Accounting Concepts and Practices: Comparing Financial Statements

VerifiedAdded on 2019/11/08

|11

|1895

|56

Homework Assignment

AI Summary

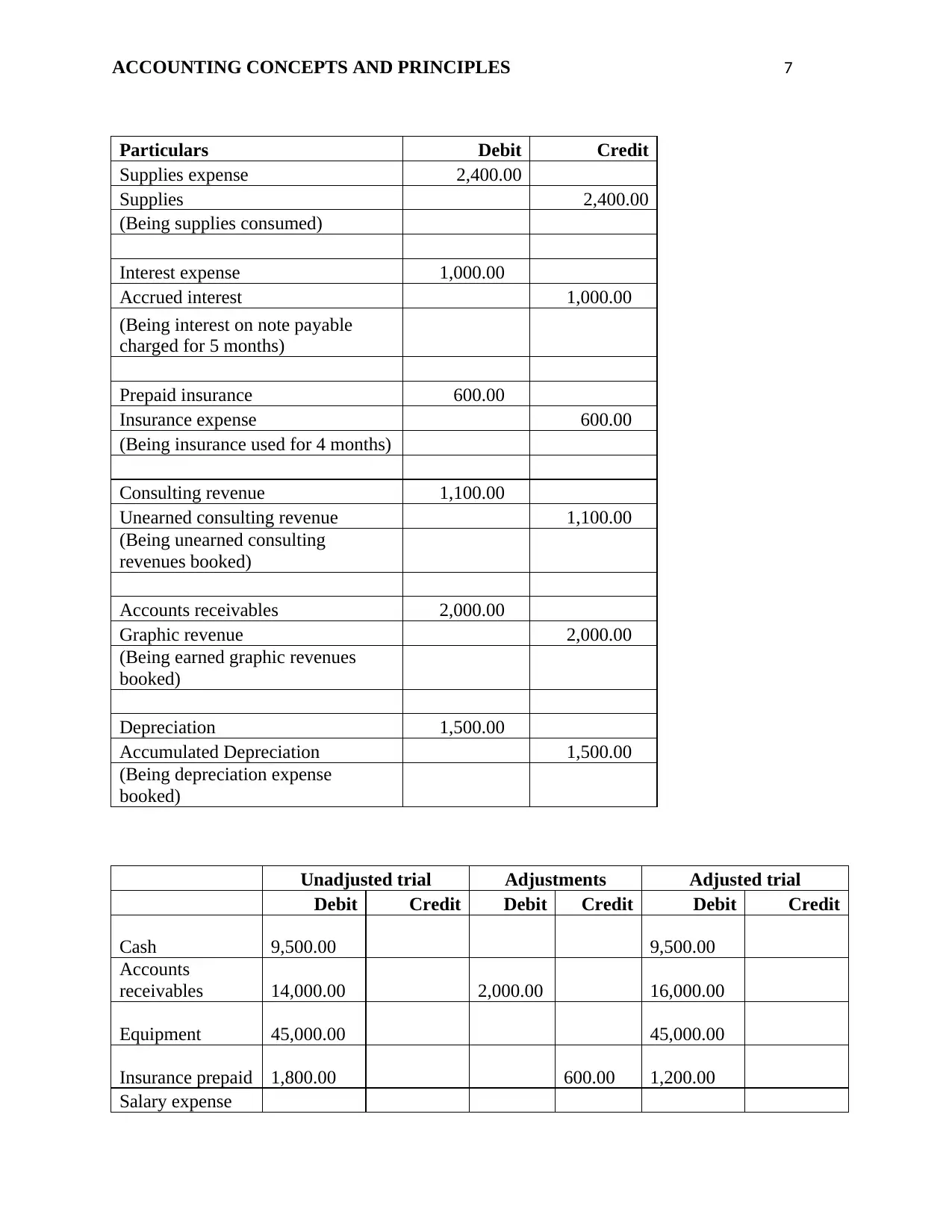

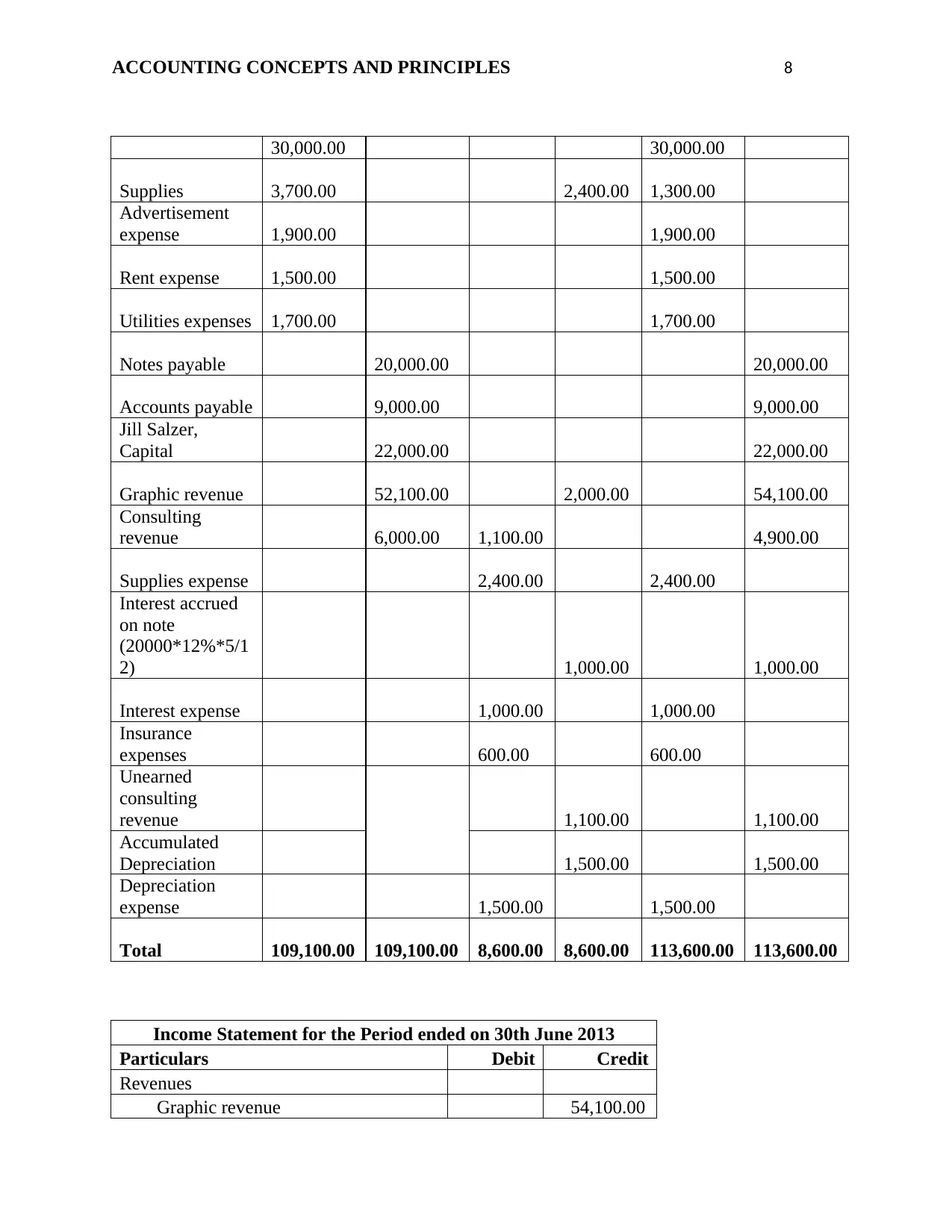

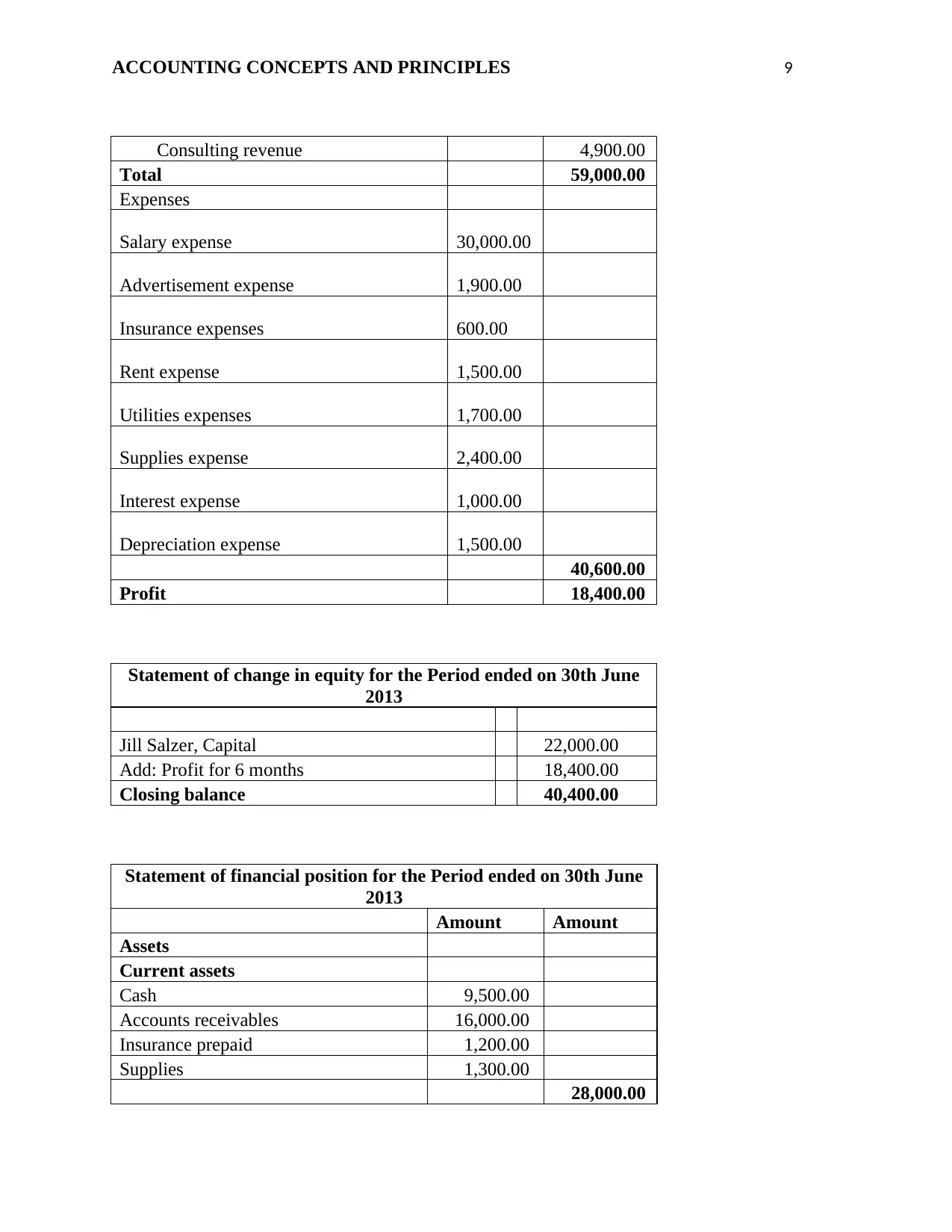

This assignment examines accounting concepts and practices, focusing on the generally accepted accounting principles (GAAP) and their application in financial statements. The discussion includes the implications of accounting conventions, standards, consolidation, and foreign currencies, particularly when comparing companies like Nestle (USA) and Patties Food Limited (Australia), which follow different GAAP frameworks (IASB and AASB, respectively). The assignment highlights similarities and differences between IASB and AASB, especially regarding consolidation and foreign currency transactions. It also analyzes the impact of changes in IFRS on companies like Nestle and discusses Nestle's business strategy and corporate governance. Furthermore, the assignment provides adjusting journal entries, an adjusted trial balance, an income statement, a statement of changes in equity, and a statement of financial position for a specific period, demonstrating practical application of accounting principles. The assignment covers the basic accounting principles and concepts, historical cost, monetary unit assumption, and economic entity assumption.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.