Accounting for Leases: A Critical Review of AASB 16 in Australia

VerifiedAdded on 2023/03/21

|11

|3829

|88

Report

AI Summary

This report critically examines the Australian Accounting Standard for leases, AASB 16, in the context of the HI6025 Accounting Theory and Current Issues course at Holmes Institute. It provides a comprehensive overview of the standard, including its objectives, and significance. The report delves into the drawbacks of the previous standard, AASB 117, and the reasons that prompted the shift to AASB 16. It explains the key changes incorporated in AASB 16, such as the single lease accounting model, the recognition of right-of-use assets and lease liabilities, and the new requirements for lease classification and measurement. Furthermore, the report explores the impact of AASB 16 on financial reporting, including increased transparency and faithful representation. It also touches on the previous preference for operating lease classification and its implications. The report covers the definition of leases, the identification of a lease, and the measurement of the leased asset's cost. Overall, the report provides a critical review of the standard and demonstrates understanding of the key issues and changes in the accounting for leases.

Australian Accounting Standards 1

AUSTRALIAN ACCOUNTING STANDARDS

By Students Name

Course Name

Professor’s name

Institution

Date

AUSTRALIAN ACCOUNTING STANDARDS

By Students Name

Course Name

Professor’s name

Institution

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Australian Accounting Standards 2

Table of Contents

Abstract

Diverse research has been conducted concerning the accounting for the two types of

leases. The primary objective of this essay is to examine the accounting standards for

leases and why a single lease accounting model replaced the old accounting standards.

The old accounting standard AASB 117 is analyzed and the flaws that existed discussed

in a bid to understand the new standard. The Australian Accounting Standards for leases

AASB 16 is critically analyzed and how it has brought positive changes in accounting for

leases. The new standard is explained, and the treatments for the leases explained

including details of existence and costing for leases. The way the new standard has

increased faithful reporting is also explained in the essay. Previous preference of

classification of leases will be touched and why firms preferred particular classification.

Leases will be defined and their new mode of reporting in financial statements included.

Australian Accounting Standard AASB 16

Introduction

Accounting standards are reporting standards prescribed for financial reporting. The

standards are developed universally hence recognized internationally. Accounting

standard prescribes how to recognize, measure, present, and disclose financial

information for purposes of reporting. The main aim of any standard is to ensure that

information disclosed by companies is relevant and represents the transactions faithfully

(Shough, 2011). The accounting standards are set by policymakers who come up with

new standards and amend the existing once where necessary. Due to new developments

and setbacks in existing standards, they are subject to constant amendment. Drawbacks

necessitate the changes in the existing standards and new developments that need to be

included in the sector.

The International Financial Reporting Standards (IFRS) contains the fact sheet for

reporting requirements which are either adopted entirely or amended. It can be noted,

however, that some standards have failed to present a faithful view of the transactions

Table of Contents

Abstract

Diverse research has been conducted concerning the accounting for the two types of

leases. The primary objective of this essay is to examine the accounting standards for

leases and why a single lease accounting model replaced the old accounting standards.

The old accounting standard AASB 117 is analyzed and the flaws that existed discussed

in a bid to understand the new standard. The Australian Accounting Standards for leases

AASB 16 is critically analyzed and how it has brought positive changes in accounting for

leases. The new standard is explained, and the treatments for the leases explained

including details of existence and costing for leases. The way the new standard has

increased faithful reporting is also explained in the essay. Previous preference of

classification of leases will be touched and why firms preferred particular classification.

Leases will be defined and their new mode of reporting in financial statements included.

Australian Accounting Standard AASB 16

Introduction

Accounting standards are reporting standards prescribed for financial reporting. The

standards are developed universally hence recognized internationally. Accounting

standard prescribes how to recognize, measure, present, and disclose financial

information for purposes of reporting. The main aim of any standard is to ensure that

information disclosed by companies is relevant and represents the transactions faithfully

(Shough, 2011). The accounting standards are set by policymakers who come up with

new standards and amend the existing once where necessary. Due to new developments

and setbacks in existing standards, they are subject to constant amendment. Drawbacks

necessitate the changes in the existing standards and new developments that need to be

included in the sector.

The International Financial Reporting Standards (IFRS) contains the fact sheet for

reporting requirements which are either adopted entirely or amended. It can be noted,

however, that some standards have failed to present a faithful view of the transactions

Australian Accounting Standards 3

while others are very complicated to use. The AASB 16 is an Australian accounting

standard reporting requirements for leasing. While IAS 16 is the accounting standard

requirement recognized internationally (Chalmers, Clinch, and Godfrey, 2011). A lease is

an agreement or a section of an arrangement that gives a party the right to use a particular

asset for a stated time in exchange for consideration.

The Australian Accounting Standards Board

AASB was founded in the year 1991 with Scott Morrison as the current minister

responsible for it and had jurisdiction in Australia. It is the government agency that

develops issues and maintains financial standards of reporting for both private and public

entities in Australia. AASB is tasked with:

Development of the conceptual framework for standard’s evaluation.

Setting up of accounting principle as prescribed under section 334 of the

Corporations Act 2001.

Formulation of accounting standards for other purposes

Participation and contribution in the expansion of worldwide accounting principles

that are a single set

Advancement and promotion of the main objects of Part 12 of the Australian

Securities and Investment Commission Act (Chalmers, Clinch, and Godfrey, 2011).

These include reduction of the cost of capital, which promotes effective competition

overseas by Australian entities, thereby maintaining investor confidence in the

economy.

The accounting Standard for Leases (AASB 117)

IAS 17 and IAS 16 are the accounting standards for leases. IAS 17 was the previous

accounting standards applicable internationally before the principles were discovered to be

flawed. This resulted in a pact between the Financial Accounting Standards and

International Accounting Standards Board the to propose new accounting principle

applicable for leases. The proposed standard was to be an improvement of the existing

and designed to report on the leasing transaction’s economics faithfully. The two bodies

proposed a standard that was principle-based and applicable internationally. This resulted

in a convergence of the accounting bodies and joint introduction of IAS 16 (Chalmers,

Clinch, and Godfrey, 2011). The AASB 16 standards are the standards applicable

while others are very complicated to use. The AASB 16 is an Australian accounting

standard reporting requirements for leasing. While IAS 16 is the accounting standard

requirement recognized internationally (Chalmers, Clinch, and Godfrey, 2011). A lease is

an agreement or a section of an arrangement that gives a party the right to use a particular

asset for a stated time in exchange for consideration.

The Australian Accounting Standards Board

AASB was founded in the year 1991 with Scott Morrison as the current minister

responsible for it and had jurisdiction in Australia. It is the government agency that

develops issues and maintains financial standards of reporting for both private and public

entities in Australia. AASB is tasked with:

Development of the conceptual framework for standard’s evaluation.

Setting up of accounting principle as prescribed under section 334 of the

Corporations Act 2001.

Formulation of accounting standards for other purposes

Participation and contribution in the expansion of worldwide accounting principles

that are a single set

Advancement and promotion of the main objects of Part 12 of the Australian

Securities and Investment Commission Act (Chalmers, Clinch, and Godfrey, 2011).

These include reduction of the cost of capital, which promotes effective competition

overseas by Australian entities, thereby maintaining investor confidence in the

economy.

The accounting Standard for Leases (AASB 117)

IAS 17 and IAS 16 are the accounting standards for leases. IAS 17 was the previous

accounting standards applicable internationally before the principles were discovered to be

flawed. This resulted in a pact between the Financial Accounting Standards and

International Accounting Standards Board the to propose new accounting principle

applicable for leases. The proposed standard was to be an improvement of the existing

and designed to report on the leasing transaction’s economics faithfully. The two bodies

proposed a standard that was principle-based and applicable internationally. This resulted

in a convergence of the accounting bodies and joint introduction of IAS 16 (Chalmers,

Clinch, and Godfrey, 2011). The AASB 16 standards are the standards applicable

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Australian Accounting Standards 4

specifically to leases Australia. They replaced the AASB 17, which was applicable before

the new standards.

Draw Backs in the AASB 117

AASB 17 on leases was discovered to have several flaws necessitating review to come up

with better standards. The review was proposed in July 2006 when a party was formed

between IASB and FASB, which proposed the new standards (Brown, Preiato, and Tarca,

2014). The drawbacks of the old accounting standards included:

a) The difference in financial leases- A clear line between the operation and finance

lease was never drawn. As a result, there was no principled difference between

operating and finance leases.

b) Accounting difference for similar transactions-Due to the unclear dividing line

between the financing and operating lease, it was discovered that same

transactions were differently accounted for. This results in a difference in financial

reports for duplicate transactions.

c) Difference in obligation- For operating leases, there was no recognition as

liabilities whereas the obligations for non-cancellable leases treated differently from

borrowings.

d) Overstated return on assets- Assets used and held by the business under the

operating lease are not included in the balance sheet. The lack of disclosure of

these assets results in an overstatement of return on assets for the business.

e) Inconsistencies between similar transactions- Leases are always scoped from

financial instrument standards. As a result, inconsistencies are prone to leases

treatments and similar transactions.

f) Conflict in lessor accounting- For a Lessor, the deferral and matching accounting

is applied, which is very different from the direction the project is likely to recognize

revenue.

Reasons for Accounting Standards Change

The drawbacks of AAS17 that brought in inconsistencies in reporting necessitated the

changes in the standards. This resulted in great challenged on the judgment of objectivity

in the reporting for both operating and financing lease (Shough, 2011). However, the

specifically to leases Australia. They replaced the AASB 17, which was applicable before

the new standards.

Draw Backs in the AASB 117

AASB 17 on leases was discovered to have several flaws necessitating review to come up

with better standards. The review was proposed in July 2006 when a party was formed

between IASB and FASB, which proposed the new standards (Brown, Preiato, and Tarca,

2014). The drawbacks of the old accounting standards included:

a) The difference in financial leases- A clear line between the operation and finance

lease was never drawn. As a result, there was no principled difference between

operating and finance leases.

b) Accounting difference for similar transactions-Due to the unclear dividing line

between the financing and operating lease, it was discovered that same

transactions were differently accounted for. This results in a difference in financial

reports for duplicate transactions.

c) Difference in obligation- For operating leases, there was no recognition as

liabilities whereas the obligations for non-cancellable leases treated differently from

borrowings.

d) Overstated return on assets- Assets used and held by the business under the

operating lease are not included in the balance sheet. The lack of disclosure of

these assets results in an overstatement of return on assets for the business.

e) Inconsistencies between similar transactions- Leases are always scoped from

financial instrument standards. As a result, inconsistencies are prone to leases

treatments and similar transactions.

f) Conflict in lessor accounting- For a Lessor, the deferral and matching accounting

is applied, which is very different from the direction the project is likely to recognize

revenue.

Reasons for Accounting Standards Change

The drawbacks of AAS17 that brought in inconsistencies in reporting necessitated the

changes in the standards. This resulted in great challenged on the judgment of objectivity

in the reporting for both operating and financing lease (Shough, 2011). However, the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Australian Accounting Standards 5

classification of leases as financing or operating lease was another field that needed

review. The removal is necessitated by:

I. All leases assign the right to use the property; as a result, a single conceptual

framework for accounting is preferred.

II. The main aim of accounting standards is to simplify accounting. The removal of the

separation could, therefore, result in simple accounting, which is desirable.

III. Classification is a cumbersome process that leads to different classification of

similar transaction (Sacarin, 2017.). As a result, removal of classification will make

treatment of similar transactions the same.

IV. Inconsistencies on the determination of minimum lease payments for classification

purposes an example is the treatment of contingent rentals as finance lease but not

operating lease.

V. Complexity in the introduction of new standards which could implement next to

impossible because the variance in current requirements of accounting

The changes in the AASB 17 were therefore long overdue as the comparison of similar

firms with a different classification of leases was never objective (Shough, 2011). The two

bodies tasked with setting up standards and amendment, therefore, came up with the new

standard AASB 16. The standards were first introduced on the 13th of January 2016. The

effective date set for transition is 1st January 2019. Businesses were, however, free to start

implementation prior to the date. The implementation is required to either employ the full

retrospective technique or cumulative catch-up technique. The full retrospective technique

is where restatement of information that is comparative in conformity with I.A.S 8

accounting procedures, error variations in accounting approximates. On the other hand,

Cumulative catch method is the system that does not restate comparatives. Adjustment to

equity on the initial application date results from the cumulative effect of initial application.

Previous Preference of Classification as Operating Lease

Businesses classified their leases in most cases operating other than financing leases

previously when AASB 117 standards of leasing were applicable. The accounting

treatment for operating leases is treatment as renting; therefore, lease payments are

treated as operating expenses (Shough, 2011). The leased asset is not involved in the

balance sheet, unlike a financing lease whose leased assets are disclosed in the financial

classification of leases as financing or operating lease was another field that needed

review. The removal is necessitated by:

I. All leases assign the right to use the property; as a result, a single conceptual

framework for accounting is preferred.

II. The main aim of accounting standards is to simplify accounting. The removal of the

separation could, therefore, result in simple accounting, which is desirable.

III. Classification is a cumbersome process that leads to different classification of

similar transaction (Sacarin, 2017.). As a result, removal of classification will make

treatment of similar transactions the same.

IV. Inconsistencies on the determination of minimum lease payments for classification

purposes an example is the treatment of contingent rentals as finance lease but not

operating lease.

V. Complexity in the introduction of new standards which could implement next to

impossible because the variance in current requirements of accounting

The changes in the AASB 17 were therefore long overdue as the comparison of similar

firms with a different classification of leases was never objective (Shough, 2011). The two

bodies tasked with setting up standards and amendment, therefore, came up with the new

standard AASB 16. The standards were first introduced on the 13th of January 2016. The

effective date set for transition is 1st January 2019. Businesses were, however, free to start

implementation prior to the date. The implementation is required to either employ the full

retrospective technique or cumulative catch-up technique. The full retrospective technique

is where restatement of information that is comparative in conformity with I.A.S 8

accounting procedures, error variations in accounting approximates. On the other hand,

Cumulative catch method is the system that does not restate comparatives. Adjustment to

equity on the initial application date results from the cumulative effect of initial application.

Previous Preference of Classification as Operating Lease

Businesses classified their leases in most cases operating other than financing leases

previously when AASB 117 standards of leasing were applicable. The accounting

treatment for operating leases is treatment as renting; therefore, lease payments are

treated as operating expenses (Shough, 2011). The leased asset is not involved in the

balance sheet, unlike a financing lease whose leased assets are disclosed in the financial

Australian Accounting Standards 6

position statement. The leased asset is treated as a loan hence ownership considered by

the lessee. The disclosure of the lease in a balance sheet made the financing lessee less

desirable to business owners. The exclusion in the financial position statement as well

gave the operating lease an added advantage as the return on investment was increased.

New Accounting Standard AASB 16

This is the newly introduced standard for reporting of leases that replaced the flawed

AASB 17. The standard is in operation after its introduction in 2016. It is an accounting

model employing the single lease method in lease classification. AASB 16 requires entities

to recognize liabilities and assets relating to both financing and operating leases with

contracts lasting more than 12months (Biondi, Bloomfield, Glover, Jamal, Ohlson,

Penman, Tsujiyama, and Wilks, 2011). The requirement, however, does not cover leases

where the particular has low value. The standards prescribe the lease to recognize leases

in the financial statement in order to eliminate overstatement of return on assets. The

right-of-use asset and the lease obligation is subject to recognition in the new standards.

Unlike the previous lease accounting that measured the right-of-use based on the liability

of the lease with adjustments on the prepayments of rent, incentives and costs incurred

the new standards account similar to financial liability (Eccles, Krzus, Rogers, and

Serafeim, 2012). AASB 16 requires extensive and different disclosures, which includes

qualitative and quantitative activities pertaining to leasing. The disclosure aims at the

provision of information on financial statements, which include the timing, uncertainties,

and cash flow from leases.

Exceptions

The AASB 16, however, does not apply where the lease is short term and where the

leased asset is of low value. Such a situation where the lessor does not apply the

standards the lessee is required to recognize lease payments in relation to the leases as

expense (Joubert, Garvie, and Parle, 2017). A lease modification or any changes made to

the lease warrants entry of the modified lease as a new lease during reporting.

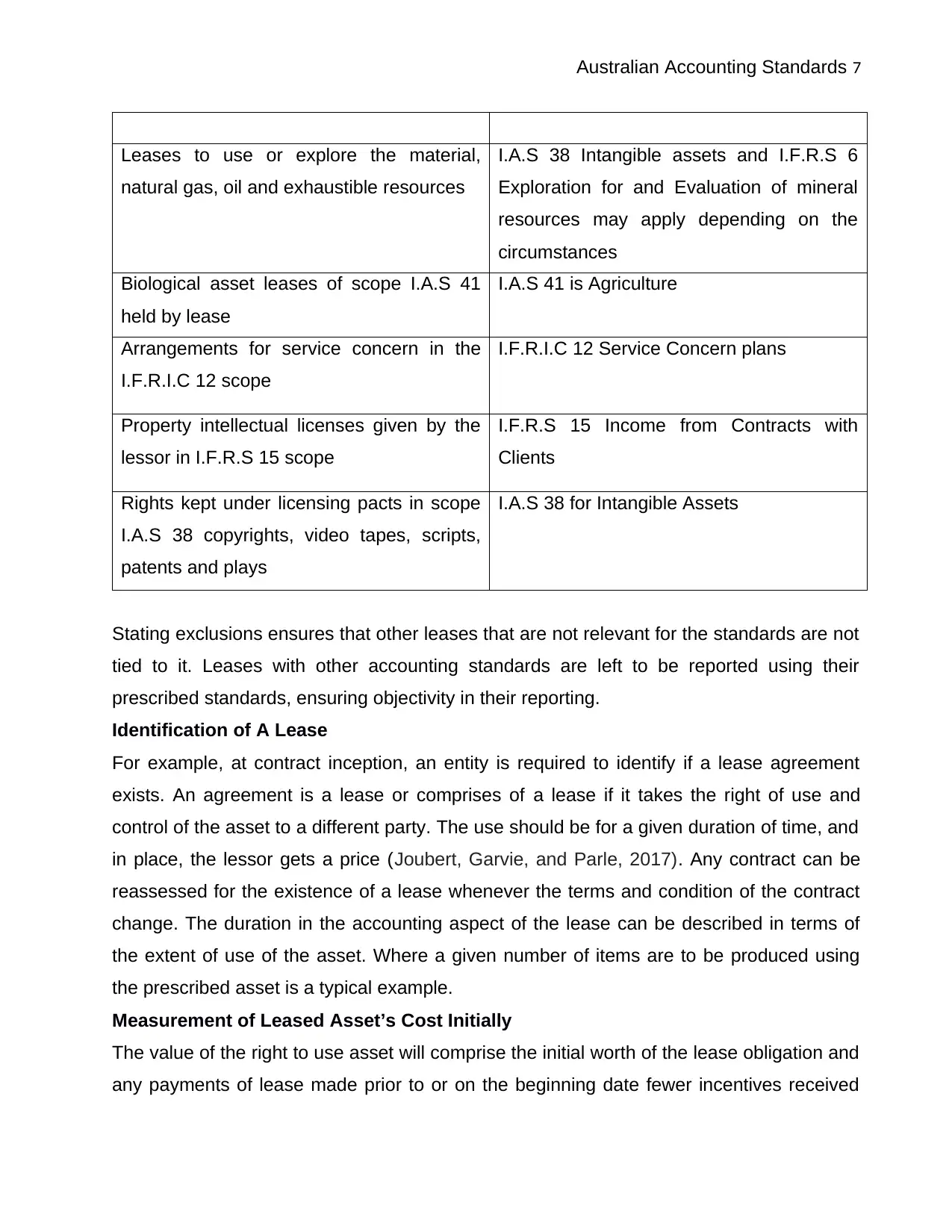

The AASB 16, however, has exclusion, which is situations when the AASB 16 standards

do not apply but other specified or unspecified standards. The exceptions are tabled

below.

Scope Exclusion Standard Applicable

position statement. The leased asset is treated as a loan hence ownership considered by

the lessee. The disclosure of the lease in a balance sheet made the financing lessee less

desirable to business owners. The exclusion in the financial position statement as well

gave the operating lease an added advantage as the return on investment was increased.

New Accounting Standard AASB 16

This is the newly introduced standard for reporting of leases that replaced the flawed

AASB 17. The standard is in operation after its introduction in 2016. It is an accounting

model employing the single lease method in lease classification. AASB 16 requires entities

to recognize liabilities and assets relating to both financing and operating leases with

contracts lasting more than 12months (Biondi, Bloomfield, Glover, Jamal, Ohlson,

Penman, Tsujiyama, and Wilks, 2011). The requirement, however, does not cover leases

where the particular has low value. The standards prescribe the lease to recognize leases

in the financial statement in order to eliminate overstatement of return on assets. The

right-of-use asset and the lease obligation is subject to recognition in the new standards.

Unlike the previous lease accounting that measured the right-of-use based on the liability

of the lease with adjustments on the prepayments of rent, incentives and costs incurred

the new standards account similar to financial liability (Eccles, Krzus, Rogers, and

Serafeim, 2012). AASB 16 requires extensive and different disclosures, which includes

qualitative and quantitative activities pertaining to leasing. The disclosure aims at the

provision of information on financial statements, which include the timing, uncertainties,

and cash flow from leases.

Exceptions

The AASB 16, however, does not apply where the lease is short term and where the

leased asset is of low value. Such a situation where the lessor does not apply the

standards the lessee is required to recognize lease payments in relation to the leases as

expense (Joubert, Garvie, and Parle, 2017). A lease modification or any changes made to

the lease warrants entry of the modified lease as a new lease during reporting.

The AASB 16, however, has exclusion, which is situations when the AASB 16 standards

do not apply but other specified or unspecified standards. The exceptions are tabled

below.

Scope Exclusion Standard Applicable

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Australian Accounting Standards 7

Leases to use or explore the material,

natural gas, oil and exhaustible resources

I.A.S 38 Intangible assets and I.F.R.S 6

Exploration for and Evaluation of mineral

resources may apply depending on the

circumstances

Biological asset leases of scope I.A.S 41

held by lease

I.A.S 41 is Agriculture

Arrangements for service concern in the

I.F.R.I.C 12 scope

I.F.R.I.C 12 Service Concern plans

Property intellectual licenses given by the

lessor in I.F.R.S 15 scope

I.F.R.S 15 Income from Contracts with

Clients

Rights kept under licensing pacts in scope

I.A.S 38 copyrights, video tapes, scripts,

patents and plays

I.A.S 38 for Intangible Assets

Stating exclusions ensures that other leases that are not relevant for the standards are not

tied to it. Leases with other accounting standards are left to be reported using their

prescribed standards, ensuring objectivity in their reporting.

Identification of A Lease

For example, at contract inception, an entity is required to identify if a lease agreement

exists. An agreement is a lease or comprises of a lease if it takes the right of use and

control of the asset to a different party. The use should be for a given duration of time, and

in place, the lessor gets a price (Joubert, Garvie, and Parle, 2017). Any contract can be

reassessed for the existence of a lease whenever the terms and condition of the contract

change. The duration in the accounting aspect of the lease can be described in terms of

the extent of use of the asset. Where a given number of items are to be produced using

the prescribed asset is a typical example.

Measurement of Leased Asset’s Cost Initially

The value of the right to use asset will comprise the initial worth of the lease obligation and

any payments of lease made prior to or on the beginning date fewer incentives received

Leases to use or explore the material,

natural gas, oil and exhaustible resources

I.A.S 38 Intangible assets and I.F.R.S 6

Exploration for and Evaluation of mineral

resources may apply depending on the

circumstances

Biological asset leases of scope I.A.S 41

held by lease

I.A.S 41 is Agriculture

Arrangements for service concern in the

I.F.R.I.C 12 scope

I.F.R.I.C 12 Service Concern plans

Property intellectual licenses given by the

lessor in I.F.R.S 15 scope

I.F.R.S 15 Income from Contracts with

Clients

Rights kept under licensing pacts in scope

I.A.S 38 copyrights, video tapes, scripts,

patents and plays

I.A.S 38 for Intangible Assets

Stating exclusions ensures that other leases that are not relevant for the standards are not

tied to it. Leases with other accounting standards are left to be reported using their

prescribed standards, ensuring objectivity in their reporting.

Identification of A Lease

For example, at contract inception, an entity is required to identify if a lease agreement

exists. An agreement is a lease or comprises of a lease if it takes the right of use and

control of the asset to a different party. The use should be for a given duration of time, and

in place, the lessor gets a price (Joubert, Garvie, and Parle, 2017). Any contract can be

reassessed for the existence of a lease whenever the terms and condition of the contract

change. The duration in the accounting aspect of the lease can be described in terms of

the extent of use of the asset. Where a given number of items are to be produced using

the prescribed asset is a typical example.

Measurement of Leased Asset’s Cost Initially

The value of the right to use asset will comprise the initial worth of the lease obligation and

any payments of lease made prior to or on the beginning date fewer incentives received

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Australian Accounting Standards 8

(Brown, Preiato, and Tarca, 2014). The incurred costs by the lessee before

commencement and the estimated costs to be incurred to dismantle and restore the site of

the location to the state prescribed in conditions and terms determine the cost of the lease.

Subsequent Measurement of the Leased Asset Value

A leased asset can be valued at cost, meaning the current charge less accrued

devaluation and any damage losses accumulated with the re-measurement of lease

adjusted liability. The depreciation requirements for plant, property, and equipment as

prescribed in AASB16 are applied in depreciating right-to-use asset (Brown, Preiato, and

Tarca, 2014). Where the leased asset is subject to sale to the lessee the period for

depreciation is the start date to the conclusion of the assets' valuable life. Otherwise,

depreciation is applied to the conclusion of valuable life or end of the lease term.

Determination of Initial Lease Liability

At the date of commencement, a lessee is required to determine the present worth of the

lease payments not paid at that date (Eccles, Krzus, Rogers, and Serafeim, 2012). Upon

determination, the interest rate is subject to a discounted rate of interest contained in the

lease if the determination of the rate is possible. In cases where the rate cannot be gladly

determined, the incremental borrowing rate for the lessee shall be applied.

Subsequent Measurement of Liability

This is applicable to the lessee (Brown, 2011). After the commencement date, the lessee

shall determine liability by either raising the carrying money to show on the lease charge.

Otherwise, lower the carrying amount to show lease costs already paid and re-measuring

the carrying amount to show the re-assessment or modification.

Effects of the New Standard on Firms with High Levels of Finance Leases

Lease payment is expenses, and the straight-line method is applied over the validity

period of the agreement or using another suitable method. The standard requires that the

lessee's present right-of-use assets on the financial position statement separately or

disclose separately in notes (Chalmers, Clinch, and Godfrey, 2011). Lease liabilities are

also subject to separate disclosure separate from other liabilities in the financial position

statement or separately in notes. The lease liability for the right-to-use asset is also

subject to separation from depreciation expense in the statement of income. In the cash

flows statement of, the financing activities include the cash outflows meant for the portion

(Brown, Preiato, and Tarca, 2014). The incurred costs by the lessee before

commencement and the estimated costs to be incurred to dismantle and restore the site of

the location to the state prescribed in conditions and terms determine the cost of the lease.

Subsequent Measurement of the Leased Asset Value

A leased asset can be valued at cost, meaning the current charge less accrued

devaluation and any damage losses accumulated with the re-measurement of lease

adjusted liability. The depreciation requirements for plant, property, and equipment as

prescribed in AASB16 are applied in depreciating right-to-use asset (Brown, Preiato, and

Tarca, 2014). Where the leased asset is subject to sale to the lessee the period for

depreciation is the start date to the conclusion of the assets' valuable life. Otherwise,

depreciation is applied to the conclusion of valuable life or end of the lease term.

Determination of Initial Lease Liability

At the date of commencement, a lessee is required to determine the present worth of the

lease payments not paid at that date (Eccles, Krzus, Rogers, and Serafeim, 2012). Upon

determination, the interest rate is subject to a discounted rate of interest contained in the

lease if the determination of the rate is possible. In cases where the rate cannot be gladly

determined, the incremental borrowing rate for the lessee shall be applied.

Subsequent Measurement of Liability

This is applicable to the lessee (Brown, 2011). After the commencement date, the lessee

shall determine liability by either raising the carrying money to show on the lease charge.

Otherwise, lower the carrying amount to show lease costs already paid and re-measuring

the carrying amount to show the re-assessment or modification.

Effects of the New Standard on Firms with High Levels of Finance Leases

Lease payment is expenses, and the straight-line method is applied over the validity

period of the agreement or using another suitable method. The standard requires that the

lessee's present right-of-use assets on the financial position statement separately or

disclose separately in notes (Chalmers, Clinch, and Godfrey, 2011). Lease liabilities are

also subject to separate disclosure separate from other liabilities in the financial position

statement or separately in notes. The lease liability for the right-to-use asset is also

subject to separation from depreciation expense in the statement of income. In the cash

flows statement of, the financing activities include the cash outflows meant for the portion

Australian Accounting Standards 9

principal while the financing or operating activities will include outflows for the portion of

interest.

Lessor Accounting

The lessor’s requirements for leasing agreements did not change with the change in

accounting standards. The lessor is required to give a clear distinction between finance

and operating lease (Joubert, Garvie, and Parle, 2017). The lessor must give the definition

of both the finance lease, including the indicators that support the finance lease. Lastly, for

the lessor, basic accounting mechanics did not change, including variable payments, lease

modifications sub-leases, and the treatment of lessor disclosures and initial direct costs.

How Changes in Accounting Standards has Affected Businesses

The introduction of AASB 16 has marked a great step in accounting for leases. With a

large number of flaws in the AASB 17, AASB 16 has made accounting for leases simpler

and more objective. With the previous separation of financing and operating leases, which

created big differences for a business that treated them separately, the new standards

have eliminated such differences. AASB16 has changed the reporting without changing

the financial commitment; hence, adoption is much easier. With few rules, the correct state

of financial affairs will be reflected in the financial statements (Brumm, and Liu, 2019).

With the use of the interest rate of borrowing of the lessee’s, the lessor is better informed

of the lessee’s credit risk hence more prepared and equipped concerning the risk.

Provision of lease data on financial statements makes them more complete and

understandable. Lease information provided in footnotes is always unclear.

AASB 16 and Asset Ownership

Addition of leases to balance sheet makes them appear more leveraged, which is untrue

and leads to the increased cost of finance. The increased finance cost makes business

owners to take the option of buying rather than leasing the asset. The adjustment on

reporting of leases will increase the cost and complexity of reporting this will affect large

volumes of small leases (Xu, Davidson, and Cheong, 2017). Firms with large numbers of

small leases will, therefore, cut down accounting costs by buying assets rather than

leasing. The use of the lessee’s rate borrowing exposes the internal affairs of the

business. These reasons give business owners a reason to buy other than lease assets

since the costs are cut down and the business affairs are kept secret.

principal while the financing or operating activities will include outflows for the portion of

interest.

Lessor Accounting

The lessor’s requirements for leasing agreements did not change with the change in

accounting standards. The lessor is required to give a clear distinction between finance

and operating lease (Joubert, Garvie, and Parle, 2017). The lessor must give the definition

of both the finance lease, including the indicators that support the finance lease. Lastly, for

the lessor, basic accounting mechanics did not change, including variable payments, lease

modifications sub-leases, and the treatment of lessor disclosures and initial direct costs.

How Changes in Accounting Standards has Affected Businesses

The introduction of AASB 16 has marked a great step in accounting for leases. With a

large number of flaws in the AASB 17, AASB 16 has made accounting for leases simpler

and more objective. With the previous separation of financing and operating leases, which

created big differences for a business that treated them separately, the new standards

have eliminated such differences. AASB16 has changed the reporting without changing

the financial commitment; hence, adoption is much easier. With few rules, the correct state

of financial affairs will be reflected in the financial statements (Brumm, and Liu, 2019).

With the use of the interest rate of borrowing of the lessee’s, the lessor is better informed

of the lessee’s credit risk hence more prepared and equipped concerning the risk.

Provision of lease data on financial statements makes them more complete and

understandable. Lease information provided in footnotes is always unclear.

AASB 16 and Asset Ownership

Addition of leases to balance sheet makes them appear more leveraged, which is untrue

and leads to the increased cost of finance. The increased finance cost makes business

owners to take the option of buying rather than leasing the asset. The adjustment on

reporting of leases will increase the cost and complexity of reporting this will affect large

volumes of small leases (Xu, Davidson, and Cheong, 2017). Firms with large numbers of

small leases will, therefore, cut down accounting costs by buying assets rather than

leasing. The use of the lessee’s rate borrowing exposes the internal affairs of the

business. These reasons give business owners a reason to buy other than lease assets

since the costs are cut down and the business affairs are kept secret.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Australian Accounting Standards 10

Air New Zealand Limited (AIZ)

Air New Zealand Limited is an airline company listed in the Australian Stock Exchange.

Following the transition, the company has explained the new treatment of its leases in

footnotes (Joubert, Garvie, and Parle, 2017). The company, in its financial report of 2018,

has included footnotes on the accounting treatments for leases. The financing leases have

been disclosed in the statement of financial position and footnotes included for

clarification.

Conclusion

AASB 16 standards have been the best solution for lease accounting. With many

drawbacks in the AASB 17 standard, the change of the standards was inevitable in order

to make accounting reports fair and to reflect the true affairs of a firm’s including its

financial position. Inclusion of the leased assets in the financial position statement makes

the value of return on assets more accurate and objective as the overstated return on

assets is eliminated. The treatment of operating and financing leases similarly has

eliminated the difference caused by the different treatment of financial and operating

lease. The combination of the financing and operating lease has also simplified accounting

for leases since the distinction is no longer needed. The accounting standard having

provided the various ways in which disclosure of lease transactions in the financial

statement has given users of financial information a clear way to analyze the financial

statement. It is therefore advisable for any business to adopt the new standards in

reporting for leases to ensure faithfulness in reporting.

Air New Zealand Limited (AIZ)

Air New Zealand Limited is an airline company listed in the Australian Stock Exchange.

Following the transition, the company has explained the new treatment of its leases in

footnotes (Joubert, Garvie, and Parle, 2017). The company, in its financial report of 2018,

has included footnotes on the accounting treatments for leases. The financing leases have

been disclosed in the statement of financial position and footnotes included for

clarification.

Conclusion

AASB 16 standards have been the best solution for lease accounting. With many

drawbacks in the AASB 17 standard, the change of the standards was inevitable in order

to make accounting reports fair and to reflect the true affairs of a firm’s including its

financial position. Inclusion of the leased assets in the financial position statement makes

the value of return on assets more accurate and objective as the overstated return on

assets is eliminated. The treatment of operating and financing leases similarly has

eliminated the difference caused by the different treatment of financial and operating

lease. The combination of the financing and operating lease has also simplified accounting

for leases since the distinction is no longer needed. The accounting standard having

provided the various ways in which disclosure of lease transactions in the financial

statement has given users of financial information a clear way to analyze the financial

statement. It is therefore advisable for any business to adopt the new standards in

reporting for leases to ensure faithfulness in reporting.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Australian Accounting Standards 11

References

Biondi, Y., Bloomfield, R.J., Glover, J.C., Jamal, K., Ohlson, J.A., Penman, S.H.,

Tsujiyama, E. and Wilks, T.J., 2011. A perspective on the joint IASB/FASB exposure draft

on accounting for leases: American Accounting Association's Financial Accounting

Standards Committee (AAA FASC). Accounting Horizons, 25(4), pp.861-871.

Brown, P., 2011. International Financial Reporting Standards: what are the

benefits?. Accounting and business research, 41(3), pp.269-285.

Brown, P., Preiato, J., and Tarca, A., 2014. Measuring country differences in enforcement

of accounting standards: An audit and enforcement proxy. Journal of Business Finance &

Accounting, 41(1-2), pp.1-52.

Brumm, L., and Liu, J., 2019. New leasing accounting standard. Taxation in

Australia, 53(8), p.449.

Chalmers, K., Clinch, G., and Godfrey, J.M., 2011. Changes in value relevance of

accounting information upon IFRS adoption: Evidence from Australia. Australian Journal

of management, 36(2), pp.151-173.

Eccles, R.G., Krzus, M.P., Rogers, J., and Serafeim, G., 2012. The need for sector‐

specific materiality and sustainability reporting standards. Journal of Applied Corporate

Finance, 24(2), pp.65-71.

Joubert, M., Garvie, L., and Parle, G., 2017. Implications of the New Accounting Standard

for Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance

Sheet. The Journal of New Business Ideas & Trends, 15(2), pp.1-11.

Sacarin, M., 2017. IFRS 16 “Leases”–consequences on the financial statements and

financial indicators. The Audit Financiar journal, 15(145), pp.114-114.Shough, S., 2011.

Proposed Lease Accounting For Lessees. Journal of Business & Economics

Research, 9(1), pp.63-70.

Xu, W., Davidson, R.A., and Cheong, C.S., 2017. Converting financial statements:

operating to capitalized leases. Pacific accounting review, 29(1), pp.34-54

References

Biondi, Y., Bloomfield, R.J., Glover, J.C., Jamal, K., Ohlson, J.A., Penman, S.H.,

Tsujiyama, E. and Wilks, T.J., 2011. A perspective on the joint IASB/FASB exposure draft

on accounting for leases: American Accounting Association's Financial Accounting

Standards Committee (AAA FASC). Accounting Horizons, 25(4), pp.861-871.

Brown, P., 2011. International Financial Reporting Standards: what are the

benefits?. Accounting and business research, 41(3), pp.269-285.

Brown, P., Preiato, J., and Tarca, A., 2014. Measuring country differences in enforcement

of accounting standards: An audit and enforcement proxy. Journal of Business Finance &

Accounting, 41(1-2), pp.1-52.

Brumm, L., and Liu, J., 2019. New leasing accounting standard. Taxation in

Australia, 53(8), p.449.

Chalmers, K., Clinch, G., and Godfrey, J.M., 2011. Changes in value relevance of

accounting information upon IFRS adoption: Evidence from Australia. Australian Journal

of management, 36(2), pp.151-173.

Eccles, R.G., Krzus, M.P., Rogers, J., and Serafeim, G., 2012. The need for sector‐

specific materiality and sustainability reporting standards. Journal of Applied Corporate

Finance, 24(2), pp.65-71.

Joubert, M., Garvie, L., and Parle, G., 2017. Implications of the New Accounting Standard

for Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance

Sheet. The Journal of New Business Ideas & Trends, 15(2), pp.1-11.

Sacarin, M., 2017. IFRS 16 “Leases”–consequences on the financial statements and

financial indicators. The Audit Financiar journal, 15(145), pp.114-114.Shough, S., 2011.

Proposed Lease Accounting For Lessees. Journal of Business & Economics

Research, 9(1), pp.63-70.

Xu, W., Davidson, R.A., and Cheong, C.S., 2017. Converting financial statements:

operating to capitalized leases. Pacific accounting review, 29(1), pp.34-54

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.