Unit 5: Accounting Principles - Context and Financial Statements

VerifiedAdded on 2022/01/15

|22

|4046

|40

Report

AI Summary

This report delves into the core concepts of accounting, exploring the context and purpose of accounting within organizations, including regulatory and ethical constraints. It examines the differences between management and financial accounting, and identifies various user types for private universities. The report then analyzes cost allocation methods (absorption and marginal costing) with calculations, and discusses inventory management systems, including Just-in-Time (JIT) and Just-in-Case (JIC) approaches, along with Economic Order Quantity (EOQ). Furthermore, the report covers the preparation of basic financial statements for unincorporated and small business organizations, in accordance with accounting principles, conventions, and standards. The report includes source documents, journals, ledger accounts, trial balances, and the accounting cycle. Detailed examples and calculations are provided throughout the report to illustrate the concepts discussed.

RECORDING AND FEEDING BACK ON LEARNER ACHIEVEMENT

Course / Award Pearson BTEC HND Level 5 in Business

Management

Unit 5 Accounting Principles

Student Name Nguyen Huu BaoTran_20BM40211

Assessment criteria that

have been achieved

Assessment Criteria that

are still to be achieved

Assessor’s feedback (specific to assessment criteria)

Student Name/Signature Rework Due

Date

Assessor Name /

Signature Date

IV Name / Signature Date

Assessor’s feedback on the rework:

Student Name/Signature Date

Assessor Name /

Signature Date

IV Name / Signature Date

Course / Award Pearson BTEC HND Level 5 in Business

Management

Unit 5 Accounting Principles

Student Name Nguyen Huu BaoTran_20BM40211

Assessment criteria that

have been achieved

Assessment Criteria that

are still to be achieved

Assessor’s feedback (specific to assessment criteria)

Student Name/Signature Rework Due

Date

Assessor Name /

Signature Date

IV Name / Signature Date

Assessor’s feedback on the rework:

Student Name/Signature Date

Assessor Name /

Signature Date

IV Name / Signature Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assignment Brief

Student Name/ID Number Nguyen Huu BaoTran_20BM40211

Unit Number and Title Unit 5: Accounting Principles

Academic Year 2021-2022

Unit Tutor Sumit Dhull

Assignment Title 1/2: Accounting in Context and Budgetary Control

Issue Date 03 December 2021

Submission Date 03 January 2022

Internal Verifier Dang Quang Vang

Date of IV 02 January 2022

Student declaration

I certify that the work submitted for this assignment is my own. I have clearly referenced any

sources used in the work. I understand that false declaration is a form of malpractice.

Student signature: Nguyễn Hữu Bảo Trân Date: 02th January, 2022

TABLE OF CONTENTS

2

Student Name/ID Number Nguyen Huu BaoTran_20BM40211

Unit Number and Title Unit 5: Accounting Principles

Academic Year 2021-2022

Unit Tutor Sumit Dhull

Assignment Title 1/2: Accounting in Context and Budgetary Control

Issue Date 03 December 2021

Submission Date 03 January 2022

Internal Verifier Dang Quang Vang

Date of IV 02 January 2022

Student declaration

I certify that the work submitted for this assignment is my own. I have clearly referenced any

sources used in the work. I understand that false declaration is a form of malpractice.

Student signature: Nguyễn Hữu Bảo Trân Date: 02th January, 2022

TABLE OF CONTENTS

2

I/ INTRODUCTION..........................................................................................................4

II/ EXAMINE THE CONTEXT AND PURPOSE OF ACCOUNTING..............................5

A. The purpose of the accounting function.............................................................5

1. The accounting function.......................................................................................5

2. Difference between management accounting and finance accounting...............5

3. Types of Various users for private university.......................................................5

B. The accounting function within the organization in the context of regulatory

and ethical constraints..........................................................................................5

1. The structure of the cost allocation method.........................................................5

2. Calculation formula of cost allocation method......................................................6

3. Inventory management system............................................................................7

III/ BASIC FINANCIAL STATEMENTS FOR UNINCORPORATED AND SMALL

BUSINESS ORGANIZATIONS IN ACCORDANCE WITH ACCOUNTING PRINCIPLES,

CONVENTIONS, AND STANDARDS.............................................................................9

A. Accounting principles, conventions, and standards........................................9

1. Source documents................................................................................................9

2. Journals................................................................................................................10

3. Ledger (‘T’ account) .............................................................................................11

4. Trial Balance.........................................................................................................11

B. Financial statement................................................................................................12

1. Journals................................................................................................................12

2. Ledger (‘T’ account) .............................................................................................14

3. Trial Balance.........................................................................................................17

IV/ CONCLUSION...........................................................................................................18

V/ APPENDIX..................................................................................................................19

1. The accounting function.........................................................................................19

2. Difference between management accounting and finance accounting.................19

3. Types of Various users for private university........................................................21

VI/ REFERENCE.............................................................................................................22

I. INTRODUCTION

3

II/ EXAMINE THE CONTEXT AND PURPOSE OF ACCOUNTING..............................5

A. The purpose of the accounting function.............................................................5

1. The accounting function.......................................................................................5

2. Difference between management accounting and finance accounting...............5

3. Types of Various users for private university.......................................................5

B. The accounting function within the organization in the context of regulatory

and ethical constraints..........................................................................................5

1. The structure of the cost allocation method.........................................................5

2. Calculation formula of cost allocation method......................................................6

3. Inventory management system............................................................................7

III/ BASIC FINANCIAL STATEMENTS FOR UNINCORPORATED AND SMALL

BUSINESS ORGANIZATIONS IN ACCORDANCE WITH ACCOUNTING PRINCIPLES,

CONVENTIONS, AND STANDARDS.............................................................................9

A. Accounting principles, conventions, and standards........................................9

1. Source documents................................................................................................9

2. Journals................................................................................................................10

3. Ledger (‘T’ account) .............................................................................................11

4. Trial Balance.........................................................................................................11

B. Financial statement................................................................................................12

1. Journals................................................................................................................12

2. Ledger (‘T’ account) .............................................................................................14

3. Trial Balance.........................................................................................................17

IV/ CONCLUSION...........................................................................................................18

V/ APPENDIX..................................................................................................................19

1. The accounting function.........................................................................................19

2. Difference between management accounting and finance accounting.................19

3. Types of Various users for private university........................................................21

VI/ REFERENCE.............................................................................................................22

I. INTRODUCTION

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In the field of finance, accountants can understand and apply concepts and methods of

financial analysis accurately. The problems raised are scientifically arranged with

detailed solutions.

In this report, I will talk about the context, purpose of the accounting function in an

organization, Types of accounting and difference between management accounting and

financial accounting, Different types of users for private universities. The accounting

function within the organization in the context of regulatory and ethical constraints

includes the structure of the cost allocation method, the Calculation formula of the cost

allocation method, and the Inventory management system.

Next, I will evaluate the accounting function in the organization in the context of

regulatory and ethical constraints including what are the methods of cost allocation?

Explain these two methods in detail with their structure to calculate profit then calculate

and use a table to show the calculation. Moreover, I will explain JIT & JIC, order cost,

implementation cost, EOQ (with graph) and then I will calculate for JIT and JIC.

Finally prepare the basic financial statements for small business and unincorporated

organizations in accordance with accounting principles, conventions and standards by

preparing the financial statements from a certain trial balance for sole traders,

partnerships, and nonprofits, to meet accounting principles, conventions, and standards.

Next, I will explain the accounting cycle in great detail. About rules for the journal, steps

for the journal, 'T' Account, steps like prepare format, transfer log and find balance, trial

balance, and trial balance rule and then is to show the calculations on the following with

explanations.

II. EXAMINE THE CONTEXT AND PURPOSE OF ACCOUNTING

A. The purpose of the accounting function

4

financial analysis accurately. The problems raised are scientifically arranged with

detailed solutions.

In this report, I will talk about the context, purpose of the accounting function in an

organization, Types of accounting and difference between management accounting and

financial accounting, Different types of users for private universities. The accounting

function within the organization in the context of regulatory and ethical constraints

includes the structure of the cost allocation method, the Calculation formula of the cost

allocation method, and the Inventory management system.

Next, I will evaluate the accounting function in the organization in the context of

regulatory and ethical constraints including what are the methods of cost allocation?

Explain these two methods in detail with their structure to calculate profit then calculate

and use a table to show the calculation. Moreover, I will explain JIT & JIC, order cost,

implementation cost, EOQ (with graph) and then I will calculate for JIT and JIC.

Finally prepare the basic financial statements for small business and unincorporated

organizations in accordance with accounting principles, conventions and standards by

preparing the financial statements from a certain trial balance for sole traders,

partnerships, and nonprofits, to meet accounting principles, conventions, and standards.

Next, I will explain the accounting cycle in great detail. About rules for the journal, steps

for the journal, 'T' Account, steps like prepare format, transfer log and find balance, trial

balance, and trial balance rule and then is to show the calculations on the following with

explanations.

II. EXAMINE THE CONTEXT AND PURPOSE OF ACCOUNTING

A. The purpose of the accounting function

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

See appendix page 18

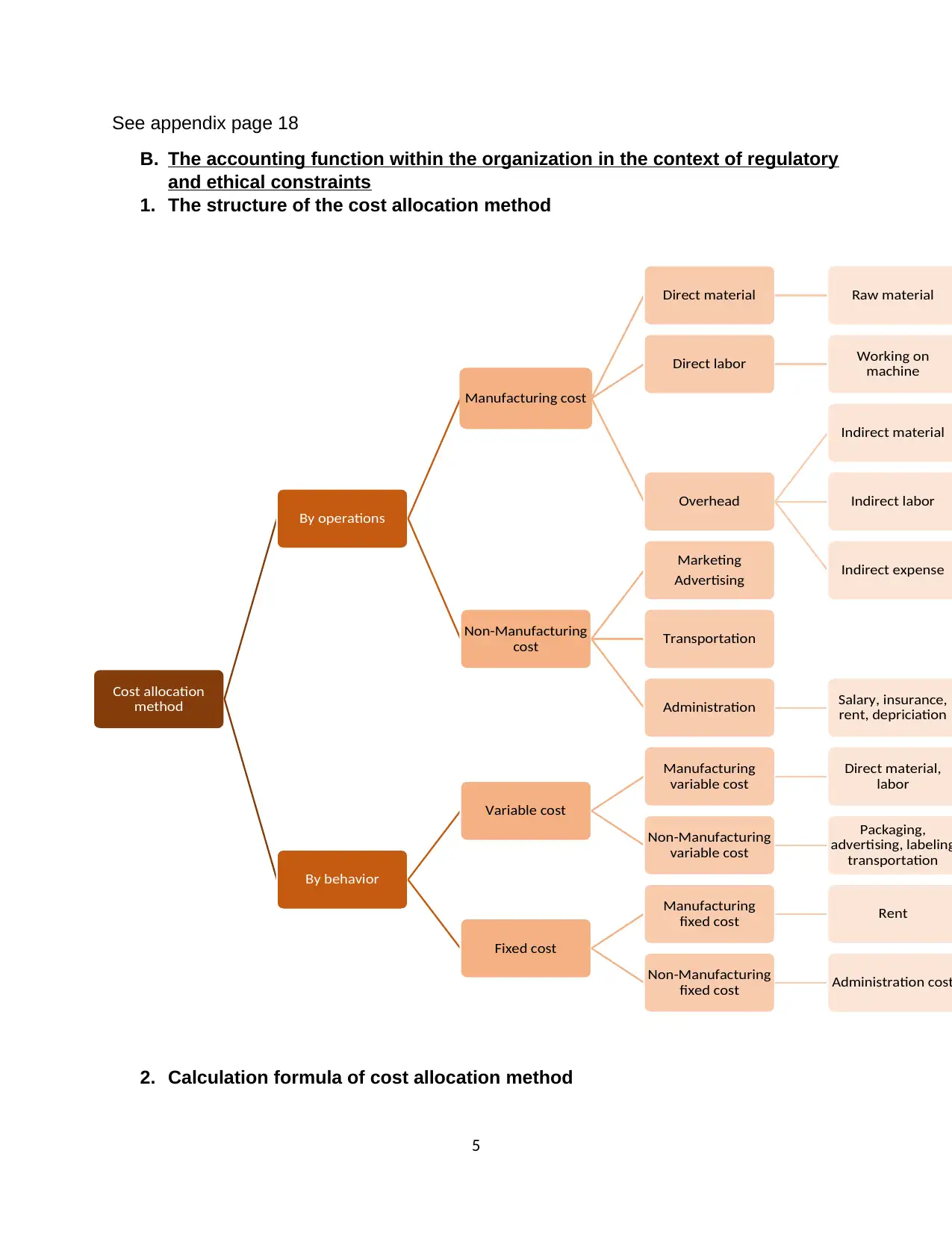

B. The accounting function within the organization in the context of regulatory

and ethical constraints

1. The structure of the cost allocation method

2. Calculation formula of cost allocation method

5

Cost allocation

method

By operations

Manufacturing cost

Direct material Raw material

Direct labor Working on

machine

Overhead

Indirect material

Indirect labor

Indirect expense

Non-Manufacturing

cost

Marketing

Advertising

Transportation

Administration Salary, insurance,

rent, depriciation

By behavior

Variable cost

Manufacturing

variable cost

Direct material,

labor

Non-Manufacturing

variable cost

Packaging,

advertising, labeling

transportation

Fixed cost

Manufacturing

fixed cost Rent

Non-Manufacturing

fixed cost Administration cost

B. The accounting function within the organization in the context of regulatory

and ethical constraints

1. The structure of the cost allocation method

2. Calculation formula of cost allocation method

5

Cost allocation

method

By operations

Manufacturing cost

Direct material Raw material

Direct labor Working on

machine

Overhead

Indirect material

Indirect labor

Indirect expense

Non-Manufacturing

cost

Marketing

Advertising

Transportation

Administration Salary, insurance,

rent, depriciation

By behavior

Variable cost

Manufacturing

variable cost

Direct material,

labor

Non-Manufacturing

variable cost

Packaging,

advertising, labeling

transportation

Fixed cost

Manufacturing

fixed cost Rent

Non-Manufacturing

fixed cost Administration cost

Absorption costing

• Sales - Cost Of Goods Sold= Gross Profit - Non-manufacturing Cost = Net Profit

Or Loss

• Opening Inventory (Unit) +Production (Unit) - Closing Inventory (Unit) = COGS In

Unit x Manufacturing Cost per Unit (Direct & Indirect) = COGS In $

January February March

Sales(1) 16500 22000 22000

Cost Of Goods Sold(2) 12000 16000 16000

Gross Profit 4500 6000 6000

Non-manufacturing

Cost

0 0 0

Net Profit 4500 6000 6000

(1) Sales= sales unit x selling price per unit = 1,500 x £11 = 16500

(2) COGS= units sold x manufacturing cost per unit (variable cost per unit + fixed cost

per unit) = 1,500 x 8 = 12000

Marginal costing

• Sales - Variable Manufacturing Cost - Variable Non-manufacturing Cost =

Contribution Margin - Fix Manufacturing Cost - Fix Non-manufacturing = Net

Profit Or Loss

January February March

Sales (1) 16500 22000 22000

Cost Of Goods Sold

(2)

7500 10000 10000

Variable non-

manufacturing cost

0 0 0

Contribution margin

(3)

9000 12000 12000

Fix manufacturing

cost (4)

9000 9000 9000

Fix non-

manufacturing cost

0 0 0

Net profit or loss 0 3000 3000

(1) Sales= sales unit x selling price per unit = 1,500 x £11 = 16500

(2) COGS= sales unit x variable cost per unit = 1,500 x £5 = 7500

(3) Contribution margin= Sales – COGS= 16500 – 7500= 9000

6

• Sales - Cost Of Goods Sold= Gross Profit - Non-manufacturing Cost = Net Profit

Or Loss

• Opening Inventory (Unit) +Production (Unit) - Closing Inventory (Unit) = COGS In

Unit x Manufacturing Cost per Unit (Direct & Indirect) = COGS In $

January February March

Sales(1) 16500 22000 22000

Cost Of Goods Sold(2) 12000 16000 16000

Gross Profit 4500 6000 6000

Non-manufacturing

Cost

0 0 0

Net Profit 4500 6000 6000

(1) Sales= sales unit x selling price per unit = 1,500 x £11 = 16500

(2) COGS= units sold x manufacturing cost per unit (variable cost per unit + fixed cost

per unit) = 1,500 x 8 = 12000

Marginal costing

• Sales - Variable Manufacturing Cost - Variable Non-manufacturing Cost =

Contribution Margin - Fix Manufacturing Cost - Fix Non-manufacturing = Net

Profit Or Loss

January February March

Sales (1) 16500 22000 22000

Cost Of Goods Sold

(2)

7500 10000 10000

Variable non-

manufacturing cost

0 0 0

Contribution margin

(3)

9000 12000 12000

Fix manufacturing

cost (4)

9000 9000 9000

Fix non-

manufacturing cost

0 0 0

Net profit or loss 0 3000 3000

(1) Sales= sales unit x selling price per unit = 1,500 x £11 = 16500

(2) COGS= sales unit x variable cost per unit = 1,500 x £5 = 7500

(3) Contribution margin= Sales – COGS= 16500 – 7500= 9000

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(4) Fix manufacturing cost= Fixed factory overhead for the year / 12 month = £108,000 /

12= 9000

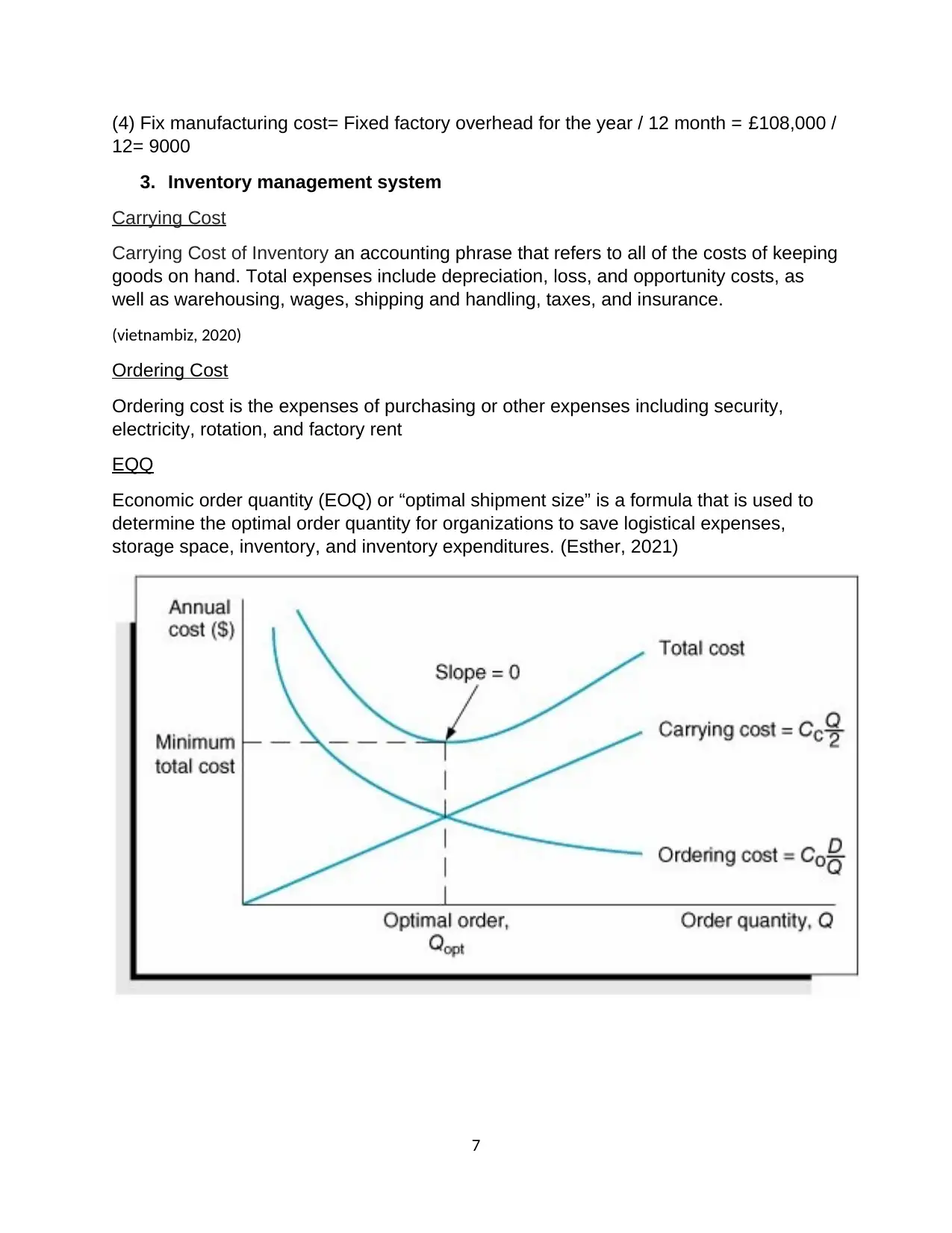

3. Inventory management system

Carrying Cost

Carrying Cost of Inventory an accounting phrase that refers to all of the costs of keeping

goods on hand. Total expenses include depreciation, loss, and opportunity costs, as

well as warehousing, wages, shipping and handling, taxes, and insurance.

(vietnambiz, 2020)

Ordering Cost

Ordering cost is the expenses of purchasing or other expenses including security,

electricity, rotation, and factory rent

EQQ

Economic order quantity (EOQ) or “optimal shipment size” is a formula that is used to

determine the optimal order quantity for organizations to save logistical expenses,

storage space, inventory, and inventory expenditures. (Esther, 2021)

7

12= 9000

3. Inventory management system

Carrying Cost

Carrying Cost of Inventory an accounting phrase that refers to all of the costs of keeping

goods on hand. Total expenses include depreciation, loss, and opportunity costs, as

well as warehousing, wages, shipping and handling, taxes, and insurance.

(vietnambiz, 2020)

Ordering Cost

Ordering cost is the expenses of purchasing or other expenses including security,

electricity, rotation, and factory rent

EQQ

Economic order quantity (EOQ) or “optimal shipment size” is a formula that is used to

determine the optimal order quantity for organizations to save logistical expenses,

storage space, inventory, and inventory expenditures. (Esther, 2021)

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

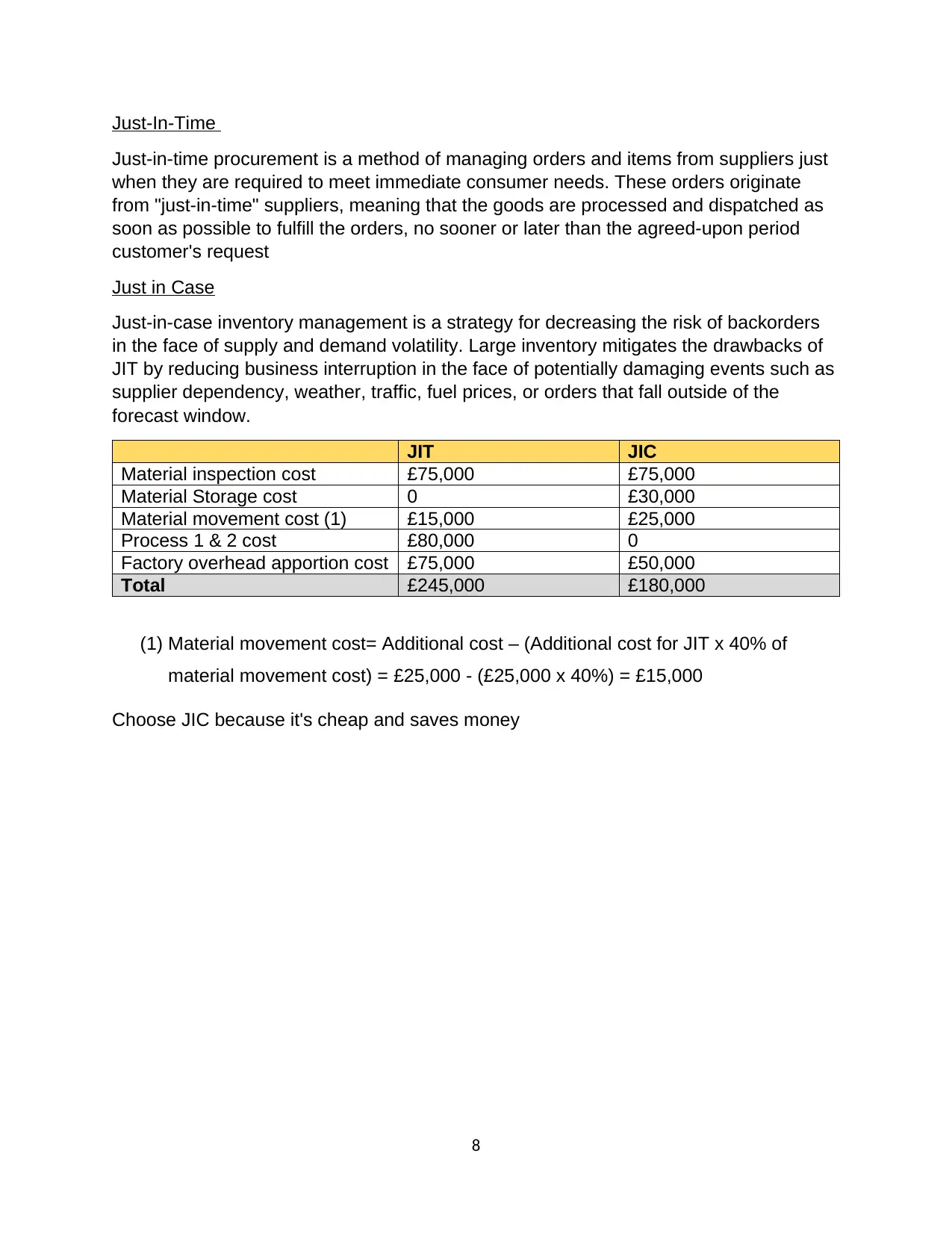

Just-In-Time

Just-in-time procurement is a method of managing orders and items from suppliers just

when they are required to meet immediate consumer needs. These orders originate

from "just-in-time" suppliers, meaning that the goods are processed and dispatched as

soon as possible to fulfill the orders, no sooner or later than the agreed-upon period

customer's request

Just in Case

Just-in-case inventory management is a strategy for decreasing the risk of backorders

in the face of supply and demand volatility. Large inventory mitigates the drawbacks of

JIT by reducing business interruption in the face of potentially damaging events such as

supplier dependency, weather, traffic, fuel prices, or orders that fall outside of the

forecast window.

JIT JIC

Material inspection cost £75,000 £75,000

Material Storage cost 0 £30,000

Material movement cost (1) £15,000 £25,000

Process 1 & 2 cost £80,000 0

Factory overhead apportion cost £75,000 £50,000

Total £245,000 £180,000

(1) Material movement cost= Additional cost – (Additional cost for JIT x 40% of

material movement cost) = £25,000 - (£25,000 x 40%) = £15,000

Choose JIC because it's cheap and saves money

8

Just-in-time procurement is a method of managing orders and items from suppliers just

when they are required to meet immediate consumer needs. These orders originate

from "just-in-time" suppliers, meaning that the goods are processed and dispatched as

soon as possible to fulfill the orders, no sooner or later than the agreed-upon period

customer's request

Just in Case

Just-in-case inventory management is a strategy for decreasing the risk of backorders

in the face of supply and demand volatility. Large inventory mitigates the drawbacks of

JIT by reducing business interruption in the face of potentially damaging events such as

supplier dependency, weather, traffic, fuel prices, or orders that fall outside of the

forecast window.

JIT JIC

Material inspection cost £75,000 £75,000

Material Storage cost 0 £30,000

Material movement cost (1) £15,000 £25,000

Process 1 & 2 cost £80,000 0

Factory overhead apportion cost £75,000 £50,000

Total £245,000 £180,000

(1) Material movement cost= Additional cost – (Additional cost for JIT x 40% of

material movement cost) = £25,000 - (£25,000 x 40%) = £15,000

Choose JIC because it's cheap and saves money

8

III. BASIC FINANCIAL STATEMENTS FOR UNINCORPORATED AND SMALL

BUSINESS ORGANIZATIONS IN ACCORDANCE WITH ACCOUNTING

PRINCIPLES, CONVENTIONS, AND STANDARDS.

A. Accounting principles, conventions, and standards.

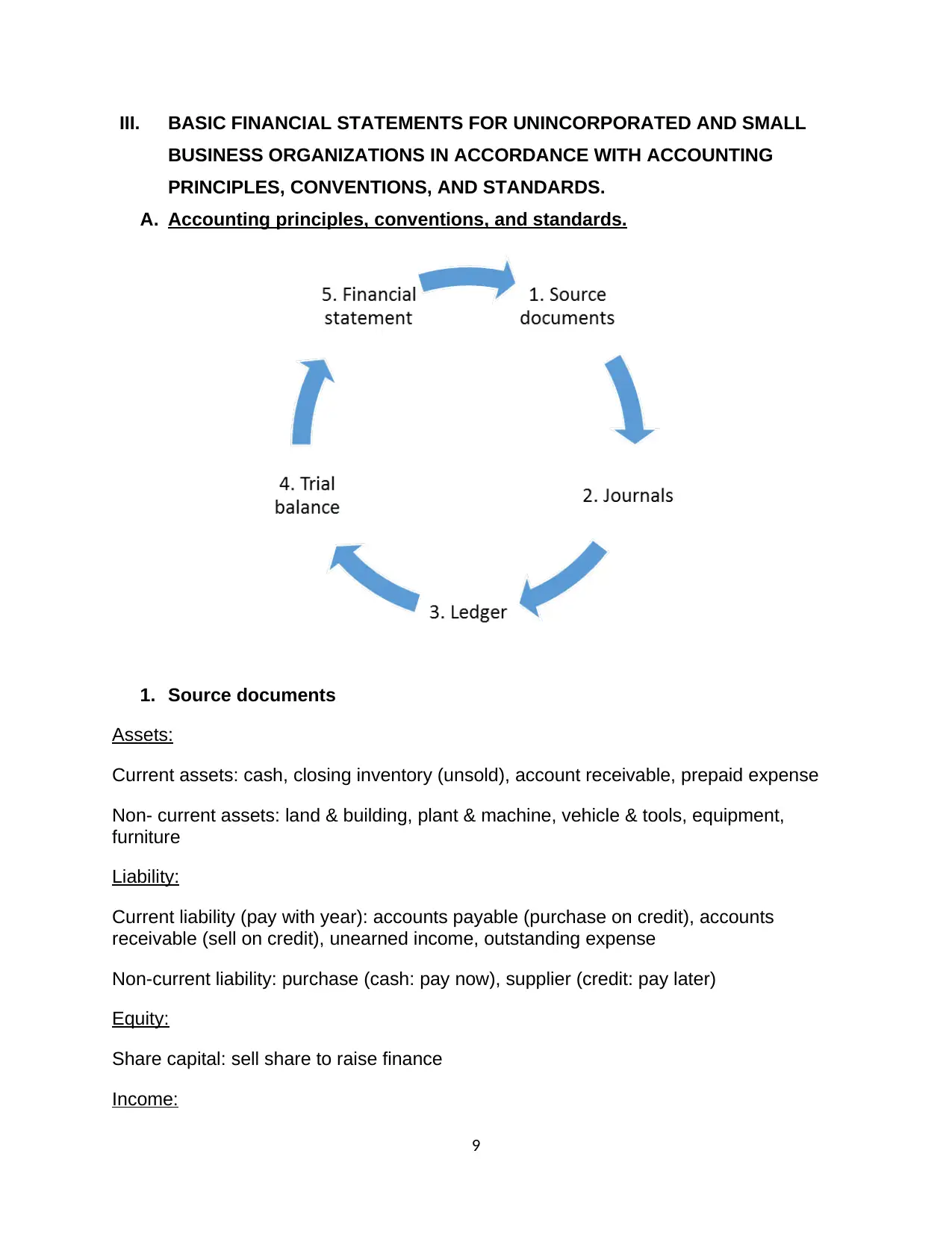

1. Source documents

Assets:

Current assets: cash, closing inventory (unsold), account receivable, prepaid expense

Non- current assets: land & building, plant & machine, vehicle & tools, equipment,

furniture

Liability:

Current liability (pay with year): accounts payable (purchase on credit), accounts

receivable (sell on credit), unearned income, outstanding expense

Non-current liability: purchase (cash: pay now), supplier (credit: pay later)

Equity:

Share capital: sell share to raise finance

Income:

9

BUSINESS ORGANIZATIONS IN ACCORDANCE WITH ACCOUNTING

PRINCIPLES, CONVENTIONS, AND STANDARDS.

A. Accounting principles, conventions, and standards.

1. Source documents

Assets:

Current assets: cash, closing inventory (unsold), account receivable, prepaid expense

Non- current assets: land & building, plant & machine, vehicle & tools, equipment,

furniture

Liability:

Current liability (pay with year): accounts payable (purchase on credit), accounts

receivable (sell on credit), unearned income, outstanding expense

Non-current liability: purchase (cash: pay now), supplier (credit: pay later)

Equity:

Share capital: sell share to raise finance

Income:

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Selling product & service for revenue, rent income, interest income, dividend income,

etc.

Expense:

Material, labor, marketing, electricity, water, tax, interest expense, dividend expense,

etc.

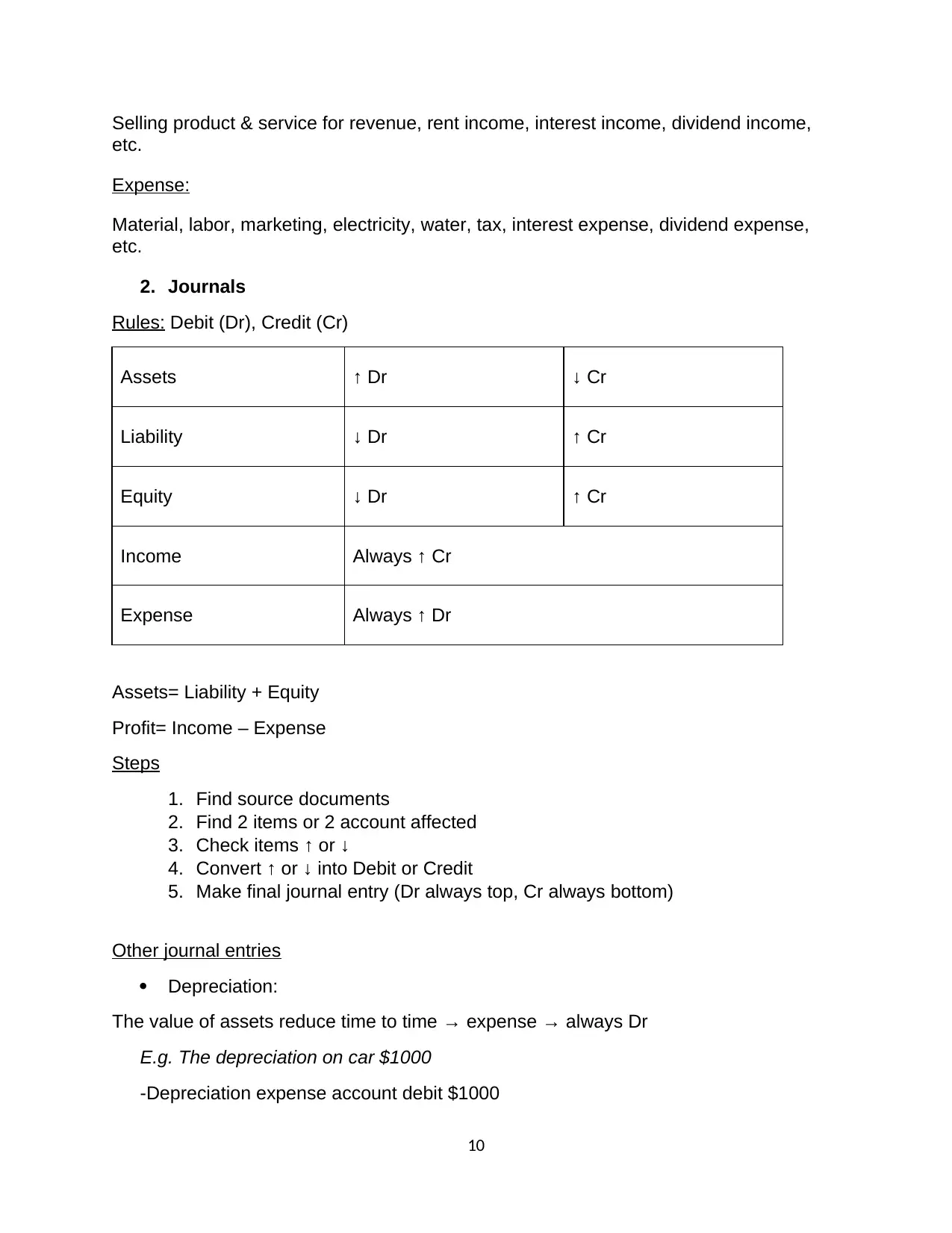

2. Journals

Rules: Debit (Dr), Credit (Cr)

Assets ↑ Dr ↓ Cr

Liability ↓ Dr ↑ Cr

Equity ↓ Dr ↑ Cr

Income Always ↑ Cr

Expense Always ↑ Dr

Assets= Liability + Equity

Profit= Income – Expense

Steps

1. Find source documents

2. Find 2 items or 2 account affected

3. Check items ↑ or ↓

4. Convert ↑ or ↓ into Debit or Credit

5. Make final journal entry (Dr always top, Cr always bottom)

Other journal entries

Depreciation:

The value of assets reduce time to time → expense → always Dr

E.g. The depreciation on car $1000

-Depreciation expense account debit $1000

10

etc.

Expense:

Material, labor, marketing, electricity, water, tax, interest expense, dividend expense,

etc.

2. Journals

Rules: Debit (Dr), Credit (Cr)

Assets ↑ Dr ↓ Cr

Liability ↓ Dr ↑ Cr

Equity ↓ Dr ↑ Cr

Income Always ↑ Cr

Expense Always ↑ Dr

Assets= Liability + Equity

Profit= Income – Expense

Steps

1. Find source documents

2. Find 2 items or 2 account affected

3. Check items ↑ or ↓

4. Convert ↑ or ↓ into Debit or Credit

5. Make final journal entry (Dr always top, Cr always bottom)

Other journal entries

Depreciation:

The value of assets reduce time to time → expense → always Dr

E.g. The depreciation on car $1000

-Depreciation expense account debit $1000

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

-Car account credit $1000

Bad debts:

When your account receivable don’t turn your money → loss → always Dr

E.g. Account receivable valued $1500 turned to bad debts

-Bad debts account debit $1500

-Account receivable account credit $1500

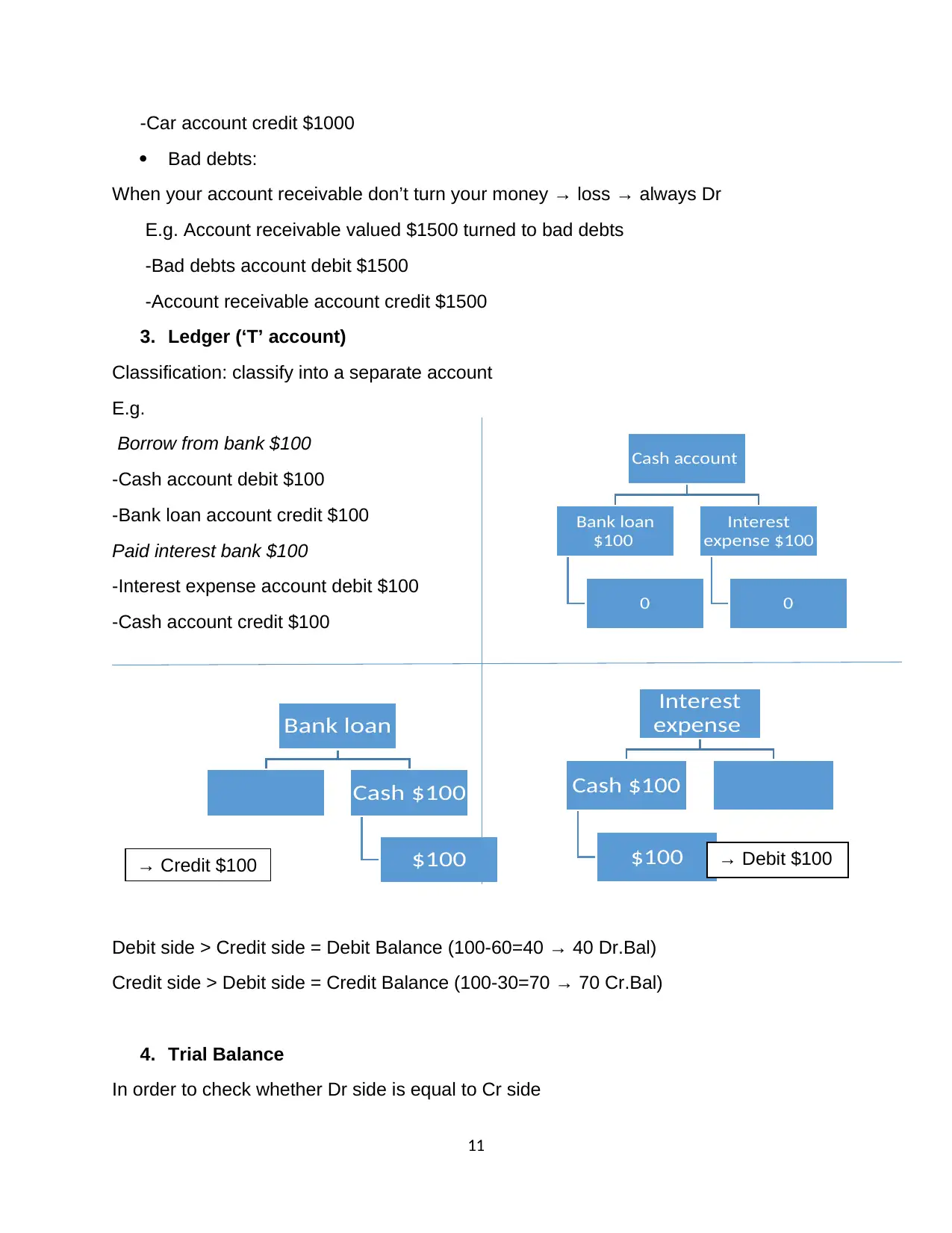

3. Ledger (‘T’ account)

Classification: classify into a separate account

E.g.

Borrow from bank $100

-Cash account debit $100

-Bank loan account credit $100

Paid interest bank $100

-Interest expense account debit $100

-Cash account credit $100

Debit side > Credit side = Debit Balance (100-60=40 → 40 Dr.Bal)

Credit side > Debit side = Credit Balance (100-30=70 → 70 Cr.Bal)

4. Trial Balance

In order to check whether Dr side is equal to Cr side

11

Cash account

Bank loan

$100

0

Interest

expense $100

0

Bank loan

Cash $100

$100

Interest

expense

Cash $100

$100→ Credit $100 → Debit $100

Bad debts:

When your account receivable don’t turn your money → loss → always Dr

E.g. Account receivable valued $1500 turned to bad debts

-Bad debts account debit $1500

-Account receivable account credit $1500

3. Ledger (‘T’ account)

Classification: classify into a separate account

E.g.

Borrow from bank $100

-Cash account debit $100

-Bank loan account credit $100

Paid interest bank $100

-Interest expense account debit $100

-Cash account credit $100

Debit side > Credit side = Debit Balance (100-60=40 → 40 Dr.Bal)

Credit side > Debit side = Credit Balance (100-30=70 → 70 Cr.Bal)

4. Trial Balance

In order to check whether Dr side is equal to Cr side

11

Cash account

Bank loan

$100

0

Interest

expense $100

0

Bank loan

Cash $100

$100

Interest

expense

Cash $100

$100→ Credit $100 → Debit $100

E.g.

Dr Cr

Cash 0 0

Bank loan 0 100

Interest expense 100 0

TOTAL 100 100

If the trial balance is an equal → right

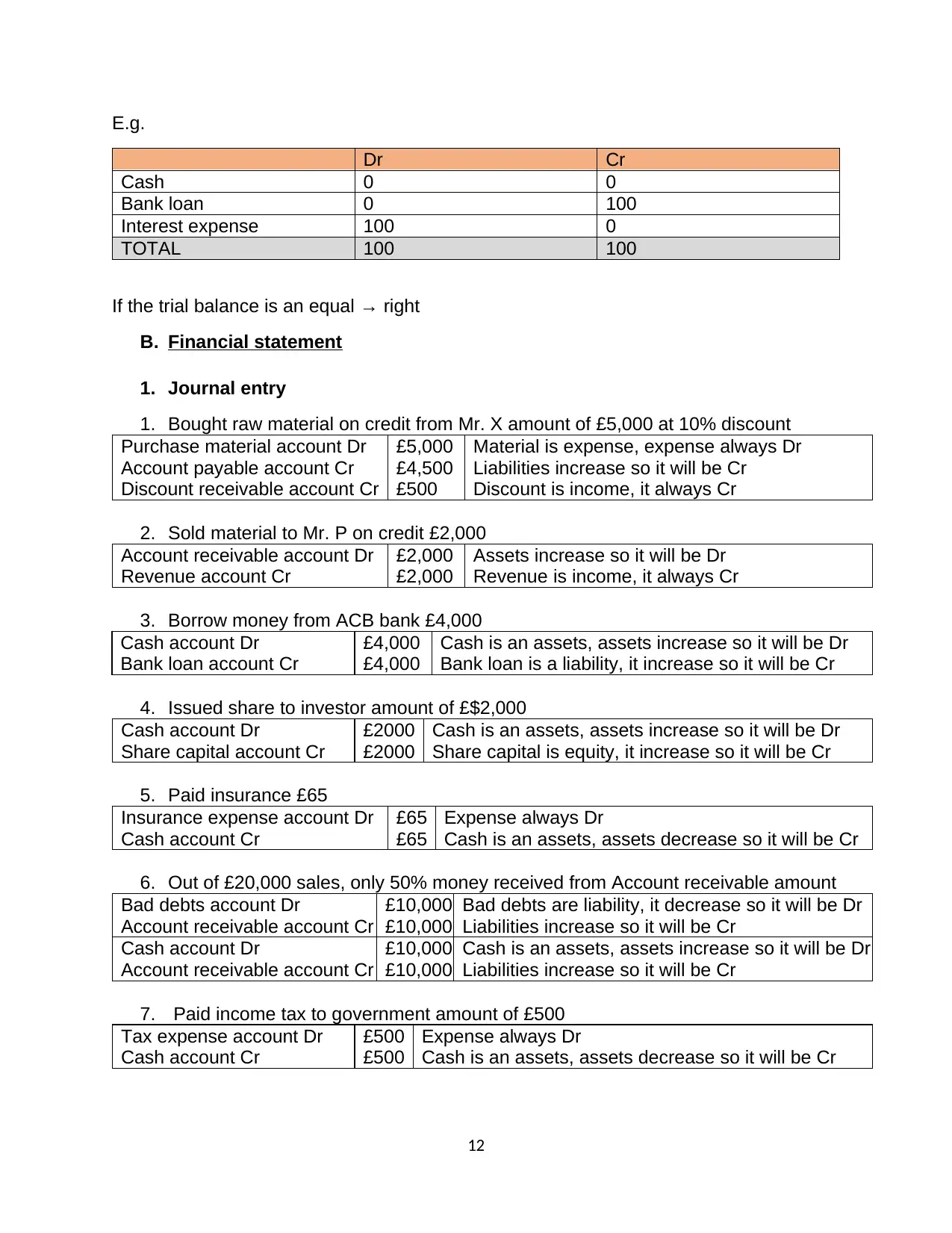

B. Financial statement

1. Journal entry

1. Bought raw material on credit from Mr. X amount of £5,000 at 10% discount

Purchase material account Dr £5,000 Material is expense, expense always Dr

Account payable account Cr £4,500 Liabilities increase so it will be Cr

Discount receivable account Cr £500 Discount is income, it always Cr

2. Sold material to Mr. P on credit £2,000

Account receivable account Dr £2,000 Assets increase so it will be Dr

Revenue account Cr £2,000 Revenue is income, it always Cr

3. Borrow money from ACB bank £4,000

Cash account Dr £4,000 Cash is an assets, assets increase so it will be Dr

Bank loan account Cr £4,000 Bank loan is a liability, it increase so it will be Cr

4. Issued share to investor amount of £$2,000

Cash account Dr £2000 Cash is an assets, assets increase so it will be Dr

Share capital account Cr £2000 Share capital is equity, it increase so it will be Cr

5. Paid insurance £65

Insurance expense account Dr £65 Expense always Dr

Cash account Cr £65 Cash is an assets, assets decrease so it will be Cr

6. Out of £20,000 sales, only 50% money received from Account receivable amount

Bad debts account Dr £10,000 Bad debts are liability, it decrease so it will be Dr

Account receivable account Cr £10,000 Liabilities increase so it will be Cr

Cash account Dr £10,000 Cash is an assets, assets increase so it will be Dr

Account receivable account Cr £10,000 Liabilities increase so it will be Cr

7. Paid income tax to government amount of £500

Tax expense account Dr £500 Expense always Dr

Cash account Cr £500 Cash is an assets, assets decrease so it will be Cr

12

Dr Cr

Cash 0 0

Bank loan 0 100

Interest expense 100 0

TOTAL 100 100

If the trial balance is an equal → right

B. Financial statement

1. Journal entry

1. Bought raw material on credit from Mr. X amount of £5,000 at 10% discount

Purchase material account Dr £5,000 Material is expense, expense always Dr

Account payable account Cr £4,500 Liabilities increase so it will be Cr

Discount receivable account Cr £500 Discount is income, it always Cr

2. Sold material to Mr. P on credit £2,000

Account receivable account Dr £2,000 Assets increase so it will be Dr

Revenue account Cr £2,000 Revenue is income, it always Cr

3. Borrow money from ACB bank £4,000

Cash account Dr £4,000 Cash is an assets, assets increase so it will be Dr

Bank loan account Cr £4,000 Bank loan is a liability, it increase so it will be Cr

4. Issued share to investor amount of £$2,000

Cash account Dr £2000 Cash is an assets, assets increase so it will be Dr

Share capital account Cr £2000 Share capital is equity, it increase so it will be Cr

5. Paid insurance £65

Insurance expense account Dr £65 Expense always Dr

Cash account Cr £65 Cash is an assets, assets decrease so it will be Cr

6. Out of £20,000 sales, only 50% money received from Account receivable amount

Bad debts account Dr £10,000 Bad debts are liability, it decrease so it will be Dr

Account receivable account Cr £10,000 Liabilities increase so it will be Cr

Cash account Dr £10,000 Cash is an assets, assets increase so it will be Dr

Account receivable account Cr £10,000 Liabilities increase so it will be Cr

7. Paid income tax to government amount of £500

Tax expense account Dr £500 Expense always Dr

Cash account Cr £500 Cash is an assets, assets decrease so it will be Cr

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.