Australian Accounting Standards for Forfeiture and Reissue of Shares

VerifiedAdded on 2023/06/11

|7

|1762

|373

Report

AI Summary

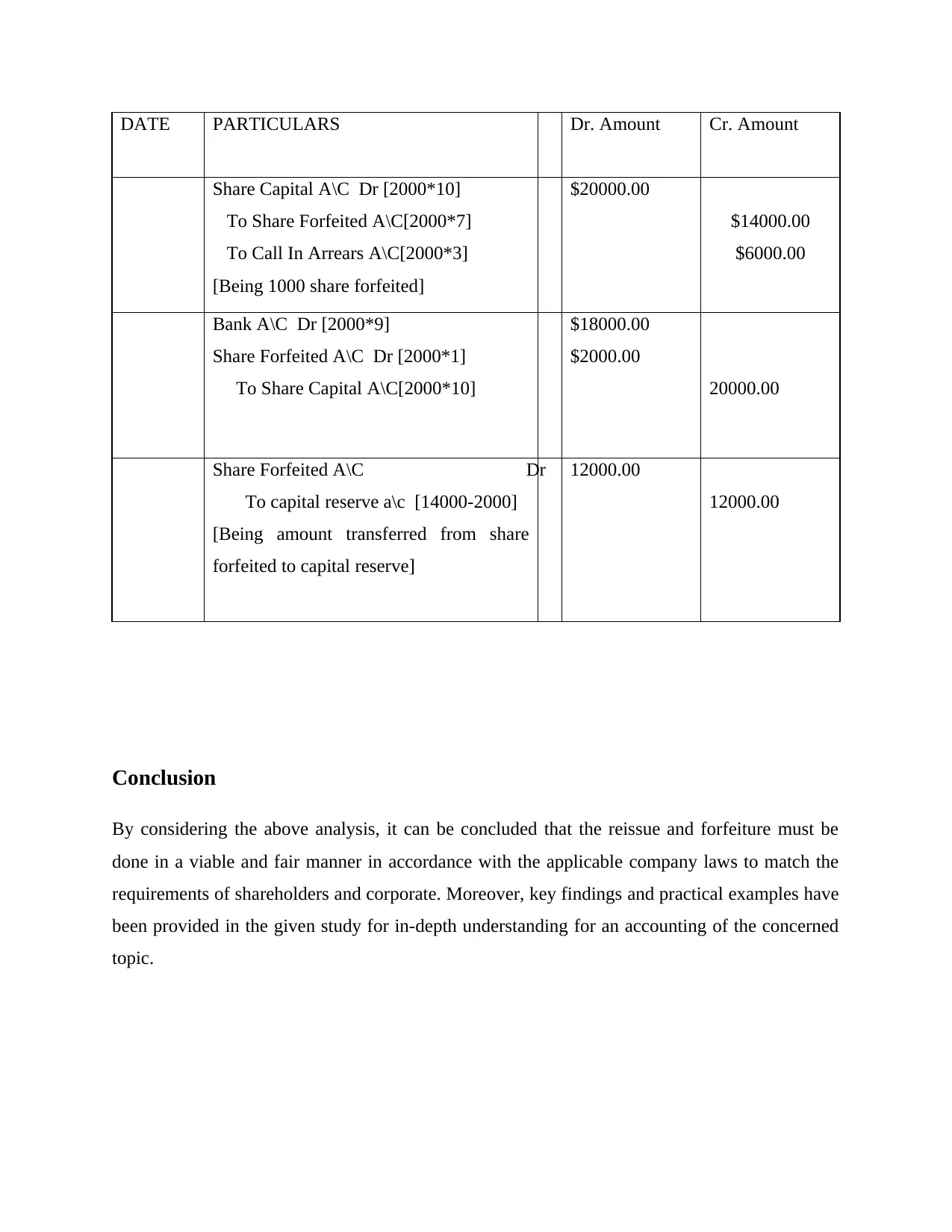

This report provides an evaluation and analysis of the accounting treatment for the forfeiture and reissue of shares by Australian corporate entities. It covers the cancellation of membership rights due to unpaid share amounts and the subsequent reissuance of these shares. The report details the conditions under which shares can be forfeited, the rights of shareholders, and the accounting procedures for reissuing shares at par, premium, or discount. It includes journal entries for various scenarios, such as the reissue of shares, the transfer of surplus amounts to the capital reserve account, and the treatment of premium amounts. The report provides a practical example to illustrate the accounting entries involved in share forfeiture and reissue, concluding that these processes must be conducted fairly and in accordance with applicable company laws to meet the requirements of both shareholders and the corporation.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.