Accounting for Labour: Costs, Remuneration, and Efficiency Analysis

VerifiedAdded on 2022/06/08

|23

|6965

|14

Homework Assignment

AI Summary

This assignment provides a comprehensive overview of accounting for labor costs. It begins by distinguishing between direct and indirect labor costs, including basic pay, bonuses, and overtime premiums, with examples to illustrate calculations. The assignment then explores methods for relating labor costs to work done, such as time sheets, time cards, and job sheets, and explains the role of the payroll department in calculating gross and net wages. Furthermore, it delves into different remuneration methods, including time-based and piecework systems, as well as individual and group incentive schemes. The document also addresses the calculation and analysis of labor turnover, efficiency, capacity, and production volume ratios. Through detailed explanations and examples, the assignment equips students with the knowledge to effectively manage and account for labor costs within an organization.

Accounting for labour - VISEMIH

The learning objectives

Upon completion of this chapter you will be able to:

calculate direct and indirect costs of labour

explain the methods used to relate input labour costs to work done

prepare the journal and ledger entries to record labour costs inputs and outputs, and

interpret entries in the labour account

describe different remuneration methods: time-based systems; piecework systems;

individual incentive schemes; group incentive schemes

calculate the level, and analyse the costs and causes of labour turnover

explain and calculate labour efficiency, capacity and production volume ratios.

The learning objectives

Upon completion of this chapter you will be able to:

calculate direct and indirect costs of labour

explain the methods used to relate input labour costs to work done

prepare the journal and ledger entries to record labour costs inputs and outputs, and

interpret entries in the labour account

describe different remuneration methods: time-based systems; piecework systems;

individual incentive schemes; group incentive schemes

calculate the level, and analyse the costs and causes of labour turnover

explain and calculate labour efficiency, capacity and production volume ratios.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

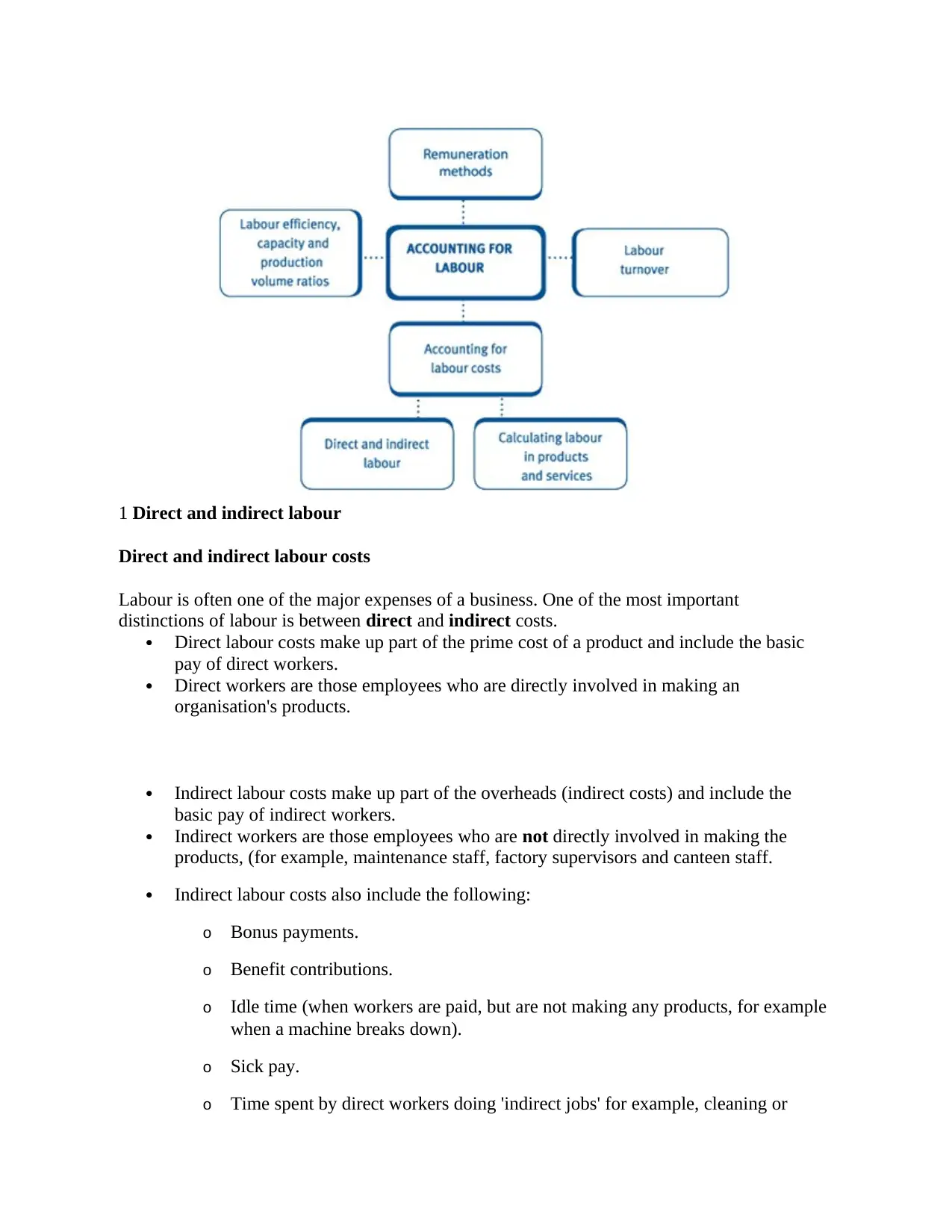

1 Direct and indirect labour

Direct and indirect labour costs

Labour is often one of the major expenses of a business. One of the most important

distinctions of labour is between direct and indirect costs.

Direct labour costs make up part of the prime cost of a product and include the basic

pay of direct workers.

Direct workers are those employees who are directly involved in making an

organisation's products.

Indirect labour costs make up part of the overheads (indirect costs) and include the

basic pay of indirect workers.

Indirect workers are those employees who are not directly involved in making the

products, (for example, maintenance staff, factory supervisors and canteen staff.

Indirect labour costs also include the following:

o Bonus payments.

o Benefit contributions.

o Idle time (when workers are paid, but are not making any products, for example

when a machine breaks down).

o Sick pay.

o Time spent by direct workers doing 'indirect jobs' for example, cleaning or

Direct and indirect labour costs

Labour is often one of the major expenses of a business. One of the most important

distinctions of labour is between direct and indirect costs.

Direct labour costs make up part of the prime cost of a product and include the basic

pay of direct workers.

Direct workers are those employees who are directly involved in making an

organisation's products.

Indirect labour costs make up part of the overheads (indirect costs) and include the

basic pay of indirect workers.

Indirect workers are those employees who are not directly involved in making the

products, (for example, maintenance staff, factory supervisors and canteen staff.

Indirect labour costs also include the following:

o Bonus payments.

o Benefit contributions.

o Idle time (when workers are paid, but are not making any products, for example

when a machine breaks down).

o Sick pay.

o Time spent by direct workers doing 'indirect jobs' for example, cleaning or

repairing machines.

Overtime and overtime premiums

When employees work overtime, they receive a basic pay element and an overtime

premium.

For example, if Fred is paid 80 FCFA per hour and overtime is paid at time and a half,

when Fred works overtime, he will receive 120 FCFA per hour (80 + 40 (50% x 80)).

It is important that his pay is analysed into direct and indirect labour costs:

Basic Pay per Hour = 80 FCFA Direct Cost

Overtime Premium = 40 FCFA Indirect Cost

Total Pay per Hour = 120 FCFA

Overtime premiums are treated as direct labour costs, if at the specific request of a

customer, because they want a job to be finished as soon as possible.

Employees who work night shifts, or other anti-social hours may be entitled to a shift

allowance or shift premium. Shift premiums are similar to overtime premiums where

the extra amount paid above the basic rate is treated as an indirect labour cost.

Illustration 1: Direct and indirect labour

Vienna is a direct labour employee who works a standard 35 hours per week and is paid a

basic rate of 120 FCFA per hour. Overtime is paid at time and a third. In week 8 she worked

42 hours and received a 500 FCFA bonus. Solution is in the following table:

Details Direct Labour Cost Indirect Labour Cost Total

FCFA

Basic Pay for Standard Hours 4,200 4,200

Basic Pay for Overtime Hours 840 840

Overtime Premium 280 280

Bonus Pay 500 500

Toal 5040 780 5,820

Workings:

(1) Basic pay for standard hours = 35 hours × 120 per hour = 4,200 FCFA

Basic pay for standard hours is a direct labour cost, because the work involved is directly

attributable to production.

(2) Basic pay for overtime hours = 7 hours × 120 = 840 FCFA

This is also a direct labour cost, because the basic rate for overtime is part of the direct

labour cost. It is the overtime premium which is usually part of the indirect labour cost.

(3) Overtime premium = 1/3 of 120 = 40 FCFA

Overtime and overtime premiums

When employees work overtime, they receive a basic pay element and an overtime

premium.

For example, if Fred is paid 80 FCFA per hour and overtime is paid at time and a half,

when Fred works overtime, he will receive 120 FCFA per hour (80 + 40 (50% x 80)).

It is important that his pay is analysed into direct and indirect labour costs:

Basic Pay per Hour = 80 FCFA Direct Cost

Overtime Premium = 40 FCFA Indirect Cost

Total Pay per Hour = 120 FCFA

Overtime premiums are treated as direct labour costs, if at the specific request of a

customer, because they want a job to be finished as soon as possible.

Employees who work night shifts, or other anti-social hours may be entitled to a shift

allowance or shift premium. Shift premiums are similar to overtime premiums where

the extra amount paid above the basic rate is treated as an indirect labour cost.

Illustration 1: Direct and indirect labour

Vienna is a direct labour employee who works a standard 35 hours per week and is paid a

basic rate of 120 FCFA per hour. Overtime is paid at time and a third. In week 8 she worked

42 hours and received a 500 FCFA bonus. Solution is in the following table:

Details Direct Labour Cost Indirect Labour Cost Total

FCFA

Basic Pay for Standard Hours 4,200 4,200

Basic Pay for Overtime Hours 840 840

Overtime Premium 280 280

Bonus Pay 500 500

Toal 5040 780 5,820

Workings:

(1) Basic pay for standard hours = 35 hours × 120 per hour = 4,200 FCFA

Basic pay for standard hours is a direct labour cost, because the work involved is directly

attributable to production.

(2) Basic pay for overtime hours = 7 hours × 120 = 840 FCFA

This is also a direct labour cost, because the basic rate for overtime is part of the direct

labour cost. It is the overtime premium which is usually part of the indirect labour cost.

(3) Overtime premium = 1/3 of 120 = 40 FCFA

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total overtime premium = 7 hours × 40 = 280 FCFA

Unless overtime is worked at the specific request of a customer, overtime premium is part of

the indirect labour costs of an organisation.

Test your understanding 1

A company operates a factory which employed 40 direct workers throughout the four-week

period just ended. Direct employees were paid at a basic rate of 400 FCFA per hour for a 38 -

hour week. Total hours of the direct workers in the four-week period were 6,528. Overtime,

which is paid at a premium of 35 %, is worked in order to meet general production

requirements. Employee deductions total 30 % of gross wages. 188 hours of direct workers'

time were registered as idle.

Calculate the following for the four-week period just ended.

S.N Details Amount

1 Gross Wages

2 Deductions

3 Net

Wages

4 Direct Labour Cost

5 Indirect Labour Cost

2 Calculating labour cost in products and services

Determining time spent doing jobs

Methods can include:

time sheets

time cards

job sheets.

Unless overtime is worked at the specific request of a customer, overtime premium is part of

the indirect labour costs of an organisation.

Test your understanding 1

A company operates a factory which employed 40 direct workers throughout the four-week

period just ended. Direct employees were paid at a basic rate of 400 FCFA per hour for a 38 -

hour week. Total hours of the direct workers in the four-week period were 6,528. Overtime,

which is paid at a premium of 35 %, is worked in order to meet general production

requirements. Employee deductions total 30 % of gross wages. 188 hours of direct workers'

time were registered as idle.

Calculate the following for the four-week period just ended.

S.N Details Amount

1 Gross Wages

2 Deductions

3 Net

Wages

4 Direct Labour Cost

5 Indirect Labour Cost

2 Calculating labour cost in products and services

Determining time spent doing jobs

Methods can include:

time sheets

time cards

job sheets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Time records

It is essential that organisations employ relevant methods in both manufacturing and service

industries to relate the labour costs incurred to the work done. One of the ways in which this

can be done is to make records of the time spent by employees doing jobs.

Time recording is required both for payment purposes and also for determining the

costs to be charged to specific jobs.

In manufacturing industries, both direct and indirect workers will be supplied with an

attendance record on which to record their time of arrival and departure from the

factory. Such records are known as time cards (gate or clock cards) and are used to

calculate wages and rates of pay.

The most sophisticated time recorders use plastic 'swipe' cards which are directly

linked to a central computer.

Activity time records

Another method of relating work done to costs incurred is by the use of activity time records.

Activity time records may be either period related or time related.

Period-related timesheets are commonly used in service industries, for example in

accountancy firms where time spent working for different clients is analysed, often to

the nearest 15 minutes.

Period-related timesheets are records that may cover days, weeks or sometimes longer

periods.

Task-related activity time records are known as job sheets, operations charts or

piecework tickets. They are generally more accurate and reliable than time-related

activity time records, and are essential when incentive schemes are in use.

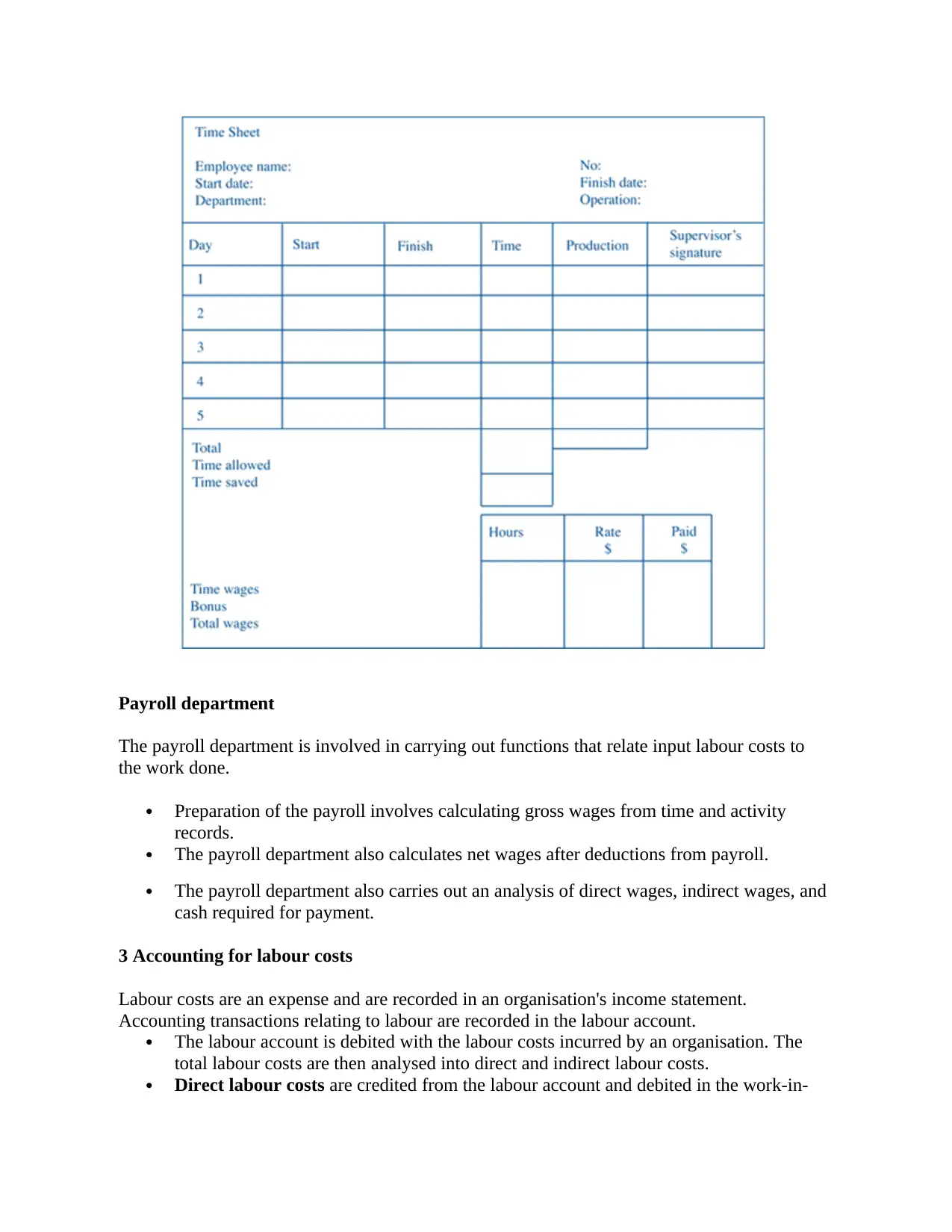

An example of a daily timesheet is illustrated below.

It is essential that organisations employ relevant methods in both manufacturing and service

industries to relate the labour costs incurred to the work done. One of the ways in which this

can be done is to make records of the time spent by employees doing jobs.

Time recording is required both for payment purposes and also for determining the

costs to be charged to specific jobs.

In manufacturing industries, both direct and indirect workers will be supplied with an

attendance record on which to record their time of arrival and departure from the

factory. Such records are known as time cards (gate or clock cards) and are used to

calculate wages and rates of pay.

The most sophisticated time recorders use plastic 'swipe' cards which are directly

linked to a central computer.

Activity time records

Another method of relating work done to costs incurred is by the use of activity time records.

Activity time records may be either period related or time related.

Period-related timesheets are commonly used in service industries, for example in

accountancy firms where time spent working for different clients is analysed, often to

the nearest 15 minutes.

Period-related timesheets are records that may cover days, weeks or sometimes longer

periods.

Task-related activity time records are known as job sheets, operations charts or

piecework tickets. They are generally more accurate and reliable than time-related

activity time records, and are essential when incentive schemes are in use.

An example of a daily timesheet is illustrated below.

Payroll department

The payroll department is involved in carrying out functions that relate input labour costs to

the work done.

Preparation of the payroll involves calculating gross wages from time and activity

records.

The payroll department also calculates net wages after deductions from payroll.

The payroll department also carries out an analysis of direct wages, indirect wages, and

cash required for payment.

3 Accounting for labour costs

Labour costs are an expense and are recorded in an organisation's income statement.

Accounting transactions relating to labour are recorded in the labour account.

The labour account is debited with the labour costs incurred by an organisation. The

total labour costs are then analysed into direct and indirect labour costs.

Direct labour costs are credited from the labour account and debited in the work-in-

The payroll department is involved in carrying out functions that relate input labour costs to

the work done.

Preparation of the payroll involves calculating gross wages from time and activity

records.

The payroll department also calculates net wages after deductions from payroll.

The payroll department also carries out an analysis of direct wages, indirect wages, and

cash required for payment.

3 Accounting for labour costs

Labour costs are an expense and are recorded in an organisation's income statement.

Accounting transactions relating to labour are recorded in the labour account.

The labour account is debited with the labour costs incurred by an organisation. The

total labour costs are then analysed into direct and indirect labour costs.

Direct labour costs are credited from the labour account and debited in the work-in-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

progress (WIP) account. Remember, direct labour costs are directly involved in

production and are therefore transferred to WIP before being transferred to finished

goods and then cost of sales.

Indirect labour costs are also credited 'out of' the labour account and debited to the

production overheads account. It is important that total labour costs are analysed into

their direct and indirect elements.

Illustration 2: “ Accounting for labour costs

DR Labour Account CR

‘000’ ‘000’

Bank (1) 800 WIP (2) 600

Production overheads (3)

Indirect labour 140

Overtime premium 20

Shift Premium 20

Sick pay 10

Idle time pay 10

800 800

(1) Labour costs incurred are paid out of the bank, before they are analysed further in the

labour account.

(2) The majority of the labour costs incurred by a manufacturing organisation are in respect of

direct labour costs. Direct labour costs are directly involved in production and are transferred

out of the labour account via a credit entry to the WIP account as shown above.

(3) Indirect labour costs include in direct labour (costs of indirect labour workers), overtime

premium (unless overtime is worked at the specific request of a customer), shift premium, sick

pay and idle time. All of these indirect labour costs are collected in the production overheads

account. They are transferred there via a credit entry out of the labour account and then

debited in the production overheads account.

Test your understanding 2

The following information is taken from the payroll records of a company.

Details Direct Workers Indirect Workers Total

FCFA FCFA FCFA

Basic pay for basic hours 430,000 170,000 600,000

Overtime – basic pay 100,000 45,000 145,000

Overtime – premium 50,000 22,500 72,500

Training 25,000 12,500 37,500

Sick pay 7,500 2,500 10,000

Idle Time 12,000 - 12,000

production and are therefore transferred to WIP before being transferred to finished

goods and then cost of sales.

Indirect labour costs are also credited 'out of' the labour account and debited to the

production overheads account. It is important that total labour costs are analysed into

their direct and indirect elements.

Illustration 2: “ Accounting for labour costs

DR Labour Account CR

‘000’ ‘000’

Bank (1) 800 WIP (2) 600

Production overheads (3)

Indirect labour 140

Overtime premium 20

Shift Premium 20

Sick pay 10

Idle time pay 10

800 800

(1) Labour costs incurred are paid out of the bank, before they are analysed further in the

labour account.

(2) The majority of the labour costs incurred by a manufacturing organisation are in respect of

direct labour costs. Direct labour costs are directly involved in production and are transferred

out of the labour account via a credit entry to the WIP account as shown above.

(3) Indirect labour costs include in direct labour (costs of indirect labour workers), overtime

premium (unless overtime is worked at the specific request of a customer), shift premium, sick

pay and idle time. All of these indirect labour costs are collected in the production overheads

account. They are transferred there via a credit entry out of the labour account and then

debited in the production overheads account.

Test your understanding 2

The following information is taken from the payroll records of a company.

Details Direct Workers Indirect Workers Total

FCFA FCFA FCFA

Basic pay for basic hours 430,000 170,000 600,000

Overtime – basic pay 100,000 45,000 145,000

Overtime – premium 50,000 22,500 72,500

Training 25,000 12,500 37,500

Sick pay 7,500 2,500 10,000

Idle Time 12,000 - 12,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Required:

Using the information given, complete the labour account shown below.

DR Labour Account CR

FCFA FCFA

4 Remuneration methods

There are two basic approaches to remuneration, time-related or output-related. The two basic

methods are time-based and piece work systems.

a. Time-based systems

We looked at time-based systems, the most common remuneration method, at the beginning of

this chapter.

Employees are paid a basic rate per hour, day, week or month.

Basic time-based systems do not provide any incentive for employees to improve

productivity and close supervision is often necessary.

The basic formula for a time-based system is as follows.

Total wages = (hours worked x basic rate of pay per hour) + (overtime hours worked x

overtime premium per hour)

b. Piecework systems

A piecework system pays a fixed amount per unit produced. The basic formula for a

piecework system is as follows.

Total wages = (units produced x rate of pay per unit)

Using the information given, complete the labour account shown below.

DR Labour Account CR

FCFA FCFA

4 Remuneration methods

There are two basic approaches to remuneration, time-related or output-related. The two basic

methods are time-based and piece work systems.

a. Time-based systems

We looked at time-based systems, the most common remuneration method, at the beginning of

this chapter.

Employees are paid a basic rate per hour, day, week or month.

Basic time-based systems do not provide any incentive for employees to improve

productivity and close supervision is often necessary.

The basic formula for a time-based system is as follows.

Total wages = (hours worked x basic rate of pay per hour) + (overtime hours worked x

overtime premium per hour)

b. Piecework systems

A piecework system pays a fixed amount per unit produced. The basic formula for a

piecework system is as follows.

Total wages = (units produced x rate of pay per unit)

Types of piecework system

There are two main piecework systems that you need to know about:

Straight piecework systems: “these systems are almost extinct today as employees

are more likely to be paid a guaranteed minimum wage within a straight piecework

system. A variation on the straight piecework system is the differential piecework

system.

Differential piecework systems: “these systems are the most widely used piecework

systems and involve different piece rates for different levels of production.

Illustration 3: Piecework schemes

A company operates a piecework system of remuneration, but also guarantees its employees

75% of a time-based rate of pay which is based on 190 FCFA per hour for an eight hour

working day. Three minutes is the standard time allowed per unit of output. Piecework is paid

at the rate of 180 FCFA per standard hour.

If an employee produces 200 units in eight hours on a particular day, what is the employee’s

gross pay for that day?

A 1140

B 1520

C 1800

D 1900

Answer:

C

200 units x standard time of 3 minutes per unit = 600 minutes divided 60 = 10 hours.

Employee gross pay = 10 hours x 18 = 1800 FCFA

Guaranteed (190 x 8 hours) x 75% = 1520 x 75% = 1140 FCFA

As gross pay exceeds the guaranteed amount, the answer is 1800 FCFA.

There are two main piecework systems that you need to know about:

Straight piecework systems: “these systems are almost extinct today as employees

are more likely to be paid a guaranteed minimum wage within a straight piecework

system. A variation on the straight piecework system is the differential piecework

system.

Differential piecework systems: “these systems are the most widely used piecework

systems and involve different piece rates for different levels of production.

Illustration 3: Piecework schemes

A company operates a piecework system of remuneration, but also guarantees its employees

75% of a time-based rate of pay which is based on 190 FCFA per hour for an eight hour

working day. Three minutes is the standard time allowed per unit of output. Piecework is paid

at the rate of 180 FCFA per standard hour.

If an employee produces 200 units in eight hours on a particular day, what is the employee’s

gross pay for that day?

A 1140

B 1520

C 1800

D 1900

Answer:

C

200 units x standard time of 3 minutes per unit = 600 minutes divided 60 = 10 hours.

Employee gross pay = 10 hours x 18 = 1800 FCFA

Guaranteed (190 x 8 hours) x 75% = 1520 x 75% = 1140 FCFA

As gross pay exceeds the guaranteed amount, the answer is 1800 FCFA.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

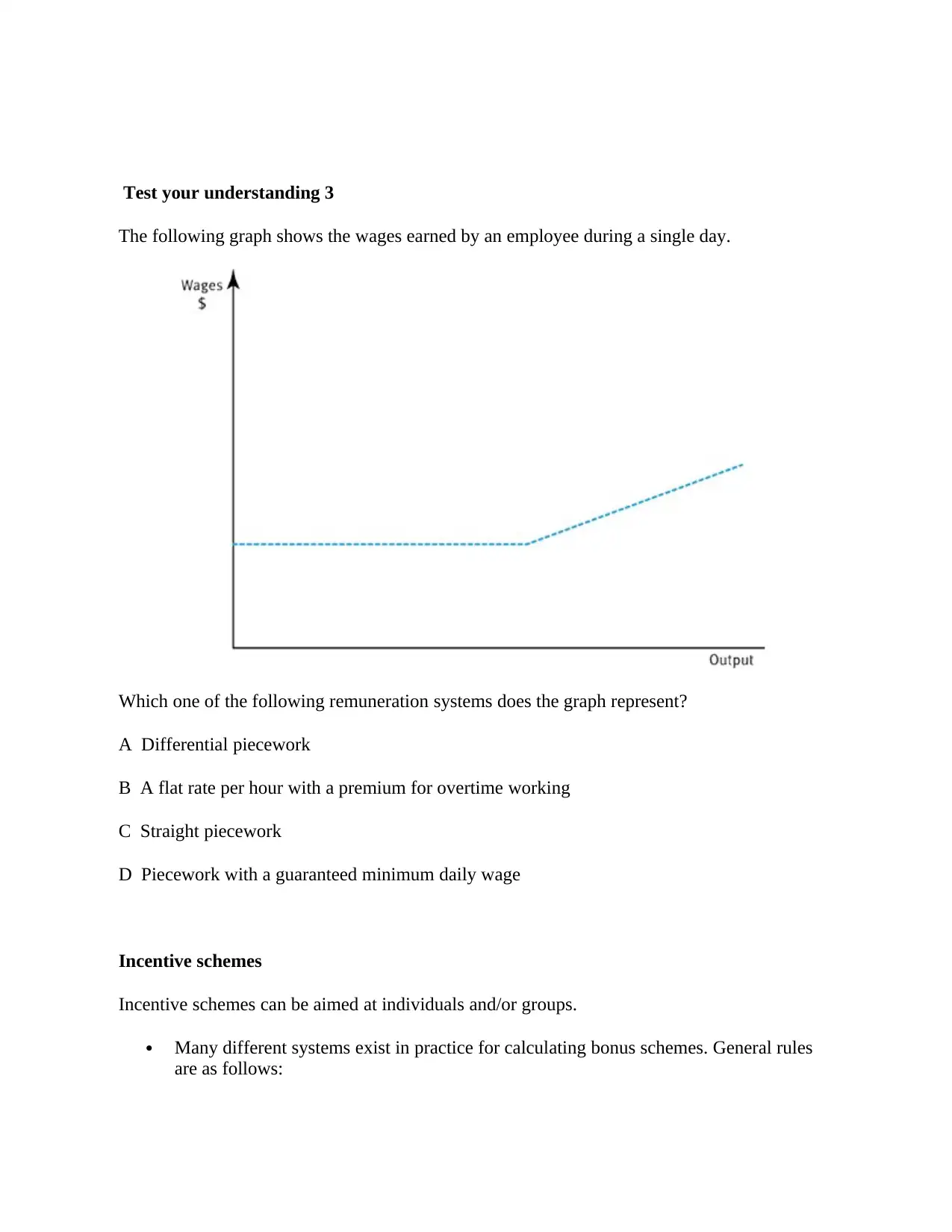

Test your understanding 3

The following graph shows the wages earned by an employee during a single day.

Which one of the following remuneration systems does the graph represent?

A Differential piecework

B A flat rate per hour with a premium for overtime working

C Straight piecework

D Piecework with a guaranteed minimum daily wage

Incentive schemes

Incentive schemes can be aimed at individuals and/or groups.

Many different systems exist in practice for calculating bonus schemes. General rules

are as follows:

The following graph shows the wages earned by an employee during a single day.

Which one of the following remuneration systems does the graph represent?

A Differential piecework

B A flat rate per hour with a premium for overtime working

C Straight piecework

D Piecework with a guaranteed minimum daily wage

Incentive schemes

Incentive schemes can be aimed at individuals and/or groups.

Many different systems exist in practice for calculating bonus schemes. General rules

are as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

o They should be closely related to the effort expended by employees.

o They should be agreed by employers/employees before being implemented.

o They should be easy to understand and simple to operate.

o They must be beneficial to all of those employees taking part in the scheme.

Most bonus schemes pay a basic time rate, plus a portion of the time saved as

compared to some agreed allowed time. These bonus schemes are known premium

bonus plans. Examples of such schemes are Halsey and Rowan.

Halsey: the employee receives 50% of the time saved.

Rowan: the proportion paid to the employee is based on the ratio of time taken to time

allowed.

Measured day work: the concept of this approach is to pay a high time rate, but this

rate is based on an analysis of past performance. Initially, work measurement is used to

calculate the allowed time per unit. This allowed time is compared to the time actually

taken in the past by the employee, and if this is better than the allowed time an

incentive is agreed, e.g. suppose the allowed time is 1 hour per unit and that the

average time taken by an employee over the last three months is 50 minutes. If the

normal rate is 120/hour, then an agreed incentive rate of (say) 140/hour could be used.

Share of production: share of production plans are based on acceptance by both

management and labour representatives of a constant share of value added for payroll.

Thus, any gains in value added, whether by improved production performance or cost

savings are shared by employees in a given ratio.

Illustration 4: Remuneration methods

The following data relate to Job A.

Employee’s basic rate of pay 480 FCFA per Hour

Time allowed for Job A 1 hour

Time taken 36 minutes

o They should be agreed by employers/employees before being implemented.

o They should be easy to understand and simple to operate.

o They must be beneficial to all of those employees taking part in the scheme.

Most bonus schemes pay a basic time rate, plus a portion of the time saved as

compared to some agreed allowed time. These bonus schemes are known premium

bonus plans. Examples of such schemes are Halsey and Rowan.

Halsey: the employee receives 50% of the time saved.

Rowan: the proportion paid to the employee is based on the ratio of time taken to time

allowed.

Measured day work: the concept of this approach is to pay a high time rate, but this

rate is based on an analysis of past performance. Initially, work measurement is used to

calculate the allowed time per unit. This allowed time is compared to the time actually

taken in the past by the employee, and if this is better than the allowed time an

incentive is agreed, e.g. suppose the allowed time is 1 hour per unit and that the

average time taken by an employee over the last three months is 50 minutes. If the

normal rate is 120/hour, then an agreed incentive rate of (say) 140/hour could be used.

Share of production: share of production plans are based on acceptance by both

management and labour representatives of a constant share of value added for payroll.

Thus, any gains in value added, whether by improved production performance or cost

savings are shared by employees in a given ratio.

Illustration 4: Remuneration methods

The following data relate to Job A.

Employee’s basic rate of pay 480 FCFA per Hour

Time allowed for Job A 1 hour

Time taken 36 minutes

The employee is paid the basic rate for the allowed time for the job and then the bonus based

on any time saved.

Halsey Scheme – Total payment for Job A = FCFA

Rowan Scheme – Total payment for Job A = FCFA

Solution

Halsey Scheme – Total payment for Job A = FCFA 576

Rowan Scheme – Total payment for Job A = FCFA 595.2

Workings:

Halsey Scheme

Bonus - Time saved = 60 – 36 = 24 minutes/60 x half x 480 = 96 FCFA

Plus basic rate pay = 480 FCFA

576 FCFA

Rowan Scheme

Bonus - 36/60 x 24 divided by 60 x 480 = 115.2 FCFA

Plus basic rate pay = 480 FCFA

595.2 FCFA

Additional test your understanding

Ten employees work as a group. When production of the group exceeds the standard 200

pieces per hour each employee in the group is paid a bonus for the excess production in

addition to wages at hourly rates.

The bonus is computed thus: the percentage of production in excess of the standard quantity is

found, and one half of the percentage is regarded as the employees' share. Each employee in

the group is paid as a bonus this percentage of a wage rate of 520 FCFA per hour. There is no

relationship between the individual worker's hourly rate and the bonus rate.

The following is one week's record:

on any time saved.

Halsey Scheme – Total payment for Job A = FCFA

Rowan Scheme – Total payment for Job A = FCFA

Solution

Halsey Scheme – Total payment for Job A = FCFA 576

Rowan Scheme – Total payment for Job A = FCFA 595.2

Workings:

Halsey Scheme

Bonus - Time saved = 60 – 36 = 24 minutes/60 x half x 480 = 96 FCFA

Plus basic rate pay = 480 FCFA

576 FCFA

Rowan Scheme

Bonus - 36/60 x 24 divided by 60 x 480 = 115.2 FCFA

Plus basic rate pay = 480 FCFA

595.2 FCFA

Additional test your understanding

Ten employees work as a group. When production of the group exceeds the standard 200

pieces per hour each employee in the group is paid a bonus for the excess production in

addition to wages at hourly rates.

The bonus is computed thus: the percentage of production in excess of the standard quantity is

found, and one half of the percentage is regarded as the employees' share. Each employee in

the group is paid as a bonus this percentage of a wage rate of 520 FCFA per hour. There is no

relationship between the individual worker's hourly rate and the bonus rate.

The following is one week's record:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.