University Accounting Assignment: Inventory, Receivables, and Reports

VerifiedAdded on 2020/10/04

|37

|4061

|53

Homework Assignment

AI Summary

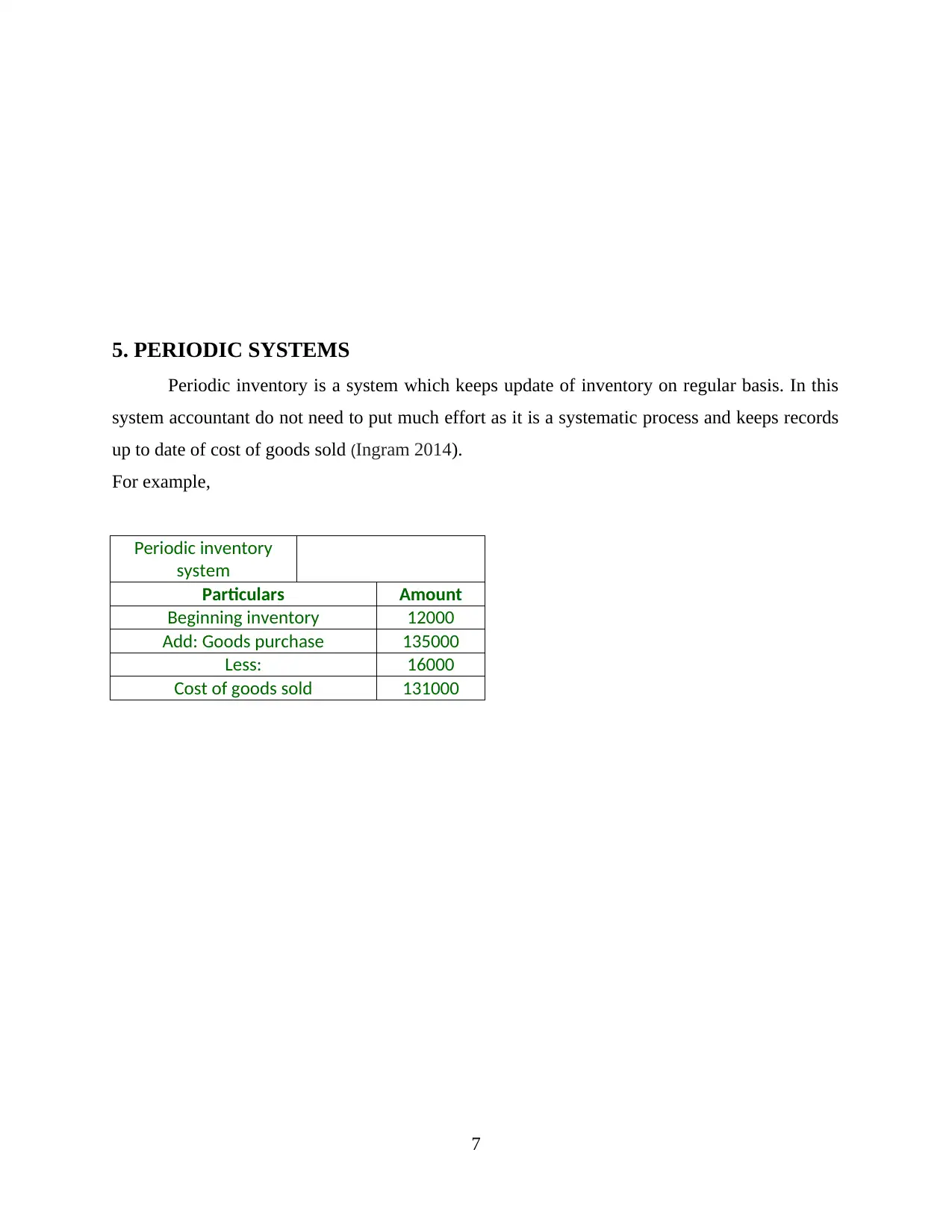

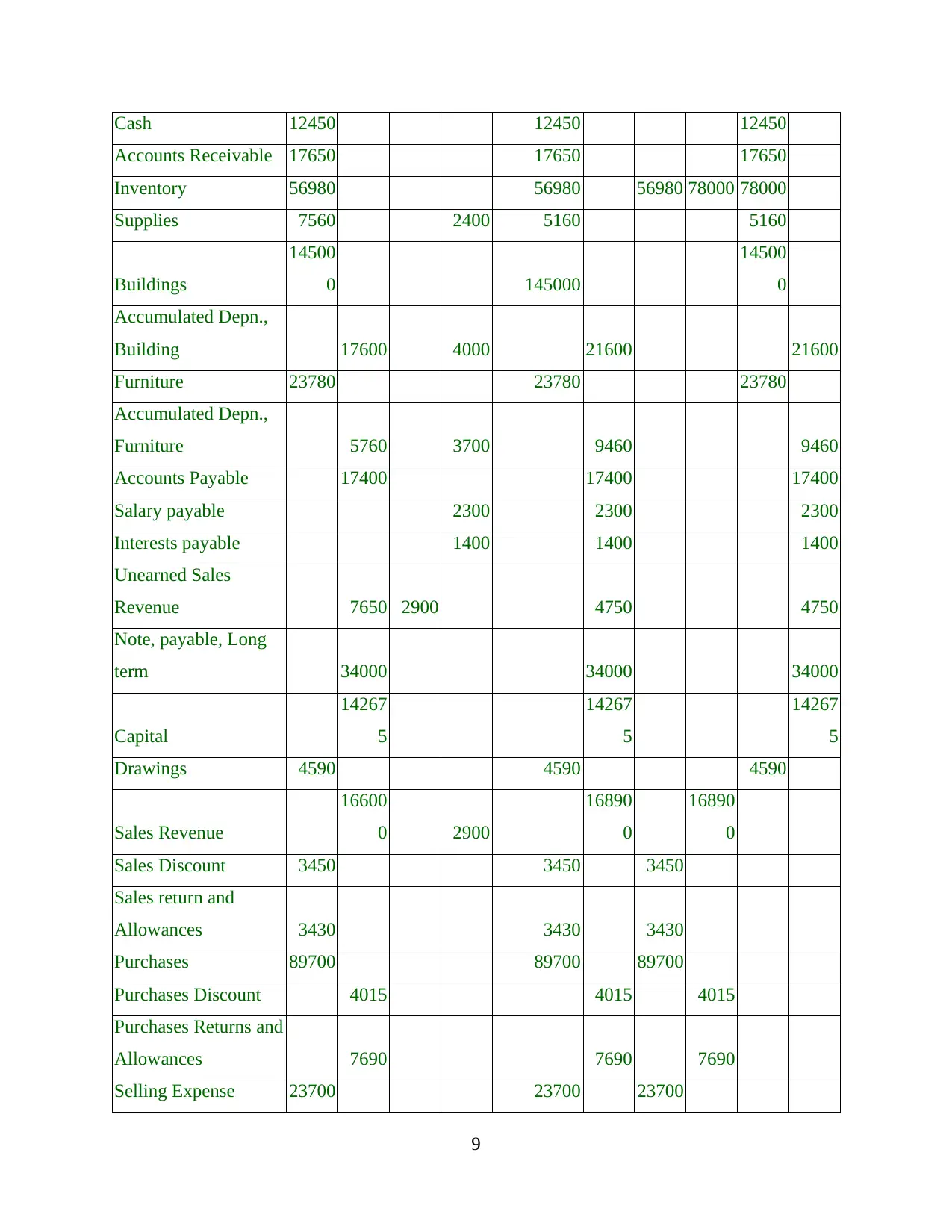

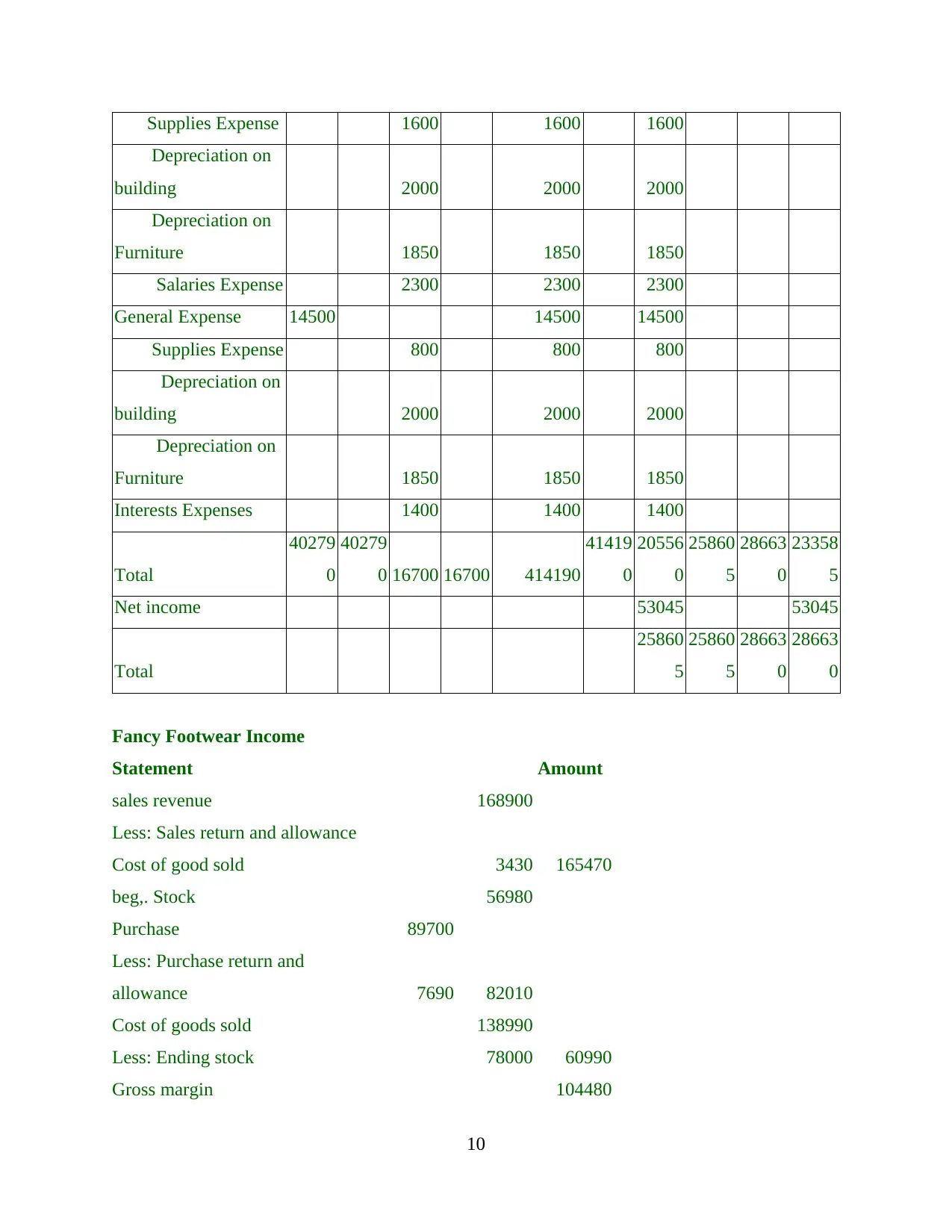

This document presents a comprehensive solution to an accounting assignment, covering key topics such as naming cells, negative numbers, spreadsheet design for data entry and reporting, and the use of IF statements. It delves into periodic inventory systems, worksheet creation, and the preparation of financial reports, including handwritten and spreadsheet solutions. The assignment further explores inventory flow assumptions (FIFO, LIFO, Average Cost), bank reconciliation (handwritten and spreadsheet methods), journalizing accounts receivable entries, and methods for estimating bad debts (percentage of credit sales and aging of accounts receivable). It concludes with an analysis of how receivables are used to evaluate a firm's financial position, the treatment of dishonored notes receivable, and a work-integrated assessment, providing a well-rounded understanding of fundamental accounting principles and practices. The solution includes examples and spreadsheet designs to illustrate the concepts.

1 out of 37

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.