University Accounting Assignment: Financial Reporting and Analysis

VerifiedAdded on 2021/04/17

|18

|2488

|43

Homework Assignment

AI Summary

This accounting assignment solution covers a range of topics, including plagiarism, spreadsheet views (normal and formula), website resources for accounting, and the Association of Accounting Technicians (AAT). It explores the impact of technology in accounting, using computers for data saving, protection, emails, and accessibility while also noting the risks of hacking and lack of internal control. The assignment analyzes the ABC Learning case, highlighting financial reporting, ethical issues, and the importance of sound accounting principles. It further discusses PALER segregation, owner's drawings calculation, normal debit and credit balance accounts, and adjusting entries (accrued revenue, expenses, deferred revenue, and expenses). Additionally, it defines current and non-current liabilities with examples. The document provides detailed answers and explanations for each question, offering a comprehensive overview of fundamental accounting concepts and their practical application.

Running head: ACCOUNTING

Accounting

Name of the Student:

Name of the University:

Author’s Note:

Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING

Answer to Question 1:

Plagiarism can be defined as the as a form of academic dishonesty or a breach of the

required ethics. The activities that can be defined as a form of plagiarism are as follows:

Copying of information

Presentation of an idea that previously belonged to someone else without the providence

of required referencing

Paraphrasing the written work of another individual

Providence of information that is incorrect or irrelevant in nature and has been executed

with the intention of cheating

Collusion

Plagiarism or collusion is certainly unfair to honest students. This is because plagiarism

enables the unworthy students to get results that they do not deserve. Moreover, a particular

student committing plagiarism, sources these types of documents from experts who help them to

achieve a higher grade thus, resulting in achievement of the academic remarks, which is not fair

to the students who follow an honest procedure to carry out the assignment work (Angélil-Carter,

2014).

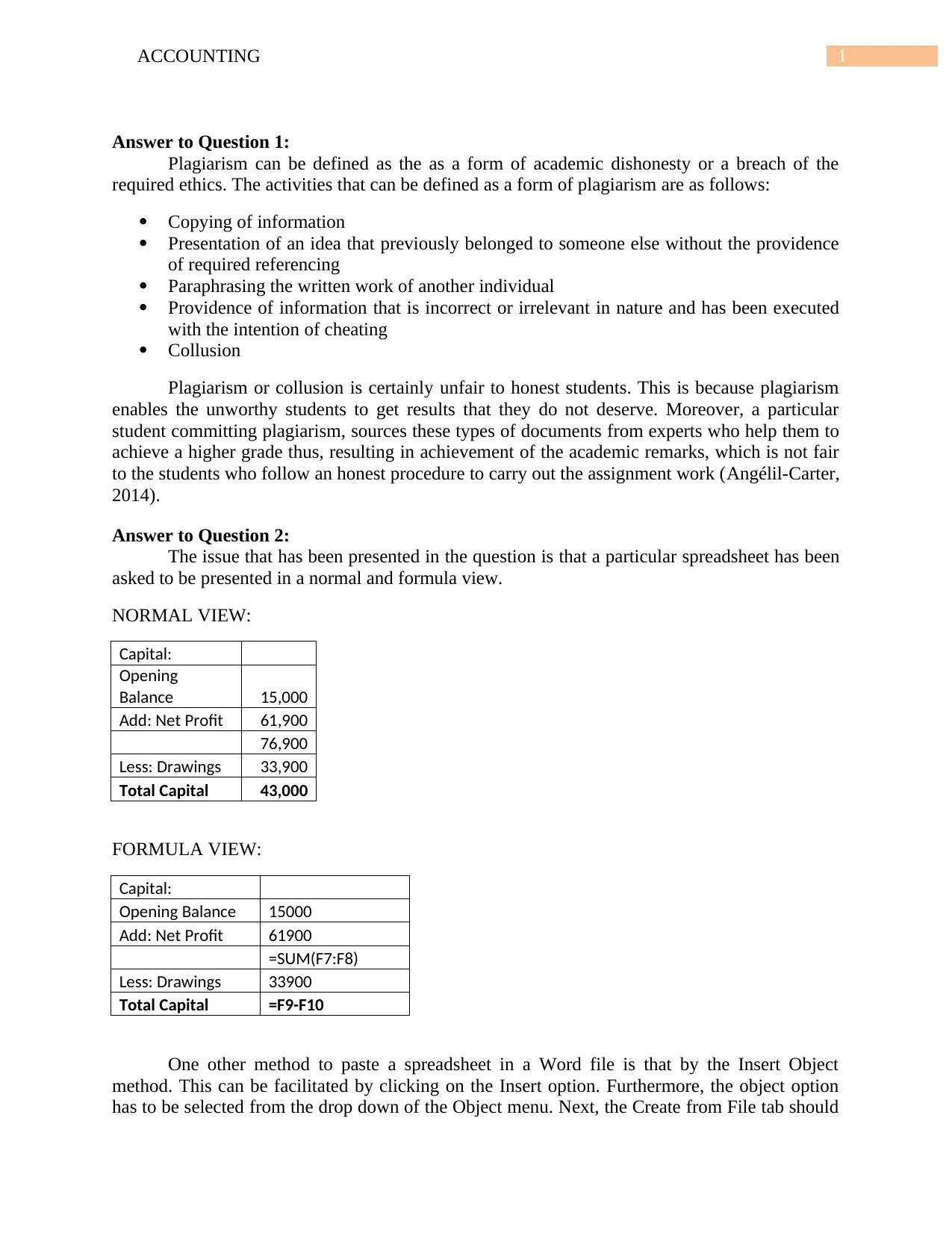

Answer to Question 2:

The issue that has been presented in the question is that a particular spreadsheet has been

asked to be presented in a normal and formula view.

NORMAL VIEW:

Capital:

Opening

Balance 15,000

Add: Net Profit 61,900

76,900

Less: Drawings 33,900

Total Capital 43,000

FORMULA VIEW:

Capital:

Opening Balance 15000

Add: Net Profit 61900

=SUM(F7:F8)

Less: Drawings 33900

Total Capital =F9-F10

One other method to paste a spreadsheet in a Word file is that by the Insert Object

method. This can be facilitated by clicking on the Insert option. Furthermore, the object option

has to be selected from the drop down of the Object menu. Next, the Create from File tab should

Answer to Question 1:

Plagiarism can be defined as the as a form of academic dishonesty or a breach of the

required ethics. The activities that can be defined as a form of plagiarism are as follows:

Copying of information

Presentation of an idea that previously belonged to someone else without the providence

of required referencing

Paraphrasing the written work of another individual

Providence of information that is incorrect or irrelevant in nature and has been executed

with the intention of cheating

Collusion

Plagiarism or collusion is certainly unfair to honest students. This is because plagiarism

enables the unworthy students to get results that they do not deserve. Moreover, a particular

student committing plagiarism, sources these types of documents from experts who help them to

achieve a higher grade thus, resulting in achievement of the academic remarks, which is not fair

to the students who follow an honest procedure to carry out the assignment work (Angélil-Carter,

2014).

Answer to Question 2:

The issue that has been presented in the question is that a particular spreadsheet has been

asked to be presented in a normal and formula view.

NORMAL VIEW:

Capital:

Opening

Balance 15,000

Add: Net Profit 61,900

76,900

Less: Drawings 33,900

Total Capital 43,000

FORMULA VIEW:

Capital:

Opening Balance 15000

Add: Net Profit 61900

=SUM(F7:F8)

Less: Drawings 33900

Total Capital =F9-F10

One other method to paste a spreadsheet in a Word file is that by the Insert Object

method. This can be facilitated by clicking on the Insert option. Furthermore, the object option

has to be selected from the drop down of the Object menu. Next, the Create from File tab should

2ACCOUNTING

be clicked on. Then the created spreadsheet has to be linked with the word document. It must be

noted here that this particular method will facilitate the linking of the complete set of contents of

the spreadsheet into Word instead of a portion of the spreadsheet.

Answer to Question 3:

The issue that has been presented in the question is that six relevant websites have been

asked to list and identify along with their URLs. These websites are as follows:

Accounting Coach - The particular website Accounting Coach had been established in the

financial year of 2003 for permitting the students, bookkeepers and small business

owners for the purpose of improving their accounting skills.

URL - https://www.accountingcoach.com/

Sleeter – The particular website of Sleeter provides educational resources for the public

certified accountants and small business owners.

URL - https://www.accountexnetwork.com/

Skoda Minotti Blog – This particular website aims to provide accounting services to their

customers in order to facilitate their growth and prosper.

URL - https://skodaminotti.com/blog/blog-content-gone-green/

Accounting for management - This particular website aims to present an overview into

the different accounting situations that a particular business firm faces.

URL - https://www.accountingformanagement.org/

Evergreen Small Business – This particular website aims to provide an overview into the

situations that a small business owner might face. This website fundamentally provides

the required advice to the small business owners in regards to financial management of

the firm.

URL - https://evergreensmallbusiness.com/

Investopedia – This particular website provides an overview into the different accounting

concepts that are utilized by the small business owners.

URL - https://www.investopedia.com/

Answer to Question 4:

The Australian professional accounting organization that has been chosen for the purpose

of this study is the Association of Accounting Technicians (AAT). It must be noted here that it is

the largest accounting professional body and provides the required service in the accounting,

finance and bookkeeping sector. This particular accounting professional body results in the

generation of self employed bookkeepers, payroll officers, BAS agents, assistant accountants and

accounting support staff.

The Association of Accounting Technician has been chosen due to the fact that AAT has

been the largest professional body of the country and has displayed dedication and commitment

towards improving the particular profession of accounting and bookkeeping.

Answer to Question 5:

The current trend in the industry has been a huge shift from the manual work force to an

automated work force that has been dominated by the providence of computers. It must be noted

be clicked on. Then the created spreadsheet has to be linked with the word document. It must be

noted here that this particular method will facilitate the linking of the complete set of contents of

the spreadsheet into Word instead of a portion of the spreadsheet.

Answer to Question 3:

The issue that has been presented in the question is that six relevant websites have been

asked to list and identify along with their URLs. These websites are as follows:

Accounting Coach - The particular website Accounting Coach had been established in the

financial year of 2003 for permitting the students, bookkeepers and small business

owners for the purpose of improving their accounting skills.

URL - https://www.accountingcoach.com/

Sleeter – The particular website of Sleeter provides educational resources for the public

certified accountants and small business owners.

URL - https://www.accountexnetwork.com/

Skoda Minotti Blog – This particular website aims to provide accounting services to their

customers in order to facilitate their growth and prosper.

URL - https://skodaminotti.com/blog/blog-content-gone-green/

Accounting for management - This particular website aims to present an overview into

the different accounting situations that a particular business firm faces.

URL - https://www.accountingformanagement.org/

Evergreen Small Business – This particular website aims to provide an overview into the

situations that a small business owner might face. This website fundamentally provides

the required advice to the small business owners in regards to financial management of

the firm.

URL - https://evergreensmallbusiness.com/

Investopedia – This particular website provides an overview into the different accounting

concepts that are utilized by the small business owners.

URL - https://www.investopedia.com/

Answer to Question 4:

The Australian professional accounting organization that has been chosen for the purpose

of this study is the Association of Accounting Technicians (AAT). It must be noted here that it is

the largest accounting professional body and provides the required service in the accounting,

finance and bookkeeping sector. This particular accounting professional body results in the

generation of self employed bookkeepers, payroll officers, BAS agents, assistant accountants and

accounting support staff.

The Association of Accounting Technician has been chosen due to the fact that AAT has

been the largest professional body of the country and has displayed dedication and commitment

towards improving the particular profession of accounting and bookkeeping.

Answer to Question 5:

The current trend in the industry has been a huge shift from the manual work force to an

automated work force that has been dominated by the providence of computers. It must be noted

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING

here that the running of an organization needs computers as the human body needs oxygen. The

workplace in the previous office had been nice and well accommodated. The main function of

the organization had been providing private classes in regards to engineering and management

courses. A network of computers managed all the work in regards to the management and

administration of the institute. The different facilities that have been provided by the network of

computers are as follows:

Data saving – the providence of computers facilitated the input of relevant student

information via the computers of the institute.

Data protection – the data that is being entered into the computers had been successfully

protected. This means that the utilization of proper framework of computers protected the

data by the facilitation of safety portals or passwords.

Emails – the advertisement and the marketing facilities in regards to the educational

institute had been facilitated via emails on the computers.

Accessibility – the aspect of accessibility of the crucial information of the educational

institution had been influenced by the utilization of the computers. This means that the

staff of the organization can get access permitted access to the official documents by just

logging into the computer.

Prone to hacking risks - it must be noted here that the network of computers that had

been used in the educational institute had been exposed to the risk of breach of security as

a proper antivirus software had not been used in the business entity

Lack of internal control – Moreover, the lack of a proper implementation of internal

control for the physical safety of the equipments was another major issue in the previous

work place.

Answer to Question 6:

The issue that has been presented in the question is that the ABC Learning case studies

have been asked to review and analyze. The ABC learning case studies reflect the fact that a

certain company falls only at the moment when the corporate entity ignores the fundamentals of

the sound accounting. The ignoring of the accounting regulations for controlling the financial

accounts of a certain business entity will result in the failure of the firm. ABC learning is a

potential example of a company that had not given the much needed attention to this much

needed truth.

ABC had been founded in the in the financial year of 1988 as a childcare centre. It was in

1996 when ABC managed a number of childcare centres and was a major player in the selected

sector. It was then when the corporate entity decided the fact that it would take the advantage of

expansion and acquired properties in prime locations. By the year of 1999, it had acquired 30

centres. In 2001, ABC had been listed on the Australian Stock Exchange. Post the listing of the

company, the profits that had been acquired by the firm grew exponentially. The last reported

profit acquired by the corporate entity was $143.1 million. The corporate entity at that time

owned a number of 2238 centres in Australia and New Zealand. This was the time when the firm

was overwhelmed by the facility of debt repayments and had been forced to make a sale of 60

percent of total proportions of its US subsidiary and the complete subsidiary in UK. The last

traded price of the firm had been $0.54 that represented a steep fall from the peak value of the

shares that was $8.62. The firm had been finally delisted from the Australian Stock Exchange

and went into receivership. The major reasons that have been specified as the contributing

here that the running of an organization needs computers as the human body needs oxygen. The

workplace in the previous office had been nice and well accommodated. The main function of

the organization had been providing private classes in regards to engineering and management

courses. A network of computers managed all the work in regards to the management and

administration of the institute. The different facilities that have been provided by the network of

computers are as follows:

Data saving – the providence of computers facilitated the input of relevant student

information via the computers of the institute.

Data protection – the data that is being entered into the computers had been successfully

protected. This means that the utilization of proper framework of computers protected the

data by the facilitation of safety portals or passwords.

Emails – the advertisement and the marketing facilities in regards to the educational

institute had been facilitated via emails on the computers.

Accessibility – the aspect of accessibility of the crucial information of the educational

institution had been influenced by the utilization of the computers. This means that the

staff of the organization can get access permitted access to the official documents by just

logging into the computer.

Prone to hacking risks - it must be noted here that the network of computers that had

been used in the educational institute had been exposed to the risk of breach of security as

a proper antivirus software had not been used in the business entity

Lack of internal control – Moreover, the lack of a proper implementation of internal

control for the physical safety of the equipments was another major issue in the previous

work place.

Answer to Question 6:

The issue that has been presented in the question is that the ABC Learning case studies

have been asked to review and analyze. The ABC learning case studies reflect the fact that a

certain company falls only at the moment when the corporate entity ignores the fundamentals of

the sound accounting. The ignoring of the accounting regulations for controlling the financial

accounts of a certain business entity will result in the failure of the firm. ABC learning is a

potential example of a company that had not given the much needed attention to this much

needed truth.

ABC had been founded in the in the financial year of 1988 as a childcare centre. It was in

1996 when ABC managed a number of childcare centres and was a major player in the selected

sector. It was then when the corporate entity decided the fact that it would take the advantage of

expansion and acquired properties in prime locations. By the year of 1999, it had acquired 30

centres. In 2001, ABC had been listed on the Australian Stock Exchange. Post the listing of the

company, the profits that had been acquired by the firm grew exponentially. The last reported

profit acquired by the corporate entity was $143.1 million. The corporate entity at that time

owned a number of 2238 centres in Australia and New Zealand. This was the time when the firm

was overwhelmed by the facility of debt repayments and had been forced to make a sale of 60

percent of total proportions of its US subsidiary and the complete subsidiary in UK. The last

traded price of the firm had been $0.54 that represented a steep fall from the peak value of the

shares that was $8.62. The firm had been finally delisted from the Australian Stock Exchange

and went into receivership. The major reasons that have been specified as the contributing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING

factors for the delisting of the company are faulty business model of the organization, bad

acquisitions, ignoring of the accounting principles established by the regulatory bodies, a

worsened debt position of the company and weak operating cash flow (Laskov, 2014).

The major financial reports that are utilized by the companies as mandated by the

accounting regulatory bodies like AASB and GAAP are as follows:

The first major financial report that is utilized by the corporate entities for the purpose of

reflecting the financial position of the corporate entity whose financial report is prepared

is the statement of changes in equity

Next, the second major financial report that is prepared is the cash flow statement

Thirdly, the income statement is prepared

Lastly, the major financial report that is finally prepared is the balance sheet of the firm

Objectives:

Statement of changes in equity – the statement of the changes in equity reflects the

changes in the owner’s equity over the accounting period by revealing the changes in the

reserves that comprises of the shareholder’s equity.

Cash flow statement – the cash flow statement represents the total amount of money that

is flowing in and out of business over a stipulated time period

Income statement - the income statement reflects the net profit that has been incurred by

the firm for an accounting year

Balance sheet – the balance sheet of the firm is the most essential financial report that

reflects the financial and the liquidity position of the firm. Moreover, this particular

financial statement reflects the essentialities of a business firm like the current assets and

the fixed assets as well as the current liabilities as well as the noncurrent liabilities of the

business entity

The three ethical issues from the case study are as follows:

The firm has been completely dependent on the aspect of profitability

The audit team had not been competent enough in their practices

The accounting principles had been intentionally ignored in order to highlight the

profitability of the firm

Answer to Question 7:

Answer A:

PALER is a segregation technique that is utilized for carrying out the segregation of the

different accounts. PALER stands for proprietorship, assets, liabilities, expenses and revenue.

This particular technique is utilized by the accountants for simplifying a range of financial

accounts.

factors for the delisting of the company are faulty business model of the organization, bad

acquisitions, ignoring of the accounting principles established by the regulatory bodies, a

worsened debt position of the company and weak operating cash flow (Laskov, 2014).

The major financial reports that are utilized by the companies as mandated by the

accounting regulatory bodies like AASB and GAAP are as follows:

The first major financial report that is utilized by the corporate entities for the purpose of

reflecting the financial position of the corporate entity whose financial report is prepared

is the statement of changes in equity

Next, the second major financial report that is prepared is the cash flow statement

Thirdly, the income statement is prepared

Lastly, the major financial report that is finally prepared is the balance sheet of the firm

Objectives:

Statement of changes in equity – the statement of the changes in equity reflects the

changes in the owner’s equity over the accounting period by revealing the changes in the

reserves that comprises of the shareholder’s equity.

Cash flow statement – the cash flow statement represents the total amount of money that

is flowing in and out of business over a stipulated time period

Income statement - the income statement reflects the net profit that has been incurred by

the firm for an accounting year

Balance sheet – the balance sheet of the firm is the most essential financial report that

reflects the financial and the liquidity position of the firm. Moreover, this particular

financial statement reflects the essentialities of a business firm like the current assets and

the fixed assets as well as the current liabilities as well as the noncurrent liabilities of the

business entity

The three ethical issues from the case study are as follows:

The firm has been completely dependent on the aspect of profitability

The audit team had not been competent enough in their practices

The accounting principles had been intentionally ignored in order to highlight the

profitability of the firm

Answer to Question 7:

Answer A:

PALER is a segregation technique that is utilized for carrying out the segregation of the

different accounts. PALER stands for proprietorship, assets, liabilities, expenses and revenue.

This particular technique is utilized by the accountants for simplifying a range of financial

accounts.

5ACCOUNTING

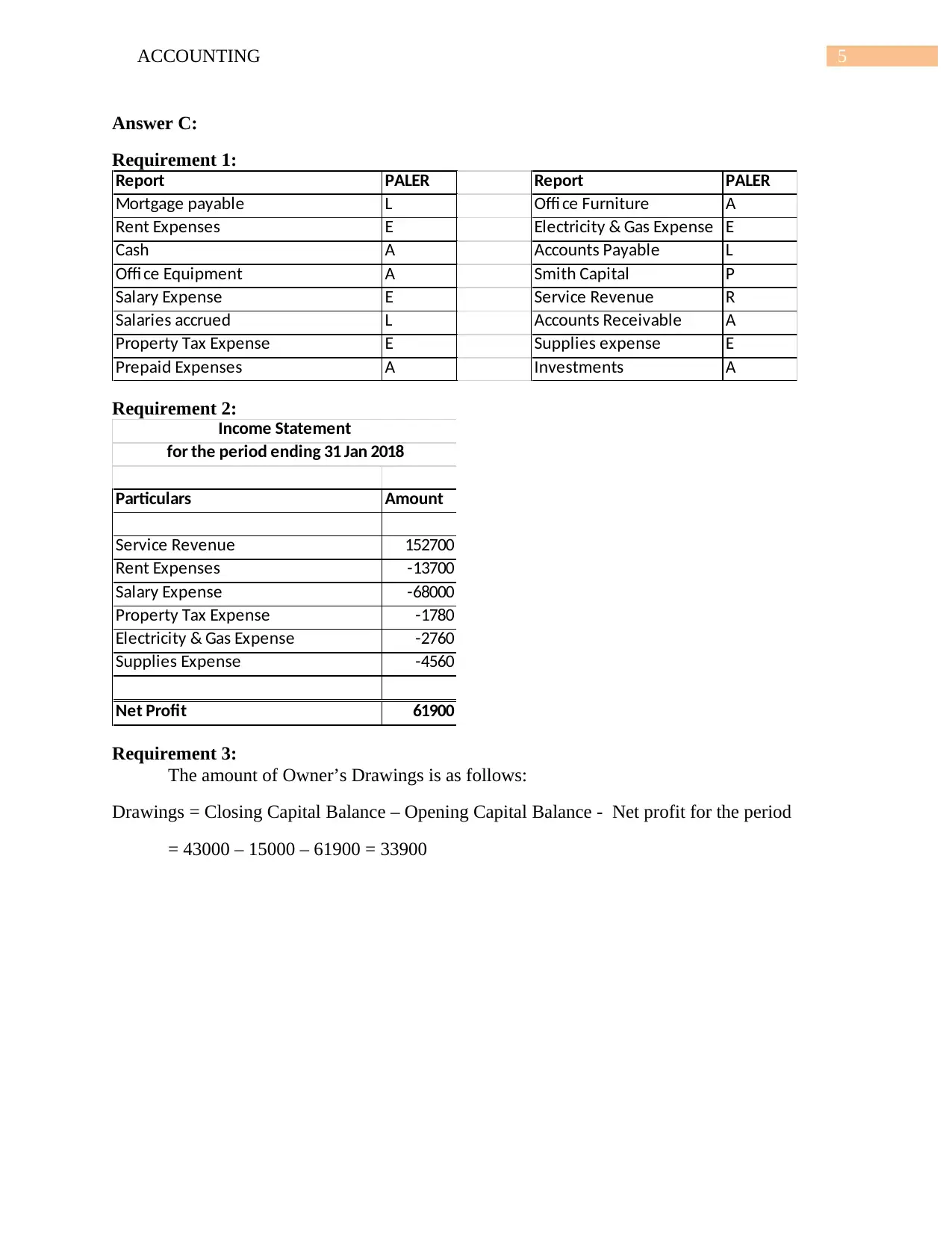

Answer C:

Requirement 1:

Report PALER Report PALER

Mortgage payable L Offi ce Furniture A

Rent Expenses E Electricity & Gas Expense E

Cash A Accounts Payable L

Offi ce Equipment A Smith Capital P

Salary Expense E Service Revenue R

Salaries accrued L Accounts Receivable A

Property Tax Expense E Supplies expense E

Prepaid Expenses A Investments A

Requirement 2:

Particulars Amount

Service Revenue 152700

Rent Expenses -13700

Salary Expense -68000

Property Tax Expense -1780

Electricity & Gas Expense -2760

Supplies Expense -4560

Net Profit 61900

Income Statement

for the period ending 31 Jan 2018

Requirement 3:

The amount of Owner’s Drawings is as follows:

Drawings = Closing Capital Balance – Opening Capital Balance - Net profit for the period

= 43000 – 15000 – 61900 = 33900

Answer C:

Requirement 1:

Report PALER Report PALER

Mortgage payable L Offi ce Furniture A

Rent Expenses E Electricity & Gas Expense E

Cash A Accounts Payable L

Offi ce Equipment A Smith Capital P

Salary Expense E Service Revenue R

Salaries accrued L Accounts Receivable A

Property Tax Expense E Supplies expense E

Prepaid Expenses A Investments A

Requirement 2:

Particulars Amount

Service Revenue 152700

Rent Expenses -13700

Salary Expense -68000

Property Tax Expense -1780

Electricity & Gas Expense -2760

Supplies Expense -4560

Net Profit 61900

Income Statement

for the period ending 31 Jan 2018

Requirement 3:

The amount of Owner’s Drawings is as follows:

Drawings = Closing Capital Balance – Opening Capital Balance - Net profit for the period

= 43000 – 15000 – 61900 = 33900

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING

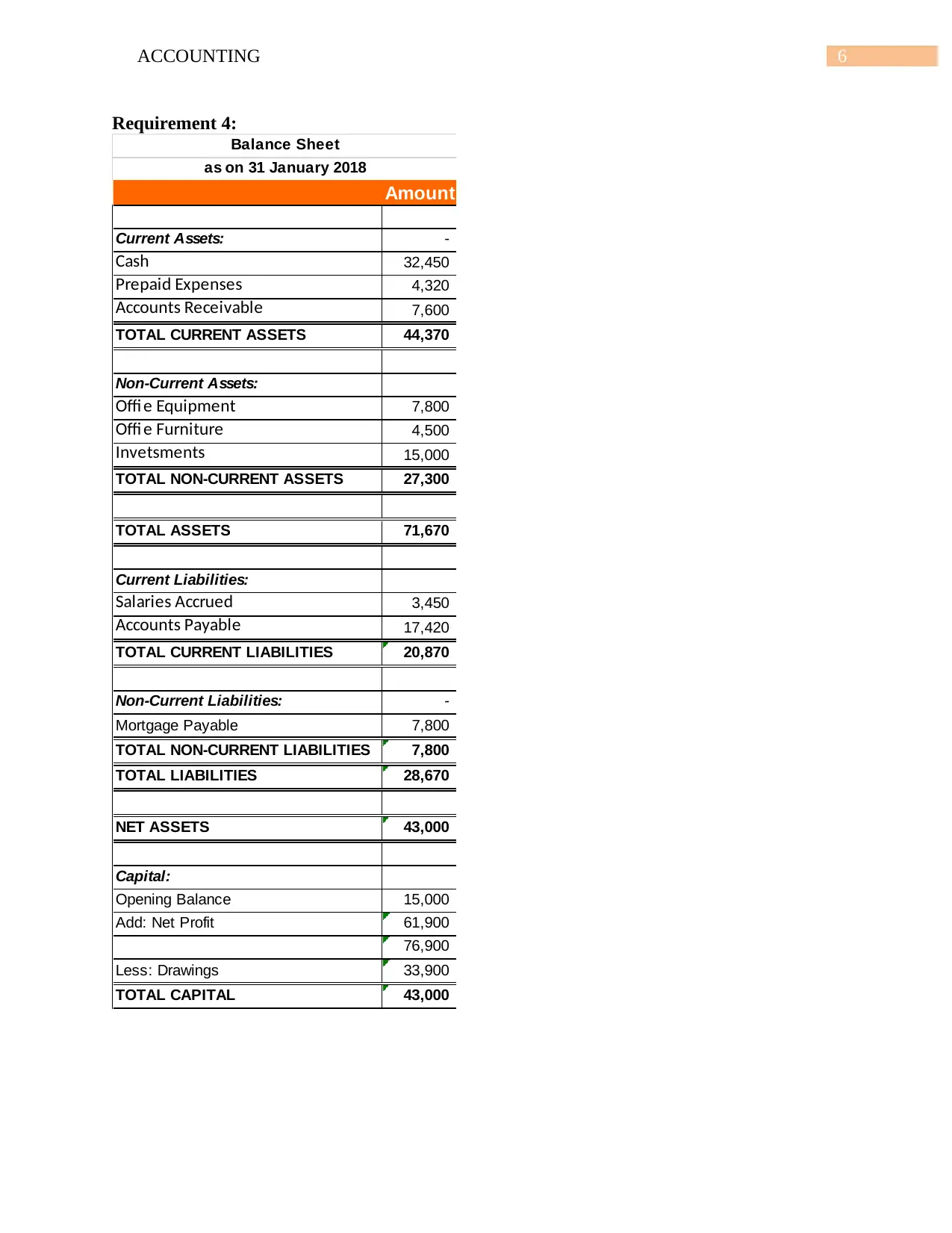

Requirement 4:

Amount

Current Assets: -

Cash 32,450

Prepaid Expenses 4,320

Accounts Receivable 7,600

TOTAL CURRENT ASSETS 44,370

Non-Current Assets:

Offi e Equipment 7,800

Offi e Furniture 4,500

Invetsments 15,000

TOTAL NON-CURRENT ASSETS 27,300

TOTAL ASSETS 71,670

Current Liabilities:

Salaries Accrued 3,450

Accounts Payable 17,420

TOTAL CURRENT LIABILITIES 20,870

Non-Current Liabilities: -

Mortgage Payable 7,800

TOTAL NON-CURRENT LIABILITIES 7,800

TOTAL LIABILITIES 28,670

NET ASSETS 43,000

Capital:

Opening Balance 15,000

Add: Net Profit 61,900

76,900

Less: Drawings 33,900

TOTAL CAPITAL 43,000

Balance Sheet

as on 31 January 2018

Requirement 4:

Amount

Current Assets: -

Cash 32,450

Prepaid Expenses 4,320

Accounts Receivable 7,600

TOTAL CURRENT ASSETS 44,370

Non-Current Assets:

Offi e Equipment 7,800

Offi e Furniture 4,500

Invetsments 15,000

TOTAL NON-CURRENT ASSETS 27,300

TOTAL ASSETS 71,670

Current Liabilities:

Salaries Accrued 3,450

Accounts Payable 17,420

TOTAL CURRENT LIABILITIES 20,870

Non-Current Liabilities: -

Mortgage Payable 7,800

TOTAL NON-CURRENT LIABILITIES 7,800

TOTAL LIABILITIES 28,670

NET ASSETS 43,000

Capital:

Opening Balance 15,000

Add: Net Profit 61,900

76,900

Less: Drawings 33,900

TOTAL CAPITAL 43,000

Balance Sheet

as on 31 January 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING

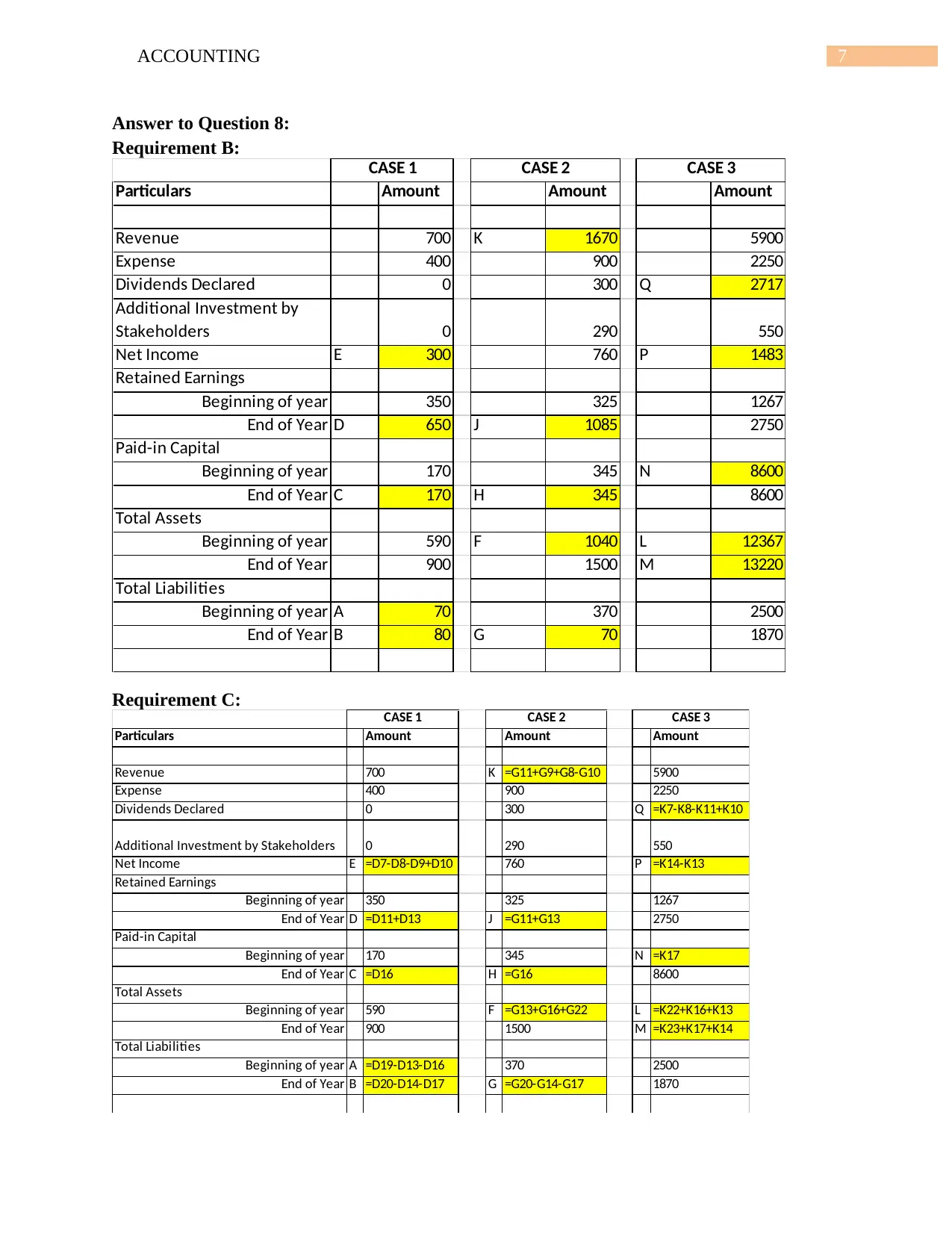

Answer to Question 8:

Requirement B:

Particulars Amount Amount Amount

Revenue 700 K 1670 5900

Expense 400 900 2250

Dividends Declared 0 300 Q 2717

Additional Investment by

Stakeholders 0 290 550

Net Income E 300 760 P 1483

Retained Earnings

Beginning of year 350 325 1267

End of Year D 650 J 1085 2750

Paid-in Capital

Beginning of year 170 345 N 8600

End of Year C 170 H 345 8600

Total Assets

Beginning of year 590 F 1040 L 12367

End of Year 900 1500 M 13220

Total Liabilities

Beginning of year A 70 370 2500

End of Year B 80 G 70 1870

CASE 1 CASE 3CASE 2

Requirement C:

Particulars Amount Amount Amount

Revenue 700 K =G11+G9+G8-G10 5900

Expense 400 900 2250

Dividends Declared 0 300 Q =K7-K8-K11+K10

Additional Investment by Stakeholders 0 290 550

Net Income E =D7-D8-D9+D10 760 P =K14-K13

Retained Earnings

Beginning of year 350 325 1267

End of Year D =D11+D13 J =G11+G13 2750

Paid-in Capital

Beginning of year 170 345 N =K17

End of Year C =D16 H =G16 8600

Total Assets

Beginning of year 590 F =G13+G16+G22 L =K22+K16+K13

End of Year 900 1500 M =K23+K17+K14

Total Liabilities

Beginning of year A =D19-D13-D16 370 2500

End of Year B =D20-D14-D17 G =G20-G14-G17 1870

CASE 1 CASE 2 CASE 3

Answer to Question 8:

Requirement B:

Particulars Amount Amount Amount

Revenue 700 K 1670 5900

Expense 400 900 2250

Dividends Declared 0 300 Q 2717

Additional Investment by

Stakeholders 0 290 550

Net Income E 300 760 P 1483

Retained Earnings

Beginning of year 350 325 1267

End of Year D 650 J 1085 2750

Paid-in Capital

Beginning of year 170 345 N 8600

End of Year C 170 H 345 8600

Total Assets

Beginning of year 590 F 1040 L 12367

End of Year 900 1500 M 13220

Total Liabilities

Beginning of year A 70 370 2500

End of Year B 80 G 70 1870

CASE 1 CASE 3CASE 2

Requirement C:

Particulars Amount Amount Amount

Revenue 700 K =G11+G9+G8-G10 5900

Expense 400 900 2250

Dividends Declared 0 300 Q =K7-K8-K11+K10

Additional Investment by Stakeholders 0 290 550

Net Income E =D7-D8-D9+D10 760 P =K14-K13

Retained Earnings

Beginning of year 350 325 1267

End of Year D =D11+D13 J =G11+G13 2750

Paid-in Capital

Beginning of year 170 345 N =K17

End of Year C =D16 H =G16 8600

Total Assets

Beginning of year 590 F =G13+G16+G22 L =K22+K16+K13

End of Year 900 1500 M =K23+K17+K14

Total Liabilities

Beginning of year A =D19-D13-D16 370 2500

End of Year B =D20-D14-D17 G =G20-G14-G17 1870

CASE 1 CASE 2 CASE 3

8ACCOUNTING

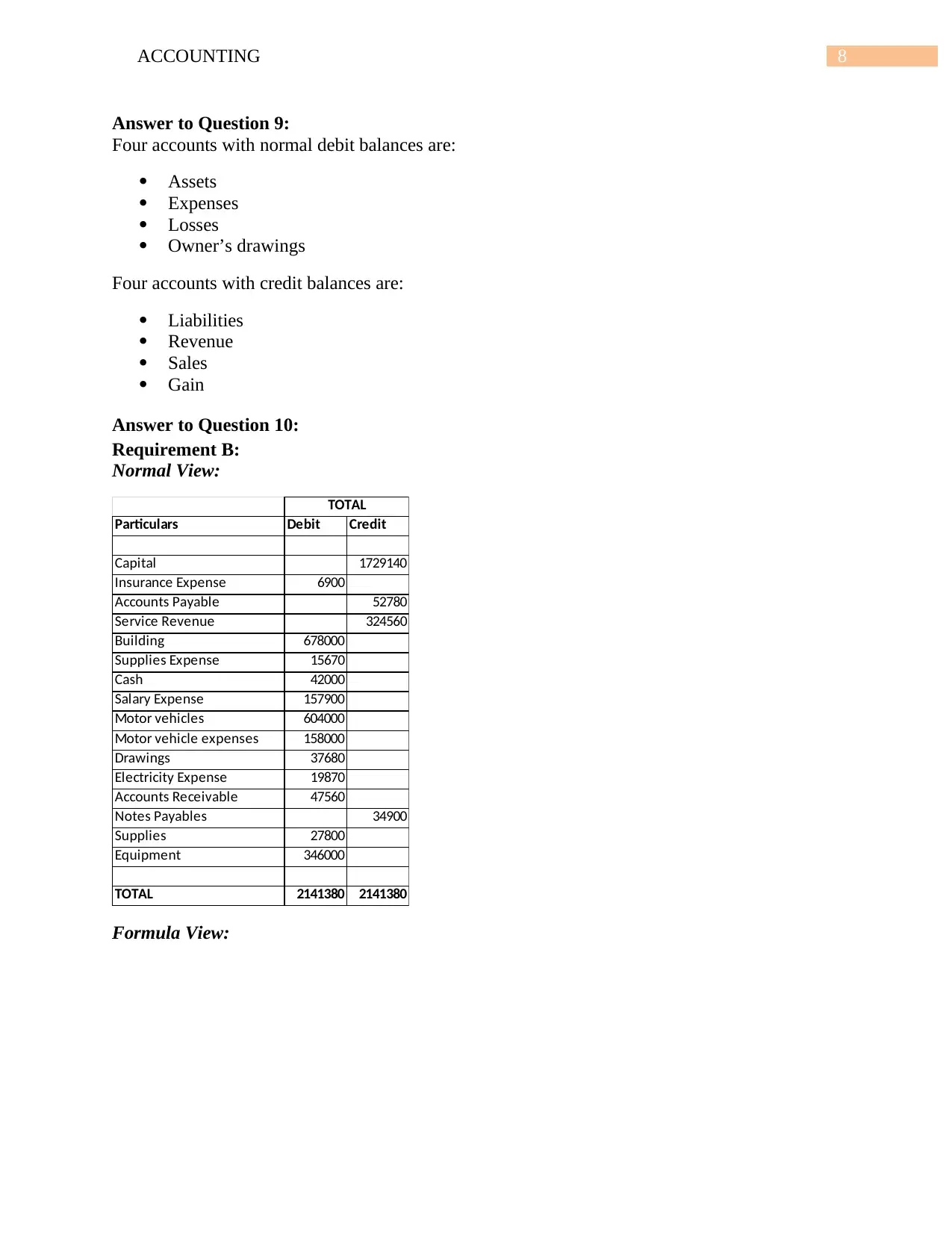

Answer to Question 9:

Four accounts with normal debit balances are:

Assets

Expenses

Losses

Owner’s drawings

Four accounts with credit balances are:

Liabilities

Revenue

Sales

Gain

Answer to Question 10:

Requirement B:

Normal View:

Particulars Debit Credit

Capital 1729140

Insurance Expense 6900

Accounts Payable 52780

Service Revenue 324560

Building 678000

Supplies Expense 15670

Cash 42000

Salary Expense 157900

Motor vehicles 604000

Motor vehicle expenses 158000

Drawings 37680

Electricity Expense 19870

Accounts Receivable 47560

Notes Payables 34900

Supplies 27800

Equipment 346000

TOTAL 2141380 2141380

TOTAL

Formula View:

Answer to Question 9:

Four accounts with normal debit balances are:

Assets

Expenses

Losses

Owner’s drawings

Four accounts with credit balances are:

Liabilities

Revenue

Sales

Gain

Answer to Question 10:

Requirement B:

Normal View:

Particulars Debit Credit

Capital 1729140

Insurance Expense 6900

Accounts Payable 52780

Service Revenue 324560

Building 678000

Supplies Expense 15670

Cash 42000

Salary Expense 157900

Motor vehicles 604000

Motor vehicle expenses 158000

Drawings 37680

Electricity Expense 19870

Accounts Receivable 47560

Notes Payables 34900

Supplies 27800

Equipment 346000

TOTAL 2141380 2141380

TOTAL

Formula View:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING

Particulars Debit Credit

Capital 1729140

Insurance Expense 6900

Accounts Payable 52780

Service Revenue 324560

Building 678000

Supplies Expense 15670

Cash 42000

Salary Expense 157900

Motor vehicles 604000

Motor vehicle expenses 158000

Drawings 37680

Electricity Expense 19870

Accounts Receivable 47560

Notes Payables 34900

Supplies 27800

Equipment 346000

TOTAL =SUM(C10:C26) =SUM(D10:D26)

TOTAL

Requirement C:

Particulars Debit Credit

Capital 1729140

Insurance Expense 6900

Accounts Payable 37680

Service Revenue 303560

Building 678000

Supplies Expense 15670

Cash 21000

Salary Expense 157900

Motor vehicles 604000

Motor vehicle expenses 158000

Drawings 37680

Electricity Expense 19870

Accounts Receivable 47560

Notes Payables 50000

Supplies 27800

Equipment 346000

TOTAL 2120380 2120380

TOTAL

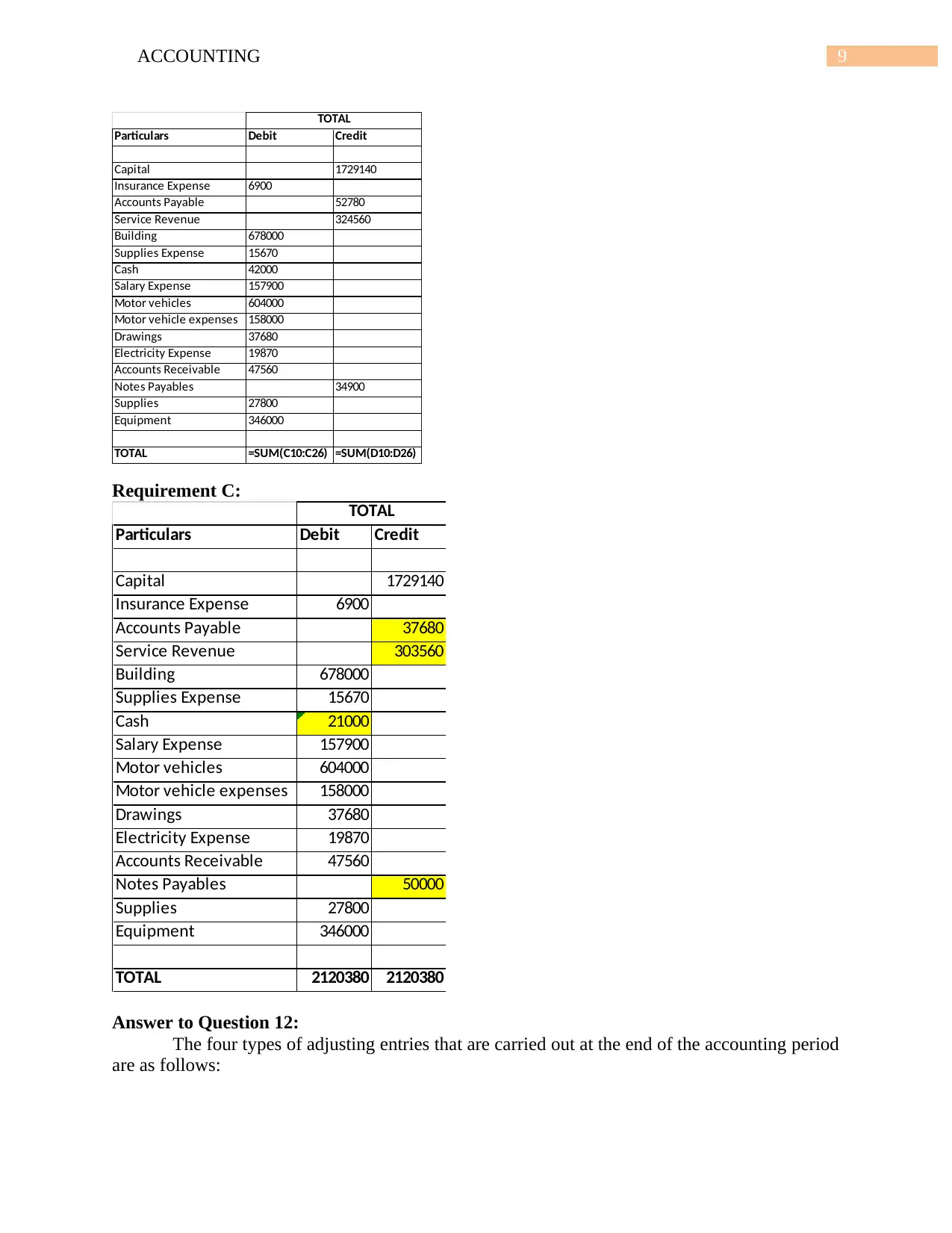

Answer to Question 12:

The four types of adjusting entries that are carried out at the end of the accounting period

are as follows:

Particulars Debit Credit

Capital 1729140

Insurance Expense 6900

Accounts Payable 52780

Service Revenue 324560

Building 678000

Supplies Expense 15670

Cash 42000

Salary Expense 157900

Motor vehicles 604000

Motor vehicle expenses 158000

Drawings 37680

Electricity Expense 19870

Accounts Receivable 47560

Notes Payables 34900

Supplies 27800

Equipment 346000

TOTAL =SUM(C10:C26) =SUM(D10:D26)

TOTAL

Requirement C:

Particulars Debit Credit

Capital 1729140

Insurance Expense 6900

Accounts Payable 37680

Service Revenue 303560

Building 678000

Supplies Expense 15670

Cash 21000

Salary Expense 157900

Motor vehicles 604000

Motor vehicle expenses 158000

Drawings 37680

Electricity Expense 19870

Accounts Receivable 47560

Notes Payables 50000

Supplies 27800

Equipment 346000

TOTAL 2120380 2120380

TOTAL

Answer to Question 12:

The four types of adjusting entries that are carried out at the end of the accounting period

are as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING

Accrued revenue – the journal entry for accrued revenue is that the accounts receivable

has to be debited and the particular revenue account that is due has to be credited

(Ajupov, Kurilova, & Evstigneeva, 2015).

Accrued expenses – the journal entry for accrued expenses is that the particular expense

account that has to be paid by the company should be debited and the accounts payable

should have to be credited.

Deferred revenue – the journal entry for this particular financial transaction is that the

deferred revenue account has to be debited and the particular income account that has still

not been received should be credited

Deferred expenses - the journal entry for deferred expenses is that the expenses account

should be debited and the deferred expenses account should be credited

Answer to Question 13:

Current liabilities are the liabilities that are liquid in nature. This means that these

liabilities have a high degree of liquidity. Moreover, current liabilities refer to the liabilities that

are incurred by the firm in the regular course of business. The current liabilities are due within

the same accounting year. Two examples of current liabilities are accrued expenses and customer

deposits.

Non-current liabilities are the liabilities that are not due within the next twelve months.

These liabilities refer to the long term financial obligations that are reflected in the balance sheet

of the corporate entity. Two examples of non-current liabilities are long-term borrowings and

bonds payable (Yu caes et al., 2014).

Answer to Question 14:

The current ratio refers to the liquidity position of a business entity. This means that the

current ratio refers to the capability of the current assets of the firm to compensate for the current

liabilities of the firm. The formula for current ratio is (current assets / current liabilities) (Yu caes

et al., 2014).

For instance, the current assets of a business entity is $20 million and the current

liabilities of the same corporate entity is $10 million. Therefore, the current ratio will be (20/10)

2.

Answer to Question 15:

Requirement B:

Normal View:

Accrued revenue – the journal entry for accrued revenue is that the accounts receivable

has to be debited and the particular revenue account that is due has to be credited

(Ajupov, Kurilova, & Evstigneeva, 2015).

Accrued expenses – the journal entry for accrued expenses is that the particular expense

account that has to be paid by the company should be debited and the accounts payable

should have to be credited.

Deferred revenue – the journal entry for this particular financial transaction is that the

deferred revenue account has to be debited and the particular income account that has still

not been received should be credited

Deferred expenses - the journal entry for deferred expenses is that the expenses account

should be debited and the deferred expenses account should be credited

Answer to Question 13:

Current liabilities are the liabilities that are liquid in nature. This means that these

liabilities have a high degree of liquidity. Moreover, current liabilities refer to the liabilities that

are incurred by the firm in the regular course of business. The current liabilities are due within

the same accounting year. Two examples of current liabilities are accrued expenses and customer

deposits.

Non-current liabilities are the liabilities that are not due within the next twelve months.

These liabilities refer to the long term financial obligations that are reflected in the balance sheet

of the corporate entity. Two examples of non-current liabilities are long-term borrowings and

bonds payable (Yu caes et al., 2014).

Answer to Question 14:

The current ratio refers to the liquidity position of a business entity. This means that the

current ratio refers to the capability of the current assets of the firm to compensate for the current

liabilities of the firm. The formula for current ratio is (current assets / current liabilities) (Yu caes

et al., 2014).

For instance, the current assets of a business entity is $20 million and the current

liabilities of the same corporate entity is $10 million. Therefore, the current ratio will be (20/10)

2.

Answer to Question 15:

Requirement B:

Normal View:

11ACCOUNTING

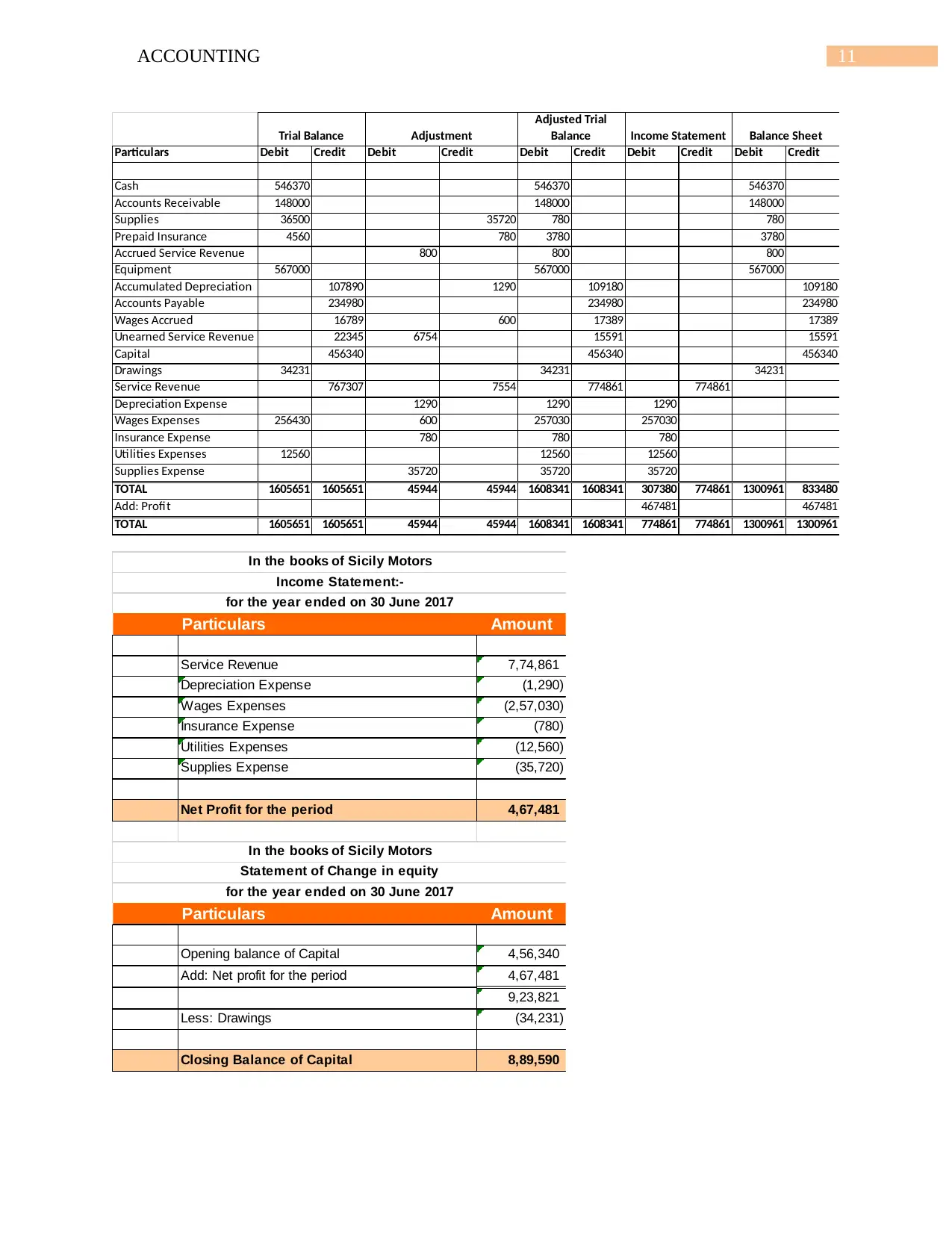

Particulars Debit Credit Debit Credit Debit Credit Debit Credit Debit Credit

Cash 546370 546370 546370

Accounts Receivable 148000 148000 148000

Supplies 36500 35720 780 780

Prepaid Insurance 4560 780 3780 3780

Accrued Service Revenue 800 800 800

Equipment 567000 567000 567000

Accumulated Depreciation 107890 1290 109180 109180

Accounts Payable 234980 234980 234980

Wages Accrued 16789 600 17389 17389

Unearned Service Revenue 22345 6754 15591 15591

Capital 456340 456340 456340

Drawings 34231 34231 34231

Service Revenue 767307 7554 774861 774861

Depreciation Expense 1290 1290 1290

Wages Expenses 256430 600 257030 257030

Insurance Expense 780 780 780

Utilities Expenses 12560 12560 12560

Supplies Expense 35720 35720 35720

TOTAL 1605651 1605651 45944 45944 1608341 1608341 307380 774861 1300961 833480

Add: Profit 467481 467481

TOTAL 1605651 1605651 45944 45944 1608341 1608341 774861 774861 1300961 1300961

Adjusted Trial

Balance Income Statement Balance SheetTrial Balance Adjustment

Particulars Amount

Service Revenue 7,74,861

Depreciation Expense (1,290)

Wages Expenses (2,57,030)

Insurance Expense (780)

Utilities Expenses (12,560)

Supplies Expense (35,720)

Net Profit for the period 4,67,481

Particulars Amount

Opening balance of Capital 4,56,340

Add: Net profit for the period 4,67,481

9,23,821

Less: Drawings (34,231)

Closing Balance of Capital 8,89,590

for the year ended on 30 June 2017

In the books of Sicily Motors

Income Statement:-

for the year ended on 30 June 2017

In the books of Sicily Motors

Statement of Change in equity

Particulars Debit Credit Debit Credit Debit Credit Debit Credit Debit Credit

Cash 546370 546370 546370

Accounts Receivable 148000 148000 148000

Supplies 36500 35720 780 780

Prepaid Insurance 4560 780 3780 3780

Accrued Service Revenue 800 800 800

Equipment 567000 567000 567000

Accumulated Depreciation 107890 1290 109180 109180

Accounts Payable 234980 234980 234980

Wages Accrued 16789 600 17389 17389

Unearned Service Revenue 22345 6754 15591 15591

Capital 456340 456340 456340

Drawings 34231 34231 34231

Service Revenue 767307 7554 774861 774861

Depreciation Expense 1290 1290 1290

Wages Expenses 256430 600 257030 257030

Insurance Expense 780 780 780

Utilities Expenses 12560 12560 12560

Supplies Expense 35720 35720 35720

TOTAL 1605651 1605651 45944 45944 1608341 1608341 307380 774861 1300961 833480

Add: Profit 467481 467481

TOTAL 1605651 1605651 45944 45944 1608341 1608341 774861 774861 1300961 1300961

Adjusted Trial

Balance Income Statement Balance SheetTrial Balance Adjustment

Particulars Amount

Service Revenue 7,74,861

Depreciation Expense (1,290)

Wages Expenses (2,57,030)

Insurance Expense (780)

Utilities Expenses (12,560)

Supplies Expense (35,720)

Net Profit for the period 4,67,481

Particulars Amount

Opening balance of Capital 4,56,340

Add: Net profit for the period 4,67,481

9,23,821

Less: Drawings (34,231)

Closing Balance of Capital 8,89,590

for the year ended on 30 June 2017

In the books of Sicily Motors

Income Statement:-

for the year ended on 30 June 2017

In the books of Sicily Motors

Statement of Change in equity

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

![Accounting System and Process - [Course Code] Assignment Solution](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fuz%2Fdbb768d80ca143b8a73f4afd68255951.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.