Essay: Accounting Fundamentals, Financial Statements & Analysis

VerifiedAdded on 2023/01/10

|13

|2971

|81

Essay

AI Summary

This essay provides a comprehensive overview of accounting fundamentals, beginning with journal entries and culminating in the preparation and analysis of financial statements. The essay covers the formulation of trial balances, profit and loss accounts, and balance sheets, emphasizing their relevance to various users, including investors, employees, and government entities. A significant portion is dedicated to contrasting and comparing liquidity and profitability, highlighting their distinct roles in assessing a company's financial health. Through detailed explanations and practical examples, the essay illustrates how financial statements serve as crucial tools for decision-making, both internally and externally, ensuring stakeholders can assess a company's performance and make informed strategic choices. The essay also delves into the relevance of financial statements for different users, such as suppliers, investors, and creditors, and how these statements inform their respective decision-making processes. Finally, the essay explores the differences and similarities between liquidity and profitability, emphasizing their roles in the financial health of a company.

Essay on Accounting

Fundamental

Fundamental

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Question 1....................................................................................................................................1

Question 2....................................................................................................................................3

Question 3....................................................................................................................................5

Question 4....................................................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Question 1....................................................................................................................................1

Question 2....................................................................................................................................3

Question 3....................................................................................................................................5

Question 4....................................................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

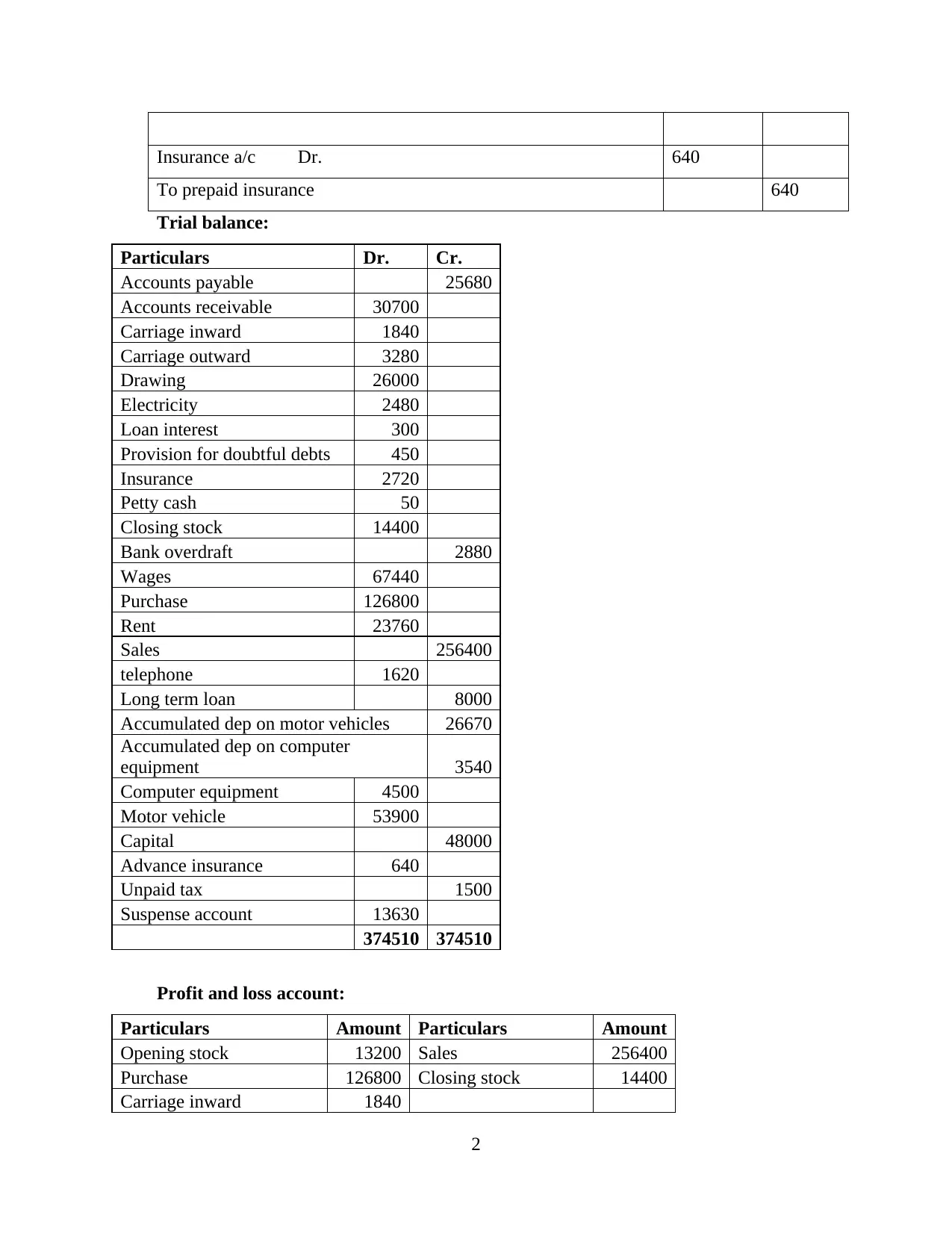

INTRODUCTION

Accounting can be defined as the process of recording business transactions in the books

and final accounts. With the help of it, details of all the incomes and expenses are recorded in

different reports that are generated by an organisation. While planning to determine actual

position of business as well as company it is very important for all the companies to make sure

that they are able to conduct accounting in systematic manner (Burger and Curtis, 2017). It will

help to formulate future policies for betterment of company. Present essay is based upon

formulation of trial balance and financial statements such as profit and loss account and balance

sheet. Apart from this, discussion regarding relevancy of final accounts for users along with

contrasting and comparison of liquidity and profitability are also discussed in this essay.

MAIN BODY

Question 1

Journals entries:

Particulars Debit Credit

Depreciation on motor vehicle a/c Dr. 11670

To accumulated dep a/c 11670

Accumulated dep a/c Dr. 11670

To Motor vehicle a/c 11670

Depreciation on computer equipment a/c Dr. 900

To accumulated dep a/c 900

Accumulated dep a/c Dr. 900

To motor equipment a/c 900

Telephone bill a/c Dr. 180

To cash a/c 180

1

Accounting can be defined as the process of recording business transactions in the books

and final accounts. With the help of it, details of all the incomes and expenses are recorded in

different reports that are generated by an organisation. While planning to determine actual

position of business as well as company it is very important for all the companies to make sure

that they are able to conduct accounting in systematic manner (Burger and Curtis, 2017). It will

help to formulate future policies for betterment of company. Present essay is based upon

formulation of trial balance and financial statements such as profit and loss account and balance

sheet. Apart from this, discussion regarding relevancy of final accounts for users along with

contrasting and comparison of liquidity and profitability are also discussed in this essay.

MAIN BODY

Question 1

Journals entries:

Particulars Debit Credit

Depreciation on motor vehicle a/c Dr. 11670

To accumulated dep a/c 11670

Accumulated dep a/c Dr. 11670

To Motor vehicle a/c 11670

Depreciation on computer equipment a/c Dr. 900

To accumulated dep a/c 900

Accumulated dep a/c Dr. 900

To motor equipment a/c 900

Telephone bill a/c Dr. 180

To cash a/c 180

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Insurance a/c Dr. 640

To prepaid insurance 640

Trial balance:

Particulars Dr. Cr.

Accounts payable 25680

Accounts receivable 30700

Carriage inward 1840

Carriage outward 3280

Drawing 26000

Electricity 2480

Loan interest 300

Provision for doubtful debts 450

Insurance 2720

Petty cash 50

Closing stock 14400

Bank overdraft 2880

Wages 67440

Purchase 126800

Rent 23760

Sales 256400

telephone 1620

Long term loan 8000

Accumulated dep on motor vehicles 26670

Accumulated dep on computer

equipment 3540

Computer equipment 4500

Motor vehicle 53900

Capital 48000

Advance insurance 640

Unpaid tax 1500

Suspense account 13630

374510 374510

Profit and loss account:

Particulars Amount Particulars Amount

Opening stock 13200 Sales 256400

Purchase 126800 Closing stock 14400

Carriage inward 1840

2

To prepaid insurance 640

Trial balance:

Particulars Dr. Cr.

Accounts payable 25680

Accounts receivable 30700

Carriage inward 1840

Carriage outward 3280

Drawing 26000

Electricity 2480

Loan interest 300

Provision for doubtful debts 450

Insurance 2720

Petty cash 50

Closing stock 14400

Bank overdraft 2880

Wages 67440

Purchase 126800

Rent 23760

Sales 256400

telephone 1620

Long term loan 8000

Accumulated dep on motor vehicles 26670

Accumulated dep on computer

equipment 3540

Computer equipment 4500

Motor vehicle 53900

Capital 48000

Advance insurance 640

Unpaid tax 1500

Suspense account 13630

374510 374510

Profit and loss account:

Particulars Amount Particulars Amount

Opening stock 13200 Sales 256400

Purchase 126800 Closing stock 14400

Carriage inward 1840

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

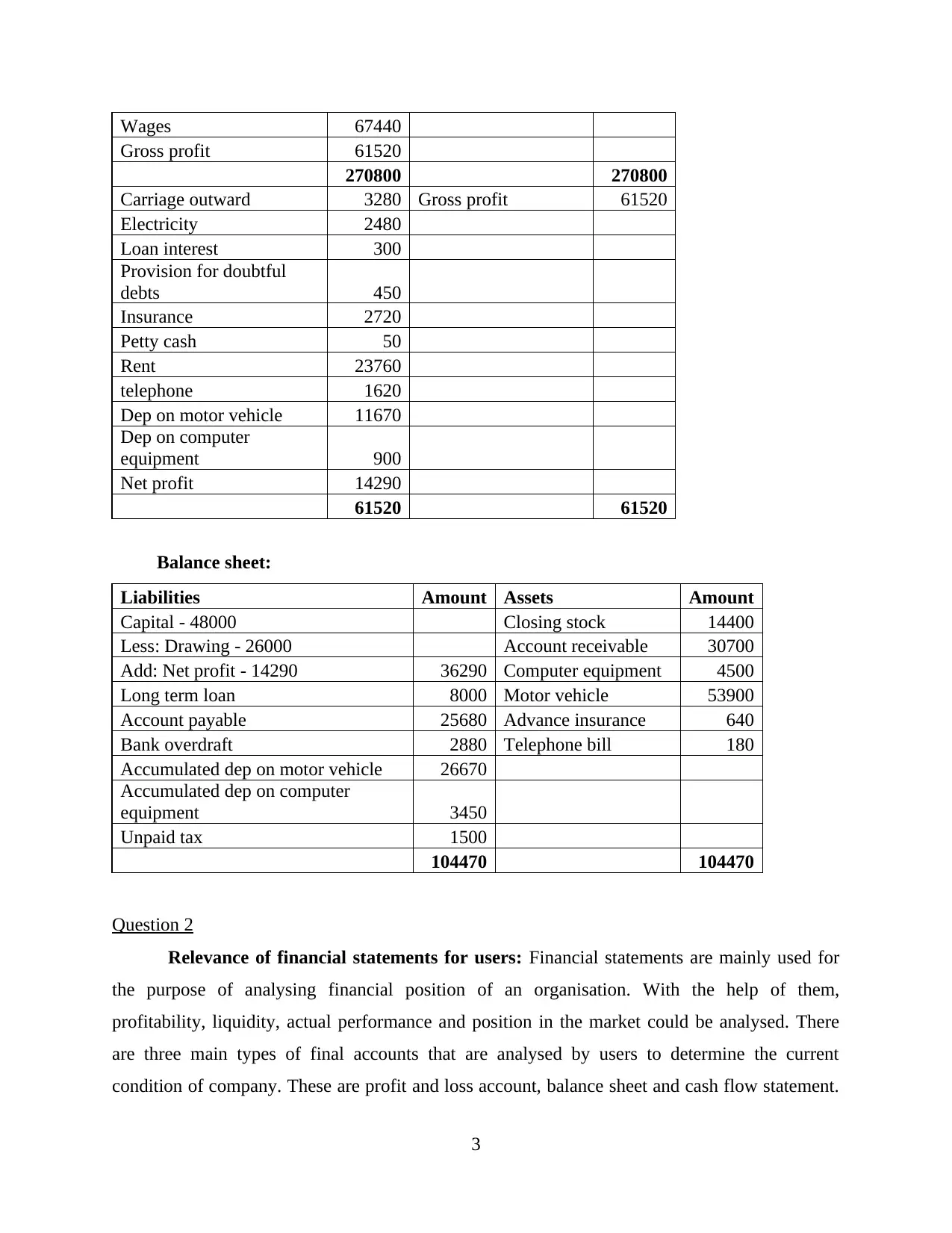

Wages 67440

Gross profit 61520

270800 270800

Carriage outward 3280 Gross profit 61520

Electricity 2480

Loan interest 300

Provision for doubtful

debts 450

Insurance 2720

Petty cash 50

Rent 23760

telephone 1620

Dep on motor vehicle 11670

Dep on computer

equipment 900

Net profit 14290

61520 61520

Balance sheet:

Liabilities Amount Assets Amount

Capital - 48000 Closing stock 14400

Less: Drawing - 26000 Account receivable 30700

Add: Net profit - 14290 36290 Computer equipment 4500

Long term loan 8000 Motor vehicle 53900

Account payable 25680 Advance insurance 640

Bank overdraft 2880 Telephone bill 180

Accumulated dep on motor vehicle 26670

Accumulated dep on computer

equipment 3450

Unpaid tax 1500

104470 104470

Question 2

Relevance of financial statements for users: Financial statements are mainly used for

the purpose of analysing financial position of an organisation. With the help of them,

profitability, liquidity, actual performance and position in the market could be analysed. There

are three main types of final accounts that are analysed by users to determine the current

condition of company. These are profit and loss account, balance sheet and cash flow statement.

3

Gross profit 61520

270800 270800

Carriage outward 3280 Gross profit 61520

Electricity 2480

Loan interest 300

Provision for doubtful

debts 450

Insurance 2720

Petty cash 50

Rent 23760

telephone 1620

Dep on motor vehicle 11670

Dep on computer

equipment 900

Net profit 14290

61520 61520

Balance sheet:

Liabilities Amount Assets Amount

Capital - 48000 Closing stock 14400

Less: Drawing - 26000 Account receivable 30700

Add: Net profit - 14290 36290 Computer equipment 4500

Long term loan 8000 Motor vehicle 53900

Account payable 25680 Advance insurance 640

Bank overdraft 2880 Telephone bill 180

Accumulated dep on motor vehicle 26670

Accumulated dep on computer

equipment 3450

Unpaid tax 1500

104470 104470

Question 2

Relevance of financial statements for users: Financial statements are mainly used for

the purpose of analysing financial position of an organisation. With the help of them,

profitability, liquidity, actual performance and position in the market could be analysed. There

are three main types of final accounts that are analysed by users to determine the current

condition of company. These are profit and loss account, balance sheet and cash flow statement.

3

The detailed information of all the incomes, expenses, losses, gains, profits etc. is recorded in

income statement which is also known as profit and loss account. Details regarding all the

liabilities that are required to be paid by company along with assets that are used to carry out

operations are recorded in balance sheet and it is also called statement of financial position. Part

from this, information of equities that are part of shareholders are also reflected in the same final

account. Cash flow statement is generated to record all the cash transactions that are made by an

organisation in a specific time period (Fisher, Shah and Titman, 2016).

All the financial statements are having separate information and these are relevant to

different users. There are various users of the final accounts. These are suppliers, investors,

customers, government, creditors, shareholders, employees, managers etc. All of them analyse

financial statements for different purposes and all of them are relevant to each one of the users.

The external stakeholders who are delivering goods to the company use financial statements to

analyse credibility of the entity in order to determine that the organisation will be able to make

their payments on time or not. Final accounts are relevant to this user as with the help of them

supplier can determine performance of company. Investors are the external parties which are

having interest in company to invest monetary funds and have right to get interest on the amount

which is being invested by them within the company. Financial statements are relevant for them

because with the help of final accounts they can analyse profitability of company. It will help

them to estimate that the entity will be able to provide the good returns on the finds which are

invested by the within the company (Hoyle, Schaefer and Doupnik, 2018).

Employees are internal stakeholders and they also analyse financial statements to make

sure that they are working in a company which is having good position. Final accounts are

relevant for them as all of them will help the staff to assess that they are working in a financially

strong or weak company. It also helps them to make decision regarding working in the same

enterprise or changing the organisation. Managers are also the internal users of financial

statements as they use final accounts to determine the position of business. These are relevant for

them as with the help of them managers can perform their job of improving performance of

company. By analysing income statement and balance sheet they can formulate effective

strategies which may result in enhanced performed of business (Lallemand and Strauss, 2016).

Customer are external users of financial statements who analyse the performance of

company for the purpose of making sure that they are buying products from a profitable firm or

4

income statement which is also known as profit and loss account. Details regarding all the

liabilities that are required to be paid by company along with assets that are used to carry out

operations are recorded in balance sheet and it is also called statement of financial position. Part

from this, information of equities that are part of shareholders are also reflected in the same final

account. Cash flow statement is generated to record all the cash transactions that are made by an

organisation in a specific time period (Fisher, Shah and Titman, 2016).

All the financial statements are having separate information and these are relevant to

different users. There are various users of the final accounts. These are suppliers, investors,

customers, government, creditors, shareholders, employees, managers etc. All of them analyse

financial statements for different purposes and all of them are relevant to each one of the users.

The external stakeholders who are delivering goods to the company use financial statements to

analyse credibility of the entity in order to determine that the organisation will be able to make

their payments on time or not. Final accounts are relevant to this user as with the help of them

supplier can determine performance of company. Investors are the external parties which are

having interest in company to invest monetary funds and have right to get interest on the amount

which is being invested by them within the company. Financial statements are relevant for them

because with the help of final accounts they can analyse profitability of company. It will help

them to estimate that the entity will be able to provide the good returns on the finds which are

invested by the within the company (Hoyle, Schaefer and Doupnik, 2018).

Employees are internal stakeholders and they also analyse financial statements to make

sure that they are working in a company which is having good position. Final accounts are

relevant for them as all of them will help the staff to assess that they are working in a financially

strong or weak company. It also helps them to make decision regarding working in the same

enterprise or changing the organisation. Managers are also the internal users of financial

statements as they use final accounts to determine the position of business. These are relevant for

them as with the help of them managers can perform their job of improving performance of

company. By analysing income statement and balance sheet they can formulate effective

strategies which may result in enhanced performed of business (Lallemand and Strauss, 2016).

Customer are external users of financial statements who analyse the performance of

company for the purpose of making sure that they are buying products from a profitable firm or

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

not. Final accounts are relevant for them to form the purchasing decisions and be the part of the

organisation for long run. Government is also considered as stakeholders for an entity as

financial statements are analysed by legal authorities to analyse that the company is operating

business in ethical manner or not. Final accounts are relevant for governmental body because

they can guide the legal authority to determine that organisation is paying right amount of tax on

the incomes or not. Apart from this, it can also guide government to analyse the accuracy and

transparency level of figures that are recorded in the final accounts (Nichols, Wahlen and

Wieland, 2017).

Shareholders are the internal users of financial statements who use final accounts to

measure financial viability and sustainability of business. These are relevant for them as it can

help them to make decisions of withdrawing funds or making more investment in the business.

Apart from this, they also assess profit and loss account, balance sheet, cash flow statement etc.

for the purpose of analysing that they will be able to receive dividend or not. Creditors are the

external users of final accounts and they use it for the purpose of evaluating performance of

business. If it is good then only, they will provide credit to the company of they assess that the

organisation is not able to perform appropriately then they will not offer credit to the companies

(Ogneva, Piotroski and Zakolyukina, 2019).

The above discussion shows that final accounts such as profit and loss account, balance

sheet and cash flow statement are relevant for the users of them which are investors, customers,

government, shareholders, managers, employees, creditors, suppliers etc. With the help of

financial statements all of them make strategic decisions for future so that they can attain

benefits in long run. In order to keep all of them engaged in business it is very important for all

the companies to make sure that they are providing them detailed and accurate information about

business.

Question 3

Journals entries:

Particulars Debit Credit

Depreciation on building a/c Dr. 1000

To accumulated dep a/c 1000

5

organisation for long run. Government is also considered as stakeholders for an entity as

financial statements are analysed by legal authorities to analyse that the company is operating

business in ethical manner or not. Final accounts are relevant for governmental body because

they can guide the legal authority to determine that organisation is paying right amount of tax on

the incomes or not. Apart from this, it can also guide government to analyse the accuracy and

transparency level of figures that are recorded in the final accounts (Nichols, Wahlen and

Wieland, 2017).

Shareholders are the internal users of financial statements who use final accounts to

measure financial viability and sustainability of business. These are relevant for them as it can

help them to make decisions of withdrawing funds or making more investment in the business.

Apart from this, they also assess profit and loss account, balance sheet, cash flow statement etc.

for the purpose of analysing that they will be able to receive dividend or not. Creditors are the

external users of final accounts and they use it for the purpose of evaluating performance of

business. If it is good then only, they will provide credit to the company of they assess that the

organisation is not able to perform appropriately then they will not offer credit to the companies

(Ogneva, Piotroski and Zakolyukina, 2019).

The above discussion shows that final accounts such as profit and loss account, balance

sheet and cash flow statement are relevant for the users of them which are investors, customers,

government, shareholders, managers, employees, creditors, suppliers etc. With the help of

financial statements all of them make strategic decisions for future so that they can attain

benefits in long run. In order to keep all of them engaged in business it is very important for all

the companies to make sure that they are providing them detailed and accurate information about

business.

Question 3

Journals entries:

Particulars Debit Credit

Depreciation on building a/c Dr. 1000

To accumulated dep a/c 1000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

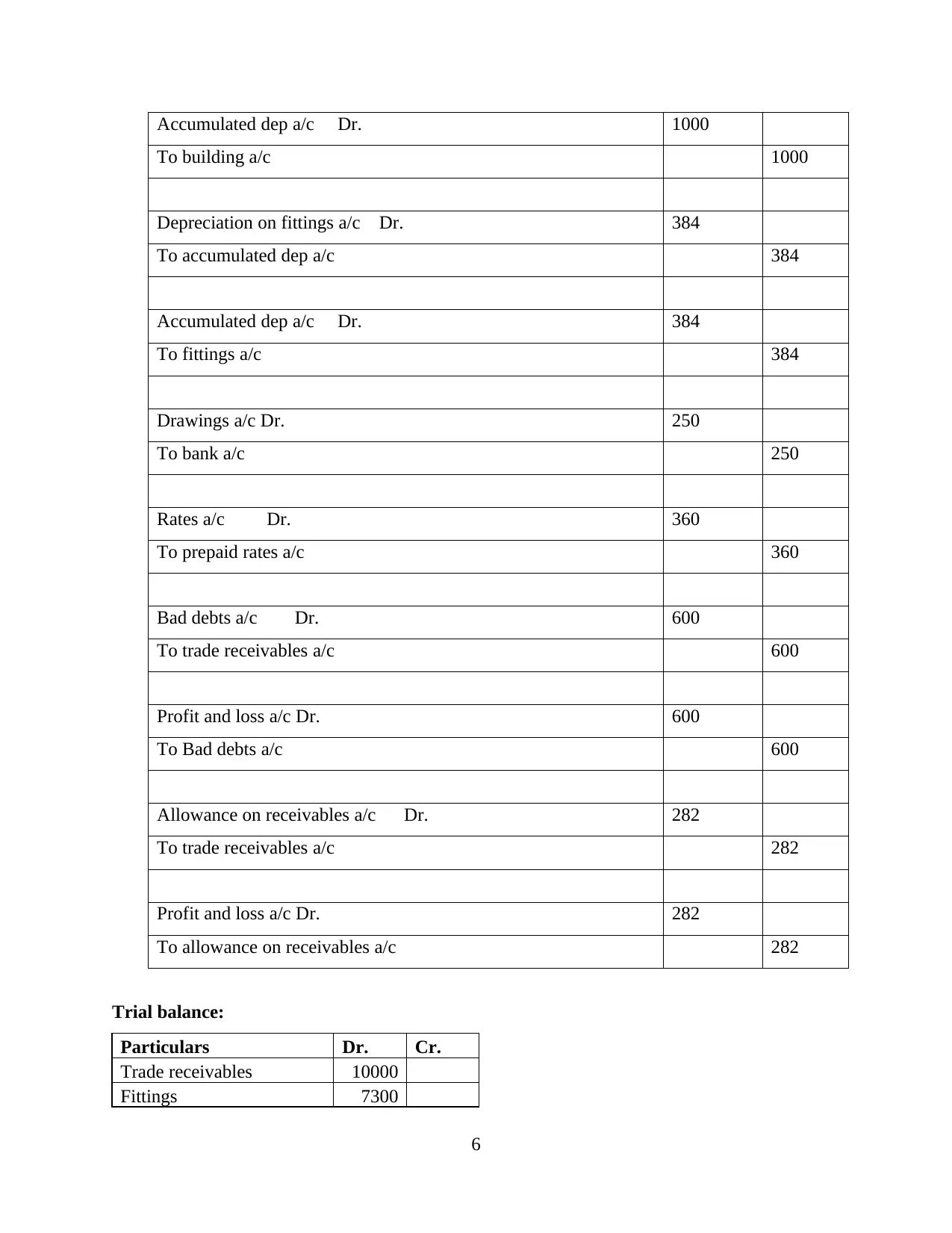

Accumulated dep a/c Dr. 1000

To building a/c 1000

Depreciation on fittings a/c Dr. 384

To accumulated dep a/c 384

Accumulated dep a/c Dr. 384

To fittings a/c 384

Drawings a/c Dr. 250

To bank a/c 250

Rates a/c Dr. 360

To prepaid rates a/c 360

Bad debts a/c Dr. 600

To trade receivables a/c 600

Profit and loss a/c Dr. 600

To Bad debts a/c 600

Allowance on receivables a/c Dr. 282

To trade receivables a/c 282

Profit and loss a/c Dr. 282

To allowance on receivables a/c 282

Trial balance:

Particulars Dr. Cr.

Trade receivables 10000

Fittings 7300

6

To building a/c 1000

Depreciation on fittings a/c Dr. 384

To accumulated dep a/c 384

Accumulated dep a/c Dr. 384

To fittings a/c 384

Drawings a/c Dr. 250

To bank a/c 250

Rates a/c Dr. 360

To prepaid rates a/c 360

Bad debts a/c Dr. 600

To trade receivables a/c 600

Profit and loss a/c Dr. 600

To Bad debts a/c 600

Allowance on receivables a/c Dr. 282

To trade receivables a/c 282

Profit and loss a/c Dr. 282

To allowance on receivables a/c 282

Trial balance:

Particulars Dr. Cr.

Trade receivables 10000

Fittings 7300

6

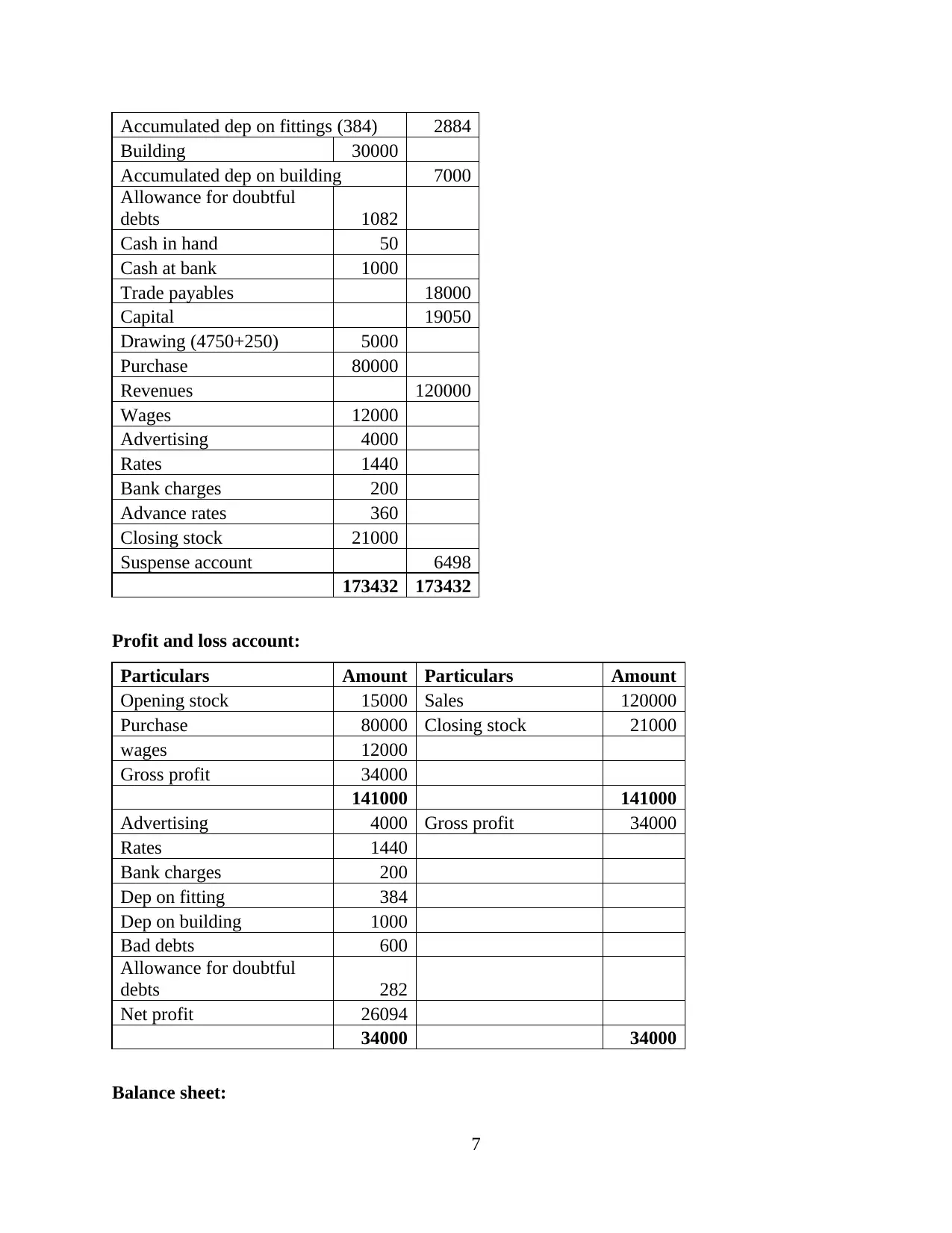

Accumulated dep on fittings (384) 2884

Building 30000

Accumulated dep on building 7000

Allowance for doubtful

debts 1082

Cash in hand 50

Cash at bank 1000

Trade payables 18000

Capital 19050

Drawing (4750+250) 5000

Purchase 80000

Revenues 120000

Wages 12000

Advertising 4000

Rates 1440

Bank charges 200

Advance rates 360

Closing stock 21000

Suspense account 6498

173432 173432

Profit and loss account:

Particulars Amount Particulars Amount

Opening stock 15000 Sales 120000

Purchase 80000 Closing stock 21000

wages 12000

Gross profit 34000

141000 141000

Advertising 4000 Gross profit 34000

Rates 1440

Bank charges 200

Dep on fitting 384

Dep on building 1000

Bad debts 600

Allowance for doubtful

debts 282

Net profit 26094

34000 34000

Balance sheet:

7

Building 30000

Accumulated dep on building 7000

Allowance for doubtful

debts 1082

Cash in hand 50

Cash at bank 1000

Trade payables 18000

Capital 19050

Drawing (4750+250) 5000

Purchase 80000

Revenues 120000

Wages 12000

Advertising 4000

Rates 1440

Bank charges 200

Advance rates 360

Closing stock 21000

Suspense account 6498

173432 173432

Profit and loss account:

Particulars Amount Particulars Amount

Opening stock 15000 Sales 120000

Purchase 80000 Closing stock 21000

wages 12000

Gross profit 34000

141000 141000

Advertising 4000 Gross profit 34000

Rates 1440

Bank charges 200

Dep on fitting 384

Dep on building 1000

Bad debts 600

Allowance for doubtful

debts 282

Net profit 26094

34000 34000

Balance sheet:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

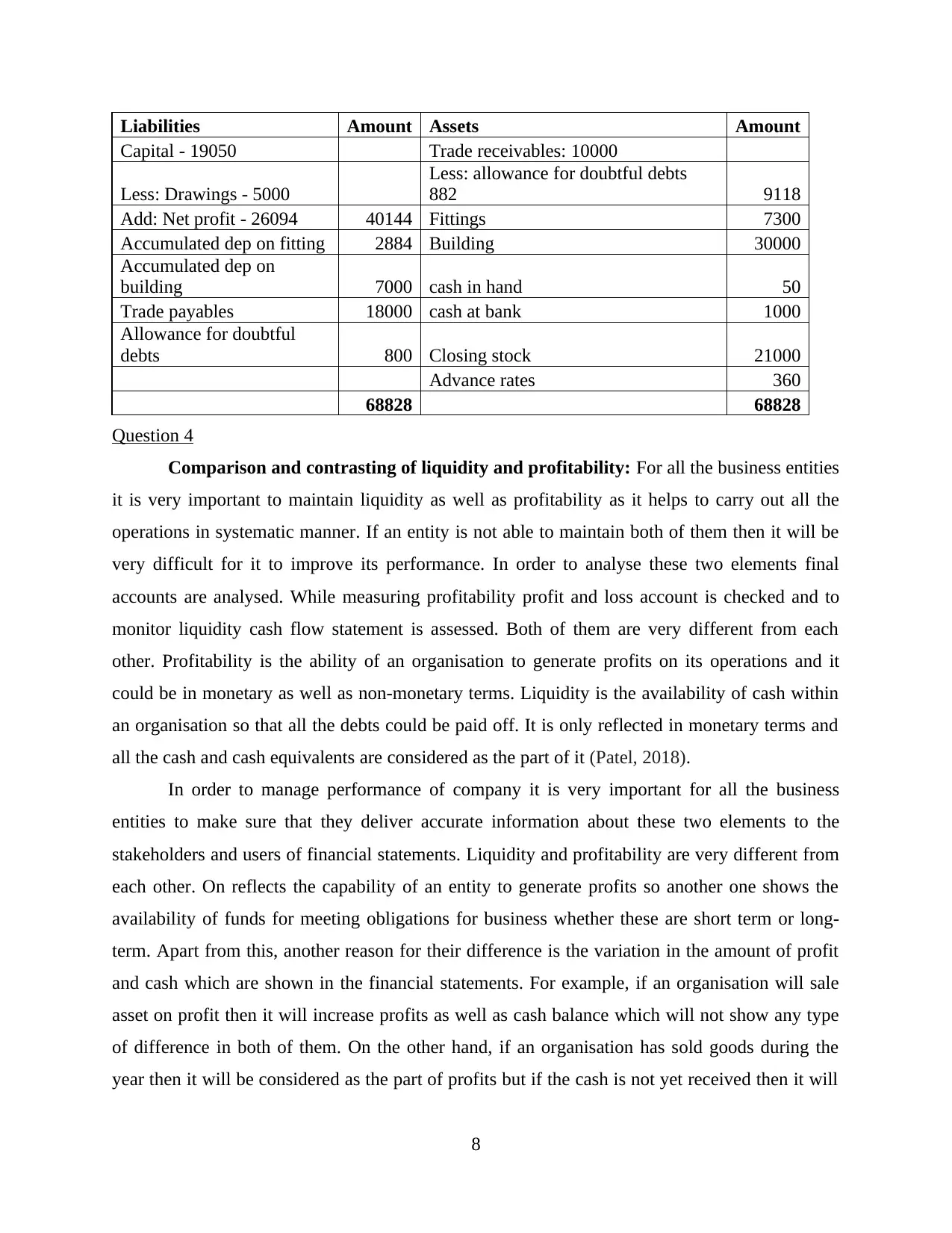

Liabilities Amount Assets Amount

Capital - 19050 Trade receivables: 10000

Less: Drawings - 5000

Less: allowance for doubtful debts

882 9118

Add: Net profit - 26094 40144 Fittings 7300

Accumulated dep on fitting 2884 Building 30000

Accumulated dep on

building 7000 cash in hand 50

Trade payables 18000 cash at bank 1000

Allowance for doubtful

debts 800 Closing stock 21000

Advance rates 360

68828 68828

Question 4

Comparison and contrasting of liquidity and profitability: For all the business entities

it is very important to maintain liquidity as well as profitability as it helps to carry out all the

operations in systematic manner. If an entity is not able to maintain both of them then it will be

very difficult for it to improve its performance. In order to analyse these two elements final

accounts are analysed. While measuring profitability profit and loss account is checked and to

monitor liquidity cash flow statement is assessed. Both of them are very different from each

other. Profitability is the ability of an organisation to generate profits on its operations and it

could be in monetary as well as non-monetary terms. Liquidity is the availability of cash within

an organisation so that all the debts could be paid off. It is only reflected in monetary terms and

all the cash and cash equivalents are considered as the part of it (Patel, 2018).

In order to manage performance of company it is very important for all the business

entities to make sure that they deliver accurate information about these two elements to the

stakeholders and users of financial statements. Liquidity and profitability are very different from

each other. On reflects the capability of an entity to generate profits so another one shows the

availability of funds for meeting obligations for business whether these are short term or long-

term. Apart from this, another reason for their difference is the variation in the amount of profit

and cash which are shown in the financial statements. For example, if an organisation will sale

asset on profit then it will increase profits as well as cash balance which will not show any type

of difference in both of them. On the other hand, if an organisation has sold goods during the

year then it will be considered as the part of profits but if the cash is not yet received then it will

8

Capital - 19050 Trade receivables: 10000

Less: Drawings - 5000

Less: allowance for doubtful debts

882 9118

Add: Net profit - 26094 40144 Fittings 7300

Accumulated dep on fitting 2884 Building 30000

Accumulated dep on

building 7000 cash in hand 50

Trade payables 18000 cash at bank 1000

Allowance for doubtful

debts 800 Closing stock 21000

Advance rates 360

68828 68828

Question 4

Comparison and contrasting of liquidity and profitability: For all the business entities

it is very important to maintain liquidity as well as profitability as it helps to carry out all the

operations in systematic manner. If an entity is not able to maintain both of them then it will be

very difficult for it to improve its performance. In order to analyse these two elements final

accounts are analysed. While measuring profitability profit and loss account is checked and to

monitor liquidity cash flow statement is assessed. Both of them are very different from each

other. Profitability is the ability of an organisation to generate profits on its operations and it

could be in monetary as well as non-monetary terms. Liquidity is the availability of cash within

an organisation so that all the debts could be paid off. It is only reflected in monetary terms and

all the cash and cash equivalents are considered as the part of it (Patel, 2018).

In order to manage performance of company it is very important for all the business

entities to make sure that they deliver accurate information about these two elements to the

stakeholders and users of financial statements. Liquidity and profitability are very different from

each other. On reflects the capability of an entity to generate profits so another one shows the

availability of funds for meeting obligations for business whether these are short term or long-

term. Apart from this, another reason for their difference is the variation in the amount of profit

and cash which are shown in the financial statements. For example, if an organisation will sale

asset on profit then it will increase profits as well as cash balance which will not show any type

of difference in both of them. On the other hand, if an organisation has sold goods during the

year then it will be considered as the part of profits but if the cash is not yet received then it will

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

not be considered as the part of liquidity. It is the main reason why the profits and cash balance

in financial statements varies (Ward and Calabrese, 2018).

There are various similarities in liquidity and profitability. Both of them are analysed by the

stakeholders for the purpose of formulating long term strategic decisions. Creditors analyse

liquidity so that they can make sure that company is able to make payment of them in the

specific time period. Investors analyse both of them to make sure that that they will be able to

generate good returns on the funds that will be invested by them in the business. These are two

main elements of final accounts which are required to be focused by all the companies to meet

the business obligations. Both of them reflect position and performance of business so that the

management can formulate specific policies to improve the market image and performance of the

organisation. While planning to attract large number of investors and customers liquidity as well

as profitability are focused by the entities as with the help of them, they can attract large number

of investors who will provide funds to operate business in more systematic manner. It is very

important for all the companies to make sure that they are able to manage and maintain these two

specific qualities as high level of them reflect good position (Wright, 2017).

The above discussion shows that liquidity and profitability have various differences and

similarities. Apart from this, there are various types of transactions that may result in variation in

profit and cash balance of final accounts. One of them is credit sales, if organisation will make

sales on credit then it will increase the profitability but liquidity will not be increased due to this.

The liquidity will be increased if the company will receive the credit balance.

CONCLUSION

From the above project report it has been concluded that, accounting is a process which is

required to be followed by all the organisations to record all the transactions that are made during

an accounting year. It is essential for the accounting professionals to make sure that they are able

to follow all the accounting principles that are required to formulate yearly records. There are

various types of final accounts that are generated by companies to evaluate yearly performance.

These are profit and loss account, balance sheet and cash flow statement. With the help of all of

them, actual position and performance of business could be determined. Apart from this, it can

also help to formulate future decisions. These financial statements are relevant for the users like

shareholders, investors, customers, creditors, suppliers, employees, managers, government for

different objectives. Some of their purposes are investment, buying products, getting dividend,

9

in financial statements varies (Ward and Calabrese, 2018).

There are various similarities in liquidity and profitability. Both of them are analysed by the

stakeholders for the purpose of formulating long term strategic decisions. Creditors analyse

liquidity so that they can make sure that company is able to make payment of them in the

specific time period. Investors analyse both of them to make sure that that they will be able to

generate good returns on the funds that will be invested by them in the business. These are two

main elements of final accounts which are required to be focused by all the companies to meet

the business obligations. Both of them reflect position and performance of business so that the

management can formulate specific policies to improve the market image and performance of the

organisation. While planning to attract large number of investors and customers liquidity as well

as profitability are focused by the entities as with the help of them, they can attract large number

of investors who will provide funds to operate business in more systematic manner. It is very

important for all the companies to make sure that they are able to manage and maintain these two

specific qualities as high level of them reflect good position (Wright, 2017).

The above discussion shows that liquidity and profitability have various differences and

similarities. Apart from this, there are various types of transactions that may result in variation in

profit and cash balance of final accounts. One of them is credit sales, if organisation will make

sales on credit then it will increase the profitability but liquidity will not be increased due to this.

The liquidity will be increased if the company will receive the credit balance.

CONCLUSION

From the above project report it has been concluded that, accounting is a process which is

required to be followed by all the organisations to record all the transactions that are made during

an accounting year. It is essential for the accounting professionals to make sure that they are able

to follow all the accounting principles that are required to formulate yearly records. There are

various types of final accounts that are generated by companies to evaluate yearly performance.

These are profit and loss account, balance sheet and cash flow statement. With the help of all of

them, actual position and performance of business could be determined. Apart from this, it can

also help to formulate future decisions. These financial statements are relevant for the users like

shareholders, investors, customers, creditors, suppliers, employees, managers, government for

different objectives. Some of their purposes are investment, buying products, getting dividend,

9

measuring credibility, viability and sustainability. All the stakeholders want that company should

share accurate and transparent information with them so that they can form strategic decisions.

Liquidity and profitability are two main elements that are focused by them as by measuring them

they can form specific decisions. These two elements of final accounts guide them to assess that

the company will be able to meet their expectations or not.

10

share accurate and transparent information with them so that they can form strategic decisions.

Liquidity and profitability are two main elements that are focused by them as by measuring them

they can form specific decisions. These two elements of final accounts guide them to assess that

the company will be able to meet their expectations or not.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.