Holmes Institute HI6025 Accounting for Lease: AASB 16 Critical Review

VerifiedAdded on 2022/11/24

|17

|4701

|456

Report

AI Summary

This report critically evaluates the new Australian Accounting Standard for Lease (AASB 16), contrasting it with the previous standard (AASB 117). It highlights the drawbacks of AASB 117, such as issues in asset recognition and financial representation, which AASB 16 addresses by eliminating the classification of leases into finance and operating leases. The report examines the need for change, the specific changes incorporated in AASB 16, and the impact of these changes on companies with significant lease financing. It also explores the shift towards classifying leases as operating leases and its relation to managerial behavior, the improvements in comparability offered by IFRS 16, and potential effects on companies' asset purchasing decisions. The report includes a summary of key disclosures made by a specified company regarding their accounting for leases, including transitional provisions and the impact of transitioning from AASB 117 to AASB 16.

Accounting Theory and Current Issues

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ABSTRACT

The purpose of the prevailing study is to evaluate and analyze the new accounting standard for

lease AASB 16 and to describe its need, objectives and impact. The study shows that the

previous standard for lease accounting (AASB 117) was not very effective, and had some

problems in terms of recognition of assets, representation of financial position, and so on.

Further, this has been solved by the AASB 16, by eliminating the classification of leases by the

lessee as either finance leases as well as operating leases.

The purpose of the prevailing study is to evaluate and analyze the new accounting standard for

lease AASB 16 and to describe its need, objectives and impact. The study shows that the

previous standard for lease accounting (AASB 117) was not very effective, and had some

problems in terms of recognition of assets, representation of financial position, and so on.

Further, this has been solved by the AASB 16, by eliminating the classification of leases by the

lessee as either finance leases as well as operating leases.

Table of Contents

Abstract............................................................................................................................................2

Introduction......................................................................................................................................5

Main Body.......................................................................................................................................5

Critical evaluation of AASB 116 accounting lease standard, emphasizing on its drawbacks.....5

Requirement for change...............................................................................................................6

Types of changes incorporated in the AASB 16 new lease accounting standard........................7

Impact of change on companies having considerable lease financing level................................8

Classification of most lease contracts as operating lease by companies, and its relation of

manager’s behaviour....................................................................................................................9

Expectancy from 1FRS 16 to improvise comparability between companies who engaging in

leasing assets or borrowing to buy assets....................................................................................9

Explanation of the tendency reporting entities have in buying more assets and lesser lease

assets after the adoption of AASB 16........................................................................................10

Key disclosers made by Wesfarmers on its accounting for leases by considering the

transitional provision and effect to AASB 16 to AASB 117.....................................................11

Conclusion.....................................................................................................................................13

References......................................................................................................................................14

Abstract............................................................................................................................................2

Introduction......................................................................................................................................5

Main Body.......................................................................................................................................5

Critical evaluation of AASB 116 accounting lease standard, emphasizing on its drawbacks.....5

Requirement for change...............................................................................................................6

Types of changes incorporated in the AASB 16 new lease accounting standard........................7

Impact of change on companies having considerable lease financing level................................8

Classification of most lease contracts as operating lease by companies, and its relation of

manager’s behaviour....................................................................................................................9

Expectancy from 1FRS 16 to improvise comparability between companies who engaging in

leasing assets or borrowing to buy assets....................................................................................9

Explanation of the tendency reporting entities have in buying more assets and lesser lease

assets after the adoption of AASB 16........................................................................................10

Key disclosers made by Wesfarmers on its accounting for leases by considering the

transitional provision and effect to AASB 16 to AASB 117.....................................................11

Conclusion.....................................................................................................................................13

References......................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

List of Figures

Figure 1: Group operating lease commitments as lessee...............................................................11

Figure 2: Commitment and Contingencies....................................................................................11

Figure 1: Group operating lease commitments as lessee...............................................................11

Figure 2: Commitment and Contingencies....................................................................................11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

The present study provides critical evaluation and analysis of the former accounting standard

relating to lease, i.e. AASB 117 while highlighting particularly on its drawbacks. The study will

also state about the need for change and the changes incorporated in the new AASB 16 lease

accounting standard. The study will also describe the impacts of changes on companies with a

significant level of lease financing while considering the tendency of companies for the

classification of most lease contracts as an operating lease, and the relation of positive

accounting theory to this managerial behaviour. Along with this, the study also covers the

justification of the comparability improved by IFRS 16 as per the view of IASB with a relevant

example. The prevailing study also emphasizes on whether the AASB 16 implementation has an

impact on the decision by companies relating to purchase of assets ion to buy more assets, and

consequently lease fewer assets. Lastly, the key disclosures made by Woolworth Group Limited

on its accounting for leases has been summarised, comprising on the transitional provision and

transition effect to AASB 16 from AASB 117.

MAIN BODY

Critical evaluation of AASB 116 accounting lease standard, emphasizing on its drawbacks

The Australian Accounting Standards Broads has provided a framework of AASB 116

Accounting Standard Leases as per the S (334) of the Corporation Act 2001. The aim of this

standard is to set provisions for lessees and lessors along with the suitable policies of accounting

as well as to disclosure requirements regarding leases. As per the provisions of AASB 117/IAS

17 Leases, there was a requirement by lessees to recognize in the financial position statements,

leased assets as well as their related liabilities taking place from any of the classification of lease

as finance lease, at the same time other leased assets and their related liabilities were entitled to

be off-balance sheet that it those emerging from operating leases (Xu, Davidson and Cheong,

2017). Further, recognising that not reporting assets and liabilities associated with operating

leases in the lessee’s financial statement might eventually lead to misleading information by not

offering a true and faithful presentation of transactions for leases. Thus, the standard setters made

decisions to eradicate the classification of this lease as finance leases or operating leases as

The present study provides critical evaluation and analysis of the former accounting standard

relating to lease, i.e. AASB 117 while highlighting particularly on its drawbacks. The study will

also state about the need for change and the changes incorporated in the new AASB 16 lease

accounting standard. The study will also describe the impacts of changes on companies with a

significant level of lease financing while considering the tendency of companies for the

classification of most lease contracts as an operating lease, and the relation of positive

accounting theory to this managerial behaviour. Along with this, the study also covers the

justification of the comparability improved by IFRS 16 as per the view of IASB with a relevant

example. The prevailing study also emphasizes on whether the AASB 16 implementation has an

impact on the decision by companies relating to purchase of assets ion to buy more assets, and

consequently lease fewer assets. Lastly, the key disclosures made by Woolworth Group Limited

on its accounting for leases has been summarised, comprising on the transitional provision and

transition effect to AASB 16 from AASB 117.

MAIN BODY

Critical evaluation of AASB 116 accounting lease standard, emphasizing on its drawbacks

The Australian Accounting Standards Broads has provided a framework of AASB 116

Accounting Standard Leases as per the S (334) of the Corporation Act 2001. The aim of this

standard is to set provisions for lessees and lessors along with the suitable policies of accounting

as well as to disclosure requirements regarding leases. As per the provisions of AASB 117/IAS

17 Leases, there was a requirement by lessees to recognize in the financial position statements,

leased assets as well as their related liabilities taking place from any of the classification of lease

as finance lease, at the same time other leased assets and their related liabilities were entitled to

be off-balance sheet that it those emerging from operating leases (Xu, Davidson and Cheong,

2017). Further, recognising that not reporting assets and liabilities associated with operating

leases in the lessee’s financial statement might eventually lead to misleading information by not

offering a true and faithful presentation of transactions for leases. Thus, the standard setters made

decisions to eradicate the classification of this lease as finance leases or operating leases as

provided in AASB 117/IAS 17 and rather made introduction of a single lessee accounting for

each and every lease (Wong and Joshi, 2015). The existing requirements for lease accounting in

the IAS 17 Leases have been long criticized for being unsuccessful in completing needs of

financial statement users, especially because of the reason that IAS 17 does not need lessees to

recognize assets and liabilities taking place from the operating leases.

Leasing offers a significant and flexible financing source for most of the companies. On the other

hand, the previous accounting standard, i.e. IAS Leases makes it complicated for investors and

other related parties to retain a correct and true representation of lease assets and liabilities of

companies, especially for industries, for example, transport, airline and retail industries (Tran

and Zhu, 2017). Further, this typically offered stakeholders and investors an incorrect

representation of financial statement an incorrect account of the due expenses of the company,

stressing them to assume the obligations off the balance sheet, which generally lead

overestimations. Under the old standard, it was highly complex to make a comparison of

companies leasing with those companies who buy (De George and Shivakumar, 2016).

Requirement for change

There is a need for change; it is because the new accounting requirement will come up with

effective and optimal accounting till the ending of the twenty-first century, ending the engaged

guesswork while computing an often-considerable lease obligation of a company. Further, the

new standard will also offer more demanded transparency on the details relating to lease

transactions of the companies (Joubert, Garvie, and Parle, 2017).This means that all of the off-

balance sheet based lease financial will be no longer lurk in the shadows.

Furthermore, this will also offer adequate disclosure regarding ompanies that conduct lease and

those that conduct borrowing to buy assets. The IFRS 16 considerably carries forward the

accounting requirement of the lessor in the IAS 17. In accordance with the same, a lessor makes

continuous efforts to do the classification of leases as finance leases or operating leases

(Morales-Díaz and Zamora-Ramírez, 2018). The new Leases Standard has been attributed to

numerous rounds of board-level deliberation and public consultation, and all of them have been

carried out in the webcast and public. It can be said that IASB has operated closely with the US

Financial Accounting Standards Board (FASB) for the new standard development. In addition,

the two boards are in the line with the core issue of positioning leases on the balance sheet and

each and every lease (Wong and Joshi, 2015). The existing requirements for lease accounting in

the IAS 17 Leases have been long criticized for being unsuccessful in completing needs of

financial statement users, especially because of the reason that IAS 17 does not need lessees to

recognize assets and liabilities taking place from the operating leases.

Leasing offers a significant and flexible financing source for most of the companies. On the other

hand, the previous accounting standard, i.e. IAS Leases makes it complicated for investors and

other related parties to retain a correct and true representation of lease assets and liabilities of

companies, especially for industries, for example, transport, airline and retail industries (Tran

and Zhu, 2017). Further, this typically offered stakeholders and investors an incorrect

representation of financial statement an incorrect account of the due expenses of the company,

stressing them to assume the obligations off the balance sheet, which generally lead

overestimations. Under the old standard, it was highly complex to make a comparison of

companies leasing with those companies who buy (De George and Shivakumar, 2016).

Requirement for change

There is a need for change; it is because the new accounting requirement will come up with

effective and optimal accounting till the ending of the twenty-first century, ending the engaged

guesswork while computing an often-considerable lease obligation of a company. Further, the

new standard will also offer more demanded transparency on the details relating to lease

transactions of the companies (Joubert, Garvie, and Parle, 2017).This means that all of the off-

balance sheet based lease financial will be no longer lurk in the shadows.

Furthermore, this will also offer adequate disclosure regarding ompanies that conduct lease and

those that conduct borrowing to buy assets. The IFRS 16 considerably carries forward the

accounting requirement of the lessor in the IAS 17. In accordance with the same, a lessor makes

continuous efforts to do the classification of leases as finance leases or operating leases

(Morales-Díaz and Zamora-Ramírez, 2018). The new Leases Standard has been attributed to

numerous rounds of board-level deliberation and public consultation, and all of them have been

carried out in the webcast and public. It can be said that IASB has operated closely with the US

Financial Accounting Standards Board (FASB) for the new standard development. In addition,

the two boards are in the line with the core issue of positioning leases on the balance sheet and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

on the lease definition and in what ways measurement of the lease must be considered. It can be

reflected that the old standard for lease accounting no longer fit the purpose, so this major

revision was requires wherein companies can account for leases more accurately (Warren, 2016).

This change was thus needed; it is because it was not possible to compare business that lease

assets with the business who buy them, as a precise sign of the operating leases are eliminated

out of the equations (Magli, Nobolo, and Ogliari, 2018). The aim of the changes is to ensure that

all companies return information for the leased items as assets in a similar manner, converting

their existence more comparable and transparent on a financial basis. As well as disclosure

relating to lease which is not cancellable will also be provided in financial statements.

Types of changes incorporated in the AASB 16 new lease accounting standard

In the same way, IFRS Leases were introduced for the replacement of IAS 17 Leases and was

implemented promptly by AASB. Further, this new standard necessitates the lessee for the

recognition of leases on the financial position statement (Kabir and Rahman, 2018). The

accounting regime is considerably changed by the IFRS 16 for the lessees. Further, this new

requirement alleviates primarily off-balance sheet transactions for lessees as well as redefines

most of the employed financial metrics like the EBITDA and the gearing ratio and EBITDA.

Similarly, this will improvise comparability, but also impacts covenants, borrowing costs and

credit rates (van Kints and Spoor, 2019). Without a doubt, one of the greatest changes to the

accounting of lease is the outcomes of recognizing operating leases as per new accounting

standard would face big difference in several financial metrics.

The new Standard eradicates the classification of leases by the lessee as either finance leases or

operating leases. Rather, nearly all of the leases are capitalised with the recognition of a lease

liability as well as right-to-use asset above the balance sheet. The new standard changes the

overall treatment of operating leases with this the lessee’s book considerably. Before operating

leases stayed totally off the lessee’s balance sheet, on the other hand, with this standard, lessees

will be required to do recognition of right-to-use assets on the balance sheet, and simultaneously

a lease liability will be formed in the side of liability (Morales Díaz and Zamora Ramírez, 2018).

Changes in AASB 16 provides a more transparent and correct representation of the business

financial position by completely reflecting all the liabilities, while also offering valuable facts in

the financial reporting for shareholders as well as investors. Moreover, the new standard will also

reflected that the old standard for lease accounting no longer fit the purpose, so this major

revision was requires wherein companies can account for leases more accurately (Warren, 2016).

This change was thus needed; it is because it was not possible to compare business that lease

assets with the business who buy them, as a precise sign of the operating leases are eliminated

out of the equations (Magli, Nobolo, and Ogliari, 2018). The aim of the changes is to ensure that

all companies return information for the leased items as assets in a similar manner, converting

their existence more comparable and transparent on a financial basis. As well as disclosure

relating to lease which is not cancellable will also be provided in financial statements.

Types of changes incorporated in the AASB 16 new lease accounting standard

In the same way, IFRS Leases were introduced for the replacement of IAS 17 Leases and was

implemented promptly by AASB. Further, this new standard necessitates the lessee for the

recognition of leases on the financial position statement (Kabir and Rahman, 2018). The

accounting regime is considerably changed by the IFRS 16 for the lessees. Further, this new

requirement alleviates primarily off-balance sheet transactions for lessees as well as redefines

most of the employed financial metrics like the EBITDA and the gearing ratio and EBITDA.

Similarly, this will improvise comparability, but also impacts covenants, borrowing costs and

credit rates (van Kints and Spoor, 2019). Without a doubt, one of the greatest changes to the

accounting of lease is the outcomes of recognizing operating leases as per new accounting

standard would face big difference in several financial metrics.

The new Standard eradicates the classification of leases by the lessee as either finance leases or

operating leases. Rather, nearly all of the leases are capitalised with the recognition of a lease

liability as well as right-to-use asset above the balance sheet. The new standard changes the

overall treatment of operating leases with this the lessee’s book considerably. Before operating

leases stayed totally off the lessee’s balance sheet, on the other hand, with this standard, lessees

will be required to do recognition of right-to-use assets on the balance sheet, and simultaneously

a lease liability will be formed in the side of liability (Morales Díaz and Zamora Ramírez, 2018).

Changes in AASB 16 provides a more transparent and correct representation of the business

financial position by completely reflecting all the liabilities, while also offering valuable facts in

the financial reporting for shareholders as well as investors. Moreover, the new standard will also

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

chance the expense profile, instead of being a straight-line rental expenditure, there will be

highly expensed in initial years and lower in subsequent years. It also offers a basis for the

financial statement users for assessing the amount, uncertainty and timing of the cash flows

taking place from leases. For meeting that objective, a lessee is required to recognise assets as

well as liabilities occurring from a lease. IFRS 16 makes the introduction of an individual lessee

accounting model and needs a lessee for the recognition of assets and liabilities for each and

every lease with the term of over 12 months, till the time the underlying assets is of less value

(Fajardo, 2016).

Impact of change on companies having considerable lease financing level

IFRS can be likely to create a significant impact, especially for the business entities that have

formerly kept a large percentage of their finance leases off the balance sheet in the form of

operating leases. Further, the companies having material off-balance sheet lease commitments

will face considerable changes within the financial metrics like valuation multiples and leverage

ratio because of the IFRS 16 implication (Czajor and Michalak, 2017). The new leasing standard

will call for a major amount of new financial statement disclosures, in terms of quantitative as

well as qualitative, for lessees as well as lessors. This is inclusive of the information regarding

important estimations and judgements. Companies, by this, would face large impacts into their

balance sheet, yet the expenditure recognized in the income statement will most be expected not

to be impacted (Giner and Pardo, 2018).

It can be said that companies would be required to update their business procedures and

promoting technologies to adhere to the standards (Chen, Correia, and Urcan, 2018). IFRS 16

will also create a significant impact on the cash flow classification of the company and the needs

of its wide disclosure requirements within the financial statements. Business leasing assets will

materialize from the balance sheet to be richer in terms of asset, but they will also seem to carry

a larger debt pressure. The bigger the company’s lease number agreements would be, the bigger

the impact onto the balance sheet would be (James, 2016). If the company possess a huge finance

lease portfolio, then they will consider that the changes will dramatically impact their financial

ratios and key accounting rations. However this can also reduce the possible attractiveness of the

firm to investors and its capability for raising finance.

highly expensed in initial years and lower in subsequent years. It also offers a basis for the

financial statement users for assessing the amount, uncertainty and timing of the cash flows

taking place from leases. For meeting that objective, a lessee is required to recognise assets as

well as liabilities occurring from a lease. IFRS 16 makes the introduction of an individual lessee

accounting model and needs a lessee for the recognition of assets and liabilities for each and

every lease with the term of over 12 months, till the time the underlying assets is of less value

(Fajardo, 2016).

Impact of change on companies having considerable lease financing level

IFRS can be likely to create a significant impact, especially for the business entities that have

formerly kept a large percentage of their finance leases off the balance sheet in the form of

operating leases. Further, the companies having material off-balance sheet lease commitments

will face considerable changes within the financial metrics like valuation multiples and leverage

ratio because of the IFRS 16 implication (Czajor and Michalak, 2017). The new leasing standard

will call for a major amount of new financial statement disclosures, in terms of quantitative as

well as qualitative, for lessees as well as lessors. This is inclusive of the information regarding

important estimations and judgements. Companies, by this, would face large impacts into their

balance sheet, yet the expenditure recognized in the income statement will most be expected not

to be impacted (Giner and Pardo, 2018).

It can be said that companies would be required to update their business procedures and

promoting technologies to adhere to the standards (Chen, Correia, and Urcan, 2018). IFRS 16

will also create a significant impact on the cash flow classification of the company and the needs

of its wide disclosure requirements within the financial statements. Business leasing assets will

materialize from the balance sheet to be richer in terms of asset, but they will also seem to carry

a larger debt pressure. The bigger the company’s lease number agreements would be, the bigger

the impact onto the balance sheet would be (James, 2016). If the company possess a huge finance

lease portfolio, then they will consider that the changes will dramatically impact their financial

ratios and key accounting rations. However this can also reduce the possible attractiveness of the

firm to investors and its capability for raising finance.

Classification of most lease contracts as an operating lease by companies, and its relation of

manager’s behaviour

It can be said that companies seem indifferent in terms of leasing or buying, low tax rate

companies are more expected to make use of operating leases rather than finance leases, which is

stable with the aspect that companies with higher-effective rate of tax are more expected to

implement income reducing strategies like finance leases (Wong, Wong, and Jeter, 2016). The

anotehr rationale of company tending to choose recognition of lease as the operating lease is that

they are more willing to get expenditure deduction in the income tax, and with the same, they get

tax benefit advantage.

In relation to the positive accounting theory, it aims to create a relationship with a range of

people while depicting the use and implementation of accounting in operating such relations. It

helps the manager in determining overall economic outcomes. It forecast actions that take place

because of choosing the accounting policies by organization in a way wherein they react to the

new accounting standard implementation (Mellado and Parte, 2017). It can be said that in the

case manager can depict the lease as an operating lease, thus rent payment could be charged as

expenditure rather than asset recognition, but there is the presence of opportunity to decrease

debt amount. Thus, the positive accounting theory states that when managers have an option

between accounting methods, then they seek to reduce the adverse economic consequences of

accounting (Firth and Gounopoulos, 2017).

Expectancy from 1FRS 16 to improvise comparability between companies who are engaging in

leasing assets or borrowing to buy assets

IFRS will improvise the visibility of the lease commitments of the companies and effectively

represent economic reality. This new standard also facilitates financial statement users to make a

comparison of companies who lease their assets with those companies who borrow money to

purchase their assets, thereby forming a more level playing field (Lin, Riccardi, Wang, Hopkins,

and Kabureck, 2017).

The IASB expects that IFRS will substantially enhance the transparency and adequateness of of

financial information provided in financial statements.. It is because companies will do

recognition of assets and liabilities, in general, for all of the leases involved, does the

measurement of all lease assets as well as all lease liability simultaneously, and considers the

manager’s behaviour

It can be said that companies seem indifferent in terms of leasing or buying, low tax rate

companies are more expected to make use of operating leases rather than finance leases, which is

stable with the aspect that companies with higher-effective rate of tax are more expected to

implement income reducing strategies like finance leases (Wong, Wong, and Jeter, 2016). The

anotehr rationale of company tending to choose recognition of lease as the operating lease is that

they are more willing to get expenditure deduction in the income tax, and with the same, they get

tax benefit advantage.

In relation to the positive accounting theory, it aims to create a relationship with a range of

people while depicting the use and implementation of accounting in operating such relations. It

helps the manager in determining overall economic outcomes. It forecast actions that take place

because of choosing the accounting policies by organization in a way wherein they react to the

new accounting standard implementation (Mellado and Parte, 2017). It can be said that in the

case manager can depict the lease as an operating lease, thus rent payment could be charged as

expenditure rather than asset recognition, but there is the presence of opportunity to decrease

debt amount. Thus, the positive accounting theory states that when managers have an option

between accounting methods, then they seek to reduce the adverse economic consequences of

accounting (Firth and Gounopoulos, 2017).

Expectancy from 1FRS 16 to improvise comparability between companies who are engaging in

leasing assets or borrowing to buy assets

IFRS will improvise the visibility of the lease commitments of the companies and effectively

represent economic reality. This new standard also facilitates financial statement users to make a

comparison of companies who lease their assets with those companies who borrow money to

purchase their assets, thereby forming a more level playing field (Lin, Riccardi, Wang, Hopkins,

and Kabureck, 2017).

The IASB expects that IFRS will substantially enhance the transparency and adequateness of of

financial information provided in financial statements.. It is because companies will do

recognition of assets and liabilities, in general, for all of the leases involved, does the

measurement of all lease assets as well as all lease liability simultaneously, and considers the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

recognition of just the rights that are acquired and the incurred liabilities. Consequently, the

financial statement will showcase the varying operating based decisions made by the various

companies (Cullen, van de Ven, and Zwijnenburg, 2017). IT then adds comparability as well as

transparency onto the balance sheet, and the users of financial statement can have a clear picture

of operating leases and have a helpful base for comparatively with other related companies. It

can be stated that, if the lease is economically same to borrowing in order to purchase an asset,

taking an example of a lease of a new aircraft for more than 20 years, then the reported amount

applicable to the IFRS 16 would be same to the amounts that are reported in case the company

borrows to buy aircraft (De Gennaro, 2017). Thus, the reported assets and liabilities would be

lower than the expected, if the company would borrow to buy the aircraft. In such case, the right

to use the asset by the company for 7 years is comparatively distinct from the rights that it would

acquire if it buys the aircraft (Hoitash and et.al. 2018).

Explanation of the tendency reporting entities have in buying more assets and lesser lease assets

after the adoption of AASB 16

It has been acknowledged by the IASB that the changes within the lease accounting can create an

impact over the leasing market, in case the companies make decisions to buy more of assets and

as a result, lease fewer assets. Further, IASB views that there are several reasons behind the

aspect of why the company does leasing of assets that continue to take place, after the effective

implementation of IFRS 16 (Freeman, 2018). Thus, the IASB has not supposed considerable

behavioural changes at the time when IFRS 16 come into effect that is a company is not likely to

methodically borrow to buy assets instead of leasing them, as a consequence, of the accounting

change.

The IASB assessed if or if not the IFRS 16 might influence relating to decision of purchase of

asset that would eventually impact the leasing market. For instance, due to the requirement for

lease accounting in IFRS 16 offer higher comparability among those business leasing assets and

those business buying assets, further, a company can make a decision to buy assets instead of

leasing them (McCall, 2017). It has been expected by the IASB that some of the companies

make the decision to buy certain assets than leasing them, specifically if they were to pay higher

for leases as the reporting of those leases were no done onto the balance sheet. Even if certain

companies make decisions to emerge into few leases, then they still require asset financing, and

financial statement will showcase the varying operating based decisions made by the various

companies (Cullen, van de Ven, and Zwijnenburg, 2017). IT then adds comparability as well as

transparency onto the balance sheet, and the users of financial statement can have a clear picture

of operating leases and have a helpful base for comparatively with other related companies. It

can be stated that, if the lease is economically same to borrowing in order to purchase an asset,

taking an example of a lease of a new aircraft for more than 20 years, then the reported amount

applicable to the IFRS 16 would be same to the amounts that are reported in case the company

borrows to buy aircraft (De Gennaro, 2017). Thus, the reported assets and liabilities would be

lower than the expected, if the company would borrow to buy the aircraft. In such case, the right

to use the asset by the company for 7 years is comparatively distinct from the rights that it would

acquire if it buys the aircraft (Hoitash and et.al. 2018).

Explanation of the tendency reporting entities have in buying more assets and lesser lease assets

after the adoption of AASB 16

It has been acknowledged by the IASB that the changes within the lease accounting can create an

impact over the leasing market, in case the companies make decisions to buy more of assets and

as a result, lease fewer assets. Further, IASB views that there are several reasons behind the

aspect of why the company does leasing of assets that continue to take place, after the effective

implementation of IFRS 16 (Freeman, 2018). Thus, the IASB has not supposed considerable

behavioural changes at the time when IFRS 16 come into effect that is a company is not likely to

methodically borrow to buy assets instead of leasing them, as a consequence, of the accounting

change.

The IASB assessed if or if not the IFRS 16 might influence relating to decision of purchase of

asset that would eventually impact the leasing market. For instance, due to the requirement for

lease accounting in IFRS 16 offer higher comparability among those business leasing assets and

those business buying assets, further, a company can make a decision to buy assets instead of

leasing them (McCall, 2017). It has been expected by the IASB that some of the companies

make the decision to buy certain assets than leasing them, specifically if they were to pay higher

for leases as the reporting of those leases were no done onto the balance sheet. Even if certain

companies make decisions to emerge into few leases, then they still require asset financing, and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the same is generally offered by suppliers, leasing assets too (Poole, Rivat, and Berger, 2019). In

accordance with the same, certain lesser might lease fewer assets but offer greater financing for

assets for a higher number of assets.

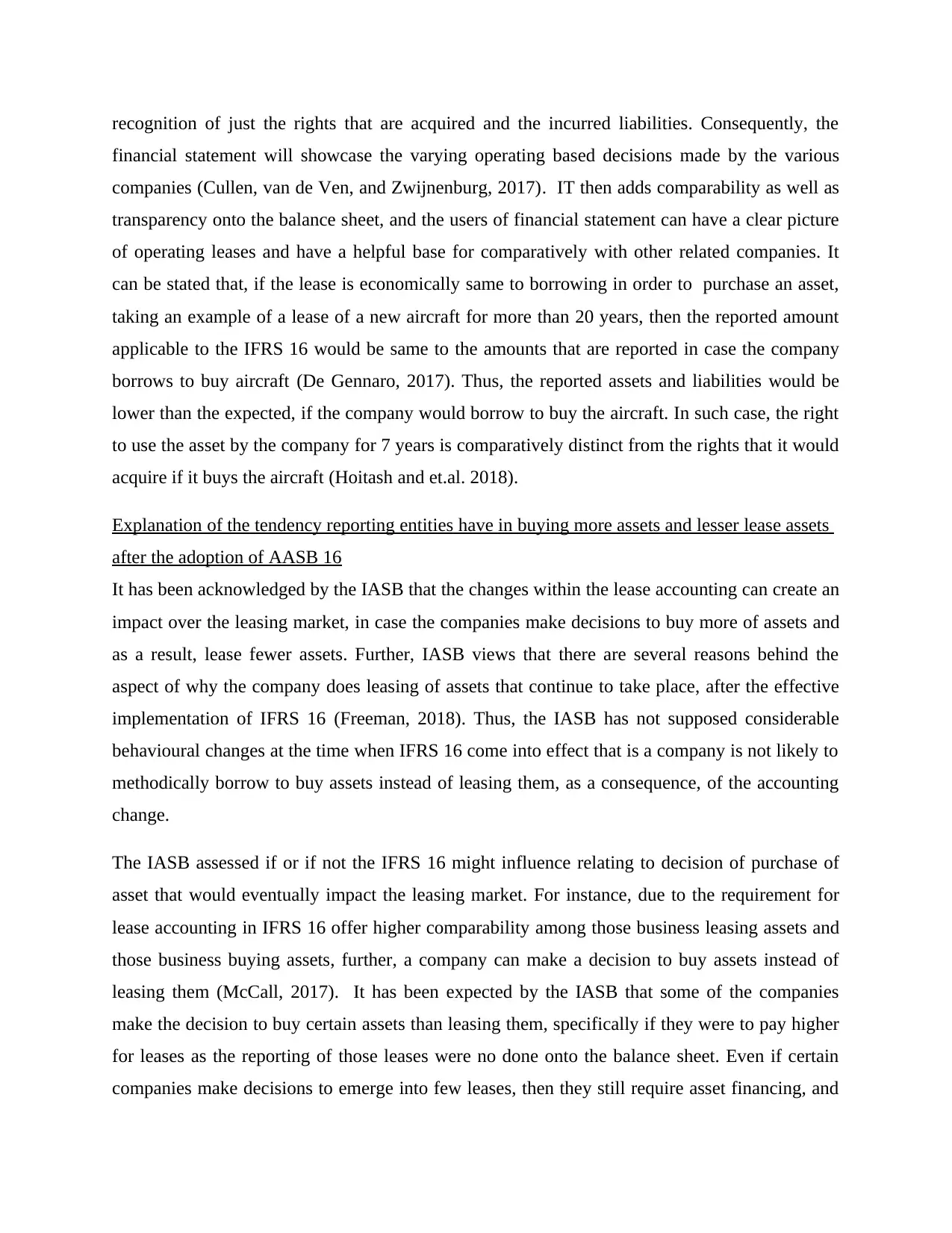

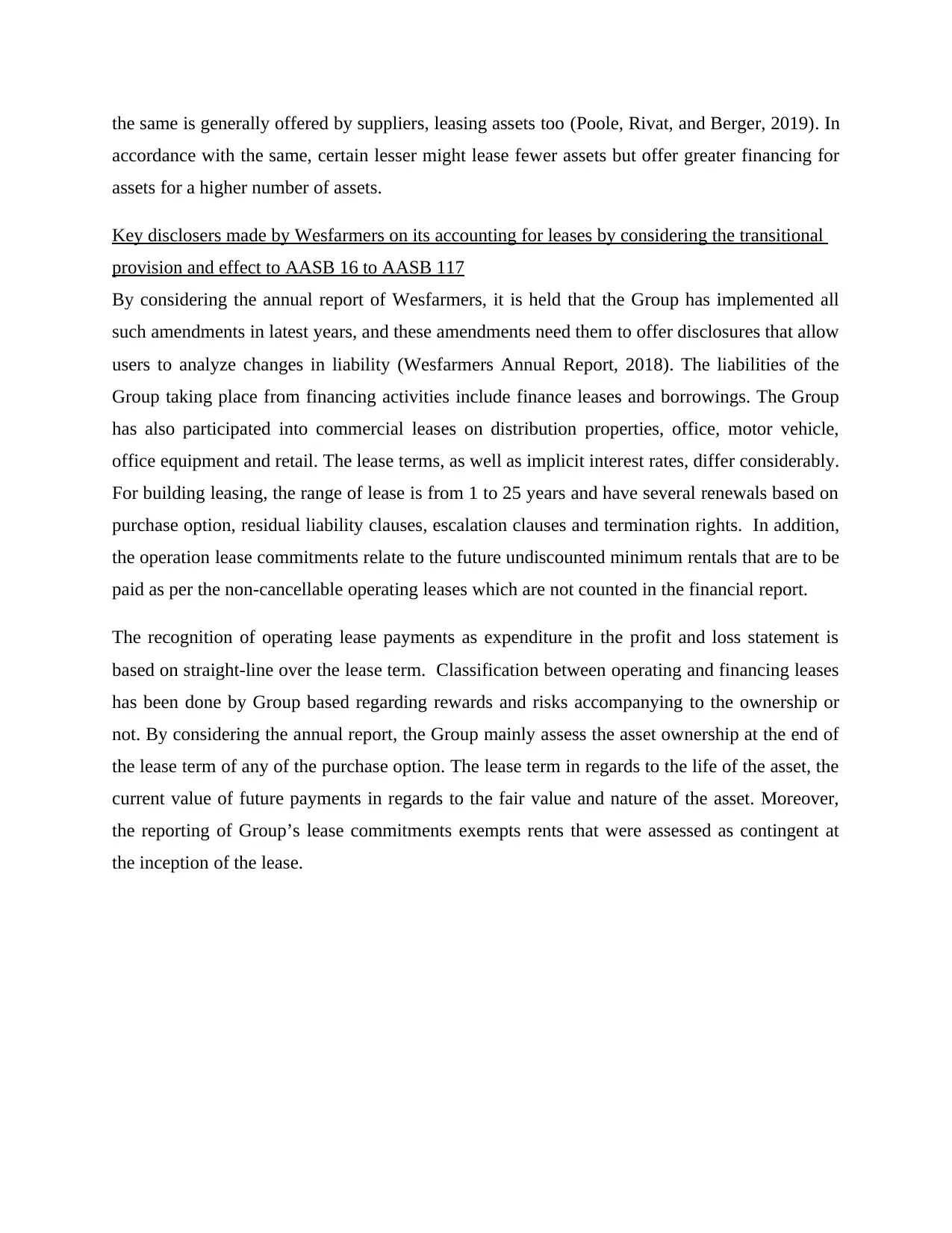

Key disclosers made by Wesfarmers on its accounting for leases by considering the transitional

provision and effect to AASB 16 to AASB 117

By considering the annual report of Wesfarmers, it is held that the Group has implemented all

such amendments in latest years, and these amendments need them to offer disclosures that allow

users to analyze changes in liability (Wesfarmers Annual Report, 2018). The liabilities of the

Group taking place from financing activities include finance leases and borrowings. The Group

has also participated into commercial leases on distribution properties, office, motor vehicle,

office equipment and retail. The lease terms, as well as implicit interest rates, differ considerably.

For building leasing, the range of lease is from 1 to 25 years and have several renewals based on

purchase option, residual liability clauses, escalation clauses and termination rights. In addition,

the operation lease commitments relate to the future undiscounted minimum rentals that are to be

paid as per the non-cancellable operating leases which are not counted in the financial report.

The recognition of operating lease payments as expenditure in the profit and loss statement is

based on straight-line over the lease term. Classification between operating and financing leases

has been done by Group based regarding rewards and risks accompanying to the ownership or

not. By considering the annual report, the Group mainly assess the asset ownership at the end of

the lease term of any of the purchase option. The lease term in regards to the life of the asset, the

current value of future payments in regards to the fair value and nature of the asset. Moreover,

the reporting of Group’s lease commitments exempts rents that were assessed as contingent at

the inception of the lease.

accordance with the same, certain lesser might lease fewer assets but offer greater financing for

assets for a higher number of assets.

Key disclosers made by Wesfarmers on its accounting for leases by considering the transitional

provision and effect to AASB 16 to AASB 117

By considering the annual report of Wesfarmers, it is held that the Group has implemented all

such amendments in latest years, and these amendments need them to offer disclosures that allow

users to analyze changes in liability (Wesfarmers Annual Report, 2018). The liabilities of the

Group taking place from financing activities include finance leases and borrowings. The Group

has also participated into commercial leases on distribution properties, office, motor vehicle,

office equipment and retail. The lease terms, as well as implicit interest rates, differ considerably.

For building leasing, the range of lease is from 1 to 25 years and have several renewals based on

purchase option, residual liability clauses, escalation clauses and termination rights. In addition,

the operation lease commitments relate to the future undiscounted minimum rentals that are to be

paid as per the non-cancellable operating leases which are not counted in the financial report.

The recognition of operating lease payments as expenditure in the profit and loss statement is

based on straight-line over the lease term. Classification between operating and financing leases

has been done by Group based regarding rewards and risks accompanying to the ownership or

not. By considering the annual report, the Group mainly assess the asset ownership at the end of

the lease term of any of the purchase option. The lease term in regards to the life of the asset, the

current value of future payments in regards to the fair value and nature of the asset. Moreover,

the reporting of Group’s lease commitments exempts rents that were assessed as contingent at

the inception of the lease.

Figure 1: Group operating lease commitments as lessee

Source: (Wesfarmers Annual Report, 2018)

Figure 2: Commitment and Contingencies

Source: (Wesfarmers Annual Report, 2018)

However, it has been planned by the Group to implement the modified retrospective transition

approach in which there is a choice based on the lease-by-lease basis for the calculation of the

right-of-use asset (ROU) as equivalent to the lease liability or in regards with the historical lease

payments. Information on the operating lease commitment undiscounted amount of the Group

has been provided at the 30 June 2018 as per the provisions of AASB 117, and the new lease

standard requires provided detail disclosure relating to transactions of the lease. In accordance

with the AASB 16, the value of the current commitment would be presented as a liability onto

the balance sheet along with the asset showing ROU. It is held that a project team has been

engaged in the management of the transition, as the Group analyze the AASB 16 implications. It

Source: (Wesfarmers Annual Report, 2018)

Figure 2: Commitment and Contingencies

Source: (Wesfarmers Annual Report, 2018)

However, it has been planned by the Group to implement the modified retrospective transition

approach in which there is a choice based on the lease-by-lease basis for the calculation of the

right-of-use asset (ROU) as equivalent to the lease liability or in regards with the historical lease

payments. Information on the operating lease commitment undiscounted amount of the Group

has been provided at the 30 June 2018 as per the provisions of AASB 117, and the new lease

standard requires provided detail disclosure relating to transactions of the lease. In accordance

with the AASB 16, the value of the current commitment would be presented as a liability onto

the balance sheet along with the asset showing ROU. It is held that a project team has been

engaged in the management of the transition, as the Group analyze the AASB 16 implications. It

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.