Accounting and Financial Management Report: Analysis and Review

VerifiedAdded on 2022/08/25

|21

|5645

|12

Report

AI Summary

This report provides a comprehensive analysis of accounting and financial management principles. It begins with an examination of International Financial Reporting Standards (IFRS) and their role in harmonizing global accounting practices, discussing obstacles such as nationalism and the differences between rules-based and principles-based accounting. The report then includes the creation of a simplified balance sheet, calculation of working capital, and analysis of financial statements using common-size analysis. Profitability ratios are computed and interpreted to assess the company's financial performance. The report demonstrates the application of accounting concepts through practical financial analysis, including the interpretation of financial data and the evaluation of the company's financial health and operational efficiency. The report also analyses the company's debt, equity, and cash flow, providing a holistic view of its financial position and performance over several years.

Running head: ACCOUNTING & FINANCIAL MANAGEMENT

Accounting & Financial Management

Name of the Student

Name of the University

Author Note

Accounting & Financial Management

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING & FINANCIAL MANAGEMENT

Table of Contents

Part A...........................................................................................................................................2

Question one................................................................................................................................2

Question two................................................................................................................................5

Question three..............................................................................................................................5

Question four................................................................................................................................6

Question five................................................................................................................................7

Question six..................................................................................................................................8

Part B..........................................................................................................................................10

Question One..............................................................................................................................10

Question two..............................................................................................................................11

Question three............................................................................................................................13

References..................................................................................................................................18

ACCOUNTING & FINANCIAL MANAGEMENT

Table of Contents

Part A...........................................................................................................................................2

Question one................................................................................................................................2

Question two................................................................................................................................5

Question three..............................................................................................................................5

Question four................................................................................................................................6

Question five................................................................................................................................7

Question six..................................................................................................................................8

Part B..........................................................................................................................................10

Question One..............................................................................................................................10

Question two..............................................................................................................................11

Question three............................................................................................................................13

References..................................................................................................................................18

2

ACCOUNTING & FINANCIAL MANAGEMENT

Part A

Question one

The International Financial Reporting Standards (IFRS) are a set of common reporting

rules which are useful in preparing the financial statements in a consistent, transparent and

comparable manner around the world. Issued by the International Accounting Standards Board

(IASB), these guidelines specify how companies should report and maintain their accounts. The

process of harmonisation of financial statements is one where the comparability of accounting

practices is increased by reducing the degree of variation. In order to reduce the variation

between the financial statements, the compatibility of accounting practices is improved by

setting bounds to the degree of the variation of the financial statements. This is different from

standardisation in the sense that it does not impose a more rigid or narrow set of rules in

preparing the financial statements. In other words, harmonization of accounting practices does

not bring out uniformity by reducing the available alternatives but combines the different

elements of accounting practices into a structure.

Many of the regulators worldwide believe that the IFRS developed by the IASB brings

harmonization to the accounting standards followed across the world. This is because the

adoption of IFRS not only provides superior information to the users of the financial statements

but also helps the company in making strategic decisions. Due to the increased transparency in

the information provided by the financial statements, the comparability of the information

becomes much easier. While the methods of accounting may be different, the manner in which

they were applied by the firms is clearly stated. Hence, the adoption of IFRS brings a positive

impact on the comparability of financial statements. For companies from developing countries

which are looking to be a part of the process of globalisation, adoption of IFRS is the best option

ACCOUNTING & FINANCIAL MANAGEMENT

Part A

Question one

The International Financial Reporting Standards (IFRS) are a set of common reporting

rules which are useful in preparing the financial statements in a consistent, transparent and

comparable manner around the world. Issued by the International Accounting Standards Board

(IASB), these guidelines specify how companies should report and maintain their accounts. The

process of harmonisation of financial statements is one where the comparability of accounting

practices is increased by reducing the degree of variation. In order to reduce the variation

between the financial statements, the compatibility of accounting practices is improved by

setting bounds to the degree of the variation of the financial statements. This is different from

standardisation in the sense that it does not impose a more rigid or narrow set of rules in

preparing the financial statements. In other words, harmonization of accounting practices does

not bring out uniformity by reducing the available alternatives but combines the different

elements of accounting practices into a structure.

Many of the regulators worldwide believe that the IFRS developed by the IASB brings

harmonization to the accounting standards followed across the world. This is because the

adoption of IFRS not only provides superior information to the users of the financial statements

but also helps the company in making strategic decisions. Due to the increased transparency in

the information provided by the financial statements, the comparability of the information

becomes much easier. While the methods of accounting may be different, the manner in which

they were applied by the firms is clearly stated. Hence, the adoption of IFRS brings a positive

impact on the comparability of financial statements. For companies from developing countries

which are looking to be a part of the process of globalisation, adoption of IFRS is the best option

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING & FINANCIAL MANAGEMENT

in becoming a part of the foreign exchange markets. This not only results in an increase in the

quality of the reporting but also makes the firm global in every manner possible. Several

countries like India and the European nations have announced their convergence with the IFRS

as a part of improving the process of harmonization of financial statements (Desai 2016). The

technical developments brought by the IFRS has resulted in the opportunity for accelerating the

process of accounting and making it more precise. Some of the techniques like the constant

calculation of time value of money and the revaluation of the fixed assets of the company have

been made easier by the adoption of IFRS as a part of the financial reporting of the entity. The

availability of the new technologies and the adoption of these aspects as a part of IFRS has made

it much easier to calculate the changes occurring in the business (Darabos and Hrerczeg 2015).

Individual studies in case of Tunisian firms suggests that the level of harmonisation in

case of the accounting policies has remained at the same level irrespective of the level of

adoption of IFRS. Hence, some of the studies in relation to the harmonisation after IFRS provide

results which may not be consistent with the results of prior studies. This also reveals that there

is a lack of information about the evaluation of the accounting practices and the impact in case of

developing countries. However, due to the recent adoption of the practices of IFRS, the studies

conducted in developing countries are limited to a very short span of time. A broader set of

information in relation to the same is not available for the process of analysis (Alnaas 2017).

Another reason for the lack of quicker harmonisation in the accounting practices is the lack of

uniformity in the adoption of IFRS principles by the business. Some firms tend to adopt IFRS

more vigorously while other firms are not particularly active in the complete adoption of IFRS as

a part of the business. The adoption of the specific standards by the business is also a result of

the specific characteristics of the firm. Due to these differences, firms tend to become selective

ACCOUNTING & FINANCIAL MANAGEMENT

in becoming a part of the foreign exchange markets. This not only results in an increase in the

quality of the reporting but also makes the firm global in every manner possible. Several

countries like India and the European nations have announced their convergence with the IFRS

as a part of improving the process of harmonization of financial statements (Desai 2016). The

technical developments brought by the IFRS has resulted in the opportunity for accelerating the

process of accounting and making it more precise. Some of the techniques like the constant

calculation of time value of money and the revaluation of the fixed assets of the company have

been made easier by the adoption of IFRS as a part of the financial reporting of the entity. The

availability of the new technologies and the adoption of these aspects as a part of IFRS has made

it much easier to calculate the changes occurring in the business (Darabos and Hrerczeg 2015).

Individual studies in case of Tunisian firms suggests that the level of harmonisation in

case of the accounting policies has remained at the same level irrespective of the level of

adoption of IFRS. Hence, some of the studies in relation to the harmonisation after IFRS provide

results which may not be consistent with the results of prior studies. This also reveals that there

is a lack of information about the evaluation of the accounting practices and the impact in case of

developing countries. However, due to the recent adoption of the practices of IFRS, the studies

conducted in developing countries are limited to a very short span of time. A broader set of

information in relation to the same is not available for the process of analysis (Alnaas 2017).

Another reason for the lack of quicker harmonisation in the accounting practices is the lack of

uniformity in the adoption of IFRS principles by the business. Some firms tend to adopt IFRS

more vigorously while other firms are not particularly active in the complete adoption of IFRS as

a part of the business. The adoption of the specific standards by the business is also a result of

the specific characteristics of the firm. Due to these differences, firms tend to become selective

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING & FINANCIAL MANAGEMENT

in the accounting procedures adopted by them which makes the process of harmonisation

difficult. Hence, an improvement in the level of compliance would result in the better adoption

of the accounting practices by the firm. As the assessment of the financial performance of the

firm becomes better with the adoption of IFRS, it is necessary that the firms are more actively

involved in the process of adoption of IFRS. In case of countries like Turkey, this will quicken

the decision-making related to foreign investment in the country (Uyar, Kılıç and Gökçen 2016).

In case of countries like Australia which are the mandatory adopters of IFRS, then has been no

significant difference in the accounting results of the firms. This is because of a similarity in the

previously existing principles guiding the accounting practices along with the current accounting

practices (Bryce, Ali and Mather 2015). This insignificance casts more doubts on the

harmonisation of accounting practices for countries yet to adopt the IFRS as a part of the

reporting guidelines. It also suggests that the quality of accounting harmonisation is not merely

dependent on the adoption of the practices. The audit committees and other aspects responsible

for the selection of accounting policies need to be more proactive in the adoption of the

accounting practices as a part of the business.

However, it needs to be kept in mind that the research conducted in the present day in

relation to the accounting harmonisation by the adoption of IFRS is incomplete and focuses on

selected aspects of the business. There is a common consensus regarding the fact that the

harmonisation of accounting process is a broader process which requires significant effort on the

part of the people preparing the financial statements. The adoption of IFRS has however been

associated with an improvement in the quality and comparability of the information provided by

the financial statements (Legenzova 2016).

ACCOUNTING & FINANCIAL MANAGEMENT

in the accounting procedures adopted by them which makes the process of harmonisation

difficult. Hence, an improvement in the level of compliance would result in the better adoption

of the accounting practices by the firm. As the assessment of the financial performance of the

firm becomes better with the adoption of IFRS, it is necessary that the firms are more actively

involved in the process of adoption of IFRS. In case of countries like Turkey, this will quicken

the decision-making related to foreign investment in the country (Uyar, Kılıç and Gökçen 2016).

In case of countries like Australia which are the mandatory adopters of IFRS, then has been no

significant difference in the accounting results of the firms. This is because of a similarity in the

previously existing principles guiding the accounting practices along with the current accounting

practices (Bryce, Ali and Mather 2015). This insignificance casts more doubts on the

harmonisation of accounting practices for countries yet to adopt the IFRS as a part of the

reporting guidelines. It also suggests that the quality of accounting harmonisation is not merely

dependent on the adoption of the practices. The audit committees and other aspects responsible

for the selection of accounting policies need to be more proactive in the adoption of the

accounting practices as a part of the business.

However, it needs to be kept in mind that the research conducted in the present day in

relation to the accounting harmonisation by the adoption of IFRS is incomplete and focuses on

selected aspects of the business. There is a common consensus regarding the fact that the

harmonisation of accounting process is a broader process which requires significant effort on the

part of the people preparing the financial statements. The adoption of IFRS has however been

associated with an improvement in the quality and comparability of the information provided by

the financial statements (Legenzova 2016).

5

ACCOUNTING & FINANCIAL MANAGEMENT

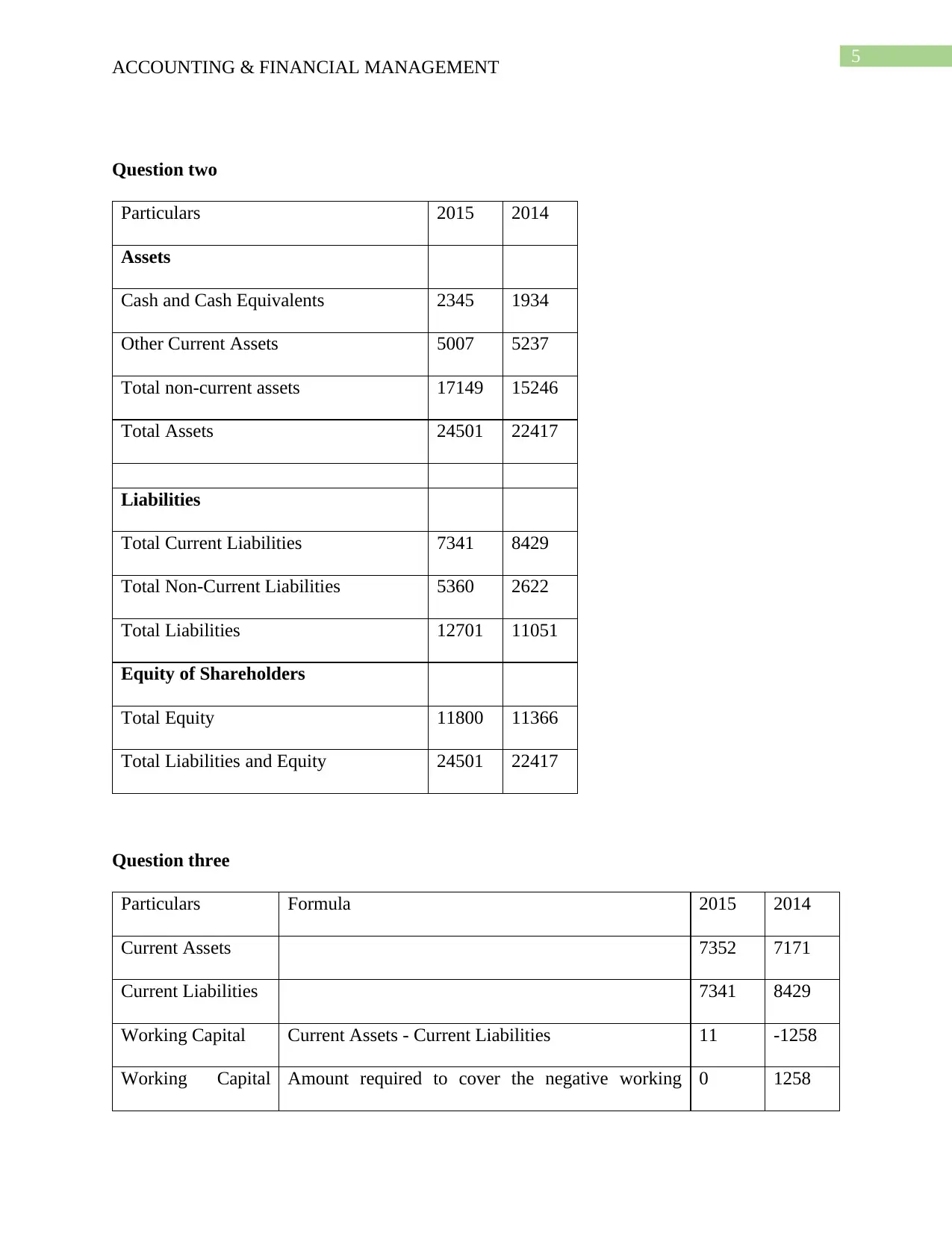

Question two

Particulars 2015 2014

Assets

Cash and Cash Equivalents 2345 1934

Other Current Assets 5007 5237

Total non-current assets 17149 15246

Total Assets 24501 22417

Liabilities

Total Current Liabilities 7341 8429

Total Non-Current Liabilities 5360 2622

Total Liabilities 12701 11051

Equity of Shareholders

Total Equity 11800 11366

Total Liabilities and Equity 24501 22417

Question three

Particulars Formula 2015 2014

Current Assets 7352 7171

Current Liabilities 7341 8429

Working Capital Current Assets - Current Liabilities 11 -1258

Working Capital Amount required to cover the negative working 0 1258

ACCOUNTING & FINANCIAL MANAGEMENT

Question two

Particulars 2015 2014

Assets

Cash and Cash Equivalents 2345 1934

Other Current Assets 5007 5237

Total non-current assets 17149 15246

Total Assets 24501 22417

Liabilities

Total Current Liabilities 7341 8429

Total Non-Current Liabilities 5360 2622

Total Liabilities 12701 11051

Equity of Shareholders

Total Equity 11800 11366

Total Liabilities and Equity 24501 22417

Question three

Particulars Formula 2015 2014

Current Assets 7352 7171

Current Liabilities 7341 8429

Working Capital Current Assets - Current Liabilities 11 -1258

Working Capital Amount required to cover the negative working 0 1258

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING & FINANCIAL MANAGEMENT

need capital

Net Cash Cash - Total Liabilities -10356 -9117

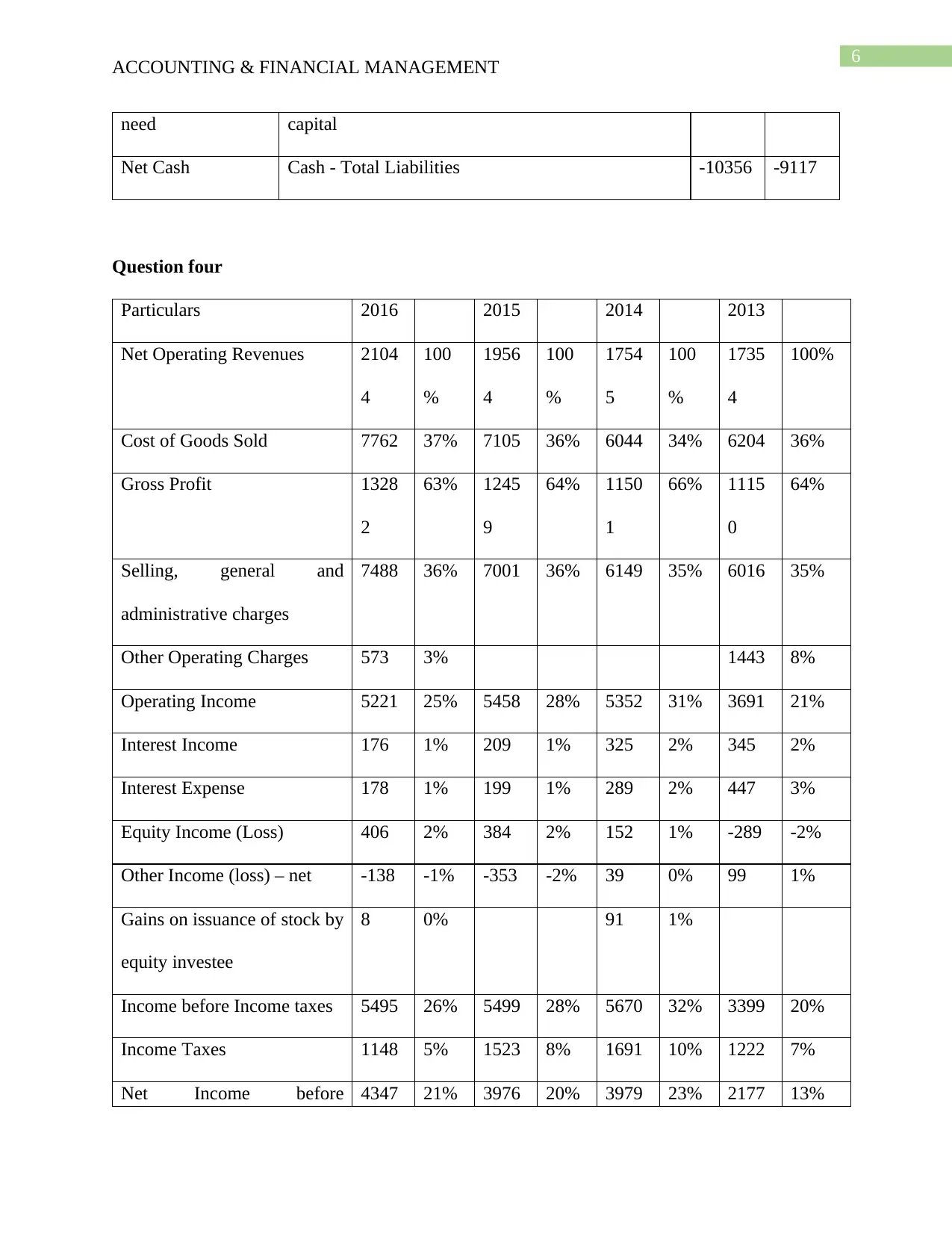

Question four

Particulars 2016 2015 2014 2013

Net Operating Revenues 2104

4

100

%

1956

4

100

%

1754

5

100

%

1735

4

100%

Cost of Goods Sold 7762 37% 7105 36% 6044 34% 6204 36%

Gross Profit 1328

2

63% 1245

9

64% 1150

1

66% 1115

0

64%

Selling, general and

administrative charges

7488 36% 7001 36% 6149 35% 6016 35%

Other Operating Charges 573 3% 1443 8%

Operating Income 5221 25% 5458 28% 5352 31% 3691 21%

Interest Income 176 1% 209 1% 325 2% 345 2%

Interest Expense 178 1% 199 1% 289 2% 447 3%

Equity Income (Loss) 406 2% 384 2% 152 1% -289 -2%

Other Income (loss) – net -138 -1% -353 -2% 39 0% 99 1%

Gains on issuance of stock by

equity investee

8 0% 91 1%

Income before Income taxes 5495 26% 5499 28% 5670 32% 3399 20%

Income Taxes 1148 5% 1523 8% 1691 10% 1222 7%

Net Income before 4347 21% 3976 20% 3979 23% 2177 13%

ACCOUNTING & FINANCIAL MANAGEMENT

need capital

Net Cash Cash - Total Liabilities -10356 -9117

Question four

Particulars 2016 2015 2014 2013

Net Operating Revenues 2104

4

100

%

1956

4

100

%

1754

5

100

%

1735

4

100%

Cost of Goods Sold 7762 37% 7105 36% 6044 34% 6204 36%

Gross Profit 1328

2

63% 1245

9

64% 1150

1

66% 1115

0

64%

Selling, general and

administrative charges

7488 36% 7001 36% 6149 35% 6016 35%

Other Operating Charges 573 3% 1443 8%

Operating Income 5221 25% 5458 28% 5352 31% 3691 21%

Interest Income 176 1% 209 1% 325 2% 345 2%

Interest Expense 178 1% 199 1% 289 2% 447 3%

Equity Income (Loss) 406 2% 384 2% 152 1% -289 -2%

Other Income (loss) – net -138 -1% -353 -2% 39 0% 99 1%

Gains on issuance of stock by

equity investee

8 0% 91 1%

Income before Income taxes 5495 26% 5499 28% 5670 32% 3399 20%

Income Taxes 1148 5% 1523 8% 1691 10% 1222 7%

Net Income before 4347 21% 3976 20% 3979 23% 2177 13%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING & FINANCIAL MANAGEMENT

cumulative effect of

accounting change

Cumulative effect of

accounting change

Company Operations -367 -2%

Equity Investees -559 -3%

Cumulative effect of

accounting change

0% -10 0%

Net Income 4347 21% 3050 16% 3969 23% 2177 13%

Question five

The operating income of the business has been fluctuating due to the changes occurring

in the additional operating charges incurred by the business. This suggests that the entity has not

been able to maintain consistency in the management of the operating overheads. This needs to

become more efficient. As operating income is a measure of the efficiency of the core businesses

of the entity, it is necessary to maintain a high margin of the same. As the interest expense and

tax rates to a business are variable and tend to change on the basis of the nature of the business,

operating income is a more reliable measure of the business efficiency (Ehrhardt and Brigham

2016). There is a need to keep the additional operating charges under control. The net income

generated by the business has however been positive over the years. This suggests that the

business is efficient in its core operations with some improvement required in the additional

expenditure incurred by the business. As these expenditures like the additional operating

ACCOUNTING & FINANCIAL MANAGEMENT

cumulative effect of

accounting change

Cumulative effect of

accounting change

Company Operations -367 -2%

Equity Investees -559 -3%

Cumulative effect of

accounting change

0% -10 0%

Net Income 4347 21% 3050 16% 3969 23% 2177 13%

Question five

The operating income of the business has been fluctuating due to the changes occurring

in the additional operating charges incurred by the business. This suggests that the entity has not

been able to maintain consistency in the management of the operating overheads. This needs to

become more efficient. As operating income is a measure of the efficiency of the core businesses

of the entity, it is necessary to maintain a high margin of the same. As the interest expense and

tax rates to a business are variable and tend to change on the basis of the nature of the business,

operating income is a more reliable measure of the business efficiency (Ehrhardt and Brigham

2016). There is a need to keep the additional operating charges under control. The net income

generated by the business has however been positive over the years. This suggests that the

business is efficient in its core operations with some improvement required in the additional

expenditure incurred by the business. As these expenditures like the additional operating

8

ACCOUNTING & FINANCIAL MANAGEMENT

expenditure and loss from equity investees are more occasional, it can be said that the

performance of the business has been consistent.

The main concern when analysing the Balance Sheet of the business is the increase in the

debt of the company by more than 100%. However, the equity of the business has remained the

same. This suggests that the entity has been depending on the availability of debt funds to fund

its growth. While there is a significant increase in the performance of the company, it also

increases the pressure on the business to pay the debt obligations in a timely manner. Otherwise,

the business faces the risk of bankruptcy. The amount of assets contained by the business like the

Machinery and Equipment indicates that the business has been using the debt funds to purchase

the required assets (Yazdanfar and Öhman 2015). There is also a reduction of the short term debt

along with an increase in the cash balances of the company. The advantage of using the long

term debt as a part of the business is that the interest payments made by the business are tax

deductible. They also allow the company more time to pay the debt. An overview of the

performance of the business suggests that it has been able to maintain a consistent level of

performance in the short run with an increased focus on improving its stability in the long run.

These are indicators of good performance by the business (Badoer and James 2016).

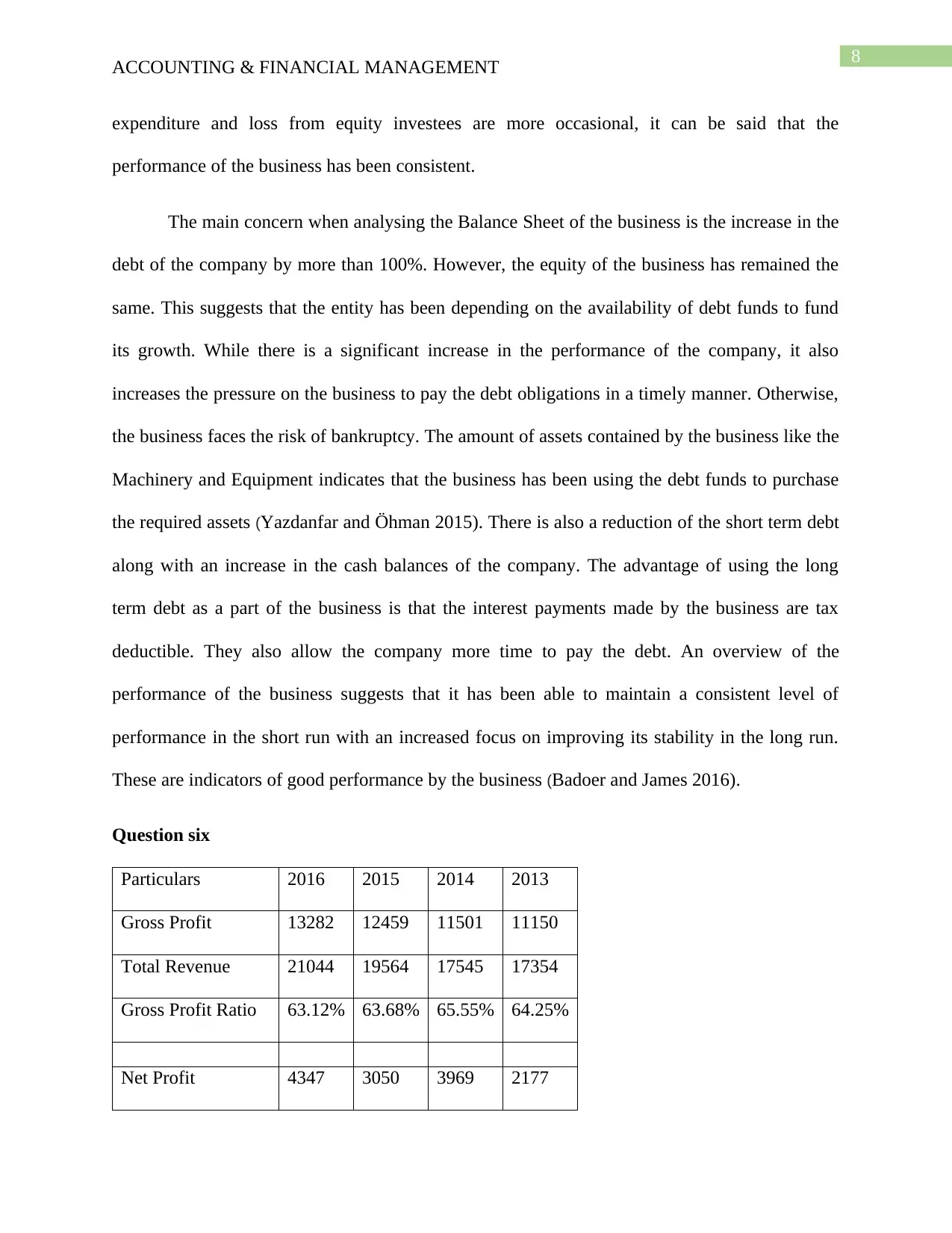

Question six

Particulars 2016 2015 2014 2013

Gross Profit 13282 12459 11501 11150

Total Revenue 21044 19564 17545 17354

Gross Profit Ratio 63.12% 63.68% 65.55% 64.25%

Net Profit 4347 3050 3969 2177

ACCOUNTING & FINANCIAL MANAGEMENT

expenditure and loss from equity investees are more occasional, it can be said that the

performance of the business has been consistent.

The main concern when analysing the Balance Sheet of the business is the increase in the

debt of the company by more than 100%. However, the equity of the business has remained the

same. This suggests that the entity has been depending on the availability of debt funds to fund

its growth. While there is a significant increase in the performance of the company, it also

increases the pressure on the business to pay the debt obligations in a timely manner. Otherwise,

the business faces the risk of bankruptcy. The amount of assets contained by the business like the

Machinery and Equipment indicates that the business has been using the debt funds to purchase

the required assets (Yazdanfar and Öhman 2015). There is also a reduction of the short term debt

along with an increase in the cash balances of the company. The advantage of using the long

term debt as a part of the business is that the interest payments made by the business are tax

deductible. They also allow the company more time to pay the debt. An overview of the

performance of the business suggests that it has been able to maintain a consistent level of

performance in the short run with an increased focus on improving its stability in the long run.

These are indicators of good performance by the business (Badoer and James 2016).

Question six

Particulars 2016 2015 2014 2013

Gross Profit 13282 12459 11501 11150

Total Revenue 21044 19564 17545 17354

Gross Profit Ratio 63.12% 63.68% 65.55% 64.25%

Net Profit 4347 3050 3969 2177

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

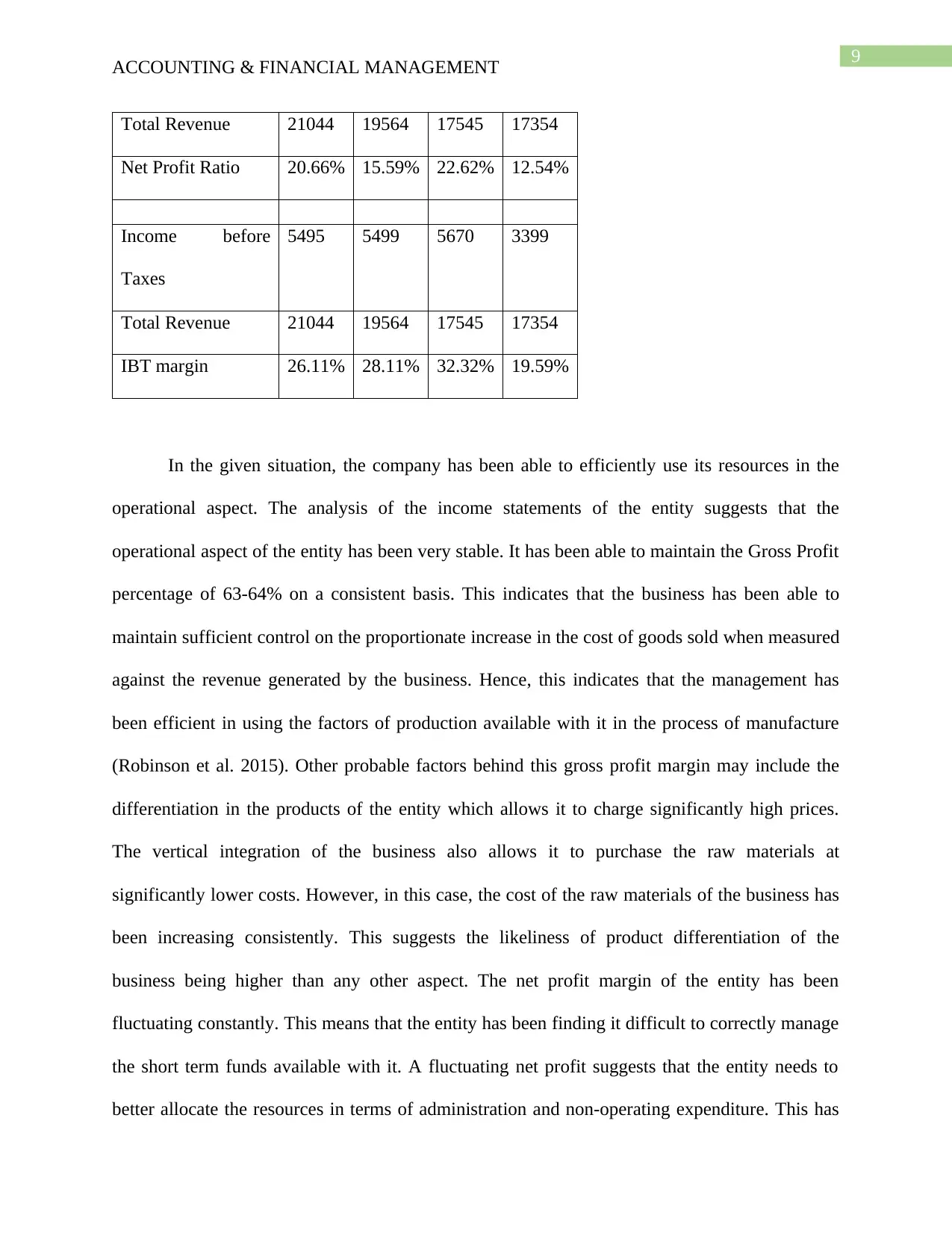

ACCOUNTING & FINANCIAL MANAGEMENT

Total Revenue 21044 19564 17545 17354

Net Profit Ratio 20.66% 15.59% 22.62% 12.54%

Income before

Taxes

5495 5499 5670 3399

Total Revenue 21044 19564 17545 17354

IBT margin 26.11% 28.11% 32.32% 19.59%

In the given situation, the company has been able to efficiently use its resources in the

operational aspect. The analysis of the income statements of the entity suggests that the

operational aspect of the entity has been very stable. It has been able to maintain the Gross Profit

percentage of 63-64% on a consistent basis. This indicates that the business has been able to

maintain sufficient control on the proportionate increase in the cost of goods sold when measured

against the revenue generated by the business. Hence, this indicates that the management has

been efficient in using the factors of production available with it in the process of manufacture

(Robinson et al. 2015). Other probable factors behind this gross profit margin may include the

differentiation in the products of the entity which allows it to charge significantly high prices.

The vertical integration of the business also allows it to purchase the raw materials at

significantly lower costs. However, in this case, the cost of the raw materials of the business has

been increasing consistently. This suggests the likeliness of product differentiation of the

business being higher than any other aspect. The net profit margin of the entity has been

fluctuating constantly. This means that the entity has been finding it difficult to correctly manage

the short term funds available with it. A fluctuating net profit suggests that the entity needs to

better allocate the resources in terms of administration and non-operating expenditure. This has

ACCOUNTING & FINANCIAL MANAGEMENT

Total Revenue 21044 19564 17545 17354

Net Profit Ratio 20.66% 15.59% 22.62% 12.54%

Income before

Taxes

5495 5499 5670 3399

Total Revenue 21044 19564 17545 17354

IBT margin 26.11% 28.11% 32.32% 19.59%

In the given situation, the company has been able to efficiently use its resources in the

operational aspect. The analysis of the income statements of the entity suggests that the

operational aspect of the entity has been very stable. It has been able to maintain the Gross Profit

percentage of 63-64% on a consistent basis. This indicates that the business has been able to

maintain sufficient control on the proportionate increase in the cost of goods sold when measured

against the revenue generated by the business. Hence, this indicates that the management has

been efficient in using the factors of production available with it in the process of manufacture

(Robinson et al. 2015). Other probable factors behind this gross profit margin may include the

differentiation in the products of the entity which allows it to charge significantly high prices.

The vertical integration of the business also allows it to purchase the raw materials at

significantly lower costs. However, in this case, the cost of the raw materials of the business has

been increasing consistently. This suggests the likeliness of product differentiation of the

business being higher than any other aspect. The net profit margin of the entity has been

fluctuating constantly. This means that the entity has been finding it difficult to correctly manage

the short term funds available with it. A fluctuating net profit suggests that the entity needs to

better allocate the resources in terms of administration and non-operating expenditure. This has

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING & FINANCIAL MANAGEMENT

been extremely inconsistent and fluctuating wildly. The lower net profit returns also suggests

that the business will not have sufficient resources to distribute amongst the shareholders of the

business. Hence, there is a need to focus on this aspect and reduce the additional non-operating

expenditure incurred by the business. The benefits in relation to this will be faced by the business

in the long run. The other aspect of profitability which has been analysed in relation to the

business is the profits before the income taxes paid by the entity. Income taxes are not under the

control of the business and may vary on the basis of the nature of the industry in which the

business is operating. Hence, in order to understand the operating and administration efficiency

of the firm, it is necessary to determine the IBT margin of the entity. In case of the business, the

IBT has also been declining in comparison to the past year. This suggests that the business needs

to increase the focus on its operations. While net profit may be dependent on the income taxes

paid by the entity, the IBT is a fair representation of the financial performance and the operating

decisions of the entity. Hence, the long term debt funds implemented by the business should be

put to better use to ensure the benefit of the firm.

Part B

Question One

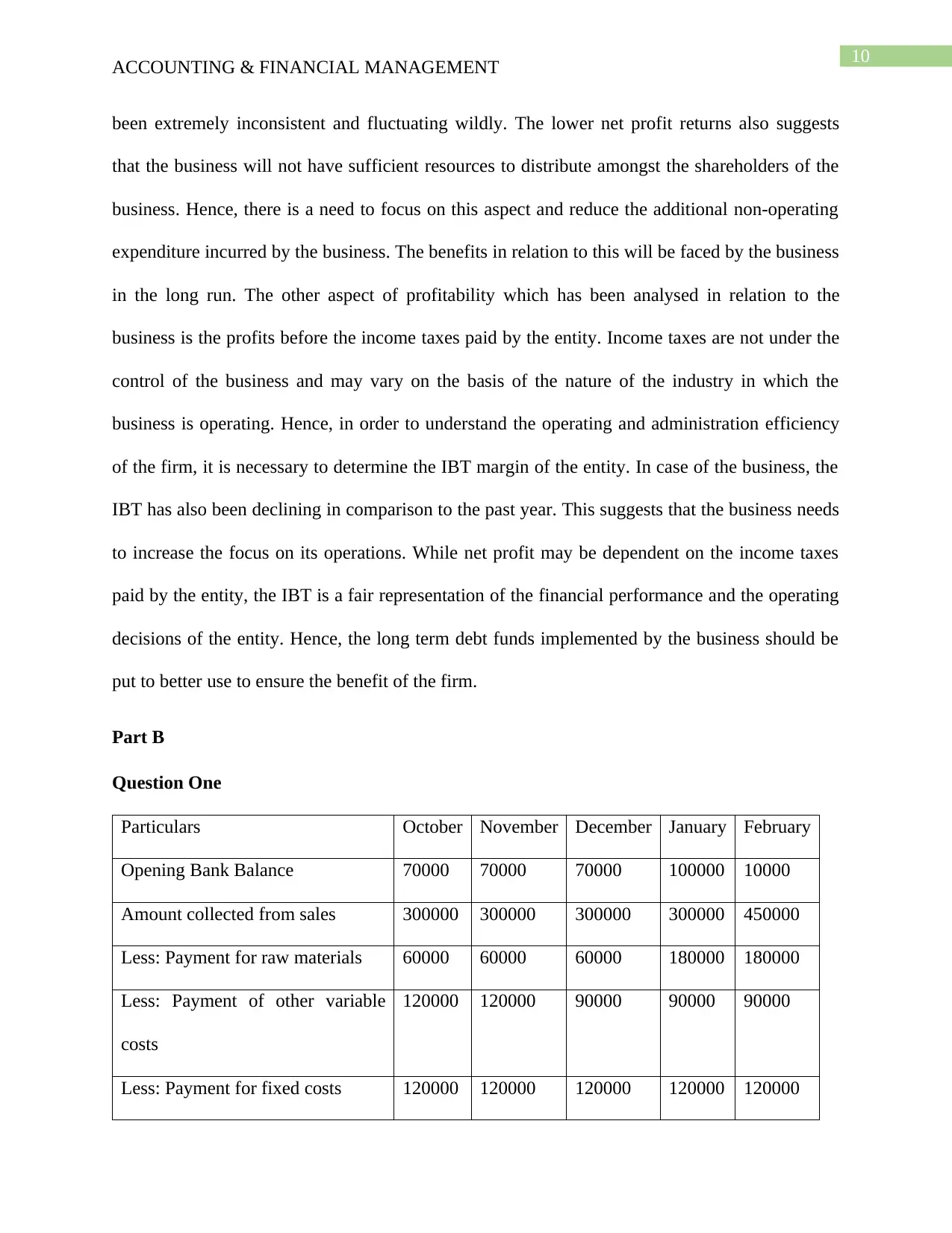

Particulars October November December January February

Opening Bank Balance 70000 70000 70000 100000 10000

Amount collected from sales 300000 300000 300000 300000 450000

Less: Payment for raw materials 60000 60000 60000 180000 180000

Less: Payment of other variable

costs

120000 120000 90000 90000 90000

Less: Payment for fixed costs 120000 120000 120000 120000 120000

ACCOUNTING & FINANCIAL MANAGEMENT

been extremely inconsistent and fluctuating wildly. The lower net profit returns also suggests

that the business will not have sufficient resources to distribute amongst the shareholders of the

business. Hence, there is a need to focus on this aspect and reduce the additional non-operating

expenditure incurred by the business. The benefits in relation to this will be faced by the business

in the long run. The other aspect of profitability which has been analysed in relation to the

business is the profits before the income taxes paid by the entity. Income taxes are not under the

control of the business and may vary on the basis of the nature of the industry in which the

business is operating. Hence, in order to understand the operating and administration efficiency

of the firm, it is necessary to determine the IBT margin of the entity. In case of the business, the

IBT has also been declining in comparison to the past year. This suggests that the business needs

to increase the focus on its operations. While net profit may be dependent on the income taxes

paid by the entity, the IBT is a fair representation of the financial performance and the operating

decisions of the entity. Hence, the long term debt funds implemented by the business should be

put to better use to ensure the benefit of the firm.

Part B

Question One

Particulars October November December January February

Opening Bank Balance 70000 70000 70000 100000 10000

Amount collected from sales 300000 300000 300000 300000 450000

Less: Payment for raw materials 60000 60000 60000 180000 180000

Less: Payment of other variable

costs

120000 120000 90000 90000 90000

Less: Payment for fixed costs 120000 120000 120000 120000 120000

11

ACCOUNTING & FINANCIAL MANAGEMENT

Net cash flow during the month 70000 70000 100000 10000 70000

In the above situation, the cash flow is prepared on the basis of the assumption that the

proposed sales plan of the business goes ahead. However, the statement being prepared in the

current situation is the cash budget which is concerned with the collections made by the business

from the sales made by it and not other aspects. Hence, the amount collected from the sales up to

the month of December remains the same in till the month of December. However, since

December, there is a decrease in the variable costs incurred by the entity. This results in the

increase in the net cash available with the firm at the end of the month. Due to this particular

reason, there is a change in the overall cash flow of the entity from the month of January. There

is a significant improvement in the amount of sales generated by the entity from the process of

increased collection of funds by the business. However, these benefits do not remain for a long

period of time and are offset by the increase in the variable costs incurred by the entity for the

month of January and February. The impact of these changes is severely felt in the month of

January when the cash flows generated by the business are extremely low at $10000. However,

the business again recovers from this situation and the overall cash flows generated by the

business increase in February. On an overall basis, it can be suggested that the adoption of a new

sales model does not essentially result in a drastic changes in the cash flows generated by the

entities. Hence, unless the business has sufficient capabilities to reduce the costs incurred by it,

there is no suggestion that the new sales policy results in an improvement in the sales generated

by the entity.

ACCOUNTING & FINANCIAL MANAGEMENT

Net cash flow during the month 70000 70000 100000 10000 70000

In the above situation, the cash flow is prepared on the basis of the assumption that the

proposed sales plan of the business goes ahead. However, the statement being prepared in the

current situation is the cash budget which is concerned with the collections made by the business

from the sales made by it and not other aspects. Hence, the amount collected from the sales up to

the month of December remains the same in till the month of December. However, since

December, there is a decrease in the variable costs incurred by the entity. This results in the

increase in the net cash available with the firm at the end of the month. Due to this particular

reason, there is a change in the overall cash flow of the entity from the month of January. There

is a significant improvement in the amount of sales generated by the entity from the process of

increased collection of funds by the business. However, these benefits do not remain for a long

period of time and are offset by the increase in the variable costs incurred by the entity for the

month of January and February. The impact of these changes is severely felt in the month of

January when the cash flows generated by the business are extremely low at $10000. However,

the business again recovers from this situation and the overall cash flows generated by the

business increase in February. On an overall basis, it can be suggested that the adoption of a new

sales model does not essentially result in a drastic changes in the cash flows generated by the

entities. Hence, unless the business has sufficient capabilities to reduce the costs incurred by it,

there is no suggestion that the new sales policy results in an improvement in the sales generated

by the entity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.