Accounting Fundamentals: Financial Reporting for Maxim, Pendo, Mafuta

VerifiedAdded on 2021/01/01

|22

|4827

|473

Homework Assignment

AI Summary

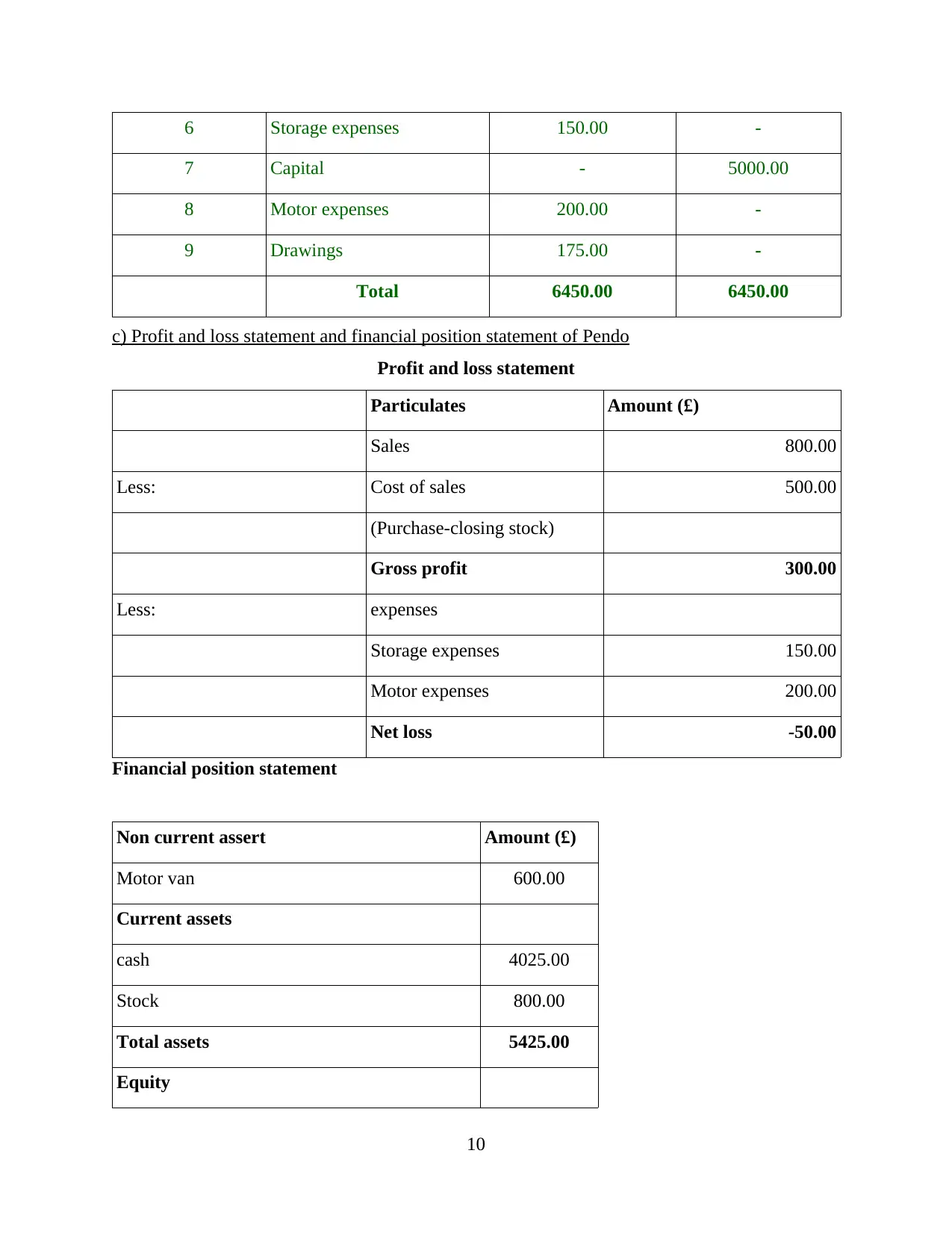

This assignment delves into the core principles of accounting through the analysis of three businesses: Maxim, Pendo, and Mafuta. It begins with journal entries and ledger postings for each company, meticulously recording financial transactions. The assignment then progresses to the creation of trial balances, ensuring the accuracy of the recorded data. Following the trial balances, profit and loss statements and financial position statements are prepared for each business, providing a comprehensive view of their financial performance and position. The tasks cover various transactions, including capital contributions, purchases, sales, loan activities, and expense management, demonstrating a practical application of accounting concepts. The report also touches upon the difference between capital and revenue expenditures, reinforcing fundamental accounting knowledge. This assignment serves as a valuable resource for understanding financial reporting and analysis.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.