Accounting Principles and Financial Reporting Assignment

VerifiedAdded on 2021/05/31

|23

|1676

|46

Homework Assignment

AI Summary

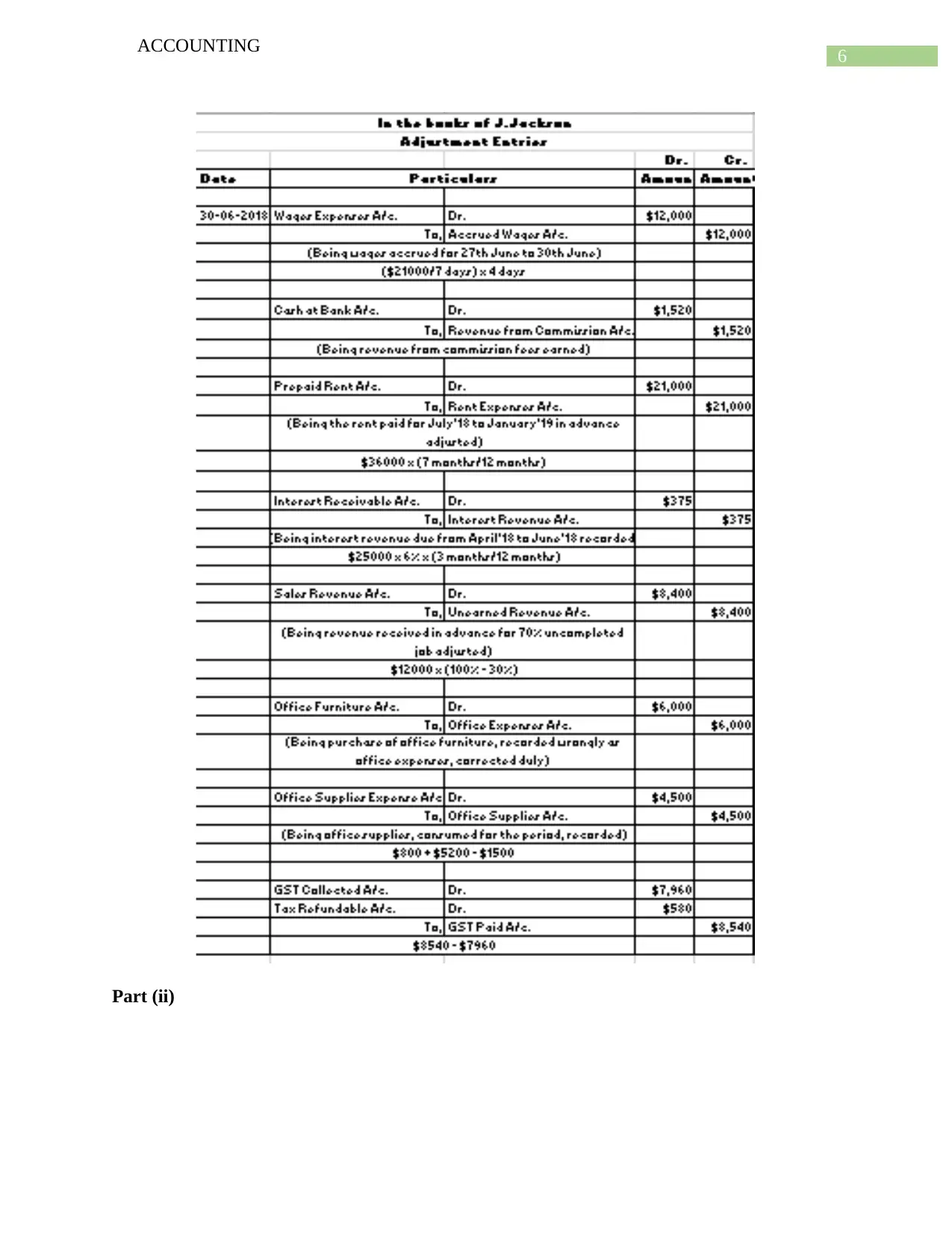

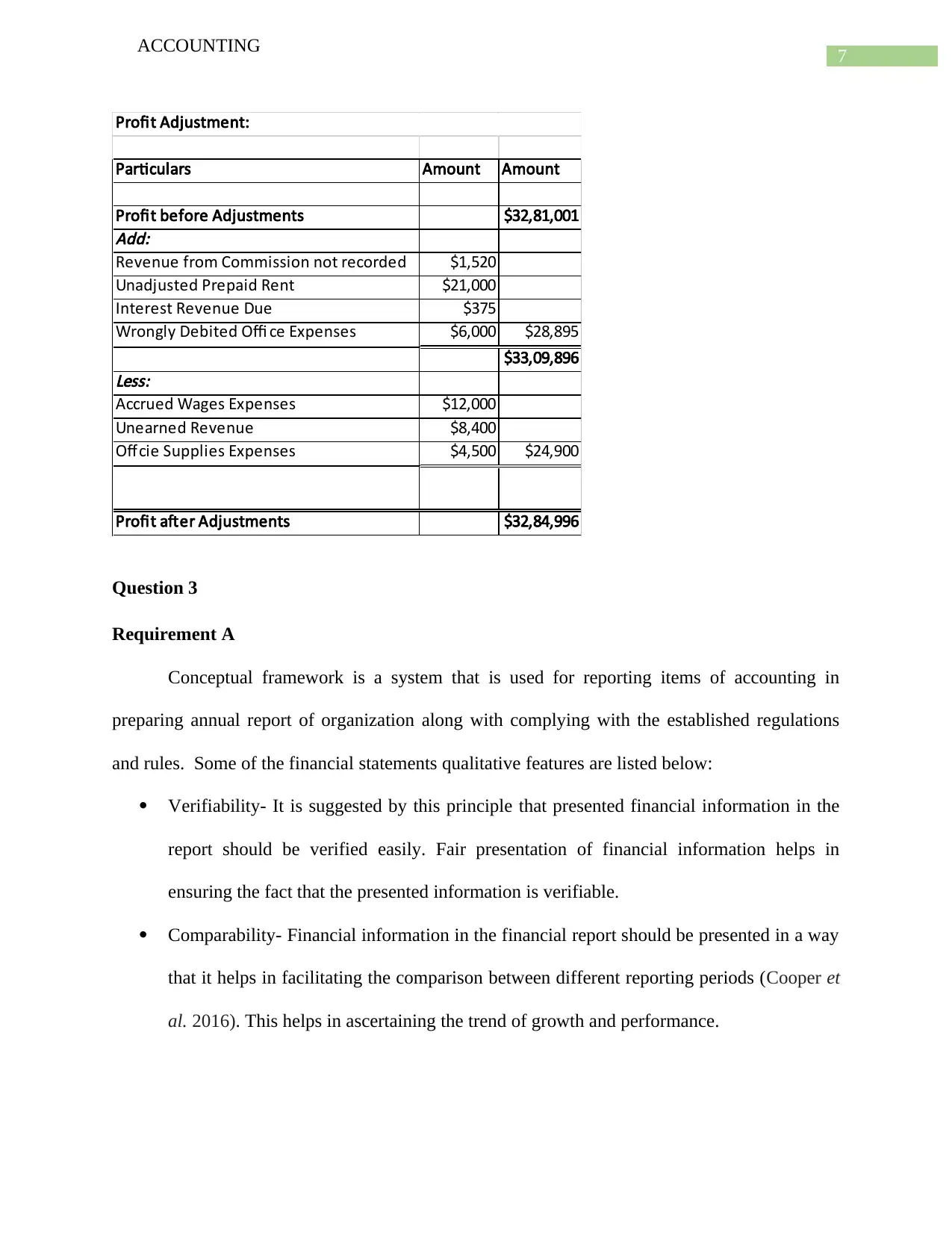

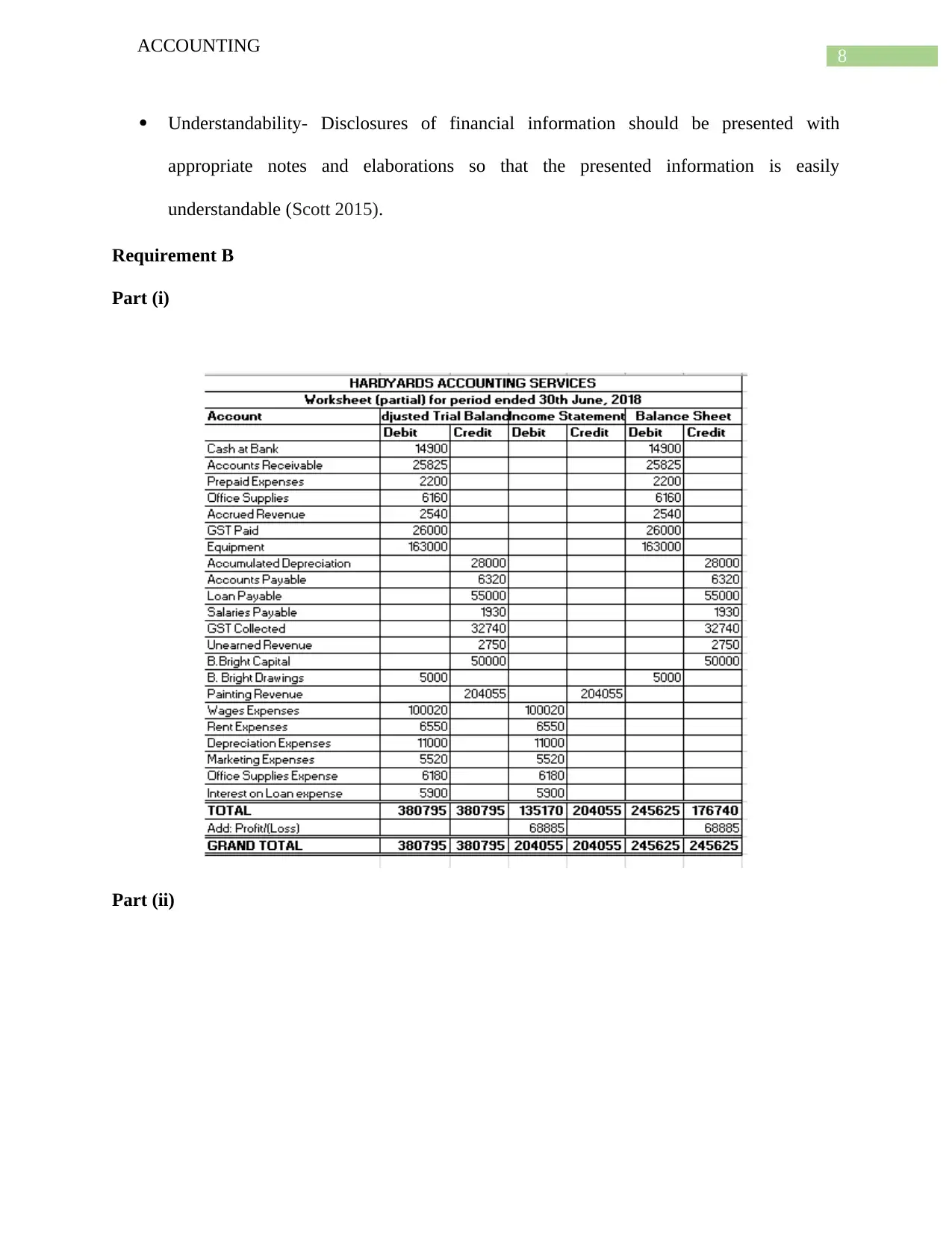

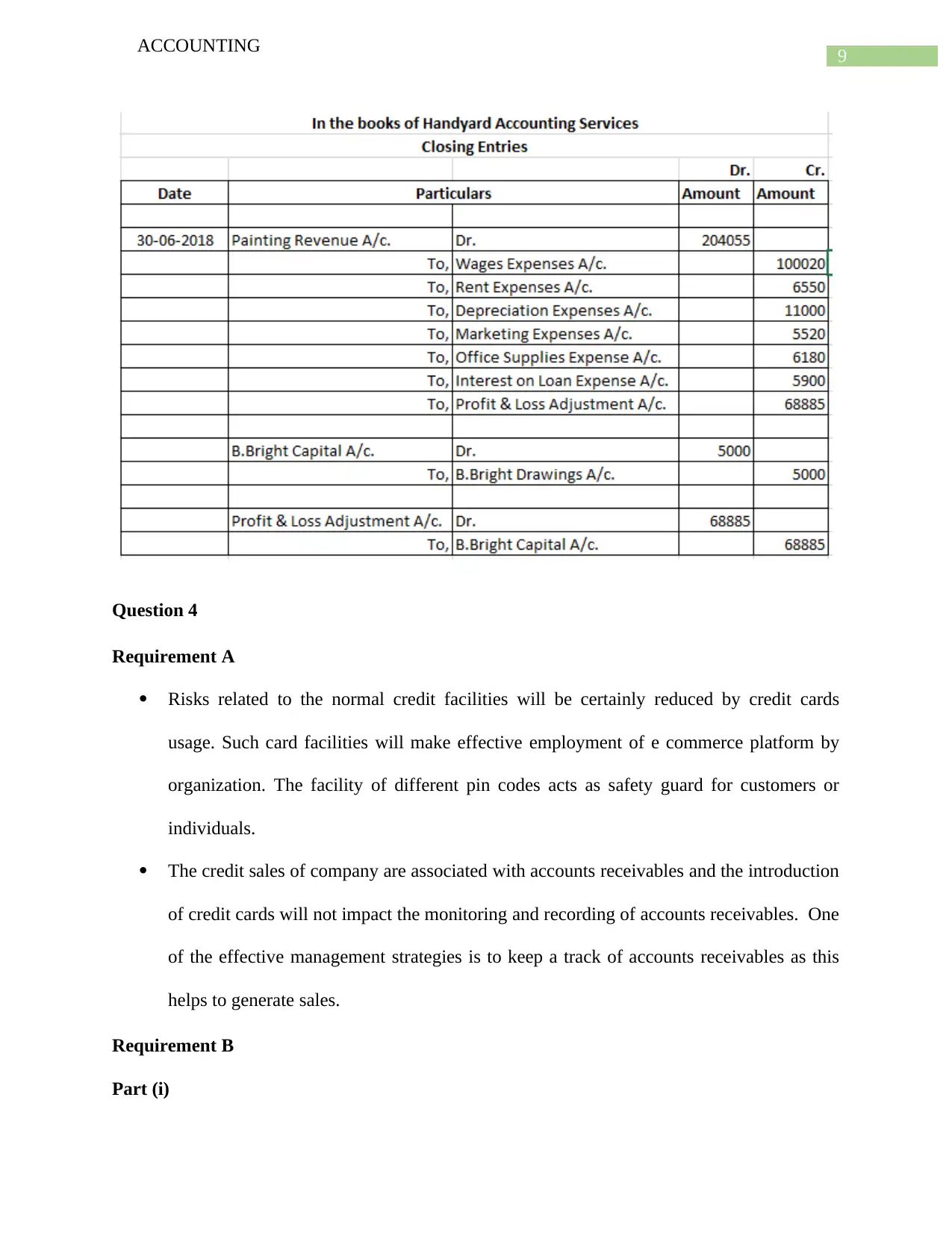

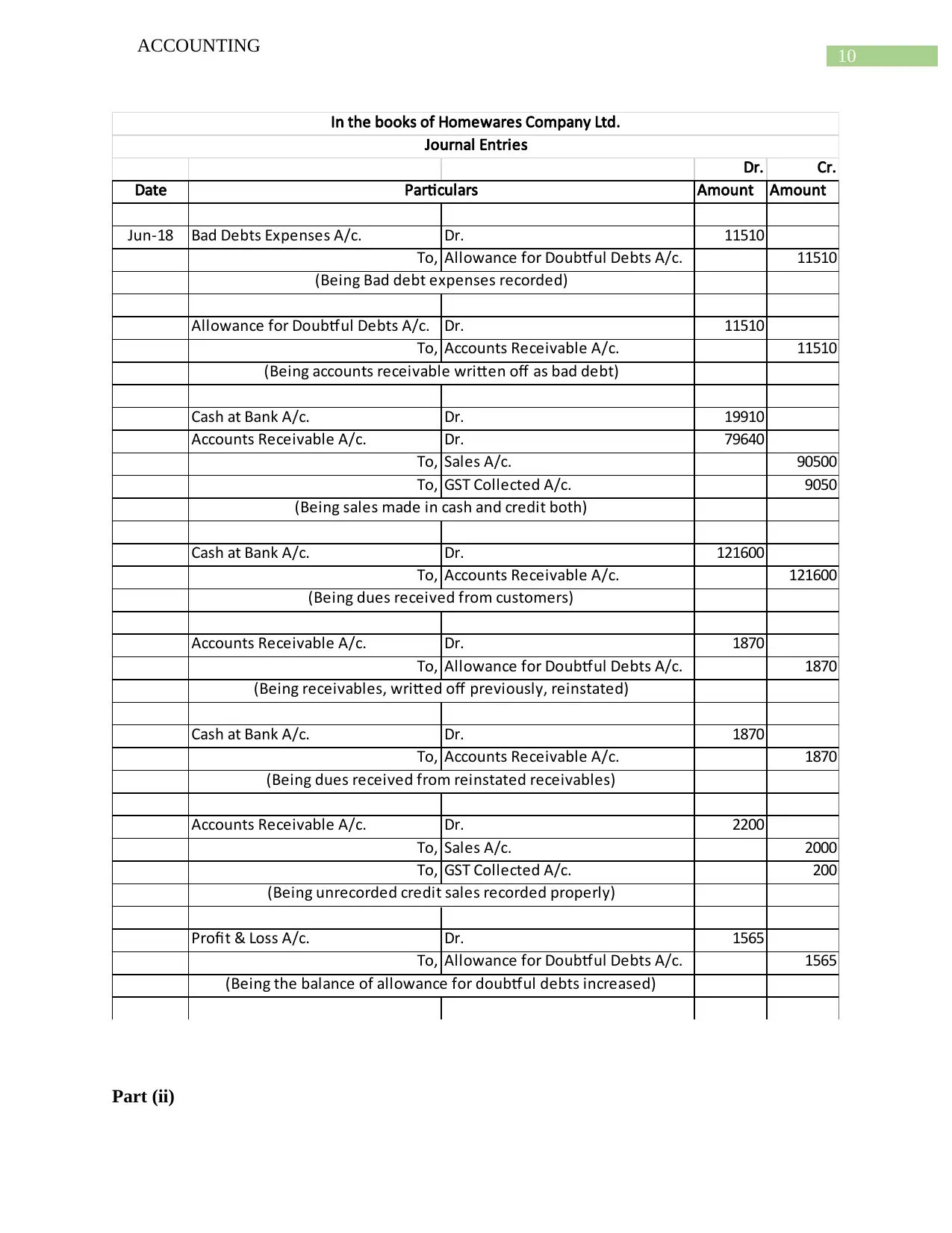

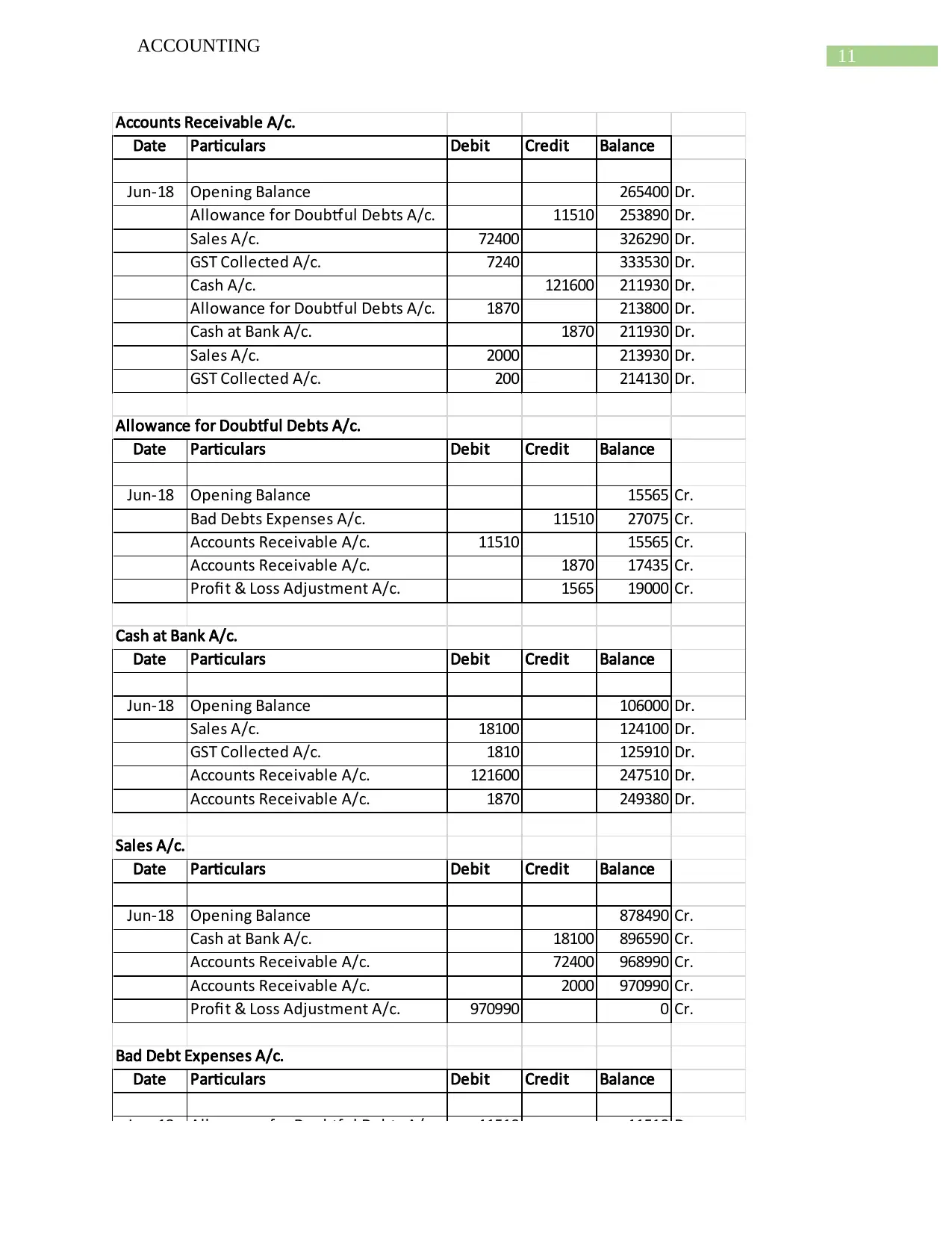

This accounting assignment solution covers various key concepts in financial accounting. It begins with an explanation of the trial balance, its purpose, and limitations. The solution then delves into accrual accounting, contrasting it with the cash basis and emphasizing the matching concept. The assignment further explores the conceptual framework of accounting, highlighting qualitative characteristics such as verifiability, comparability, and understandability. It also discusses the impact of credit cards on financial management, particularly concerning accounts receivable. Depreciation methods, including the straight-line and diminishing value methods, are analyzed, along with asset revaluation. The solution provides detailed journal entries and explores inventory valuation methods, including perpetual systems and the lower of cost or net realizable value principle. Finally, the assignment touches upon revenue recognition and the importance of sustainability reporting.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.