the business.

TASK 3

P4 Explain the advantages and disadvantages of different types of planning tools

Planning and budgetary control: Budget is the important tool in planning and control

process. It includes three main elements such as mission, goals and objectives. It describes

performances report that help to make budget program. It possesses advantages such as definite

planning, enhance efficiency, proper communication, control and delegation of authority. However,

it also includes disadvantages such as in business there is lack of participation of several people, ity

can causes perception of unfairness. It creates competition for resources and politics.

Planning tools used by the selected business for budgetary control: Following are

different planning tools are used by the selected business for budgetary-control: Financial budget: Financial budgets includes details about expect to get its cash for coming

time. It includes several elements such as cash budget, capital expenditure budget, balance

sheet budget, etc. With using this tool, the organisation has advantages to cater relevant

information in cash, etc. Advantages of this tool is to assess amount which essentially

require for business development. However, it includes disadvantages such as reduction in

monetary value. Operating budget: This type of budget includes expression of the planned operations for the

particular period. In this way, different types of budget can be calculated such as sales and

revenue budget, expenses budget and project budget. Advantages of this budget are manager

can easily understand about future financial position. However, it includes disadvantage that

it enhance expenses which create problem in the business. Non-monetary budget: In this type of budget expressed non financial sales and revenue such

as profit. When anticipated profit is too small, there are several steps needed to enhance

sales budget and cut expenses as well. Due to cut expenses budget, organisation unable to

cater their actual profit in significant manner. Cash Budget: It is the simplest method that assists to forecast cash receipts and

12

incurred in the business of small scale enterprise through marginal or absorption costing statements.

It has been noticed that net profit is higher in absorption costing as compared to the results obtained

through marginal costing. The difference among both the methods is due to the treatment of fixed

cost. In absorption costing fixed cost is treated as production cost in the business but on the other

hand same fixed cost is treated as period cost in marginal costing. The reason behind considering

fixed cost as period cost as this is wholly deducted from the contribution of the business.

TASK 3

P4 Explain the advantages and disadvantages of different types of planning tools

Planning and budgetary control: Budget is the important tool in planning and control

process. It includes three main elements such as mission, goals and objectives. It describes

performances report that help to make budget program. It possesses advantages such as definite

planning, enhance efficiency, proper communication, control and delegation of authority. However,

it also includes disadvantages such as in business there is lack of participation of several people, ity

can causes perception of unfairness. It creates competition for resources and politics.

Planning tools used by the selected business for budgetary control: Following are

different planning tools are used by the selected business for budgetary-control: Financial budget: Financial budgets includes details about expect to get its cash for coming

time. It includes several elements such as cash budget, capital expenditure budget, balance

sheet budget, etc. With using this tool, the organisation has advantages to cater relevant

information in cash, etc. Advantages of this tool is to assess amount which essentially

require for business development. However, it includes disadvantages such as reduction in

monetary value. Operating budget: This type of budget includes expression of the planned operations for the

particular period. In this way, different types of budget can be calculated such as sales and

revenue budget, expenses budget and project budget. Advantages of this budget are manager

can easily understand about future financial position. However, it includes disadvantage that

it enhance expenses which create problem in the business. Non-monetary budget: In this type of budget expressed non financial sales and revenue such

as profit. When anticipated profit is too small, there are several steps needed to enhance

sales budget and cut expenses as well. Due to cut expenses budget, organisation unable to

cater their actual profit in significant manner. Cash Budget: It is the simplest method that assists to forecast cash receipts and

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.