Financial Statement Analysis: Accounting for Managers Assignment

VerifiedAdded on 2022/10/02

|9

|1079

|39

Homework Assignment

AI Summary

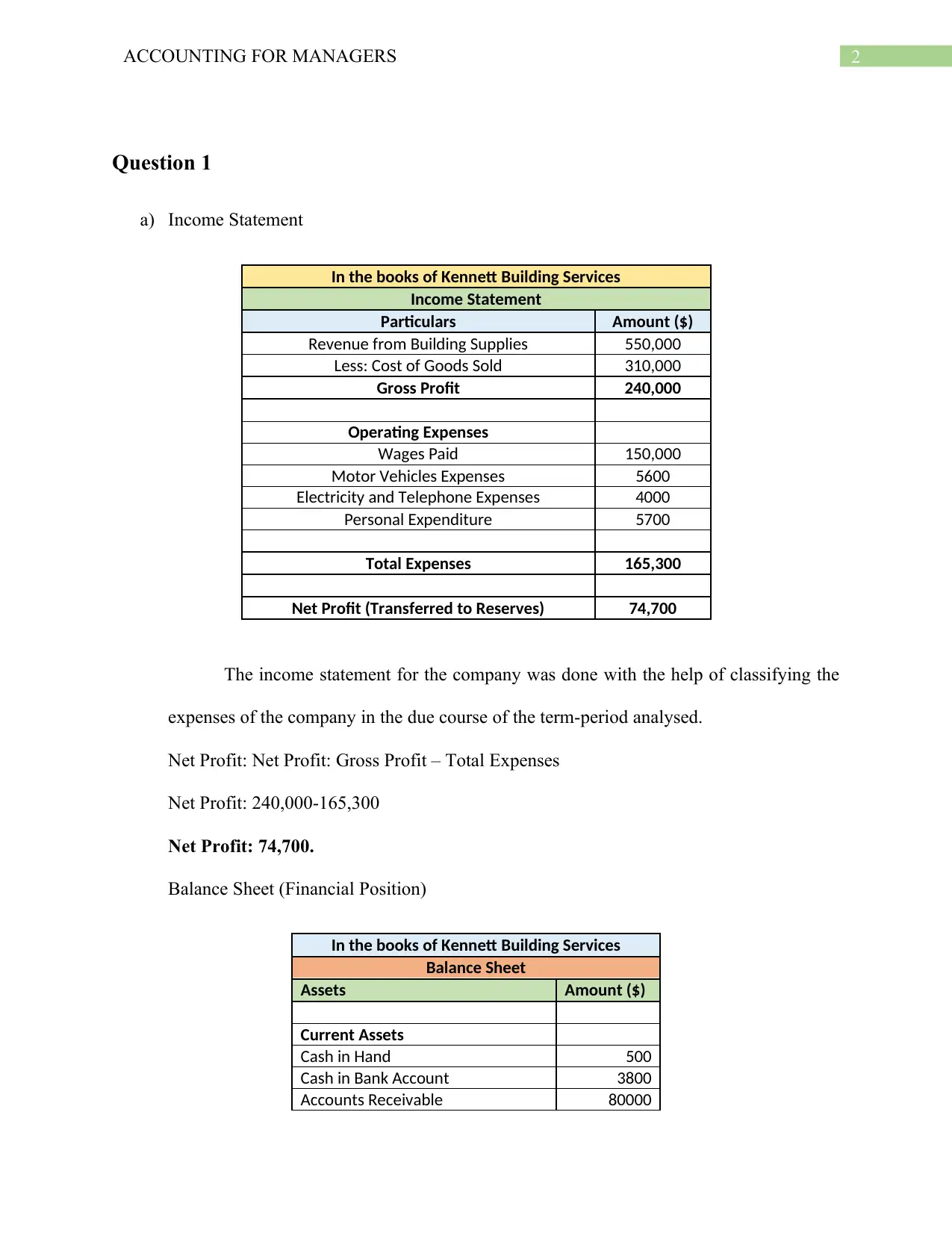

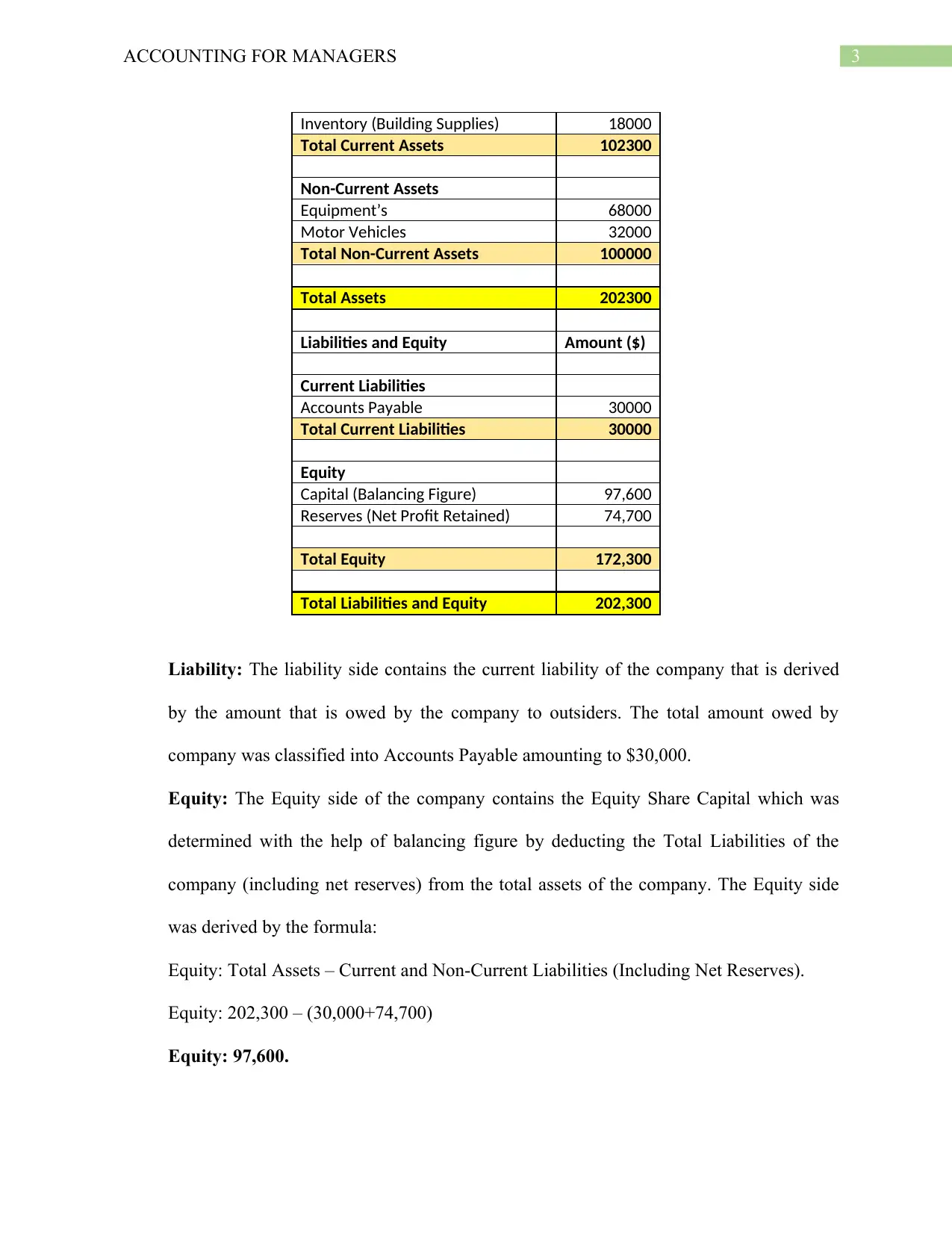

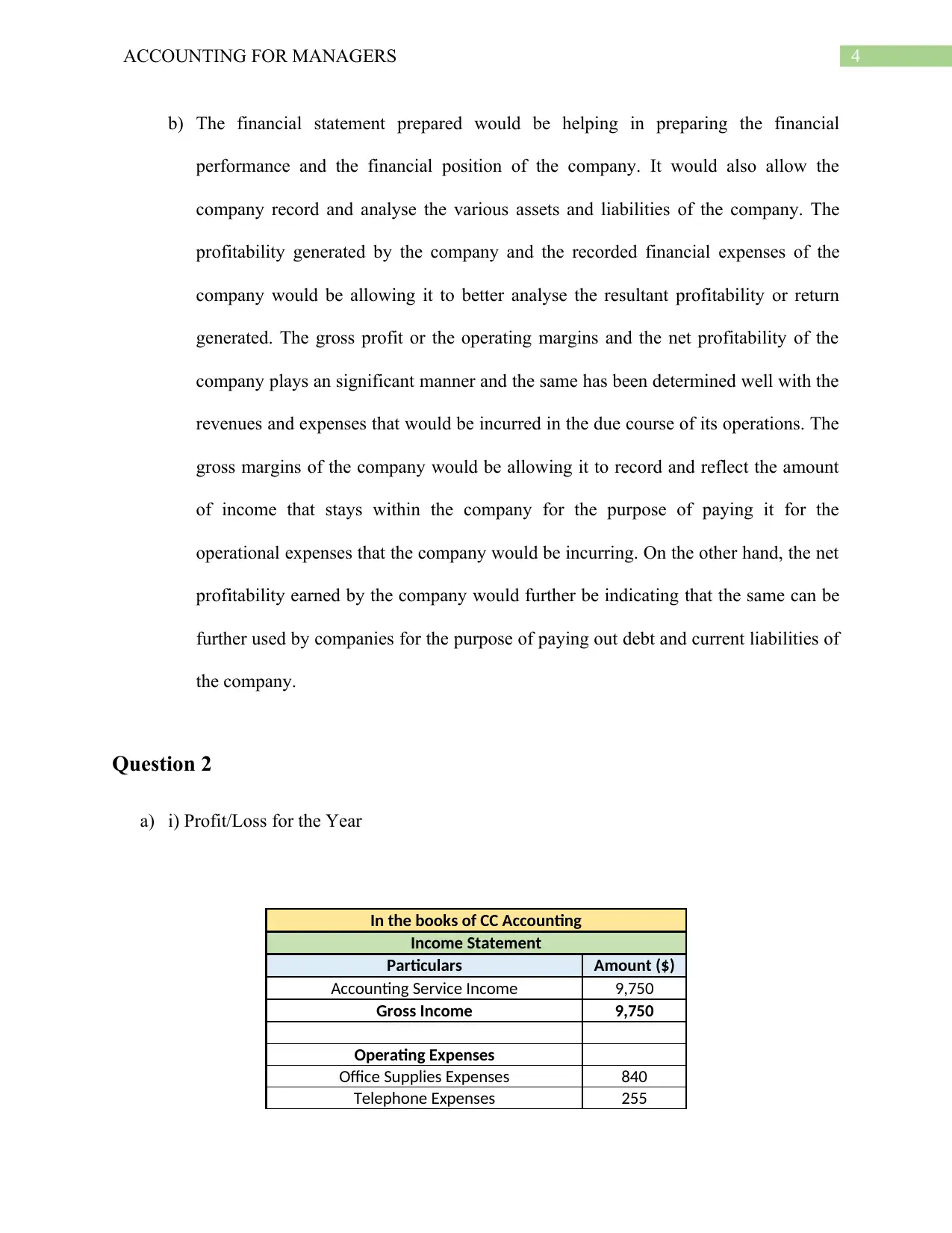

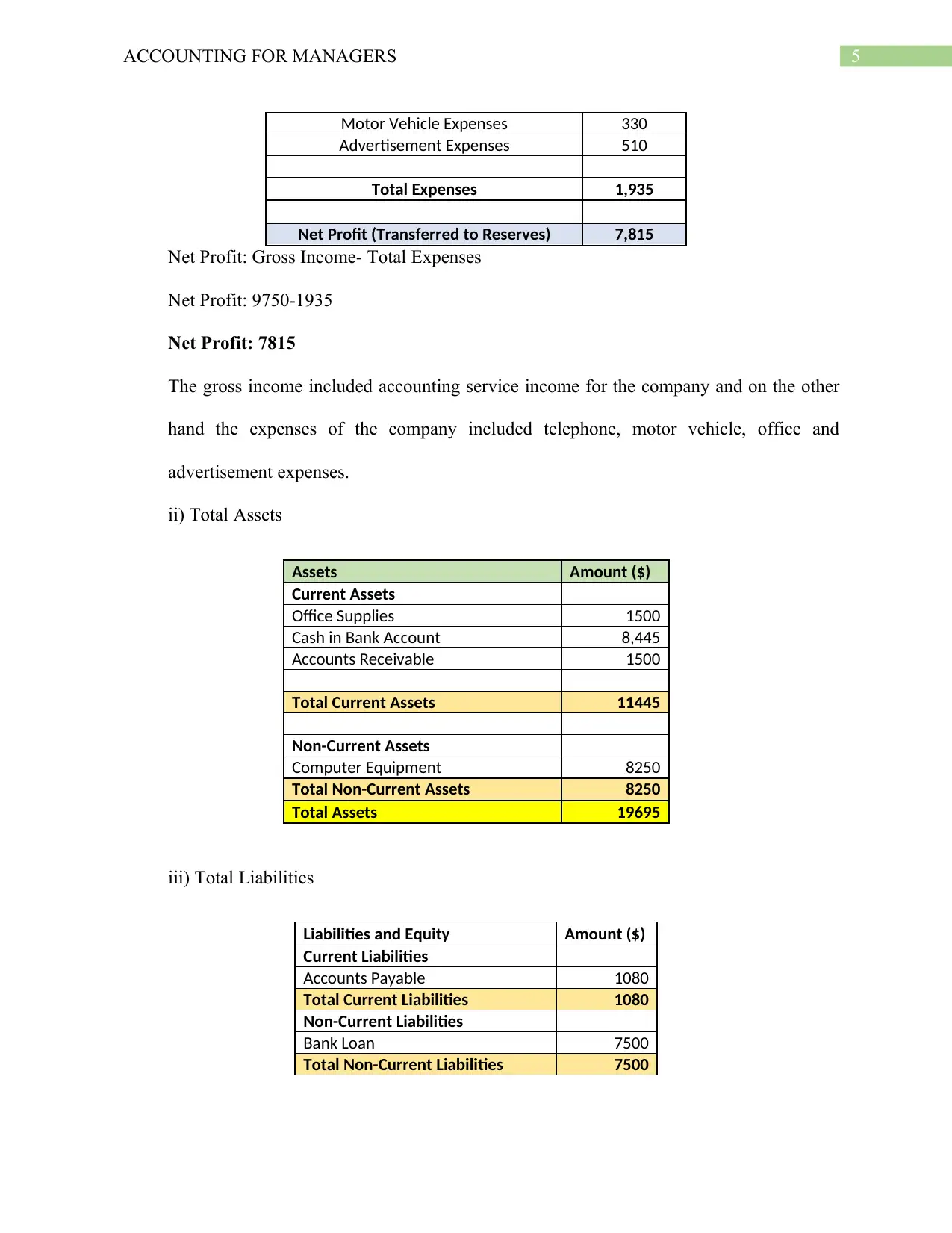

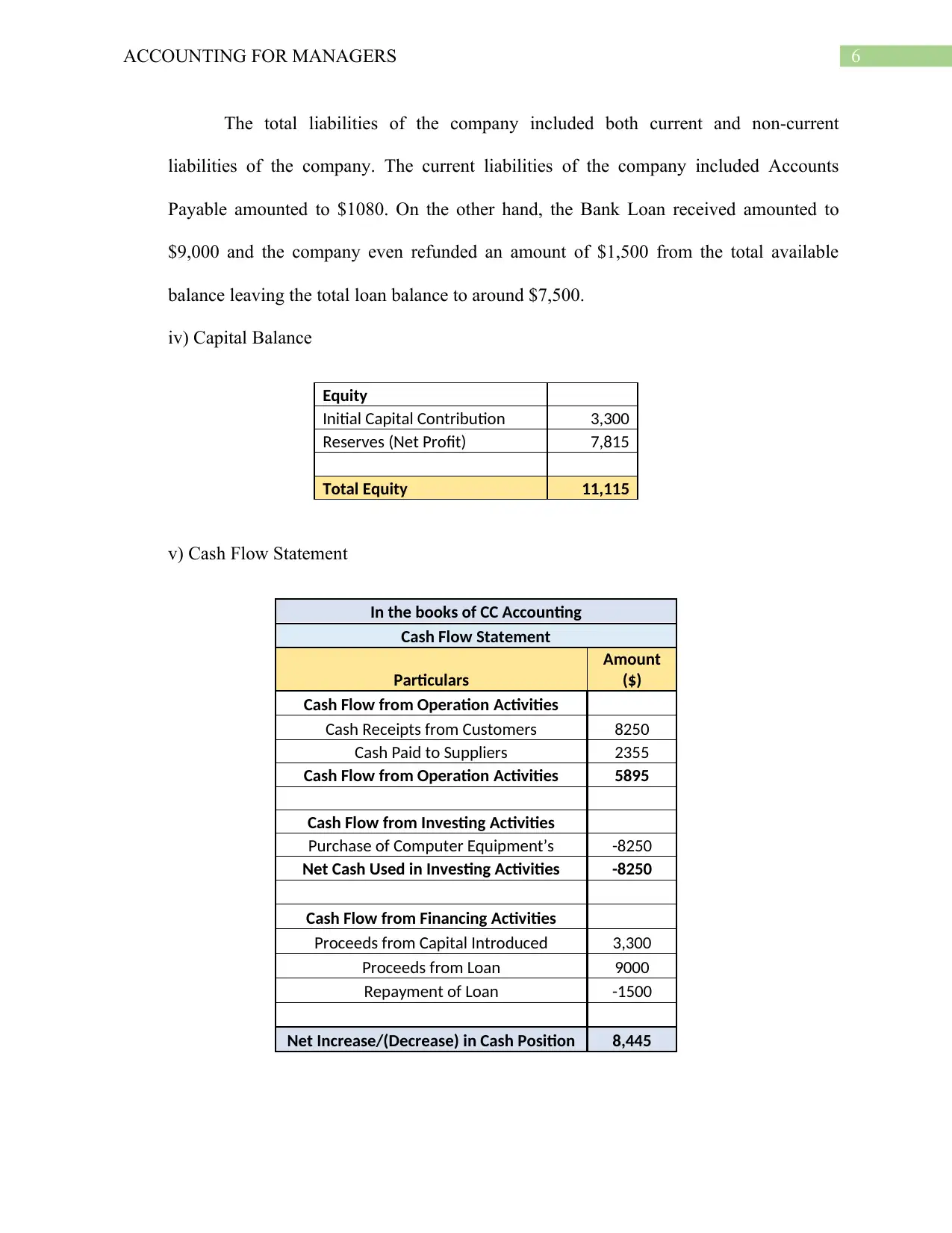

This assignment solution provides a comprehensive analysis of financial statements for an Accounting for Managers course. The document includes the preparation of an income statement and balance sheet for Kennett Building Services, detailing revenue, expenses, assets, liabilities, and equity. It also presents a second question, which includes an income statement, a balance sheet, a cash flow statement, and an analysis of how a client withdrawal would impact the financial statements. The assignment covers key accounting concepts such as gross profit, net profit, current and non-current assets and liabilities, and equity. The solution demonstrates the application of accounting principles to real-world business scenarios and provides insights into financial performance and position, offering a practical guide for students studying accounting.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.