Accounting for Business: Financial Performance Comparison Report

VerifiedAdded on 2020/05/16

|10

|1571

|52

Report

AI Summary

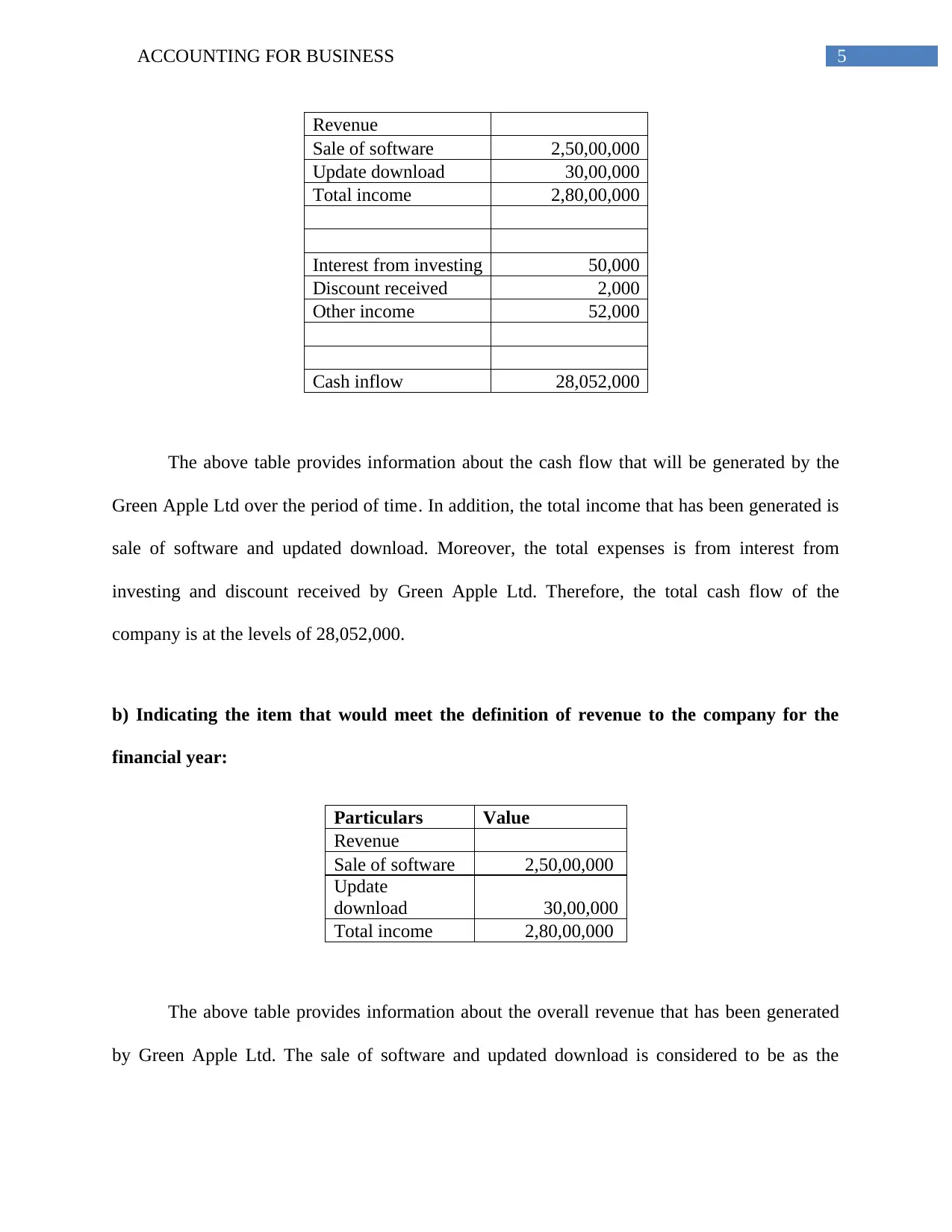

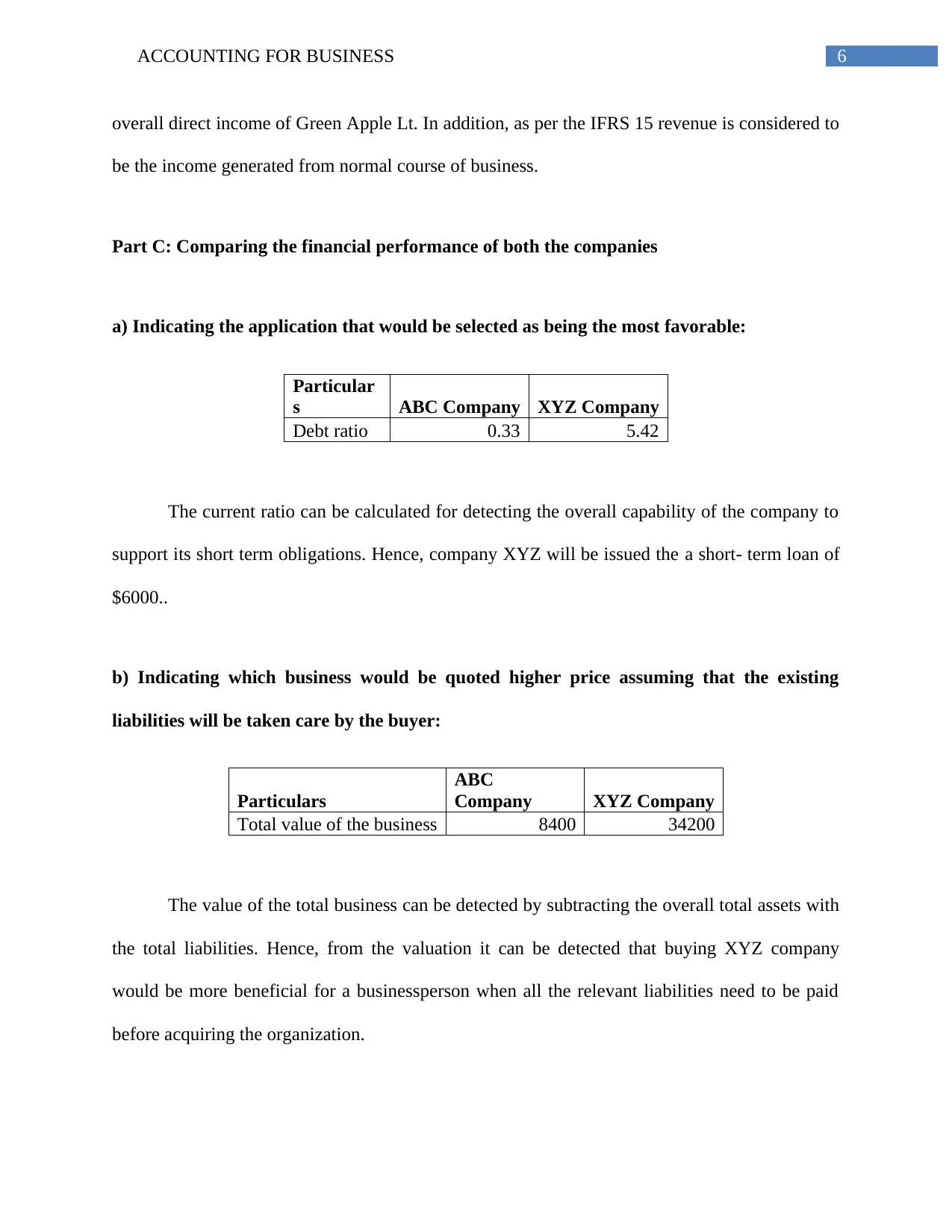

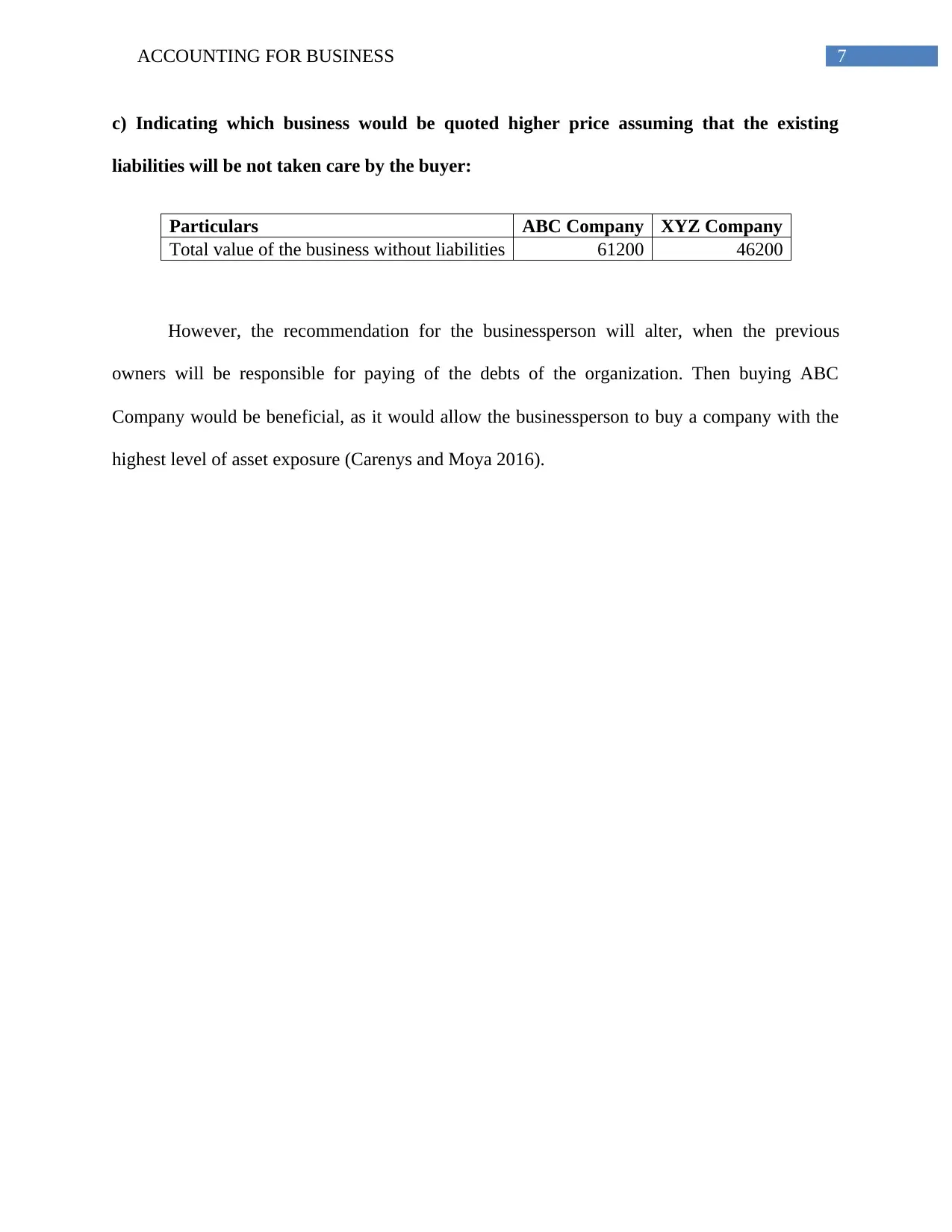

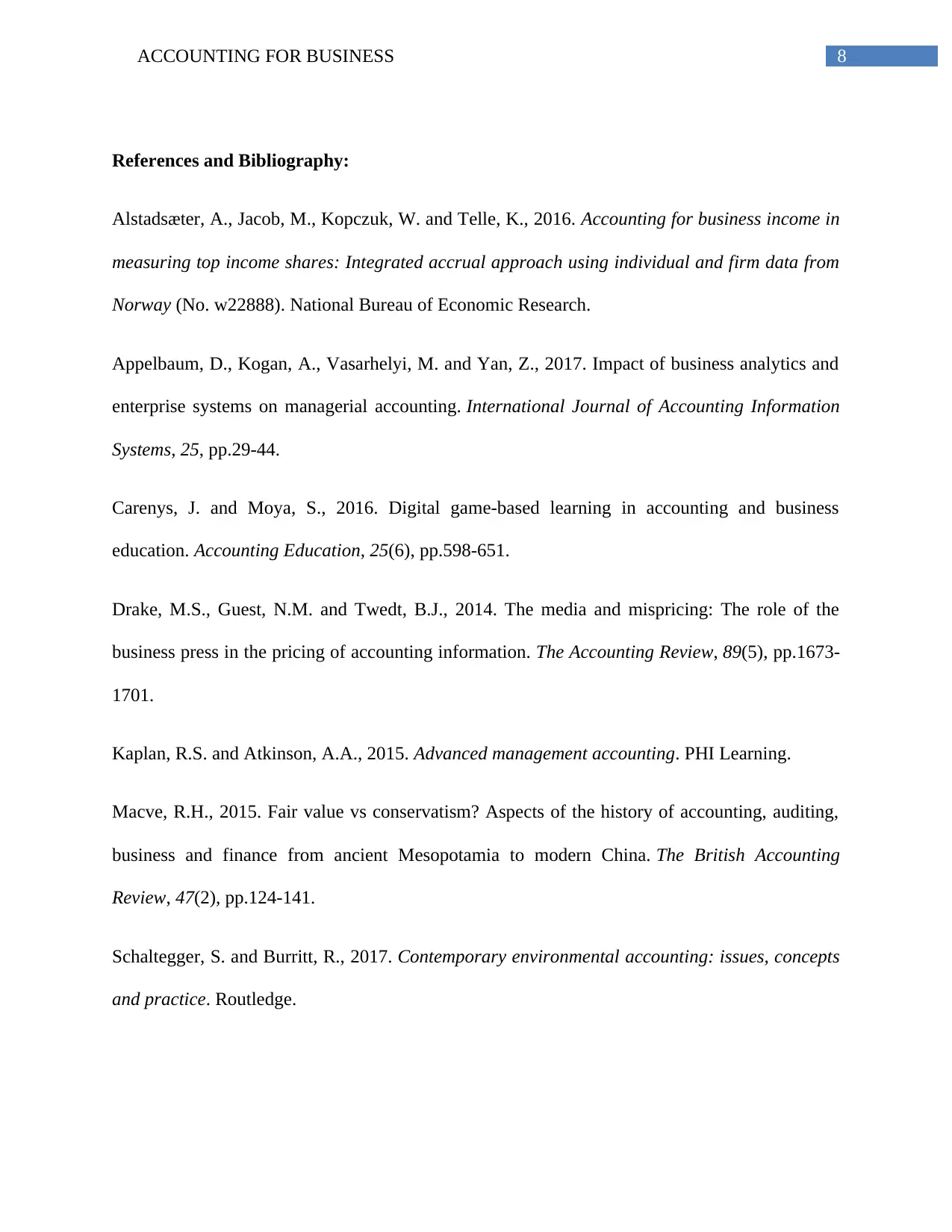

This accounting report provides a comprehensive financial analysis of two companies, Big Bang Pty Ltd and Green Apple Ltd. It begins by calculating and explaining key financial ratios such as current ratio, quick ratio, accounts receivable turnover ratio, and inventory turnover ratio for Big Bang Pty Ltd, assessing its short-term solvency and operational efficiency. The report then examines the definition of income and revenue for Green Apple Ltd, detailing its cash flow and identifying items that meet the criteria for revenue. Finally, the report compares the financial performance of both companies, determining which business would be more favorable for different investment scenarios, considering debt ratios, total business value with and without liabilities, and providing insights into which company would be quoted at a higher price under varying conditions. The report references several academic sources to support its analysis.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.